el futuro económico de américa latina: ¿hecho en...

TRANSCRIPT

1 1

El Futuro Económico de América Latina: ¿Hecho en China?

2012 Latin American Cities Conferences

“Panama: Where the World Meets”

Ciudad de Panamá 2 de marzo del 2012

Augusto de la Torre Economista Jefe América Latina y el Caribe

Desacoplamiento cíclico – centro vs. periferia

2 Note: The group of developed countries refers to OECD countries excluding Turkey, Mexico, Republic of Korea, and Central European countries. Source: CPB (Netherlands Bureau for Economic Policy Analysis).

51%38%

27%

34%44%

57%

8% 7% 8%8% 11% 8%

0%

20%

40%

60%

80%

100%

1996-2001 2001-2006 2009-2011

Contribution to World Economic GDPas a % of World GDP increase (PPP)

Others Other Advanced EconomiesEM - 20 Euro (15)+US+Japan+Canada+UK

80

85

90

95

100

105

110

115

120

Jan-

06

Jul-0

6

Jan-

07

Jul-0

7

Jan-

08

Jul-0

8

Jan-

09

Jul-0

9

Jan-

10

Jul-1

0

Jan-

11

Jul-1

1

Jan-

12

World Industrial ProductionIndex Apr-08 = 100

CrisisAdvanced Economies (a)Emerging Economies

Cambios tectónicos en la distribución de la actividad económica global

3 Source: IMF WEO (September 2011)

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

Share of World GDP

Advanced economies

Emerging and developing economies

China

Para el 2030, los países emergentes y en desarrollo contribuirán 2/3 de la

actividad económica global

¿Cambiará el bajo número de países que logran liberase de la “trampa del mediano ingreso”?

4 Source: “China 2030” joint report by the World Bank and the Development Research Ceneter of the People’s Republic of China (2012).

5

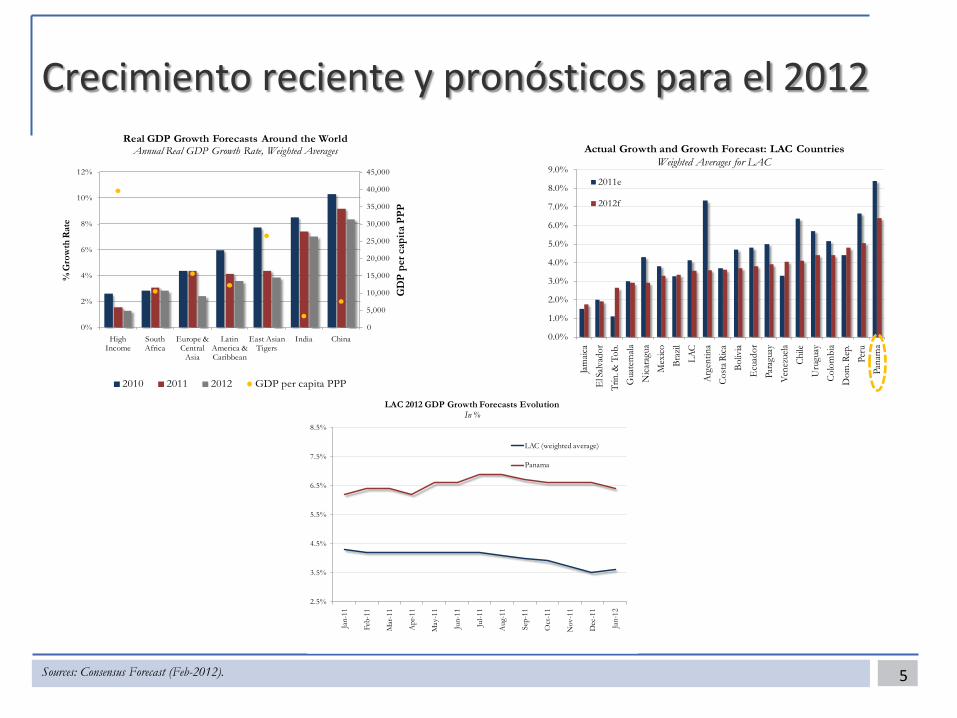

Crecimiento reciente y pronósticos para el 2012

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

Jam

aica

El S

alvad

orTr

in. &

Tob

.G

uate

mala

Nica

ragu

aM

exico

Braz

ilLA

CA

rgen

tina

Cost

a Rica

Boliv

iaE

cuad

orPa

ragu

ayVe

nezu

elaCh

ileU

rugu

ayCo

lom

bia

Dom

. Rep

.Pe

ruPa

nam

a

Actual Growth and Growth Forecast: LAC CountriesWeighted Averages for LAC

2011e

2012f

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

0%

2%

4%

6%

8%

10%

12%

High Income

South Africa

Europe & Central

Asia

Latin America & Caribbean

East Asian Tigers

India China

GD

P pe

r cap

ita P

PP

% G

row

th R

ate

Real GDP Growth Forecasts Around the WorldAnnual Real GDP Growth Rate, Weighted Averages

2010 2011 2012 GDP per capita PPP

2.5%

3.5%

4.5%

5.5%

6.5%

7.5%

8.5%

Jan-

11

Feb-

11

Mar

-11

Apr

-11

May

-11

Jun-

11

Jul-1

1

Aug

-11

Sep-

11

Oct

-11

Nov

-11

Dec

-11

Jan-

12

LAC 2012 GDP Growth Forecasts Evolution In %

LAC (weighted average)

Panama

Sources: Consensus Forecast (Feb-2012).

El crecimiento tendencial (no solo el cíclico) de LAC se desacopló en la última década

6 Notes: In Panel B, High Performance EAP includes Korea Rep., Taiwan, Hong Kong, and Singapore; Low Performance EAP includes Indonesia, Philippines, Thailand, and Malaysia; LAC includes the following countries: Argentina, Brazil, Chile, Colombia, Mexico, Peru, Uruguay, Venezuela, Bolivia, Costa Rica, Dominican Republic, Ecuador, El Salvador, Guatemala, Haiti, Honduras, Jamaica, Nicaragua, Panama, and Paraguay. The weights are calculated using the 2007 nominal GDP. Source: Penn World Tables.

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%19

6119

6319

6519

6719

6919

7119

7319

7519

7719

7919

8119

8319

8519

8719

8919

9119

9319

9519

9719

9920

0120

0320

0520

07

Cyclical Adjusted Growth

High-Income

Latin America

7

El super-ciclo de commodities ciertamente ayudó…

-20% 10% 40% 70% 100% 130%

Honduras

Costa Rica

Panama

Jamaica

Brazil

Guatemala

Mexico

Uruguay

Colombia

LAC

Argentina

Ecuador

Chile

Peru

Cumulative Change in Terms of TradeMonthly Data, Avg. 2002Q1 vs. Avg. 2011Q1

30

50

70

90

110

130

150

50

100

150

200

250

300

350

400

Jan-0

5

Jan-0

6

Jan-0

7

Jan-0

8

Jan-0

9

Jan-1

0

Jan-1

1

Jan-1

2

Oil

WTI

, Cur

rent

US$

Whe

at, C

oppe

r and

Soyb

ean,

In

dex 0

1-Jan

-05=

100

Commodity PricesOil WTI in Current US$, Wheat, Copper and Soybean: Index base

Jan-05=100

Sources: Bloomberg and World Bank Global Economic Monitor

Alrededor del 93% de la población de LAC y 97%

de su actividad económica está en países exportadores netos de commodities

Ha sido el ciclo más comprehensivo y largo desde

que hay data, afectando al mayor número de países en LAC

Pero las mejoras en la política económica son también una parte importante de esta historia

8 Notes: In Panel B, High Performance EAP includes Korea Rep., Taiwan, Hong Kong, and Singapore; Low Performance EAP includes Indonesia, Philippines, Thailand, and Malaysia; LAC includes the following countries: Argentina, Brazil, Chile, Colombia, Mexico, Peru, Uruguay, Venezuela, Bolivia, Costa Rica, Dominican Republic, Ecuador, El Salvador, Guatemala, Haiti, Honduras, Jamaica, Nicaragua, Panama, and Paraguay. The weights are calculated using the 2007 nominal GDP. Source: Penn World Tables.

-0.5 0.0 0.5 1.0 1.5 2.0 2.5 3.0 3.5

HondurasEcuadorParaguay

NicaraguaGuatemala

JamaicaChile

MexicoUruguay

El SalvadorLAC

ColombiaCosta Rica

BoliviaArgentina

BrazilIndonesia

Dom. Rep.Peru

TailandPanamaChina*

Total Factor Productivity Growth in LAC and EAPAverage Annual Trend-Growth in TFP During 2000-7, in %)

Desigual desempeño económico en la región La heterogeneidad ha ido mutando en la última década

9 Sources: Potential GPD is computed as the average rate of growth between 2007 and 2003. Simple averages are used to construct the composite. The categorization of each group is as follow: Slow-growth are those countries that showed a less than 3.5% in their 2011-2008 GDP real growth rate; Medium-growth are those between 3.5% and 10%: High-growth are those with 10% or more. WEO (September– 2011).

80

100

120

140

160

180

200

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

PanamaGDP Index 2002=100

Panama

2003-2007 trend

80

100

120

140

160

180

200

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Low-Growth CountriesGDP Index 2002=100

Actual

2003-2007 Trend

80

100

120

140

160

180

200

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Intermediate-Growth CountriesGDP Index 2002=100

Actual

2003-2007 Trend

80

100

120

140

160

180

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

High Growth CountriesGDP Index 2002=100

Actual

2003-2007 Trend

Desigual desempeño económico Importa menos la ubicación que la conexión

10 Sources: World Bank’s World Development Indicators – WDI (December 2010), IMF's World Economic Outlook – WEO (April 2011), and Consensus Forecasts (June 2011) – Latest available forecasts. Potential GDP is calculated computing the annual average real growth rate for the 2002-2007 to 2007 GDP. Weighted averages (2007 Nominal GDP in USD Billions).

(Geometric) Mean growth

2003-2007Simple Average

(Geometric) Mean growth

2007-2009Simple Average

(Geometric) Mean growth

2009-2012Simple Average

Min. 2009-2012

Max. 2009-2012

Low growth (13) 4.9% -1.6% 1.3% -0.1% 4.3%Medium growth (7) 4.5% 1.7% 3.4% 2.6% 4.4%Panama 8.8% 9.5% 8.4% 8.4% 8.4%High growth (12) 5.9% 4.5% 6.0% 4.5% 8.7%LAC (all countries) 4.8% 1.1% 3.5% -0.1% 8.7%

Low growth: Antigua and Barbuda, Bahamas, Barbados, Dominica, El Salvador, Grenada, Jamaica, Mexico, St. Kitts and Nevis, St. Vincent and the Grenadines, St. Lucia, Trinidad and Tobago, and Venezuela

Intermediate growth: Belize, Costa Rica, Ecuador, Guatemala, Haiti, Honduras, and Nicaragua

High growth: Argentina, Bolivia, Brazil, Chile, Colombia, Dominican Republic, Guyana, Panama , Paraguay, Peru, Suriname and Uruguay

11

Mucho del futuro económico de LAC dependerá de la forma como se re-conecte, no solo con China

Sources: WDI, and WITS COMTRADE.

-0.2

-0.1

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

Jan-0

4

Jun-

04

Nov

-04

Apr-0

5

Sep-

05

Feb-

06

Jul-0

6

Dec

-06

May

-07

Oct

-07

Mar

-08

Aug-

08

Jan-0

9

Jun-

09

Nov

-09

Apr-1

0

Sep-

10

Feb-

11

Jul-1

1

Industrial Production: Latin America w.r.t Asia, US and Europe

AsiaUSEurope

-0.8

-0.6

-0.4

-0.2

0.0

0.2

0.4

0.6

0.8

1980 1984 1988 1992 1996 2000 2004 2008

Output Co-Movement Between LAC and China20 years rolling correlation of the Real GDP Growth

Brazil Chile ColombiaMexico Peru ArgentinaPanama Guatemala

El pasado no es inspirador en este sentido 100 años de soledad en el crecimiento

12 Sources: Penn World Tables.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%19

0019

0519

1019

1519

2019

2519

3019

3519

4019

4519

5019

5519

6019

6519

7019

7519

8019

8519

9019

9520

0020

0520

10

GDP Per Capita of Relative to the USSelected Regions, Weighted Averages

LAC EAP: High Income Panama

WashingtonDissensus

Gold Standard Period

Interwar Period Import Substitution WashingtonConsensus

LostDecade

Síndrome de bajo crecimiento ha sido generalizado

13 Notes: Maddison (2007-2009) was used from 1900 to 2006 and Real Per Capita GDP growth from WDI was used to calculate the levels from 2006 to 2010. Source: LCRCE Staff calculations based on Maddison (2007, 2009) and WDI.

0%

10%

20%

30%

40%

50%

60%

70%

80%

1950

1955

1960

1965

1970

1975

1980

1985

1990

1995

2000

2005

2010

Diverging

Venezuela Argentina Uruguay

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

1950

1955

1960

1965

1970

1975

1980

1985

1990

1995

2000

2005

2010

Fluctuating

Mexico Brazil

0%

10%

20%

30%

40%

50%

60%

70%

80%

1900

1905

1910

1915

1920

1925

1930

1935

1940

1945

1950

1955

1960

1965

1970

1975

1980

1985

1990

1995

2000

2005

2010

Non-Converging

Colombia Guatemala El Salvador Bolivia Paraguay

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

1950

1955

1960

1965

1970

1975

1980

1985

1990

1995

2000

2005

2010

Semi - Converging

Chile Dominican Republic Panama

0%

10%

20%

30%

40%

50%

60%

-4% -2% 0% 2% 4% 6% 8% 10%

Infla

tion

GDP Growth

Inflation and GrowthGDP and CPI trend growth

EAP Countries

LAC Countries

Others

La máquina económica de LAC no ha sido capaz de aumentar la velocidad sin recalentarse

14 Source: Barro-Lee (2010), US Energy Information Administration Source: IMF WEO (September 2011)

LAC: ¿mejor sustento social para la agenda de crecimiento?

15 Source: LCSPP based on Socio-Economic Database for Latin America and the Caribbean (CEDLAS and The World Bank).

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

20

25

30

35

40

45

1994

1996

1998

2000

2002

2004

2006

2008

2010

GDP P

er Ca

pita

US D

ollar

s

Mod

erate

Pove

rty R

ate

US$ 4

a Da

y

Per Capita GDP Growth and Poverty LAC Countries

Poverty Headcount GDP Per Capita

LAC: The Rise of the Middle Class

Los fundamentos del crecimiento de largo plazo Acumulación – ahorro e inversión

16 Source: Penn World Tables and World Development Indicators.

0%

5%

10%

15%

20%

25%

30%

35%

40%

1960's 1970's 1980's 1990's 2000's

% o

f G

DP

Investment Decade Average

LAC-7

EAP

Panama

0%

5%

10%

15%

20%

25%

30%

35%

1960's 1970's 1980's 1990's 2000's

% o

f G

DP

Gross Domestic SavingsDecade Average

LAC-7

EAP

Panama

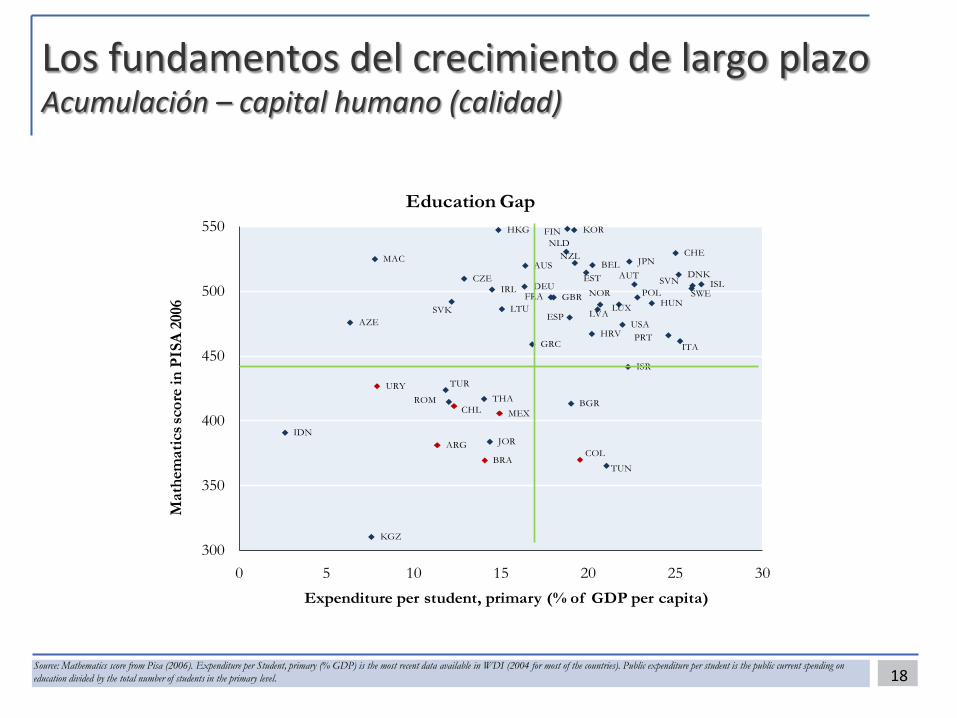

Los fundamentos del crecimiento de largo plazo Acumulación – capital humano

17 Source: Author’s calculation based on Household datasets and Barro-Lee (2010)

19.3

40.9

29.7

10

East Asian Tigers1990

16.4

51

23.1

9.5

LAC-71990

9.7

29.3

40.7

20.3

East Asian Tigers2010

7.9

40.3

37.5

14.2

LAC-72010

12.2

43.830.2

13.8

Panama1990

No SchoolPrimarySecondaryTertiary

6

31.9

39.4

22.7

Panama2010

Los fundamentos del crecimiento de largo plazo Acumulación – capital humano (calidad)

18

ARG

AUSAUT

AZE

BEL

BRA

BGRCHL

COL

HRV

CZE DNKEST

FIN

FRADEU

GRC

HKG

HUN

ISL

IDN

IRL

ISR

ITA

JPN

JOR

KOR

KGZ

LVALTU LUX

MAC

MEX

NLDNZL

NOR POL

PRT

ROM

SVK

SVN

ESP

SWE

CHE

THA

TUN

TUR

GBR

USA

URY

300

350

400

450

500

550

0 5 10 15 20 25 30

Mat

hem

atic

s sco

re in

PIS

A 20

06

Expenditure per student, primary (% of GDP per capita)

Education Gap

Source: Mathematics score from Pisa (2006). Expenditure per Student, primary (% GDP) is the most recent data available in WDI (2004 for most of the countries). Public expenditure per student is the public current spending on education divided by the total number of students in the primary level.

Los fundamentos del crecimiento de largo plazo Acumulación – capital físico

19 Source: Barro-Lee (2010), US Energy Information Administration

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

Electricity Installed CapacityIn thousands of KW per 1000 people, simple averages

EAP

LAC7 + URY

Panama

0.0000

0.0010

0.0020

0.0030

0.0040

0.0050

0.0060

0.0070

0.0080

0.0090

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

Road DensityIn thousands of KM per 1000 people, simple average

LAC7 + URY Panama

Los fundamentos del crecimiento de largo plazo Productividad – cambio tecnológico

20 Source: Mathematics score from Pisa (2006). Expenditure per Student, primary (% GDP) is the most recent data available in WDI (2004 for most of the countries). Public expenditure per student is the public current spending on education divided by the total number of students in the primary level.

21

Los fundamentos del crecimiento de largo plazo Productividad – instituciones

Source: D. Kaufmann, A. Kraay, and M. Mastruzzi 2003: G

Panama

-2

-1.5

-1

-0.5

0

0.5

1

1.5

2

2.5

3

4 5 6 7 8 9 10 11 12

Log of GDP per capita PPP in 2010

Control of Corruption

Others

LAC

-2.5

-2

-1.5

-1

-0.5

0

0.5

1

1.5

2

2.5

4 5 6 7 8 9 10 11 12

Log of GDP per capita PPP in 2010

Rule of Law

Others

LAC

Panama

-2.5

-2

-1.5

-1

-0.5

0

0.5

1

1.5

2

2.5

4 5 6 7 8 9 10 11 12

Log of GDP per capita PPP in 2010

Regulatory Quality

Others

LAC

Panama

-2

-1.5

-1

-0.5

0

0.5

1

1.5

2

2.5

4 5 6 7 8 9 10 11 12

Log of GDP per capita PPP in 2010

Government Effectiveness

Others

LAC

Panama

Panamá: ¿camino a ser el Singapur de las Américas?

22

Singapore

PanamaSri Lanka

Jamaica

BahamasDominican Rep.

Costa Rica Guatemala

Uruguay ChilePeru

Egypt

0

10

20

30

40

50

60

70

80

90

100

110

0 20 40 60 80 100 120 140 160 180 200

Shipping Conectivity and GDP

GDP (US$B) 2009

Line

r Shi

ppin

g C

onec

tivity

Inde

x, 20

10 (M

ax 2

004=

100)

TransshipmentCenters , Hubs

& Canals

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

0

20

40

60

80

100

120

Sing

apor

e

Net

herla

nds

Spai

n

Japa

n

Pana

ma

Jam

aica

Col

ombi

a

Bah

amas

Dom

inic

an R

ep.

Liner Shipping Connectivity Index

LSC

I201

0 (M

axim

um 2

004=

100)

Global players

Regional Transshipment Centers

Source: UNCTAD.

23

Gracias