egyptian trade openness

TRANSCRIPT

1

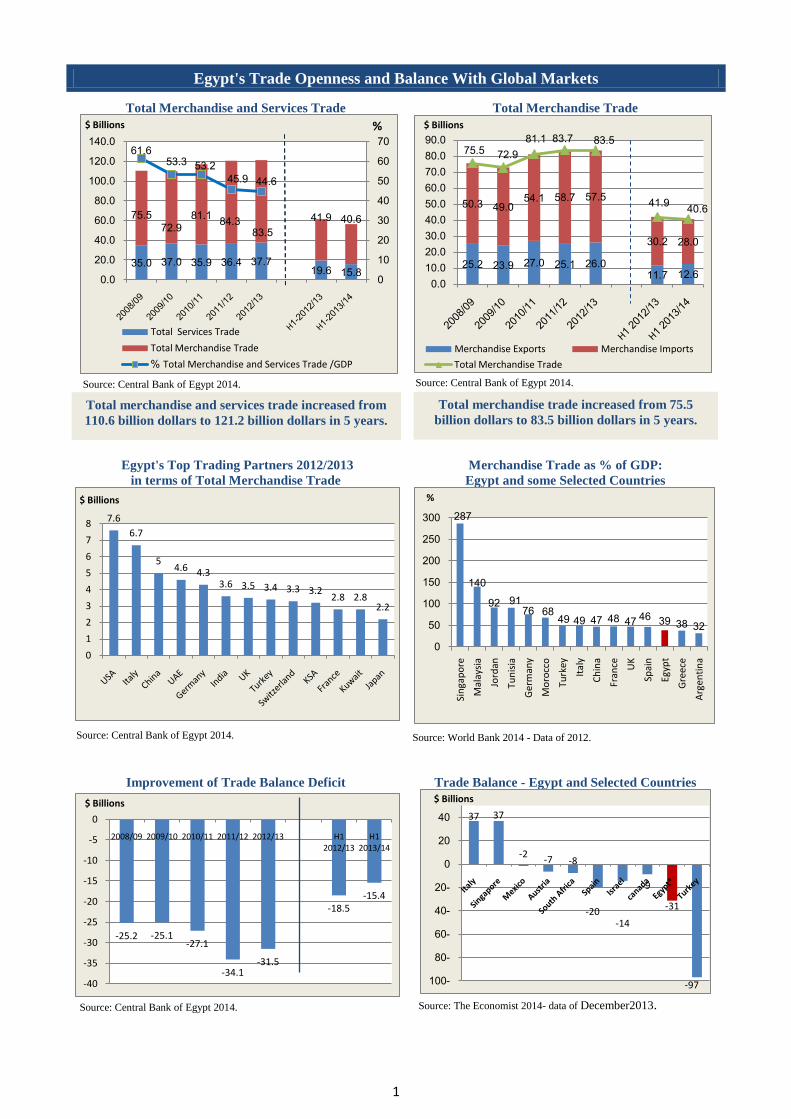

Egypt's Trade Openness and Balance With Global Markets

Total Merchandise and Services Trade

Source: Central Bank of Egypt 2014.

Total Merchandise Trade

Source: Central Bank of Egypt 2014.

Egypt's Top Trading Partners 2012/2013

in terms of Total Merchandise Trade

Source: Central Bank of Egypt 2014.

Merchandise Trade as % of GDP:

Egypt and some Selected Countries

Source: World Bank 2014 - Data of 2012.

Improvement of Trade Balance Deficit

Source: Central Bank of Egypt 2014.

Trade Balance - Egypt and Selected Countries

Source: The Economist 2014- data of December2013.

25.2 23.9 27.0 25.1 26.011.7 12.6

50.3 49.054.1 58.7 57.5

30.2 28.0

75.5 72.9

81.1 83.7 83.5

41.940.6

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

90.0

$ Billions

Merchandise Exports Merchandise Imports

Total Merchandise Trade

7.6

6.7

54.6 4.3

3.6 3.5 3.4 3.3 3.22.8 2.8

2.2

0

1

2

3

4

5

6

7

8

$ Billions

287

140

92 9176 68

49 49 47 48 47 46 39 38 32

0

50

100

150

200

250

300

Sin

gap

ore

Mal

aysi

a

Jord

an

Tun

isia

Ger

man

y

Mo

rocc

o

Turk

ey

Ital

y

Ch

ina

Fran

ce UK

Spai

n

Egyp

t

Gre

ece

Arg

enti

na

%

-25.2 -25.1-27.1

-34.1-31.5

-18.5-15.4

-40

-35

-30

-25

-20

-15

-10

-5

0

2008/09 2009/10 2010/11 2011/12 2012/13 H1 2012/13

H1 2013/14

$ Billions37 37

-2-7 -8

-20-14

-9

-31

-97-100

-80

-60

-40

-20

0

20

40

$ Billions

Total merchandise and services trade increased from

110.6 billion dollars to 121.2 billion dollars in 5 years.

Total merchandise trade increased from 75.5

billion dollars to 83.5 billion dollars in 5 years.

35.0 37.0 35.9 36.4 37.719.6 15.8

75.5

72.981.1

84.383.5

41.9 40.6

61.653.3 53.2

45.9 44.6

0

10

20

30

40

50

60

70

0.0

20.0

40.0

60.0

80.0

100.0

120.0

140.0

$ Billions %

Total Services Trade

Total Merchandise Trade

Total Merchandise and Services Trade /GDP %

2

Total Merchandise Trade1

Exports Imports

Non-Petroleum Exports Share to Total Exports

increased to 54% in 2012/2013

Decline in Total Imports by 2.9% in 2012/2013

Industrial Exports constitute about 48%

of Total Exports

Merchandise Imports Feed Production Process

rather than Consumption

EU, Arab and Asian Countries comprise 75% of Egypt's Total

Exports Destinations.

Egypt's Exports to Arab Countries increased from 15% to

20% in 5 years.

Egypt’s Imports from Europe, Asia and Arab Countries

constitute 81% of total Imports.

Egypt Imports from Arab Countries doubled in 5 years.

1 Source: Central Bank of Egypt- 2014.

11 10.3 12.1 13.1 12.04.7 6.0

14.2 13.6 14.9 13.8 14.0

7.0 6.5

25.2 23.927.0

25.1 26.0

11.7 12.6

0

5

10

15

20

25

30

2008/09 2009/10 2010/11 2011/12 2012/13 H1 2012/13

H1 2013/14

$ Billions

Petroleum Exports Non-Petroleum Exports

Total Exports

7.0 5.29.3 11.8 12.5

6.7 5.9

43.3 43.8 44.8 47.4 45.0

23.5 22.1

50.3 49.054.1

58.7 57.5

30.2 28.0

0.0

20.0

40.0

60.0

80.0

2008/09 2009/10 2010/11 2011/12 2012/13 H1

2012/13

H1

2013/14

$ Billions

Petroleum Imports Non-Petroleum Imports

Total Imports

Fuels, Minerals Oil &

Products47%

Raw Maretials5%

Semi-finished Commodities

8%

Finished Commodities

40%

Egyptian Exports, by degree of manufacturing 2012/2013

Fuels, Minerals Oil &

Products16.50%

Raw Materials15%

Intermediate Goods

28%

Investment Goods

17%

Consumer Goods22.50%

Undistributed Commodities

1%

Egyptian Imports, by degree of use 2012/2013

EU37%

Other Europian Countries

7%

Russian Federation

1%USA

14%

Arab Countries

20%

Asian Countries (excluding

Arab Countries)

18%

African Countries (excluding

Arab Countries)

2%

Other Countries &

Regions2%

Geographic Distribution of Egyptian Exports 2012/2013

EU31%

Other European Countries

9%

Russian Federation

3.50%USA7%

Arab Countries

20%

Asian Countries (excluding

Arab Countries)

21%

Other Countries &

Regions9%

Geographic Distribution of Egyptian Imports 2012/2013

In H1 2013/14, Egypt’s Merchandise Exports

increased by 7.5% In H1 2013/14, Egypt’s Merchandise Imports

declined by 7.4%

3

44

67

80

9893

110

131 133

147

44

67.4

80

100

120130

145

2030405060708090

100110120130140150160

2005 2006 2007 2008 2009 2010 2011 2012 2013

L.E

Bill

ion

Actual Exports Represent 102% of Planned Exports in 2013

actual planned

2010: Start of the Plan

2005: establishingExport Councils

2013: End of the Plan

Building Materials22%

Chemicals & Fertilizers

20%Food Industry

13%

Engineering & Electronics

10%

Fresh (Agro) Products

9%

Ready-made Garments

7%

Others19%

Structure of Export Councils as at end of 2013

Positive Impact of Export Promotion Strategy (2010-2013)2

2 Source: General Organization for Export and Import Control (GOEIC), Foreign Trade Data Warehouse - 2014.

0.0

20.0

40.035% 60%

81%40% 20%

32% 132% 61% 77% 46% 59% 72%

L.E

Bill

ion

All Export Councils Witnessed Significant Growth Rates

2009 (Start of Export Plan) 2013(End of Export Plan)

Almost 60% increase

in total Councils'

exports by the end of

the Plan (2013)

compared to prior of

the Plan (2009).

Leading Export Councils that exceeded Actual vs. Planned in 2013: Spinning and Weaving Council: 180%, Home -Wear Council: 151%, Food Industry Council: 131%, Building Materials Council: 118%, and Fresh (Agro) Products Council: 108%.

Six Export Councils represent

81% of the Egyptian exports

at end of 2013.

Greater impact of the Plan on some sectors

e.g. Spinning & Weaving, Food

Industry, Pharmaceuticals,

Home-wear, Chemicals &

Fertilizers, and others.

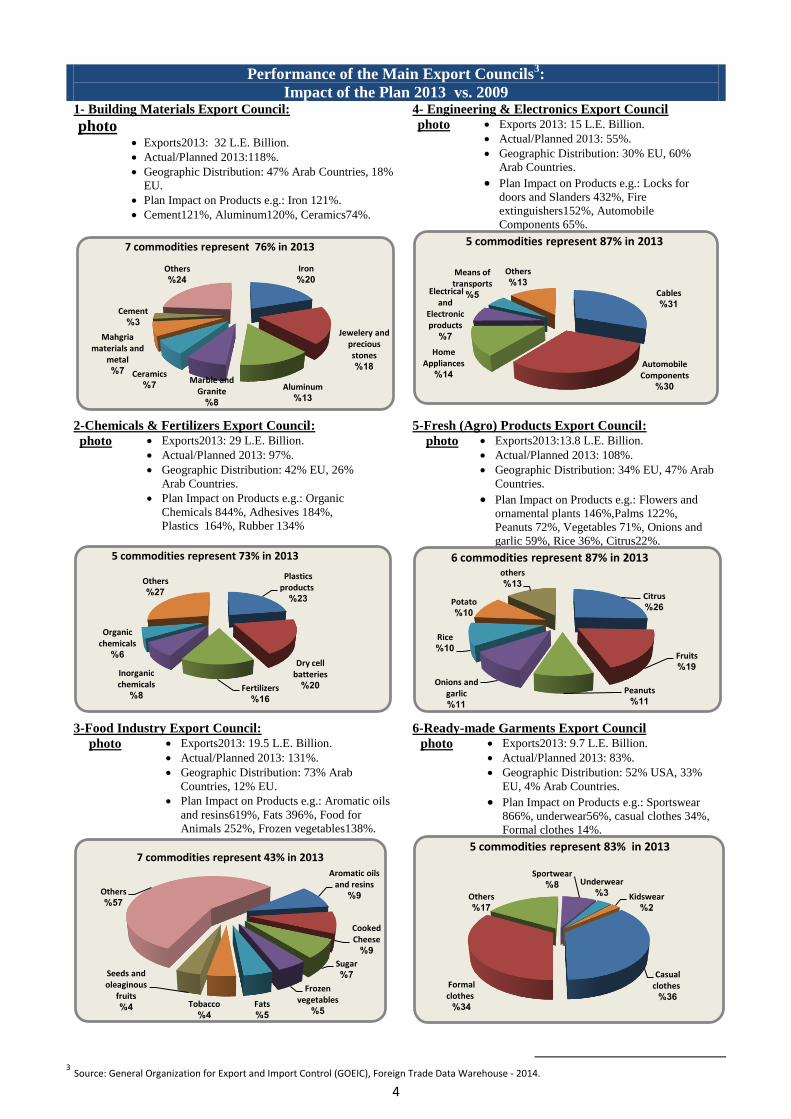

4

Performance of the Main Export Councils3:

Impact of the Plan 2013 vs. 2009 1- Building Materials Export Council:

photo Exports2013: 32 L.E. Billion.

Actual/Planned 2013:118%.

Geographic Distribution: 47% Arab Countries, 18%

EU.

Plan Impact on Products e.g.: Iron 121%.

Cement121%, Aluminum120%, Ceramics74%.

4- Engineering & Electronics Export Council Exports 2013: 15 L.E. Billion.

Actual/Planned 2013: 55%.

Geographic Distribution: 30% EU, 60%

Arab Countries.

Plan Impact on Products e.g.: Locks for

doors and Slanders 432%, Fire

extinguishers152%, Automobile

Components 65%.

photo

2-Chemicals & Fertilizers Export Council: Exports2013: 29 L.E. Billion.

Actual/Planned 2013: 97%.

Geographic Distribution: 42% EU, 26%

Arab Countries.

Plan Impact on Products e.g.: Organic

Chemicals 844%, Adhesives 184%,

Plastics 164%, Rubber 134%

photo

5-Fresh (Agro) Products Export Council:

photo

Exports2013:13.8 L.E. Billion.

Actual/Planned 2013: 108%.

Geographic Distribution: 34% EU, 47% Arab

Countries.

Plan Impact on Products e.g.: Flowers and

ornamental plants 146%,Palms 122%,

Peanuts 72%, Vegetables 71%, Onions and

garlic 59%, Rice 36%, Citrus22%.

3-Food Industry Export Council:

Exports2013: 19.5 L.E. Billion.

Actual/Planned 2013: 131%.

Geographic Distribution: 73% Arab

Countries, 12% EU.

Plan Impact on Products e.g.: Aromatic oils

and resins619%, Fats 396%, Food for

Animals 252%, Frozen vegetables138%.

photo

6-Ready-made Garments Export Council Exports2013: 9.7 L.E. Billion.

Actual/Planned 2013: 83%.

Geographic Distribution: 52% USA, 33%

EU, 4% Arab Countries.

Plan Impact on Products e.g.: Sportswear

866%, underwear56%, casual clothes 34%,

Formal clothes 14%.

photo

3 Source: General Organization for Export and Import Control (GOEIC), Foreign Trade Data Warehouse - 2014.

Iron20%

Jewelery and precious stones

18%

Aluminum13%

Marble and Granite

8%

Ceramics7%

Mahgria materials and

metal7%

Cement3%

Others24%

7 commodities represent 76% in 2013

Cables31%

Automobile Components

30%

Home Appliances

14%

Electrical and

Electronic products

7%

Means of transports

5%

Others13%

5 commodities represent 87% in 2013

Plastics products

23%

Dry cell batteries

20%Fertilizers16%

Inorganic chemicals

8%

Organic chemicals

6%

Others27%

5 commodities represent 73% in 2013

Citrus26%

Fruits19%

Peanuts11%

Onions and garlic

11%

Rice10%

Potato10%

others13%

6 commodities represent 87% in 2013

Aromatic oils and resins

9%

Cooked Cheese

9%

Sugar7%

Frozen vegetables

5%Fats

5%

Tobacco4%

Seeds and oleaginous

fruits4%

Others57%

7 commodities represent 43% in 2013

Casual clothes

36%

Formal clothes

34%

Others17%

Sportwear8% Underwear

3% Kidswear2%

5 commodities represent 83% in 2013

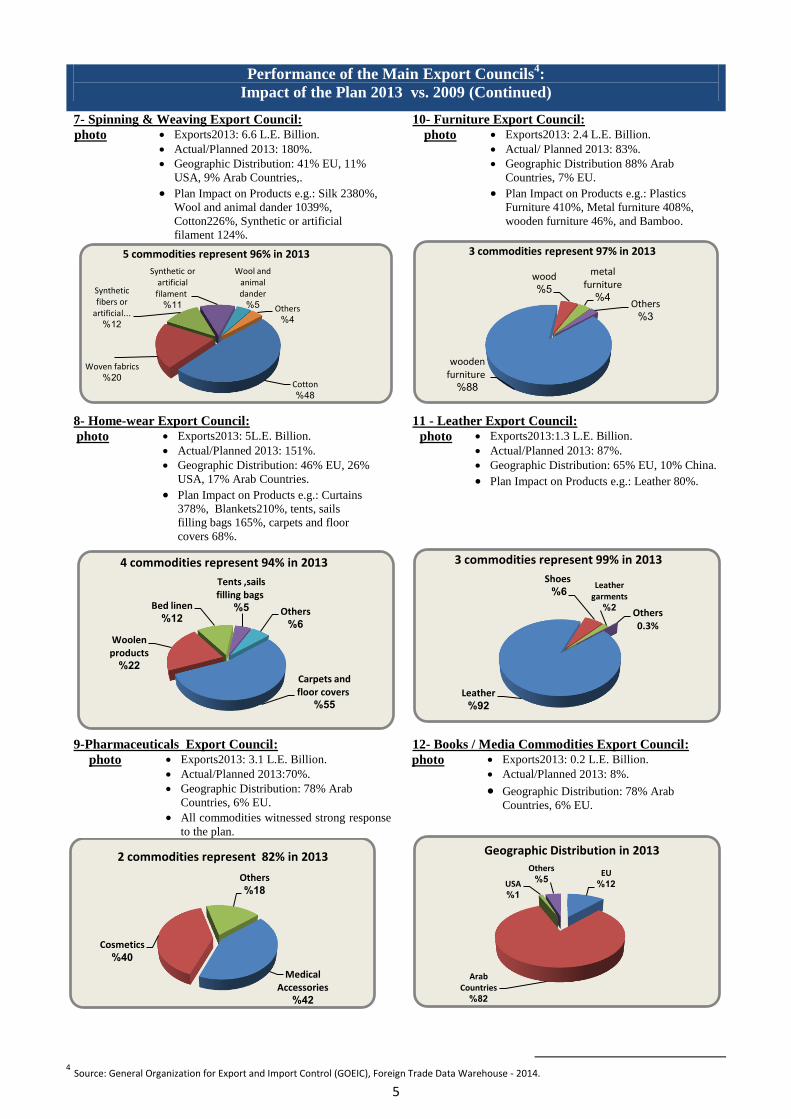

5

Performance of the Main Export Councils4:

Impact of the Plan 2013 vs. 2009 (Continued)

7- Spinning & Weaving Export Council: Exports2013: 6.6 L.E. Billion.

Actual/Planned 2013: 180%.

Geographic Distribution: 41% EU, 11%

USA, 9% Arab Countries,.

Plan Impact on Products e.g.: Silk 2380%,

Wool and animal dander 1039%,

Cotton226%, Synthetic or artificial

filament 124%.

photo

10- Furniture Export Council: Exports2013: 2.4 L.E. Billion.

Actual/ Planned 2013: 83%.

Geographic Distribution 88% Arab

Countries, 7% EU.

Plan Impact on Products e.g.: Plastics

Furniture 410%, Metal furniture 408%,

wooden furniture 46%, and Bamboo.

photo

8- Home-wear Export Council: Exports2013: 5L.E. Billion.

Actual/Planned 2013: 151%.

Geographic Distribution: 46% EU, 26%

USA, 17% Arab Countries.

Plan Impact on Products e.g.: Curtains

378%, Blankets210%, tents, sails

filling bags 165%, carpets and floor

covers 68%.

photo

11 - Leather Export Council: Exports2013:1.3 L.E. Billion.

Actual/Planned 2013: 87%.

Geographic Distribution: 65% EU, 10% China.

Plan Impact on Products e.g.: Leather 80%.

photo

9-Pharmaceuticals Export Council: Exports2013: 3.1 L.E. Billion.

Actual/Planned 2013:70%.

Geographic Distribution: 78% Arab

Countries, 6% EU.

All commodities witnessed strong response

to the plan.

photo

12- Books / Media Commodities Export Council: Exports2013: 0.2 L.E. Billion.

Actual/Planned 2013: 8%.

Geographic Distribution: 78% Arab

Countries, 6% EU.

photo

4 Source: General Organization for Export and Import Control (GOEIC), Foreign Trade Data Warehouse - 2014.

Cotton48%

Woven fabrics20%

Synthetic fibers or

artificial...12%

Synthetic or artificial filament

11%

Wool and animal dander

5% Others4%

5 commodities represent 96% in 2013

wooden furniture

88%

wood5%

metal furniture

4%Others

3%

3 commodities represent 97% in 2013

Carpets and floor covers

55%

Woolen products

22%

Bed linen12%

Tents ,sails filling bags

5% Others6%

4 commodities represent 94% in 2013

Leather92%

Shoes 6%

Leather garments

2%Others0.3%

3 commodities represent 99% in 2013

Medical Accessories

42%

Cosmetics40%

Others18%

2 commodities represent 82% in 2013EU12%

Arab Countries

82%

USA1%

Others5%

Geographic Distribution in 2013

6

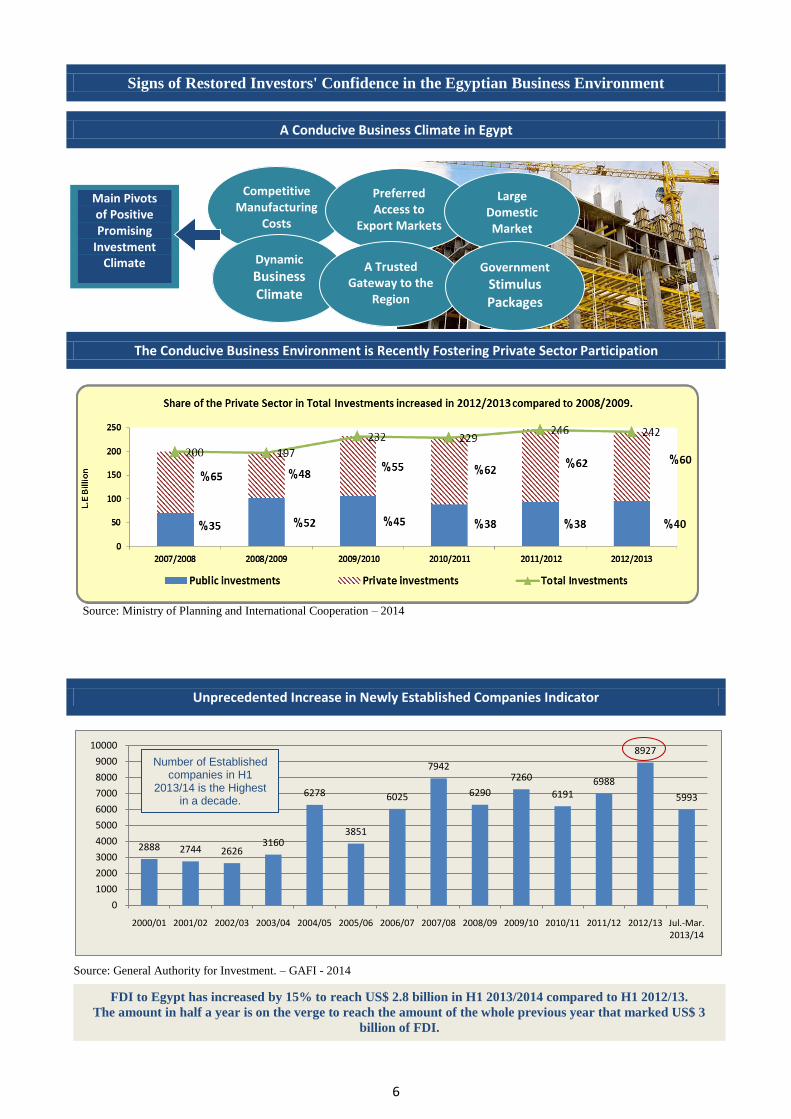

Signs of Restored Investors' Confidence in the Egyptian Business Environment

A Conducive Business Climate in Egypt

The Conducive Business Environment is Recently Fostering Private Sector Participation

Source: Ministry of Planning and International Cooperation – 2014

Unprecedented Increase in Newly Established Companies Indicator

Source: General Authority for Investment. – GAFI - 2014

2888 2744 26263160

6278

3851

6025

7942

6290

7260

61916988

8927

5993

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

10000

2000/01 2001/02 2002/03 2003/04 2004/05 2005/06 2006/07 2007/08 2008/09 2009/10 2010/11 2011/12 2012/13 Jul.-Mar. 2013/14

Main Pivots of Positive Promising

Investment Climate

Competitive Manufacturing

Costs

Preferred Access to

Export Markets

Large Domestic

Market

Dynamic Business Climate

A Trusted Gateway to the

Region

Government Stimulus Packages

Number of Established companies in H1

2013/14 is the Highest in a decade.

FDI to Egypt has increased by 15% to reach US$ 2.8 billion in H1 2013/2014 compared to H1 2012/13.

The amount in half a year is on the verge to reach the amount of the whole previous year that marked US$ 3

billion of FDI.

7

Recent Multinationals Investments amidst Transitional Stage illustrating Greater Investors' Confidence

The following are examples of recently signed contracts and pledges of some multinational investments, underscoring

the success of strides carried out by the Government, and the importance of Egypt as an international and regional hub

for foreign investors.

Samsung

Electronics to

establish the first

phase of its new

project is in Beni

Swief, amounting to 1.7 L.E. billion.

The total investments in all stages of

the project is 9 L.E. billion almost

1.5 US$ billion.

Nestlé Egypt,

a subsidiary of

Nestlé Switzerland, has

inaugurated a

new distribution centre in Luxor;

to meet potential growth in Upper

Egypt area. This would increase

employment in Upper Egypt office

by 50%.

A signed

Cooperation

agreement

between Carbon

holding Co. and

Italian Maire

Tecnimont Italian Group, and

German Archirodon Company Ltd.

Investments amount to 1.7 Billion,

with expected 23 thousands job

opportunities.

United Arab Emirates Al-Futtaim real

estate group, has invested L.E. 7

billion in the first phase of Cairo

Festival City project. It will invest

L.E. 12 billion to

implement the second

and third phases, with

around 30,000 expected

job opportunities. Also,

Al-Futtaim retail group plans to

establish five commercial malls in

Egypt over the next five years.

Morpho S.A. a French

multinational company of

Safran revealed that it

is planning to

invest L.E. 500

million in

Egypt within the current fiscal

year, with possible further

expansions in the future due to

high potentiality of the

Egyptian market.

As part of its

investment,

Coca-Cola pledges US$

500 million

in Egypt. Its total number of

employees in Egypt amounted to

12000 Egyptians. The company also

plans to refurbish 100 rural villages

by 2020 under the Egypt livelihood

community programme.

Some Highlights on Business Environment Recent Development

GOE pledged to resolving legal disputes with investors as a priority, sending a positive message to all "honest

investors", either Egyptians, Arabs or foreigners. In accordance, indicators show that 43% of disputes resolved.

The issuance of the new Egyptian law preventing Third Parties from challenging contracts made between

Government and an investor has had positive effect on restoring credibility and confidence in the business

environment in Egypt.

The recent repayment of delayed arrears by the government to private sector companies has given a boost to further

confident market operations.

The Central Bank of Egypt revision of foreign repatriation of dividends has had a significant impact.

The re-adoption of “ERADA” initiative to review streamline Egyptian legislative climate is a pivotal core of the

public private consultation and crucial process.

The New Urban Communities Authority’s board of directors has approved the leasing of industrial land on a

usufruct basis for 30 years to overcome land allocation hindrance and to foster industrial growth and development.

During the Initial Public Offerings (IPO) Summit, it was announced that by the beginning of 2015, the infrastructure

work in the Suez Canal Axis Development national project will be issued to international companies on a usufruct

basis for 25 years.

International Recognition of Growth Potentials in Egypt

Regarding recent developments in Egypt

"Business confidence is recovering, but the

economic situation remains troubled….

Financial conditions have eased."….Projections

of "GDP Growth in 2014/2015 is 4.1 percent".

"Egypt’s GDP growth rate is predicted

to increase in 2015.. it would be the

highest since 2010 (about 5.1%), but is

still much lower than Egypt’s potential

or pre-revolutionary growth rates."

"GOE has continued to recognize

that business and investment climate is crucial

to realizing Egypt’s potential, and has

remained committed to a process of reform".

BC Review of Egypt – 2014.

“Compared with other emerging

markets, foreign firms, though wary,

have not abandoned Egypt. … A Bank is

scouting for opportunities to expand,

even as the bank scales back from

nearby countries”.

8

Prospects of Recovery of Industrial Indicators

Source: Ministry of Planning, 2014 - Includes the manufacturing sector and oil refining.

Towards a Balanced Regional Industrial Development5

Industrial Strategies Sustainable Initiatives

5 Source: Industrial Development Authority IDA - 2014.

8

4.25.3

0.9 0.7

2.3

0123456789

2007/08 2008/09 2009/10 2010/11 2011/12 2012/13

%

Industrial Real Growth Rate Increased to 2.3% in 2012/2013 compared to 0.7% in 2011/2012

139164.5

194.3216.2

238.3262.5

120.9 123.2

0

50

100

150

200

250

300

L.E

Bill

ion

s

Industrial GDP increased by 21.4% in post compared to before Revolution

Post RevolutionBefore Revolution

42.3

29.725.5 23.8 22.5 25.1

13.617.4

0

10

20

30

40

50

2007/08 2008/09 2009/10 2010/11 2011/12 2012/13 H1 2012/13

H1 2013/14

L.E

Bill

ion

s

Despite Political/ Economic Turmoil in Egypt: Industrial Investments increased by 5.5% in 2012/2013 compared to 2010/2011

Before Revolution Post Revolution

21%

21%8%6%

13%

7%

2%

19% 2% 1%

Sectoral Structure of Manufacturing Entities

Food and drinks Textile and leatherWood Paper and its productsBasic chemicals Building materialsBasic metal Engineering and electronicManufacturing Other

27%

12%

11%10%

8%

7%

7%

5%

3% 3% 7%

Geographic Structure of Manufacturing Entities

Cairo Al-Sharqia Qalyubia Giza

Alex Gharbia Upper Egypt Dakahlia

Monufia Damietta Other

In H1 2013/14 the

proportion of the

manufacturing investment

increased to 98% of the

total industrial investment

compared to 62% in H1

2012/13

Sign of Recovery

New Generation

of Industrial

Zones

Availability

of Industrial

Lands

Egypt

Investment Map

E- Services

Industrial

Clusters

Specialized

Industrial Units

for SMEs

Excellence

Centre for

Prototyping &

Modeling

Industrial

Zones

Procedures

Simplification

Local

Manufacturing

Main Pillars

There are around 35,000 formally registered industrial establishments with investments of LE 622

billion, employing nearly 2 million workers. (Cumulative till mid 2014).

9

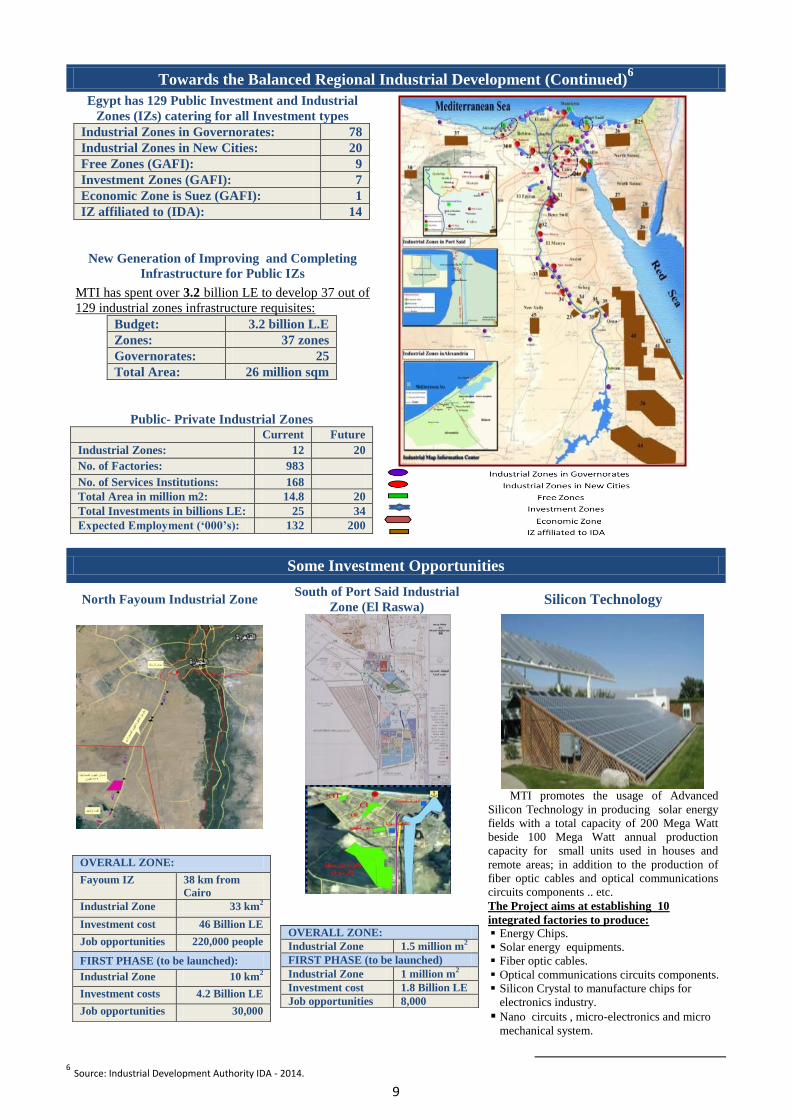

Towards the Balanced Regional Industrial Development (Continued)6

Egypt has 129 Public Investment and Industrial

Zones (IZs) catering for all Investment types

Industrial Zones in Governorates: 78

Industrial Zones in New Cities: 20

Free Zones (GAFI): 9

Investment Zones (GAFI): 7

Economic Zone is Suez (GAFI): 1

IZ affiliated to (IDA): 14

New Generation of Improving and Completing

Infrastructure for Public IZs

MTI has spent over 3.2 billion LE to develop 37 out of

129 industrial zones infrastructure requisites:

Budget: 3.2 billion L.E

Zones: 37 zones

Governorates: 25

Total Area: 26 million sqm

Public- Private Industrial Zones Current Future

Industrial Zones: 12 20

No. of Factories: 983

No. of Services Institutions: 168

Total Area in million m2: 14.8 20

Total Investments in billions LE: 25 34

Expected Employment (‘000’s): 132 200

Some Investment Opportunities

North Fayoum Industrial Zone South of Port Said Industrial

Zone (El Raswa) Silicon Technology

[

OVERALL ZONE:

Fayoum IZ 38 km from

Cairo

Industrial Zone 33 km2

Investment cost 46 Billion LE

Job opportunities 220,000 people

FIRST PHASE (to be launched):

Industrial Zone 10 km2

Investment costs 4.2 Billion LE

Job opportunities 30,000

OVERALL ZONE:

Industrial Zone 1.5 million m2

FIRST PHASE (to be launched)

Industrial Zone 1 million m2

Investment cost 1.8 Billion LE

Job opportunities 8,000

MTI promotes the usage of Advanced

Silicon Technology in producing solar energy

fields with a total capacity of 200 Mega Watt

beside 100 Mega Watt annual production

capacity for small units used in houses and

remote areas; in addition to the production of

fiber optic cables and optical communications

circuits components .. etc.

The Project aims at establishing 10

integrated factories to produce:

Energy Chips.

Solar energy equipments.

Fiber optic cables.

Optical communications circuits components.

Silicon Crystal to manufacture chips for

electronics industry.

Nano circuits , micro-electronics and micro

mechanical system.

6 Source: Industrial Development Authority IDA - 2014.

10

Enhanced Modern Industrialization Programs to Foster Competitiveness7

Main Programs in collaboration with Stakeholders:

( Ministries, Private Sector Federations, International Institutions and others)

National Policy Support

Program:

IMC Enterprise Development

Program:

Energy Efficiency &

Environment Protection

Program:

Access to Finance

Program:

Developing strategies and

studies to create a jump shift

in the performance of the

different sectors and

generate a positive impact

on the industry at large,

with the Industrial

Chambers at FEI.

Sectors: Textile and Ready

Made Garments, Food

Processing, Leather

Industries, and Agriculture

Industries and others.

Work to institutional

Capacity Building through:

- Management Support.

- Organizational

Restructuring & Re-

engineering.

- Technological Support.

- Laboratories Upgrade.

Targeting eligible enterprises in

14 different industrial sectors on

individual basis and 19 branches

distributed geographically all

over Egypt.

Services :

1. Management.

2. Marketing / Export Promotion.

3. Human Resources.

4. Finance and Financial Services.

5. Production.

6. Quality.

7. Information Technology and

Management Information System

(MIS).

8. Energy Saving & Environmental

Protection.

9. Corporate Sustainability and

Social Responsibility.

10. Governance.

11. Technology and Know-How

Transfer.

12. Training (vocational and

technical courses).

This program aims at

reducing the specific

energy consumption per

product unit without any

negative impact on the

product quality or quantity.

Raising of Energy

Efficiency awareness.

Promoting direct uses

renewable and solar

energy.

Services:

1- Preliminary Energy Audits

2- Energy Efficiency/

Technical Assistance

Service.

3. Energy Management

Systems (Planned) in

accordance to ISO Criteria

4. Environment Services.

5. Human Capacity Building

and Training.

Coordination with

financial institutions

to qualifying

companies for Access

to Finance.

Funding for

Development

Program:

1. Banking operations.

2. Finance Leasing

3. Credit guarantees

Program (whereby CGC

would guarantee the

repayment by the

beneficiary client with

maximum 75% of the

loan provided by the

banks).

4. Private Equity Funds

5. Stock Exchange for

Small and Medium

Enterprises (NILEX)

support of 50% of

enlisting costs.

National Quality Awareness

Program:

Egyptian Corporate Responsibility

Center (ECRC):

Enhancing IT Implementation in

Industrial Companies :

Aims to dialog among all

stakeholders in the process of

adjusting the Egyptian conformity

assessment infrastructure and

modernizing the industry through

optimizing:

Concepts and principles of quality.

Cost of quality.

Customer relation.

Continuous Improvement.

Promote awareness for effective

corporate social responsibility.

Develop CSR codes and guidelines.

Build the capacities by delivering

internationally accredited training

programs.

Policy advocacy and knowledge

center.

Assist the companies to comply with

labor and environmental standards by

enhancing transparency.

Providing vertical solutions enabling the

managers and the executives to better utilize

the information system. Also reaching out to

SMEs seeking to automate their businesses.

Services:

1. Basic manufacturing Applications.

2. Advanced Manufacturing Application.

3. Sector Projects.

4. Customer Relationship Management

System (CRM).

7 Source: Industrial Modernization Center - 2014.

11

Main KPIs of Industrial/ Creative Clusters:

Activity Creative Industrial

Artisan 690 142

Cluster 9 6

Workshops' 173 74

55%

20%

14%

8%3%

The Sectoral Structure of Services

Greater Cairo Delta Alexandria Upper Egypt Canal

17%

9%

16%

6%16%

14%

8%

2%4% 4% 4% 0.2%

The Sectoral Structure of Services

Textile Industry Services Food

Furniture Engineering Chemicals

Constructions Leather Agro

Creative Industries' Clusters Map

Industrial Clusters Program:

Objective: Strengthen and expand SMEs development

of value chain industrial cluster products on integrated

demand based approach.

Sectors: Furniture, Stones & Marbles, Food and Agro

Business.

Thus, generating higher aggregate value added and

more inclusive socio-economic opportunities.

Governorates: Siwa – Upper Egypt – Sinai – Damietta

– Shak Elteaban – Others.

Creative Industries' Clusters Program:

As important source of sustainable income in cultural

heritage of crafts.

Objective: Integrate creative IC into national and

international supply chains through naturally

geographic formed clusters.

Sectors: Textile, Leather, Alabaster, Pottery,

Metalwork, and Glass.

Technical Assistant Services Offered: Technical

Knowhow and Production- Capacity Building-

Design- Quality Upgrading Services- Export

Promotion and Marketing.

Value Chain Development Program: Targeted (5) sectors: Chemicals, food and Agro, Engineering,

Business Sector, Leather, Textile.

This is achieved by boosting vertical integration, improving

SMEs business linkages, creating a domestic supplier base for

the local and global industry leaders and enhancing the

competitiveness of the Egyptian feeding industries.

High potential Enterprise (Tiger Program):

Target sectors: Chemicals, food and Agro, Engineering.

Eligibility targeting high potential medium enterprises in the

food & Agro, Chemical and Engineering Industrial sectors

with annual turnover from 20 to 50 million LE.

The Selected companies will participate in a business

development path (Graduation Process) starting from

technology enhancement, productivity improvement towards,

competitiveness. A path that will graduate them into large

enterprise that can compete o a global level.

Average Operation Achieved 90%.

Upper Egypt and Sinai – Incentive Package:

Upper Egypt, Sinai, Suez, New valley.

Reduce the company’s contribution of the cost of

business development services by 50%.

free technical service in the first year for new plants

(phases during preproduction or start period)

Non –Performing Enterprise Program:

Total Number of Applications received: 900

Eliminated (either due public sector. legal issues, other

reasons): 496

cases Processed: 404 ( coordinated with banks, SFD,

and others, for financial and technical support)

To face economic challenges to help potential series

enterprise, with relevant concerned parties.

Aim to re-boost companies to re-operate with high

production, employment and competitiveness.

12

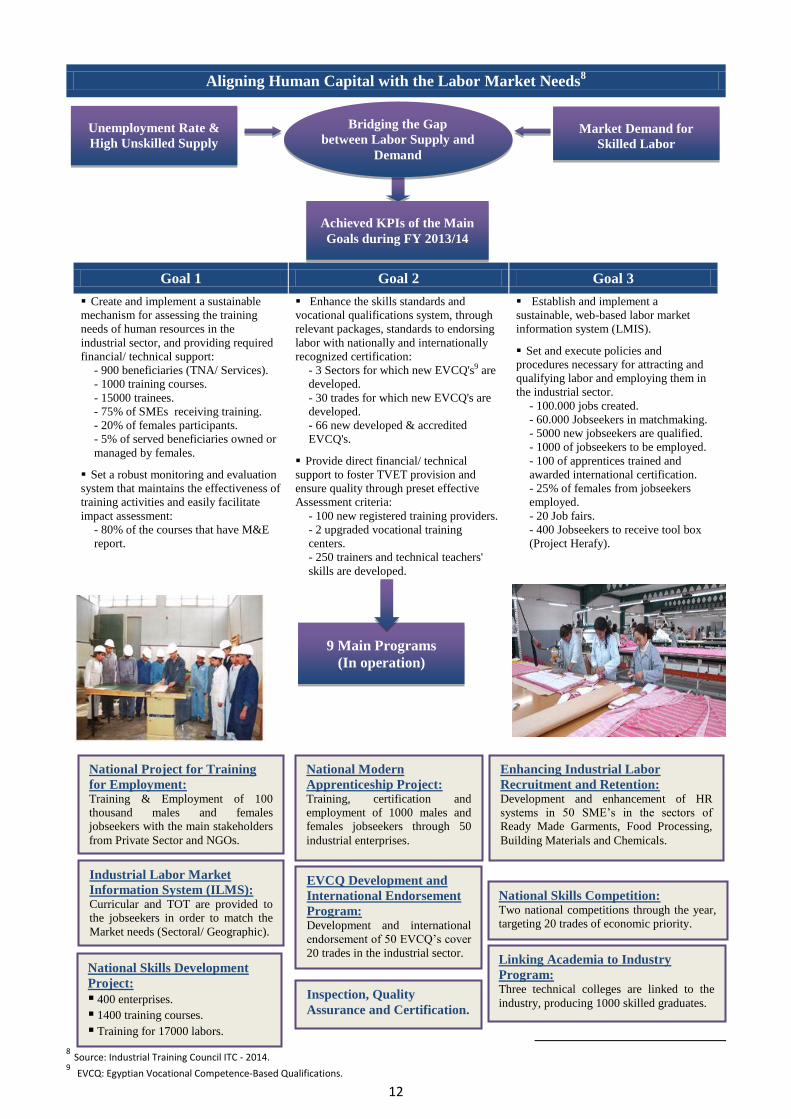

Aligning Human Capital with the Labor Market Needs8

Goal 1 Goal 2 Goal 3

Create and implement a sustainable

mechanism for assessing the training

needs of human resources in the

industrial sector, and providing required

financial/ technical support:

- 900 beneficiaries (TNA/ Services).

- 1000 training courses.

- 15000 trainees.

- 75% of SMEs receiving training.

- 20% of females participants.

- 5% of served beneficiaries owned or

managed by females.

Set a robust monitoring and evaluation

system that maintains the effectiveness of

training activities and easily facilitate

impact assessment:

- 80% of the courses that have M&E

report.

Enhance the skills standards and

vocational qualifications system, through

relevant packages, standards to endorsing

labor with nationally and internationally

recognized certification:

- 3 Sectors for which new EVCQ's9 are

developed.

- 30 trades for which new EVCQ's are

developed.

- 66 new developed & accredited

EVCQ's.

Provide direct financial/ technical

support to foster TVET provision and

ensure quality through preset effective

Assessment criteria:

- 100 new registered training providers.

- 2 upgraded vocational training

centers.

- 250 trainers and technical teachers'

skills are developed.

Establish and implement a

sustainable, web-based labor market

information system (LMIS).

Set and execute policies and

procedures necessary for attracting and

qualifying labor and employing them in

the industrial sector.

- 100.000 jobs created.

- 60.000 Jobseekers in matchmaking.

- 5000 new jobseekers are qualified.

- 1000 of jobseekers to be employed.

- 100 of apprentices trained and

awarded international certification.

- 25% of females from jobseekers

employed.

- 20 Job fairs.

- 400 Jobseekers to receive tool box

(Project Herafy).

8 Source: Industrial Training Council ITC - 2014.

9 EVCQ: Egyptian Vocational Competence-Based Qualifications.

Achieved KPIs of the Main

Goals during FY 2013/14

Unemployment Rate &

High Unskilled Supply

Market Demand for

Skilled Labor

9 Main Programs

(In operation)

National Modern

Apprenticeship Project: Training, certification and

employment of 1000 males and

females jobseekers through 50

industrial enterprises.

National Project for Training

for Employment: Training & Employment of 100

thousand males and females

jobseekers with the main stakeholders

from Private Sector and NGOs.

Industrial Labor Market

Information System (ILMS): Curricular and TOT are provided to

the jobseekers in order to match the

Market needs (Sectoral/ Geographic).

National Skills Development

Project:

400 enterprises.

1400 training courses.

Training for 17000 labors.

EVCQ Development and

International Endorsement

Program: Development and international

endorsement of 50 EVCQ’s cover

20 trades in the industrial sector.

Inspection, Quality

Assurance and Certification.

Enhancing Industrial Labor

Recruitment and Retention: Development and enhancement of HR

systems in 50 SME’s in the sectors of

Ready Made Garments, Food Processing,

Building Materials and Chemicals.

National Skills Competition: Two national competitions through the year,

targeting 20 trades of economic priority.

Linking Academia to Industry

Program: Three technical colleges are linked to the

industry, producing 1000 skilled graduates.

Bridging the Gap

between Labor Supply and

Demand

13

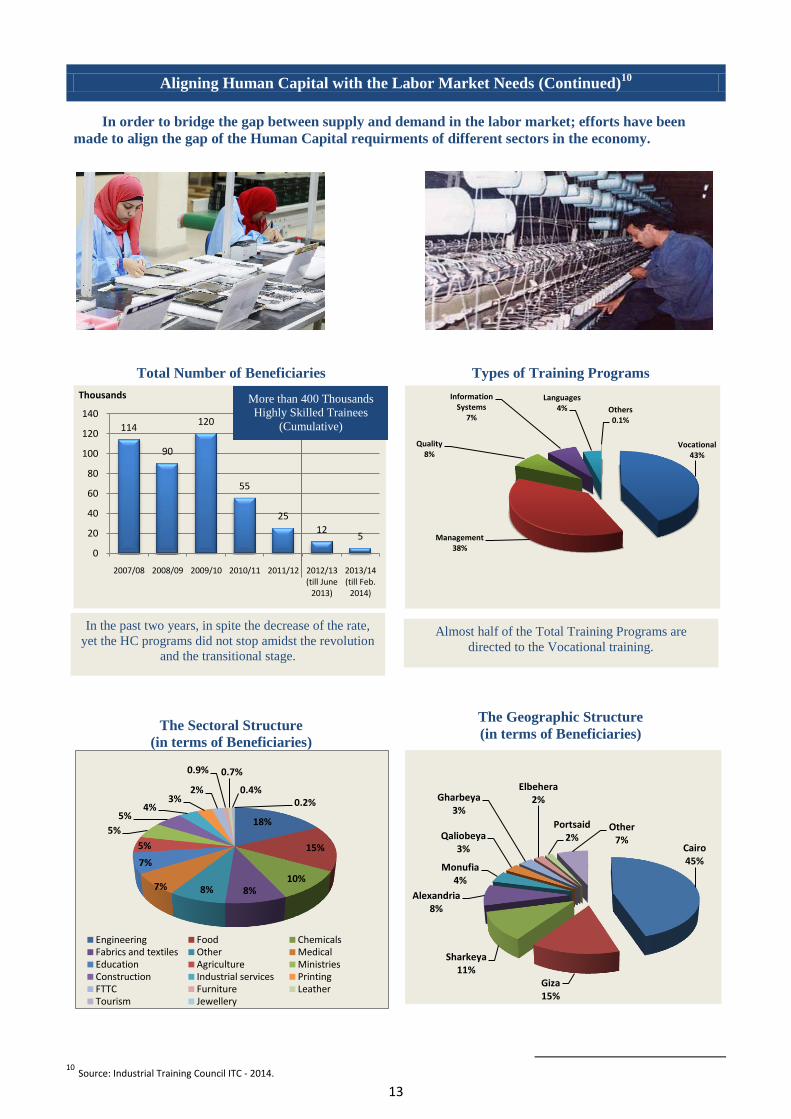

Aligning Human Capital with the Labor Market Needs (Continued)10

In order to bridge the gap between supply and demand in the labor market; efforts have been

made to align the gap of the Human Capital requirments of different sectors in the economy.

Total Number of Beneficiaries Types of Training Programs

The Sectoral Structure

(in terms of Beneficiaries)

The Geographic Structure

(in terms of Beneficiaries)

10

Source: Industrial Training Council ITC - 2014.

114

90

120

55

25

125

0

20

40

60

80

100

120

140

2007/08 2008/09 2009/10 2010/11 2011/12 2012/13 (till June

2013)

2013/14 (till Feb.

2014)

Thousands

Vocational 43%

Management38%

Quality 8%

Information Systems

7%

Languages 4% Others

0.1%

18%

15%

10%8%8%7%

7%

5%

5%

5%4%

3%2%

0.9% 0.7%

0.4%0.2%

Engineering Food Chemicals Fabrics and textiles Other Medical Education Agriculture Ministries Construction Industrial services PrintingFTTC Furniture Leather Tourism Jewellery

Cairo45%

Giza15%

Sharkeya11%

Alexandria8%

Monufia4%

Qaliobeya3%

Gharbeya3%

Elbehera2%

Portsaid2%

Other7%

Almost half of the Total Training Programs are

directed to the Vocational training.

In the past two years, in spite the decrease of the rate,

yet the HC programs did not stop amidst the revolution

and the transitional stage.

More than 400 Thousands

Highly Skilled Trainees

(Cumulative)