economic expansion, commercial real estate-what’s next?€¦ · economic expansion & real...

TRANSCRIPT

Keynote:

Economic Expansion, Commercial Real Estate- What’s Next?

Economic Expansion & Real EstateWhat’s Next – Near Term & Long Term?Business Cycles, Technological Change, the Policy Environment, and the Future of Multifamily & Commercial Real Estate

April 30, 2019Victor Calanog PhD | Chief EconomistMoody’s Analytics | REIS

REIS, Real Estate Solutions by Moody’s Analytics

1. ECONOMIC OVERVIEW AND OUR OUTLOOK FOR THE NEAR TERM.

2. THE LATEST TRENDS FOR MULTIFAMILY, OFFICE, RETAIL, AND INDUSTRIAL. CHANGES IN DEMOGRAPHICS, USE OF SPACE, TECHNOLOGY, AND THE POLICY ENVIRONMENT THAT AFFECTS THE FUTURE OF SPECIFIC PROPERTY TYPES.

3. A DISCUSSION OF INTEREST RATES, THE YIELD CURVE, AND VARIOUS RECESSIONARY RISK FACTORS.

4. Q & A

Agenda

REIS, Real Estate Solutions by Moody’s Analytics

1.0%

1.8%

2.8%

3.8%3.3%

2.7%

1.8%

‐0.3%

‐2.8%

2.6%

1.6%2.2%

1.8%

2.5%2.9%

1.6%

2.2%

2.9%

2.3%

0.7%

3.1%

2.2% 2.2%

‐4.0%

‐3.0%

‐2.0%

‐1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

2001 2003 2005 2007 2009 2011 2013 2015 2017 2019 2021 2023

Annual GDP Growth2001 - 2023

Source: Bureau of Economic Analysis; Economy.com

Forecast

REIS, Real Estate Solutions by Moody’s Analytics

World’s Region North America Other Countries Africa Asia Australia Europe South America Middle East

The World Economy2017 GDP, $ in trillions

Source: Worldbank

REIS, Real Estate Solutions by Moody’s Analytics

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

‐900

‐700

‐500

‐300

‐100

100

300

500

700

Jan2007

Jan2008

Jan2009

Jan2010

Jan2011

Jan2012

Jan2013

Jan2014

Jan2015

Jan2016

Jan2017

Jan2018

Jan2019

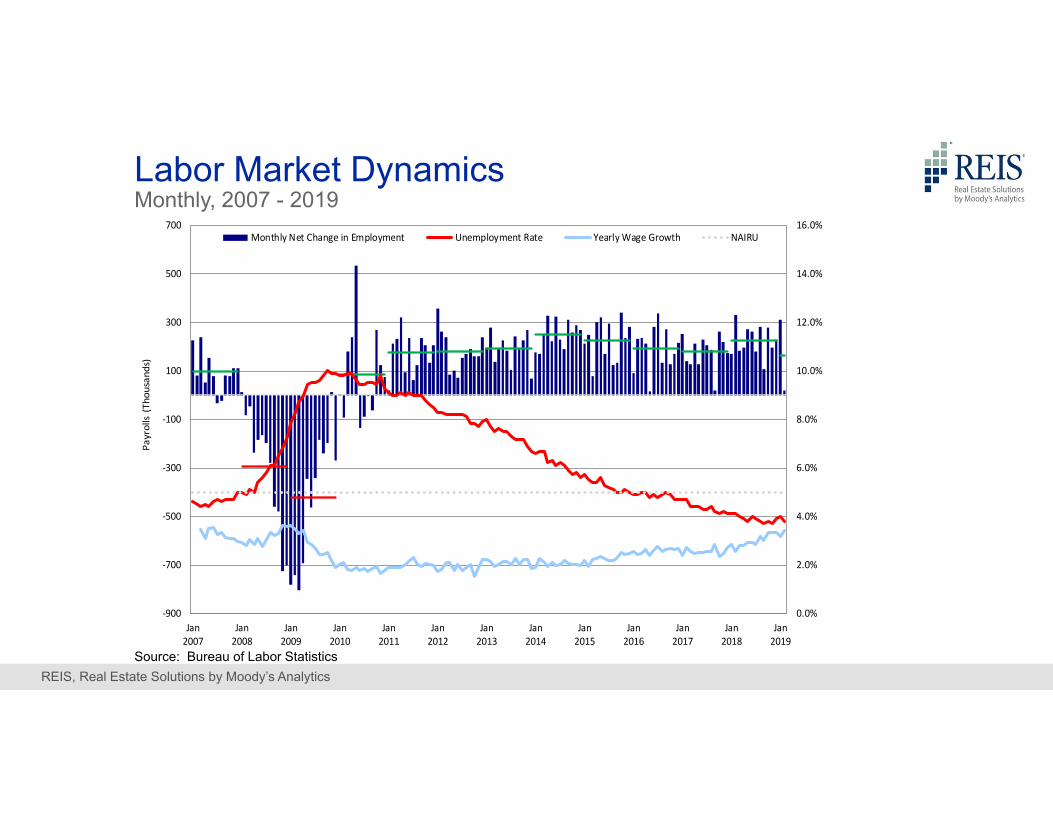

Payrolls (Thousands)

Monthly Net Change in Employment Unemployment Rate Yearly Wage Growth NAIRU

Labor Market DynamicsMonthly, 2007 - 2019

Source: Bureau of Labor Statistics

REIS, Real Estate Solutions by Moody’s Analytics

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%

5.5%

6,000

8,000

10,000

12,000

14,000

16,000

18,000

20,000

22,000

24,000

26,000

28,000

4/1/2010 4/1/2011 4/1/2012 4/1/2013 4/1/2014 4/1/2015 4/1/2016 4/1/2017 4/1/2018 4/1/2019

10‐Year Treasury Rate

Dow

Jones Industria

l Average

Dow Jones Industrial Average 10 Year Treasury Rate

DJIA vs. 10-Year Treasury RateDaily, 04/2010 – 04/2019

Source: FRED; Federal Reserve Bank of Philadelphia

REIS, Real Estate Solutions by Moody’s Analytics

The Economic Outlook

» US GDP growth for 2018 likely to have been as strong as in 2014 (the strongest growth year since the end of the last recession); consensus forecasts suggest that 2019 will drop back down to the low 2s, which has been CAGR since the end of the recession in mid‐2009.

» Moderation does not mean contraction, although this does render growth vulnerable to shocks or shifts in sentiment.

» How does all this translate to how different property types performed in late 2018 and early 2019?

» We will, however, discuss some thoughts on what will cause the next recession, towards the end of this presentation. Hang on!

Key Takeaways for 2018 and 2019

REIS, Real Estate Solutions by Moody’s Analytics

Year QtrAsking Rent

Percent Change

Effect ive Rent

Percent Change

Vacancy Rate

2011 4 $1,070 0.5% $1,019 0.6% 5.3%2012 1 $1,077 0.6% $1,028 0.9% 5.0%2012 2 $1,089 1.2% $1,043 1.4% 4.9%2012 3 $1,100 1.0% $1,053 1.0% 4.8%2012 4 $1,107 0.7% $1,061 0.7% 4.7%2013 1 $1,114 0.6% $1,068 0.7% 4.4%2013 2 $1,123 0.9% $1,078 0.9% 4.4%2013 3 $1,135 1.1% $1,090 1.1% 4.4%2013 4 $1,146 0.9% $1,100 1.0% 4.4%2014 1 $1,155 0.8% $1,110 0.8% 4.2%2014 2 $1,168 1.1% $1,123 1.2% 4.3%2014 3 $1,183 1.3% $1,137 1.3% 4.3%2014 4 $1,192 0.8% $1,146 0.8% 4.3%2015 1 $1,205 1.0% $1,158 1.1% 4.2%2015 2 $1,226 1.8% $1,179 1.7% 4.2%2015 3 $1,248 1.8% $1,199 1.8% 4.2%2015 4 $1,262 1.1% $1,212 1.1% 4.3%2016 1 $1,273 0.9% $1,223 0.9% 4.3%2016 2 $1,291 1.4% $1,239 1.3% 4.2%2016 3 $1,307 1.3% $1,254 1.2% 4.1%2016 4 $1,313 0.5% $1,260 0.4% 4.2%2017 1 $1,324 0.9% $1,268 0.6% 4.3%2017 2 $1,345 1.6% $1,285 1.4% 4.3%2017 3 $1,364 1.4% $1,301 1.3% 4.4%2017 4 $1,373 0.7% $1,309 0.6% 4.6%2018 1 $1,389 1.1% $1,324 1.1% 4.7%2018 2 $1,409 1.5% $1,342 1.4% 4.7%2018 3 $1,429 1.4% $1,360 1.3% 4.8%2018 4 $1,441 0.8% $1,371 0.8% 4.9%

National Apartment MarketQuarterly and Annual Market Conditions

Source: Reis, Real Estate Solutions by Moody’s Analytics; 79 of 275 Apartment Markets

» Vacancies continuing to rise – as expected –ending the fourth quarter at 4.9%.

» Asking and effective rents still relatively healthy at 0.8% in the fourth quarter.

» Delays have moved relief from supply glut issues to next year, as 2019 promises to be the sector’s ‘cyclical high.’ Measures of demand remain strong, however.

YearAskingRent

Percent Change

Effect ive Rent

Percent Change

Vacancy Rate

2009 $1,026 ‐2.3% $969 ‐2.5% 8.0%2010 $1,045 1.8% $992 2.4% 6.6%2011 $1,070 2.4% $1,019 2.7% 5.3%2012 $1,107 3.5% $1,061 4.1% 4.7%2013 $1,146 3.5% $1,100 3.7% 4.4%2014 $1,192 4.0% $1,146 4.2% 4.3%2015 $1,262 5.8% $1,212 5.8% 4.3%2016 $1,313 4.0% $1,260 3.9% 4.2%2017 $1,373 4.6% $1,309 4.0% 4.6%2018 $1,441 4.9% $1,371 4.7% 4.9%2019 $1,500 4.2% $1,425 4.0% 5.1%2020 $1,546 3.0% $1,466 2.9% 5.2%2021 $1,582 2.4% $1,499 2.2% 5.2%2022 $1,617 2.2% $1,530 2.1% 5.3%2023 $1,651 2.1% $1,561 2.0% 5.4%

REIS, Real Estate Solutions by Moody’s Analytics

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

‐50

0

50

100

150

200

250

300

350

400

1983 1987 1991 1995 1999 2003 2007 2011 2015 2019 2023

Vacancy Rate

Units (In Thou

sand

s)

Completions Net Absorption Vacancy Percent

Forecast

National Apartment MarketSupply & Demand Trends

Source: Reis, Real Estate Solutions by Moody’s Analytics; Top 50 Primary Apartment Markets

REIS, Real Estate Solutions by Moody’s Analytics

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

‐2

‐1

0

1

2

3

4

5

6

7

1983 1987 1991 1995 1999 2003 2007 2011 2015 2019 2023

Vacancy Rate

Units (In Thousands)

Completions Net Absorption Vacancy Percent

Forecast

DC Apartment MarketSupply & Demand Trends

Source: Reis, Real Estate Solutions by Moody’s Analytics

REIS, Real Estate Solutions by Moody’s Analytics

0

1

2

3

4

5

6

2012 2013 2014 2015 2016 2017 2018

Units

(In Thou

sand

s)

Anacostia/Northeast DC Other Capitol Hill/Southwest Downtown/Logan Circle

Completions by Submarket (DC)2012-2018, Yearly

Source: Reis, Real Estate Solutions by Moody’s Analytics

REIS, Real Estate Solutions by Moody’s Analytics

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

0

2

4

6

8

10

12

14

16

18

1983 1987 1991 1995 1999 2003 2007 2011 2015 2019 2023

Vacancy Rate

Units (In Thou

sand

s)

Completions Net Absorption Vacancy Percent

Forecast

NY Apartment MarketSupply & Demand Trends

Source: Reis, Real Estate Solutions by Moody’s Analytics

REIS, Real Estate Solutions by Moody’s Analytics

Completions by Submarket (NY)2012-2018, Yearly

Source: Reis, Real Estate Solutions by Moody’s Analytics

REIS, Real Estate Solutions by Moody’s Analytics

Demographic Tailwinds

Source: U.S. Census Bureau, Population Division

3.0

3.2

3.4

3.6

3.8

4.0

4.2

4.4

4.6

4.8

5.0

19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42

Popu

latio

n (M

illions)

Age in 2018

REIS, Real Estate Solutions by Moody’s Analytics

3%

6%

9%

12%

15%

18%

21%

24%

‐150

‐100

‐50

0

50

100

150

200

1983 1987 1991 1995 1999 2003 2007 2011 2015 2019 2023

Vacancy Rate

Square Feet (In M

illions)

Completions Net Absorption Vacancy Percent

Forecast

National Office MarketSupply & Demand Trends

Source: Reis, Real Estate Solutions by Moody’s Analytics; Top 50 Primary Office Markets

REIS, Real Estate Solutions by Moody’s Analytics

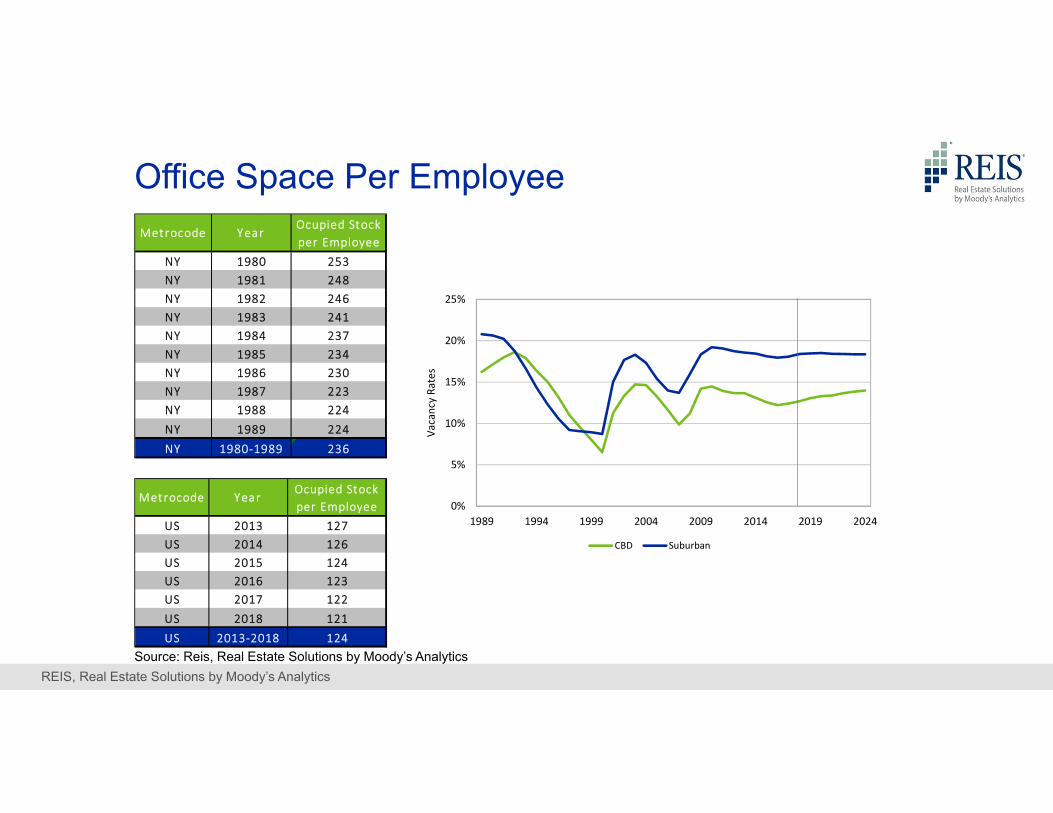

Office Space Per Employee

0%

5%

10%

15%

20%

25%

1989 1994 1999 2004 2009 2014 2019 2024

Vacancy Ra

tes

CBD Suburban

NY 1980 253NY 1981 248NY 1982 246NY 1983 241NY 1984 237NY 1985 234NY 1986 230NY 1987 223NY 1988 224NY 1989 224NY 1980‐1989 236

Metrocode YearOcupied Stock per Employee

US 2013 127US 2014 126US 2015 124US 2016 123US 2017 122US 2018 121US 2013‐2018 124

Metrocode YearOcupied Stock per Employee

Source: Reis, Real Estate Solutions by Moody’s Analytics

REIS, Real Estate Solutions by Moody’s Analytics

3.5

3.6

3.9

5.1

5.2

0 2 4 6

Bank of America/Merrill Lynch

Morgan Stanley

CitiGroup

WeWork

JPMorgan Chase & Co.

Millions of Square Feet

WeWork’s Growing InfluenceManhattan’s Largest Office Tenants by Square Footage

Source: Cushman & Wakefield(As of August 2018)

» As of September 2018, WeWork is now the largest office tenant in Manhattan with 5.3 Million Square Feet

» The Co-Sharing Company is the second largest occupier of office space in London, after government office space

REIS, Real Estate Solutions by Moody’s Analytics

2008 Y $40.48 0.3% 7.1%2009 Y $39.03 ‐3.6% 8.8%2010 Y $38.79 ‐0.6% 8.7%2011 Y $38.92 0.3% 9.2%2012 Y $39.31 1.0% 8.6%2013 Y $39.95 1.6% 7.9%2014 Y $40.66 1.8% 8.0%2015 Y $41.54 2.2% 7.8%2016 Y $42.38 2.0% 7.8%2017 Y $43.00 1.5% 8.3%2018 Y $43.35 0.8% 9.0%

Year QuarterAsking Rent

Percent Change

Vacancy Rate

2009 ‐21.5 $19.13 ‐2.0% $16.75 ‐3.7% 10.6%2010 ‐3.2 $18.99 ‐0.7% $16.51 ‐1.4% 11.0%2011 6.3 $18.99 0.0% $16.50 ‐0.1% 11.0%2012 11.3 $19.08 0.5% $16.59 0.5% 10.7%2013 12.7 $19.35 1.4% $16.83 1.4% 10.4%2014 13.4 $19.70 1.8% $17.17 2.0% 10.2%2015 12.3 $20.11 2.1% $17.55 2.2% 10.0%2016 12.4 $20.48 1.8% $17.90 2.0% 9.9%2017 9.4 $20.88 2.0% $18.27 2.1% 10.0%2018 1.4 $21.21 1.6% $18.57 1.6% 10.2%2019 5.8 $21.51 1.4% $18.84 1.5% 10.3%2020 7.5 $21.79 1.3% $19.09 1.3% 10.3%2021 7.8 $22.14 1.6% $19.39 1.6% 10.2%2022 8.1 $22.54 1.8% $19.73 1.8% 10.2%2023 8.7 $22.96 1.9% $20.09 1.8% 10.1%

Percent Change

Vacancy Rate

YearNet

Absorpt ionAsking Rent

Percent Change

Effect ive Rent

2011 4 4.5 $18.99 0.1% $16.50 0.1% 11.0%2012 1 3.5 $19.00 0.1% $16.52 0.1% 10.9%2012 2 2.7 $19.03 0.2% $16.54 0.1% 10.8%2012 3 2.1 $19.06 0.2% $16.57 0.2% 10.8%2012 4 3.1 $19.08 0.1% $16.59 0.1% 10.7%2013 1 2.9 $19.14 0.3% $16.64 0.3% 10.6%2013 2 2.9 $19.20 0.3% $16.69 0.3% 10.5%2013 3 2.2 $19.26 0.3% $16.75 0.4% 10.5%2013 4 4.6 $19.35 0.5% $16.83 0.5% 10.4%2014 1 1.2 $19.43 0.4% $16.91 0.5% 10.4%2014 2 3.3 $19.52 0.5% $16.99 0.5% 10.3%2014 3 4.1 $19.60 0.4% $17.07 0.5% 10.3%2014 4 4.8 $19.70 0.5% $17.17 0.6% 10.2%2015 1 3.6 $19.80 0.5% $17.27 0.6% 10.1%2015 2 2.5 $19.90 0.5% $17.36 0.5% 10.1%2015 3 3.7 $20.01 0.6% $17.46 0.6% 10.0%2015 4 2.5 $20.11 0.5% $17.55 0.5% 10.0%2016 1 3.1 $20.22 0.5% $17.66 0.6% 9.9%2016 2 3.8 $20.30 0.4% $17.73 0.4% 9.8%2016 3 1.1 $20.39 0.4% $17.81 0.5% 9.9%2016 4 4.4 $20.48 0.4% $17.90 0.5% 9.9%2017 1 2.7 $20.56 0.4% $17.98 0.4% 9.9%2017 2 1.1 $20.66 0.5% $18.07 0.5% 10.0%2017 3 1.9 $20.76 0.5% $18.16 0.5% 10.0%2017 4 3.6 $20.88 0.6% $18.27 0.6% 10.0%2018 1 1.2 $20.97 0.4% $18.36 0.5% 10.0%2018 2 ‐3.7 $21.03 0.3% $18.41 0.3% 10.2%2018 3 2.6 $21.13 0.5% $18.49 0.4% 10.2%2018 4 1.4 $21.21 0.4% $18.57 0.4% 10.2%

Percent Change

Vacancy Rate

Year QtrNet

Absorpt ionAsking Rent

Percent Change

Effect ive Rent

National Retail MarketQuarterly and Annual Market Conditions

Source: Reis, Real Estate Solutions by Moody’s Analytics; 77 of 190 Office MarketsNet Absorption figures are in millions of square feet.

Regional/Super Regional Malls

Neighborhood and Community Shopping Centers

REIS, Real Estate Solutions by Moody’s Analytics

5%

6%

7%

8%

9%

10%

11%

12%

‐30

‐15

0

15

30

45

60

75

1983 1987 1991 1995 1999 2003 2007 2011 2015 2019 2023

Vacancy Rate

Square Feet (in M

illions)

Completions Net Absorption Vacancy Percent

Forecast

National Retail MarketSupply & Demand Trends

Source: Reis, Real Estate Solutions by Moody’s Analytics; Top 50 Primary Retail Markets

REIS, Real Estate Solutions by Moody’s Analytics

Retail e-commerce trends

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

$0

$2

$4

$6

$8

$10

2004 2006 2008 2010 2012 2014 2016

Billion

s of Dollars in

Sales

Electronics and appliance stores

Sporting goods, hobby, musical instrument, and book stores

Clothing Stores

% of Retail Revenue from E‐commerce

Source: U.S. Census Bureau, Population Division

REIS, Real Estate Solutions by Moody’s Analytics

8%

9%

10%

11%

12%

13%

0.3%

0.4%

0.5%

0.6%

0.7%

0.8%

0.9%

1.0%

1.1%

1.2%

1.3%

2015Q4 2016Q2 2016Q4 2017Q2 2017Q4 2018Q2 2018Q4

Vacancy Rate

Effective Re

nt Growth

Effective Rent Growth Vacancy Rate

9%

10%

11%

12%

13%

14%

0.1%

0.2%

0.3%

0.4%

0.5%

0.6%

0.7%

0.8%

0.9%

1.0%

1.1%

2015Q4 2016Q2 2016Q4 2017Q2 2017Q4 2018Q2 2018Q4

Vacancy Rate

Effective Re

nt Growth

Effective Rent Growth Vacancy Rate

» Flex/R&D vacancies rose by 10 basis points to 9.8% after falling the previous quarter.

» Effective rents grew at the same clip as the past quarter.

» Warehouse/distribution vacancies fell to 9.3% in the fourth quarter.

» Some evidence of recovery on the pricing side, with effective rents growing by 0.8% (an improvement over the first half of the year).

Industrial: Upward for 2018

Source: Reis, Real Estate Solutions by Moody’s Analytics

Flex/R&D

Wareh

ouse/

Distrib

ution

REIS, Real Estate Solutions by Moody’s Analytics

‐2%

‐1%

0%

1%

2%

West Southwest South Atlantic Northeast Midwest

Year‐Over‐Year Rent Growth by Region, 2018Q4 (Non‐Climate Controlled 10x10 Units)

86%

88%

90%

92%

2015Q4 2016Q2 2016Q4 2017Q2 2017Q4 2018Q2 2018Q4

National Occupancy Rates (50 Metropolitan Areas)» Occupancies weakened by 150 basis points in the fourth quarter, ending the period at 86.6%

» Climate-controlled 10x10 unit rents fell by 2.4%, and non-climate-controlled 10x10 unit rents fell by 1.8%

» Supply concerns may ease as soon as this year, but it remains to be seen if sector fundamentals will improve significantly as it tries to absorb new deliveries.

Self-Storage in the Fourth Quarter

Source: Reis, Real Estate Solutions by Moody’s Analytics

REIS, Real Estate Solutions by Moody’s Analytics

How About All the Others?

Source: U.S. Census Bureau, Population Division

REIS, Real Estate Solutions by Moody’s Analytics

8.2%

8.3%

8.4%

8.5%

8.6%

8.7%

8.8%

8.9%

9.0%

9.1%

9.2%

9.3%

9.4%

9.5%

9.6%

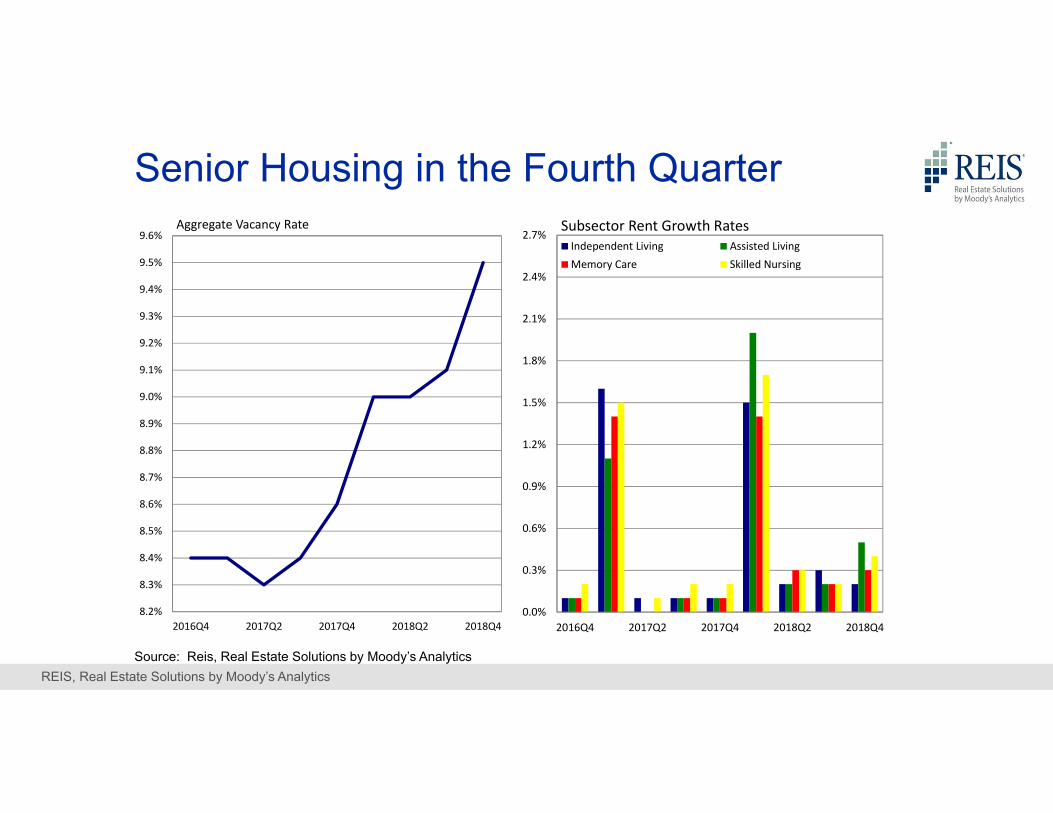

2016Q4 2017Q2 2017Q4 2018Q2 2018Q4

Aggregate Vacancy Rate

0.0%

0.3%

0.6%

0.9%

1.2%

1.5%

1.8%

2.1%

2.4%

2.7%

2016Q4 2017Q2 2017Q4 2018Q2 2018Q4

Subsector Rent Growth RatesIndependent Living Assisted LivingMemory Care Skilled Nursing

Senior Housing in the Fourth Quarter

Source: Reis, Real Estate Solutions by Moody’s Analytics

REIS, Real Estate Solutions by Moody’s Analytics

0

10

20

30

40

50

60

70

80

1996 1998 2000 2002 2004 2006 2008 2010 2012 20140

20

40

60

80

100

120Thousands

A Slide That Will Remain UntitledHow Did That Slide Get In There?

Source: Center for Disease Control

26

REIS, Real Estate Solutions by Moody’s Analytics

Vacancy Rate Vacancy Chg, BPS Rent Growth Inventory GrowthBed 4.6% ‐40 2.7% 5.4%Unit 2.5% ‐10 2.6% 2.6%

National Student Housing Market, Fall 2018 – Fall 2019

0% 1% 2% 3% 4% 5%

National

Northeast

South Atlantic

Midwest

Southwest

West

Regional Rent Growth, Fall 2018 – Fall 2019

Unit Bed

» Tables present Fall 2018 to Fall 2019 expected trends in vacancies and rent change.

» We expect a continued decrease in vacancies, despite strong supply growth, particularly for properties that rent by the Bed.

» We expect a good year (Fall 2018 to Fall 2019) for student housing properties – with properties in the Southwest that rent by the Unit forecasted to show the strongest rent growth.

Student Housing in the Fourth Quarter

Source: Reis, Real Estate Solutions by Moody’s Analytics

REIS, Real Estate Solutions by Moody’s Analytics

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

0.0%

0.3%

0.6%

0.9%

1.2%

1.5%

1.8%

2.1%

2.4%

2.7%

Detroit Oakland‐EastBay

Nashville Cincinnati Los Angeles US Aggregate

Vacancy RateRent Growth

Top Five Affordable Housing Markets by 2018Q4 Rent Growth

Affordable Rent Growth Market Rate Rent Growth Affordable Vacancy Market Rate Vacancy

» National aggregations for vacancies of LIHTC properties remained very tight at 2.3% (though this represents a 20 basis point increase year over year).

» Because of tax reform lowering the value of LIHTC tax credits, we estimate a 40% reduction in LIHTC deliveries over the five year forecast period – relative to baseline. What is to be done?

LIHTC in the Fourth Quarter

Source: Reis, Real Estate Solutions by Moody’s Analytics

REIS, Real Estate Solutions by Moody’s Analytics

Driverless CarsInvestor’s Expectations of AV’s Impact on Parking and Development Opportunities

Source: Deloitte

REIS, Real Estate Solutions by Moody’s Analytics

» Opportunity Zones as the latest iteration of “investing in places.”

» Who wins when places compete for business? The Amazon HQ2 story.

» How should one think of policy interventions and assess its impacts?

» What about other real estate related policy initiatives? Is infrastructure spending even part of the conversation these days (it should be)?

The Changing Policy Environment

REIS, Real Estate Solutions by Moody’s Analytics

2.3%

2.4%

2.5%

2.6%

2.7%

2.8%

2.9%

3.0%

11/25/2018 12/5/2018 12/15/2018 12/25/2018 1/4/2019 1/14/2019 1/24/2019 2/3/2019

2 Yr 3 Yr 5 Yr

2.1%

2.3%

2.5%

2.7%

2.9%

3.1%

3.3%

3.5%

11/25/2018 12/5/2018 12/15/2018 12/25/2018 1/4/2019 1/14/2019 1/24/2019 2/3/2019

2 Yr 3 Yr 5 Yr 10 Yr 20 Yr 30 Yr

Yield Curve TighteningShorter term maturities invert, longer maturities retain higher rates

Shorter term InversionShorter term yields vs. 5‐Yr TSY recently inverted

However…Longer maturities have not yet dropped below shorter term yields

Source: U.S. Department of the Treasury

REIS, Real Estate Solutions by Moody’s Analytics

» The US economy grew by 2.9% in 2018 – matching the recent cyclical high from 2014, dated from when the last recession ended.

» A climb down back to the low 2s in 2019 does not mean a contraction.

» Short of an exogenous shock, a recession (however minor) can stem from a multitude of firms and individuals cutting back, however slightly, because they are acting prudently. The systemic result, however, can be economic contraction. Are you talking yourself into a recession?

» Multifamily and Self-Storage vacancies rising because of supply conditions, but will ease as soon as next year. Student Housing and Affordable Housing properties are relatively tight; Senior Housing needs to deal with demographic challenges. Other commercial property types not doing nearly as well as multifamily (with the possible exception of Industrial).

Summary and Parting ThoughtsSo, what will cause the next recession?

Economic Expansion & Real EstateWhat’s Next – Near Term & Long Term?Business Cycles, Technological Change, the Policy Environment, and the Future of Multifamily & Commercial Real Estate

April 30, 2019Victor Calanog PhD | Chief EconomistMoody’s Analytics | REIS