editorial team - zenith bank - in your best interest team marcel okeke editor eunice sampson deputy...

TRANSCRIPT

EDITORIAL TEAM

MARCEL OKEKEEditor

EUNICE SAMPSONDeputy Editor

ELAINE DELANEYAssociate Editor

CHARLES UJOMUIBRAHIM ABUBAKAR

SUNDAY ENEBELI-UZOROLUWASEUN OLAOYE

Analysts

JOHN LUCKY ETOHProduction Supervisor

SYLVESTER UKUTROTIMI AROWOBUSOYE

Layout/Design

EDITORIAL BOARD OF ADVISERS

UDOM EMMANUELGIDEON JARIKREPAT NWARACHE

OCHUKO OKITI

ZENITH ECONOMIC QUARTERLYis published four times a year

by Zenith Bank Plc.

Printed by PLANET PRESS LTD.Tel 234-1-7731899, 4701279, 08024624306,

E-mail:[email protected]

The views and opinionsexpressed in this journal

do not necessarily reflectthose of the Bank.

All correspondence to:The Editor,

Zenith Economic Quarterly,Research & EIG,Zenith Bank Plc

7th Floor, Zenith HeightsPlot 87, Ajose Adeogun Street,

Victoria Island, Lagos.Tel. Nos.: 2781046-49, 2781064-65

Fax: 2703192.E-mail:[email protected],

[email protected]: 0189-9732

FROM THE MAIL BOXThis contains some of the acknowledg-ments/commendation letters from ourteeming readers across the globe. Pg. 4

PERISCOPEThis is a panoramic analysis of majordevelopments in the economy during theperiod under review and the factorsunderpinning them. Pg. 5

POLICYThis contains the recently published mediumterm expenditure framework and fiscalstrategy paper of the Federal Governmentfor 2012 - 2015. Pg. 14

GOLBAL WATCHAn overview of the global economic growthprospects in 2012 and the factors thatcould hinder growth. Pg. 20

ISSUES (I)An analysis of Nigeria’s budget 2012 andthe issues that must be addressed if theeconomy is to achieve sustainabledevelopment. Pg. 27

ISSUES (II)A critique of Nigeria’s efforts at combatingmoney laundering and the challenges to beaddressed in this regard. Pg. 37

ISSUES (III)Examines the Nigerian rail transport systemwith emphasis on prospects and recentmilestones. Pg. 46

FOREIGN INSIGHTSAn indepth analysis of the global financialmarket, challenges and investment optionsin 2012. Pg. 56

DISCOURSEEvaluates the growing trend of multiplerebranding in the Nigerian corporateenvironment with emphasis on the businessenvironmental factors driving it. Pg. 66

FACTS & FIGURESThis contains economic, financial andbusiness indicators with annotations. Pg. 76

2 Zenith Economic Quarterly January 2012

T

memorial governments have been cheered or jeered based onthe visible improvement or deterioration in the standard ofliving of the citizenry. Yet there has been no fool-proof man-agement or leadership approach in run-ning the economy, whether planned orunplanned, to guarantee the desired im-provement.

This, for most countries includingNigeria, has posed the ever-present chal-lenge of what instruments to deploy inplanning and running the economy toachieve consistent improvement in thequality of life of the citizenry—that iseconomic development—as against theusually superficial economic growth.One critical instrument in Nigeria hasbeen the annual budget—a kind of an-nual plan. This is why our key article on“Nigeria’s Budget 2012: Options forAttaining Sustainable Development”takes a panoramic view of the plan docu-ment that was presented to the NationalAssembly by President GoodluckJonathan in December 2011.

The author recognises that as in thepreceding year, the watch word for thebudget is fiscal consolidation, indicat-ing government’s resolve to cause a change of direction in itsfinances—finance being the life-blood of the annual plan. High-lighted also are the likely risks and challenges of the budgetincluding monetary and fiscal policy disconnect, expenditureoverload, petroleum subsidy conundrum and the usual budgetimplementation drag. All said, the critical and transformationalrole of agriculture is acknowledged; and indeed, flaunted as oneof the trump-cards for attaining most the wholesome objec-tives of the budget.

In a related treatise, focus is directed at the “Railway System:Nigeria’s Neglected Critical Transport Infrastructure”, and thedamaging long neglect of that key haulage facility is deeplyanalysed, just as the renewed attention it is getting in recenttimes is appraised. Thus, the author sums up that it is expectedthat upon the completion of the ongoing resuscitation andmodernization of the rail system, it will become attractive forconcessioning and further investments which will in turn propel

the expansion of the rail system to meet growing demand acrossthe country.

Yet, our concern for the economy moves to the ‘GlobalWatch’ where we raise our apprehension under the rubric: “Glo-bal Economy in 2012: Another Recession Imminent?” Here,the author analyses the economic conditions in the Euro-zone,America, Asia, Latin America, among others, summing up that“even if the global economy manages to escape a full blown

crisis, the world would still grow farweaker than the post 2008-2009 reces-sion levels.” In a related discourse: “2012:Be on High Alert for the Much AwaitedReturn of Global Growth,” our man inLondon holds a similar opinion. Forhim, growth will most certainly not beuniform; some countries will not feel thebenefits of the much promised andmuch awaited global upswing this yearor even next.

In another treatise, we delve into oneof the deliberate efforts of the govern-ment to entrench the culture of due pro-cess, transparency and dignity of labourin the consciousness of the generality ofNigerians. Thus, the article “Due Pro-cess and Transparency: Money Launder-ing” dwells on the most misunderstoodand abused subject of money launder-ing and its ever-spreading tentacles. Theauthor traces the enabling laws, expos-ing the ramifications of the hydra-headedcrime, the local and international dimen-

sions, and its dominant presence in the financial and businessworld.

Other regular sections of the journal also treat a number ofcritical issues including the topic “Economy: Reforms, StabilityPrevails” which is a panoramic view of Nigeria’s economic sec-tors, policies and activities during the relevant period. We alsohave annotated diagrammatic presentation of all the economicindicators under the section ‘Facts & Figures’ as well as the 2012to 2015 expenditure framework and fiscal strategy paper as re-leased by the Federal Government.

This is indeed another rich package for you. It is unputdownable,I promise!

ndoubtedly, economy management has remainedthe most crucial yardstick for gauging the perfor-mance of politicians or governments in all juris-dictions, such that hardly do other indicatorsmatter, when the chips are down. From time im-U

From time immemo-

rial governments

have been cheered

or jeered based on

the visible improve-

ment or deterioration

in the standard of

living of the citizenry.

4 Zenith Economic Quarterly January 2012

I am directed to acknowledge withthanks receipt of your publication,the Zenith Economic QuarterlyZEQ) Vol. & No. 4 October, 2011which focuses on the “SovereignWealth Fund as a DevelopmentImperative”. Zenith EconomicQuarterly (ZEQ) which holds aprominent place in NRC researchlibrary is now a must read Journalby Railway Directors. The Corpo-ration will therefore appreciatethat you retain the NRC on yoursubscription list. Please accept theassurances of the ManagingDirector’s highest regards.W. A. Yinkorefor: Managing Director (NRC)Office of the Managing Di-rectorNigeria Railway Corporation,Lagos

With appreciation, I acknowledgethe receipt of a copy of your Ze-nith Economic Quarterly (ZEQ),Vol. 7, No. 4 of October, 2011,which focuses on the SovereignWealth Fund and the CashlessEconomy, amongst other issues.Your journal is a veritable instru-ment and priceless resource guidefor economic policy and cooper-ate investment. I accept your re-gard and thank you for this valu-able material that I hope wouldprovide useful reference and in-formation to me and my team.Please, accept the assurance of mybest wishes.Chukwuma C. ChinyeCommissionerMinistry of Commerce andIndustryGovernment of Rivers State ofNigeria

I wish to acknowledge withthanks the receipt of the abovemagazine October 2011 editionforwarded to the Mission. Themagazine no doubt, provides criti-cal information on Nigeria and glo-bal economy for strategic policydecisions.Warm regards.A. N. MadubikeFor: High CommissionerHigh Commission of the Fed-eral Republic of Nigeria,Pretoria

I am directed to acknowledge withthanks, receipt if your letter ofthe above subject, dated 28th De-cember 2011 and to inform youthat the High Commissioner ap-preciates the role of the accom-panying magazine in the economicsector of our dear country.Warm regards.J. OlowodahunsiAdministrative Attaché 1For: High CommissionerNigeria High Commission,Kampala-Uganda

I am directed by the AttorneyGeneral & Commissioner for Jus-tice, Mr. Ade Ipaye to acknowl-edge the receipt of your letterdated December 28, 2011 withthe copy of the October,2011 Edition of the ZenithEconomic Quarterly Jour-nal.I am to express the AttorneyGeneral’s appreciation forthe journal and assure you ofhis highest regard.Iyabode OshodiFor: Attorney General &Commissioner for JusticeLagos State Government,Alausa

I write to acknowledge withthanks receipt of your letterdated 28 December 2011 for-warding a copy of the Octo-ber, 2011 edition of the Ze-nith Economic Quarterly (ZEQ).I found the publication quite in-formative and educative, and itwill, no doubt, assist the missionin its task of promoting Nigeria’sinterest in Singapore. I am there-fore grateful for your gesture.While wishing you continued goodhealth, please accept the assurancesof my highest regards.Danjuma Nanpon SheniActing High CommissionerNigeria High Commission,Singapore

His Excellency the President ofthe Senate, Distinguished SenatorDavid A. B. Mark, GCON Ac-knowledges with thanks your let-ter forwarding a copy of yourZenith Economic Quarterly Pub-lication.

Please accept the assurance of HisExcellency’s high regards and bestwishes.Sen. (Amb) Anthony G. ManzoFRCSChief of Staff to the Presidentof the Senate

We wish to acknowledge withgratitude receipt of a copy of theOctober 2011 edition of the Ze-nith Economic Quarterly (ZEQ)and to inform that the ZEQ hasproven to be a valuable source ofrelevant information on importanteconomic issues.The journal has been a useful ref-erence material because its inci-sive analysis has provided signifi-cant insight into regional and glo-

bal economic matters.Please accept the assurances of theHead of Mission’s highest regards.Yours sincerely,Beatrice AyokhaiAdmin. Attaché IIFor: AmbassadorEmbassy of Nigeria Conakry,Guinea

I am directed to acknowledge withthanks your letter dated 28th De-cember, 2011 forwarding a copyof the October, 2011 Edition ofthe above-named publication. Iwish to add that the receipt ofthe publication was timely as itwould serve as a veritable sourceof reference material in the

Mission’s engagements with theIrish Business Community. Kindlyaccept our most sincere apprecia-tion, please.Nkwocha E.N.First SecretaryFor: AmbassadorEmbassy of Nigeria, Ireland

Your Branch Manager at ZenithBank Plc, Awka recently gave methe October, 2011edition of your well written Ze-nith Economic Quarterly (ZEQ).Let me first register my apprecia-tion for the expertise exhibited inthe topics discussedin that edition of ZEQ.Researchers and Policy Makerswill no doubt find the journal a

good reference materialfor our developing

economy.In fact, you have made available,very sound, educative and topicalinformation for growing minds.Please, accept my compliments forthe nice work. Continue this goodwork and do remember toalways include me in your mailinglist.Kind regards!Charlie O. OkekeDPRSMinistry of EducationAwka, Anambra State

Januar 2012 Zenith Economic Quarterly 5

Periscope

*By Marcel Okeke

Tsome of the key features and drivers of thenational economy during the last quarter 2011.Other specific policy proposals during the pe-riod include the ‘cashless’ economy, petroleumsubsidy removal, ‘nationalization’ of some res-cued banks, adoption of the International Fi-nancial Reporting Standard (IFRS), and runup to the take off of the Sovereign WealthFund (SWF). Consistent increase in crude oilprices in the international market, just as inthe previous quarters, also prevailed in theperiod under review—thus providing somestimulus to the nation’s external reserves.

President Goodluck Jonathan presented theN4.749 trillion 2012 Appropriation Bill to the na-tional assembly (NASS) on December 13, 2011,following the earlier presentation and adoption ofthe (2012—2015) MTEF and the Fiscal StrategyPaper (FSP) by the NASS.

The MTEF and FSP comprise the macroeco-nomic framework which gives an analysis of keymacroeconomic trends of recent years and pro-vides insight on future policy direction. The FSPoutlines fiscal strategy, analyses expenditure andrevenue figures for the years under review; detailsthe assumptions underlying these projections; re-views the previous budget and gives an overviewof consolidated debt and possible fiscal risks. The2012 budget is premised on the assumption of $70per barrel of crude oil and production level of 2.48million barrels per day during the budget year. It isbroken down into a capital expenditure ofN1.32trillion (or 28 percent), recurrent expenditure

he plethora of ongoing re-forms in various sectors, pro-posals for a number of policyinitiatives including the 2012Federal budget as well as theMedium Term ExpenditureFramework (MTEF) were

6 Zenith Economic Quarterly January 2012

PERISCOPE | Economy:Reforms, stability prevail

component ofN2.472trillion (or 52 per-cent); statutory transfers– N398 billion (or 8.3 per-cent) and debt servicing– N560 billion (or 11.7percent). These proposalswere however under leg-islative debates and evenexecutive revisions at thetime of this report.

Another major factorthat influenced theeconomy during the quar-ter under review was theupgrading of outlook onthe Federal Republic ofNigeria to ‘positive’ from‘stable’, by the global rat-ing agency—Standard &Poor’s. This revision, ac-cording to S & P, indi-cates that there is at leasta one-in-three likelihoodof an upgrade, ifNigeria’s reform initia-tives support economicgrowth, build strongerbuffers against currentdependence on petroleumrevenue and reduce pres-sure on the exchange rate.Similarly, according to theEconomist Intelligence Unit (EIU) Democracy Index data,despite the fact that 2011 was an exceptionally turbulent yearpolitically, democracy in Nigeria recorded an improvement—by 10.4 per cent—placing the country in the 119th position in2011, compared with the 123rd position it occupied in 2010.

Democracy Index which provides an assessment of thestate of democracy worldwide for 165 independent states andtwo territories, ranks each country on such factors as qualityof elections, civil liberties, democratic culture, among others.

From the EIU survey,Nigeria’s overall democ-racy index increased from3.47 in 2010 to 3.83 in2011 as a result of high in-crease from electoral pro-cess and pluralism index.

The impact of these in-fluences on the economyin the period under reviewwas a mixed outcome:double digit inflation, de-preciated national currency,improved gross domesticproduct, some accretion toexternal reserves, increasein national debt, etc. Spe-cifically, inf lation rateended the year 2011 at10.30 per cent, slightlydown from the 10.50 percent in November andOctober, as against the car-dinal goal of the CentralBank of Nigeria (CBN) toachieve a single digit infla-tion rate. Apparently, infla-tionary pressure was sus-tained by the structural de-ficiency of the Nigerianeconomy, huge import bill,high public sector fiscalprofile, among others. And

according to the apex bank, single digit inflation rate inthe country would lead to positive real return on fixedincome securities and encourage investment in theseinstruments and thus engender savings.

In the foreign exchange market, excessive demandfor foreign currencies remained unabated all through2011, causing the value of the Naira to slide againstthe US Dollar. For example, in October and rest ofthe year, the nation’s currency met severe head winds

The impact of these influences on the

economy in the period under review

was a mixed outcome: double digit

inflation, depreciated national cur-

rency, improved gross domestic prod-

uct, some accretion to external re-

serves, increase in national debt, etc.

6 Zenith Economic Quarterly January 2012

Januar 2012 Zenith Economic Quarterly 7

PERISCOPE | Economy:Reforms, stability prevail

with much pressure coming from im-porters, downstream oil companies aswell as speculators. Indeed, the nationalcurrency breached the CBN’s adoptedtrading band of N150 (+/-3 percent),sparking rumours of possible devalu-ation. In the face of this ugly trend,the CBN tinkered with a number ofmeasures to bring about some stabilityto the market, the overall effect re-mained a depreciated Naira. Some ofthese measures include increase in the

sale of foreign exchange, removal oflimit of dollars sold to Bureau DeChange (BDCs), target audit of theauthorized dealers to prevent specula-tive demand on dollars, lifting of re-striction on the holding period in gov-ernment securities by foreign investors,increase in MPR, and close to year-end, the reduction in net open limit ofbanks’ shareholders funds. Despitethese measures, the Naira depreciatedin all the three segments of the for-eign exchange market against the USDollar. Indeed, it ended 2011at

N156.7/$1 and 164/$1 at the officialand parallel markets respectively.

While the Naira experienced depre-ciation during the period under review,the nation’s Gross Domestic Product(GDP) moved in the opposite direc-tion. Available data from the NationalBureau of Statistics (NBS) show thatthe GDP grew by 7.40 per cent in thethird quarter 2011, and closed last quar-ter of the year at an estimated 8.68per cent. This growth was driven

mainly by activities recorded in Agri-culture, Wholesale & Retail Trade, Tele-communications, Manufacturing andFinance & Insurance sectors. Similarly,the nation’s stock of public debt expe-rienced significant accretion all through2011. Data from the Debt Manage-ment Office (DMO) show thatNigeria’s debt stock (addition of ex-ternal and domestic debt) as at Decem-ber 31, 2011 stood at N6.51 trillion,representing an increase of about24.38 per cent from the December2010 figure of N5.24 trillion. It was

N6.199 trillion as at September 30,2011.

A breakdown of the debt stock asat year-end 2011 show that externaldebt accounted for 13.64 per cent ofthe total debt, standing at N887.95 bil-lion, while the domestic componentaccounted for 86.36 per cent or N5.623trillion. Furthermore analysis of theyear-end 2011 debt stock show that itis about 17.50 per cent of Nigeria’sGDP , as against the applicable critical

This growth was driven

mainly by activities

recorded in Agriculture,

Wholesale & Retail

Trade, Telecommunica-

tions, Manufacturing

and Finance & Insur-

ance sectors.

http://www.bagco-ng.com/pages/weaving%205.jpg

8 Zenith Economic Quarterly January 2012

PERISCOPE | Economy:Reforms, stability prevail

limit of 40 per cent for countries inNigeria’s economic peer group. This stillunderpins Nigeria’s claim to wide fis-cal sustainability space. But while thenation’s public debt stock was inchingup, its external reserves were decliningor remained flat, standing at US $32.64 billion as at December 31, 2011, asagainst US$32.34 billion level at De-cember 31, 2010. The CBN has allthrough 2011 expressed concernsabout the persistent demand pressurein the foreign exchange market andemphasized the need for tighter fiscalcontrols around oil revenue. The apexbank noted that the solution to reservedepletion resided in the implementa-tion of appropriate reforms with re-gard to industrial and trade policiesaimed at reducing import-dependencynature of the Nigerian economy whichwill help to conserve some foreign ex-

change.Preparation towards the take-off

of the compulsory adoption of theInternational Financial Reporting Stan-dards (IFRS) by all publicly quotedcompanies in the country reached afeverish pitch during the last quarter2011. In line with the subsisting policy,effective January 01, 2012, public

companies operating in Nigeria are ex-pected to migrate from the NigerianGenerally Accepted Accounting Poli-cies (N-GAAP) to IFRS. This requiresthe preparation of 2011 accounts basedon IFRS. IFRS are principles-basedstandards, interpretations and theframework, adopted by the Interna-tional Accounting Standards Board(IASB). Towards the adoption of theIFRS in the country, the Nigerian Ac-counting Standards Board (NASB) hassince transformed to the FinancialReporting Council of Nigeria, sequelto a Bill that was signed into law on 20July 2011. With this development inNigeria “more meaningful and decisionenhancing information can now be ar-rived at from financial statements is-sued in Nigeria because accounting,actuarial, valuation and auditing stan-dards used in the preparation of these

http://www.globalhomesmagazine.com/wp-content/uploads/2011/08/World_Bank_buildingweb.jpg

Through its Commercial

Agriculture Development

Project (CADP), the World

Bank is also giving a push to

agriculture in the country by

reaching more states in the

six geopolitical zones with

its US$150 million facility.

Januar 2012 Zenith Economic Quarterly 9

PERISCOPE | Economy:Reforms, stability prevail

statements shall be issued and regulatedby this Financial Reporting Council,”according to the Minister of Trade andInvestment, Olusegun Aganga.

The transformation agenda ofthe Federal Government contin-ued to gain expression in the ag-ricultural sector of the Nigerianeconomy during the period un-der review. Sequel to the roll outof the Agricultural Transforma-tion Action Plan (ATAP), the Fed-eral Government has also initiatedthe Growth Enhancement Sup-port (GES) under which farmers,agro-dealers, seed and fertilizercompanies will be supported tomake a success of their agric busi-ness. Also, efforts to establishStaple Crops Processing Zones,Clusters, Commodity MarketingCorporations jointly with the pri-vate sector have commenced.Through its Commercial Agricul-ture Development Project(CADP), the World Bank is alsogiving a push to agriculture in thecountry by reaching more statesin the six geopolitical zones withits US$150 million facility. In thisdrive, ten states are the benefi-ciaries under the CADP, includ-ing Kano, Kaduna, Lagos, CrossRiver, Enugu, among others.

In a similar vein, the CBNstrengthened its agric credit guar-antee scheme, under which it guar-anteed about N10.20 billion toover fifty-six thousand farmers in

the 36 states and the Federal CapitalTerritory (FCT) in 2011. A breakdownof this sum shows that the apex bank

guaranteed a total of N969.40 millionin the first quarter 2011, N1.38 billionin the second quarter, and N3.55 bil-lion in the third quarter. The guaran-tee shot up to N4.44 billion in the lastquarter 2011. The purpose of the Ag-ricultural Credit Guarantee Scheme(ACGS) is to provide guarantee in re-spect of banks’ loans to farmers foragricultural activities, with the primaryobjective of increasing the level ofbank credit to the sector. The loansnormally comprise advances, over-drafts and any other credit facilities.

Another creative funding supportfor the agric sector came during theperiod under review, when the Federalgovernment through the DMO issuedsovereign guarantees to banks, secur-ing up to 70 per cent of the loansgranted by banks to agro dealer. Thisinnovative funding is intended to getseeds and fertilizer (agric inputs) intothe hands of farmers directly and helpboost food production in the country.This totally obviates the challenge ofGovernment using its funds for directprocurement and distribution of theseinputs. About 12 banks are participat-ing in this new arrangement.

THE CAPITAL MARKETContrary to the predictions of mostanalysts about the behavior of the capi-tal market in 2011due to the spillovereffect of the steps taken by the CBNin 2010 to rescue some banks and in-crease investors’ confidence, the bear

10 Zenith Economic Quarterly January 2012

PERISCOPE NIGERIA: EconomicTeam Takes Off, Sustains Stability

ruled the market. Indeed, such predic-tions turned out to be false at the closeof the year—with the All-Share Index(ASI) losing about 17 per cent of itsvalue to stand at 19, 526 points andthe Market Capitalization declining byabout 18 per cent, closing at N6.5 tril-lion. Rising unemployment, weakenedpurchasing power and poor investorconfidence, all combined to exert downward pressure on the stock marketduring the period under review.

From the external front came the‘contagion’ of the lingering global eco-nomic meltdown, which reflected onthe market in form of foreign inves-tors almost cashing out of the scene,even as their local counterparts soughtrefuge in short and medium-term gov-ernment securities. Specifically, theEuro-zone sovereign debt crisis whichled to underweighting of frontier andemerging markets resulted to with-drawal of foreign investments. Also,persistent interest rate hike by the CBN(with MPR raised from 6.25 per centin January to 12 per cent in October2011) to curb inflation and pressureon the Naira robbed off negatively onthe capital market.

Over all, the capital market datashow that in 2011, 28 Bonds issued in

the market totalled N79b billion naira;those of States (Delta, Ekiti, Niger andBenue) and Corporate Bonds collec-tively amounted to N84 billion. Also,there were 16 new Issues; six rights is-sues; nine private placements and onepreference share issue, totalling N142billion. Foreign portfolio investmentinto the market amounted toN478billion naira during the year.

Significantly, the banking sub-sec-tor closed the year with less numberof quoted/listed banks as a result ofsuccessful mergers and acquisitionsthat took place in the sector within thelast quarter of the year. A number of

the acquired banks were de-listedfrom the daily official list (DOL)of the Nigerian Stock Exchange(NSE); thus, the market closedwith 15 strong and healthy banksas against 21 banks that startedthe year.

BANKING ANDFINANCEThe Central Bank of Nigeria(CBN) pursued with vigour, its re-forms in the banking sector allthrough 2011—leading to a waveof mergers and acquisitions (M& A), recapitalization and nation-alization. On the M & A train,Access Bank took up Interconti-nental Bank; EcobankTransnational Incorporated Plc(ETI) acquired 100 per cent ofthe outstanding share capital ofOceanic Bank, just as First CityMonument Bank (FCMB) took

over Finbank and Equitorial TrustBank merged with Sterling Bank. Onthe other hand, Union Bank embarkedon a rights issue of five new sharesfor every nine shares held. This waspart of its re-capitalization effortswhere a core investor—a consortiumof private equity firms headed by Af-rican Capital Alliance—took majorstake in the bank. The CBN had ear-lier nationalized and revoked the li-censes of three other banks for failingto recapitalize ahead the stipulateddeadline. The assets of these bankswere transferred to three newly cre-ated, nationalized banks: KeystoneBank, Enterprise Bank and MainstreetBank.

The apex bank also tenaciously tooksteps towards implementing its “cash-less” economy policy—havingemphasised for so long that the Nige-rian economy was too heavily cash-ori-ented in the transactions of goods andservices. According to the CBN, hugevolumes of cash transactions imposeenormous costs to the banking systemand consequently, the customer, interms of cash management, frequentprinting of currency notes, currencysorting and cash movements. It opinedthat these cash-fuelled transactions in

The apex bank alsotenaciously took stepstowards implementingits “cashless”economy policy—having emphasised forso long that the Nige-rian economy was tooheavily cash-orientedin the transactions ofgoods and services.

Januar 2012 Zenith Economic Quarterly 11

PERISCOPE | Economy:Reforms, stability prevail

the economy informed the preferenceby the banks to lend to the capitalmarket and oil and gas industry ratherthan the real sector and small & me-dium scale enterprises (SMEs). Fur-thermore, the apex bank insists thatthe spiralling cash management cost,most of which is passed to the cus-tomers in the form of bank chargesand lending rates, is as a result of the

porate respectively will attract a charge.The pilot phase of the “cashless” policyhas commenced in Lagos, and willgradually cover Port Harcourt, Kano,Aba and the Federal Capital Territory(FCT), among others.

TELECOMMUNICATIONSThe GSM segment of the telecomsindustry continues to dominate theperformance of the sector by all indi-ces. The Nigerian CommunicationsCommission (NCC) data for year 2011show that the segment recorded a to-tal subscriber-base of 90, 566, 238 outof the 95,886,714 industry-wide.MTN Nigeria, with 41,641,089 sub-scribers, representing 46 per cent ofthe segment, maintained its leadingposition. Globacom with 19,886,014lines accounting for 22 per cent rankssecond. Airtel controls 20 per cent ofthe GSM segment with 18,028,385subscribers, while Etisalat had10,752,230 subscribers, representing 12per cent of the segment. M-tel’s258,520 subscribers represent zero percent in that market segment.

A further breakdown of NCC fig-ures show that on a quarterly basis,Etisalat witnessed the most impressivegrowth rate of 13.02 per cent betweenthe third and fourth quarter. Airtel alsogrew impressively at 8.06 per cent whileMTN and Globacom grew marginallyat 1.30 and 0.16 per cent respectively.Etisalat’s market also witnessed themost gain as it grew to 12 per centfrom the 10 per cent in the precedingquarter. Again the only gainer in mar-ket share on a quarter-to-quarter basiswas Etisalat which moved from nineper cent as at end of first quarter 2011to 10 per cent as at the end of thesecond quarter. Airtel’s market sharealso increased to 20 per cent from 19in the preceding quarter. On the otherhand, MTN’s market share declinedfrom 48 per cent in the third quarterto close the year at 46 per cent whileGlobacom also closed the year at 22per cent, down one per cent from 23per cent as at end of third quarter.

In the CDMA segment of themarket, which had 4,601,070 subscrib-ers as at end 2011, Visafone improvedits dominance with 2,604,038 subscrib-

cash dominant economy.Thus, all through the last quarter

2011, both the deposit money banks(DMBs) and the CBN were in a frenzyworking out the logistics for the take-off of the new retail cash policy whichcommenced January 1, 2012. Thepolicy stipulates that over the countercash transaction above N150,000 andN1,000,000 for individuals and cor-

12 Zenith Economic Quarterly January 2012

PERISCOPE NIGERIA: EconomicTeam Takes Off, Sustains Stability

ers representing 57 per cent of themarket share. Starcomms ranks nextwith 980,109 subscribers accountingfor 21 per cent. Multilinks-Telkom with701,304 subscribers controls 15 percent of the segment, while Reltel con-trols seven per cent of the segmentwith 315,619 subscribers. The onlygainer in market share from the sec-ond quarter 2011 in the CDMA seg-ment is Visafone which moved from47 per cent as at the end of secondquarter 2011 to 57 per cent (a growthof 11 per cent) as at end of the year.Conversely, the market share ofMultilinks-Telkom slipped from 17 percent to seven per cent in the same pe-riod.

The industry regulator, NCC, hascompleted the Subscriber IdentificationModule (SIM) cards registration, andalso taken steps towards achieving num-ber portability and Quality of Service(QoS) improvement in the industry. Inthis regard, it has appointed a consor-tium of three companies: Intercon-nect/Saab Grintek/Telecodia, as thepreferred implementers of the num-ber portability service in the country.

POWER ANDELECTRICITYAs part of the ongoing transformationin the power sector, the Federal gov-ernment during the period under re-view formally issued operational li-censes to 20 new power generationcompanies, a distribution firm and theNigerian Bulk Electricity Trading Com-pany Plc (NBETC). The distributioncompanies have also executed a ‘vest-ing contract’ with the Bulk Taker(NBETC)—a process which providesthe arrangement to ensure that avail-able power is shared equitably amongthe distributing companies. Ahead ofthis, the Bureau for Public Enterprises(BPE) in tune with the revised timelinefor the privatization of the successorcompanies created from the PowerHolding Company of Nigeria (PHCN),released the industry agreements whichare the draft Power Purchase Agree-ment (PPA) and the draft Vesting Con-tract.

About 135 pre-qualified firms forbidding for the successor companies

to the PHCN also commenced physi-cal due diligence on 17 power firmsthat have been put up for sale by theFederal government. Some of theprequalified companies includeDangote Industries Limited, OandoPlc, Essar Consortium, HoneywellEnergy Resources International Lim-ited, Kenya Electricity GeneratingCompany, Odu’a Distribution Com-pany Limited and Rockson Engineer-ing, among others.

In a related development, the Fed-eral government has set up a commit-tee headed by the Governor of CrossRiver, Lyel Imoke, to look into powerdistribution across the country. Mem-bers of the committee include fourother state governors, minister ofpower, national planning, Chief Eco-nomic Adviser to the President as wellas the Director General of Bureau forPublic Procurement.

In line with the privatizationprogramme, the PHCN has also beenwound up, with workers at its head-quarters redeployed to its successorcompanies. Effort has also commencedat privatizing existing thermal plants ofthe PHCN, just as the hydro plants areslated for concessioning. The Federalgovernment has, on the other hand,signed a Memorandum of Understand-ing (MoU) with Global Biofuels Lim-ited, for the construction of 15 inte-grated bio-fuel plants in Nigeria. TheN424 billion project will generate about450 megawatts of electricity and willcreate about 120,000 jobs on comple-tion.(* Marcel Okeke is the Editor, Ze-nith Economic Quarterly)

In a related devel-

opment, the

Federal govern-

ment has set up a

committee

headed by the

Governor of

Cross River, Lyel

Imoke, to look

into power distri-

bution across the

country.

14 Zenith Economic Quarterly January 2012

Polic

y

1. IntroductionThe Medium Term ExpenditureFramework (MTEF) & Fiscal Strat-egy Paper (FSP) are statutory docu-ments which articulateGovernment’s revenue and spend-ing plan as well as its fiscal policyobjectives over the period. Section11 of the Fiscal Responsibility Act(FRA) 2007 requires the Ministerof Finance to prepare the MTEF& FSP and lay it before the Fed-eral Executive Council and the Na-tional Assembly for consideration.

The MTEF & FSP is composedof the macroeconomic frameworkwhich gives an analysis of key mac-roeconomic trends of recent yearsand provides insight on futurepolicy direction. The FSP outlinesfiscal strategy, analyses expenditureand revenue figures for the yearsunder review, details the assump-tions underlying these projections,reviews the previous budget andgives an overview of consolidateddebt and possible fiscal risks.

2. Macroeconomic Framework2.1 Global Economic OverviewRecovery from the global recessionhas slowed down significantly asdownside risks are on the increaseon the back of the debt crisis inthe Euro area and concerns aboutthe trajectory of US recovery giventhe recent downgrade by Standard andPoor’s (S&P). Poor GDP growth fig-ures from Organisation for EconomicCooperation and Development(OECD) countries over the last fewquarters and high unemployment fig-

ures have further increased fears of adouble-dip recession.

Global growth remains unbalancedas many advanced economies, espe-cially in the Euro area periphery, con-tinue to struggle with high levels of

sovereign debt. Japan’sgrowth prospects havebeen weakened consider-ably by the recent nuclearcrisis and effects of the tsu-nami and earthquake cul-minating in the recentdowngrade of Japan’scredit rating. Emerging mar-kets are leading the recov-ery, in particular, China andIndia, although overheatingconcerns persist.

Although it is expectedthat emerging and develop-ing countries such as Nige-ria would continue to leadthe recovery in the mediumterm, rising food and com-modity prices as well asother inflationary pressuresmust be managed forgrowth to proceed.

2.2 Overview of Nige-rian Economic Perfor-manceAlthough the Nigerianeconomy has recoveredconsiderably from theworst effects of the globaleconomic crisis, global eco-nomic activities, particu-larly the outlook for inter-national oil prices, remain

a source of concern. The main trans-mission mechanisms of the crisis tothe economy were the internationalprice of oil, foreign capital inflowsthrough remittances, portfolio invest-ment and FDI. The oil price has been

January 2012 Zenith Economic Quarterly 15

POLICY | 2012-2015 Medium Term ExpenditureFramework & Fiscal Strategy Paper

above $100 per barrel since February2011; however weak economic growthprospects pose considerable downsiderisks to the global demand for oil.

Reforms in the banking sector,such as the creation of AMCON toclear up non-performing loans on bankbalance sheets and NSE reforms tointroduce tighter regulations in themarket, are also aiding recovery inthese areas but there is a long way togo. To mitigate the possibility of a re-duction in oil revenue receipts, Gov-ernment will continue to implement thepolicy of fiscal consolidation com-menced in the 2011 fiscal year. Increas-ing inflationary pressures and theirimpact on macroeconomic stabilitythrough adverse interest and exchangerate movements necessitates this.Greater coordination between mon-etary and fiscal authorities will seek tomitigate these concerns. The goal willbe low inflation, interest rates consis-tent with strong and sustained eco-nomic growth, a stable exchange ratereflective of real market conditions anda build up in external reserves in thepresence of high oil prices.

3. Review of the 2010 Budgets –Amended and SupplementaryBudgetsThe 2010 Budgets were stimulus bud-gets intended to mitigate the negativeconsequences of the global economiccrisis. The 2010 Appropriation Bill wasbased on aggregate expenditure ofN4.637 trillion; however to address therealities of revenue constraints, the Na-tional Assembly passed an AmendmentBudget of N4.427 trillion in May 2010.The approved Amendment Budget wasbased on an oil benchmark price ofUS$60 per barrel, oil production of2.25 million barrels per day and anexchange rate of N150/US$.

A first Supplementary Budget ofN644.75 billion was appropriated tomake provision for some unanticipatedexpenditure items such as the wage in-creases awarded to civil servants, uni-versity lecturers, and medical person-nel amongst others as well as the PHCNarrears of monetisation. A secondSupplementary Budget of N87.72 bil-

lion was approved for INEC in prepa-ration for the 2011 Elections.

3.1 2010 Budget Performance:Revenue OutturnsInternational oil prices averaged US$81per barrel in 2010 while data fromNNPC indicated average oil produc-tion of 2.462 mbpd for the year. Thisresulted in gross oil revenue of N5.396trillion, 10% higher than the budgetedrevenue of N4.902 trillion while FGNRetained Revenue which was projectedat N3.18 trillion; fell short by N221.15billion (or 6.95%) as of the end ofDecember, 2010 as only N2.959 tril-lion was realised.

FGN’s share ofoil revenue wasN1.267 trillion againstthe budgeted N1.456trillion, representing ashortfall of N188.6billion (or 12.96%).Its aggregate share ofVAT, CIT and Cus-toms Duties fell shortof the N530.1 billiontarget by 1.70% withN521.05 billionrealised as at the endof December, 2010.Breakdown of non-oil revenue perfor-mance indicates thatthe main driver wasCIT, with collectionsbeing 12.63% abovethe budgeted figure;whereas customs collections fell shortby 22.74%.

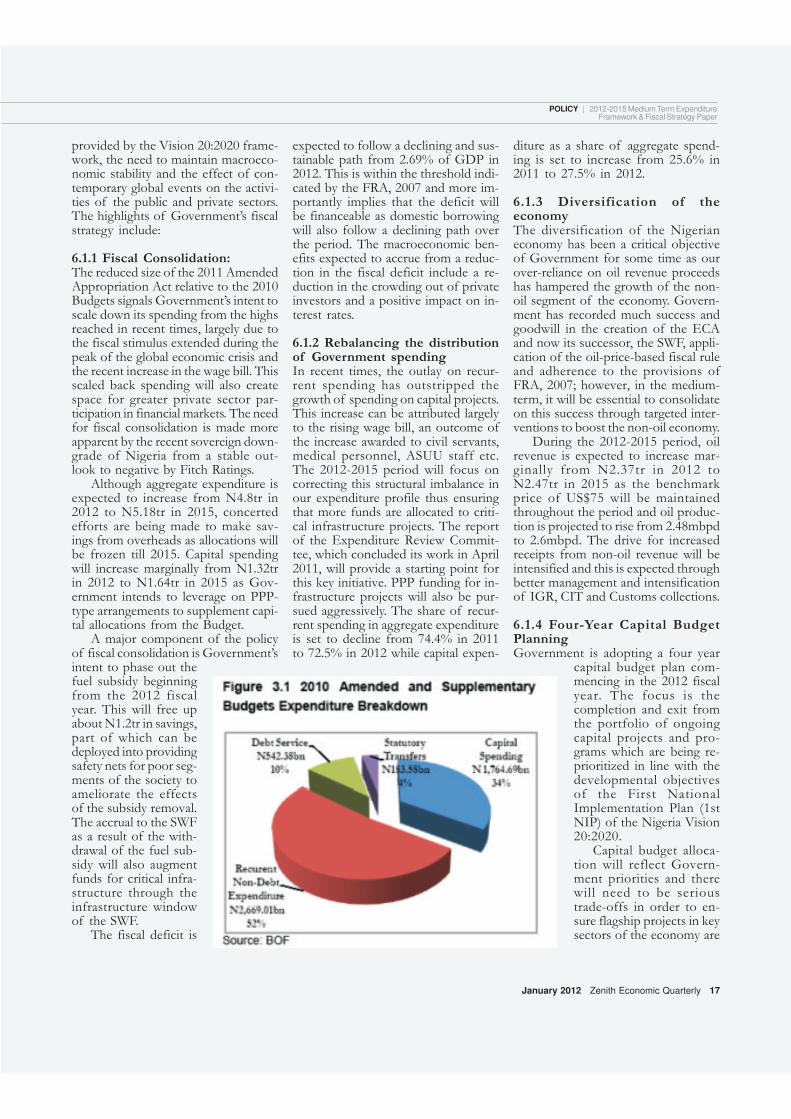

3.2 2010 Budget Performance: Ex-penditure OutturnsAggregate expenditure approved in the2010 Budgets (Amendment, Supple-mentary I and II) amounted to N5.16trillion, of which N1.765 trillion wasallocated to capital expenditure andN2.669 trillion to recurrent spending.

Of the N1.765 trillion budgetedfor capital expenditure, only N956.11billion was released and cash-backed,as it was clear ab initio that the capitalvote approved by NASS was far inexcess of available resources. Of theamount cash-backed, MDAs utilised

N935.61 billion after the fiscal yearwas extended to March 31st, 2011. Atthe end of the period under consider-ation, N935.61 billion had been utilised,resulting in average capital utilisationof 97.86%. This was an improvementover the 70.42% performance as at31st December, 2010.

Inability to fully fund the capitalbudget raises the issue of the skew-ness of the budget towards recurrentspending and the squeeze it places onfunds for capital spending. Approvedsalary increases of 53.7% for core civilservants and medical personnelamongst others raised the wage bill sub-stantially. The payroll bill, representing

34% of aggregate expenditure, in-creased by 61% from N857.04 billionin 2009 to N1.381 trillion in 2010 andto N1.506 trillion in 2011.

To ensure greater efficiency inGovernment spending, Governmenthas approved the engagement of capi-tal programme and project portfoliomanagers, with the objective to workwith pilot MDAs to improve the qual-ity and efficiency of their capital projectimplementation. Government is alsocompiling a database of ongoingprojects for MDAs that will focus at-tention on completing and exiting thelarge portfolio of uncompleted capitalprojects. Moreover, it would help tominimise the incidence of duplication

16 Zenith Economic Quarterly January 2012

POLICY | 2012-2015 Medium Term ExpenditureFramework & Fiscal Strategy Paper

of projects within andacross MDAs, aban-doned projects, andavoid spreading re-sources too thinly acrossmultiple initiatives.

4. Review of the 2011Amended BudgetThe 2011 Budget, withaggregate expenditure ofN4.226 tr (subsequentlyincreased to N4.388tr)was presented to NASSby Mr. President in De-cember 2010. This wasa budget of fiscal con-solidation as the totallevel of spending implieda deficit of 3.62 percentof GDP, a significant re-duction from the 6.06 percent ofGDP in 2010.

NASS passed a budget of N4.972tr in March 2011, which was deemedtoo large and the resultant deficit of4.23 percent of GDP. On this basis,the Executive and the Legislature col-laborated to reduce the level of spend-ing while still accommodating criticalexpenditure. Discussions on reducingthe level of spending were prolongedby the 2011 Elections and were notfinalised until May 2011. The outcomeof the negotiations between the Ex-ecutive and NASS was an AmendedBudget with Aggregate Expenditure ofN4.485 tr which comprises StatutoryTransfers of N417.82 bn (this nowincludes the total allocations to NASSand INEC as per S.81 of 1999 Con-stitution, as amended), Debt Serviceof N495.1bn, Personnel Costs ofN1.503 tr, Overheads of N288.05 tr,Capital Expenditure of N1.148 tr, Pen-sions of N154.75 bn, MYTO of N37bn and other Service-Wide Vote itemsof N439.16 bn.

Implementation of the 2011 Bud-get is still ongoing. Reports from theOAGF indicate that FGN revenue fellbelow target by N231bn as of August2011, mainly due to shortfalls in non-oil revenue as oil revenue receipts wereon target. Expenditure releases arelargely on track.

5. Assumptions Underlying Projec-tions of Oil and Non-Oil Revenue5.1 Oil Production & Market Priceof OilProjected oil production for 2011 is2.3 mbpd. Data from NNPC indicatesthat average production recorded inthe first quarter of 2011 was 2.43mbpd, or 5.65% over the budgetbenchmark oil production. On this basisand after consultations with NNPC,average oil production is estimated at2.480 mbpd, 2.550 mbpd, 2.575 mbpdand 2.600 mbpd in 2012, 2013, 2014and 2015 respectively.

5.2 Benchmark Price of Oil In con-tinuation of the adoption of an oil-price based fiscal rule, oil benchmarkprices significantly below the currentmarket prices will be adopted for the2012-2015 period. Revenue in excessof the benchmark price will continueto be set aside in the Sovereign WealthFund (SWF) The SWF, whichformalises the ECA, was designed toguarantee savings for future genera-tions, to promote the development ofcritical infrastructure thus promotinggrowth and diversifying the economyand to protect the budget against nega-tive oil price shocks. Based on a com-bination of a 5-year and 10-year mov-ing average, an oil benchmark price ofUS$75 per barrel has been adopted for2012-2015 as baseline scenario. Less

optimistic scenarios ofUS$65 and US$70 perbarrel have also been pre-pared in recognition ofpotential volatilities in theinternational oil market.

5.3 Non-Oil RevenueBaseline AssumptionsEstimates of non-oil rev-enue are the result ofchanges in the relevantcomponents of GDP. Theunderlying tax bases are asfollows:

• for CIT the underly-ing base is the portion ofnominal GDP liable forCIT;

• for VAT the under-lying base is the share of

consumption liable for VAT;• for Customs Duty the underlying

base is Import CIF.It is important to note that our pro-

jections also take into account the im-pact of ongoing reforms and includeefficiency factors accounting for op-erational improvements in the varioustax administration agencies. Projectedgross revenue figures for CIT, VATand Customs duties for 2012 are pre-sented below:

6. Fiscal Strategy for 2012-2015 6.1The Fiscal Strategy & EconomicObjectives of Government Over the2012-2015 period, Government willfocus a large portion of its spendingon key sectors which include Security,Infrastructure (including Power), Agri-culture, Manufacturing, Housing andConstruction, Entertainment, Educa-tion, Health and ICT. By investingfunds in these sectors, Governmentintends to support job-creating oppor-tunities which will in turn foster greaterand diversified economic growth.

Government will also continue itsstrategy of fiscal consolidation bywhich expenditure, particularly on re-current spending, will be reined in anddirected to its most productive andgrowth-enhancing use while efforts willbe intensified to increase revenue. Thisstrategy is guided by Government’slong-term development objectives as

January 2012 Zenith Economic Quarterly 17

POLICY | 2012-2015 Medium Term ExpenditureFramework & Fiscal Strategy Paper

provided by the Vision 20:2020 frame-work, the need to maintain macroeco-nomic stability and the effect of con-temporary global events on the activi-ties of the public and private sectors.The highlights of Government’s fiscalstrategy include:

6.1.1 Fiscal Consolidation:The reduced size of the 2011 AmendedAppropriation Act relative to the 2010Budgets signals Government’s intent toscale down its spending from the highsreached in recent times, largely due tothe fiscal stimulus extended during thepeak of the global economic crisis andthe recent increase in the wage bill. Thisscaled back spending will also createspace for greater private sector par-ticipation in financial markets. The needfor fiscal consolidation is made moreapparent by the recent sovereign down-grade of Nigeria from a stable out-look to negative by Fitch Ratings.

Although aggregate expenditure isexpected to increase from N4.8tr in2012 to N5.18tr in 2015, concertedefforts are being made to make sav-ings from overheads as allocations willbe frozen till 2015. Capital spendingwill increase marginally from N1.32trin 2012 to N1.64tr in 2015 as Gov-ernment intends to leverage on PPP-type arrangements to supplement capi-tal allocations from the Budget.

A major component of the policyof fiscal consolidation is Government’sintent to phase out thefuel subsidy beginningfrom the 2012 fiscalyear. This will free upabout N1.2tr in savings,part of which can bedeployed into providingsafety nets for poor seg-ments of the society toameliorate the effectsof the subsidy removal.The accrual to the SWFas a result of the with-drawal of the fuel sub-sidy will also augmentfunds for critical infra-structure through theinfrastructure windowof the SWF.

The fiscal deficit is

expected to follow a declining and sus-tainable path from 2.69% of GDP in2012. This is within the threshold indi-cated by the FRA, 2007 and more im-portantly implies that the deficit willbe financeable as domestic borrowingwill also follow a declining path overthe period. The macroeconomic ben-efits expected to accrue from a reduc-tion in the fiscal deficit include a re-duction in the crowding out of privateinvestors and a positive impact on in-terest rates.

6.1.2 Rebalancing the distributionof Government spendingIn recent times, the outlay on recur-rent spending has outstripped thegrowth of spending on capital projects.This increase can be attributed largelyto the rising wage bill, an outcome ofthe increase awarded to civil servants,medical personnel, ASUU staff etc.The 2012-2015 period will focus oncorrecting this structural imbalance inour expenditure profile thus ensuringthat more funds are allocated to criti-cal infrastructure projects. The reportof the Expenditure Review Commit-tee, which concluded its work in April2011, will provide a starting point forthis key initiative. PPP funding for in-frastructure projects will also be pur-sued aggressively. The share of recur-rent spending in aggregate expenditureis set to decline from 74.4% in 2011to 72.5% in 2012 while capital expen-

diture as a share of aggregate spend-ing is set to increase from 25.6% in2011 to 27.5% in 2012.

6.1.3 Diversification of theeconomyThe diversification of the Nigerianeconomy has been a critical objectiveof Government for some time as ourover-reliance on oil revenue proceedshas hampered the growth of the non-oil segment of the economy. Govern-ment has recorded much success andgoodwill in the creation of the ECAand now its successor, the SWF, appli-cation of the oil-price-based fiscal ruleand adherence to the provisions ofFRA, 2007; however, in the medium-term, it will be essential to consolidateon this success through targeted inter-ventions to boost the non-oil economy.

During the 2012-2015 period, oilrevenue is expected to increase mar-ginally from N2.37tr in 2012 toN2.47tr in 2015 as the benchmarkprice of US$75 will be maintainedthroughout the period and oil produc-tion is projected to rise from 2.48mbpdto 2.6mbpd. The drive for increasedreceipts from non-oil revenue will beintensified and this is expected throughbetter management and intensificationof IGR, CIT and Customs collections.

6.1.4 Four-Year Capital BudgetPlanningGovernment is adopting a four year

capital budget plan com-mencing in the 2012 fiscalyear. The focus is thecompletion and exit fromthe portfolio of ongoingcapital projects and pro-grams which are being re-prioritized in line with thedevelopmental objectivesof the First NationalImplementation Plan (1stNIP) of the Nigeria Vision20:2020.

Capital budget alloca-tion will reflect Govern-ment priorities and therewill need to be serioustrade-offs in order to en-sure flagship projects in keysectors of the economy are

18 Zenith Economic Quarterly January 2012

POLICY | 2012-2015 Medium Term ExpenditureFramework & Fiscal Strategy Paper

adequately funded.Fiscal tables for the 2012-2015

period are provided in the Annex.

7. Analysis and Statement on Con-solidated Debt and Contingent Li-abilitiesRecent events worldwide, particularlyin the United States and Euro-zonearea, have highlighted the importanceof sustainable debt in maintaining eco-nomic stability. During the first fewyears of the global economic crisis,many developed countries had limitedfiscal space to accommodate additionalspending by Government and had toresort to the debt markets to raise fundsto keep their economies running.Emerging and developing countrieshave fared much better in this regardgiven that many, including Nigeria, hadembarked on successful macroeco-nomic reforms prior to the start ofthe crisis. Nigeria was able to enjoy fis-cal space owing to the successful ParisClub debt relief arrangement and onthe back of ongoing macroeconomicreform. The reforms have resulted inlower inflation levels, higher GDPgrowth and lower debt levels; however,in recent times, the rising domestic debtprofile has become a source of con-cern.

7.1 Debt ServiceDebt service payments are made toservice our obligations to foreign anddomestic creditors. Although the do-mestic debt stock had been on the risein recent years, with our current policyof fiscal consolidation and its positiveimpact on the size of the fiscal impactand thus domestic borrowing, a reduc-tion in the domestic debt stock is ex-pected.

7.2 Debt SustainabilityNigeria conducts a Debt SustainabilityAnalysis on a yearly basis in conjunc-tion with the World Bank and IMF. TheDSA utilises macroeconomic data toassess a country’s debt sustainability inrelation to current debt burden thresh-olds and projects its future ability toservice its debt.

The results from the DSA indicatethat Nigeria is well within the debt

sustainability threshold for all the yearscovered up to 2030 and is still at a lowlevel of debt distress. According toDMO, the current Net Present Value(NPV) of Debt to GDP ratio is about18 percent (domestic debt to GDPratio of 16.4 percent) while the rec-ommended threshold for countriessimilar to Nigeria is 40 percent.

7.3 Nature & Fiscal Implication ofContingent LiabilitiesContingent liabilities are potential obli-gations which crystallise at the occur-rence of a future event. These liabili-ties could arise where guarantees ofdebt, made by the Federal Governmentwith regard to contract agreements forcapital projects entered into by MDAs,crystallise into actual obligations. Withour current move towards PPPs indriving capital projects, the possibilitythat these liabilities are realised is quitereal; hence, the need for careful andrigorous analysis of potential projectsfor the PPP scheme.

8. Fiscal Risk8.1 Global Economic TrendsThe global economy has witnessed anumber of upheavals since 2010 thathave posed a challenge to global GDPgrowth and recovery from the globaleconomic crisis. The unfolding Eurozone debt crisis particularly is having ahuge impact on global financial mar-kets. The crisis is sending shockwavesthrough the markets as commodityand stock prices are exhibiting greatervolatility on concerns about the riskof default by the affected countries.The bailouts of Greece, Ireland andPortugal introduced greater stability inthe markets but current developmentsindicate that uncertainty persists. Therecent debt ceiling negotiations in theUnited States and downgrade of theUS economy to AA+ from AAA havealso contributed to market tensions.Japan’s recovery from the recentnuclear, tsunami and earthquake disas-ters has also led to a downgrade of itscredit ratings. As a result, uncertaintyon global economic recovery in themedium-term is highly uncertain.

8.2 Global Oil TrendsGlobal oil demand projections for 2011have been lowered due to the slow-down in global economic growth. Thedemand outlook for 2012, althoughinitially more positive due to post-con-struction efforts in Japan and demandfrom emerging countries like China andIndia, has also been revised downwards.The downside risk from persistentlyhigh oil prices has become more pro-nounced in recent times; however,China, India and the United States willcontinue to remain major drivers ofoil demand growth.

The unfolding events in the MENAregion, particularly the ongoing conflictin Libya, will have an impact on oilsupply as well as the future trajectoryof international oil prices. The supplyoutlook for 2011 is cautious consider-ing the uprising in the MENA regionis still unfolding.

8.3 Risks to Oil Production & PriceOil production in Nigeria has improvedconsiderably as the Niger Delta Am-nesty Initiative has resulted in peaceand stability in the region. Accordingto data from the NNPC, actual pro-duction figures in 2010 were higherthan projected; however, caution willbe exercised in making projections for2012.

International oil prices have beenrelatively high since late 2009 althoughgreater volatilities have been exhibitedin recent times due to global eventssuch as the uprisings in the MENAregion, the earthquake, tsunami andnuclear crisis in Japan and the Euro-zone debt crisis. In line with our ef-forts at fiscal discipline we will con-tinue to abide by the oil-price basedfiscal rule by setting a prudent budgetbenchmark price for the 2012-2015period. Recent world events and theuncertainty concerning current eventslinked to oil price movements also sug-gest that caution should be applied insetting the benchmark price.

8.4 Risks to Non-Oil RevenueIn 2010, the non-oil economy was thelargest contributor to GDP growth withagriculture, wholesale and retail tradein the forefront, in line with the pat-

January 2012 Zenith Economic Quarterly 19

POLICY | 2012-2015 Medium Term ExpenditureFramework & Fiscal Strategy Paper

tern in recent years. Aswe accelerate the diver-sification of theeconomy, we expectnon-oil revenue to con-tribute a greater shareof budget revenue com-pared to the currentcontribution of about30%. The performanceof non-oil revenue in2010 was below expec-tations as Customs andVAT collections werebelow target althoughCorporate Tax per-formed above target forthe 2010 fiscal year.

With the accelerationof recent reform ef-forts by Governmentand the implementationof initiatives to boostkey non-oil sectors, thisperformance should im-prove. Government isactively engaging withrevenue generation andcollection agencies toimprove collections. Inaddition, moves are be-ing made to harmonisethe establishing acts ofMDAs to ensure consis-tency with provisions ofthe 1999 Constitution (as amended) andFRA, 2007, thereby increasing receipts.

9. ConclusionThe 2012-2015 FSP and MTEF havebeen prepared against a backdrop ofheightened global economic uncer-tainty. The debt crisis in the Euro Area,its possible contagion effects, the down-grade of the US economy by S&P andthe possible downgrade of major EUeconomies is having a dampening ef-fect on financial markets and potentialfor global economic recovery in themedium-term.

The downside risks to economicgrowth have been taken into consider-ation in the preparation of the MTEF& FSP. The priority sectors identifiedby Government will receive the bulkof capital allocations over the period.Government intends to continue to

implement a fiscal consolidation policyespecially in view of the structure ofexpenditure which has increasinglytilted towards recurrent expenditure inrecent times. To correct this bias, Gov-ernment is implementing a 4-year capi-tal project plan commencing in 2012,which will ensure that we exit from thecurrent portfolio of ongoing projects.In addition, measures to rationalise re-current expenditure as identified by theExpenditure Review Committee will befully implemented.

On the revenue side, the strategyof adopting an oil price-based fiscalrule and the accrual of windfall oil sav-ings will continue. A baseline Bench-mark oil price of US$75 per barrel isproposed for the 2012-2015 periodwhile oil production of 2.480mbpd,2.500mbpd, 2.575mbpd and 2.600

mbpd will be adopted for the 2012,2013, 2014 and 2015 fiscal years re-spectively. To increase non-oil revenuereceipts, efforts to improve collectionswill be stepped up, taking off from therecently concluded audits of revenue-generating and collecting agencies. Gov-ernment will also advance current workto improve IGR remittances by rec-onciling establishing acts of parastatalsand agencies with the provisions of theFRA, 2007.

The policies outlined in the 2012-2015 MTEF & FSP are in line withthe 1st National Implementation Planand Vision 20: 2020. These will con-tinue to serve as the guiding vision ofGovernment’s fiscal strategy over themedium term towards the actualisationof the Transformation Agenda of theAdministration.

20 Zenith Economic Quarterly January 2012

I$12 trillion, second only to the UnitedStates, casts shadows on the global eco-nomic outlook for 2012.

But the scope of the problem goesfar beyond the euro-zone. Other ma-jor economies in the European Union,including the United Kingdom, havecontinued to struggle since the 2008-2009 global recession. For the leadingemerging economies including Brazil,

Russia, India and China, the euro-zonecrisis has slowed export earnings andforeign investments while markets haveremained volatile in reaction to uncer-tainties in much of Western Europe.This is a major setback for an eco-nomic bloc that would otherwise havedriven global growth at a time like this.

Observers opine that should the2012 recession happen, a major chal-

solvent; not the gigantic, ‘too-big-to-fail’corporate institutions that clusterround Wall Street. And when sover-eigns go broke, who bails them out?

For sure, the euro-zone is boundfor a recession in 2012. Reasons in-clude the worsening debt crisis thereand the threat of a contagion, withmajor economies in the zone, includ-ing Italy, Spain, France, and God knowswhere next, highly vulnerable. Themassive size of the euro-zone eco-nomic bloc with nominal GDP of over

In 2008-2009 it was theUnited States; today, it is theeuro-zone that is pushing theglobal economy into anotherbrink of recession. This time,it is sovereigns that are in-

Glo

bal W

atc

h

By EUNICE SAMPSON

January 2012 Zenith Economic Quarterly 21

lenge for most economies would betheir huge debt overhang and fiscaldeficits following the 2008-2009 reces-sion. This would make it difficult forthe impending recession to be foughtwith the same level of fiscal aggres-sion as was deployed during the lastglobal economic slump.

A recent World Bank report ob-served that the coordinated global re-sponse to the 2008-2009 economicdownturn, especially in the form ofstimulus helped to lower interest rate,increase public spending, cut taxes andease liquidity. These outcomes reducedthe longevity and impact of the crisis.But with economies already strugglingwith massive deficits, sovereign debtand over bloated balance sheets, a re-

peat of these measures might not bepossible this time around.

Global GrowthStatistics in 2011For virtually all the major economies,available data shows a drop in growthduring several quarters in 2011, an in-dication that year-end results may havedeclined for several of these econo-mies. Preliminary data released in themiddle of January reveals that theUnited States managed a real GDPgrowth of 1.7% year-on-year in 2011,compared to a robust 2010 growth of3.0%. After a 1.6% growth in firstquarter 2011, which subsequent dataproved to be its best quarterly ad-

vancement last year, the United King-dom maintained a below 1% growthfor the last three quarters of 2011.Year end 2011 position is thereforeexpected at, at best, 1.0%.

The Euro-zone experienced 1.4%advancement in 3rd quarter 2011, witha poorer performance expected in thelast quarter of the year. Estonia (8.5%),Slovakia (3.0%), Finland (2.7%), Aus-tria (2.6%) and Germany (2.5%) werethe high flyers; with Greece (-5%),Portugal (-1.7%), Slovenia (-0.1%), Ire-land (-0.1%) and Italy (0.2%) being theworst performers, in that order. Someof these sluggards could end up inoutright recession by first quarter 2012.

Year end data shows that theeconomy of Germany enjoyed a ro-

htt

p:/

/th

esky

lark

film

.file

s.w

ord

pre

ss.c

om

/20

10/

05/

img_

1944

.jpg

22 Zenith Economic Quarterly January 2012

GLOBAL WATCH | Global Economyin 2012: Another Recession Imminent?

export, slowing demands for raw andfinished products and capital flows,very few attained the heights recordedin 2010. And 2012 looks even glim-mer unless the spreading crisis in theEuro-zone is halted soon enough.

World Bank/IMF OutlookFor 2012The World Bank in its half-yearly Glo-bal Economic Prospects report pub-lished on January 18 noted that theworld has “entered a very difficultphase characterized by significantdownside risks and fragility” and warnedpolicy makers around the world to ‘pre-pare for the worst’. The growing glo-bal economic weakness is evident in

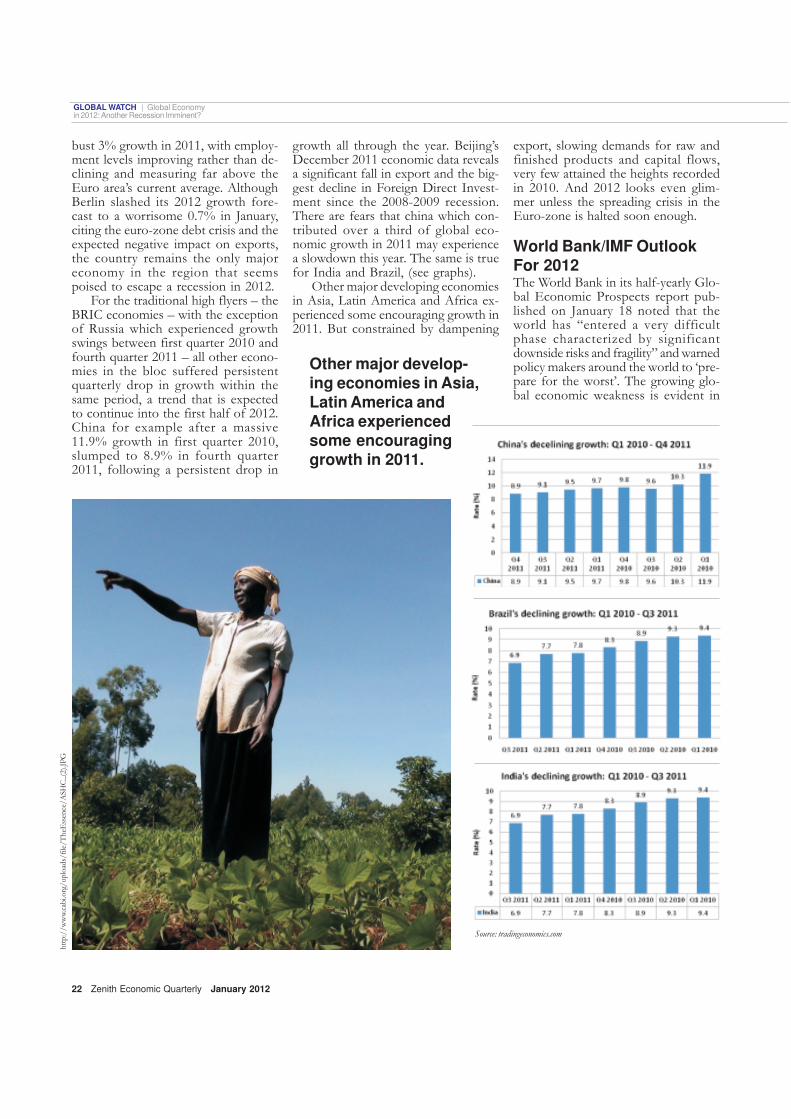

growth all through the year. Beijing’sDecember 2011 economic data revealsa significant fall in export and the big-gest decline in Foreign Direct Invest-ment since the 2008-2009 recession.There are fears that china which con-tributed over a third of global eco-nomic growth in 2011 may experiencea slowdown this year. The same is truefor India and Brazil, (see graphs).

Other major developing economiesin Asia, Latin America and Africa ex-perienced some encouraging growth in2011. But constrained by dampening

bust 3% growth in 2011, with employ-ment levels improving rather than de-clining and measuring far above theEuro area’s current average. AlthoughBerlin slashed its 2012 growth fore-cast to a worrisome 0.7% in January,citing the euro-zone debt crisis and theexpected negative impact on exports,the country remains the only majoreconomy in the region that seemspoised to escape a recession in 2012.

For the traditional high flyers – theBRIC economies – with the exceptionof Russia which experienced growthswings between first quarter 2010 andfourth quarter 2011 – all other econo-mies in the bloc suffered persistentquarterly drop in growth within thesame period, a trend that is expectedto continue into the first half of 2012.China for example after a massive11.9% growth in first quarter 2010,slumped to 8.9% in fourth quarter2011, following a persistent drop in

Other major develop-ing economies in Asia,Latin America andAfrica experiencedsome encouraginggrowth in 2011.

Source: tradingeconomics.com

htt

p:/

/w

ww

.cab

i.org

/up

load

s/fi

le/T

heE

ssen

ce/A

SHC

_(2

).JP

G

January 2012 Zenith Economic Quarterly 23

slower trade and capital flows to de-veloping economies, lower commod-ity prices and the threat of a meltdownin global financial markets. Money sup-ply is on a decline, keeping interest rateshigh in most countries of the world,all of which have been carried over tothe New Year. The Bank thereforelowered its global growth forecast for2012 from 3.4% to 2.5%.

The World Bank also cut its 2012growth forecasts for several individualcountries from its earlier estimates witha warning that the world is on the brinkof another recession that could be asbad as the 2008-2009 experience.

According to the report, growth indeveloped economies will shrink to amere 1.4%, which is barely half of anearlier estimate of 2.7%. The euro-zone economies will end the year on anegative territory of -0.3%, rather thanan earlier predicted growth of 1.8%.Without the euro-zone, the rest of thedeveloped world will grow at a pro-jected 2.1%. The United States, with aprojected growth of 2.2%, down froman earlier World Bank forecast of 2.9%will remain one of the fastest growingdeveloped economies in 2012.

Emerging and developing econo-mies will drive global growth this yeareven though they are currently notwithout their own challenges. The re-cent World Bank forecast puts pro-jected growth for these economies in2012 at 5.4%, lower than the 6.2%projected last June. China, the leaderof the pack will see a slower growthof about 8.4% this year, far below its9.2% advancement in 2011 and 10.3%in 2010.

The threat factors observed in thereport include the escalating debt cri-sis in Europe, crash in commodityprices, dampened global consumptionand demand and a possible hard land-ing in some critical developing econo-mies.

While much of the impact wouldbe felt in the high income economies,the developing world would feel thepinch, especially in the areas of trade,commodity prices, remittances, liquid-ity and capital flows which could af-fect output in these economies. Thechallenge, according to The World Bank

htt

p:/

/w

ww

.th

e-tr

avel

s.co

m/

wp

-co

nte

nt/

up

load

s/20

11/

09/

Agr

a-U

ttar

-Pra

des

h-I

nd

ia.jp

g

GLOBAL WATCH | Global Economyin 2012: Another Recession Imminent?

Agra, Utta Pradesh, India

Jesus Statue, Rio de Janeiro, Brazil

remains how to avoid acontagion which if it hap-pens, will spare noeconomy.

Even if the globaleconomy manages to es-cape a full blown crisis,the world would still growfar weaker than the post2008-2009 recession lev-els. The World Bankprojects a 2.5% growth in2012, down from an esti-mated growth of 2.7% in2011 and 4.1% in 2010.

In its World Eco-nomic Outlook publishedon January 24, 2012, theInternational MonetaryFund, IMF, expressed thesame worries about thefate of the global

Source: tradingeconomics.com

Source: tradingeconomics.com

24 Zenith Economic Quarterly January 2012

GLOBAL WATCH | Global Economyin 2012: Another Recession Imminent?

economy this year, urgingworld leaders to focus ongrowth more than severe aus-terity measures.

The Fund also lowered itsglobal growth forecast for thisyear to 3.25%, down from itsSeptember 2011 forecast of4%. It predicts that the euroarea will shrink 0.5% this year,down from an earlier predic-tion of 1.1% growth.

The IMF expects theUnited States to grow 1.8% atthe end of the year, unchangedfrom its earlier projection. TheUS has witnessed relative im-provement in its major eco-nomic indicators, includingemployment generation andconsumer confidence andspending.

The IMF also cut China’sgrowth outlook this year to8.25%, from 9.0% forecast lastSeptember. After growing9.2% in 2011, its first singledigit growth in several yearsand yet the world’s best per-formance among major econo-mies, China will remain the keyglobal growth factor again thisyear.

Can the globaleconomy avoid arecession in 2012?Most of the major economiesthat determine the pace of glo-bal economic growth seem to bestruggling with one economicchallenge or the other. Despitethe recent improved recoveriesin the United States, for example,especially during the last twoquarters of 2011 which saw adrop in unemployment levels, risein consumer confidence andspending and an improved ad-vancement in GDP, the world’sleading economy is still far fromachieving its traditional growthpace. Euro-zone and its neigh-bors, including the United King-dom could experience near stag-nation or outright negative growth

this year with no quick fix in sightfor the highly indebted Europeancountries.

There is no doubt about it; theworld is again faced with threatsof another bad recession. But de-spite these scary prospects, it is notimpossible for the global economyto avoid a recession in 2012.

To start with, the United States,a country that contributes a thirdof the total global GDP just mightconsolidate on the gains of the lasttwo quarters to further strengthenits growth outlook this year. Thisreasoning is supported by the factthat 2012 is a Presidential electionyear with the incumbent PresidentBarack Obama and his Demo-cratic Party eager to impress vot-ers with policies that could stimu-late growth and the people’swellbeing.

htt

p:/

/w

ww

.zas

tavk

i.co

m/

pic

ture

s/19

20x1

200/

2010

/W

orl

d_

Ch

ina_

Lak

e_in

_th

e_fo

oth

ills_

of_

Ch

ina_

0221

80_

.jpg

Source: The Economic Times; IMF

January 2012 Zenith Economic Quarterly 25

GLOBAL WATCH | Global Economyin 2012: Another Recession Imminent?

As leaders of the euro-zone, theepicenter of the whole recession threatcontinue their struggle for a way outof the debt mess, and as other worldleaders lend their support, a workablesolution to the debacle could still befound. Especially now that the Greekshave at last agreed to a new round ofeconomic measures that would qualifythem for a second IMF/EU bailoutplan, there just might be a light at theend of the tunnel, sooner than ex-pected.

Also, China despite the relativeslowdown in growth in 2011 could pullsome economic surprises that couldbring it back to double digit growth.Though both the IMF and the WorldBank have posited lower growth ex-pectations for China this year, it wouldnot be the first time that the Chineseeconomy advances far beyond econo-mists’ expectations. Brazil, India, Rus-sia and other major developing econo-

mies could well shake off the dust ofthe previous year and improve theiroutput performance in 2012.

Food for Thought?At this point, global leaders are facedwith the challenge of efficiently man-aging policies and resources to stimu-late growth. Decision makers in ad-vanced and emerging economies alikemust somehow balance their deficitstatus with a need for a relatively ex-pansionary spending to help maintaina growth track. The IMF has reiter-ated that fiscal tightening policies,which are a spontaneous reaction ofpolicy makers during periods of fiscaldeficits such as this, would not helpthe situation. The global economy re-quires a boost and only some level ofdeliberate stimulation would ensuresustained growth throughout the year.

The IMF also warns that steps by

global leaders to cut debts and budgetdeficits should be phased rather thanshort term, to ensure that growth pros-pects are not subdued.

At this point, the Breton Woodsinstitutions should also be up to thetask, especially in policy support andfiscal bailout for more economies thatmight require them. ‘A stitch in time’,going forward, would help save theworld from other instances of theGreek ‘wahala’. The cooperation of allstakeholders including global and re-gional leaders, multilaterals, etc wouldbe required; and joint, collective actionswould be necessary if the world is toescape this impending slump. As IMF’sChristine Lagarde puts it, “It is notabout saving any one country or anyone region,” but about “saving theworld from a downward economic spi-ral.”

In sum, if a quicker than expectedsolution is found to the seemingly wors-ening debt crisis in the euro-zone; theBRIC economies manage to find theirgrowth rhythm near double digit; glo-bal leaders team up against this immi-nent menace; nations adopt monetaryand fiscal discipline; global demand andconsumption manage to recover sig-nificantly; and perhaps, very impor-tantly, if the US economy continues tosustain the recent pickup in retail sales,mortgage, employment levels, etc, theworld could still avoid the much pre-dicted recession in 2012.

Bye and large, though a significantadvancement might be out of thequestion, the global economy still standsthe chance of dodging two successivequarterly decline in growth, which tech-nically translates into a recession, andinstead get away with some slowedgrowth this year.

After the dark days that were over-come barely two years ago, the last thingthe global economy needs right now isanother round of recession. While thecurrent glaring risk factors cannot bewished away, yet the ‘sentence’ of arecession this year is still very muchsubject to an ‘appeal’.

(*Eunice Sampson is theDeputy Editor, Zenith EconomicQuarterly)

January 2012 Zenith Economic Quarterly 27

* By Mike Uzor

he 2012 budget has been constructed in re-flection of concerns for a deteriorating exter-nal sector and the challenges facing the nationin the domestic economic front. The nation’seconomy lies highly vulnerable to the manyimponderables in the international oil market;oil being the commodity on which the Nige-rian economy largely.

The 2012 budget therefore represents aneffort by government to navigate the economythrough a narrow path of tight revenue andsticky expenditure profile. Achieving the speci-fied budget targets will require great ingenuityon the path of government and to a large ex-tent an element of luck that the global eco-nomic conditions eventually turn out muchbetter than feared.

As in the preceding year, the watch wordfor the budget is fiscal consolidation, indicat-ing government’s resolve to cause a change ofdirection in its finances. Apparently the

favourable revenue environment in 2011 did notpermit much progress in terms of fiscal restraint,which it had pursued. The high prospects for rev-enue disappointments in the current year havemade fiscal retrenchment quite compelling.

Cost cutting hitchesDespite compelling economic circumstances, re-ducing cost in government operations isn’t goingto be that easy. Government’s decisions and ac-tions are usually subject to a lot of compromisesthat must be made to attain a social balance. Thisis why technocrats have to take it easy with gov-ernment.

Those whose jobs begin and end with lendingand recovering money can hardly excel in politicaladministration. Neither can political leadershipstand without sufficiently diluting advice and rec-ommendations based on pure economic numbers.The attempt at full deregulation of downstreamoil sector is a clear demonstration that government

Issues (

I)

28 Zenith Economic Quarterly January 2012

ISSUES (I) | Nigeria’s Budget 2012: Optionsfor Attaining Sustainable Development

cannot attain the fiscal targets beingrequired by technocrats without a greatdeal of political and social disharmony.

The high cost structure of govern-ment emerged gradually over the years

and cannot easily be reversed suddenly.What the 2012 budget has done, whichis what an annual budget can do, is tomerely scratch the structural problemon the surface. Hence, despitegovernment’s disposition towards fis-cal consolidation, budget numbers aren’tsaying much about fiscal restraint.

Aggregate expenditure of the fed-eral government is projected at N4,749billion for fiscal year 2012. This repre-sents a moderate increase of 6.0% -

which is lower than the anticipated in-flation rate of 9.5% for the year. Gov-ernment revenue is projected to growslightly ahead of expenditure at 9.0%to N3,644 billion. The budget will

therefore run on a fiscal deficit but theamount of the deficit is provided todrop by 20.1% to N1,110 billion in2012.