ekonomikos augimo veiksmŲ programa - tid · web viewpublic ownership of land, transport...

TRANSCRIPT

Operational Programme for Economic Growthfor 2007–2013

15th July 2007, Vilnius,

TABLE OF CONTENT

1. analysis of current socio-economic situation and of development prospects in lithuania 5

1.1. GENERAL OVERVIEW OF THE LITHUANIAN ECONOMY/ PRODUCTION SECTOR...........51.2. RESEARCH AND DEVELOPMENT. INNOVATIONS 291.3. DEVELOPMENT OF INFORMATION SOCIETY 391.4. TRANSPORT NETWORK 431.5. ENERGY SUPPLY NETWORKS 541.6. SWOT ANALYSIS 59

2. OPERATIONAL PROGRAMME STRATEGY 622.1. VISIONS AND OBJECTIVES 622.2. PRIORITY 1: RESEARCH AND DEVELOPMENT FOR COMPETITIVENESS AND GROWTH OF THE ECONOMY 712.3. PRIORITY 2: INCREASING BUSINESS PRODUCTIVITY AND IMPROVING ENVIRONMENT FOR BUSINESS 762.4. PRIORITY 3: INFORMATION SOCIETY FOR ALL 822.5. PRIORITY 4: BASIC ECONOMIC INFRASTRUCTURE 872.6. PRIORITY 5: DEVELOPMENT OF TRANS-EUROPEAN TRANSPORT NETWORKS 92

2.7. PRIORITY 6: TECHNICAL ASSISTANCE FOR THE IMPLEMENTATION OF THE OPERATIONAL PROGRAMME ON ECONOMY GROWTH...............................................................................................................95

2.8. CORRESPONDENCE TO HORIZONTAL THEMES AND THEIR IMPLEMENTATION 98

3. FINANCIAL PLAN 1014. QUANTIFICATION OF OBJECTIVES 1025. PREPARATION OF THE OPERATIONAL PROGRAMME 112

5.1. PARTNERSHIP 1125.2. EX-ANTE EVALUATION 1145.3. STRATEGIC ENVIRONMENTAL IMPACT ASSESSMENT 116

6. IMPLEMENTING PROVISIONS 119

ANNEX I. BREAKDOWN OF EXPENDITURE BY CATEGORIES..........................................................134

ANNEX II. INDICATIVE LIST OF MAJOR PROJECTS.....................................................................................136

ANNEX III. FINANCIAL FLOWS........................................................................................................................137

ANNEX IV. EX-ANTE RECOMMENDATIONS – OPERATIONAL PROGRAMME ON ECONOMIC GROWTH............................................................................................................................................138

ANNEX V. COMPATIBILITY OF ASSISTANCE WITH OTHER OPERATIONAL PROGRAMMES AND OTHER EU FINANCIAL INSTRUMENTS.............................................................................................152

ANNEX VI. STATE AID CLAUSE.......................................................................................................................158

ANNEX VII. PUBLIC PROCUREMENT...................................................................................................................159

ANNEX VIII. REGIONS FOR ECONOMIC CHANGE INITIATIVE...................................................................160

ANNEX IX. COOPERATION WITH THE BALTIC SEA COUNTRIES...............................................................161

ANNEX X. RECOMMENDATIONS ON STRATEGIC ENVIRONMENTAL IMPACT ASSESSMENT OF OPERATIONAL PROGRAMMES IMPLEMENTING THE LITHUANIAN STRATEGY FOR THE USE OF EUROPEAN UNION STRUCTURAL ASSISTANCE FOR 2007–2013.......................................................................162

2

LIST OF FIGURES

Figure 1. Labour productivity by sectors of the economy in 2002–2005, LTL/hour......................7Figure 2. Structure of value added created by industries in 2005, %..............................................7Figure 3. Labour productivity in sectors of manufacturing industry by countries in 2003, EUR’0008………………………………………………………………………………………....8Figure 4. Structure of products sold by high and medium-high technology industries...................9Figure 5. Structure of products sold by low and semi-low technology industries...........................9Figure 6. Investment share of GDP in 2005, %.............................................................................10Figure 7. Share of investments by businesses in GDP in 2005, %................................................11Figure 8. Goods exports and exports of goods of Lithuanian origin in 2000–2005, LTL m. .....12Figure 9. Structure of products sold by main industries in 2005 (preliminary data provided by the Department of Statistics), ..........................................................................................................14Figure 10. Structure of exports of goods of Lithuanian origin by goods chapters, 2005..............14Figure 11. Annual volumes of FDI in Lithuania, LTL m..............................................................18Figure 12. Annual FDI per capita in the new EU Member States, EUR .....................................18Figure 13. Share of GDP created by SMEs in 2001–2004, %.......................................................22Figure 14. Structure of active SMEs according to type of economic activity as of the end of 2001–2004, % ...............................................................................................................................23Figure 15. Infrastructure of public services for business...............................................................26Figure 16. Ratio between expenditure for RD and GDP in Lithuania, ..................................31Figure 17. Expenditure for R&D by financing sources in Lithuania in 2004. .............................33Figure 18. Innovation businesses by types of economic activities in 2002–2004, % ...................34Figure 19. Cooperation partners of innovative businesses............................................................35Figure 20. Factors hindering innovations, of total number of businesses according to high importance ...........................................................................................................................36Figure 21. Volumes of cargo carriage by rail in Lithuania in 2000–2005.....................................48Figure 22. Dynamics of passenger carriage volumes at Lithuanian airports in 1993–2005..........50Figure 23. Number of 110 kV transformer substations in the transmission network, by age......53Figure 24. Share of natural gas in the EU primary energy balance in 2004..................................55Figure 25. Administration scheme of the Operational Programme on Economy Growth…...…118

3

LIST OF TABLES

Table 1. Growth of GDP in Lithuania in 2001–2005......................................................................5Table 2. Comparison of GDP per capita by counties......................................................................6Table 3. Ratings of Lithuanian’s competitiveness factors in the European context......................15Table 4. Methodologies for determining competitive strength/weakness of Lithuania................15Table 5. Air emissions of pollutants..............................................................................................16Table 6. Energy consumption intensity in Lithuania.....................................................................17Table 7. FDI per capita by Lithuanian counties.............................................................................18Table 8. Annual demand for industrial lots for greenfield investments.......................................20Table 9. Employment of residents according to employment statistics, 2004–2005....................27Table 10. Key discrepancies between Lithuania and the EU average...........................................28Table 11. Participation of Lithuanian institutions in the EU Sixth Framework Programme for Research and Technological Development, 2002–2006 I half-year..............................................37Table 12. Main discrepancies between Lithuania and the EU average.........................................37Table 13. Discrepancies between Lithuania and the EU in the area of information society.........42Table 14. Lithuanian transport network.........................................................................................44Table 15. Share of gravel roads in the total Lithuanian road network...........................................45Table 16. Discrepancies between Lithuania and the EU in the transport sector...........................52Table 17. Discrepancies between Lithuania and the EU in the energy sector...............................57Table 18. SWOT analysis .............................................................................................................58Table 19. Breakdown of assistance by years and funds, EUR million..........................................99Table 20. Breakdown of assistance by priorities, EUR million.....................................................99

4

1. ANALYSIS OF CURRENT SOCIO-ECONOMIC SITUATION AND OF DEVELOPMENT PROSPECTS IN LITHUANIA

1.1. GENERAL OVERVIEW OF THE LITHUANIAN ECONOMY/ PRODUCTION SECTOR

Main statements: The rates of growth of Lithuanian economy are sufficiently high; however, the growth has

been caused by the opening of new European markets and high domestic consumption and borrowing rates. Therefore, if no internal sources for increasing competitiveness are sought, the growth may slow down.

Low and medium-low technology sectors prevail in the Lithuanian economy; value added created by them is low, which prevents the country from reaching high competitive positions in the global markets.

Although technological renovation in the economy has been on the rise, its rates are considerably lower than those of dynamically developing states and/or states of similar size, therefore, Lithuanian economy is characterized by low productivity in all sectors including those which sufficiently good growth performance.

Lithuania as an open economy with a small domestic market has insufficient levels of export of Lithuanian goods.

The rates of attraction of direct foreign investments is very low, while accrued FDI per capita is the lowest among European countries.

Information and communications technologies infrastructure is being developed, however, the development is not even throughout the country. Insufficient availability of public services into the electronic environment prevents optimization of business processes.

There are almost no strategic investors whose business strategy in Lithuania is based on investments in the development of intellectual capital rather than lower operating costs.

The infrastructure of public services for business is in the initial stage of development. The intensity of provision and quality of services to businesses are insufficient.

Clusterisation and partnership networks are underdeveloped. Industry is the sector of the Lithuanian economy characterized by highest energy-

consumption rates.

General economic situation in Lithuania and analysis of key economic sectors

Compared to the economy of the European Union, Lithuanian economy is rapidly growing. In 2001–2005 the growth of Lithuania’s GDP was 7.6% on average – one of the highest among the EU Member States

5

Table 1. Growth of GDP in Lithuania in 2001–2005.2001 2002 2003 2004 2005

Growth in Lithuania’s GDP, % (at comparative prices of 2000)

6,4 6,8 10,5 7,0 7,5

Source: Department of Statistics under the Government of the Republic of Lithuania.

Macroeconomic environment in Lithuania is considered to be stable. In 2004, Lithuania’s macroeconomic stability index accounted for 90.4% of the EU-15 index1. Stable macroeconomic situation results in relatively high international competitiveness ratings, however, this in substance is a pre-condition for rather than a factor of competitiveness. Stable macroeconomic position is a pre-condition for the emergence and growth of competitiveness, therefore, it must be maintained. However, macroeconomic environment is not a specific factor of competitiveness, i.e. it does not by itself increase businesses’ ability to compete under rapidly changing conditions2.

Despite rapid growth in 2004 Lithuania’s GDP per capita was as low as 48% of the EU average. Furthermore, according to economists3, in 2006–2008 GDP growth will slow down due to various factors such as cyclic character of economic development, forecast growth in interest rates, and “cooling” of the domestic market. The present rapid economic growth can be explained by significant falling behind European countries in terms of development, therefore, the growth arises from natural and unavoidable integration processes.

An analysis of GDP/cap. by counties for 2000–2004 shows that there are considerable discrepancies in economic development of Lithuanian counties and such discrepancies are not diminishing (see Table 2). The ratio between the highest (Vilnius county) and the lowest (Tauragė county) GDP/cap. has grown in 2000–2003 from 2.16 to 2.65 and a slight decrease was observed only in 2004, when the ratio was 2.62. During the entire period from 2000 till 2004, only two counties (Vilnius and Klaipėda) exceeded the national average of GDP/cap., while in other counties this value was lower (and in Tauragė and Marijampolė counties much lower) than the national average. Deviations from the average are marked and are still increasing. In 2000, GDP/cap. in Vilnius county exceeded the national average by 33.4%, while in Tauragė county it accounted for just 61.7% of the average. In 2004, GDP/cap. in Vilnius county was already 44.3% above national average, while in Tauragė county in 2004 DGP/cap. it still accounted for only 55% of the average.

Table 2. GDP per capita by counties GDP per capita, LTL’000 Compared to national average, %

2000 2001 2002 2003 2004 2000 2001 2002 2003 2004

National average 13,1 13,9 15 16,4 18,2 100 100 100 100 100

Alytus county 10,7 11,2 11,6 11,9 12,9 81,9 80,2 77,1 72,5 71,1

Kaunas county 12,6 13,7 14,1 15,8 17,5 95,9 97,9 94,2 96,1 96,1

Klaipėda county 14,8 15,4 16,2 17,5 18,7 112,7 110,3 108,5 106,5 102,9

Marijampolė county 9,6 9,4 9,9 11,3 11,8 73,2 67,7 66,4 68,6 65,1

Panevėžys county 11,8 12,4 13 13,7 15,4 90,4 89 86,6 83,1 84,5

Šiauliai county 10,2 10,4 11,1 12,4 13,7 77,5 74,4 74,1 75,2 75,6

Tauragė county 8,1 8,5 8,7 8,9 10 61,7 60,8 57,9 54,1 55

Telšiai county 11,2 12,1 12,5 13,9 16,2 85,3 86,7 83,4 84,6 89,3

Utena county 11,1 11,6 12,4 14 15,1 84,5 83,4 82,6 85,1 83,2

1 In 2004 the value of the EU-15 macroeconomic stability index was 4.93, Lithuania’s index - 4.46. Source: The Global Competitiveness Report, 2004 according to the Comprehensive Study of Sources (Factors) of Growth and Competitiveness of the Lithuanian Economy, Vilnius, 2006, p. 9.2 Comprehensive Study of Sources (Factors) of Growth and Competitiveness of the Lithuanian Economy, Vilnius, 2006, p. 253, 247.3 AB SEB Vilniaus Bankas. Lithuanian Macroeconomic Overview, 4 (24), March 2006.

6

Vilnius county 17,5 19 21,5 23,6 26,2 133,4 136,3 143,3 143,4 144,3Source: Department of Statistics under the Government of the Republic of Lithuania.

Labour productivity is steadily increasing in Lithuania, however, the rate of growth is insufficient: in 2004 the overall labour productivity in the country accounted for only 41.7% of the labour productivity (GDP created by the economy per working hour) of the old EU Member States4. According to this indicator Lithuania is above only its closest neighbours Latvia and Estonia, however, it lags behind other new EU Member States: Czech Republic (49,9%), Poland (47,6%), Slovenia (66%) and Slovakia (52.8%). Further economic growth is threatened by insufficient changes in overall labour productivity during recent years5 (2.6% growth in 2004, 3% in 2005) and by the slowdown or even decrease in labour productivity in certain sectors (see Fig. 1).

Figure 1. Labour productivity by sectors of the economy in 2002–2005, LTL/hour

Source: Calculated according to data provided by Department of Statistics under the Government of the Republic of Lithuania.

Manufacturing industry is the most important sector of Lithuanian economy in terms of creation of value added (see Fig. 2) and it accounts for the largest share of the country’s export: 60% of its products are exported.

4 EUROSTAT, Labour productivity per hour worked.5 Average value added created by a worker during 1 hour.

0

10

20

30

40

50

60

70

80

90

100

Manufacturing industry

Supply of power,gas and water

Building Domest.trade Transport,warehousing

Commu-nications

Financialintermediation

Real estate etc.

Labo

ur p

rodu

ctiv

ity, L

TL/h

our

2002 2003 2004 2005

7

Figure 2. Structure of value added created by industries in 2005,

Source: Department of Statistics under the Government of the Republic of Lithuania.

However, the rate of growth in labour productivity in the manufacturing industry has decreased in recent years, which shows the need for the modernization of industry and investment into new technologies. In addition, productivity of Lithuanian industry is still considerably lagging behind the EU Member States: according to EUROSTAT, in 2003 the ratio between the value added and the number of workers in the manufacturing industry was approx. 7 times lower than the EU-25 average. According to the same source, Lithuania’s productivity indicator is 7–9 times lower than those of United Kingdom and Germany and approx. 2 times than those of Estonia and Czech Republic even in wood processing industry, where the advantages of Lithuanian enterprises are traditionally recognized (see Fig. 3).

Manufacturing industry

22%

Education5%

Agriculture6%

Public administration and defence

5%

Health and social work

3%Mining

1%Real estate

ad other activities10%

Power, gas and water supply

4%Construction

8%Domestic trade

18%Hotels and restaurants

2%

Transport, warehousing

10%

Financialintermediation

3%Communications

3%

8

Figure 3. Labour productivity in sectors of manufacturing industry by countries in 2003, by countries, EUR’000

Source: EUROSTAT.

Unsatisfactory labour productivity rates are partially determined by a small share of the product created by high and medium-high technology sectors6 in the country’s industry as a whole.

According to the Lithuanian Department of Statistics, in 2005 the product created by high and medium-high technology sectors accounted for just 16.1% of the industrial products sold (see Figures below). Another reason for low labour productivity is low value added created by traditional sectors accounting for the largest part of the Lithuanian economy.

6 According to NAC classification defined by EUROSTAT and OECD. This term is used further in this document:High and medium-high technology sectors: medicines industry, production of medical chemical products and botanical products (24.4), production of chemicals and chemical industry products (24 except 24.4), production of office equipment and computers (30), production of radio, television and communications equipment and devices (32), production of medical, high-precision and optical devices and clocks of various types (33); production of other electric machinery and equipment not elsewhere classified (31), production of motor vehicles, trailers and semi-trailers (34), production of railway and tramway locomotives and rolling stock (35.2), production of aircraft and spaceships (35.30), production of motorcycles and bicycles (35.4), production of other transport equipment not classsified elsewhere (35.5), production of other machinery and equipment not elsewhere classified (29), also the knowledge-intensive high-technology service sectors: post and telecommunications (64), computers and related activities (72), research and development (73).

020406080

100120140160

Wood and wood

productsindustry

Furniture industry Textile industry Chemicals industry

Machine building

Belgium Denmark G.Britain Germany Czech R. Estonia Latvia Poland Lithuania

Labour productivity, thousands E

UR

9

Figure 4. Structure of products sold by high and medium-high technology industries (share in total sales: 16.1%).

Source: Department of Statistics under the Government of the Republic of Lithuania, 2005

Figure 5. Structure of products sold by low and medium-low technology industries (share in total sales: 83.9%).

Source: Department of Statistics under the Government of the Republic of Lithuania, 2005

In Lithuania the largest part of value added is created by the service sector, however, the growth in labour productivity and in value added per worker of the service sector is unsatisfactory as in this sector the introduction of process- and technology-related innovations is quite complicated, while highly-qualified labour force is the main factor of productivity.

In macroeconomic terms, material investments or investments in the formation of capital base is the main precondition for long-term growth of the economy. This, in part, reflects a traditional view that growth in productivity is related to the increase in the share of capital-intensive business sectors/businesses, which results in a higher GDP per capita.

According to EUROSTAT, in 2005 the share of investments in the formation of capital base of GDP in Lithuania was 22.3%, exceeding the average of the old EU Member States (19.8%). However, this value was lower than those of most new Member States (see Fig. 6), with the value of China, which is marked by increasing competitiveness and influence in the global economy, being as high as 45.6% in 2004.

Office equipment and computer

industry 0.1

Radio, TV and comm.equipment industry

, 2.6

Chemicals

industry 5.6

Motor vehicles, trailers and s.trailers industry

0.4

Medical, precision and optical devices industry

0.8

Other transport equipment industryį

1.9Machinery and equipment 2.4

Electrical machinery and equipment industry

2.3

Foodstuffs and beverages industry

17.5 Refined oil products industry

30.3

Other (less than 4%), 17.2

Rubber and plastic articles industry

4.0

Furniture industry and other production not elsewhere classified

4.4

Sewing of clothing, hide industry

4.9

Wood and wood products industry

(except furniture) 5.7

10

Figure 6. Investment share of GDP in 2005, %

0 5 10 15 20 25 30 35

Belgija

Čekija

Danija

Vokietija

Estija

Latvija

Lietuva

Lenkija

Didžioji Britanija

Vengrija

Slovėnija

Slovakija

% nuo BVP

Source: EUROSTAT.

Concerns are aroused by the fact that in Lithuania the majority of capital formation costs, which are of particular importance in order to achieve higher productivity and competitiveness of industries, are formed of investments into buildings, engineering structures and land (68% in 2005) rather than of productive investments in equipment and machinery (32% in 2005)7.

Furthermore, according to EUROSTAT, in 2004 the share of Lithuanian business investments in the national GDP structure exceeded the average of the old EU Member States (Lithuania 18.5%, EU-15 average 17.1%) to a lesser extent that the share of total investments in GDP and was lower than that of most new EU Member States (see Fig. 7).

7 Department of Statistics under the RL Government, www.std.lt. 11

Figure 7. Share of investments by businesses in GDP in 2005, %

0 5 10 15 20 25 30

Belgija

Čekija

Danija

Vokietija

Estija

Latvija

Lietuva

Lenkija

Didžioji Britanija

Vengrija

Slovėnija

Slovakija

% nuo BVP

Source: EUROSTAT.

Although at present knowledge and innovations are considered to be the main driver of economic growth and are in the centre of growth strategies adopted by most developed countries, Lithuania is a country of transitional economy and medium income, therefore, the importance of capital base formation as a productivity growth factor should not be underestimated; it must be coordinated with the qualifications improvement and creation of knowledge in target areas in order to achieve long-term economic growth.

International trade is of great significance for Lithuania as a state with a small domestic market. Although growth trends prevail in the export of goods and services (in 2005 there was a 26.9% growth in both types of export), however, lately the share of re-export has been increasing: last year re-export volume increased by more than 40% and accounted for more than 1/5 of total export volumes. The increase in the exportation in products of Lithuanian origin was more moderate last year – by nearly 23% (LTL 25.6 billion in 2005); mineral products (whose value was increased by leaps of oil product prices) excluded – by just 16% (LTL 16.76 m) (see Fig. 8).

12

Figure 8. Goods exports and exports of goods of Lithuanian origin in 2000–2005, LTL m

Source: Department of Statistics under the Government of the Republic of Lithuania.

Production of Lithuanian industries is increasingly aimed at foreign markets. In 2005, export sales accounted for 60,1% of products sold by the mining, quarry and manufacturing industry (or 52,6 % excluding sales of refined oil products). Industries producing foodstuffs and beverages, construction materials and ceramic products target mainly the domestic market.

The structure of products sold by individual industries is shown in Fig. 9.

0

5000

10000

15000

20000

25000

30000

35000

2000 2001 2002 2003 2004 2005

Goods export Export of goods of Lithuanian originExport of goods of Lithuanian origin excl. mineral products

13

Figure 9. Structure of products sold by main industries in 2005 (preliminary data provided by the Department of Statistics),

Source: Overview of Economic and Social Condition of the Economy of the Republic of Lithuania in 2005

Manufacture and mining and quarryingManufacture of food products and beveragesManufacture of textilesManufacture of wearing apparel; dressing and dyeing of furManufacture of wood products Manufacture of pulp, paper and paper product industryManufacture of refined petroleum productsManufacture of chemicals and chemical productsManufacture of other non metallic materialManufacture of machinery and equipmentManufacture of electrical machinery and apparatusManufacture of radio, television and communication apparatusManufacture of rubber and plastic products

An analysis of exports by classes of goods (Fig. 10) shows that mineral products, machinery and electric equipment, textiles and textile articles, vehicles and equipment, and products of chemical and allied industries accounted for the largest part of Lithuanian exports in 2005.

14

Figure 10. Structure of exports of goods of Lithuanian origin by goods chapters, 2005, %

Source: Department of Statistics under the Government of the Republic of Lithuania.

As economic growth of Lithuania largely depends on the development of export, promotion of export-oriented business is essential. Furthermore, more rapid growth of re-export of investment goods compared to that of import of the same goods testifies to insufficient increase in the domestic demand for such goods and confirms the aforesaid statement about insufficient investment into productivity-increasing measures.

Evaluation of International Competitiveness of Lithuanian Economy

Labour, capital, knowledge and entrepreneurship are the factors of economic growth. The level of development of these factors as well as their use in economic activities determines, on its turn, the main condition of the country’s sustainable growth – competitiveness of the national economy on international scale. Competitiveness is always related to productivity, however, whereas productivity shows the position of the economy in the short term, competitiveness shows it in the long term. Competitiveness and productivity of Lithuanian business are relatively low and insufficient compared with performance of European undertakings.

Furthermore, it has been established that8 competitive advantages of most businesses, which are “statistically” classified as high-value-added sector businesses, are based not on knowledge and innovations but on relatively lower operating costs, i.e. lower wages and cheaper raw materials compared to the old EU Member States or basic technologies introduced in previous years. In particular, this can be said about traditional industries whose competitiveness has traditionally been based on low labour cost.

As the main factor of competitiveness – cheap qualified labour force (in terms of productivity) – has been exhausted for Lithuania, the national economy loses the basis for long-term growth, in particular taking account of the growth of the Asian economies and increasing competitiveness of Asian industries on an international scale. This issue concerns the EU economy as a whole, not only Lithuania, however, it is and will be most painful for the Lithuanian economy as it is dominated by traditional industries with low value added.8 Comprehensive Study of Sources (Factors) of Growth and Competitiveness of the Lithuanian Economy, Vilnius, 2006, p. 257.

34,6

6,8

10,28,9

2,6

36,9

V. Mineral products

VI. Chemicals industry

XI. Textiles and textile articles

XVI. Machinery and mechanical equipment

XVII. Vehicles

Other products

15

According to the Global Competitiveness Report published by the World Economic Forum, in 2001–2005 Lithuania’s rating of growth in competitiveness was between 36 and 43 (the number of countries participating in the surveys is increasing every year). In 2001, Lithuania was 43 among 75 participating countries, in 2002 – 39 (among 80), in 2003 – 40 (among 102), in 2004 – 36 (among 104), and in 2005 Lithuania descended to the 43rd position again (among 117 countries of the world, although only 2 new EU member states demonstrated better performance than Lithuania).

Three factors of competitiveness should be identified within the framework of the Operational Programme on Economic Growth: “2. Technology Level: Innovation and Dissemination of Technologies”, “7. Sophistication of Businesses” (both of them having unsatisfactory indicators) and “6. Domestic Competition and Formation of Clusters” (see Table 3).

Table 3. Ratings of Lithuanian’s competitiveness factors in the European context.Lithuania’s position on Europe Strong Neutral Weak

1 Macroeconomic environment 8 3 10

2Technological level: innovations and spread of technologies 0 4 17

3Human resources: education, health care and labour productivity 3 4 4

4 Public infrastructure 0 1 75 Public administration institutions 1 5 216 Domestic competition and clusterisation 1 6 47 Sophistication of businesses 2 9 138 Environmental protection 0 4 5

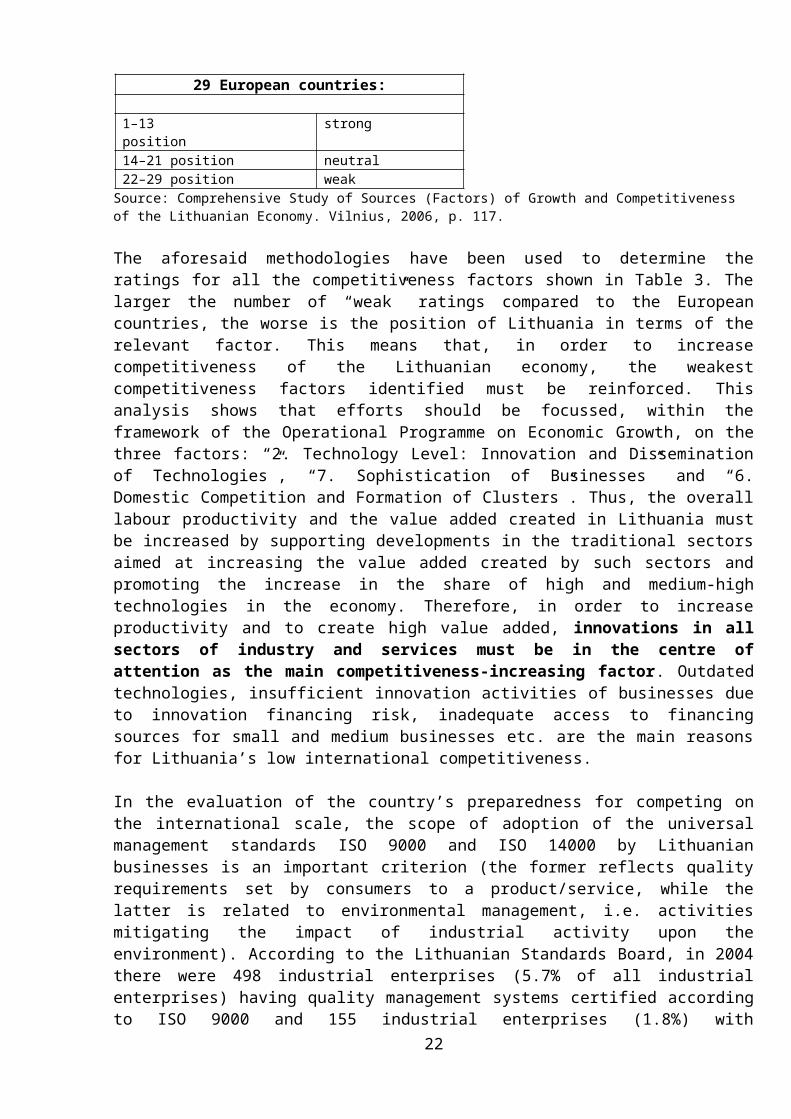

Note: Each indicator of relevant factor is assessed in comparison with indicators of the 29 European countries within the range (Strong-Neutral-Weak). The number of indicators within each category is presented in the Table.Source: Comprehensive Study of Sources (Factors) of Growth and Competitiveness of the Lithuanian Economy. Vilnius, 2006, p. 123.

Each factor of competitiveness presented in Table 3 above has been assessed using relevant indicators. For example, 21 indicators have been used for the competitiveness factor “Macroeconomic Environment” (probability of recession, influence of terrorism upon business, sophistication of financial market, strength of banks etc.). Lithuania’s relative position among the 29 European states (25 EU Member States and 4 EEA states – Switzerland, Norway, Israel and Iceland) has been estimated according to each of these indicators, rating it as “strong”, “neutral” or “weak” in accordance with the methodology presented in Table 4 below.

Table 4. Methodologies for determining competitive strength/weakness of Lithuania

Lithuania’s position in the ratings of 29 European countries:

1–13 position strong 14–21 position neutral22–29 position weak

Source: Comprehensive Study of Sources (Factors) of Growth and Competitiveness of the Lithuanian Economy. Vilnius, 2006, p. 117.

The aforesaid methodologies have been used to determine the ratings for all the competitiveness factors shown in Table 3. The larger the number of “weak” ratings compared to the European countries, the worse is the position of Lithuania in terms of the relevant factor. This means that, in order to increase competitiveness of the Lithuanian economy, the weakest competitiveness factors identified must be reinforced. This analysis shows that efforts should be focussed, within the

16

framework of the Operational Programme on Economic Growth, on the three factors: “2. Technology Level: Innovation and Dissemination of Technologies”, “7. Sophistication of Businesses” and “6. Domestic Competition and Formation of Clusters”. Thus, the overall labour productivity and the value added created in Lithuania must be increased by supporting developments in the traditional sectors aimed at increasing the value added created by such sectors and promoting the increase in the share of high and medium-high technologies in the economy. Therefore, in order to increase productivity and to create high value added, innovations in all sectors of industry and services must be in the centre of attention as the main competitiveness-increasing factor. Outdated technologies, insufficient innovation activities of businesses due to innovation financing risk, inadequate access to financing sources for small and medium businesses etc. are the main reasons for Lithuania’s low international competitiveness.

In the evaluation of the country’s preparedness for competing on the international scale, the scope of adoption of the universal management standards ISO 9000 and ISO 14000 by Lithuanian businesses is an important criterion (the former reflects quality requirements set by consumers to a product/service, while the latter is related to environmental management, i.e. activities mitigating the impact of industrial activity upon the environment). According to the Lithuanian Standards Board, in 2004 there were 498 industrial enterprises (5.7% of all industrial enterprises) having quality management systems certified according to ISO 9000 and 155 industrial enterprises (1.8%) with environmental management systems certified according to ISO 14001 in place. Lithuania, just like other new EU Member States, lags behind the old Member States according to the number of ISO 9000 certificates issued. In this respect, only Hungary and Slovenia stand out – these countries are active participants in the international technological networks.

The insufficient spread of quality control mechanisms in Lithuania9 shows both Lithuanian businesses’ poor preparedness for international competition and limited potential for increasing production efficiency (the importance of the aforesaid quality control mechanisms for the increasing of products’ competitiveness and efficiency has been internationally recognised). Lack of guarantees for product quality and of quality control mechanisms shows that there is no strong basis for innovativeness at businesses.

During the period 2000–2004, only in 2001 emissions of pollutants into the air had noticeably decreased in absolute terms (see Table 5); in this period industrial emissions into the air increased 1.62 times (from 56,200 t in 2000 to 91,200 t in 2004). In general, emissions into the air have been reduced by 16% during the past decade, however, in industry they increased by 40% in the same period. There have been positive trends in the ratio between the pollutant emissions into the air and the GDP. In 1995 this ratio was 20.4 t/GDP LTL m; during the decade it decreased nearly 3 times – to 7 t/ GDP LTL m.

Table 5. Air emissions of pollutantsThou. Tons1995 2000 2001 2002 2003 2004

Total emissions 522 445,6 414 417,2 423,6 438,7T / LTL m GDP 20,4 9,7 8,5 8 7,4 7Industry 65 56,2 62,9 64,1 80,1 91,2Energy 176 191,3 186,9 182,5 170,5 162,6Transport 281 198,1 164,2 170,6 173 184,9Source: Department of Statistics under the Government of the Republic of Lithuania.

9 Comprehensive Study of Sources (Factors) of Growth and Competitiveness of the Lithuanian Economy. Vilnius, 2006.

17

Industry remains the most energy-intensive sector of the economy (see Table 6). The energy intensity of industry has decreased 2.2 times over the past decade. In the service sector, the decrease has been insignificant during 2000–2004 (1.09 times), however, since 1995 energy intensity has halved both in this sector and in the economy as a whole.

Table 6. Energy consumption intensity in Lithuania Tons of oil equivalent (TOE) / million LTL of GDP1995 2000 2001 2002 2003 2004

Overall 122,4 79,5 77,5 75,2 69,8 68,1Agriculture 59,7 27,7 29,4 29,6 25,8 26,5Industry 104 58,8 52,5 54,3 49,2 47,1Construction 16,9 15 12,9 12,6 11,3 11Transport 28 23 23,6 22,9 21,2 21,8Services 31,5 16,4 15,7 15,2 15,2 15Households 44,2 29,3 28,1 26,4 24 22,2Source: Department of Statistics under the Government of the Republic of Lithuania.

The dynamics of energy consumption and energy intensity in Lithuania is in line with the average EU trends: there has been an increase in final energy consumption (according to EUROSTAT, a 10.9% growth in EU-25 in 1995–2004), while energy intensity is decreasing (according to EUROSTAT, a 9.3% decrease in EU-25 in 1995–2004).

Foreign Direct Investments

Many EU Member States place emphasis upon the improvement of investment environment in order to increase competitiveness on international scale as foreign direct investment (FDI) is one of the most important factors creating favourable conditions for technological progress and economic growth. FDI is an important source of formation of capital base and competences, therefore, attracting FDI, in particular in knowledge-intensive or technological breakthrough areas, is essential to Lithuania if it wishes to secure long-term economic growth and re-orientate business toward creation of higher value added. Lithuania has accumulated research potential in certain strategic areas that are competitive on the international scale, therefore, this forms a basis for the attraction of strategic investments to knowledge-intensive sectors even from the USA or Asian countries. In this way the European Union’s competitiveness and attractiveness for investors would be promoted.

Different indexes are used to compare FDI volumes and effectiveness on international scale. UNCTAD (United Nations Conference on Trade and Development) investment indexes such as the Inward FDI Performance Index and the Inward FDI Potential Index are among the most widely used. Lithuania’s performance as measured by these FDI indexes has been positive in the past decade. According to the Inward FDI Performance Index, Lithuania has risen from the 78 th position in the UNCTAD rating in 1990–1992 to the 55th position in 2001–2003. According to the Inward FDI Potential Index, in 1990–1992 Lithuania was in the 70th position and in 2003–2004 – in the 47th

position.

However, recent trends in attracting FDI to the Lithuanian economy are not satisfactory:

firstly, there is no explicit increasing trend in the recent years’ annual FDI volumes: a comparison of the annual FDI volumes shows marked fluctuations (see Fig. 11);

secondly, according to the comparative FDI indicators Lithuania significantly lags behind some new EU Member States such as the Czech Republic, Estonia and Hungary (see Fig. 12).

18

Figure 11. Annual volumes of FDI in Lithuania, LTL m

1394,8 1361,3

2338,7

1750,9

1085,21324,6

2521,9

515,6

2493,2

0

500

1000

1500

2000

2500

3000

1996 1997 1998 1999 2000 2001 2002 2003 2004

Source: Calculated according to data provided by the Department of Statistics under the Government of the Republic of Lithuania.

Figure 12. Annual FDI per capita in the new EU Member States, EUR

Source: EUROSTAT.

Differences in FDI by counties testify to economic discrepancies among Lithuania’s regions (see Table 7): the lower the level of development of a region, the lesser the region’s attractiveness to foreign investors. In Vilnius County, FDI per capita was LTL 11,721 at the beginning of 2005, exceeding the national average by more than 2 times.

Table 7. FDI per capita by Lithuanian countiesFDI per cap. at year beginning, LTL Compared with national average, %

2001 2002 2003 2004 2005 2001 2002 2003 2004 2005

National average 2678 3068 3808 3976 4727 100 100 100 100 100

Alytus county 1162 784 758 1026 933 43,4 25,6 19,9 25,8 19,7

Kaunas county 1725 1874 2260 2675 2751 64,4 61,1 59,3 67,3 58,2

Klaipėda county 2966 3363 3547 4038 4561 110,8 109,6 93,1 101,6 96,5

Marijampolė county 142 325 392 419 604 5,3 10,6 10,3 10,5 12,8

Panevėžys county 1271 1515 1545 2299 2491 47,5 49,4 40,6 57,8 52,7

Šiauliai county 419 449 488 514 537 15,6 14,6 12,8 12,9 11,4

Tauragė county 160 146 109 170 163 6 4,8 2,9 4,3 3,4

Telšiai county 478 95 3102 4311 6619 17,8 3,1 81,5 108,4 140

Utena county 586 1109 1831 1390 1120 21,9 36,1 48,1 35 23,7

Vilnius county 7032 8232 10010 9581 11721 262,6 268,3 262,9 241 248Source: Department of Statistics under the Government of the Republic of Lithuania.

0200400600800

10001200140016001800

Czech R.Estonia Latvia LithuaniaPoland Hungary Slovenia Slovakia

EUR

19

Foreign investors’ behaviour has been changing, and not to Lithuania’s benefit: recently, there has been a trend for directing spare capital and business to those countries which have high domestic market capacity and good prospects for the purchasing power increases (China, India, Brazil, (partly) Russia)10. Cheap qualified labour force – the main competitive advantage of Lithuania – is no longer a chief motive for selecting investment locations. Furthermore, as wages have been increasing at a higher rate than labour productivity, Lithuania will not be able to make use of this advantage in the nearest future. Therefore, Lithuania has to search for and develop other competitive advantages such as qualified labour force, availability of new specialists trained under new specialised curricula, flexibility and effectiveness of local small and medium-size enterprises (hereinafter referred to as SME), service quality and availability of scientific potential – all of which can determine Lithuania’s competitive advantage in the eyes of foreign investors.

Lithuania’s opportunities in the competition for foreign investments are diminished, among other things, by such circumstances as too detailed regulation of labour market relations, lack of territories earmarked for investment attraction (investment areas), underdeveloped business support infrastructure and overall business environment, too bureaucratic and complicated procedures for the acquisition of land and issue of building permits etc. In particular, potential investors often encounter in Lithuania such obstacles as incomplete restitution procedure in respect of land lots, fragmentation of lots where a land lot of acceptable size consists of several lots owned by different persons, unclear procedure for the transfer of public land to municipal ownership, lack of opportunities for investors to acquire land in a way other than auction, limited opportunities for land disposal by municipalities etc.

In 2004 alone, 36 foreign companies were looking for an opportunity to invest and failed to invest through the lack of satisfactory conditions. Almost LTL 1.4 billion were not invested and over 4,800 jobs were not created11.

Attraction of investments (both local and foreign) is largely limited by the nearly total lack of fully prepared investment areas with infrastructure. According to the findings of an analysis of the demand for industrial lots in Lithuania (2005)12, the area of territories prepared for investment totalled 13.4 ha, mainly around the capital Vilnius. The estimated annual demand for industrial parks with complete infrastructure, suitable for investment, amounts to 98 ha13. Four regions account for the majority of the demand: Vilnius (35 ha/year), Kaunas and Šiauliai (15 ha/year each) and Klaipėda (10 ha/each).

If conditions for meeting this demand are not created, FDI that are a potential source of growth and competitiveness of the Lithuanian economy will leave Lithuania aside. Therefore, in order to create most favourable conditions for foreign capital investment, first of all the establishment of industrial parks with complete or partial infrastructure must be promoted. However, FDI attraction factors are not limited to the establishment of physical infrastructure – they are related to the overall business environment, qualifications of businesses and labour, and favourable conditions for research and development. Focus should also be placed on the investment attraction policy pursued by the public authorities (both central and local), which should be aimed, first of all, at attracting 10 AB SEB Vilniaus Bankas. Lithuanian Macroeconomic Overview, 4 (24), March 2006.11 According to the Lithuanian Economic Development Agency.12 Project on Assistance to Greenfield Investment in Lithuania, Technical Report No. 2 “Forecast of Industrial Lots Demand in Lithuania”, ECORYS Nederland BV, 2005.13 Ibid

Table 8. Annual demand for industrial lots for greenfield investments Region Demand, haAlytus 3Kaunas 15Klaipėda 10Marijampolė 4Panevėžys 5Šiauliai 15Tauragė 2Telšiai 6Utena 3Vilnius 35Lithuania total 98Source: Project on Assistance to Greenfield Investment in Lithuania, Technical Report No. 2 “Forecast of Industrial Lots Demand in Lithuania”, ECORYS Nederland BV, 2005.

20

high and medium-high technologies and at support for technology transfer, taking local business structures, employee qualifications and prevailing industries into consideration. Account must be taken of the fact that favourable business environment enhances the impact of FDI upon the economy and promotes the spillover effect.

Overview of Joint Business Activities

A qualitatively new role of cluster and network formations – alliances is one of the four key elements of the “new rules of game” in international competition.

Lithuania is not in a position to achieve international competitiveness in all the industries. It has neither resources nor competences for this purpose. Therefore, it is important to select the correct basis for competitiveness. It is also clear that it is difficult for individual market players (irrespective of whether they are representatives of business, research or public administration) to achieve the quality required by the new economy. The key to achieving this is partner networks, clusters and other forms of joint activities as only such structures generate the synergy effect, each interest group realises its objectives in the most effective way, and a relative advantage is created.

Names for groups of businesses and organisations as well as their specific features vary from country to country (clusters, industrial regions, local business systems, competence networks etc.). However, they have common characteristic – joint efforts to derive maximum benefit through cooperation and competition both outside and inside the group. The efficiency of the group as well of the macro system (the industry, the region, and the state) depends on the number of efficient entities forming the group as well as on the efficiency of each of them. An effective cluster functioning on partnership basis contains flows of knowledge exchange, which are intensive due to both internal and external competition and which stimulate innovations and competitive advantage and economic growth of such group.

During the past few years a number of different studies on the formation of clusters in Lithuania have been carried out.

Clusterisation processes have been most active in the wood and furniture industry; there are certain initiatives in clothing, machine and food production industry.

Machinery and apparatus industry is characterised by perhaps the greatest degree of fragmentation: the range of articles produced by the enterprises is very wide. From the standpoint of clusterisation, it is both an advantage and deficiency. At present it is too early to assert that this industry has features characteristic of clusters. One may see a lot of cooperation links between enterprises of the same sub-branch and between different sub-branches, however, in most cases the relations are not stable and mainly involve mutual supplies; the degree of partners’ involvement in joint activities is low. A competence cluster for mechatronic solutions is the most tangible potential cluster, in the establishment of which a number of enterprises and research organisations are interested.

Wood-processing and furniture industry is fully mature for an informed and targeted clusterisation. A number of micro-clusters can be identified in this industry. By its nature, wood-processing and furniture industry is favourable for the formation of regional clusters. The sector has been developing rapidly, however, closer cooperation with mechatronics and information and telecommunications (ITC) business would result in speedier modernisation of production.

Despite unfavourable international developments, textile and clothing industry has a potential of remaining an important part of the Lithuanian economy. Deep and, at the same time, horizontal clusterisation is one of the key conditions for survival and further growth for most enterprises of this industry for which clothing is final product of operations. As the Lithuanian textile and clothing industry is quite fragmented, there is a number of enterprises whose operations are not related or

21

little related to the production of clothing; operations of some of the enterprises have been quite successful. A lot of embryonic cluster developments can be observed, however, often even the enterprises themselves do not notice the depth of and opportunities provided by the relations and, therefore, do not make use of potential benefits.

The Integrated Study into the Sources (Factors) of Growth and Competitiveness of the Lithuanian Economy conducted at the beginning of 2006 identifies several main reasons why establishment of clusters in Lithuania is slow:

- lack of trust among clustered entities;

- discrepancies in the technology and management level of different businesses. This is important in order to create a sustainable chain of value creation, with quality services provided / operations performed by individual actors;

- underdeveloped business information systems. The present systems are of low quality; they are rarely used or not known at all by businesses. Also, there is a lack of quality information relations among businesses in the same sector except for information about related areas of activities, markets etc.;

- lack of competencies and experience in working with partners. Management of clusters, networks, cooperation ties and virtual business systems differs from usual management. At present Lithuanian enterprises and organisations have a very limited number of people with such competences;

- lack of entrepreneurship. Entrepreneurship is understood as an activity by an entity – a business, research organisation, state institution etc. – whereby high objectives are consciously adopted and there exist capabilities to pool resources of the entity with those of other stakeholders in order to attain the objectives in an innovative manner;

- ineffectiveness of professional and branch associations. Associative structures are an important element forming the core of a cluster. If it is absent, management and promotion of processes become more difficult;

- ineffectiveness of innovation system. Innovativeness is one of distinctive features of clusters. Innovative processes are determined by the structure of the cluster and the logic of joint activities. However, there is also a reverse dependence: an environment favourable for innovations is required for the establishment of innovative clusters. Lithuania has almost all components of the national system of innovations in place for the moment; however, the system itself has received critical evaluation and is not effective. The operation of the innovation business programme has also been ineffective; relations between research organisations and businesses are insufficient.

The aforesaid reasons show that integrated measures should be used to promote clusterisation processes, such as strengthening of relationship between businesses and research organisations, formation of innovation-friendly environment, creation of conditions for the transfer of partnership experience, support for different joint activity initiatives, and building of businesses’ capacities to use the existing competences and knowledge and to manage business processes effectively.

The Role of SMEs in the Lithuanian Economy

Small and medium-sized enterprises prevail in Lithuania just as in most other states. In 2000–2004 the share of SMEs in the total number of active enterprises was stable and amounted to 99.4% on average. At the end of 2004, micro-enterprises (less than 10 employees) accounted for 75.9% of all active SMEs (75.5% of all active enterprises). The role of SMEs in the Lithuanian economy has been increasing: SMEs create an increasingly larger share of GDP; in 2004 this share accounted for 69.1% of GDP (59.3% in 2001).

22

Figure 13. Share of GDP created by SMEs in 2001–2004, %

Source: Department of Statistics under the Government of the Republic of Lithuania, 2005

An analysis of SMEs distribution by economic activities in 2004 shows (see Fig. 14) that most of them operated in the trade sector (38.1% of all SMEs); services sector in on the second place (24.8%). In 2004 15.11% of all SMEs operated in the industrial sector. In 2001–2004 the share of industrial enterprises in the total number of SMEs was stable and was 15.6% on average, whereas in 2004 compared to 2001 the share of SMEs providing services increased by 1.6 percentage point and accounted for 24.8% of all SMEs.

Figure 14. Structure of active SMEs according to type of economic activity as of the end of 2001–2004, %

Source: Department of Statistics under the Government of the Republic of Lithuania, 2005

Trade – Industry – Services – Construction – Other activities

The role of SMEs in the national economy has been increasing due to changes on the labour market and the impact of globalisation upon competitiveness of industries, especially the role of those SMEs that are small, flexible, easily transformable, niche-order-oriented, service-oriented, and can make operational changes quickly and adapt to the dynamic environment. Therefore, it is important to implement measures to improve business environment, aimed at the establishment of SMEs and increase of competition. To meet SMEs needs, special awareness-increasing, consulting, business incubation etc. measures should be developed and access to different financing sources should be improved.

Access to Finance for Businesses

23

Ensuring appropriate and timely financing both in the initial and further phases of operation is one of the main challenges in business.

Lithuanian businesses’ requirement for external financing has been growing along with the quite speedy economic growth. According to the findings of a survey14, about 50.5% of the country’s businesses approach national financing institutions for business financing; small enterprises account for about 49% of them. Service firms are most active in this respect, although industrial enterprises are also quite active in seeking additional financing for business. Financing is mainly required for investments in equipment; followed by investments in other tangible assets; taking over of accounts receivable; and acquisition of raw materials and stocks. Investments in innovations are on the fifth place. Businesses mainly use services provided by banks and financial lease companies. According to survey results, in the future businesses intend to continue to approach mainly banks.

The Lithuanian financial market is well developed, however, investors and credit institutions are reluctant to finance venture projects, especially those undertaken by new businesses. The need for external credits caused by rapid economic growth and the credit institutions’ attempts to minimise loan portfolio administration costs have resulted in a situation where credit institutions give priority to large and medium businesses with historical operations and applying for large loans; although a gradual reversal in this trend is observed. Furthermore, financing of innovations and early development phases using debt instruments is not widely used due to quite high risks. The problem also lies on the demand side, i.e. unpreparedness of small business for bank financing, lack of collateral and information on financing instruments.

To promote the financing of innovations and early development phases using debt instruments, State guarantee institution Plc “Investment and Business Guarantees” (UAB “Investicijų ir Verslo Garantijos” – INVEGA) was established in 2001 by resolution of the Government. The company provides guarantees to banks for loans to SMEs and is responsible for the administration of partial payment of interest on such loans.

Nevertheless, other state-supported SME financing instruments actively offered by the European Commission are used very passively or not used at all, e. g. provision of small loans (microcredits) to start-ups is not active, venture capital foundations do not actively finance new innovative projects proposed by businesses.

In the European Union a lot of attention is devoted to microcredits as this is both – an important instrument to increase entrepreneurship and economic growth and a tool to resolve employment problems of certain social strata. This is particularly relevant to enterprises established by former unemployed, women or young people. Lithuanian credit institutions are not active enough in making microcredits to start-ups. Among commercial banks, only Šiaulių Bankas AB has been offering a special microcrediting service, i.e. credits ranging from EUR 1,500 to 30,000 to SMEs from the funds of the European Bank for Reconstruction and Development. In the middle of 2006, Šiaulių Bankas, Medicinos Bankas UAB and DnB NORD Bankas AB started giving microcredits up to EUR 25,000 (or equivalent) from public funds, first of all to microbusinesses. Other commercial banks operating in Lithuania also showed active interest and participated in the selection procedure, however, the public funds available were not sufficient to meet the requirement – which may be up to LTL 100 m per annum – in full. In addition, credit unions also make small loans to their members.

The Lithuanian venture capital market is still underdeveloped, whereas in the European Union venture capital foundations are widely used to finance businesses. The amount of such foundations established in the EU since 1980 exceeds EUR 200 billion. In Lithuania the amount of venture capital invested in the decade from 1 January 1995 till 1 January 2005 totalled LTL 1.4 billion; 166 investment projects were implemented. During the past decade, Lithuania’s annual venture capital investments per 1 million population were 5 times smaller than the EU average; the number of

14 Research work on Measures to Improve Financing Opportunities for Small and Medium Business (2004).24

businesses that had attracted venture capital investments (per 1 million population) was 4 smaller than the EU average15.

The country’s venture capital market is lagging behind the EU Member States mainly in the area of providing funding to innovation projects and start-up businesses. Promoters of venture projects first of all encounter a lack of seed capital – many excellent business ideas are not capable of attracting such capital16. In Lithuania, venture capital for the start-up and development of innovative business in the past decade accounted for just 19% of the EU average. 15% of the venture capital was used to finance starting up businesses; 19% - for ICT. The average venture capital amount per investment is quite large and amounts to LTL 8.2 m.

Lithuania’s venture capital market, particularly in terms of financing of innovative businesses and start-ups, is underdeveloped both due to supply and demand problems. Risk capital foundations tend to invest in companies with a history of operations rather than start-ups; they also prefer large investments with the probability of higher return-on-investment. The problem of information asymmetry remains – investors lack information on innovative projects and operations of start-ups. Whereas the problem on the demand side arises due to deficiencies of preparation of venture investment projects, lack of information on financing instruments and opportunities, and lack of financing instruments. Therefore, in order to minimise problems related to access to finance, integrated actions to consistently and systematically form the supply and the demand are required.

Ratings of the Lithuanian Business Environment and Business Competitiveness

According to the results of an analysis of 145 countries made by the World Bank and the International Finance Corporation (Doing Business in 2005)17, Lithuania is among the top 20 countries of the world with the most favourable business environment. However, it should be noted that this relatively high rating has been mainly determined by macroeconomic indicators.

Ratings of Lithuanian business activities are not so favourable. Lithuania lags behind the EU Member States according to level of entrepreneurship: in 2004, the indicator of the number of businesses/self-employed persons per 1,000 population was 42.8 compared to the EU average of 55. According to the Business Competitiveness Index18 that assesses the quality of management and strategies of businesses as well as the national environment for the adoption of business decisions, Lithuania’s rating for 2005 was as low as 41 (during the year it fell down from 36), falling behind most EU Member States except for Poland (42 position), Malta (46) and Latvia (48).

The main problems of the Lithuanian business environment and the businesses’ activities, in particular innovation activities, are related to the:lack of working capital and insufficient access to finance (in particular venture capital financing) by businesses, in particular SMEs;underdevelopment of public services and related infrastructure necessary for the establishment of enterprises and business development;insufficient scope of attraction of FDI;insufficient promotion of joint activity forms (clusters, partnerships etc.).

Services to Business and Related Infrastructure

15 Analytical Work on the Investment Portfolio of Venture Capital Funds in Lithuania, 2004.16 Beniušytė, J. Rizikos kapitalo fondų investicinis portfelis Lietuvoje, http://www.std.lt/uploads/apzvalga/L061-069.pdf17 The report Doing Business in 2005 does not take account of such EU-25 states as Luxembourg, Cyprus and Malta, therefore, information on EU-22 is further used.18 The Global Competitiveness Report 2005-2006.- Hampshire: Palgrave Macmillian, 2005.- ISBN: 1-4039-9844-2.

25

The European Commission recognises19 that the EU is not using its entrepreneurship potential in full and the rates of establishment of new businesses are too low. In Lithuania the level of entrepreneurship is very low too (at the beginning of 2005, 16 active SMEs (excluding self-employed) per 1,000 population). Lack of knowledge and fear of starting a business are among the factors affecting entrepreneurship. Furthermore, it is noted that the growth of existing enterprises can be dampened both by increased competitive pressures and by such market deficiencies as limited financing opportunities and inability to conduct integrated research and innovation activities, participate in networks and supply chains. In most EU documents on SME policies, increasing of public awareness, development of business consulting and similar services as well as improving quality of and access to such services is recognised as reasonable and proper instruments for increasing entrepreneurship. Development of high-quality public services to business focussed on the elimination of market deficiencies is a precondition for ensuring a speedier growth of SME sector and competitiveness in Lithuania. As the infrastructure of public services for business is young, Lithuania should assume best foreign practices in the area of public services for business as well as instruments that have proved to be useful in order to promote entrepreneurship and reduce the aforesaid market deficiencies.

The infrastructure of public services for business in Lithuania primarily includes non-profit organisations of different types such as business information centres, business incubators, technological business incubators, science and technology parks and innovation and technology centres established with the participation of state/municipal authorities and agencies performing functions related to economic development, promotion of business and development of technologies and innovation.

In 2005, there were 42 business information centres, 7 business incubators (including 1 technological business incubator)20, 6 science and technology parks21, 2 innovation centres etc.

19 Commission Communication Implementing the Community Lisbon Programme Modern SME Policy for Growth and Employment, KOM (2005) 551, 2005.10.11.20 Regional business incubator of Kaunas Technological University (formed in 1998), Alytus business incubator (1998), Vilnija businesss incubator (1998), Telšiai county business incubator (1998); Šiauliai business incubator (1999); Kazlų Rūda business incubator (2000); Ignalina NPP business incubator (2002). 21 Science and technology park (formed in 1993), Kaunas high and information technology park (2002), Šiaurės Miestelis technology park (2003), Klaipėda science and technology park (2002), Visoriai IT park (2002) , Šiauliai University science and technology park (2002). Technology parks currently under formation include TECHNOPOLIS in Kaunas, BIOPOLIS in Vilnius as well as Saulėtekio Slėnis (Vilnius).

Figure 15. Infrastructure of public services for business

The formation of the infrastructure for public services’ has started not long ago; most of the entities are in the early phase of formation. Lately attention has been focussed on the development of the entities’ physical infrastructure and the reinforcement of their technical facilities. Although the infrastructure and technical facilities’ development phase has not ended as yet, shortcomings in terms of the content, quality and accessibility of services provided by the entities are becoming increasingly apparent, therefore, investments are required in this area, in particular in the adopting of best practices from foreign states. It may be difficult to attain the set objectives in the area of growth in entrepreneurship without making use of this factor in full. In addition, it is important to improve the content and to increase the scope of services for existing businesses seeking competitiveness and growth opportunities.

As regards public infrastructure for business, based on experience of the EU Member States, the Nordic countries in particular, the creative sector should be separated out due to specific infrastructure required for its development22. In promoting entrepreneurship, for Lithuania it is important to develop the creative business sector, mainly micro- and small businesses that flexibly use the national cultural traditions and human creative potential; the sector covers architectural, design, fine art, stage art and other trades creating products and services representing the Lithuanian content. According to the Department of Statistics to the Government of the Republic of Lithuania, in 2002 the creative sector accounted for 2% of GDP, generating an income of LTL 2.1 billion (LTL 2.4 billion including state grants). Income by creative businesses has increased by almost 10% during a year (including state grants). For comparison purposes one may point out that in the United Kingdom creative businesses account for over 5% of GDP23. Promotion of creative businesses is an important measure to increase the value added created in the service sector, innovativeness of businesses, and residents’ entrepreneurship.

22 Public institution VšĮ Menų Spaustuvė has started activities in Vilnius; in the nearest future, another 4 specialised creative centres (incubators) will be developed in Vilnius, Kaunas, Klaipėda and Šiauliai. 23 M. Starkevičiūtė, Kūrybinių ekonominių veiklų indėlio į Lietuvos ekonomiką įvertinimas [Evaluation of the Input of Creative Economic Activities into the Lithuanian Economy], 2003, Vilnius.

Science and technology parks Business incubators Innovation centres Business information centres

Equal Opportunities in Business

The share of women remains smaller than the share of men in the total number of employers and self-employed persons. In 2004, women accounted for 38.3% and in 2005 – for 37.7% of the employers and self-employed persons (see Table 9). In 2005, only 10.7% (2004 – 11.8%) of all women in employment were employers or self-employed persons, while the majority of women were employees (85.4 % in 2005 and 83.8% in 2004).

Table 9. Employment of residents according to employment statistics, 2004–2005 2004 2005 Total, thou. By gender, % Total, thou. By gender, %Women Men Women Men Women Men Women Men

Total 702,5 733,8 48,9 51,1 723 750,9 49,1 50,9Employees 588,8 580,8 50,3 49,7 617,3 606,7 50,4 49,6Employers and self-employed persons

82,9 133,8 38,3 61,7 77,7 128,6 37,7 62,3

Family members 30,8 19,1 61,7 38,3 28 15,5 64,4 35,6Source: Department of Statistics under the Government of the Republic of Lithuania

The share of women managers in the total number of managers has markedly increased over the past 5 years: from just 29.2% in 2000 to 43% in QII of 2005.

Women are actively using the public services for business. According to the findings of the survey of 48 business information centres and business incubators carried out by the Lithuanian Small and Medium-Size Business Development Agency, women accounted for the larger part (60% on average) of the customers at almost all entities. According to EUROSTAT, in QII of 2005 the share of women managers in Lithuania exceeded the EU-25 average

Structural Funds Assistance in 2004–2006

The implementation of Lithuania’s Single Programming Document for 2004–2006 (SPD) has shown active interest of businesses in the EU Structural Funds (SF) assistance. In 2004–2005, 413 project applications under the SPD measure “Direct Support for Business” were received. The total amount required for the projects under the applications (LTL 1.25 billion) was 16 times larger than the amount available to the Ministry of Economy of the Republic of Lithuania for contracts for 2004–2005. During this period, 26 assistance agreements totalling LTL 198.9 were concluded, including 4 agreements with start-ups.

Projects on modernisation of businesses and innovations accounted for the majority of the projects (57%), while projects on research and development and on formation of relationship between industrial entities/businesses and research organisations accounted for just 17% of all the applications filed in 2004–2006. In the first half of 2006, 51 modernisation and innovation projects and 8 R&D and cooperation projects were underway.

In 2004–2006, the demand of SF financing for infrastructure and service-for-business projects was relatively high: 131 applications were submitted. 38% of applications intended for the improvement of the SMEs support system despite the fact that no new entities were established in the networks of services for business, while the existing entities were implementing projects under the services-for-business programme and other projects financed from the national budget and other sources. The

number of applications for other activities under the SPD measure “Improvement of Business Environment” was numerous as well: 17 applications for the formation of industrial zones and promotion of green field investments, 17 for science and technology parks, 12 for the improvement of the image of Lithuanian products and services, and 29 applications by associated business structures. It should be noted that in 2006 associated business structure were very active in the filing of applications (22% of the applications in 2006). It is expected that, in the course of implementation of these projects, services will be provided to over 14 thousand SMEs and support will be provided for the formation of 6 industrial zones and 4 science and technology park.

Comparison of DiscrepanciesTable 10. Key discrepancies between Lithuania and the EU average

Indicator of discrepancy Year Lithuania EU average

Evaluation

Labour productivity per hour compared with EU-15 average, %

2004 41,7 100 Large discrepancy

Entrepreneurship rate, number of businesses and self-employed persons (under business licences or registered individual business) per thou. population

2004 42,8 55 Medium discrepancy

Accumulated FDI per capita, LTL 2004 4 727 24 378 Large discrepancy

Annual venture capital investments per 1,000,000 population, LTL m

2004 74,5*** 233,5 Large discrepancy

*** Calculated according to the data provided in J. Beniušytė’s article “Investment Portfolio of Risk Capital Funds in Lithuania” (source: Beniušytė, J. Rizikos kapitalo fondų investicinis portfelis Lietuvoje. http://www.std.lt/uploads/apzvalga/L061-069.pdf ) (in 2004, venture capital investments amounted to LTL 256 m in Lithuania) and the Department of Statistics (average annual population number in Lithuania was 3.435 m).

1.2. RESEARCH AND DEVELOPMENT. INNOVATIONS

Main statements: Competitiveness of Lithuanian businesses is relatively low and insufficient, which is largely due

to insufficient innovation activities. According to international innovativeness ratings Lithuania is considerably below the EU-15 average, being in the lowest position among the new EU Member States.

The level of investment in research and development is low in Lithuania, in particular in terms of Lithuanian businesses’ investments in R&D.

Lithuania’s public sector’s expenditure for research is close to the EU average, however, both subjects and results of research conducted by universities and institutes do not match business needs; results suitable for commercialisation are lacking.

Research facilities do not meet modern standards; insufficient capacities limit the performance results and effectiveness of research.

Most investments made by businesses do not result in long-term advantages or technological dominance in the market.

Underdevelopment of the system of financial support instruments, in particular for SMEs and higher-risk projects.

International Rating of Lithuania’s Innovativeness

According to the summary innovation index (SII) published in the European Commission’s document “European Innovation Scoreboard 2005”24, the highest innovation score was assigned to Sweden (0.72) and the lowest to Turkey (0.06). Lithuania’s innovation performance has been rated as 0.27. According to its score Lithuania is as low as on the 24th position among 33 countries, with the Czech Republic, Poland, Slovakia, Latvia and some others behind it. Lithuania’s score is markedly below the EU-25 average and, the more so, from the average indicator of EU-15 (0.42 and 0.46 respectively).

Lithuania’s lag compared to the EU innovation leaders is mainly due to the low level of investments in research and development (R&D). Furthermore, it should be noted that Lithuania occupies the lowest positions among European countries according to such innovativeness-related indicators as overall technological level, number of patents, number of the Internet users and PCs, and licensing of foreign technologies. According to the Network Readiness Index annually calculated by the World Economic Forum, in 2004–2005 Lithuania lagged behind most EU Member States except for Latvia, Poland and Slovakia, occupying the 43rd position among 102 states of the world (EU-25 average: 29th position).

Most innovation performance indicators of Lithuanian businesses are lower than the EU-25 average. For example, in 2004 Lithuanian businesses’ expenditure for innovations accounted for 81% of the EU-25 average (Lithuania is on the 12th position according to this indicator) and less than one-third (31%) of Lithuanian businesses have implemented non-technological innovations, which accounts for just 63% of the EU-25 average (16th position according to this indicator).

The number of researchers working in Lithuania’s business sector is very small. According to the Department of Statistics to the Government of the Republic of Lithuania, in 2004 the number was 58925, including only 103 persons with a degree. Compared with the total number of researchers in

24 European Innovation Scoreboard 2005: Comparative analysis of Innovation Performance. The summary innovation index (SII) is obtained by recalculating 18 most popular statistical indicators used to compare innovation status in different countries. According to the methodology of calculation of the index, the lowest possible evaluation for EU-25 group is 0 and the highest - 1 score.25 Number of employees working for the main employer.

the country, researchers working at businesses account for only 6.7%. According to this indicator Lithuania is at the bottom of the EU Member States ratings.

It is only one innovation performance indicator according to which Lithuania stands out positively among the EU Member States – cooperation by the country’s businesses in innovation activities as Lithuania is characterised by active interaction and cooperation among businesses in this area). According to this indicator Lithuania is on the 4th position among EU-25, exceeding the EU-25 average by as much as 34%.