eia energy conference panel session -crude exports · pdf fileeia energy conference panel...

TRANSCRIPT

EIA Energy ConferencePanel session - Crude exportsAlan GelderJune 2017

Trusted commercial intelligencewww.woodmac.com

Trusted commercial intelligencewww.woodmac.com

2

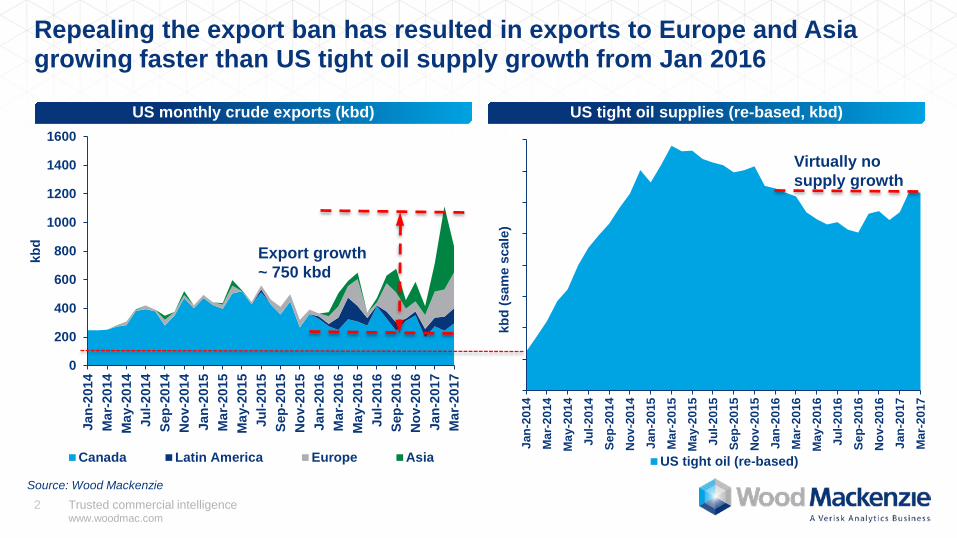

Repealing the export ban has resulted in exports to Europe and Asia growing faster than US tight oil supply growth from Jan 2016

US monthly crude exports (kbd) US tight oil supplies (re-based, kbd)

Source: Wood Mackenzie

0

200

400

600

800

1000

1200

1400

1600

Jan-

2014

Mar

-201

4M

ay-2

014

Jul-2

014

Sep-

2014

Nov

-201

4Ja

n-20

15M

ar-2

015

May

-201

5Ju

l-201

5Se

p-20

15N

ov-2

015

Jan-

2016

Mar

-201

6M

ay-2

016

Jul-2

016

Sep-

2016

Nov

-201

6Ja

n-20

17M

ar-2

017

kbd

Canada Latin America Europe Asia

Jan-

2014

Mar

-201

4M

ay-2

014

Jul-2

014

Sep-

2014

Nov

-201

4Ja

n-20

15M

ar-2

015

May

-201

5Ju

l-201

5Se

p-20

15N

ov-2

015

Jan-

2016

Mar

-201

6M

ay-2

016

Jul-2

016

Sep-

2016

Nov

-201

6Ja

n-20

17M

ar-2

017

kbd

(sam

e sc

ale)

US tight oil (re-based)

Export growth ~ 750 kbd

Virtually nosupply growth

Trusted commercial intelligencewww.woodmac.com

3

0123456789

Mill

ion

b/d

Vertical/Other HZ Wolfcamp/Bone SpringEagle Ford BakkenNiobrara Mid-Con

Source: Wood Mackenzie

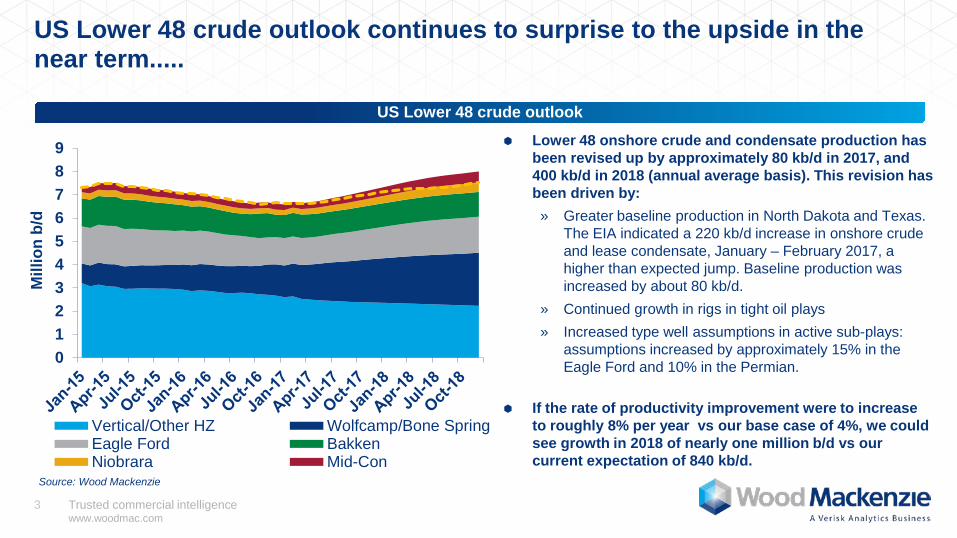

US Lower 48 crude outlook continues to surprise to the upside in the near term.....

Lower 48 onshore crude and condensate production has been revised up by approximately 80 kb/d in 2017, and 400 kb/d in 2018 (annual average basis). This revision has been driven by:» Greater baseline production in North Dakota and Texas.

The EIA indicated a 220 kb/d increase in onshore crude and lease condensate, January – February 2017, a higher than expected jump. Baseline production was increased by about 80 kb/d.

» Continued growth in rigs in tight oil plays» Increased type well assumptions in active sub-plays:

assumptions increased by approximately 15% in the Eagle Ford and 10% in the Permian.

If the rate of productivity improvement were to increase to roughly 8% per year vs our base case of 4%, we could see growth in 2018 of nearly one million b/d vs our current expectation of 840 kb/d.

US Lower 48 crude outlook

Trusted commercial intelligencewww.woodmac.com

4

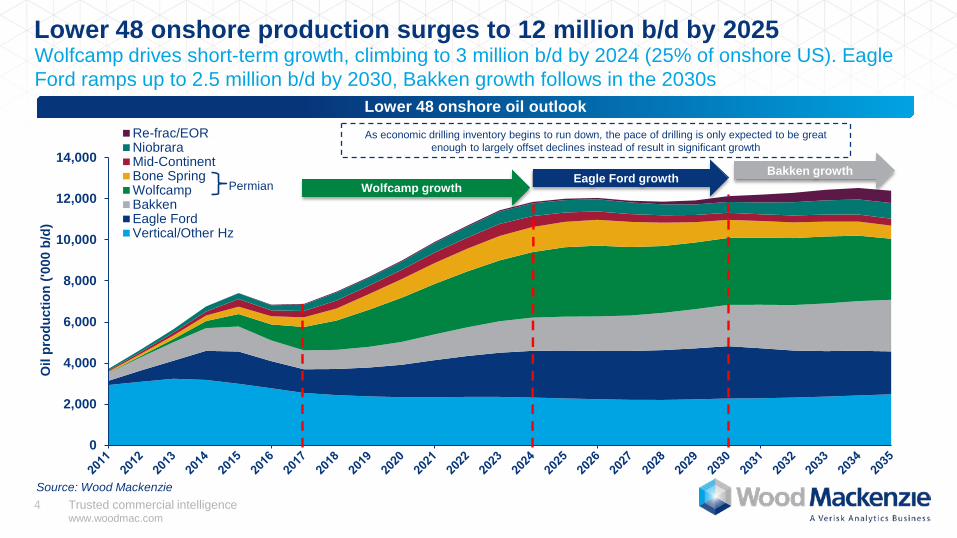

Lower 48 onshore production surges to 12 million b/d by 2025

Lower 48 onshore oil outlook

Wolfcamp drives short-term growth, climbing to 3 million b/d by 2024 (25% of onshore US). Eagle Ford ramps up to 2.5 million b/d by 2030, Bakken growth follows in the 2030s

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

Oil

prod

uctio

n ('0

00 b

/d)

Re-frac/EORNiobraraMid-ContinentBone SpringWolfcampBakkenEagle FordVertical/Other Hz

Permian

As economic drilling inventory begins to run down, the pace of drilling is only expected to be great enough to largely offset declines instead of result in significant growth

Wolfcamp growthEagle Ford growth Bakken growth

Source: Wood Mackenzie

Trusted commercial intelligencewww.woodmac.com

5

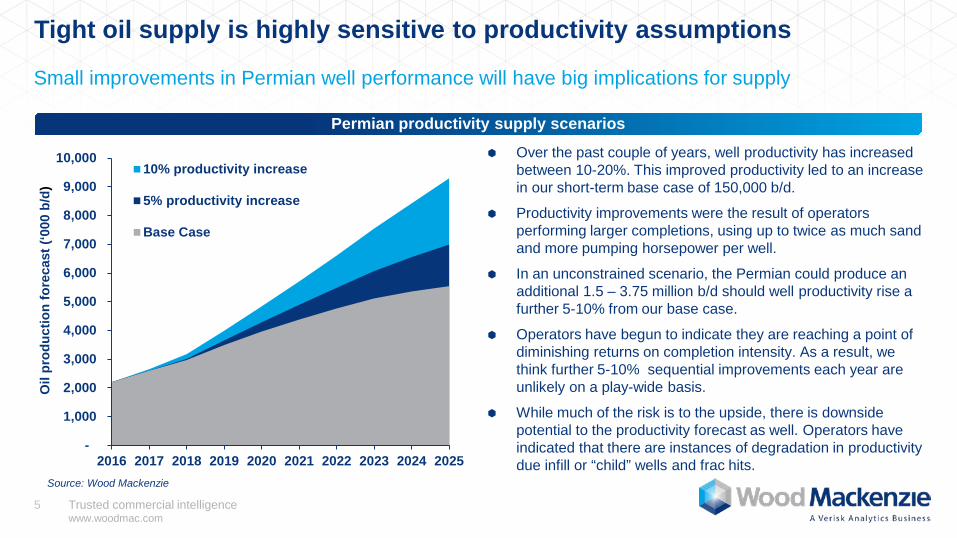

Tight oil supply is highly sensitive to productivity assumptions

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Oil

prod

uctio

n fo

reca

st (‘

000

b/d)

10% productivity increase

5% productivity increase

Base Case

Source: Wood Mackenzie

Over the past couple of years, well productivity has increased between 10-20%. This improved productivity led to an increase in our short-term base case of 150,000 b/d.

Productivity improvements were the result of operators performing larger completions, using up to twice as much sand and more pumping horsepower per well.

In an unconstrained scenario, the Permian could produce an additional 1.5 – 3.75 million b/d should well productivity rise a further 5-10% from our base case.

Operators have begun to indicate they are reaching a point of diminishing returns on completion intensity. As a result, we think further 5-10% sequential improvements each year are unlikely on a play-wide basis.

While much of the risk is to the upside, there is downside potential to the productivity forecast as well. Operators have indicated that there are instances of degradation in productivity due infill or “child” wells and frac hits.

Small improvements in Permian well performance will have big implications for supply

Permian productivity supply scenarios

Trusted commercial intelligencewww.woodmac.com

6

-

5.0

10.0

15.0

20.0

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025Heavy Medium Light

Growth in heavy Canadian oil supply outpaces declines in heavy Mexican oil supply; but crude slate gets lighterNorth American crude supply to get lighter due to US tight oil growth (excluding condensates)

North America crude oil supply outlook by quality (million bpd)

Source: Wood Mackenzie

Heavy Mexican oil production has declined for a decade while the Canadian oil sands surges ahead. We have not included the potential impact of on-going Mexican energy reform.

Note 1. < 28 API Heavy crudeNote 2. 28 – 38 API Medium crude Note 3. >38 – 51 API Light crude

Trusted commercial intelligencewww.woodmac.com

7

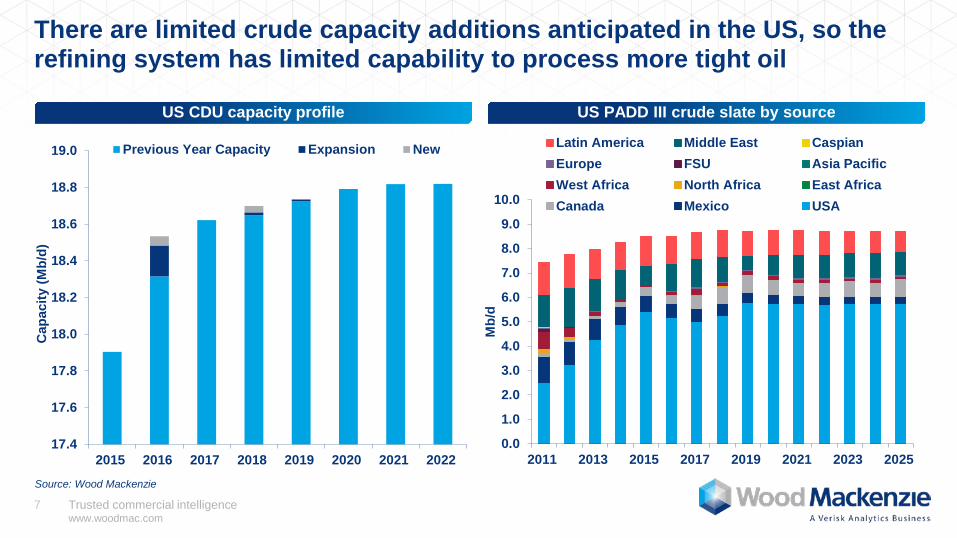

There are limited crude capacity additions anticipated in the US, so the refining system has limited capability to process more tight oil

US CDU capacity profile US PADD III crude slate by source

Source: Wood Mackenzie

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

2011 2013 2015 2017 2019 2021 2023 2025

Mb/

d

Latin America Middle East CaspianEurope FSU Asia PacificWest Africa North Africa East AfricaCanada Mexico USA

17.4

17.6

17.8

18.0

18.2

18.4

18.6

18.8

19.0

2015 2016 2017 2018 2019 2020 2021 2022

Cap

acity

(Mb/

d)

Previous Year Capacity Expansion New

Trusted commercial intelligencewww.woodmac.com

8

US crude export freights 2016 - 2035, $/bbl

IndiaUS

Europe

China/Korea

Canada

2015 Freight 2016-2025 Avg. Freight

$2.0/2.4

$2.8/3.5

$2.4/3.0$2.3/2.7

SuezmaxVLCC

Assuming a combination of Suezmax from Houston to Caribbean/Gulf of Mexico and then VLCC onwards after co-loading

To China/Korea

Assume a transit toll of $4.4/Ton for panama canal

Assume a transit toll of $2.2/Ton for Suez canal$1.1/1.3

US tight oil exports could hence be the order of 2 – 3 million bpd, targeting European and Asian marketsFreight costs to North Asia is double that of Europe due to longer freight distances. Export logistics infrastructure is key to facilitate the growing trade

Source: Wood Mackenzie

Trusted commercial intelligencewww.woodmac.com

9

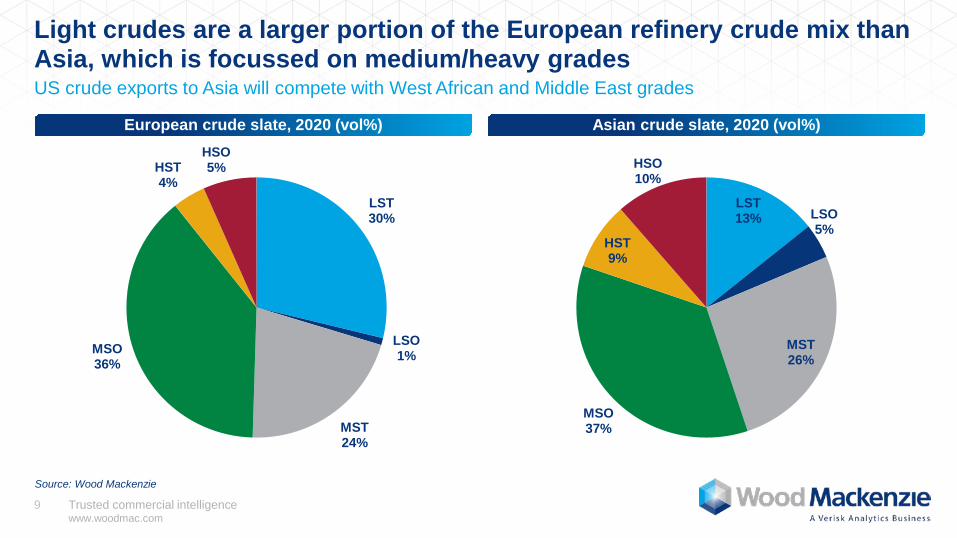

Light crudes are a larger portion of the European refinery crude mix than Asia, which is focussed on medium/heavy grades

European crude slate, 2020 (vol%) Asian crude slate, 2020 (vol%)

Source: Wood Mackenzie

LST30%

LSO1%

MST24%

MSO36%

HST4%

HSO5%

LST13% LSO

5%

MST26%

MSO37%

HST9%

HSO10%

US crude exports to Asia will compete with West African and Middle East grades

Trusted commercial intelligencewww.woodmac.com

10

European and Asian crude runs have different seasonality, suggesting crude export destinations will show such patterns

European crude runs (million bpd) Asian crude runs (million bpd)

20

22

24

26

28

30

32

Jan

Feb

Mar

Apr

May Jun

Jul

Aug Se

p

Oct

Nov Dec

Cru

de ru

ns (M

illio

n b/

d)

5 year range2016 20172018 5-yr avg

Source: History IEA MODS, APEC; Forecast Wood Mackenzie

10.0

10.5

11.0

11.5

12.0

12.5

13.0

13.5

14.0

Jan

Feb

Mar

Apr

May Jun

Jul

Aug Se

p

Oct

Nov Dec

Cru

de ru

ns (M

illio

n b/

d)

Series1 5 year range2016 20172018 5-yr avg

Source: History IEA MODS, Forecast Wood Mackenzie

Trusted commercial intelligencewww.woodmac.com

11

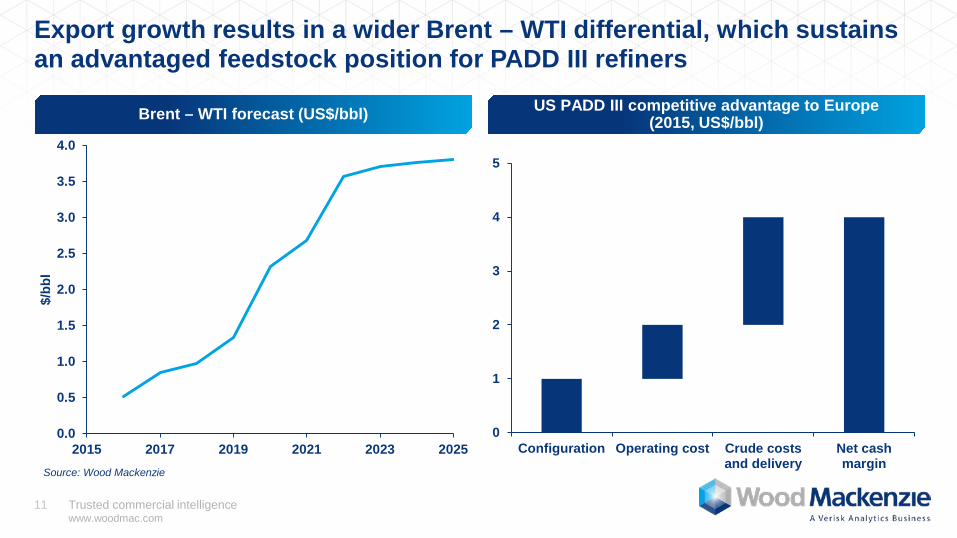

Export growth results in a wider Brent – WTI differential, which sustains an advantaged feedstock position for PADD III refiners

Brent – WTI forecast (US$/bbl) US PADD III competitive advantage to Europe(2015, US$/bbl)

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

2015 2017 2019 2021 2023 2025

$/bb

l

Source: Wood Mackenzie

0

1

2

3

4

5

Configuration Operating cost Crude costsand delivery

Net cashmargin

Trusted commercial intelligencewww.woodmac.com

12 Trusted commercial intelligencewww.woodmac.com

12

Conclusions

Key takeaways

US crude exports have grown strongly since the export ban was repealed and US tight oil supplies returned to growth

Further export growth is projected as:» US tight oil supply volumes double» Limited further investment in US refining anticipated

US crude exports will flow to both European and Asian refining centres, in significant volumes reflecting:

» Refining value of the crude» Seasonality» Freight and logistics costs

High quality export logistics are key to facilitate the future trade

Trusted commercial intelligencewww.woodmac.com

13

Disclaimer

This presentation has been prepared by Wood Mackenzie Limited. The presentation is intended solely for the benefit of attendees and its contents and conclusions are confidential and may not be disclosed to any other persons or companies without Wood Mackenzie’s prior written permission.

The information upon which this presentation comes from our own experience, knowledge and databases. The opinions expressed in this report are those of Wood Mackenzie. They have been arrived at following careful consideration and enquiry but we do not guarantee their fairness, completeness or accuracy. The opinions, as of this date, are subject to change. We do not accept any liability for your reliance upon them.

Strictly Private & Confidential

Wood Mackenzie™, a Verisk Analytics business, is a trusted source of commercial intelligence for the world'snatural resources sector. We empower clients to make better strategic decisions, providing objective analysisand advice on assets, companies and markets. For more information visit: www.woodmac.comWOOD MACKENZIE is a trade mark of Wood Mackenzie Limited and is the subject of trade mark registrations and/or applications inthe European Community, the USA and other countries around the world.

Europe +44 131 243 4400Americas +1 713 470 1600Asia Pacific +65 6518 0800

Email [email protected] www.woodmac.com