egis technology inc. - credit suisse

TRANSCRIPT

DISCLOSURE APPENDIX AT THE BACK OF THIS REPORT CONTAINS IMPORTANT DISCLOSURES, ANALYST CERTIFICATIONS, AND THE STATUS OF NON-US ANALYSTS. US Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

CREDIT SUISSE SECURITIES RESEARCH & ANALYTICS BEYOND INFORMATION®

Client-Driven Solutions, Insights, and Access

05 January 2016

Asia Pacific/Taiwan

Equity Research

Semiconductor Devices

Egis Technology Inc.

(6462.TWO / 6462 TT) INITIATION

Attractive play on fingerprint supercycle

■ Initiate with OUTPERFORM and NT$220 TP. We believe smartphone

fingerprint proliferation is still at an early stage and Egis is the only non-

Apple solution provider with its own algorithm and a proven record for mobile

payment. We believe its proprietary algorithm for payment (proven by

Samsung) and higher die/wafer (lower cost) should help gain share and

support high EPS growth in 2016-17E.

■ Fingerprint supercycle to be driven by payments. We forecast non-Apple

smartphone fingerprint shipment CAGR of 60% over 2015-18, reaching 57%

penetration in 2018 versus 16% in 2015. We believe this hyper growth should

be driven by launch of mobile payment platforms (Samsung/Apple Pay, and

others). According to Statista, global transactions at POS processed via

smartphones are expected to witness a 100% CAGR over 2015-20. We also

believe that fingerprint-enabled credit cards could be the next driver.

■ Egis's algorithm and IP offer share gain opportunities. Egis's passive

sensing technology and proprietary algorithm support small-size fingerprint

matching and also offers 360-degree matching. Its algorithm has been

adopted by Samsung's flagship models in 2015, and it has also started

shipping its own sensor chip to Chinese brands. We believe fingerprint

authentication for mobile payment has a higher entry barrier, and Egis will be a

good second-source partner for non-Apple smartphone makers.

■ Higher growth and entry barrier support valuation. We rate Egis

OUTPERFORM with our NT$220 target price implying 15x 2H16-1H17E EPS,

which is at a 7% premium to Taiwan fabless peers; we believe Egis's valuation

is justified by higher EPS growth on growing fingerprint opportunities, and the

potential take-off of fingerprint-enabled credit cards after 2018. Key risks

include slower adoption of fingerprint sensor, share loss and lower ASP.

Share price performance

40

60

80

100

120

80

130

180

Jun-14 Oct-14 Feb-15 Jun-15 Oct-15

Price (LHS) Rebased Rel (RHS)

The price relative chart measures performance against the

TAIWAN SE WEIGHTED INDEX which closed at 8114.26 on

04/01/16

On 04/01/16 the spot exchange rate was NT$33.11/US$1

Performance over 1M 3M 12M Absolute (%) -9.9 15.1 23.6 — Relative (%) -6.5 18.4 36.5 —

Financial and valuation metrics

Year 12/14A 12/15E 12/16E 12/17E Revenue (NT$ mn) 45.5 515.9 2,439.1 6,236.0 EBITDA (NT$ mn) -261.0 -8.5 491.9 1,774.5 EBIT (NT$ mn) -267.2 -22.1 473.7 1,751.7 Net profit (NT$ mn) -230.2 -41.8 403.2 1,479.8 EPS (CS adj.) (NT$) -3.88 -0.67 5.89 21.61 Change from previous EPS (%) n.a. n.m Consensus EPS (NT$) n.a. -0.0 8.1 24.2 EPS growth (%) n.m. n.m. n.m. 267.0 P/E (x) -35.0 -202.7 23.1 6.3 Dividend yield (%) 0 0 2.2 7.9 EV/EBITDA (x) -34.6 -982.0 17.5 4.2 P/B (x) 12.8 6.8 5.3 3.1 ROE (%) -52.0 -4.1 25.7 61.4 Net debt/equity (%) Net cash Net cash Net cash Net cash

Source: Company data, Thomson Reuters, Credit Suisse estimates

Rating OUTPERFORM* [V] Price (04 Jan 16, NT$) 136.00 Target price (NT$) 220.00¹ Upside/downside (%) 61.8 Mkt cap (NT$ mn) 9,311.8 (US$ 281.3) Enterprise value (NT$ mn) 8,366 Number of shares (mn) 68.47 Free float (%) 85.0 52-week price range 169.5 - 94.0 ADTO - 6M (US$ mn) 1.9

*Stock ratings are relative to the coverage universe in each

analyst's or each team's respective sector.

¹Target price is for 12 months.

[V] = Stock considered volatile (see Disclosure Appendix).

Research Analysts

Jerry Su

886 2 2715 6361

Derrick Yang

886 2 2715 6367

05 January 2016

Egis Technology Inc.

(6462.TWO / 6462 TT) 2

Focus charts and table Figure 1: Global mobile wallet POS payments to see faster

growth at 100% CAGR over 2015-2020E

Figure 2: China's non-cash payment is seeing a

significant change from 1Q15

0%

100%

200%

300%

400%

0

100

200

300

400

500

600

700

800

2014 2015 2016 2017 2018 2019 2020

US$ bn Mobile wallet POS payments YoY

64% 66%76% 73%

54% 50%

0.2% 0.6%

1.2% 4.8%

14.9%13.4%

0%

20%

40%

60%

80%

100%

2012 2013 2014 1Q15 2Q15 3Q15

On-line Mobile/POS/Other ATM Telephone Others

Source: Statista Source: PBOC

Figure 3: Fingerprints for mobile payments to be the next

new feature on smartphones

Figure 4: Non-Apple smartphone fingerprint penetration to

reach 57% by 2018E and Egis should capture a 19% share

2011 2012 2013 2014 2015 2106 2017

Generation3G 4G Pre-5G

Display size<4" 4-5" 5"+

Processor coresSingle core Dual core Quad core Octa core Deca core

Main camera5MP 8MP >13MP

NFC

FingerprintUnlock Payment

15-20% penetration 30% penetration 40-50% penetration

mn units 2014 2015E 2016E 2017E 2018E

Samsung shipments 318 330 340 345 350

Fingerprint penetration 14% 27% 39% 54% 65%

Samsung fingerprint shipments 45 89 133 186 228

Egis market share at Samsung 0% 0% 4% 6% 8%

Egis smartphone fingerprint shipments to Samsung - - 5 11 18

China and others smartphone shipments 793 873 941 979 1,019

Fingerprint penetration 3% 11% 27% 44% 54%

China/others fingerprint shipments 26 99 251 435 545

Egis market share at China/Others 0% 1% 8% 17% 23%

Egis smartphone fingerprint shipments to China/Others - 1 19 74 127

Non-Apple smartphone fingerprint shipments 71 188 385 621 774

Non-Apple smartphone fingerprint penetration 6% 16% 30% 47% 57%

Egis fingerprint shipments - 1 24 85 145

Egis total market share at non-Apple brands 0% 1% 6% 14% 19% Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

Figure 5: Global credit/debit/prepaid cards install base

reached ~9 bn units as of 2014

Figure 6: Zwipe's next-generation fingerprint-enabled credit

cards will be powered by payment terminals via NFC

0 1,000 2,000 3,000 4,000 5,000 6,000

UnionPay

Visa

MasterCard

American Express

JCB

Discover/Diners Club

mn units

Source: Company data Source: Company data

Figure 7: Egis' revenue to see strong growth in 2016-17E Figure 8: Egis's GM to be ahead of Taiwan fabless IC peers

-

500

1,000

1,500

2,000

1Q15 3Q15 1Q16E 3Q16E 1Q17E 3Q17E

NT$ mn Licensing Sensor chip/module Others

20%

25%

30%

35%

40%

45%

50%

55%

60%

2014 2015E 2016E 2017EEgis Mediatek RealtekElan FocalTech non-DDI Novatek non-DDI

77.8%

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

05 January 2016

Egis Technology Inc.

(6462.TWO / 6462 TT) 3

Attractive play on fingerprint supercycle We believe smartphone fingerprint proliferation is still at an early stage and expect mobile

payments to be the main growth driver over 2016-18. Egis is the only fingerprint solution

provider besides Apple/AuthenTec that has its own IC/algorithm, and a proven record for

mobile payments. We estimate non-Apple fingerprint shipments will witness a 60% CAGR

over 2015-2018—reaching 774 mn units by 2018—versus a 4% CAGR for smartphone unit

growth over the same period (1.61 bn units in 2018). We believe Egis's proprietary algorithm,

lower cost, and dual-sourcing opportunity should drive its earnings growth during 2016-17.

Fingerprint proliferation is still at an early stage The launch of mobile payment platforms such as Samsung/Apple Pay, and others (ZTE

Pay, Alipay, WeChat Pay, etc) will be the main driver for fingerprint adoption on mobile

devices. According to Statista, global transactions at POS processed via smartphones are

expected to witness a 100% CAGR over 2015-2020. We estimate global smartphone

fingerprint adoption of 29% in 2015 (418 mn units) and will reach 40%/55% in 2016/17E

(~100% for iPhone). For non-Apple phones, we estimate penetration of 16% in 2015,

increasing to 30%/47%/57% in 2016/17/18. The industry is also developing fingerprint-

enabled credit cards, which we believe could be the next growth area after 2018.

Egis’s algorithm and IP offer share gain opportunities Egis was formed as a result of a merger of three early specialists in Taiwan's fingerprint

industry. Its passive sensing technology and proprietary algorithm support small-size

fingerprint matching and also offers 360-degree matching, especially for area-type

sensors, that are adopted for mobile payment applications. Its algorithm has been adopted

by Samsung's flagship smartphones in 2015, and the company has also started shipping

its own sensor chip for Chinese customers in 2H15. We believe fingerprint authentication

for mobile payment has a higher entry barrier, and Egis will be a good second source

partner as Finger Print Cards dominate the China market with a ~90% share in 2015.

Moreover, Egis's 30-40% smaller die size (more die per wafer, lower cost structure) and

own algorithm for payment (4-7% support on GM) with a proven track record should help it

gain share in 2016-17E.

Fingerprint embedded within display will be an

opportunity rather than a threat for Egis We believe capacitive fingerprint sensing will be the mainstream technology for mobile

devices in the next 2-3 years, given the mature ecosystem and lower cost structure. In the

longer term, we see the possibility that fingerprint sensing could be integrated into displays.

If this happens, we believe pure fingerprint module makers could be the most vulnerable, but

we believe the impact on Egis should be minimal as it can work with display makers by

providing processing chip and algorithm. Moreover, as all panel makers are in Asia and

fingerprint-embedded display could require a more complicated IC and algorithm, we view

the integration trend to be an opportunity rather than a threat for Egis.

Higher growth and entry barrier support valuation We initiate coverage on Egis with an OUTPERFORM rating and a target price of NT$220,

based on 15x of our 2H16-1H17 EPS or 10.2x 2017 EPS. While the multiple is at a 7%

premium to TW IC design peers (14x), we believe it is justified by higher earnings growth

on the back of growing fingerprint opportunities (60% CAGR for non-Apple in 2015-18E),

further share gains, and the higher technology barrier for mobile payment.

Potential near-term catalysts include earlier-than-expected pull-in for Samsung's A-series

models, more design-wins from non-Apple smartphone makers, and alliances with

strategic partners for mobile payment in China. Key risks include slower adoption of

fingerprint sensors for non-Apple smartphones, market share loss, and weaker ASP.

Non-Apple smartphone

fingerprint demand should

post a 60% CAGR over

2015-18E versus 4% for

smartphone units

Fingerprint proliferation will

likely be driven by mobile

payment and smart cards

Fingerprint authentication

for mobile payment has a

higher entry barrier

Fingerprint embedded

display may require

a more complicated IC

and algorithm

Our TP of NT$220 is based

on 15x 2H16-1H17E EPS

05 January 2016

Egis Technology Inc.

(6462.TWO / 6462 TT) 4

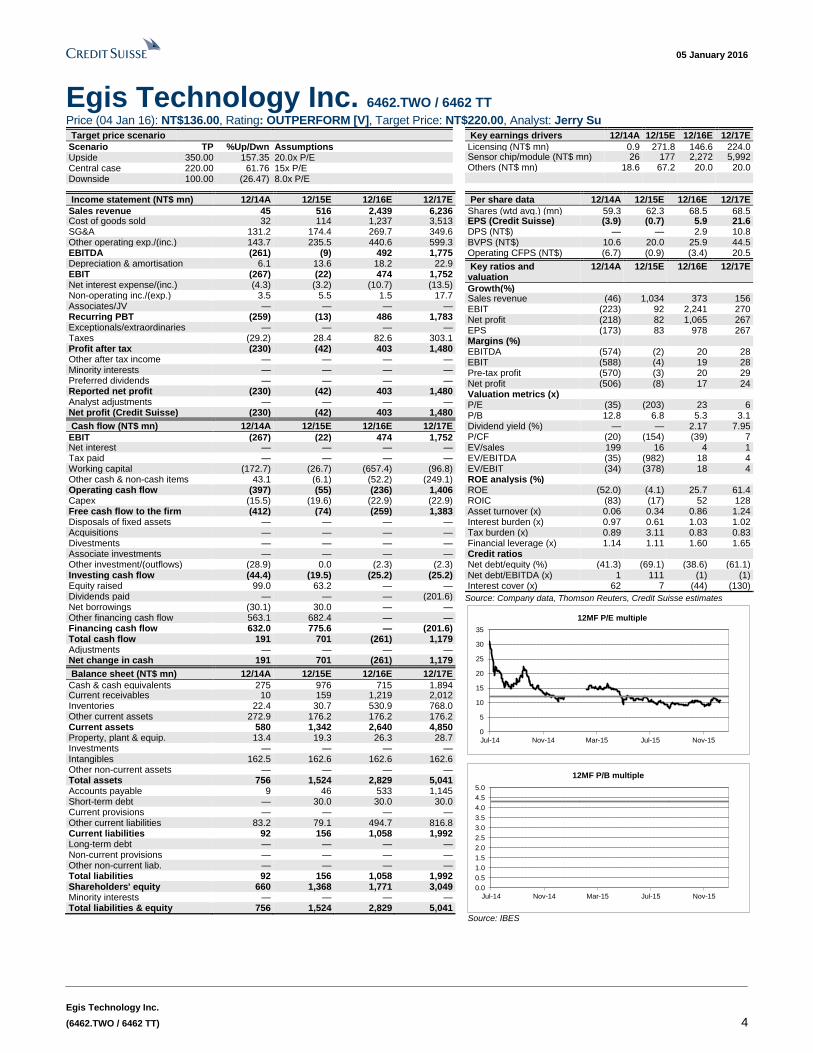

Egis Technology Inc. 6462.TWO / 6462 TT Price (04 Jan 16): NT$136.00, Rating: OUTPERFORM [V], Target Price: NT$220.00, Analyst: Jerry Su

Target price scenario

Scenario TP %Up/Dwn Assumptions Upside 350.00 157.35 20.0x P/E Central case 220.00 61.76 15x P/E Downside 100.00 (26.47) 8.0x P/E

Key earnings drivers 12/14A 12/15E 12/16E 12/17E

Licensing (NT$ mn) 0.9 271.8 146.6 224.0 Sensor chip/module (NT$ mn) 26 177 2,272 5,992 Others (NT$ mn) 18.6 67.2 20.0 20.0

Income statement (NT$ mn) 12/14A 12/15E 12/16E 12/17E

Sales revenue 45 516 2,439 6,236 Cost of goods sold 32 114 1,237 3,513 SG&A 131.2 174.4 269.7 349.6 Other operating exp./(inc.) 143.7 235.5 440.6 599.3 EBITDA (261) (9) 492 1,775 Depreciation & amortisation 6.1 13.6 18.2 22.9 EBIT (267) (22) 474 1,752 Net interest expense/(inc.) (4.3) (3.2) (10.7) (13.5) Non-operating inc./(exp.) 3.5 5.5 1.5 17.7 Associates/JV — — — — Recurring PBT (259) (13) 486 1,783 Exceptionals/extraordinaries — — — — Taxes (29.2) 28.4 82.6 303.1 Profit after tax (230) (42) 403 1,480 Other after tax income — — — — Minority interests — — — — Preferred dividends — — — — Reported net profit (230) (42) 403 1,480 Analyst adjustments — — — — Net profit (Credit Suisse) (230) (42) 403 1,480

Cash flow (NT$ mn) 12/14A 12/15E 12/16E 12/17E

EBIT (267) (22) 474 1,752 Net interest — — — — Tax paid — — — — Working capital (172.7) (26.7) (657.4) (96.8) Other cash & non-cash items 43.1 (6.1) (52.2) (249.1) Operating cash flow (397) (55) (236) 1,406 Capex (15.5) (19.6) (22.9) (22.9) Free cash flow to the firm (412) (74) (259) 1,383 Disposals of fixed assets — — — — Acquisitions — — — — Divestments — — — — Associate investments — — — — Other investment/(outflows) (28.9) 0.0 (2.3) (2.3) Investing cash flow (44.4) (19.5) (25.2) (25.2) Equity raised 99.0 63.2 — — Dividends paid — — — (201.6) Net borrowings (30.1) 30.0 — — Other financing cash flow 563.1 682.4 — — Financing cash flow 632.0 775.6 — (201.6) Total cash flow 191 701 (261) 1,179 Adjustments — — — — Net change in cash 191 701 (261) 1,179

Balance sheet (NT$ mn) 12/14A 12/15E 12/16E 12/17E

Cash & cash equivalents 275 976 715 1,894 Current receivables 10 159 1,219 2,012 Inventories 22.4 30.7 530.9 768.0 Other current assets 272.9 176.2 176.2 176.2 Current assets 580 1,342 2,640 4,850 Property, plant & equip. 13.4 19.3 26.3 28.7 Investments — — — — Intangibles 162.5 162.6 162.6 162.6 Other non-current assets — — — — Total assets 756 1,524 2,829 5,041 Accounts payable 9 46 533 1,145 Short-term debt — 30.0 30.0 30.0 Current provisions — — — — Other current liabilities 83.2 79.1 494.7 816.8 Current liabilities 92 156 1,058 1,992 Long-term debt — — — — Non-current provisions — — — — Other non-current liab. — — — — Total liabilities 92 156 1,058 1,992 Shareholders' equity 660 1,368 1,771 3,049 Minority interests — — — — Total liabilities & equity 756 1,524 2,829 5,041

Per share data 12/14A 12/15E 12/16E 12/17E

Shares (wtd avg.) (mn) 59.3 62.3 68.5 68.5 EPS (Credit Suisse) (NT$)

(3.9) (0.7) 5.9 21.6 DPS (NT$) — — 2.9 10.8 BVPS (NT$) 10.6 20.0 25.9 44.5 Operating CFPS (NT$) (6.7) (0.9) (3.4) 20.5

Key ratios and valuation

12/14A 12/15E 12/16E 12/17E

Growth(%) Sales revenue (46) 1,034 373 156 EBIT (223) 92 2,241 270 Net profit (218) 82 1,065 267 EPS (173) 83 978 267 Margins (%) EBITDA (574) (2) 20 28 EBIT (588) (4) 19 28 Pre-tax profit (570) (3) 20 29 Net profit (506) (8) 17 24 Valuation metrics (x) P/E (35) (203) 23 6 P/B 12.8 6.8 5.3 3.1 Dividend yield (%) — — 2.17 7.95 P/CF (20) (154) (39) 7 EV/sales 199 16 4 1 EV/EBITDA (35) (982) 18 4 EV/EBIT (34) (378) 18 4 ROE analysis (%) ROE (52.0) (4.1) 25.7 61.4 ROIC (83) (17) 52 128 Asset turnover (x) 0.06 0.34 0.86 1.24 Interest burden (x) 0.97 0.61 1.03 1.02 Tax burden (x) 0.89 3.11 0.83 0.83 Financial leverage (x) 1.14 1.11 1.60 1.65 Credit ratios Net debt/equity (%) (41.3) (69.1) (38.6) (61.1) Net debt/EBITDA (x) 1 111 (1) (1) Interest cover (x) 62 7 (44) (130)

Source: Company data, Thomson Reuters, Credit Suisse estimates

0

5

10

15

20

25

30

35

Jul-14 Nov-14 Mar-15 Jul-15 Nov-15

12MF P/E multiple

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

Jul-14 Nov-14 Mar-15 Jul-15 Nov-15

12MF P/B multiple

Source: IBES

05 January 2016

Egis Technology Inc.

(6462.TWO / 6462 TT) 5

Fingerprint proliferation is still at an early stage Egis was funded in December 2007, focusing on fingerprint sensor, algorithm, security

software, etc. It was formed through the merger of three early specialists in Taiwan's

fingerprint industry, including LighTuning Tech (focused on fingerprint sensor IC), ABIG

(focused on algorithm), and HiTrust (focused on encryption and security software). Egis

focused on the NB/tablet market during 2008-11 and supplied fingerprint solution provider

for leading NB/tablet brands such as Asus, Acer, HP, Lenovo, ViewSonic, etc. In 2012,

Egis started to provide fingerprint solution for China's Social Welfare program, which

helped it to further strengthen its algorithm capability.

Egis started to work on fingerprint solutions for mobile devices in 2014 and successfully

entered Samsung supply chain by providing the algorithm to Galaxy S6-series. It also

developed its own IC, which could be placed on the front, back, and side of the handset,

depending on customer requirements. Its proprietary passive sensing technology and

strong IP portfolio makes it the only fingerprint solution provider besides Apple/AuthenTec

that offers total fingerprint solution, including sensor and algorithm, especially for mobile

payment applications.

Figure 9: Egis was formed through the merger of three companies in 2007 Company name Main Business

LighTuning was established in 2002 and is specialised in

developing swipe/area type fingerprint ICs

ABiG was established in 2000 and is specialised in fingerprint

matching algorithm. Its main customers were Authentec,

UPEK, and Validity

HiTrust was established in 1998 and is specialised in

encryption and security software

Source: Company data, Credit Suisse

Payment is the main driver for fingerprint

proliferation on mobile devices

Passwords and drawing patterns are used as the primary method to unlock mobile devices

until Apple integrated the fingerprint sensor in its iPhone 5S in 3Q13. Although fingerprint

identification can provide better security versus passwords and drawing patterns, the

penetration rate for non-Apple handset didn’t really take off in 2014-15 given the higher

cost, lack of end-application/ecosystem besides unlocking the device, and limited support

from the Android operating system.

According to Statista, the global mobile payment transaction is expected to reach US$721

bn by 2017, ~30% CAGR over 2015-17. It also forecasts that the global mobile wallet POS

payments, which are the transactions at Point-of-Sale that are processed via smartphone

applications (i.e. mobile wallets), to see a 100% CAGR over 2015-20. We believe this is

mainly driven by the launch of mobile payment platforms by Samsung, Apple, and others

(ZTE Pay, Alipay, WeChat Pay, etc) and change of consumer behaviour. We also believe

the support by FIDO (Fast IDentity Online) Alliance to further accelerate mobile payment

Egis was formed through a

merger of three companies

Global mobile wallet POS

payments to see 100%

CAGR in 2015-2020E

05 January 2016

Egis Technology Inc.

(6462.TWO / 6462 TT) 6

via NFC in the next few years and will also support fingerprint proliferation. With the more

mature ecosystem and lower component cost, we believe fingerprint will become the

mainstream authentication method for these payments, replacing pin or password, as

fingerprint identification is faster and more secure.

Figure 10: Global mobile payment transaction to grow at

~30% CAGR during 2015-17E

Figure 11: Global mobile wallet POS payments to see

faster growth at 100% CAGR during 2015-20E

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0

100

200

300

400

500

600

700

800

2010 2011 2012 2013 2014 2015 2016 2017

US$ bn Annual transaction volume YoY (RHS)

0%

50%

100%

150%

200%

250%

300%

350%

400%

0

100

200

300

400

500

600

700

800

2014 2015 2016 2017 2018 2019 2020

US$ bn Mobile wallet POS payments YoY

Source: Statista Source: Statista

Figure 12: Adoption and transaction value for global

mobile wallet POS payment will also see strong growth

Figure 13: China's non-cash payment seeing a significant

change from 1Q15

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

0

50

100

150

200

250

300

350

400

450

500

2014 2015 2016 2017 2018 2019 2020

US$mn User Avg transaction value per user every year (RHS)

64% 66%76% 73%

54% 50%

0.2% 0.6%

1.2% 4.8%

14.9%13.4%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2012 2013 2014 1Q15 2Q15 3Q15

On-line Mobile/POS/Other ATM Telephone Others

Source: Statista Source: PBOC

Multiple payment platforms roll out in China would propel fingerprint adoption for

mobile devices

Apple announced Apple Pay service on 9 September 2014 and launched the service in the

US on 20 October 2014. The service was then rolled out to the UK in July 2015 and then

to Canada/Australia in November 2015. Besides using Apple Pay in the stores with NFC

contactless reader, it also supports using Apple Pay in various apps such as Best Buy,

Starbucks, Target, etc. Samsung also announced its payment service at 2015 MWC and

launched Samsung Pay in South Korea and the US in August 2015 and September 2015,

respectively. Samsung Pay supports both NFC and MST (Magnetic Secure Transmission),

which can work with more POS terminals in the US. However, Samsung’s support on in-

app payments will be enabled some time in 2016.

For the China market, both Apple and Samsung entered agreements with China’s

UnionPay on 18 December 2015, and are expected to extend their payment service into

China in early 2016. Separately, ZTE announced its ZTE Pay on 23 December 2015,

providing similar mobile payment service as Apple Pay but can also support payments for

Apple and Samsung plan to

roll-out their payment

platforms in China in early

2016

ZTE also announced ZTE

Pay in Dec 2015

05 January 2016

Egis Technology Inc.

(6462.TWO / 6462 TT) 7

public transportation. Although China’s mobile payment today is dominated by Alipay and

WeChat pay, we believe the introduction of Apple/Samsung/ZTE Pay with NFC might

change the competitive landscape, especially other local handset makers will introduce

more fingerprint-enabled devices with their own mobile payment platform or alliance with

third parties (ZTE Pay, Alipay, WeChat Pay, UnionPay, individual banks, etc) in 2016-17.

Figure 14: Mobile payment platforms to drive fingerprint authentication

Apple Pay Samsung Pay ZTE Pay Android Pay

Available countries US, UK, Canada, Australia,

China (2016)

Korea, US, China (2016) China US

Supported devices iPhone 6/6+, iPhone

6S/6S+, Watch, iPad Air2,

iPad Mini 3/4, iPad Pro

Galaxy S6, S6 Edge, S6

Edge+, Note 5

Android phones with NFC

and Fingerprint sensor

Android phones with NFC

and HCE support running

KitKat (4.4) or higher

Authentication methods Fingerprint Fingerprint or PIN Fingerprint PIN, fingerprint (future)

Cards accepted Credit, debit, and selected

loyalty cards

Credit and debit cards Credit, debit, public

transportation cards

Credit, debit, and selected

loyalty cards

Data transfer method NFC NFC and MST NFC NFC

In app payment Available now Available soon Developing Available now

Source: Company data, Credit Suisse

Lack of new selling points for smartphone also make

fingerprint a nice to have feature

CS Hardware team estimates global smartphone shipment growth to slow down to 4%

CAGR over 2015-18E versus 19% CAGR in 2013-15E and 36% CAGR during 2010-15E.

We believe this is mainly due to the already high installation base of smartphone,

especially in China, and that smartphone today lacks new selling points to attract

consumers’ attentions. The smartphone industry has experienced rapid growth in 2010-

2014 but competition intensified in 2015 as more local brands and whitebox makers

entered the market. Under this competitive environment, most brands tried to differentiate

themselves by offering larger size and higher resolution display, multi-core CPU, more

memory content, better camera, more stylish design (casing, curved, thickness); however,

we believe the size and spec upgrades are reaching a limit.

Figure 15: Global smartphone growth is slowing down

0%

10%

20%

30%

40%

50%

60%

70%

80%

-

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2010 2011 2012 2013 2014 2015E 2016E 2017E 2018E 2019E 2020E

mn units Smartphone YoY (RHS)

Source: Company data, Credit Suisse estimates

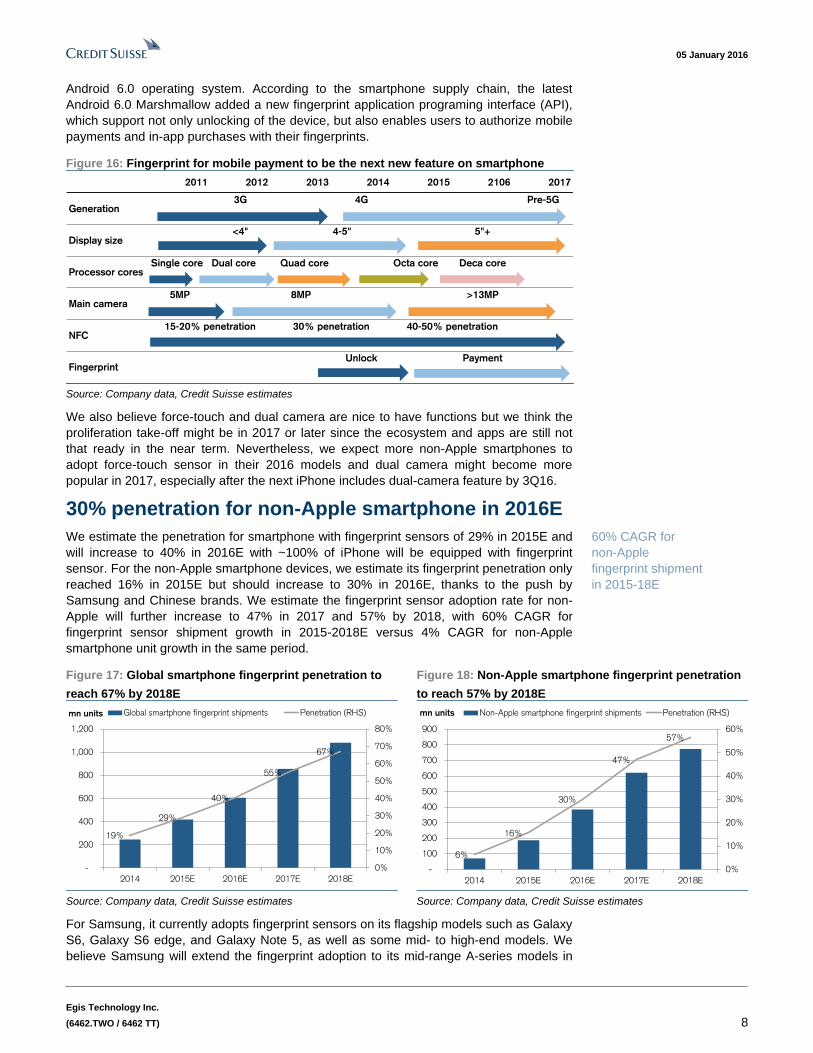

For 2016, we believe smartphone makers will adopt fingerprint sensor, force-touch, dual

camera, embedded touch, etc features as their selling points for the new models. For the

non-Apple smartphone makers, we believe fingerprint will see faster proliferation from

2016 on more established ecosystem, more affordable pricing, and the native support from

Fingerprint is becoming

more popular on

smartphone given lack of

new features

Native support from Android

6.0 will also help on the

proliferation

05 January 2016

Egis Technology Inc.

(6462.TWO / 6462 TT) 8

Android 6.0 operating system. According to the smartphone supply chain, the latest

Android 6.0 Marshmallow added a new fingerprint application programing interface (API),

which support not only unlocking of the device, but also enables users to authorize mobile

payments and in-app purchases with their fingerprints.

Figure 16: Fingerprint for mobile payment to be the next new feature on smartphone

2011 2012 2013 2014 2015 2106 2017

Generation3G 4G Pre-5G

Display size<4" 4-5" 5"+

Processor coresSingle core Dual core Quad core Octa core Deca core

Main camera5MP 8MP >13MP

NFC

FingerprintUnlock Payment

15-20% penetration 30% penetration 40-50% penetration

Source: Company data, Credit Suisse estimates

We also believe force-touch and dual camera are nice to have functions but we think the

proliferation take-off might be in 2017 or later since the ecosystem and apps are still not

that ready in the near term. Nevertheless, we expect more non-Apple smartphones to

adopt force-touch sensor in their 2016 models and dual camera might become more

popular in 2017, especially after the next iPhone includes dual-camera feature by 3Q16.

30% penetration for non-Apple smartphone in 2016E

We estimate the penetration for smartphone with fingerprint sensors of 29% in 2015E and

will increase to 40% in 2016E with ~100% of iPhone will be equipped with fingerprint

sensor. For the non-Apple smartphone devices, we estimate its fingerprint penetration only

reached 16% in 2015E but should increase to 30% in 2016E, thanks to the push by

Samsung and Chinese brands. We estimate the fingerprint sensor adoption rate for non-

Apple will further increase to 47% in 2017 and 57% by 2018, with 60% CAGR for

fingerprint sensor shipment growth in 2015-2018E versus 4% CAGR for non-Apple

smartphone unit growth in the same period.

Figure 17: Global smartphone fingerprint penetration to

reach 67% by 2018E

Figure 18: Non-Apple smartphone fingerprint penetration

to reach 57% by 2018E

19%

29%

40%

55%

67%

0%

10%

20%

30%

40%

50%

60%

70%

80%

-

200

400

600

800

1,000

1,200

2014 2015E 2016E 2017E 2018E

mn units Global smartphone fingerprint shipments Penetration (RHS)

6%

16%

30%

47%

57%

0%

10%

20%

30%

40%

50%

60%

-

100

200

300

400

500

600

700

800

900

2014 2015E 2016E 2017E 2018E

mn units Non-Apple smartphone fingerprint shipments Penetration (RHS)

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

For Samsung, it currently adopts fingerprint sensors on its flagship models such as Galaxy

S6, Galaxy S6 edge, and Galaxy Note 5, as well as some mid- to high-end models. We

believe Samsung will extend the fingerprint adoption to its mid-range A-series models in

60% CAGR for

non-Apple

fingerprint shipment

in 2015-18E

05 January 2016

Egis Technology Inc.

(6462.TWO / 6462 TT) 9

2016 and in the long term it will also expand it to the entry level J series and make

fingerprint sensor a standard feature for its smartphones.

We also believe other non-Chinese Android smartphone makers in North Asia, such as

Asus, LG, HTC, Sony, Panasonic, etc will introduce more fingerprint-enabled smartphones

in 2016. The Chinese smartphone makers, Huawei, Meizu, Oppo, Vivo, etc have

announced their fingerprint-enabled smartphones since 2014 and we have also seen other

brands such as LeTV, Xiaomi, Lenovo, ZTE, Gionee, etc launched their products in 2015.

Our supply chain visit in October 2015 also suggests whitebox makers such as Elephone,

Malata, Leagoo, etc are now adopting fingerprint onto their mid- to high-end devices.

Figure 19: Global smartphone fingerprint shipment estimates: Non-Apple to grow at 60% CAGR over 2015-18E

mn units 2014 2015E 2016E 2017E 2018E 15-18E CAGR

Total Smartphone 1,303 1,438 1,504 1,559 1,614 3.9%

YoY (RHS) 28% 10% 5% 4% 4%

iPhone shipments 193 235 222 235 245 1.4%

Fingerprint penetration 91% 98% 100% 100% 100%

iPhone fingerprint shipments 175 230 222 235 245 2.1%

Samsung shipments 318 330 340 345 350 2.0%

Fingerprint penetration 14% 27% 39% 54% 65%

Samsung fingerprint shipments 45 89 133 186 228 36.9%

China and other smartphone shipments 793 873 941 979 1,019 5.3%

Fingerprint penetration 3% 11% 27% 44% 54%

China and other smartphone fingerprint shipments 26 99 251 435 545 76.8%

Global smartphone fingerprint shipments 246 418 607 856 1,082 37.3%

Non-Apple smartphone fingerprint shipments 71 188 385 621 774 60.3%

Global smartphone fingerprint penetration 19% 29% 40% 55% 67%

Non-Apple smartphone fingerprint penetration 6% 16% 30% 47% 57%

Source: Company data, Credit Suisse estimates

However, some of the fingerprint devices announced in 2015 (for example Sony Z5, ZTE

Blade A1, LeTV Max, Oppo R7, etc), only supports unlock function, not for the payment

authentication. Nevertheless, we believe the native support by Android 6.0, maturing

ecosystems, and cheaper components cost will be the main push for the fingerprint

authentication for mobile payments among the Chinese smartphone makers.

Whitebox is also adopting

fingerprint on their mid- to

high-end devices

Not all fingerprint-enabled

devices support payment

05 January 2016

Egis Technology Inc.

(6462.TWO / 6462 TT) 10

Figure 20: Selective branded smartphones with fingerprint enabled Brand Coolpad Dove Google Huawei LeTV LeTV LG Meizu Samsung

Model name Dazen Note 3 L5 Pro Nexux 6P Honor 7 1S Max V10 MX5 A5

Fingerprint sensor FPC Goodix FPC FPC Goodix FPC FPC FPC Synaptics/Egis

Algorithm Precise Biometric Goodix Precise Biometric Precise Biometric Goodix Precise Biometric Precise Biometric Precise Biometric Samsung/Egis

Location Back Front Back Back Back Back Back Back Front

Brand Meizu Nubia OnePlus Oppo Samsung ZTE ZTE Lenovo Samsung

Model name Pro 5 Z9 Max OnePlus 2 R7+ Galaxy S6 Blade S7 Axon ZUK Z1 A7

Fingerprint sensor FPC Egis FPC FPC Synaptics Goodix FPC FPC Synaptics/Egis

Algorithm Precise Biometric Egis Precise Biometric Precise Biometric Egis Goodix Precise Biometric Precise Biometric Samsung/Egis

Location Front Side Front Back Front Front Back Front Front Source: Company data

Figure 21: Increasing numbers of whitebox smartphones adopting fingerprint solutions Company Bluboo Blackview Quality Malata Bluboo DOOGEE Maysun Malata LEAGOO Elephone Elephone 8Smobile

Model name X6 Alife P1 Pro QT-815 L508 X6 Plus F5 M5530L M1 Elite 1 P9000 Vowney 8S5631

Image

Size 5.5" 5.5" 5.5" 5.0" 5.5" 5.5" 5.5'' 5.2'' 5.5'' 5.5'' 5.5'' 5.5''

Technology TDD-LTE/FDD-LTE TDD-LTE/FDD-LTE TDD-LTE/FDD-LTE TDD-LTE/FDD-LTE TDD-LTE/FDD-LTE TDD-LTE/FDD-LTE TDD-LTE/FDD-LTE TDD-LTE/FDD-LTE TDD-LTE/FDD-LTE TDD-LTE/FDD-LTE TDD-LTE/FDD-LTE TDD-LTE/FDD-LTE

Pixels 1280*720 1280*720 1280*720 1280*720 1920*1080 1920*1080 1920*1080 1920*1080 1920*1080 1920*1080 2560*1440 2560*1440

PPI 267 267 267 293 400 400 400 423 400 400 534 534

Touch Capacitive G/F/F Capacitive G/F/F Capacitive Capacitive G/F/F G/F/F Capacitive Capacitive Capacitive Capacitive

Fingerprint ID Area (front) Area (front) Area (back) Area (front) Area (front) Area (back) Area (back) Area (back) Area (front) Area (side) Area (back) Area (back)

RAM 1GB 2GB 1GB 1GB 3GB 3GB 3GB 3GB 3GB 4GB 4GB 3GB

ROM 8GB 16GB 8GB 8GB 16GB 16GB 16GB 16GB 32GB 32GB 32GB 32GB

Camera 2MP + 8MP 5MP + 13MP 2MP + 5MP 5MP + 13MP 5MP + 13MP 5MP + 13MP 5MP + 13MP 8MP + 21MP 13MP + 16MP 8MP + 21MP 5MP + 21MP 8MP + 21MP

Battery 3000mAh 2600mAh 2900mAh 2400mAh 3000mAh 2660mAh 4000mAh 2300mAh 2400mAh 4000mAh 4000mAh

Processor Chip MT6735 MT6735 MT6735 MT6735 MT6753 MT6753 MT6753 MT6755 MT6755 (P10) MT6755 MT6795 (X10) MT6795 (X10)

Multi-core Quad Quad Quad Quad Octa Octa Octa Octa Octa Octa Octa Octa

Factory Price (USD) $85 $99 $110 $120 $125 $130 $154 $160 $167 $240 $250 $270 Source: Company data

Smart/Credit cards could be the next growth area

Master Card announced in October 2014 that it has partnered with Zwipe and introduced

the world’s first contactless payment card that integrated a fingerprint sensor. The

prototype demonstrated by Zwipe included its secure biometric authentication technology

that stores the cardholders’ biometric data on the card, not in an external database. It

claims its biometric authentication can replace the PIN entry, thus allowing cardholders to

make payments of any amount, versus current contactless payment cards in the market

today, which still requires PIN or signature for spending that exceeds a certain amount.

According to Zwipe, it is using Fingerprint Cards’ (FPC) fingerprint sensor in the pilot

product.

Master Card/Zwipe are also working on the next generation of the fingerprint-enabled

credit card that can harvest energy from the credit card payment terminals without the

need for a battery. We believe this could be a new growth driver for the fingerprint sensor

industry given the biometric authentication with contactless payment card offers security

and convenience for consumers, merchants, and banks. This technology can also be used

for other applications such as access card, networking/PC login, and other security

required applications.

Fingerprint enabled credit

card is under development

05 January 2016

Egis Technology Inc.

(6462.TWO / 6462 TT) 11

Figure 22: Zwipe's fingerprint-enabled credit card

prototype and next generation product

Figure 23: Zwipe's next generation fingerprint-enabled

credit card will be powered by payment terminal via NFC

Source: Company data Source: Company data

According to our analysis, global credit, debit, and pre-paid cards issued by Visa, Master

Card, American Express, JCB, and UnionPay have reached ~9 bn units as of 2014. The

installation base is 5-6x of the smartphone annual shipments and represents a huge

opportunity for the fingerprint sensor supply chain. Other than Master Card, China’s

UnionPay is also interested to develop fingerprint authentication solutions.

Figure 24: Global credit/debit/pre-paid cards install based

reached ~9 bn units as of 2014

Figure 25: China's credit cards and banking cards saw

significant growth in the past few years

0 1,000 2,000 3,000 4,000 5,000 6,000

UnionPay

Visa

MasterCard

American Express

JCB

Discover/Diners Club

mn units

2,000

2,500

3,000

3,500

4,000

4,500

5,000

5,500

2011 2012 2013 2014 3Q15

mn units

Source: Company data Source: PBOC

Global credit, debit, and pre-

paid cards install base is 5-

6x of the smartphone

shipments

05 January 2016

Egis Technology Inc.

(6462.TWO / 6462 TT) 12

Egis’s algorithm and IP offer share gain opportunities Capacitive sensing is the mainstream technology for mobile devices

Fingerprint sensing has been around and applied to various devices and applications for

the past decades. There are four major steps for the fingerprint sensing process flow:

fingerprint scanning, minutiae (feature) extraction, digital processing and matching. Before

Apple adopted the capacitive touch fingerprint sensor on the iPhone, optical and

capacitive swipe was the mainstream sensing technology of fingerprint scanning and was

adopted on door locks, NB, national security, banking, etc. Nevertheless, the market size

for these applications is relatively small and shipments didn’t take off until Apple adopted

the fingerprint sensor onto iPhone 5S.

Figure 26: Optical fingerprint module Figure 27: Capacitive fingerprint sensor

Source: Gingytech Source: Egis

Although optical fingerprint scanning is a mature technology, its requirement for a high

photo sensitivity camera with thicker design makes it difficult to fit into mobile devices. The

fingerprint sensors used on iPhone and other Android devices have adopted capacitive

scanning as it has the advantages of smaller form-factor, higher resolution, lower power

consumption and cheaper cost. Among the swipe and area-type capacitive fingerprint

sensing technologies, we believe area-type will become the mainstream as it is more

accurate, easier to use, and offers more flexible industrial design.

Figure 28: Comparison of area and swipe-type capacitive fingerprint sensors

Area Swipe

Chip size Medium to small Small

Image quality Good Weak

Cost Low Low

Accuracy High accuracy Less accurate

User experience Good More difficult to use

Source: Company data, Credit Suisse

Active capacitive sensing is widely adopted but need to get around Apple’s IP

Capacitive fingerprint sensing in general measures capacitance of the finger, which varies

between the ridges and valleys of the fingerprint, to form the image of the fingerprint.

There are two different sensing methods:

1) Active sensing: Active capacitive fingerprint sensing is widely adopted by several

fingerprint sensor providers such as FPC, IDEX, Synaptics, Goodix, Silead, etc,

despite potential risk for violating Apple/AuthenTec’s patents. The fingerprint module

applies a small voltage to the skin and the sensor measures the capacitance on the

finger to reform an image of the fingerprint. The pros of active sensing is that it can

measure the live skin cell layer, hence does not require the need for clean,

Area-type capacitive

sensing is the mainstream

fingerprint sensing

technology

Active sensing might face IP

issues

05 January 2016

Egis Technology Inc.

(6462.TWO / 6462 TT) 13

undamaged skin and a clean sensing surface. However, active sensing requires

additional circuits, shielding layers, metal rings, which results in a higher cost versus

passive sensing.

2) Passive sensing: Passive sensing use the sensor array pixel to detect the

capacitance on the fingerprint, which varies between the ridges and valleys of the

fingerprint. Passive sensing has the advantages of less complicated wafer processing

and better cost structure, but has a weaker signal. It requires a unique hardware

design and software/algorithm to achieve better results. Egis. Elan, IMD, FocalTech,

etc have developed their fingerprint sensors based on passive sensing technology but

we believe Egis is the only vendor that has enabled passive fingerprint sensing on

mobile devices given its superior algorithm capability.

Figure 29: Passive capacitive fingerprint sensing

structure

Figure 30: Active capacitive fingerprint sensing structure

Source: Company data, Credit Suisse Source: Company data, Credit Suisse

Algorithm for mobile payment sets a higher entry

barrier

Most of the non-Apple fingerprint solution suppliers can offer their own algorithm for using

fingerprint to unlock the phone, but still rely on third-party algorithm suppliers for the

mobile payment application. Currently, leading fingerprint solution providers such as FPC

and Synaptics, as well as new comers such as Elan, FocalTech, Silead, etc all license

algorithm from third-party suppliers such as Precise Biometric or Egis.

We believe the main reasons for this is because: (1) the sizes for the fingerprint sensor/

module become smaller on the mobile devices, which results in a smaller detection area

and requires a more complicated algorithm to meet the FAR (False Acceptance Rate,

<1/50,000) and FRR (False Rejection Rate, <3%) standards, and (2) algorithm and

software for mobile payment require longer design-in cycle as it is more complex to

integrate payment function with handset makers, payment platforms, and within an

acceptable response time. Some payment or handset makers might also require FIDO

(Fast Identity Online) certificate, which build a higher entry barrier for new entrants.

Passive sensing with lower

cost structure is feasible

with the right algorithm

Egis is the only non-Apple

fingerprint vendor that has

its own algorithm

05 January 2016

Egis Technology Inc.

(6462.TWO / 6462 TT) 14

Figure 31: Integration of payment APK and design complexity lead to higher entry barrier

Source: Egis

Egis' proprietary algorithm supports (1) small size fingerprint matching and (2) 360-degree

matching, especially for area-type sensors that are adopted for mobile payment

applications. Egis signed licensing agreements with Synaptics and Samsung in 2015, and

its algorithm has been used on Samsung’s flagship smartphone with Synaptics’ sensor.

Egis also started to develop its own sensor chip from 2014 and already have commenced

shipments for Chinese smartphone customers in 2H15. We believe Egis is the only

fingerprint solution provider for the non-Apple camp that can provide its own sensor, and

has a proven record and experience for the payment algorithm.

Figure 32: Egis is the only non-Apple fingerprint sensor supplier that has proven experience of its own algorithm

Apple

(AuthenTec)

Synaptics

(Validity)

Fingerprint

Cards

IDEX Egistec Goodix Silead Elan FocalTech

Country US US Sweden Norway Taiwan China China Taiwan Taiwan

Technology Active Active Active Active Passive Active Active Active/Passive Active/Passive

Area/Swipe Area Area/Swipe Area/Swipe Area/Swipe Area/Swipe Area Area Area/Swipe Area/Swipe

Algorithm In-house Egis, In-

house

Precise

Biometric

3rd

party In-house In-house Precise

Biometric

Precise

Biometric

Precise

Biometric

Main market Internal use Samsung China Asia China

Korea

China China China/Taiwan China

Source: Company data

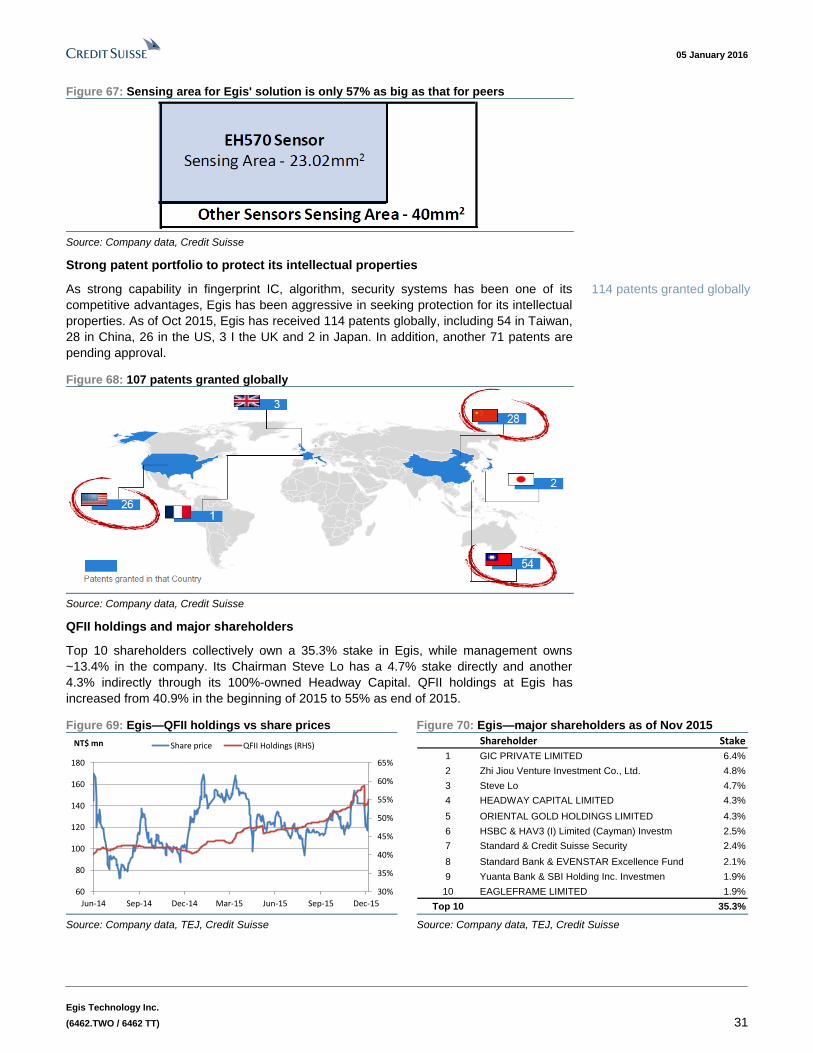

EGIS’ know-how and solid IP portfolio will help it to gain shares in 2016-17

EGIS was established in Dec 2007 by acquiring LighTuning (sensor maker), ABIG

(algorithm provider), and HiTrust (encryption and security). Notably, ABIG was founded in

2000 with customers including AuthenTec (acquired by Apple in 2012), UPEK (acquired by

AuthenTec in 2010), and Validity (acquired by Synaptics in 2013). According to Egis, it has

a total of 157 patents granted with 114 patents remaining active (107 invention patents,

seven utility patents) as of October 2015. Egis claims it has 26 fingerprint-related patents

granted in the US versus 32 for Synaptics and nine for FPC. Its patents cover chip design,

packaging technology, image capture, algorithm, firmware, mobile payment,

encryption, etc.

We estimate non-Apple fingerprint sensor shipment will grow by 105% and 61% in 2016

and 2017, respectively. Given the potential patent infringement concerns for late comers

on active sensing, we believe Egis is a good second source partner for the top-tier non-

Apple smartphone makers (Samsung, Lenovo/Motorola) and Chinese brands (Huawei,

ZTE, Xiaomi, Gionee, TCL, etc) which has a sizeable overseas business. Egis’ passive

Egis has strong IP and

know-how for fingerprint

05 January 2016

Egis Technology Inc.

(6462.TWO / 6462 TT) 15

sensing technology has less complicated wafer processing and smaller die size, which

lead to a more competitive cost structure versus its peers. We also believe its proprietary

sensing, feature extracting, and algorithm know-how on mobile payment should help it to

secure more new design-wins in 2016-17.

Figure 33: Egis has 114 active patents globally with 26 granted in the US

Source: Company data

New entrants try to catch up but most lack algorithm or may have IP infringement

issues

Besides Egis, several other new fingerprint solution providers in Taiwan and China are

trying to enter this hyper growth market. However, most source fingerprint algorithms from

Precise Biometrics and are adopting active sensing technology, which might have

potential IP infringement issues.

Elan: Elan started to develop its own fingerprint sensor in 2H14 and allied with Startek for

algorithm. Its initial target was to start shipments in mid-2015 with swipe fingerprint sensor

but it decided to shift its focus to area-type in early 2015. Given that Finger Print Card

(with algorithm from Precise Biometrics) dominated more than 90% of the market in China,

it signed a licensing agreement with Precise Biometrics in August 2015. Elan has

submitted their sample to several Asian smartphone brands and Asus. We think it could

enter Asus' supplychain and start shipment from 2Q16.

Elan's fingerprint sensor adopts a hybrid solution, i.e., active and passive, which it believes

can avoid potential patent infringement issues. It has a flexible business model as it could

provide wafer, packaged strip, or module, depending on customers' requirement.

Management believe fingerprint business should be accretive to its corporate gross margin.

FocalTech: FocalTech announced in 3Q14 that it plans to enter the fingerprint market by

sourcing fingerprint ICs from third parties (IMD and IDEX) with its own algorithm.

Nevertheless, the progress has been slow due to higher chip cost and higher entry barrier

on algorithm for mobile payment. It decided to develop its own fingerprint chip in 2H15 and

signed a licensing agreement with Precise Biometrics in December 2015. It plans to have

its chip ready for sampling in 1H16 and we targets for shipment take-off by 2H16.

FocalTech's fingerprint sensors will adopt active sensing but it plans to remove the metal

ring to minimise the IP infringement risk. Nevertheless, the company said it will still target

Chinese brands and whitebox makers initially.

Goodix: Goodix has already received several designs in China, such as Dove L5 Pro,

LeTV 1S, ZTE Blade S7, Vivo X6, and Meizu MX4 Pro and commenced shipment in 2015.

Elan, FocalTech, and Silead

all license algorithm from

Precise Biometrics

05 January 2016

Egis Technology Inc.

(6462.TWO / 6462 TT) 16

Goodix has adopted active sensing structure and developed its own algorithm, but most of

the branded smartphone makers or those focused on overseas market still have concerns

on potential IP infringement issues. Goodix is also working on under-glass sensing

solutions with leading touch module maker.

Silead: Silead is a subsidiary of GalaxyCore and focus touch IC, stylus, and fingerprint

sensors. It also licenses the algorithm from Precise Biometrics and adopts active sensing

structure. Its fingerprint solutions have been adopted by several whitebox makers in 2H15

and it plans to further support payment applications in 2016.

Fingerprint value chain and technology are still

evolving

Fingerprint sensor supply chain involves four major parts: chip, algorithm, semiconductor

foundries, and module makers. Most fingerprint sensors today adopt a sensor-on-chip

design are manufactured on 8” 0.18um process with LGA packaging. Our analysis

suggests fingerprint sensor chip accounts for 50-60% of over the BOM cost, and the

remaining 40-50% are for module assembly material/process (cover glass, coating,

connector, assembly, etc). Module assembly is an important and critical process since the

fingerprint module will appear on the outer parts of the devices and needs to match the

overall industrial design (shape, position, colour, etc).

We estimate the square/round shape of fingerprint chip ASP of US$4-7 (die and LGA

packaging) in 2H15 but will fall to US$3-5 in 2H16-2017 as more suppliers enter the

market. We also believe the overall module cost for square/round shape will fall to US$4-7

by 2H16-2017 from current US$6-10.

Figure 34: Design process flow on fingerprint sensor selection

Decide location Decide shapeDecide

coating/cover glass

Decide hardware

platform

Decide operating

system

Decide

algorithm

Decide payment

system/platformIntegration and testing

Source: Company data

Figure 35: Cost structure analysis of different types of

fingerprint modules (3Q15)

Figure 36: Stack up of different fingerprint sensor

modules

$0

$2

$4

$6

$8

$10

$12

Rectangle(hard coating)

Rectangle(cover glass)

Rectangle(sapphire)

Square/Round(hard coating)

Square/Round(cover glass)

Square/Round(sapphire)

Chip Package (LGA) FPC Protection coating/cover Connector/others Gross profit

Coating solution

Matte/Glossy Ceramic Glass Sapphire

Total

thickness160um 180um 300um 350um

Cover solution

Source: IHS, Credit Suisse estimates Source: Elan

Fingerprint ASP to decline in

2016-17E on cost reduction

and competition

05 January 2016

Egis Technology Inc.

(6462.TWO / 6462 TT) 17

Capacitive fingerprint sensing has better cost

structure versus other biometric identification

technologies

Biometric identification has become one of the new features for non-Apple smartphone

brands, especially after Samsung also adopted fingerprint sensor on its flagship models in

March 2015. Fingerprint sensing has several different detecting technologies including

optical, capacitive, and ultrasonic, but we believe capacitive fingerprint sensing is the most

mature and has better cost structure versus others.

Ultrasonic fingerprint sensing still not mature

We noted that Sonavation and Qualcomm have introduced ultrasonic fingerprint sensing

technology for mobile devices in 2015. Ultrasonic sensing has the advantage of achieving

under-glass sensing without changing industrial design of the cover glass, although capacitive

fingerprint makers are also developing similar solution. Comparing with capacitive fingerprint

sensing, ultrasonic sensing in theory should have better performance as it can sense

fingerprints even with dirty or sweaty fingers. However, we believe this technology still

requires a more complicated sensing mechanism to solve the higher noise level & more

complex data processing. We believe it might still take some more time before this technology

becomes more mature. Nevertheless, ultrasonic fingerprint sensing will still require algorithm

for fingerprint matching, hence should be less negative for Egis if it takes off.

Figure 37: Sonavation's ultrasonic fingerprint sensing

structure

Figure 38: Qualcomm also introduced its ultrasonic

fingerprint technology

Source: Sonavation Source: Qualcomm

Other biometric identification technologies are not suitable for mobile payment and

smart card applications

Other than fingerprint sensing, competing technologies for biometric identification include

eyeprint recognition, iris recognition, vein recognition, etc. EyeVerify’s Eyeprint ID detects

the eye veins and other micro features in and around the eye with the front camera. It

received multiple design wins from Alcatel (Idol 3), Vivo (X5 Pro) etc, after it being adopted

by ZTE’s Grand S III smartphone in March 2015. We believe eyeprint detection has the

lowest hardware requirement as it uses the existing front camera, but has the

disadvantages of potentially impacted by surrounding lights, weaker user experience, and

cannot be used on smart cards.

Iris and blood vein recognition both has higher security level than fingerprint and are being

used on government and high-end banking applications, but both require usage of infrared

light for detection. We believe the cost addition and user acceptance on using iris/blood

vein recognition will limit the adoption on mobile payment and smart card.

As a result, we believe capacitive fingerprint sensing is the most mature and has better

cost structure versus other biometric identification technologies on mobile devices and

smart cards.

Ultrasonic sensing

is still not mature

Iris and blood vein has

higher security but might not

be suitable on mobile

devices

05 January 2016

Egis Technology Inc.

(6462.TWO / 6462 TT) 18

Figure 39: Comparison of different biometric identification technologies

Capacitive

fingerprint

Ultrasonic

fingerprint

Eyeprint Iris Blood vein

Security High High Medium Very high High

Cost Low Medium Low High High

Form factor Small Small Small Large Large

User experience Good Good Medium Medium Good

Source: Company data, Credit Suisse

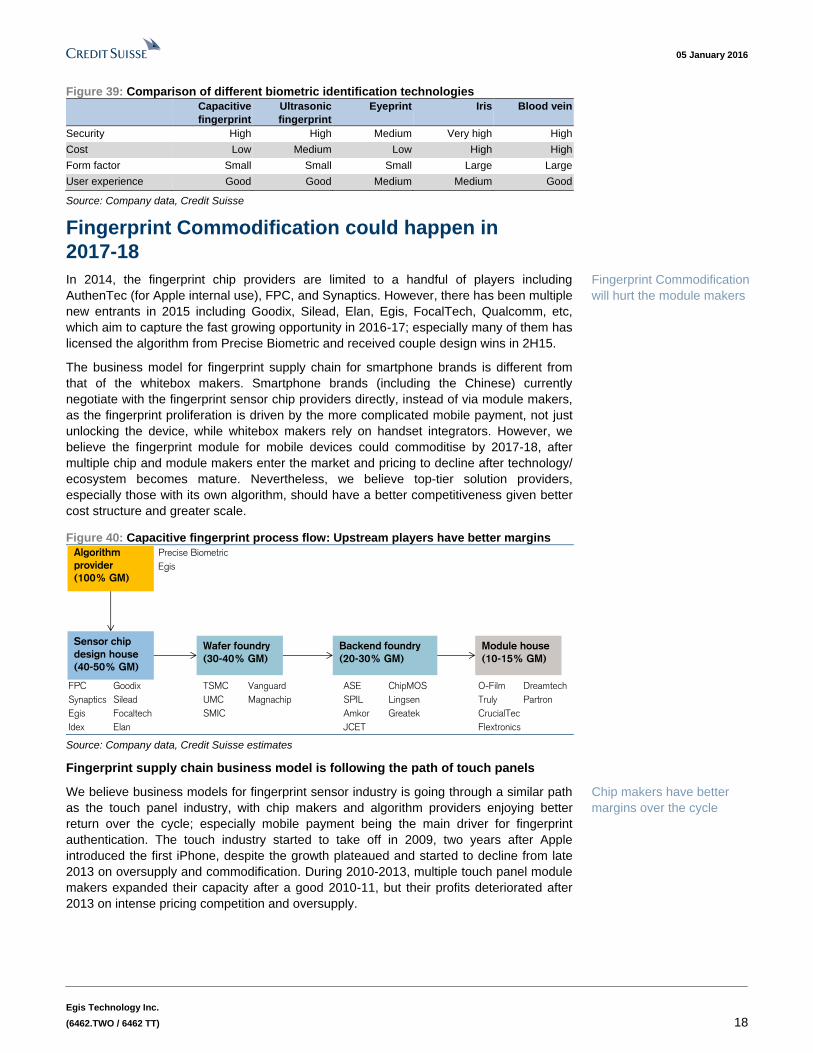

Fingerprint Commodification could happen in

2017-18

In 2014, the fingerprint chip providers are limited to a handful of players including

AuthenTec (for Apple internal use), FPC, and Synaptics. However, there has been multiple

new entrants in 2015 including Goodix, Silead, Elan, Egis, FocalTech, Qualcomm, etc,

which aim to capture the fast growing opportunity in 2016-17; especially many of them has

licensed the algorithm from Precise Biometric and received couple design wins in 2H15.

The business model for fingerprint supply chain for smartphone brands is different from

that of the whitebox makers. Smartphone brands (including the Chinese) currently

negotiate with the fingerprint sensor chip providers directly, instead of via module makers,

as the fingerprint proliferation is driven by the more complicated mobile payment, not just

unlocking the device, while whitebox makers rely on handset integrators. However, we

believe the fingerprint module for mobile devices could commoditise by 2017-18, after

multiple chip and module makers enter the market and pricing to decline after technology/

ecosystem becomes mature. Nevertheless, we believe top-tier solution providers,

especially those with its own algorithm, should have a better competitiveness given better

cost structure and greater scale.

Figure 40: Capacitive fingerprint process flow: Upstream players have better margins

Precise Biometric

Egis

FPC Goodix TSMC Vanguard ASE ChipMOS O-Film Dreamtech

Synaptics Silead UMC Magnachip SPIL Lingsen Truly Partron

Egis Focaltech SMIC Amkor Greatek CrucialTec

Idex Elan JCET Flextronics

Algorithm

provider

(100% GM)

Sensor chip

design house

(40-50% GM)

Wafer foundry

(30-40% GM)

Backend foundry

(20-30% GM)

Module house

(10-15% GM)

Source: Company data, Credit Suisse estimates

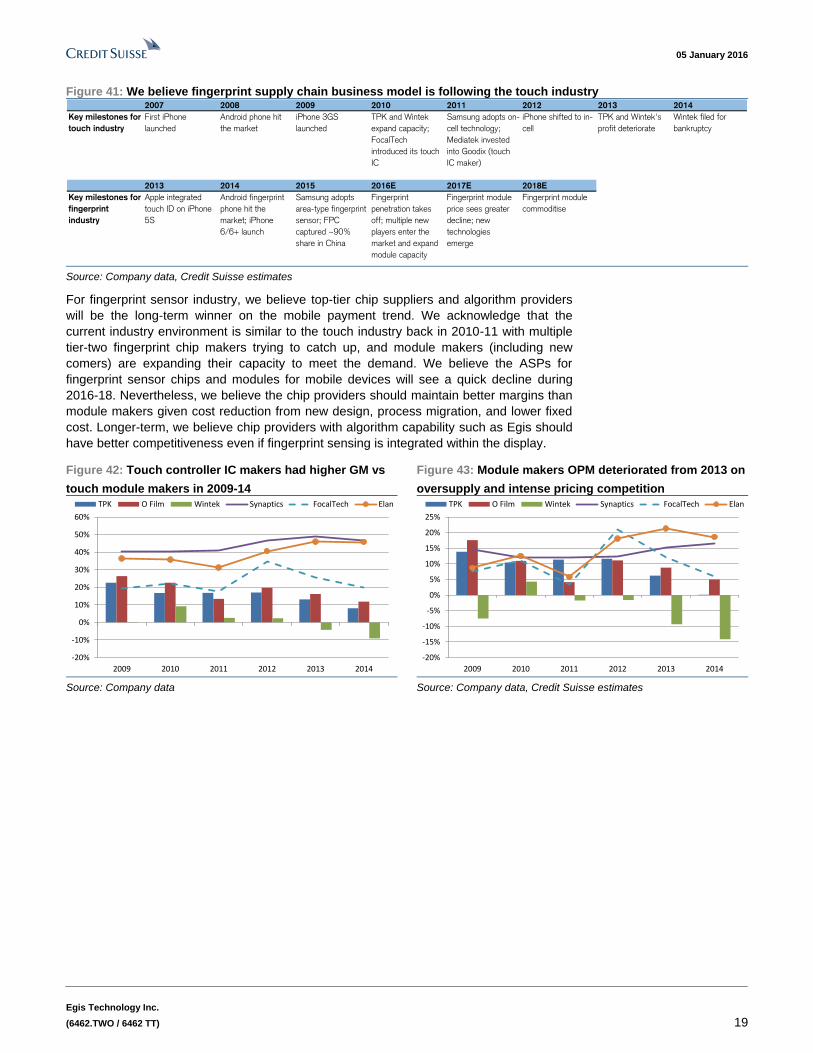

Fingerprint supply chain business model is following the path of touch panels

We believe business models for fingerprint sensor industry is going through a similar path

as the touch panel industry, with chip makers and algorithm providers enjoying better

return over the cycle; especially mobile payment being the main driver for fingerprint

authentication. The touch industry started to take off in 2009, two years after Apple

introduced the first iPhone, despite the growth plateaued and started to decline from late

2013 on oversupply and commodification. During 2010-2013, multiple touch panel module

makers expanded their capacity after a good 2010-11, but their profits deteriorated after

2013 on intense pricing competition and oversupply.

Fingerprint Commodification

will hurt the module makers

Chip makers have better

margins over the cycle

05 January 2016

Egis Technology Inc.

(6462.TWO / 6462 TT) 19

Figure 41: We believe fingerprint supply chain business model is following the touch industry 2007 2008 2009 2010 2011 2012 2013 2014

Key milestones for

touch industry

First iPhone

launched

Android phone hit

the market

iPhone 3GS

launched

TPK and Wintek

expand capacity;

FocalTech

introduced its touch

IC

Samsung adopts on-

cell technology;

Mediatek invested

into Goodix (touch

IC maker)

iPhone shifted to in-

cell

TPK and Wintek's

profit deteriorate

Wintek filed for

bankruptcy

2013 2014 2015 2016E 2017E 2018E

Key milestones for

fingerprint

industry

Apple integrated

touch ID on iPhone

5S

Android fingerprint

phone hit the

market; iPhone

6/6+ launch

Samsung adopts

area-type fingerprint

sensor; FPC

captured ~90%

share in China

Fingerprint

penetration takes

off; multiple new

players enter the

market and expand

module capacity

Fingerprint module

price sees greater

decline; new

technologies

emerge

Fingerprint module

commoditise

Source: Company data, Credit Suisse estimates

For fingerprint sensor industry, we believe top-tier chip suppliers and algorithm providers

will be the long-term winner on the mobile payment trend. We acknowledge that the

current industry environment is similar to the touch industry back in 2010-11 with multiple

tier-two fingerprint chip makers trying to catch up, and module makers (including new

comers) are expanding their capacity to meet the demand. We believe the ASPs for

fingerprint sensor chips and modules for mobile devices will see a quick decline during

2016-18. Nevertheless, we believe the chip providers should maintain better margins than

module makers given cost reduction from new design, process migration, and lower fixed

cost. Longer-term, we believe chip providers with algorithm capability such as Egis should

have better competitiveness even if fingerprint sensing is integrated within the display.

Figure 42: Touch controller IC makers had higher GM vs

touch module makers in 2009-14

Figure 43: Module makers OPM deteriorated from 2013 on

oversupply and intense pricing competition

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

2009 2010 2011 2012 2013 2014

TPK O Film Wintek Synaptics FocalTech Elan

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

2009 2010 2011 2012 2013 2014

TPK O Film Wintek Synaptics FocalTech Elan

Source: Company data Source: Company data, Credit Suisse estimates

05 January 2016

Egis Technology Inc.

(6462.TWO / 6462 TT) 20

Fingerprint embedded within display will be an opportunity rather than a threat for Egis We believe capacitive fingerprint sensor will be the mainstream for mobile devices in the

next two to three years given the mature ecosystem and lower cost structure. However, on

a longer-term basis, we see the possibility that the fingerprint sensing function could be

integrated onto display panels.

Apple filed patents with fingerprint sensor integrated into the display module

According to Apple’s patent filings, it may plan to integrate fingerprint and the touch onto a

full panel fingerprint sensor, which carries both fingerprint and touch sensing functions. It

also mentioned in the filing that fingerprint sensing technology could be capacitive,

ultrasonic, optical, infrared, thermal, etc, and the fingerprints can be acquired at the same

time. If Apple or other display makers can successfully integrate fingerprint sensing into

the display module, we believe it could negatively impact module makers’ value-adds,

where we believe it will be negative for pure fingerprint module assembler but positive for

display/touch makers.

Figure 44: Apple may plan to integrate fingerprint onto the display…

Source: Company data, USPTO

AUO also developed display panel that embedded fingerprint sensing

AUO has showcased a 2.8” QVGA mobile display with image and fingerprint scanning

technology with sensing resolution of 288 PPI in 2008. In 2014 Touch Taiwan Exhibition, it

showcased a 4.3” display with fingerprint sensing resolution of 500 PPI and is able to scan

multiple fingerprints simultaneously. Although the embedded fingerprint display technology

is not mature now, we believe it could be disruptive technology once it commercialise.

Figure 45: AUO already showcased a 2.8"

QVGA panel with fingerprint scanning (288

PPI) in 2008

Figure 46: AUO introduced 4.3" display

with 500 PPI resolution fingerprint

scanning in 2014

Source: Company data Source: Company data

Fingerprint and touch

embedded display is still

under development

05 January 2016

Egis Technology Inc.

(6462.TWO / 6462 TT) 21

Implications to Egis and the fingerprint supply chain

We believe pure fingerprint module makers could be the most vulnerable if fingerprint

sensor is being integrated into the display or touch module. Under this scenario, the value-

add will shift to touch panel or display makers from module makers, but will still require

processing chip and algorithm for matching. If the fingerprint sensor is embedded into the

TFT process like in-cell touch, then we believe it will negatively impact fingerprint and

touch module makers’ business but would still require processing chips and algorithms. As

a result, we believe the impact for Egis is minimal as it can work with touch or panel

makers by providing processing chip and algorithm. Moreover, as all the panel makers are

in Asia and full display fingerprint sensing could be more complicated, we believe the

integration trend should be viewed as an opportunity rather than a threat to Egis.

Full display fingerprint

sensing could be more

complicated and might

require a more powerful

IC/algorithm

05 January 2016

Egis Technology Inc.

(6462.TWO / 6462 TT) 22

Higher growth and entry barrier support valuation Egis has turned (operating) profitable in 3Q15, thanks to the algorithm licensing income

from Samsung. Its gross margin of 82.9% in 9M15 were mainly due to higher mix of

licensing income (55-60%), while its GM for fingerprint sensor of 35-50% (some shipments

in the form of module are lower) is in line with industry average. We believe the

proliferation of fingerprint sensors on mobile devices, customers’ demand for dual

sourcing, and Egis’ strong know-how/IP on passive sensing and algorithm should drive its

revenue and earnings growth in 2016-17. Longer-term, we believe the opportunity on

smart card/credit card could be the next growth driver.

Figure 47: Egis' quarterly revenue versus GM Figure 48: Egis' revenue to see strong growth in 2016-17E

-10%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0

50

100

150

200

250

300

1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15

NT$ mn Revenue GM (RHS)

206 139 84 45 516

2,439

6,236

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

2011 2012 2013 2014 2015E 2016E 2017E

NT$ mn Revenue

Source: Company data Source: Company data, Credit Suisse estimates

Entering Samsung supply chain as a second source

in 2016

We model Egis’ revenue to take off from 2H16, as we believe it could start shipment for

Samsung’s mid-range products and receives more design wins from Chinese smartphone

makers. Samsung’s Galaxy S6 adopted fingerprint sensor from Synaptics with Egis’

algorithm since 1Q15 and Egis has recognized decent licensing income from 2Q15. Egis

also submitted its own fingerprint sensor to Samsung for qualification, and we believe it’s

likely that Samsung will use Egis as a second source for the fingerprint solution on the

mid-range A series models. Therefore, we estimate Egis to capture 15-20% allocation at

Samsung’s A series models in 2H16 and could increase to 20-25% in 2017.

Samsung has been developing its algorithm internally and plans to adopt it on the next

generation of Galaxy S7 models in 2016. Although it is unclear whether Samsung can

successfully implement its own algorithm, we conservatively assume that Egis’ licensing

income from Samsung will end from 2Q16.

China poses a greater opportunity for Egis

We believe China will be the main growth driver for Egis in 2016-17, given increasing

adoption of fingerprint on mobile devices, fast growth of mobile payments, and the push by

multiple payment platforms including Apple Pay, Samsung Pay, Alipay, ZTE Pay, etc. We

estimate China and other brands' smartphone fingerprint unit demand of 251 mn and 435

mn units in 2016 and 2017, representing the adoption rate of 27% and 44%, respectively.

We believe Egis’ superior design capability and its proprietary algorithm know-how will

lead to a much better cost structure versus peers.

Egis has already started shipment to several Chinese smartphone makers such as ZTE,

Xiaolajiao, Haier, Oukitel, etc in 2H15 and we expect it to penetrate to other brands

Egis turned OP profitable

in 3Q15

Egis to become the second

source for Samsung's mid-

range products in 2H16

Egis is adding design-wins

in China

05 January 2016

Egis Technology Inc.

(6462.TWO / 6462 TT) 23

including tier ones such as Huawei, Xiaomi, Lenovo/Motorola, etc. Our checks suggest it

has partnered with fingerprint and touch module makers, which we believe should also

help Egis capture tier-two brands and the whitebox market. Although FPC dominated the

fingerprint market for China/others smartphone with over 90% market share in 2015 and

will remain the leader in 2016, we still expect Egis to catch up with ~10% and ~20% share

in 2016 and 2017, respectively.

Figure 49: Egis' fingerprint IC has been adopted by several Chinese brands Brand ZTE ZTE Xiaolajiao Philips Haier Calme Oukitel

Model name Nubia Z9 Weiwu 3 Red Pepper X1 i999 I701 CM7 U9

Fingerprint sensor Egis Egis Egis Egis Egis Egis Egis

algorithm Egis Egis Egis Egis Egis Egis Egis

Location Side Back Back Back Back Back Back Source: Company data

Algorithm and better design to protect GM

We model Egis’ fingerprint sensor chip shipment of 24 mn units in 2016 for 6% market

share at non-Apple camp, and will further grow to 85 mn units in 2017 for 14% market

share. We noted that there are several chip design houses in Taiwan and China that have

developed their own fingerprint solutions, but we would point out that Egis is the only one

that can provide both algorithm and chip and has a proven track record on algorithm with

Samsung. Egis' unique passive sensing structure also has the least issue on violating

Apple/AuthenTec's IPs, which is one of the concerns for top Chinese brands as they are

shifting their focus to the export market.

Figure 50: Egis' smartphone fingerprint shipment growth is driven by share gain at Samsung and China

mn units 2014 2015E 2016E 2017E 2018E

Samsung shipments 318 330 340 345 350

Fingerprint penetration 14% 27% 39% 54% 65%

Samsung fingerprint shipments 45 89 133 186 228

Egis market share at Samsung 0% 0% 4% 6% 8%

Egis smartphone fingerprint shipments to Samsung - - 5 11 18

China and others smartphone shipments 793 873 941 979 1,019

Fingerprint penetration 3% 11% 27% 44% 54%

China/others fingerprint shipments 26 99 251 435 545

Egis market share at China/Others 0% 1% 8% 17% 23%

Egis smartphone fingerprint shipments to China/Others - 1 19 74 127

Non-Apple smartphone fingerprint shipments 71 188 385 621 774

Non-Apple smartphone fingerprint penetration 6% 16% 30% 47% 57%

Egis fingerprint shipments - 1 24 85 145

Egis total market share at non-Apple brands 0% 1% 6% 14% 19%

Source: Company data, Credit Suisse estimates

In terms of pricing, we expect the fingerprint module ASP to fall from current US$6-10 to

US$4-7 by 2H16-2017, and chip ASP to reach US$3-5 in 2H16-2017 versus current

US$4-7 (die and LGA packaging) as more suppliers enter the market. As a result, we

forecast Egis' revenue of NT$2,439 mn in 2016 and NT$6,236 mn in 2017 (versus

NT$516 mn in 2015). We have not included the potential revenue contribution from smart

cards in our 2016-17 revenue assumptions.

Having its own algorithm

can help GM by 4-7%

05 January 2016

Egis Technology Inc.

(6462.TWO / 6462 TT) 24

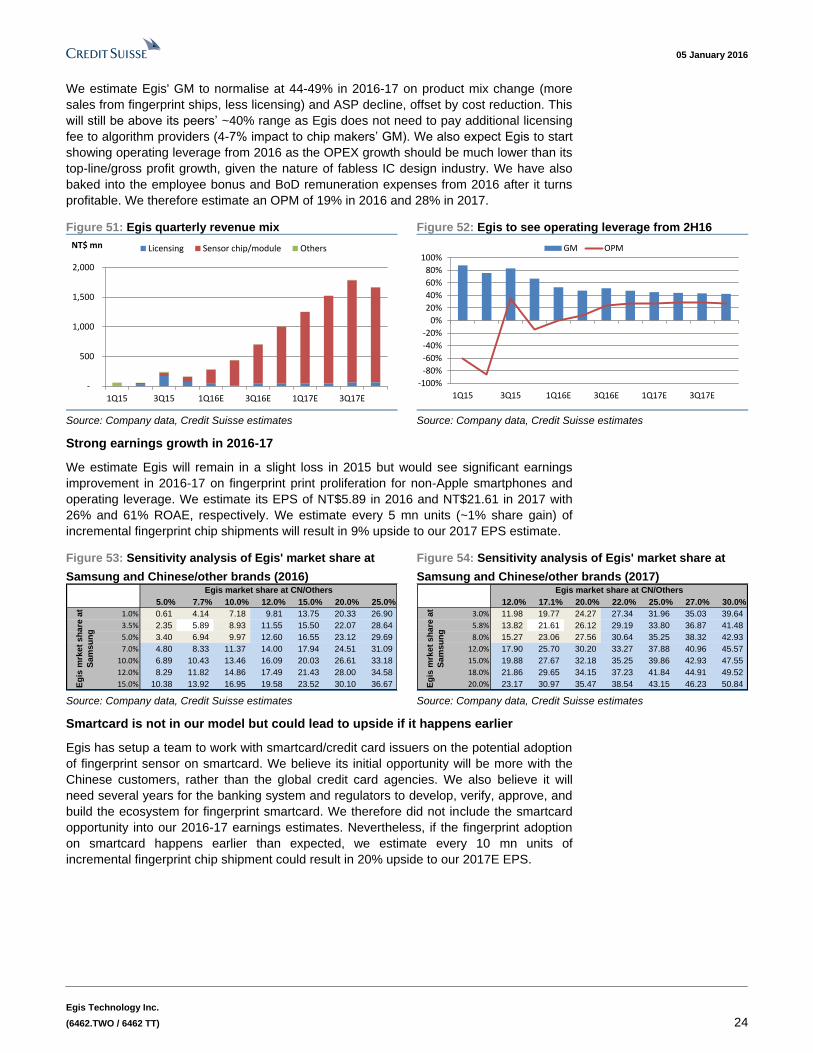

We estimate Egis' GM to normalise at 44-49% in 2016-17 on product mix change (more

sales from fingerprint ships, less licensing) and ASP decline, offset by cost reduction. This

will still be above its peers’ ~40% range as Egis does not need to pay additional licensing

fee to algorithm providers (4-7% impact to chip makers’ GM). We also expect Egis to start

showing operating leverage from 2016 as the OPEX growth should be much lower than its

top-line/gross profit growth, given the nature of fabless IC design industry. We have also

baked into the employee bonus and BoD remuneration expenses from 2016 after it turns

profitable. We therefore estimate an OPM of 19% in 2016 and 28% in 2017.

Figure 51: Egis quarterly revenue mix Figure 52: Egis to see operating leverage from 2H16

-

500

1,000

1,500

2,000

1Q15 3Q15 1Q16E 3Q16E 1Q17E 3Q17E

NT$ mn Licensing Sensor chip/module Others

-100%

-80%

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

1Q15 3Q15 1Q16E 3Q16E 1Q17E 3Q17E

GM OPM

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

Strong earnings growth in 2016-17

We estimate Egis will remain in a slight loss in 2015 but would see significant earnings

improvement in 2016-17 on fingerprint print proliferation for non-Apple smartphones and

operating leverage. We estimate its EPS of NT$5.89 in 2016 and NT$21.61 in 2017 with

26% and 61% ROAE, respectively. We estimate every 5 mn units (~1% share gain) of

incremental fingerprint chip shipments will result in 9% upside to our 2017 EPS estimate.

Figure 53: Sensitivity analysis of Egis' market share at

Samsung and Chinese/other brands (2016)

Figure 54: Sensitivity analysis of Egis' market share at

Samsung and Chinese/other brands (2017)

5.89 5.0% 7.7% 10.0% 12.0% 15.0% 20.0% 25.0%

1.0% 0.61 4.14 7.18 9.81 13.75 20.33 26.90

3.5% 2.35 5.89 8.93 11.55 15.50 22.07 28.64

5.0% 3.40 6.94 9.97 12.60 16.55 23.12 29.69

7.0% 4.80 8.33 11.37 14.00 17.94 24.51 31.09

10.0% 6.89 10.43 13.46 16.09 20.03 26.61 33.18

12.0% 8.29 11.82 14.86 17.49 21.43 28.00 34.58

15.0% 10.38 13.92 16.95 19.58 23.52 30.10 36.67

Egis market share at CN/Others

Eg

is m

rket

sh

are

at

Sam

su

ng

21.61 12.0% 17.1% 20.0% 22.0% 25.0% 27.0% 30.0%

3.0% 11.98 19.77 24.27 27.34 31.96 35.03 39.64

5.8% 13.82 21.61 26.12 29.19 33.80 36.87 41.48

8.0% 15.27 23.06 27.56 30.64 35.25 38.32 42.93

12.0% 17.90 25.70 30.20 33.27 37.88 40.96 45.57

15.0% 19.88 27.67 32.18 35.25 39.86 42.93 47.55

18.0% 21.86 29.65 34.15 37.23 41.84 44.91 49.52

20.0% 23.17 30.97 35.47 38.54 43.15 46.23 50.84

Egis market share at CN/Others

Eg

is m

rket

sh

are

at

Sam

su

ng

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

Smartcard is not in our model but could lead to upside if it happens earlier

Egis has setup a team to work with smartcard/credit card issuers on the potential adoption

of fingerprint sensor on smartcard. We believe its initial opportunity will be more with the

Chinese customers, rather than the global credit card agencies. We also believe it will

need several years for the banking system and regulators to develop, verify, approve, and

build the ecosystem for fingerprint smartcard. We therefore did not include the smartcard

opportunity into our 2016-17 earnings estimates. Nevertheless, if the fingerprint adoption

on smartcard happens earlier than expected, we estimate every 10 mn units of

incremental fingerprint chip shipment could result in 20% upside to our 2017E EPS.

05 January 2016

Egis Technology Inc.

(6462.TWO / 6462 TT) 25

Figure 55: China's credit and banking cards saw

significant growth in the past few years

Figure 56: Egis' GM should be better than its Taiwanese

fabless IC peers

2,000

2,500

3,000

3,500

4,000

4,500

5,000

5,500

2011 2012 2013 2014 3Q15

mn units

20%

25%

30%

35%

40%

45%

50%

55%

60%

2014 2015E 2016E 2017E

Egis Mediatek Realtek

Elan FocalTech non-DDI Novatek non-DDI

77.8%

Source: PBOC Source: Company data, Credit Suisse estimates

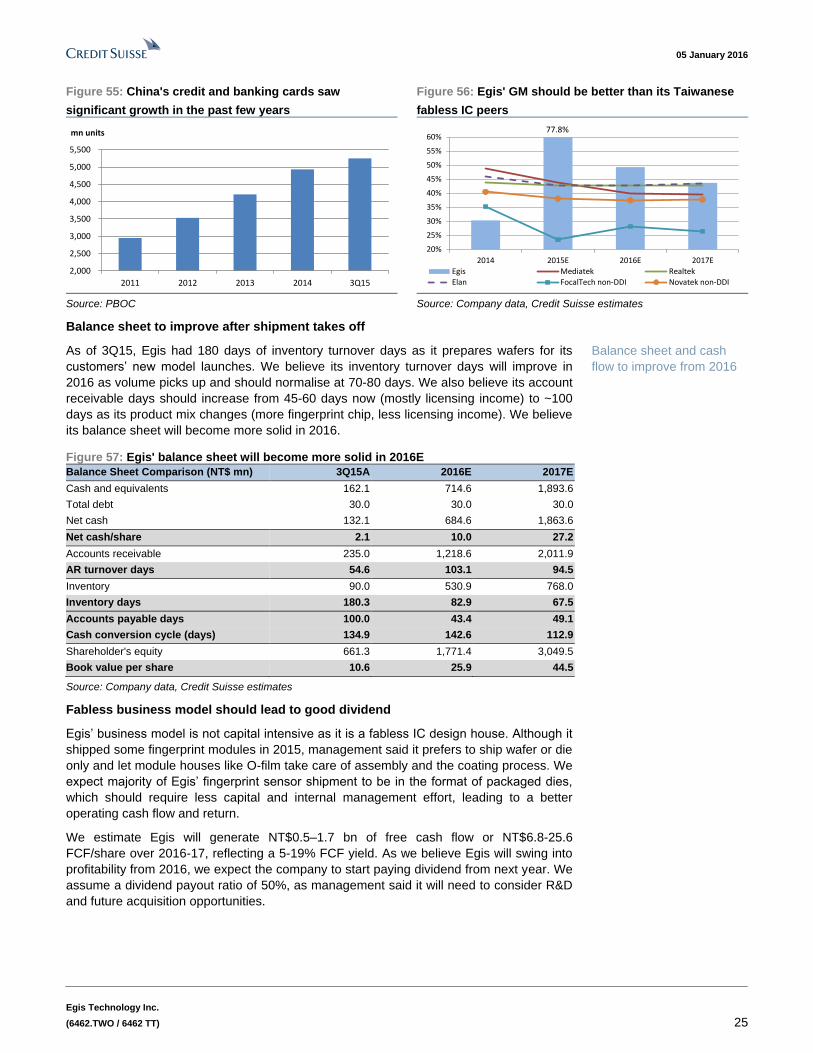

Balance sheet to improve after shipment takes off

As of 3Q15, Egis had 180 days of inventory turnover days as it prepares wafers for its

customers’ new model launches. We believe its inventory turnover days will improve in

2016 as volume picks up and should normalise at 70-80 days. We also believe its account

receivable days should increase from 45-60 days now (mostly licensing income) to ~100

days as its product mix changes (more fingerprint chip, less licensing income). We believe

its balance sheet will become more solid in 2016.

Figure 57: Egis' balance sheet will become more solid in 2016E

Balance Sheet Comparison (NT$ mn) 3Q15A 2016E 2017E