economic impact of large-scale utilisation of excess heat - assessment through regional modelling

TRANSCRIPT

Economic Impacts of Large-Scale

Utilization of Excess Heat -

Assessment through Regional

Modeling

Akram Sandvall, Erik Ahlgren, Tomas Ekvall

Energy Technology, Energy and Environment Department,

Chalmers University of Technology

Swedish Environmental Research Institutes (IVL)

IEA ETSAP Workshop, Nov.17-19, 2014, Copenhagen

4TH GENERATION DISTRICT HEATING (DH)

Time

En

erg

y

effi

cien

cy

Bu

ild

ing

en

erg

y

con

sum

pti

on

1st

Gen.

1930 1880 1970 Now Future

2nd

Gen.

3rd

Gen.

4th

Gen. Steam

• Pressurized

hot water

(over 100ºC)

• Utilizing

CHPs

Pressurized hot

water

(below100ºC)

• Pressurized hot

water (about 50 ºC)

• Heat recovery (e.g.

industrial excess

heat)

• Use of renewable

sources

Swedish DH systems

Source: Statistics Sweden & Swedish Energy Agency

0

10

20

30

40

50

60

70

19

70

19

75

19

80

19

85

19

90

19

95

20

00

20

05

20

10

Fu

el u

se

[T

Wh

]

Excess heat

Heat pumps

Electric boilers

Biofuels, Municipal solidwaste, peat

Energy coal including cokeoven and blast furnace gas

Natural gas including LPG

Oil

0

10

20

30

40

50

1980 1985 1990 1995 2000 2005 2010

Fue

l su

pp

ly [

TWh

] Peat

Tall oil pitch

Forest residues

Municipal solid waste(MSW)

0

10

20

30

40

50

60

70

1970

1975

1980

1985

1990

1995

2000

2005

2010

Fu

el u

se [

TW

h]

Industrial EH

Heat pumps

Electric boilers

Biofuels, Municipal solidwaste, peat

Energy coal including cokeoven and blast furnace gas

Natural gas including LPG

Oil

Biomass (forest residues &

energy crops)

• Renewable source

–Competition between the heat, power and transport

sectors

• Transported over short distances by trucks

–Regional market Limited resource

Heat synergy collaborations

Power

• Combined heat and power

(CHP)

• Intermittent technologies

(wind, solar)

Transport

• Bio refineries (e.g.

SNG production)

Waste management Industries

• Industrial excess heat (EH)

District

heating

Industrial EH

• Challenges

– High investment cost of building heat networks

– Possible lock-in effects

Could construction of large heat networks, shared

between several industries and DH systems be a

solution?

Research Questions

• How would the system cost of DH supply be affected at a

regional level by the construction of a large heat network

allowing for long-distance transmission of EH?

• How is the marginal cost of DH supply affected by such a large

heat network?

Methodology

• Regional level (regional market for biomass)

• Case (diverse DH systems in terms of fuel use

and DH production technology)

Västra Götaland

CASE

Methodology

• Regional level (regional market for biomass)

• Case (diverse DH systems in terms of fuel use and DH

production technology)

• Reference group

–Learning for researchers and stakeholders

–Solving imperfect information problem

Build trust

Reference Group

Stakeholders including:

– Chemical industries in Stenungsund

– Energy utility companies in Stenungsund, Kungälv,

Gothenburg

Researchers at:

– Heat and Power Technology & Energy Technology at

Chalmers

– Swedish Environmental Research Institutes (IVL)

– Sweden’s Technical Research Institute (SP)

Methodology

• Regional level (regional market for biomass)

• Case (diverse DH systems in terms of fuel use and DH

production technology)

• Reference group

• Scenario analysis (to explore not to predict)

• Sensitivity analysis

Two options:

–“Connection”

– “No-connection”

Climate policy scenarios

• 450PPM (450 ppm)

• NEWPOL (New Policies)

(Energy prices and CO2 charge calculated by ENPAC tool)

International Energy

Agency (World Energy

Outlook)

Sensitivity analysis (I)

• NONG

NG use is not allowed after 2030

• REHD (Reduced Heat Demand)

2010-2030 10% linear reduction

2030-2050 10% linear reduction

• LIC (Low Investment Cost)

About 50% lower pipeline cost

• INTRATE (INTerest RATE)

(2.5% and 30 yrs for pipelines &

11% and 15 yrs for heat exchangers)

Sensitivity analysis (II)

• REFINERY

Refineries in Gothenburg supply heat until 2050

• RES-S (Renewable Energy Sources Support)

Constant subsidies for renewable electricity at level

of 2010

• NOSNG

No alternative regional biomass demand

(single-sector perspective)

Methodology

• Regional level (regional market for biomass)

• Case (diverse DH systems in terms of fuel use and DH production

technology)

• Reference group

• Scenario analysis

• Energy system modeling (MARKAL - optimization

bottom-up model)

–Optimization (including the new infrastructure

capacity)

–Comparison of “connection” to “no-

connection”

Model

MARKAL_West_Sweden (MARKAL_WS) model representing the energy system of the Västra Götaland Region

• Time horizon: 2010-2050

– 4 seasons per year

• Cold winter (1 month)

• Winter (2 months)

• Spring and fall (4 months)

• Summer (5 months)

• 37 DH systems with different system characteristics:

– Demand levels

– Installed capacities

– Investment options for District heating supply

Model

• Investment options for the heat network between the cluster of

chemical industries in Stenungsund and the Gothenburg/

Kungälv DH systems.

• Bio-refinery, GoBiGas 1& 2, for SNG (synthetic natural gas)

production (biomass competitor)

Optimum timing and capacity

Results

Technology change in VG

Differences between “connection” and “no-connection”

Total system cost in VG

Differences between “connection” and “no-connection”

Marginal Cost in Gothenburg

Differences between “connection” and “no-connection”

Marginal Cost in Kungälv

Differences between “connection” and “no-connection”

Conclusion

• Investment in the large heat network is cost-effective except if:

– Other major sources of excess heat are more closely located.

– There is an abundance of low cost biomass available in the

region.

• Higher future fossil fuel prices are likely to increase the profitability

of the investments.

• Higher interest rates would reduce this profitability.

• Reduced marginal cost of DH supply in the Gothenburg and

Kungälv DH systems in most seasons (except for the cold

seasons).

Thank you!

NEWPOL

Policy tools 2010/2020/2030/2040/2050

CO2 charge EUR/tone 16.9/14.4/23.8/33.5/43

Renewable electricity subsidy EUR/MWh 20/20/0/0/0

Energy prices/costs (i) 2010/2020/2030/2050

NG EUR/MWh 28.7/29.2/30.2/33

EO1 EUR/MWh 64.2/66.2/70/80

EO5 EUR/MWh 41.6/43.1/46/53.5

Forest residues EUR/MWh Supply curves

Energy forest (willow) EUR/MWh 20

Wood chips EUR/MWh 21.8/29/32/38

Bio pellets EUR/MWh 35/41/45/53

Excess heat EUR/MWh 0.56

Municipal waste EUR/MWh -22

Electricity

Winter cold (1 month) EUR/MWh 70/87/96/106

Winter (2 months) EUR/MWh 64/80/88/97

Spring and fall (4 months) EUR/MWh 50/63/69/76

Summer (5 months) EUR/MWh 36/44/49/54

SNG EUR/MWh 53/71.3/76.5/88.9

Others

Land available for energy forest

(willow) Ha 1000/18950/36900/36900

Refineries in Gothenburg No excess heat delivery by 2025

NG import Allowed until 2050

Heat demand Constant (at 2010 level)

2010/2020/2030/2040/2050

16.9/25.2/68.4/110/153

450PPM

20/20/0/0/0

2010/2020/2030/2050

28.7/28.3/25.1/18.5

64.2/64.7/61.8/54.9

41.6/42/39.8/37.2/34.6

53/73/80/94

Supply curves

20

21.8/29/43/66

35/42/58/87

0.56

50/70/81/86

-22

70/97/113/119

64/89/103/109

36/49/58/61

1000/18950/36900/36900

Allowed until 2050

Constant (at 2010 level)

No excess heat delivery by 2025

SKG pipeline

Cap≤ 50 MW 1800/ 0.25 Cap≤ 50 MW 1100/ 0.25

50˂Cap≤ 100 MW 2200/ 0.12 50˂Cap≤ 100 MW 1200/0.12

100˂Cap≤ 150 MW 2600/ 0.08 100˂Cap≤ 150 MW 1300/ 0.08

Length km

SK pipeline

Investment/ Variable

O&M Cost

[EUR/m]/

[EUR/MWh

heat]

Cap≤ 50 MW 1800/ 0.16 Cap≤ 50 MW 1100/ 0.16

Length km

EH-CCIS extraction

Cap ≤ 20 MW 4.4 Cap ≤ 20 MW 4.4

20˂Cap ≤ 40 MW 6.7 20˂Cap ≤ 40 MW 6.7

40˂Cap ≤ 60 MW 12.8 40˂Cap ≤ 60 MW 12.8

60˂Cap ≤ 80 MW 20.6 60˂Cap ≤ 80 MW 20.6

80˂Cap ≤ 100 MW 26.7 80˂Cap ≤ 100 MW 26.7

100˂Cap ≤ 120 MW 37.8 100˂Cap ≤ 120 MW 37.8

120˂Cap ≤ 140 MW 51.1 120˂Cap ≤ 140 MW 51.1

140˂Cap ≤ 150 MW 61.1 140˂Cap ≤ 150 MW 61.1

450PPM and NEWPOL LIC

55

Investment/ Variable

O&M Cost

[EUR/m]/

[EUR/MWh

heat]

55

Investment cost

(80/50 hot water)MEUR

35 35

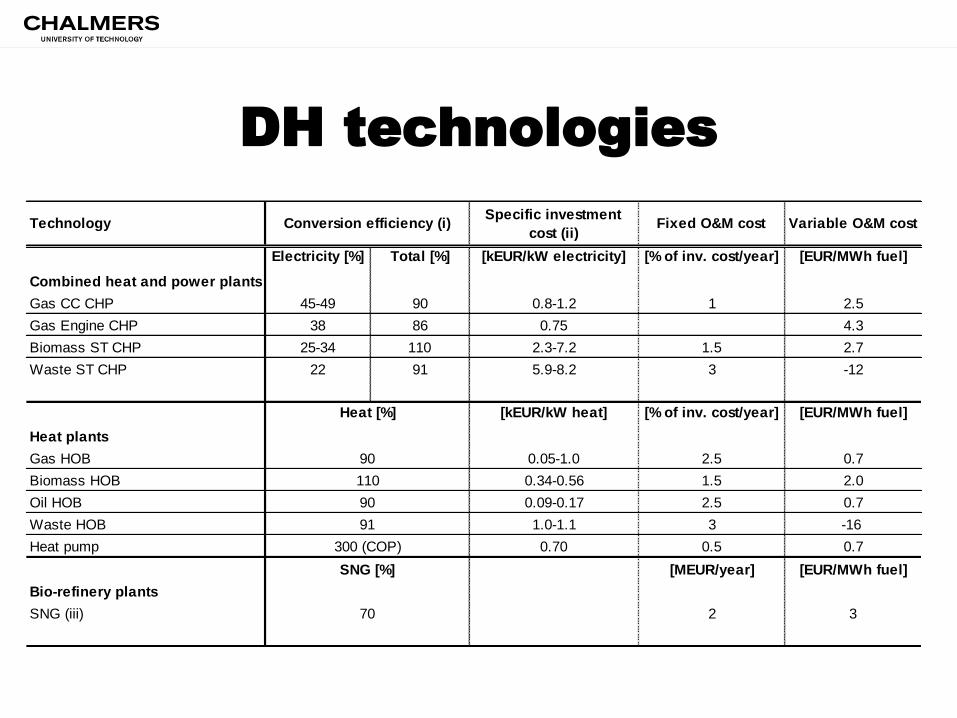

DH technologies

Gas CC CHP 45-49 90 0.8-1.2 1 2.5

Gas Engine CHP 38 86 0.75 4.3

Biomass ST CHP 25-34 110 2.3-7.2 1.5 2.7

Waste ST CHP 22 91 5.9-8.2 3 -12

Gas HOB 0.05-1.0 2.5 0.7

Biomass HOB 0.34-0.56 1.5 2.0

Oil HOB 0.09-0.17 2.5 0.7

Waste HOB 1.0-1.1 3 -16

Heat pump 0.70 0.5 0.7

[MEUR/year] [EUR/MWh fuel]

Bio-refinery plants

SNG (iii) 2 3

[EUR/MWh fuel]

Heat plants

Fixed O&M cost Variable O&M cost

Electricity [%] Total [%] [kEUR/kW electricity] [% of inv. cost/year] [EUR/MWh fuel]

Heat [%] [kEUR/kW heat]

Specific investment

cost (ii)

Combined heat and power plants

91

SNG [%]

70

300 (COP)

[% of inv. cost/year]

90

Technology Conversion efficiency (i)

110

90