edc company presentation january 2015 - … leyte-samar. •the island sub-grids are interconnected...

TRANSCRIPT

EDC COMPANY PRESENTATIONJANUARY 2015

This presentation contains certain “forward looking statements.” These forward looking statements include words or phrases such as EDCor its management “believes”, “expects”, “anticipates”, “intends”, “plans”, “foresees”, or other words or phrases of similar import. Similarly,statements that describe EDC’s objectives, plans or goals also are forward-looking statements. All such forward looking statements aresubject to certain risks and uncertainties that could cause actual results to differ materially from those contemplated by the relevantforward-looking statement. Such forward looking statements are made based on management’s current expectations or beliefs as well asassumptions made by, and information currently available to, management. EDC does not make expressed or implied representations orwarranties as to the accuracy and completeness of the information contained herein and shall not accept any responsibility or liability(including any third party liability) for any loss or damage, whether or not arising from any error or omission in compiling such information oras a result of any party’s reliance or use of such information. The information and opinions in this presentation are subject to change withoutnotice.

This presentation does not constitute a prospectus or other offering memorandum in whole or in part. Information contained in thispresentation is a summary only and is prepared for discussion purposes and is not a complete record of the discussions. This presentationshall not constitute an offer to sell or the solicitation of an offer to buy any security. There shall be no sale of these securities in any state orjurisdiction in which such offer, solicitation or sale would be unlawful prior to qualification under securities laws of such state or jurisdiction.By receiving this presentation, each investor is deemed to represent that it is a sophisticated investor and possesses sufficient investmentexpertise to understand the risks involved. Prospective investors should undertake their own assessment with regard to their investmentand they should obtain independent advice on any such investment’s suitability, inherent risks and merits and any tax, legal and accountingimplications which it may have for them.

DISCLAIMER

TABLE OF CONTENTS

Key Investment Highlights

Review of YTD 9M 2014 Financial Results

Growth Projects

Power Industry Overview8 Power Industry Restructuring, 9 Grid Profile

12 Investment Summary, 13 Domaine Expertise, 14 Cornerstone investors, 15 Contract-based

Cash Flows, 16 Track Record for Growth, 17 Favorable Industry Dynamics, 18 Financial and

Operating Results, 19 Credit Profile

22 2014 Strategic Objectives, 23 Growth Agenda, 24 Domestic Expansion, 25 Indonesia

Expansion, 26 Latin America Expansion, 27Mariposa Prospect

30 9M 2014 Significant Events, 31 Consolidated Recurring Net Income

POWER INDUSTRY OVERVIEW

8 Power Industry Overview

INDUSTRY RESTRUCTURING USHERED IN COMPETITION, AS IT ALSO MOBILIZED PRIVATE SECTOR INVESTMENTS

Customers

NPC

Distributors

Pre-EPIRA

Customers

GENCO

TRANSCO

DUs

Suppliers

Post-EPIRA

• Prior to the EPIRA, the industry was composed of NPC and the distribution utilities, e.g., Meralco, VECO, Davao Light and Power Company.

• NPC, at that time, controlled approximately 90% of the country‘s installed generating capacity and performed generation and transmission functions.

• Today, the industry has transitioned into four sectors — the deregulated generation and supply sectors and the regulated transmission and distribution sectors.

9 Power Industry Overview

Luzon54,820 73%

Visayas11,100 15%

Mindanao9,347 12%

Geothermal9,605 13%

Coal32,081 43%

Natural Gas18,791 25%

Hydro10,019 13%

Oil Based4,491 6%

New Re279 0%

2013 GROSS POWER GENERATION, BY PLANT TYPE

EDC IS STRATEGICALLY POSITIONED WITH 64% OF ITS CAPACITY SITUATED IN THE VISAYAS

In Luzon

• Bulk of generation sources are located in the northern and southern parts ofthe Island while the load center is in the Metro Manila area.

• Posted an AACGR of 3.29% for the period 2001-2013.

• Grid is divided into five island sub-grids: Panay, Negros, Cebu, Boholand Leyte-Samar.

• The island sub-grids are interconnected by submarine cables: Leyte-Cebu (2x185 MW), Cebu-Negros (2x90 MW), Negros-Panay (1x85MW) and Leyte-Bohol (1x90 MW). These cables also provide thecapability of sharing excess generation between islands toaccommodate the Visayas’ growing demand.

• Posted an AACGR of 5.90% for 2001-2013, the highest among thethree Grids. The fastest demand expansion has been recorded in DUsin Panay, Cebu and Bohol.

• In 2010, Visayas registered its highest single year increase in demandlevels equivalent to 15.3% growth).

In Visayas

• Grid is composed of six districts with bulk of power generated in thenorthern part of the island and the load centers situated in the southeast(Davao provinces) and southwest (SOCKSARGEN) regions. Power demandfrom these areas account for ~50% of island’s total.

• Posted an AACGR of 3.28% for 2001-2013.

2013 GROSS POWER GENERATION, BY GRID

In Mindanao

VISAYAS GRID REGISTERED THE HIGHEST GROWTH RATE IN DEMAND FOLLOWED BY LUZON AND MINDANAO

KEY INVESTMENT HIGHLIGHTS

12 Key Investment Highlights

TOP REASONS FOR BUYING INTO EDC -- A DIVERSIFIED RENEWABLE ENERGY POWER COMPANY, NOW GOING GLOBAL

100%Successfullyacquired power plants inside its geothermal concessions

1 of 11 light bulbs

EDC accounts for 9% of country’s electricity production

Largest vertically integrated geothermal company globally

DomaineExpertise

Contract-based Cash Flows

Track Record of Growth

Favorable Industry Dynamics

Strong Credit & Investment Profile

Into geothermal, hydro & wind and now diversifying into solar energy

YEAR

2031Concession agreements

start expiring

13

RE Act of 2008Provides

regulatory support

10% Income Tax 7-year ITH Feed-in-Tariff (FIT)

Geothermal is

11% of Installed capacity

YTD 3Q’14 Highlights

RevenuesPhp23.0 billon

RNIPhp8.0 billion

EBITDA (TTM)

Php17.2 billion

Revenue derived

from contract tenors of greater than 6 years

64%

92%Revenue derived from

long-term contract agreements

Concessions acquired in Chile & Peru

Managing Financial Risks

Interest rate on

81% of loans are

fixed

44% of revenues

are US$ indexed

4.9 yrs. loan life

6.6% Interest cost

Geothermal provides

13%of electricity production

13 Key Investment Highlights

Domaine Expertise

1

1

1

1

2

3

3

TECHNOLOGY & GEOGRAPHICALLY DIVERSE

125.0MW232.5MW180.0MW

50.9MW

Upper MahiaoMalitbogMahanagdongOptimization

2

3 112.5MW60.0MW

Palinpinon IPalinpinon II*

112.5MW Tongonan

52.0MW54.0MW

Mindanao IMindanao II

110.0MW20.0MW

Bacman IBacman II

120.0MW12.0MW

PantabanganMasiway

150.0MW Burgos

1

1

1

1

3

Note: *20 MW Nasuji Power Plant placed on preservation

1,441 MW1,159MWGeothermal

150MWWind132MWHydro

% share7% of Installed Capacity9% of Electricity Produced

EDCAT A

GLANCE

49.4MW Nasulo22

COMPANYCAPACITY (in MW)

STEAM PLANT

1 EDC 1,159 1,159

2 Comision Federal de Electricidad 958 958

3 Enel Green Power 915 915

4 Chevron 1,329 887 *

5 Ormat 689 749

Source: Bertani, Ruggero, 2010: Geothermal Power Generation in the World 2005-2010 Update Report

Note: * Not included is the 442 MW operated by the Indonesian Government through PLN

TOP 5 GEOTHERMAL COMPANIES

LARGEST VERTICALLY INTEGRATED GEOTHERMAL COMPANY GLOBALLY

Wind

Hydro

Geothermal (EDC Subsidiary)

Geothermal (Integrated)

14 Key Investment Highlights

Contract-based Cash Flows

GENERATES CASHFLOWS AT BOTH PARENT AND SUBSIDIARY LEVELS

First Gen Hydro Power Corporation (FGHPC)

120.0 MW Pantabangan12.0 MW Masiway

60%

EDC Wind Energy Holdings Inc.

100%

EDC Hong Kong Limited

100%

EDC Geothermal Corporation (EGC)

100%

172.5 MW Palinpinon (2)

112.5 MW Tongonan

Green Core Geothermal Inc. (GCGI)

100%

110.0 MW Bac-Man I20.0 MW Bac-Man II

Bac-Man Geothermal Inc. (BGI)

100%

(1)

• 743.8 MW Power Plants 588.4 MW Unified Leyte

Power Project 106.0 MW Mindanao Power

Project 49.4 MW Nasulo Power

Project

(1) Formerly First Luzon Geothermal Energy Corporation (FLGEC)(2) 20 MW Nasuji Power Plant to be placed in preservation

Lopez Group IFC GIC Public

E: 50.18 % V: 50.59%E: 1.69 % V: 1.12 % V: 3.33 %E: 4.99 % V: 44.96 %E: 43.14 %

EDC Burgos Wind Power Corp. (EBWPC)

150.0 MW Burgos(Under Development)

International Expansion

• Chile• Peru• Indonesia

100% 95/100%EDC

Parent(3)

3,290 31%

EGC6,640 63%

FGHPC614 6%

EDC Parent (3)

5,801 59%EGC

7,391 75%

FGHPC1,084 11%

EDC Parent (3)

6,646 44%

EGC 7,294 48%

FGHPC1,465 6%

(2) All figures in PHP millions as of Sept. 30, 2014(3) EDC Parent figures include the Company’s other subsidiaries

22,982

EBITDA (2) as of Sept. 2014

14,275

Net Income (2) as of Sept. 2014

10,544

Revenues (2) as of Sept. 2014

15 Key Investment Highlights

Contract-based Cash Flows

WESM, 1,909

NGCP, 593

DU, 10,370

NPC, 10,111

SPOT8%

1-2 YRS21%

3-5 YRS7%

>6 YRS64%

22,983

LIMITED EXPOSURE TO VOLATILE SPOT MARKET

LONG-TERM CONTRACTUAL AGREEMENTS

(1) Consolidated revenues as of Sept. 30, 2014

TERM STRUCTURE OF CONTRACTS(1)

In PHP Millions

2031Geothermal Renewable Energy Service Contract

CO

NC

ESSI

ON

Power Purchase Agreements (sovereign)

Power Supply Agreements (commercial)ELEC

TRIC

ITY 2022/24

2022

SPOT 1-2 YRS 3-5 YRS >6 YRS

WESM 8% - - -NGCP - 3% - -DU - 18% 7% 20%NPC - - - 44%

2031year concession agreements start expiring

92%revenue from long-term contracts 64%

revenue from contract tenors of >6 yrs 45%

expanded revenue base from non-NPC clients

16 Key Investment Highlights

Track Record of Growth

• Limited to steam field operations

19,007

25,656

10,324 15,641

8,768

5,633

(+) 125.0 MW

Upper Mahiao

(+) 49.4 MW

N. Negros

(+) 463.4 MW

Mahanagdong,Malitbog, and Optimization

(+) 132.0 MW

Pantabangan– Masiway

• Acquired geothermal concessions overseas

(-) 49.4 MW

N. Negros

(-) 20.0 MW

Botong

(+) 150.0 MW

Bac-Man I & II

(+) 106.0 MW

Mindanao I & II

(+) 305.0 MW

Palinpinon & Tongonan

SIGNIFICANT PORTFOLIO EXPANSION SINCE PRIVATIZATION

STEAMFIELD OPERATOR STEAMFIELD AND POWER PLANT OPERATOR

2007 2008 2009 2010 2011 201220061976 - 2005

current (MW) 0 125 512.8 132 411 150 (69.4) 0 0 20

cum. (MW) 0 125 637.8 769.8 1,180.8 1,330.8 1,261.4 1,261.4 1,261.4 1,281.4

2007-2013 (CAGR)

Revenues 5.1%EBITDA 7.2%Net Income 7.1%

2013 2014

(+) 49.4 MW

Nasulo

(-) 20.0 MW

Nasuji

17 Key Investment Highlights

Favorable Industry Dynamics

2013 POWER STATISTICS OF THE PHILIPPINES

Source: DOE

Geothermal11%

Coal32%

Natural Gas17%

Hydro20%

Oil Based19%

New Re1%

Geothermal9,605 13%

Coal32,081 43%

Natural Gas18,791 25%

Hydro10,019 13%

Oil Based4,491 6%

New Re279 0%

11%Geothermalas a % of Installed Capacity 13%

Geothermal as a % of Electricity Production

Fuel TypeInstalled

Capacity (MW)

Coal 5,568

Hydro 3,521

Oil-based 3,353

Geothermal 1,868

Natural Gas 2,862

New RE 153

Total 17,325

GEOTHERMAL ENERGY IS A STRATEGIC ENERGY RESOURCE FOR THE PHILIPPINES

PRINCIPAL TAX BENEFITS

PRIMARY REVENUE & COST INCENTIVES

o Income Tax Holiday (“ITH”)─ 7-year ITH from

start of commercial operation

o 10% - Corporate income tax rateNote: Subject to guidelines on pass-on savings for existing operations

o Carbon credits tax exemption

o Income Tax Holiday (“ITH”)─ 6 years under

Pioneer Status─ Plus one year bonus

o 30% - Corporate income tax rate

o Tax on carbon credits─ 30% income tax and

0% VAT

PR

EVIO

US

NO

W

o Royalties─ Steam:

Government share is 1.5% of gross margins

o 0% duties for Imported materials & equipment

o Net operating loss carryover (“NOLCO”): 3 years

o Royalties─ Steam: Government

share is 60% of net proceeds

o 0% duties for Imported materials & equipment

o Net operating loss carryover (“NOLCO”): 3 years

OTHER KEY INCENTIVES

o Feed-in tariff(1)

o Renewable Portfolio Standard(2)

o Green Energy Option(3)

(1) Feed-in Tariff - A policy designed to accelerate investment in renewable energy technologies by offering long-term contracts to renewable energy producers.

(2) Renewable Portfolio Standard - A market-based policy which requires electricity suppliers to source an agreed portion of their energy supply from eligible renewable energy resources.

(3) Green Energy Option - A mechanism that empowers end-users to choose renewable energy in meeting their energy requirements.

RENEWABLE ENERGY ACT OF 2008

18 Key Investment Highlights

Strong Credit & Investment Profile

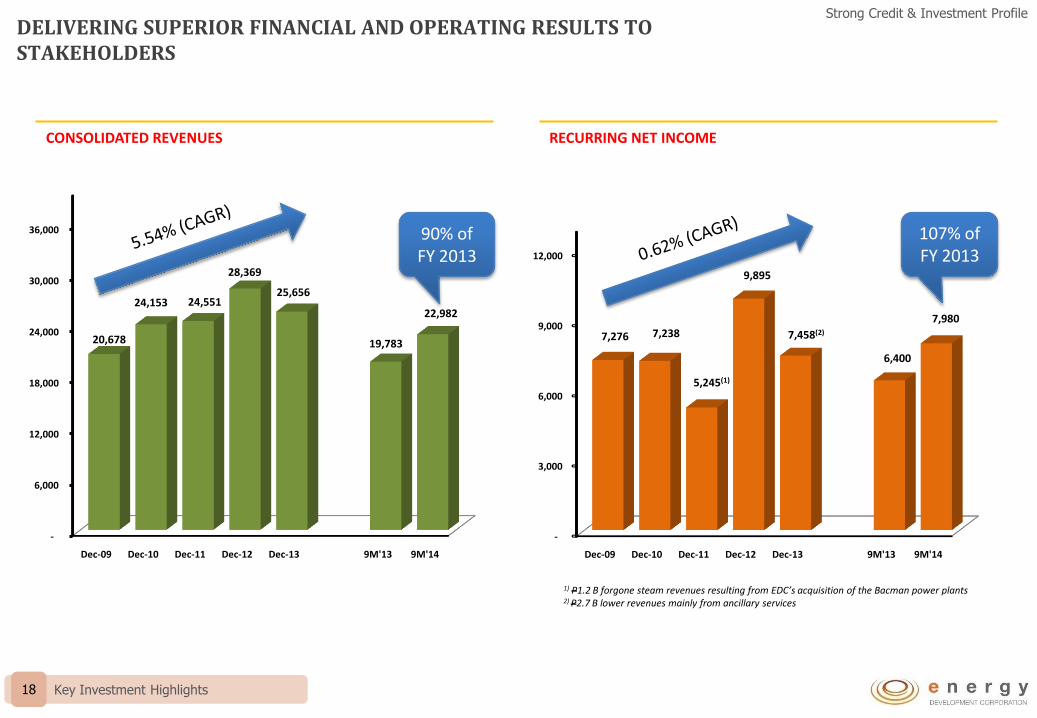

DELIVERING SUPERIOR FINANCIAL AND OPERATING RESULTS TO STAKEHOLDERS

-

3,000

6,000

9,000

12,000

Dec-09 Dec-10 Dec-11 Dec-12 Dec-13 9M'13 9M'14

7,276 7,238

5,245(1)

9,895

7,458(2)

6,400

7,980

RECURRING NET INCOME

-

6,000

12,000

18,000

24,000

30,000

36,000

Dec-09 Dec-10 Dec-11 Dec-12 Dec-13 9M'13 9M'14

20,678

24,153 24,551

28,369

25,656

19,783

22,982

CONSOLIDATED REVENUES

1) P1.2 B forgone steam revenues resulting from EDC’s acquisition of the Bacman power plants2) P2.7 B lower revenues mainly from ancillary services

90% of FY 2013

107% of FY 2013

19 Key Investment Highlights

Strong Credit & Investment Profile

MAINTAINING A ROBUST CREDIT PROFILE (1)

9M '14

9M '13

Dec-13

Dec-12

Dec-11

Dec-10

2.95x 2.26x

2.72x 2.17x

2.95x

2.56x

9M' 14

9M' 13

Dec-13

Dec-12

Dec-11

Dec-10

2.20x

1.58x

2.06x

3.24x

2.14x

2.51x

9M' 14

9M' 13

Dec-13

Dec-12

Dec-11

Dec-10

PHP 34.57

PHP 29.82

PHP 33.71

PHP 29.84

PHP 29.30

PHP 26.47

9M' 14

9M' 13

Dec-13

Dec-12

Dec-11

Dec-10

0.98x

1.03x

1.17x

1.06x

1.32x

1.09x

9M' 14

9M' 13

Dec-13

Dec-12

Dec-11

Dec-10

0.29x

0.37x

0.43x

0.30x

0.33x

0.32x

Notes:(1) Figures computed on a consolidated basis ending Sept. 30, 2014(2) EBITDA = Earnings Before Interest, Taxes, Depreciation, and Amortization,

Trailing 12 months(3) Debt Service Coverage Ratio = Net Cashflow from Operating Activities / (Short

Term Debt + Long Term Debt + Projected Interest Service for the next 12months)

(4) PHP Million per MW

NET DEBT TO MARKET CAPITALIZATION

Deteriorated with increase in price per share

NET DEBT TO EQUITY

Allows for additional fund raising

NET DEBT TO EBITDA (2)

Well within our targeted 3.6x

NET DEBT PER MW POWER (4)

Increased with the pre-funding of Burgos Project

DEBT SERVICE COVERAGE RATIO (3)

Higher than the minimum covenanted 1.2x

1.2x

3.6x

GROWTH PROJECTS

22 Growth Projects

Bacman

EDC SUCCESSFULLY DELIVERED ON ITS 2014 STRATEGIC OBJECTIVES

Nasulo Burgos

OUTPUT 968 GWH

REVENUES Php4.8 B

130.0 MW Bacman geothermal plants have returned to service

OUTPUT 382 GWH

REVENUES Php2.0 B

OUTPUT 326 GWH

REVENUES Php2.8 B

49.4 MW Nasulo geothermal plant declares commercial operations on July 2014

150.0 MW Burgos wind obtains DOE’s Certificate of Endorsement (COE) for FIT Eligibility

23 Growth Projects

EDC’S GROWTH AGENDA

305 MW Palinpinon-Tongonan acquired in 2009

130 MW Bacmanacquired in 2010

• Bid for Unified Leyte IPPA in 2014

Bid for Mindanao 1 & 2 IPPA in 2014

150 MW Burgos Wind commissioned in 4Q’14

• Wind measurement studies is on-going in 9 other concessions

• Potential 4MW solar

Granted 13 concessions & 19 pending applications in Chile & Peru

Established local offices in LatAm and Indonesia

• Drill wells in Mariposa, Chile by 2015

• Continue to prospect prime geo sites

1 2

3 4

ACQUIRE DEVELOP

CONQUERDIVERSIFY

Win key government geothermal privatization projects

Install 261MW of local geothermal capacity to address

new demand

Establish viable operations in

Asia, Latin America, and Africa

Build 200MW of wind capacity, while expandingRE portfolio

49.37 MW Nasulocommissioned in Sept. 2014

• 6 MW NNGP Plant development is on-going

• 100 MW for commissioning by 2018

2014 STATUS

24 Growth Projects

LOCAL GEOTHERMAL PROJECTS WILL BE THE MAIN SOURCE OF GROWTH IN THE MEDIUM TERM

DONE EXECUTIONADVANCED EXPLORATION

RESOURCECONFIRMATION

POWER PLANTRETROFIT

1

1

3

1

1

2 5

4

6

73

PROJECT CAPACITY 2014 2015 2016 2017Beyond

2018

Nasulo* 49 MW X

Burgos Wind 150 MW X

No. Negros 6 MW X

Burgos Solar 4 MW X

Bacman 3** up to 30 MW X

Nasuji up to 20 MW X

Botong-Rangas** up to 40 MW X

Mindanao 3 50 MW X

Pagudpod Wind X

Bacman 10 MW X

Tongonan ~12 MW X

Palinpinon ~12 MW X

Kayabon 50 MW X

Dauin 40 MW X

2

3

4

5

6

7

FRONTIER AREAS (GEOTHERMAL)

Mandalangan, Negros Occidental

Lakewood, Zamboanga del Sur

Ampiro, Misamis Occidental

Balingasag, Misamis Oriental

Mt. Zion, North Cotabato

Note: *20 MW Nasuji Power Plant placed on preservation**Resource sustainability assessment is on-going

2

2

2

1

1

1

2

3

1

4

4

FRONTIER AREAS (WIND)

Bayog I (Burgos I)

Pagali (Burgos II)

Iloilo 1

Iloilo 2

Matnog 1

Matnog 2

Matnog 3

Negros

1

2

21

25 Growth Projects

OVERSEAS EXPANSION - INDONESIA

GRAHO NYABU GEOTHERMAL PROSPECT

Results from EDC’s completed survey activities for Graho Nyabu in Sumatra shall be used by IndonesianMinistry of Energy and Mineral Resources for its upcoming tender of the Graho Nyabu concession

Currently, in partnership discussions with a geothermal concession holder for a JV in one of their geothermalsites (~ 220 MW at an ~ US 1.0 billion development cost)

26 Growth Projects

Company(Entry into LatAm)

Granted Sites Applications

Peru Chile Peru Chile

Alterra Power Corp (2008)

2 2 16 0

Hot Rock Ltd (2008)

5 1 3 12

EDC Applied/Bid Sites (2009)

0 3 4 4

TOTAL 7 6 23 16

EDC SEIZED THE OPPORTUNITY AND NOW HOLDS STAKES IN UP TO 13 CONCESSIONS AND 39 APPLICATIONS

27 Growth Projects

WE ARE NOW EXECUTING AN EXPLORATION DRILLING PROGRAM IN MARIPOSA, ONE OF THE MOST ADVANCED GEOTHERMAL PROJECTS IN CHILE

Exploration DrillingEstimate: USD 30 MM

Target COD

MAP OF THE REGIONGEOTHERMAL RESERVOIR AND

DRILLING TARGETSCIVIL WORKS

Q4 ‘15 Q2 ‘20

Site DevelopmentBudget: USD 15 MM

Q1 ‘14

Base Camp 9 Road Rehab

Drilling Materials

Santiago

Mariposa

ESTIMATES FOR MARIPOSA PUT THE POTENTIAL SIZE OF THE RESERVOIR BETWEEN 50 TO 300 MW

REVIEW OF YTD 9M 2014 FINANCIAL RESULTS

30 Review of YTD 9M 2014 Financial Results

FG Hydro Adjusted FG Hydro revenues using the ERC mandated re-computation of

Nov. and Dec. 2013 billings (P250M)

UL and Palinpinon

Received insurance proceeds for property damage due to Typhoon Yolanda (P379 M) and Typhoon Sendong (P150 M)

NNGP NNGP’s impairment recovery, net of 10% tax (P1,847 million)

Bacman Reported revenues generated by Units 1, 2 &3 (P2,146 million)

Nasulo Reported revenues following declaration of commerciality (P502 M)

Palinpinon Nasuji’s foregone NI due to Nasulo’s operation (P263M)

SIGNIFICANT EVENTS THAT AFFECTED YTD 9M 2014 FINANCIAL RESULTS

31 Review of YTD 9M 2014 Financial Results

6.40

1.49 0.41 0.24 0.10 (0.47) (0.20) (0.17)

RNI, Sept. 2013

BGBUrevenues

partly offset by higher opex

NIGBUNasulo's

commercial operation

LGBUhigher revenues

MAGBUhigher revenues

partly offset by higher opex

FG hydrolower sales,

2013 revenue adj. & higher opex

Othersint'l subs &

Burgos' opex

RNI, Sept. 2014

NCI RNI Attributable

to EDC

CONSOLIDATED RECURRING NET INCOME ATTRIBUTABLE TO EDC UP BY PHP1.6 BILLION

6.4B2013

8.0B2014

In PHP Billions

Consolidated Recurring Net Income (RNI) increased mainly dueto Bacman and Nasulo revenues, partially offset by higheroperating expenses

• BGBU’s revenues increased by P2.1 B, with the commercial operations of Bacman Units 1, 2 and 3 which was partially offset by higher power plant expenses (previously capitalized).

• NIGBU’s (Palinpinon and Nasulo) higher revenues by P0.5 B due to commercial operations of Nasulo.

• MAGBU’s revenues increased due to higher recorded energy sales and theabsence of short fall adjustments partially offset by higher expensesrelated to steamfield workover drilling.

• Partially off-setting the increase are lower revenues from FG Hydro due tothe 2013 WESM adjustment and higher operating expenses.

RNI COMPUTATION 9M 2014 9M 2013

NET INCOME (LOSS) 10,544 5,925

ADD (DEDUCT) NON-RECURRING ITEMS:

Foreign Exchange (gain)/loss 180 901

Reversal of impairment loss (2,053) 0

Capitalized borrowing cost 0 (192)

Capitalized BGI’s cost of testing 0 (401)

Insurance proceeds on property damage due to typhoon Yolanda (529) 0

Gain on sale of PPE (362) 0

Gain on sale of inventory items (120) 0

Write-off of 2006 input VAT claims denied by the Court 0 219

Income tax provision for (benefits from) non-recurring items 254 (70)

Others 66 19

RECURRING NET INCOME 7,980 6,401

RNI+25.0%

7.898.30 8.54 8.64

8.17 7.98

7.987.81

END OF PRESENTATIONwww.energy.com.ph

BACK-UP SLIDES

TABLE OF CONTENTS (Back-up)

Macroeconomics

Philippine Power Industry

Key Investment Highlights

Typhoon Proofing Cooling Tower Units

Growth Projects

Review of YTD 9M 2014 Financial Results

36 Philippines Macro Section, 37 Asean Macro Section

38 Government Issued Regulations, 39 DOE Energy Forecast (Mar-Jun 2015), 40 Luzon-Visayas

Supply-Demand Forecast (2013-2014), 41Mindanao Supply-Demand Forecast (2013-2014)

42 Ranking of Geothermal Companies, 43 Business Model, 44 Operational Statistics, 45Manpower

and Management Team, 46 CSR, 47 Loans Profile, 48 Financial Highlights, 49 Dividend Policy

50 Phases of Implementation, 51 Engineering Solutions, 52 Install Hurricane Grade CTs,

53 Design & Implement 300 kph Solution

54 Burgos Wind Project, 55 Latin America Expansion

56 Revenues, 57 Cash Balance, 58 Financial Ratios

36 Macroeconomics

PHILIPPINES MACRO SECTION

Capital Manila

Population (2Q’14) 99.7 Million

GDP per capita (2013) USD 1,581

GDP Growth (2Q’14) 6.4%

Inflation Rate, Headline(Oct. 2014)

4.3%

Unemployment Rate (July 2014)

6.7%

Credit Ratings BBB - S&PBaa3 - Moody’s

37 Macroeconomics

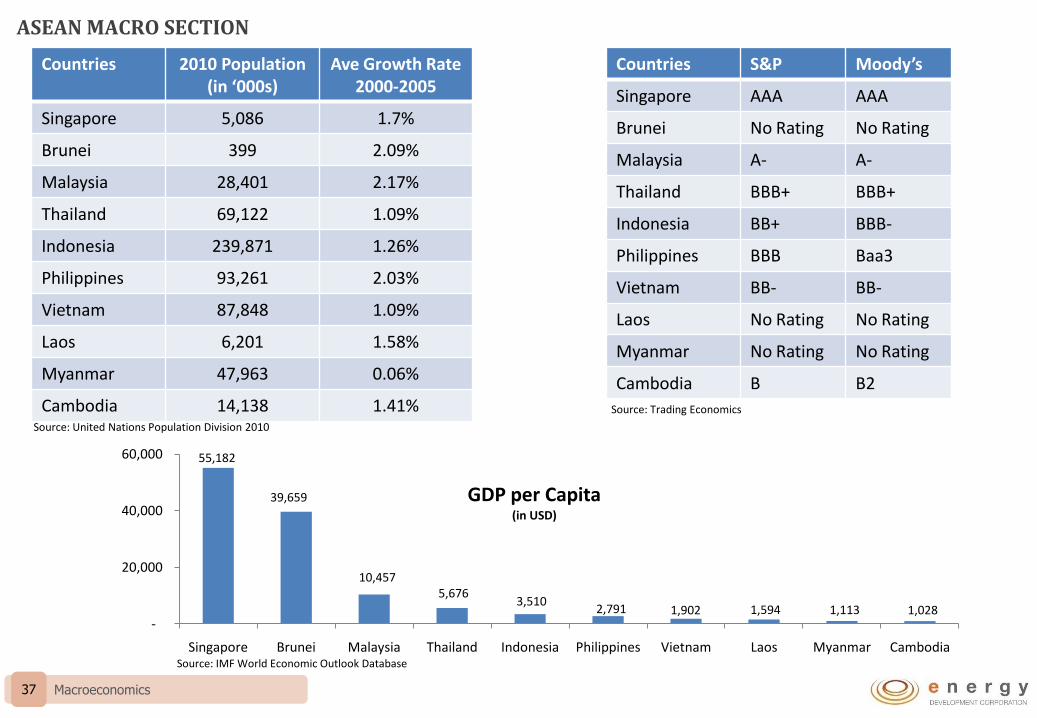

ASEAN MACRO SECTION

55,182

39,659

10,457 5,676

3,510 2,791 1,902 1,594 1,113 1,028

-

20,000

40,000

60,000

Singapore Brunei Malaysia Thailand Indonesia Philippines Vietnam Laos Myanmar Cambodia

GDP per Capita(in USD)

Source: IMF World Economic Outlook Database

Countries S&P Moody’s

Singapore AAA AAA

Brunei No Rating No Rating

Malaysia A- A-

Thailand BBB+ BBB+

Indonesia BB+ BBB-

Philippines BBB Baa3

Vietnam BB- BB-

Laos No Rating No Rating

Myanmar No Rating No Rating

Cambodia B B2

Countries 2010 Population(in ‘000s)

Ave Growth Rate 2000-2005

Singapore 5,086 1.7%

Brunei 399 2.09%

Malaysia 28,401 2.17%

Thailand 69,122 1.09%

Indonesia 239,871 1.26%

Philippines 93,261 2.03%

Vietnam 87,848 1.09%

Laos 6,201 1.58%

Myanmar 47,963 0.06%

Cambodia 14,138 1.41%Source: United Nations Population Division 2010

Source: Trading Economics

38 Philippine Power Industry

SINCE NOVEMBER 2013, THE GOVERNMENT ISSUED NEW REGULATIONS THAT AFFECT EDC PROJECTS

Secondary WESM Price Cap

• SECONDARY OFFER PRICE CAP OF PHP 6.245/KWH WHEN THE 72-HOUR AVERAGE WESM PRICE EXCEEDS PHP8.186/KWH

Revised RCOA1 Rules• LIMITS BUY-SELL OF ELECTRICITY BETWEEN AFFLIATED GENERATIO

COMPANIES, RETAIL ELECTRICITY SUPPLIERS AND END-USER CUSTOMERS AT 50%;• RESTRICTED ISSUANCE OF RES LICENSE

FIT-ALL Provisional Approval

• FIT TARIFFS FOR SELECTED RENEWABLE ENERGY SOURCES• FIT-ALL PROVISIONAL APPROVAL OF PHP 0.04057 PER KWH

(1) Retail Competition and Open Access (RCOA)

39 Philippine Power Industry

DEPARTMENT OF ENERGY FORECASTS ELECTRICITY SHORTAGE BY SUMMER OF 2015

6,000

6,500

7,000

7,500

8,000

8,500

9,000

9,500

10,000

10,500

W-9 Mar

W-10 Mar

W-11 Mar

W-12 Mar

W-13 Mar

W-14 Apr

W-15 Apr

W-16 Apr

W-17 Apr

W-18 May

W-19 May

W-20 May

W-21 May

W-22 Jun

W-23 Jun

W-24 Jun

W-25 Jun

DOE SUPPLY-DEMAND FORECAST MAR-JUN 2015

Available Capacity less FO Average FO

Projeted Demand Regulating Reserve Req't

MW

NOTE: Data sourced from DOE Presentation

W-9 Mar

W-10 Mar

W-11 Mar

W-12 Mar

W-13 Mar

W-14 Apr

W-15 Apr

W-16 Apr

W-17 Apr

W-18 May

W-19 May

W-20 May

W-21 May

W-22 Jun

W-23 Jun

W-24 Jun

W-25 Jun

INTERRUPTIBLE LOAD PROGRAM (ILP)

300 MW PLANT/CONTRACT

FIT

• Mandatory operation of end consumer gensets to unload the grid;

• Additional cost of running gensets will be spread across electricity consumers;

• Total of 438 MW of intending ILP participants as of 9/25/2014.

• Plant purchase/lease of from PHP700 M to PHP2.8 B per 100 MW;

• CAPEX to be subsidized by Malampayafunds.

• Increased FIT allocation for easy- to-set-up power plants like solar.

DOE PROPOSED SEVERAL PLANS TO ADDRESS SHORTAGE

40 Key Investment Highlights

2013 - actual 2014 2015 2016 2017 2018 2019 2020

Reqd Additional Capacity - 236 328 585 1,207 453 1,081 1,177

Committed Capacity 854 1,004 1,834 2,643 2,643 4,047 4,461 4,711

Existing Capacity 11,244 11,244 10,881 10,594 10,594 10,594 10,231 10,594

Peak Demand 9,853 10,216 10,674 11,311 11,820 12,351 12,907 13,488

Peak Demand + Req'd Reserve Margin 12,040 12,484 13,044 13,822 14,444 15,093 15,772 16,482

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

20,000

22,000

COMMITTED CAPACITIES WILL NOT BE SUFFICIENT TO MEET THE REQUIRED RESERVE MARGIN FOR THE COMBINED LUZON-VISAYAS GRID

Oil-fired plants… 2,691MW, or 18%, of

country’s capacity Php12.52/kwh(est’d

ave tariff)

Sources:1. First Gen’s internal estimates based on

actual data submitted to DOE2. DOE’s list of Existing Power Plants 2013

MW

62% OF THE COUNTRY’S POWER GENERATION CAPACITY IS 15 YEARS OR OLDER. UNEXPECTED OUTAGES IN THE AGING PLANTS COULD LEAD TO HIGH ELECTRICITY PRICES2

Luzon-Visayas Supply-Demand Forecast (2013-2020)1

Peak Demand growth: ~4.8%

110MW Bacman49MW Nasulo

150MW Burgos

194MW Avion196 MW300 MW

5MW135MW

RECalacaNNGPAyala

414MW135MW

76MW

San GabrielAyalaPasuquin

135MW41MW

8MW

PCPCAklanVillasiga

40MW364MW400MW300MW300MW

BacmanPagbilaoQPPLGN PowerToledo

414MW San Gabriel 80

250MW Green Mountain

41 Key Investment Highlights

2013 - actual 2014 2015 2016 2017 2018 2019 2020

Reqd Additional Capacity 346 365 79 - - - - -

Committed Capacity - 43 393 823 886 886 935 935

Existing Capacity 1,282 1,282 1,282 1,282 1,282 1,282 1,282 1,282

Peak Demand 1,332 1,383 1,435 1,490 1,546 1,605 1,666 1,729

Peak Demand + Req'd Reserve Margin 1,628 1,690 1,754 1,821 1,889 1,961 2,036 2,113

700

1,000

1,300

1,600

1,900

2,200

2,500

2,800

3,100

3,400

WITH UNRELIABLE HYDRO CAPACITY, THE MINDANAO GRID IS EXPECTED TO EXPERIENCE TIGHT SUPPLY UNTIL THE COAL CAPACITIES COME IN

Mindanao Supply-Demand Forecast (2013-2020)1

Source:1. First Gen’s internal estimates based on actual data submitted to DOE

Peak Demand growth: 3.8%

MW

35MW Green Power

8MW Minery Cabuhog300MW

50MWTherma SouthMindanao 3

225MW Lanao Hydro

200MW Conal Coal

5MW Camiguin Wind

30MW Puyo

23MW Bubunauan

9.75MW Cabadbaran

40.5MW9MW

TagoloanTumalaong

42 Key Investment Highlights

Domaine Expertise

LARGEST VERTICALLY INTEGRATED GEOTHERMAL COMPANY GLOBALLY

COMPANY COUNTRYSTEAM

CAPACITY (in MW)

PLANT CAPACITY

(in MW)

1 EDC Philippines 1,159 1,159

2 Comision Federal de Electricidad Mexico 958 958

3 Enel Green Power Italy 915 915

4 Chevron USA 1,329 887 *

5 Ormat Israel 689 749

6 Calpine USA 725 ** 725 **

7 Mighty River Power New Zealand 385 385

8 Terra Gen USA 337 337

9 Contact Energy New Zealand 335 335

10 Orkuveita Reykjavikur Iceland 333 333

11 CalEnergy Generation USA 329 329

12 Star Energy Ltd. Indonesia 227 227

13 Northern California Power Agency USA 220 220

Source: Bertani, Ruggero, 2010: Geothermal Power Generation in the World 2005-2010 Update ReportNote: * Not included is the 442 MW operated by the Indonesian Government through PLN

** Calpine Operating Power Plants 1Q 2014 Investor Update Conference Call May 2014

43 Key Investment Highlights

Contract-based Cash Flows

NGCP

Electric Cooperatives/Third party customers

POSSESSES STABLE AND PREDICTABLE CASH FLOWS

Subsidiaries of EDC

National Power

Corporation

Power Supply Agreements (PSAs)

Power Purchase Agreements

Electricity

Cashflow

Steam Sales Agreements (SSA)

Bac-ManGeothermal

Geothermal Resources Sales Contracts (GRSC)

Green Core Geothermal

FG Hydro

Electricity

Cashflow

Electricity

Cashflow

Electricity & Ancillary Svcs.

Cashflow

Steam

Cashflow orDividends

Steam

Cashflow orDividends

Dividends

Burgos WindElectricity

CashflowDividends

Power Supply Agreements

Power Purchase Agreements (PPAs)

Percentage of Consolidated Revenues (1)

USDLinkage

Electricity44% 73%

Sovereign off-take

Electricity56% 0%

Commercial off-take

(1) As of Sept.30, 2014

Electricity0% 0%

Feed-in-Tariff

44 Key Investment Highlights

Track Record of Growth

MAINTAINS A TRACK RECORD OF OPERATIONAL EXCELLENCE

Ava

ilab

ility

Fac

tor

(1)

(%)

Rel

iab

ility

Fac

tor(2

)

(%)

Unified Leyte Palinpinon I

Palinpinon IITongonanVisayas

Mindanao I

Mindanao IIMindanao

YTD 9M 2013

YTD 9M 2013

YTD 9M 2014

0%

20%

40%

60%

80%

100% 85%93% 99%

83%

99% 96%

47%

82%

YTD 9M 2014

0%

20%

40%

60%

80%

100% 90%99% 99% 99% 99% 99%

71%

98%

Source: Company data as of the end of September 30, 2014

(1) Availability Factor - Fraction of time a unit is capable of providing service, considering both planned and unplanned outages. (2) Reliability Factor - Measure of ability of generating units to perform their intended function, considering unplanned outages only.

Bacman I

Bacman IILuzon

0%

20%

40%

60%

80%

100%98% 96%

83%

99% 99% 99%

35%43%

0%

20%

40%

60%

80%

100%98% 99% 99% 99% 99%

94%

41% 44%

45 Key Investment Highlights

Favorable Industry Dynamics

BOARD OF DIRECTORS

LED BY AN EXPERIENCED BOARD OF DIRECTORS AND MANAGEMENT TEAM THAT IS COMMITTED TO BEST IN CLASS CORPORATE GOVERNANCE PRACTICES

• Key authorities in the power industry

• Long-standing relationships with key industry stakeholders

• Advocates of good corporate governance

• Sustainability Business Award, organized by Global Initiatives Singapore, PBE, Eco-Business, and Price Waterhouse Coopers

• Platinum Award for Corporate Governance from the Institute of Corporate Directors and Securities and Exchange Commission.

• 8th Placer in Finance Asia’s Best in Corporate Social Responsibility

• Four Philippine Quill Awards for HELEN, CAREERS & BINHI from the International Association of Business Communicators

• Three Seals of Approval for MGPF, LGPF & GCGI under DENR’s Philippine Environment Partnership Program for voluntary self-regulation & improved environmental performance

• Five Anvil Awards for Corporate Sustainability Communications Program, annual report, BINHI and calendar & planner from Public Relations Society of the Philippines

TECHNICAL EXPERTISE (1)

CORPORATE GOVERNANCE

RECENT AWARDS

• Board works directly with President to determine strategy

• EDC’s independent directors are active members of committees.

• Board Strategic Planning sessions are regularly conducted

Operations & Maintenance

Others(2)

Geosciences & Reservoir Engineering

Engineering & Construction

Drilling

56%

25%

14%

4%

1%

Average Years of Management

Experience

14+ Average Years of Engineering

Experience

13+

(1) As of July 31, 2014(2) Includes Office of the President, Finance, HR, Business Development, Supply Chain, Corporate Affairs, Business Development, Health, Environment & Safety, Information Technology, Legal & Regulatory, Marketing & Sales

46 Key Investment Highlights

Favorable Industry Dynamics

EDC HAS VARIOUS CORPORATE SOCIAL RESPONSIBILITY PARTNERSHIPS AND PROGRAMS

Health

Education

Livelihood

ENvironment

OUR SOCIAL AND ENVIRONMENTAL COMMITMENTS

• We believe that education is the most dependable way out of poverty

- 140 new trainees admitted to Kananga – EDC institute of Technology (KEITECH), with 95% employed

- 741 students enrolled at the Leyte Schools for Excellence (SFE) project

- Scholarships program: 21,875 (elementary), 1,154 (high school), 69(college, with 41 in University of the Phils.)

• We believe in being a partner in progress of the communities in which we operate

- 12,353 individuals served during medical, dental, surgical outreach activities across 5 project sites

- Assisted in 16 major livelihood projects earning a total gross income of PHP14M

- Numerous small scale contracts worth PHP224M awarded to local farmer cooperatives benefitting 3,565 members

• We believe in protecting and nurturing our environment because failing this - our resources will suffer

- BINHI Project – 833,799 trees planted for specific modules (Tree for the Future, Tree for Life and Tree for Food)P342M

Total CSR investment in 2013

47 Key Investment Highlights

Strong Credit & Investment Profile

USD596 41%PHP

841 59%

USD Revenues

16432%

PHPRevenues

34968%

DELIBERATELY MANAGING FINANCIAL RISKS

LOANS BY CURRENCY

US$ indexed revenues provide natural hedge

DEBT MATURITY PROFILE1

Sculpted to support EDC’s growth trajectoryLOANS BY STRUCTURE

Predominantly fixed debt matches nature of energy projects

Average Loan Life (Years)5.4 yrs

Average Interest Cost6.0%

LOANS

USD1,437

USD1,437

Type CurrencyOutstanding

(MM)Repayment Interest

Tenor(Years)

Maturity

175MM Club2 USD 131.0 Amortizing LIBOR+1.75% 6 2017

80MM Club USD 77.0 Amortizing LIBOR+1.80% 5.25 2018

Reg S Bonds USD 300.0 Bullet 6.50% 10 2021

PF – ECA USD 109.0 Amortizing LIBOR+0.90% 15 2029

PF – USD Com USD 28.0 Amortizing LIBOR+0.90% 15 2029

IFC Loan 1 PHP 3,074.0 Amortizing 6.07%3 15 2023

IFC Loan 2 PHP 2,886.0 Amortizing 6.66% 15 2025

PHP FXCN PHP 6,880.0 Amortizing 6.62% 10 2022

PHP Bonds PHP 12,000.0 Bullet 8.64%, 9.33% 5.5, 7.0 2015, 2016

PHP Bonds PHP 7,000.0 Bullet 4.16%, 4.73% 7.0, 10.0 2020, 2023

PF - PHP Com PHP 4,050.0 Amortizing PDST – R1 +Margin4 15 2029(1) In USD Millions as of October 31, 2014 (4) Margin: 200 bps + (PDST-F minus RDST-R1). Re-pricing on the 10th year(2) USD65 MM converted to PHP via Cross Currency Swap(3) Subject to re-pricing

Fixed1,141 79%

Floating296 21%

-

50

100

150

200

250

300

350

20

14

20

15

20

16

20

17

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

20

26

20

27

20

28

20

29

USD Debt

PHP Debt

48 Key Investment Highlights

Strong Credit & Investment Profile

DELIVERING SUPERIOR FINANCIAL AND OPERATING RESULTS TO STAKEHOLDERS

10,712

13,748 13,238

17,330 15,641

16,532 17,248

50%57% 54%

61% 61% 62% 60%

0%

20%

40%

60%

80%

100%

0

3,000

6,000

9,000

12,000

15,000

18,000

Dec-09 Dec-10 Dec-11 Dec-12 Dec-13 9M'13(12 mos)

9M'14(12 mos)

-

3,000

6,000

9,000

12,000

Dec-09 Dec-10 Dec-11 Dec-12 Dec-13 9M'13 9M'14

7,276 7,238

5,245(1)

9,895

7,458(2)

6,400

7,980

400

2,400

4,400

6,400

8,400

10,400

Dec-09 Dec-10 Dec-11 Dec-12 Dec-13 9M'13 9M'14

3,357 4,395

615(1)

10,376

5,633 5,925

10,544

CONSOLIDATED NET INCOME RECURRING NET INCOME

-

6,000

12,000

18,000

24,000

30,000

36,000

Dec-09 Dec-10 Dec-11 Dec-12 Dec-13 9M'13 9M'14

20,678 24,153

24,551 28,369

25,656

19,783 22,982

EBITDA MARGIN CONSOLIDATED REVENUES

1) Full provisioning for NNGP write-off amounting to P 5B in 2011 1) P1.2 B forgone steam revenues resulting from EDC’s acquisition of the Bacmanpower plants

2) P2.7 B lower revenues mainly from ancillary services

49 Key Investment Highlights

Strong Credit & Investment Profile

DIVIDEND POLICY IS TO DECLARE 30% OF PRIOR YEAR’S RNI

Dividend Policy Statement

At or about 30% of previous year’s Recurring Net Income subject to i) debt service requirements and loan covenants, andii) the implementation of business plans, operating expenses, budgets, funding for

new investments and acquisitions, appropriate reserves and working capital.

1,485 1,875 1,863

2,250

3,000

1,875 1,500

1,875

2,175 750

1,500

1,87530%

65%

33% 31%

45%

58%

36%

58%

0%

10%

20%

30%

40%

50%

60%

70%

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

2007 2008 2009 2010 2011 2012 2013 2014

PHP MillionDividends on Common Shares

Special Regular

Payout Ratio

PHP/share 0.099 0.27 0.125 0.120 0.160 0.140 0.160 0.200

Yield 1.7% 4.4% 3.3% 2.4% 2.7% 2.4% 2.6% 3.1%

50 Typhoon Proofing Cooling Tower Units

RETROFITTING OF COOLING TOWERS TO BE IMPLEMENTED IN 3 PHASES ON PRIORITY 1 AND 2 COOLING TOWERS

TRIAGE THE SITUATION*

PHASE 1

PROCURE & INSTALL HURRICANE GRADE CTs AVAILABLE IN THE MARKET

PHASE 2

DESIGN & IMPLEMENT A 300 KPH SOLUTION

PHASE 3

OB

JEC

TIV

E

TO RESTORE AFFECTED CTs AS QUICKLY AS POSSIBLE

TO TYPHOON PROOF CTs UP TO 232 KPH USING SPX MARLEY RTM STACKS AND SS316 ANCHORAGE RING

TO DESIGN AND IMPLEMENT AN EXTERNAL STRUCTURE TO RAISE CT TYPHOON SURVIVABILITY TO 300 KPH

• Repair Bacman Units 1 and 2 cooling towers using in-country strategic spares, i.e., parts stocked precisely for contingencies of this nature

• Fan Stacks• Replacement of wooden

decks with FRP decks• Replacement of 12 oz casings

with 16 oz casings

TASK

S

• First 7-30’ RTM Fan Stacks available @ Houston Gateway for transport to Manila by mid-November 2014 ;

• 2nd 6-28’ Fan Stacks available @ Houston Gateway mid-December 2014

• Fleet wide progressive replacement of Priority 1 Cooling Tower fan stacks using either the flexibility of N+1 feature or as opportunity shutdown works for units on scheduled major outage

• EDC and Marley are collaborating on options to increase to 300 kph or more a CT’s design wind speed through an external structure

• Initial designs have been put forward by EDC for Marley’s comments

* Ranking an issue in order of importance

AT LEAST ONE COOLING TOWER WILL BE FITTED WITH RTM FAN STACK BY END-2014

51 Typhoon Proofing Cooling Tower Units

1

2

3

4

5

6

ENGINEERING SOLUTIONS WILL PROGRESSIVELY BE IMPLEMENTED TO TYPHOON PROOF OUR COOLING TOWERS

PHILIPPINE WIND ZONE MAP

2

1

43

5

6

ZONE I B (V=250 KPH)

Bacman Geothermal

ZONE II (V=200 KPH)

Burgos Wind

Leyte Geothermal

ZONE III A (V=150 KPH)

Mindanao Geothermal

No. Negros Geothermal

So. Negros Geothermal

PRIORITY Location # of Units

OEM Cell x Fan Stack Dia.

# of Cells

1 Malitbog 3 SPX Marley 8 x 28’ 24

Mahanagdong 3 SPX Marley 7 x 30’ 21

Tongonan 3 SPX Marley 3 x 28’ 9

Malitbog Bottoming 1 SPX Marley 3 x 28’ 3

Upper Mahiao 1 SPX Marley 4 x 22’ 4

Bacman 2 Research Cottrell 6 x 28’ 12

1 ICS 2 X 30’ 2

PRIORITY 1 Sub-total 73

Total Cost, Priority 1 @ USD 100,00 PER CELL USD 7,300,000

2 Mt Apo 2 GEA 5 x 32.8’ 10

Palinpinon 1 2 Hamon 3 x 28’ 6

Palinpinon 1 1 ICS 3 X 28’ 3

Palinpinon 2 4 Shinko 2 x 28’ 8

Nasulo 1 SPX Marley 6 x 26’ 6

PRIORITY 2 Sub-total 33

TOTAL 106

PRIORITY 1: ALL BACMAN AND LEYTE COOLING TOWERS .PRIORITY 2: ALL PALINPINON & MINDANAO COOLING TOWERS .

52 Typhoon Proofing Cooling Tower Units

68 HURRICANE TOWER SETS ON ORDER TO RETROFIT EXISTING FLEET OF COOLING TOWERS

• Fan stack is the nozzle through which the fan blade draws air through the cooling tower.

• SPX Marley USA is OEM for 76/108 or 70%

• The RTM (Resin Transfer Moulding ) cold molding process increases durability, ensures laminate thickness & weight consistency, allows no porosity for delamination or structural fracture, thereby enhancing the cylinder load capacity

• RTM fan stack is designed for 233 kph winds

• Anchorage ring is cold-rolled for increased tensile strength/stiffness and is made of SS 316 to be compatible with corrosive environment

• Marley has confirmed that the incremental weight of the RTM fan stack and anchorage ring is within the existing cooling tower’s design weight limit

• To go beyond the 233 kph design of an additional structure is under evaluation.

KNOWN AS “HURRICANE TOWER” THAT WAS DEVELOPED BY SPX MARLEY

FOR CHEVRON’S USE IN US GULF COAST

SPX Marley Reflex RTM Fan Cylinder Anchorage Ring

RTM SEGMENTS ARE BOLTED TO THE ANCHORAGE RING WHICH IN TURN IS DIRECTLY BOLTED ONTO

THE COOLING TOWER’S PURLINS & JOISTS

PHASE 2: Install Hurricane Grade CTs

53 Typhoon Proofing Cooling Tower Units

SPX MARLEY AND EDC ENGINEERING DESIGN GROUP ARE COLLABORATING ON OPTIONS THAT WILL RAISE CT TYPHOON SURVIVABILITY TO 300 KPH

PHASE 3: Design & Implement 300 KPH Solution

Concept 2 (“Spider Support System”)

• The structure will include an SS support ring at the top of the fan stack & a lower ring spread out from the base of the fan cylinder

• Intermediate tubes (2x2 FRP square tubes) will connect the 2 rings

• SS pins to attach tubes to belly band and anchorage rings

• RTM fanstacks and spider support system to be installed one by one using N+1 flexibility

• Priority is 1. Malitbog, 2. Bacman, 3. Mahanagdong, 4. Tongonan

• Design review meeting completed at Marley in Missouri & Kansas October 2-3, 2014

CONCEPT AGREED; MARLEY PLANS TO COMPLETE DETAILED STRUCTURAL DESIGN BYEND OF OCTOBER AND SUBMIT DETAILED PROPOSAL TO EDC BY NOVEMBER 5

54 Growth Projects

FiT Eligibility = Achievement of “Successful Commissioning”

“Successful Commissioning” = RE Plant is physically connected to the grid

FiT Rules:

RE Project informs DOE of date of successful commissioning (100%)

DOE to validate commissioning results

DOE to issue Certification of Endorsement (COE), if MW(cum) is still within installation target

ERC to issue FiT COC to RE Developer

Nov. 5

Nov. 7-8

Nov. 12

Pending

DOE ISSUES CERTIFICATE OF ENDORSEMENT (COE) FOR FIT EIGIBILITY TO THE BURGOS WIND PROJECT

Expected End-Nov. 2014 Scenario: 200 MW Cutoff

NW:18 MW

EDC: 150 MW

UPC:32 MW

UPC: 49 MW

TA: 54 MW

55 Growth Projects

LATIN AMERICA WILL BE A DRIVER OF LONG-TERM GROWTH FOR EDC

• Large portfolio of early-stage assets

• Development team with significant experience in both geothermal and Latin America

• Long-term commitment to bring projects to completion

• Presence in Latin America provides window to other RE opportunities

56 Review of YTD 9M 2014 Financial Results

REVENUES INCREASED BY PHP3.1 B DUE TO HIGHER CONTRIBUTIONS FROM THE COMMISSIONING OF BACMAN AND NASULO PLANTS

In PHP Billions

• Bacman’s revenues increased by P2.1 B, due to the commercial operations of Bacman Units 1, 2and 3 starting January 2014, June 2014 and October 2013, respectively.

• Fresh revenue contribution by P0.5 B from Nasulo power plant

• Higher revenue contribution by P0.4 M each from Mindanao and Palinpinon-Tongonan due tohigher energy sales and the absence of adjustments covering prior year’s shortfall in Mindanao.

• Revenues from FG Hydro decreased by P0.4 B, due to lower sales volume and the re-computation of electricity spot prices for Nov. and Dec. 2013 billings as ordered by the ERC(P250).

Leyte8,245

Mindanao1,373

Tongonan I3,112

Palinpinon 5,227

Bacman19*

Pantabangan-Masiway

1,826

YTD 9M 2013 REVENUES(P millions)

Leyte8,374

Mindanao1,737

Tongonan I3,431

Palinpinon 5,327

Bacman2,146*

Nasulo502

Pantabangan-Masiway

1,465

YTD 9M 2014 REVENUES(P millions)

Notes: * - Includes trading revenues amounting to P81 Million

REVENUES+15.6%19.8B2013

22.9B2014

2.1 0.5 0.4 0.4 0.1 (0.4)

Revenues,YTD Sept. 2013

BGI Nasulo Mindanao Pal-Tong Leyte FG Hydro Revenues,YTD Sept. 2014

19.8

22.421.9

22.8 23.2 23.3

22.9

22.9

57 Review of YTD 9M 2014 Financial Results

PROJECT FINANCING WILL PRETERMINATE THE BRIDGE LOAN AND REPLENISH CASH RESOURCES ADVANCED FOR BURGOS WIND PROJECT

In PHP Billions

For the first nine months of 2014, cash generated from operations reached P12.3 B and was used to service thefollowing:

P15.3 B property, plant and equipment acquisition, of which:

P9.1 B was spent to Burgos Wind P2.5 B on capitalized cost of wells P1.0 B for Nasulo Project (N2N) P0.9 B for Bacman power plants rehab P0.7 B rehab due to typhoon Yolanda

P3.6 B interest, financing charges paid and payment of long term debts

P2.5 B payment for cash dividend

CASH BALANCE-15.6%16.0B2013

13.5B2014

16.0 13.5

12.3

6.6 ( 3.6)

(2.5)

(15.3)

Cash Balance,Dec. 2013

Cash generated from operations

Proceeds from bridge loans

Debt Servicing Cash Dividends PPE Acquisition, Input VAT and Others

Cash Balance,Sept. 2014

28.3

34.9

31.328.8

13.5

58 Review of YTD 9M 2014 Financial Results

Decreased due to lower cash balance coupled with higher current liabilities due to the reclass of the P8.5B Peso Bonds which will mature on June 2015.

Improved mainly due to equity from higher net income for the period.

Increased mainly due to higher net debt.

Sept. 2013

Sept. 2014

2.48

1.40

Current Ratio

Sept. 2013

Sept. 2014

1.53

1.45

Debt-to-Equity

Sept. 2013

Sept. 2014

2.26

2.95

Net Debt-to-EBITDA*

DEBT-TO EQUITY IMPROVED WHILE BOTH CURRENT RATIO AND NET DEBT-TO-EBITDA WEAKENED

*Trailing 12 months