effective for 2008 tax years (returns filed in 2009)

TRANSCRIPT

Effective for 2008 tax years (returns filed in 2009).

Reasons for Redesign

The IRS extensively revised the format and c0ntent of

the form based on three guiding principles:

Enhance TransparencyPromote Tax ComplianceMinimize Burden on the Filing Organization

990-N.pdf

Phased in Over Three YearsBeginning in 2008 tax years, an organization by

file Form 990-EZ if it satisfies both the gross receipts and assets tests:

TAX YEAR Gross Receipts Assets

2008 (Filed 2009) > $25,000 & < $1 mil

< $2.5 mil

2009 (Filed 2010) > $25,000 & < $500,000

< $1.25 mil

2010 and later > $500,000 & < $200,000

< $500,000

f990--dft.pdf

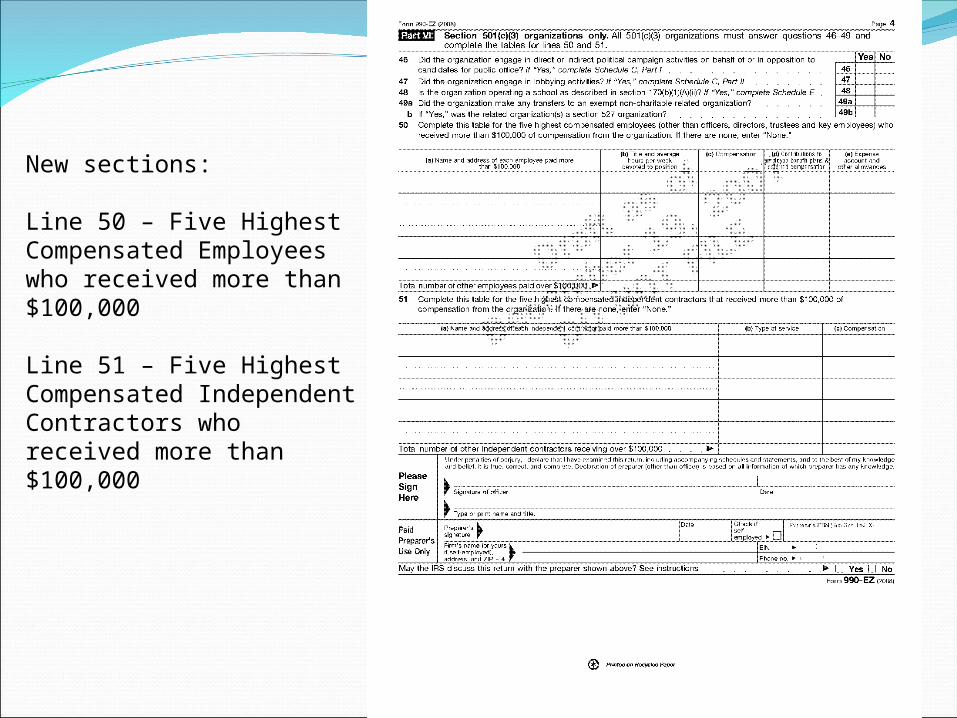

New sections:

Line 50 – Five Highest Compensated Employees who received more than $100,000

Line 51 – Five Highest Compensated Independent Contractors who received more than $100,000

NEW ITEMS TO NOTE:Total Number of Volunteers volgistics.pdf

TIMESHEET.xlsMore Descriptive Organization MissionNo more attachments as the new Form 990

provides Schedules (16)Schedule B - ContributorsSchedule D – Supplemental Financial StatementsSchedule G – FundraisingSchedule J – Compensation InformationSchedule M – Non-Cash Contributions

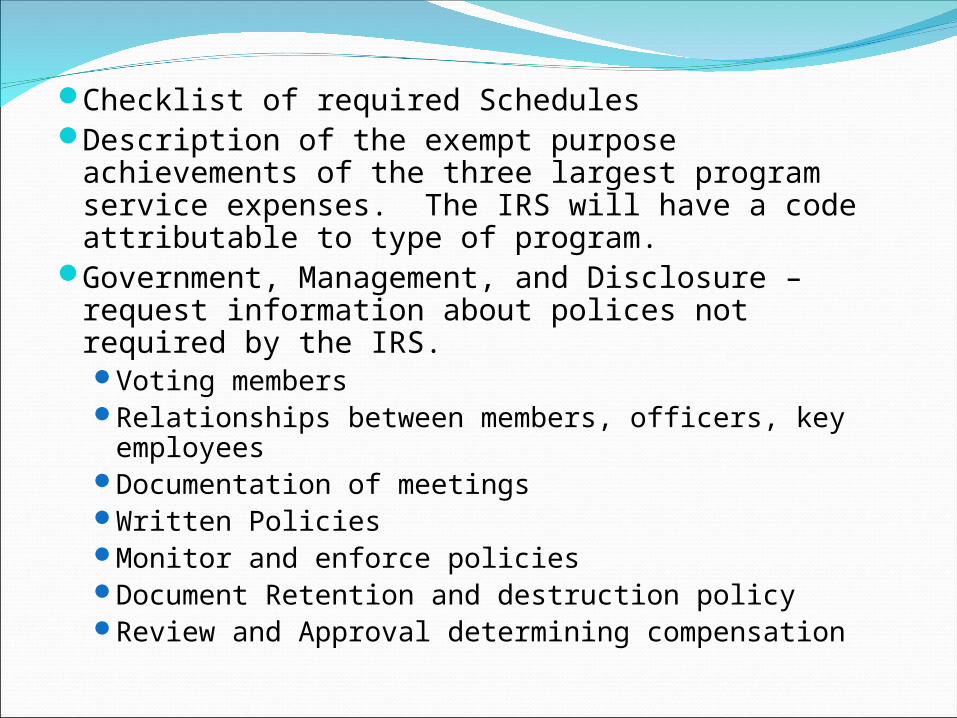

Checklist of required SchedulesDescription of the exempt purpose achievements

of the three largest program service expenses. The IRS will have a code attributable to type of program.

Government, Management, and Disclosure – request information about polices not required by the IRS.Voting membersRelationships between members, officers, key

employeesDocumentation of meetingsWritten PoliciesMonitor and enforce policiesDocument Retention and destruction policyReview and Approval determining compensation

Schedule O – How the Organization makes its governing documents, conflict of interest policy, and financial statements available for public inspection

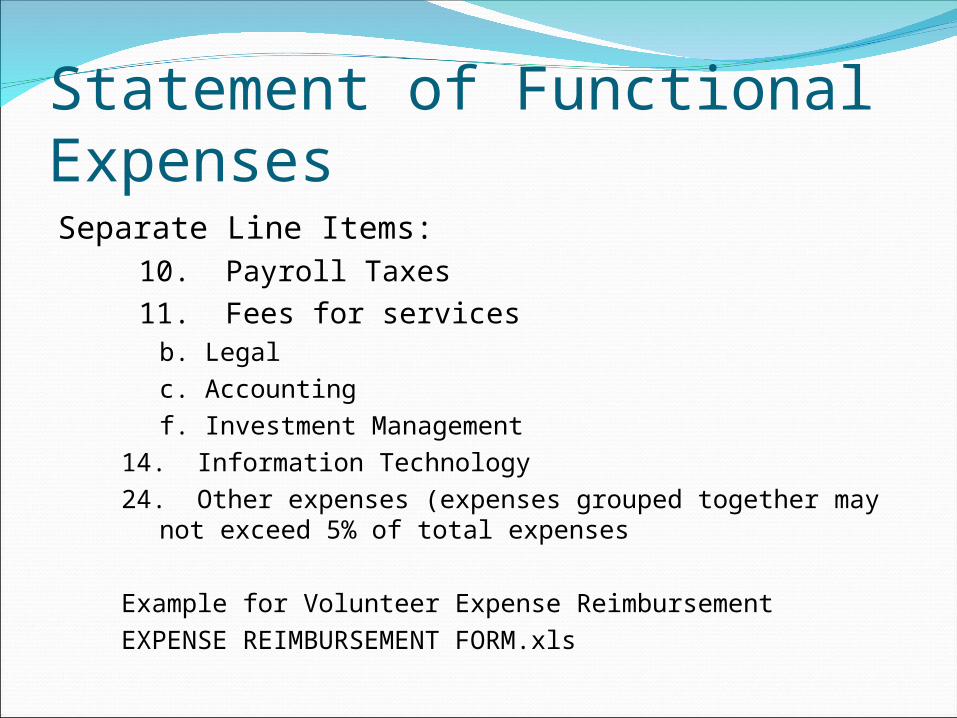

Statement of Functional ExpensesSeparate Line Items:

10. Payroll Taxes11. Fees for services

b. Legalc. Accountingf. Investment Management

14. Information Technology24. Other expenses (expenses grouped together may not

exceed 5% of total expenses

Example for Volunteer Expense ReimbursementEXPENSE REIMBURSEMENT FORM.xls

Balance Sheet

5. Receivables from current and former officers, directors, trustees, key employees or other related parties.

Schedule A (Required for 990-EZ & 990Public Charity Status and Public Support 1. A church, convention of churches, or association

of churches7. An organization that normally receives a

substantial part of its support from a governmental unit or from the general public

Complete support schedule Part II – note includes current year’s activity.

9. An organization that normally receives:(1)more than 331/3% of its support from contributions,

membership fees, and gross receipts from activities related to its exempt functions

(2)no more than 331/3% of its support from gross investment income and unrelated business taxable income

Schedule G Supplemental Information Regarding Fundraising ActivitiesHow you raised the fundsWritten or oral agreement about professional

fundraising activitiesList all states in which organization is registered

or licensed to solicit funds – in NC you must file for a solicitation license with the NC Secretary of State

http://www.secretary.state.nc.us/csl/Download.aspx

Schedule J Compensation Information

Checklist of Fringe Benefits Provided

Follow written policy regarding compensation and fringe benefits

How the organization established the compensation of the organization’s CEO/Executive Director

Checklist of items to provide tax preparer:Trial Balance

Ensure you have line items with the newly required presentation of the Statement of Functional Expenses

General LedgerBank Reconciliations & Bank StatementsRestricted Cash – documentation of restrictionsLoan history to or from employees & officersFixed Asset Inventory including:

Date Placed In ServiceDetail Description of propertyCost Depreciable Life using Straight Line

Loan History with amortization schedules listing

Payment DatesPayment amounts separated by interest &

principal

Grant DocumentsTax Matters Person (Director/Officer signing the

return)Name and Title

Backup of data

Set of Financials

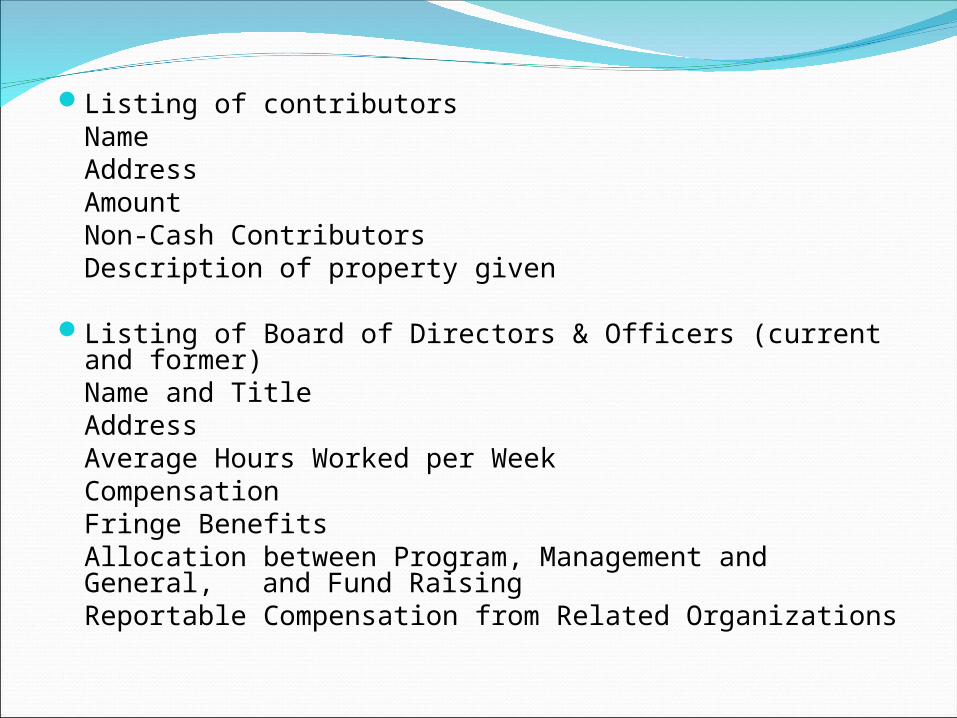

Listing of contributors NameAddressAmountNon-Cash Contributors

Description of property given

Listing of Board of Directors & Officers (current and former)

Name and TitleAddressAverage Hours Worked per WeekCompensationFringe BenefitsAllocation between Program, Management and

General, and Fund RaisingReportable Compensation from Related

Organizations

List of Independent ContractorsNameAddressDescription of ServicesAmount Paid

Minutes from Meetings

Policies and Procedures

TAX DEDUCTIONS FOR VOLUNTEERS

Although you cannot deduct the value of your services given to a qualified organization, you may be able to deduct some amounts you pay in giving services to a qualified organization. The amounts must be:UnreimbursedDirectly connected with the servicesExpenses you had only because of the services

you gave Not personal, living, or family expenses

Conventions – If you are a chosen representative attending a convention of a qualified organization, you can deduct unreimbursed expenses for travel and transportation, including reasonable amount for meals and lodging, while away form home overnight in connection with the convention. Meals are not subject to the same limitations as business related expenses whereas they are limited to 50%.

Record keeping is very important. It is wise to keep original receipts for all expenses incurred while performing volunteer activities for a qualified organization.

Examples of the types of expenditures that volunteers may deduct on their tax returns as itemized deductions include:

Transportation – air and land ( auto mileage is presently .14 cents a mile), rental car, parking, tolls…

Communication – telephone, portion of email expenses attributable to qualified organization, postage…

Supplies purchased to perform volunteer duties Non-cash contributions of property (clothing and household items)

Refer to IRS Publication 526 Charitable Contributions and consult your tax advisor. This publication can be found on the IRS website:

www.irs.gov

Host Families and Tax Treatment Publication 526 Charitable Contributions

Foster ParentsA qualified organization must designate the individuals you take into your home for foster care.

You can deduct expenses that meet both of the following requirements:

1. They are unreimbursed out-of-pocket expenses to feed, clothe, and

care for the foster child.

2. They must be mainly to benefit the qualified organization.

You are not allowed to deduct contributions to a specific individual.

Thank You and Peace Be With You.

Web Sites & Contacts:www.irs.govhttp://www.volgistics.com/0-0.htm

Lida L. Coleman, [email protected](919)968-4911