econ/fin 250: forecasting in finance and economics...

TRANSCRIPT

ECON/FIN 250: Forecasting in Finance and Economics:Section 3.2 Filtering Time Series

Patrick Herb

Brandeis University

Spring 2016

Patrick Herb (Brandeis University) Filtering Time Series ECON/FIN 250: Spring 2016 1 / 39

Course Overview

1 General Filtering Thoughts

2 Two-Sided Filters

3 One-Sided Filters

4 Local Trends

Patrick Herb (Brandeis University) Filtering Time Series ECON/FIN 250: Spring 2016 2 / 39

General Filtering Thoughts

Time series tools that can:Estimate TrendsSmooth Out NoiseAdjust for SeasonalityMake ForecastsSeparate the Cycle from the Trend

Somewhat ad hocCommon, simple rules used in business forecastingRelated to technical analysis in finance

Patrick Herb (Brandeis University) Filtering Time Series ECON/FIN 250: Spring 2016 3 / 39

Two-Sided Filters

1 General Filtering Thoughts

2 Two-Sided Filters

3 One-Sided Filters

4 Local Trends

Patrick Herb (Brandeis University) Filtering Time Series ECON/FIN 250: Spring 2016 4 / 39

Moving Average Filter

Uses Data Before & After time = tSmooths Data Using Future & Past InformationCan Choose Information SetCan Weight Observations EquallyCan Choose Alternative WeightsNot Useful for ForecastingCan Improve Understanding of the Data

Patrick Herb (Brandeis University) Filtering Time Series ECON/FIN 250: Spring 2016 5 / 39

Moving Average Filter

Equally Weighted

y∗t = 1

2m + 1

m∑j=−m

yt+j (1)

Alternative Weighting

y∗t =

m∑j=−m

ωjyt+j (2)

Weights should have the property:m∑

j=−mωj = 1 (3)

Patrick Herb (Brandeis University) Filtering Time Series ECON/FIN 250: Spring 2016 6 / 39

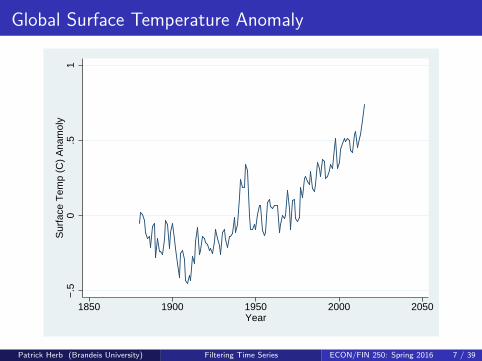

Global Surface Temperature Anomaly

−.5

0.5

1S

urfa

ce T

emp

(C)

Ana

mol

y

1850 1900 1950 2000 2050Year

Patrick Herb (Brandeis University) Filtering Time Series ECON/FIN 250: Spring 2016 7 / 39

Global Surface Temperature Anomaly

Let’s use an equally weighted moving average filter to reduce some of thenoise. Try m = 2use temperaturetsset yeartssmooth ma tempma = tempa , window (2 1 2)tsline tempa tempma

Patrick Herb (Brandeis University) Filtering Time Series ECON/FIN 250: Spring 2016 8 / 39

Global Surface Temperature Anomaly

−.5

0.5

1

1850 1900 1950 2000 2050Year

Surface Temp (C) Anamoly ma: x(t)= tempa: window(2 1 2)

Patrick Herb (Brandeis University) Filtering Time Series ECON/FIN 250: Spring 2016 9 / 39

Global Surface Temperature Anomaly

Still pretty noisy. Try m = 5tssmooth ma temp_ma = tempa , window (5 1 5)tsline tempa temp_ma

Patrick Herb (Brandeis University) Filtering Time Series ECON/FIN 250: Spring 2016 10 / 39

Global Surface Temperature Anomaly

−.5

0.5

1

1850 1900 1950 2000 2050Year

Surface Temp (C) Anamoly ma: x(t)= tempa: window(5 1 5)

Patrick Herb (Brandeis University) Filtering Time Series ECON/FIN 250: Spring 2016 11 / 39

Low Frequency Filters

Can be used to remove the trendAllows the trend to changeCommon Macroeconomic Approach

Ignore GrowthConcentrate on Business CycleOutput Gap

Patrick Herb (Brandeis University) Filtering Time Series ECON/FIN 250: Spring 2016 12 / 39

Low Frequency Filters

ExamplesHodrick / Prescott FilterBaxter / KingButterworth

Type: help filter

Patrick Herb (Brandeis University) Filtering Time Series ECON/FIN 250: Spring 2016 13 / 39

Hodrick / Prescott Filter

The HP Filter:

miny∗

t

T∑t=1

(yt − y∗t )2 + λ

T−1∑t=2

[(y∗t+1 − y∗

t )− (y∗t − y∗

t−1]2 (4)

This filter is approximately a two-way moving average with weights subjectto a damped harmonic

λ is a positive smoothing parameterSmaller λ, penalizes variability in the cyclical componentLarger λ, penalizes variability in the growth component

Patrick Herb (Brandeis University) Filtering Time Series ECON/FIN 250: Spring 2016 14 / 39

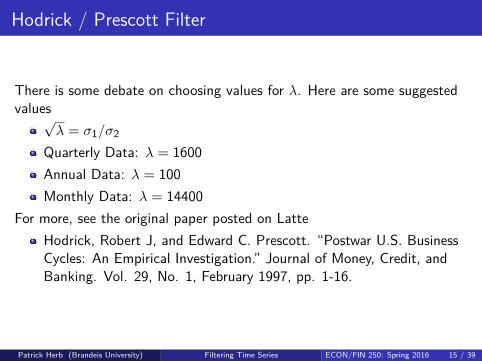

Hodrick / Prescott Filter

There is some debate on choosing values for λ. Here are some suggestedvalues√

λ = σ1/σ2

Quarterly Data: λ = 1600Annual Data: λ = 100Monthly Data: λ = 14400

For more, see the original paper posted on LatteHodrick, Robert J, and Edward C. Prescott. “Postwar U.S. BusinessCycles: An Empirical Investigation.” Journal of Money, Credit, andBanking. Vol. 29, No. 1, February 1997, pp. 1-16.

Patrick Herb (Brandeis University) Filtering Time Series ECON/FIN 250: Spring 2016 15 / 39

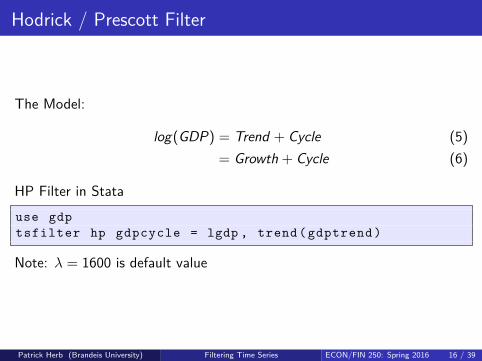

Hodrick / Prescott Filter

The Model:

log(GDP) = Trend + Cycle (5)= Growth + Cycle (6)

HP Filter in Statause gdptsfilter hp gdpcycle = lgdp , trend( gdptrend )

Note: λ = 1600 is default value

Patrick Herb (Brandeis University) Filtering Time Series ECON/FIN 250: Spring 2016 16 / 39

Log GDP & HP Trend

7.5

88.

59

9.5

1947q3 1964q3 1981q3 1998q3 2015q3dateq

lgdp lgdp trend component from hp filter

Patrick Herb (Brandeis University) Filtering Time Series ECON/FIN 250: Spring 2016 17 / 39

Log GDP & HP Trend

9.4

9.5

9.6

9.7

2000q1 2005q1 2010q1 2015q1dateq

lgdp lgdp trend component from hp filter

tsline lgdp gdptrend if dateq > tq (2000q1)

Patrick Herb (Brandeis University) Filtering Time Series ECON/FIN 250: Spring 2016 18 / 39

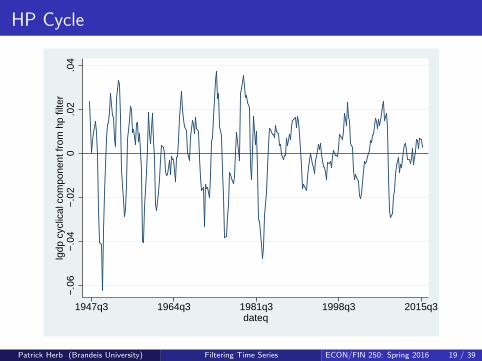

HP Cycle

−.0

6−

.04

−.0

20

.02

.04

lgdp

cyc

lical

com

pone

nt fr

om h

p fil

ter

1947q3 1964q3 1981q3 1998q3 2015q3dateq

Patrick Herb (Brandeis University) Filtering Time Series ECON/FIN 250: Spring 2016 19 / 39

Business Cycles & HP Filter

Much of modern macroeconomics applies the HP filter to many series toseparate the trend from the cycle:

GDPConsumptionInvestment

Then looks at the comovement between the cyclical components

Patrick Herb (Brandeis University) Filtering Time Series ECON/FIN 250: Spring 2016 20 / 39

One-Sided Filters

1 General Filtering Thoughts

2 Two-Sided Filters

3 One-Sided Filters

4 Local Trends

Patrick Herb (Brandeis University) Filtering Time Series ECON/FIN 250: Spring 2016 21 / 39

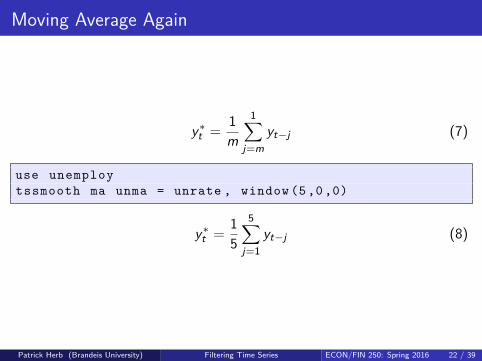

Moving Average Again

y∗t = 1

m

1∑j=m

yt−j (7)

use unemploytssmooth ma unma = unrate , window (5 ,0 ,0)

y∗t = 1

5

5∑j=1

yt−j (8)

Patrick Herb (Brandeis University) Filtering Time Series ECON/FIN 250: Spring 2016 22 / 39

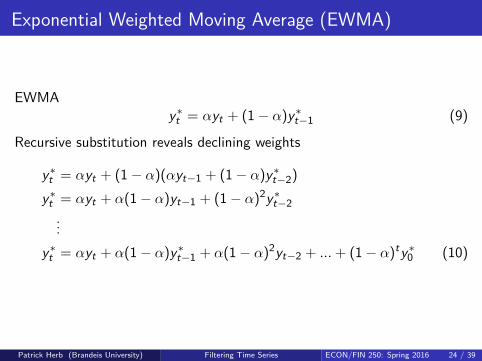

Exponential Weighted Moving Average (EWMA)

Average of past valuesDecreasing (exponentially) weightsRelated to many ideas / models in economics

Adaptive Expectations (Friedman)Rational ExpectationsAutoregressive ModelsRiskmetricsGARCH Models

Patrick Herb (Brandeis University) Filtering Time Series ECON/FIN 250: Spring 2016 23 / 39

Exponential Weighted Moving Average (EWMA)

EWMAy∗

t = αyt + (1− α)y∗t−1 (9)

Recursive substitution reveals declining weights

y∗t = αyt + (1− α)(αyt−1 + (1− α)y∗

t−2)y∗

t = αyt + α(1− α)yt−1 + (1− α)2y∗t−2

...y∗

t = αyt + α(1− α)y∗t−1 + α(1− α)2yt−2 + ...+ (1− α)ty∗

0 (10)

Patrick Herb (Brandeis University) Filtering Time Series ECON/FIN 250: Spring 2016 24 / 39

Exponential Weighted Moving Average (EWMA)

2 4 6 8 10 12 14 16 18 20

yt-j

0.05

0.1

0.15

0.2

0.25

0.3W

eigh

t

α = 0.3α = 0.2α = 0.1

Patrick Herb (Brandeis University) Filtering Time Series ECON/FIN 250: Spring 2016 25 / 39

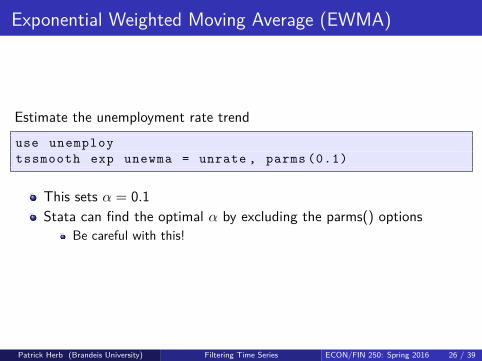

Exponential Weighted Moving Average (EWMA)

Estimate the unemployment rate trenduse unemploytssmooth exp unewma = unrate , parms (0.1)

This sets α = 0.1Stata can find the optimal α by excluding the parms() options

Be careful with this!

Patrick Herb (Brandeis University) Filtering Time Series ECON/FIN 250: Spring 2016 26 / 39

Exponential Weighted Moving Average (EWMA)

24

68

10

1950m1 1960m1 1970m1 1980m1 1990m1 2000m1 2010m1 2020m1datem

unrate exp parms(0.1000) = unrate

Patrick Herb (Brandeis University) Filtering Time Series ECON/FIN 250: Spring 2016 27 / 39

The Optimality of the EWMA

Suppose your time series comes from the following process:

xt = xt−1 + et xt = random walkyt = xt + ηt et , ηt = white noise

You do not observe xt

This implies yt is a random walk plus noiseIn this case, EWMA is the optimal forecast

Patrick Herb (Brandeis University) Filtering Time Series ECON/FIN 250: Spring 2016 28 / 39

Local Trends

1 General Filtering Thoughts

2 Two-Sided Filters

3 One-Sided Filters

4 Local Trends

Patrick Herb (Brandeis University) Filtering Time Series ECON/FIN 250: Spring 2016 29 / 39

Double Exponential Weighted Moving Average (DEWMA)

Filter Oncey∗

t = αyt + (1− α)y∗t−1 (11)

Filter Againy∗∗

t = αy∗t + (1− α)y∗∗

t−1 (12)

The double filter can follow local trendsThe trend can keep going up when the observed yt is going downGetting initial values for y∗

0 , y∗∗0 can be tricky

Patrick Herb (Brandeis University) Filtering Time Series ECON/FIN 250: Spring 2016 30 / 39

Double Exponential Weighted Moving Average

Estimate the unemployment rate trend using the double exponentialweighted moving averageuse unemploytssmooth dexp unema = unrate , parms (0.1)tsline unrate unema

Patrick Herb (Brandeis University) Filtering Time Series ECON/FIN 250: Spring 2016 31 / 39

Double Exponential Weighted Moving Average

24

68

10

1950m1 1960m1 1970m1 1980m1 1990m1 2000m1 2010m1 2020m1datem

unrate dexp parms(0.1000) = unrate

Patrick Herb (Brandeis University) Filtering Time Series ECON/FIN 250: Spring 2016 32 / 39

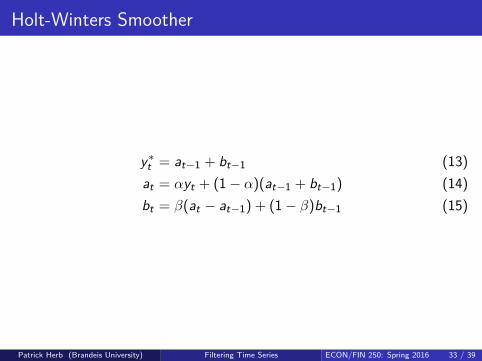

Holt-Winters Smoother

y∗t = at−1 + bt−1 (13)

at = αyt + (1− α)(at−1 + bt−1) (14)bt = β(at − at−1) + (1− β)bt−1 (15)

Patrick Herb (Brandeis University) Filtering Time Series ECON/FIN 250: Spring 2016 33 / 39

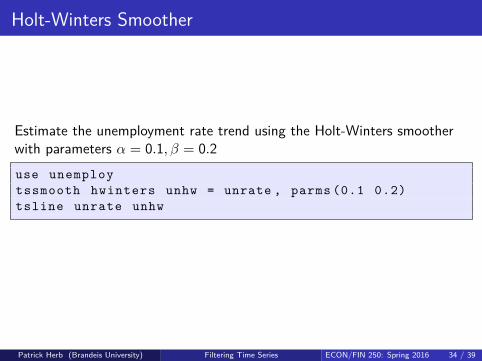

Holt-Winters Smoother

Estimate the unemployment rate trend using the Holt-Winters smootherwith parameters α = 0.1, β = 0.2use unemploytssmooth hwinters unhw = unrate , parms (0.1 0.2)tsline unrate unhw

Patrick Herb (Brandeis University) Filtering Time Series ECON/FIN 250: Spring 2016 34 / 39

Holt-Winters & Unemployment Rate

24

68

1012

1950m1 1960m1 1970m1 1980m1 1990m1 2000m1 2010m1 2020m1datem

unrate hw parms(0.100 0.200) = unrate

Patrick Herb (Brandeis University) Filtering Time Series ECON/FIN 250: Spring 2016 35 / 39

Holt-Winters Seasonal Smoother

Seasonal version of Holt-WintersSt is a repeating seasonal adjustmentThis is the multiplicative version (there is an additive version)s specifies the period of the seasonality

monthly data would have s = 12

y∗t = (at−1 + bt−1)St (16)

at = αyt

St−s) + (1− α)(at−1 + bt−1) (17)

bt = β(at − at−1) + (1− β)bt−1 (18)

St = γytat

+ (1− γ)St−s (19)

Patrick Herb (Brandeis University) Filtering Time Series ECON/FIN 250: Spring 2016 36 / 39

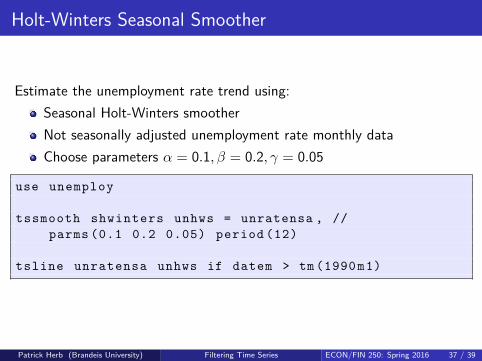

Holt-Winters Seasonal Smoother

Estimate the unemployment rate trend using:Seasonal Holt-Winters smootherNot seasonally adjusted unemployment rate monthly dataChoose parameters α = 0.1, β = 0.2, γ = 0.05

use unemploy

tssmooth shwinters unhws = unratensa , //parms (0.1 0.2 0.05) period (12)

tsline unratensa unhws if datem > tm (1990m1)

Patrick Herb (Brandeis University) Filtering Time Series ECON/FIN 250: Spring 2016 37 / 39

Seasonal Holt-Winters & Unemployment Rate NSA

46

810

12

1995m1 2000m1 2005m1 2010m1 2015m1datem

unratensa shw parms(0.100 0.200 0.050) = unratensa

Patrick Herb (Brandeis University) Filtering Time Series ECON/FIN 250: Spring 2016 38 / 39

Summary

yt = (Trend) + (Seasonal) + (Cycle) + (Noise) (20)

Filters can help separate partsFilters can help smooth out the noiseNot necessarily predictiveSometimes difficult to estimate

Initial value problemsAlso, a little ad hoc

Not clear what the data generating process is

Patrick Herb (Brandeis University) Filtering Time Series ECON/FIN 250: Spring 2016 39 / 39