ec.europa.eu · proposal for member states to amend their existing law to provide: –a more...

TRANSCRIPT

Tackling cross-border Inheritance Tax problems

the European Commission proposals

Richard Frimston

Solicitor & Notary Public of England & Wales

Russell-Cooke LLP

Chairman of STEP EU Policy Committee

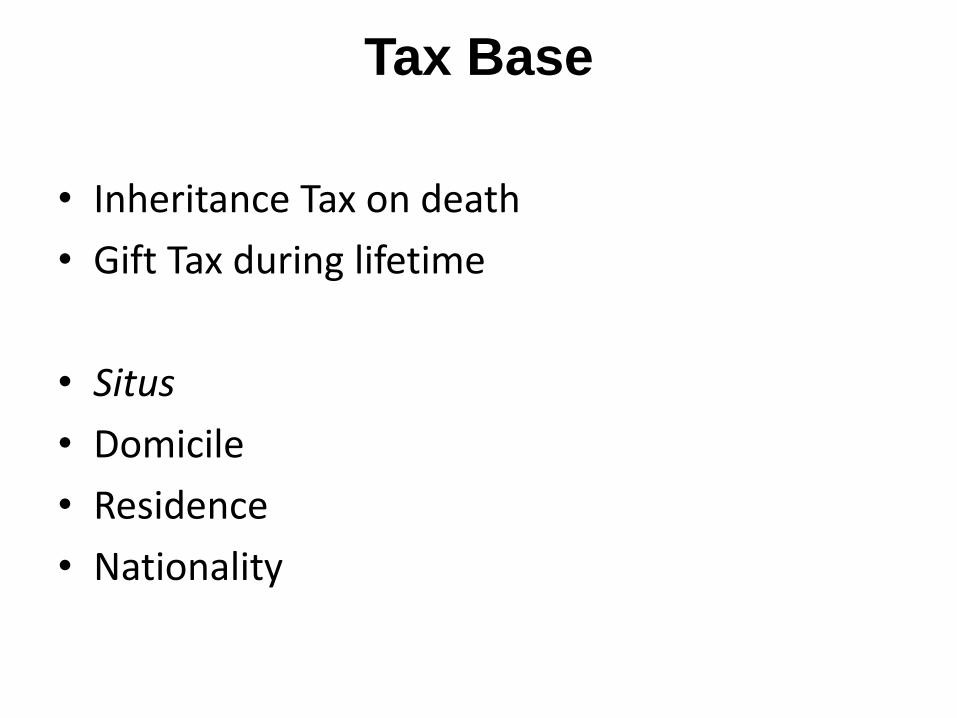

Tax Base

• Inheritance Tax on death

• Gift Tax during lifetime

• Situs

• Domicile

• Residence

• Nationality

Discrimination

• Former Discriminations

– Charities

– Valuation of Land

– Agricultural Land

– Businesses

• Outstanding Discriminations

– spouse discrimination

– heritage property

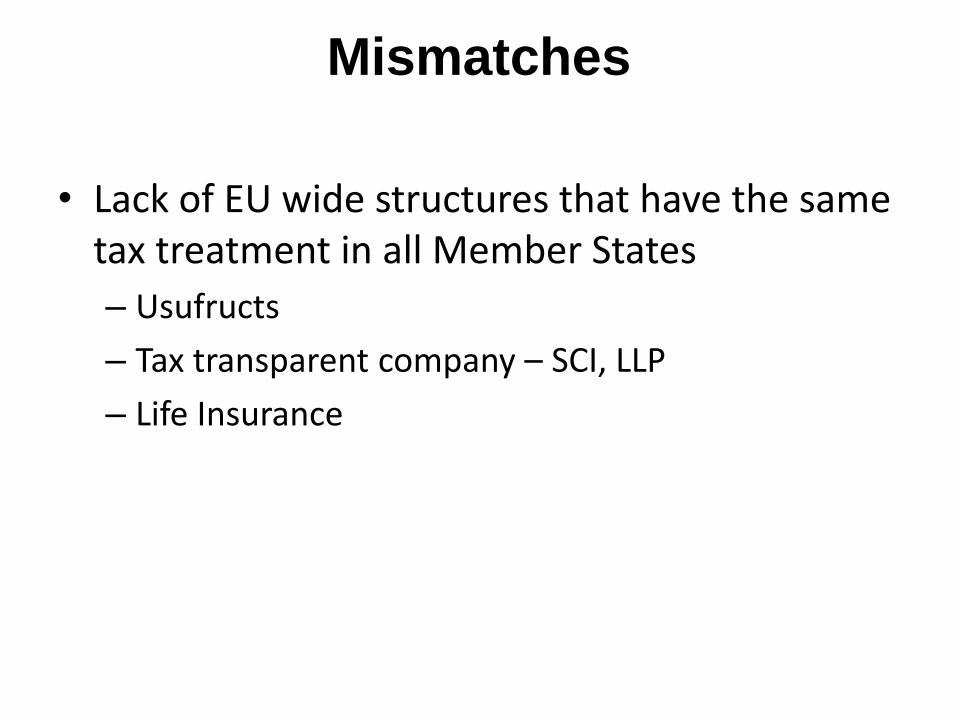

Mismatches

• Lack of EU wide structures that have the same tax treatment in all Member States

– Usufructs

– Tax transparent company – SCI, LLP

– Life Insurance

Succession Law

• The Inheritance Tax of a Member State is generally geared to its internal succession law

– Heirs with Succession Rights are subject to lower tax rates

– Succession Law does not follow the Tax Base

– Succession Regulation (EU) No 650/2012 from 17 August 2015

Treaty and Unilateral Relief

• Treaties are part of the internal law of a Member State

– create their own forms of discrimination between nationals of different Member States

• Unilateral Relief is generally available but

– no relief against tax paid on a different event or at a different time

– Unilateral Relief is usually not available against foreign tax paid on local assets

Commission Draft

Recommendation

• We support the Commission’s continued work to remove areas of discrimination

• We welcome the draft Recommendation’s proposal for Member States to amend their existing law to provide:

– a more limited tax base for inheritance tax

– clearer rules for unilateral relief

– tie breaker rules

Tackling cross-border Inheritance Tax problems

the European Commission proposals

Richard Frimston

Solicitor & Notary Public of England & Wales

Russell-Cooke LLP

Chairman of STEP EU Policy Committee

1

Tackling Cross-Border Inheritance Tax Problems

Richard Frimston BSc ARCS TEP

Solicitor and Notary Public

Chairman STEP EU Policy Committee

STEP greatly welcomes the proposed Commission Recommendation.

For the citizen, the present European situation is often unfair and usually complex resulting not only in multiple taxation, but also the requirement for specialist and expert advice.

Inheritance Taxation in the United Kingdom.

The United Kingdom has Inheritance Tax (“IHT”) on death. IHT is actually an estate tax that taxes the estate of the deceased.

UK assets are always subject to IHT.

The worldwide assets of a person dying domiciled or deemed domiciled in the UK, are subject to IHT.

The assets that are subject to IHT are the estate of the deceased at death, some trust assets in which the deceased had the right to income, assets given away by the deceased in the seven years before death (Potentially Exempt Transfers – “PETs”- that have failed) and assets given away in which the deceased retained a benefit (Gifts with a Reservation of Benefit – “GROBs”). For lifetime gifts, the United Kingdom does not have a gift tax. Gifts are subject to Capital Gains Tax (“CGT”) triggered on the market value of the asset.

UK assets are not necessarily subject to CGT.

2

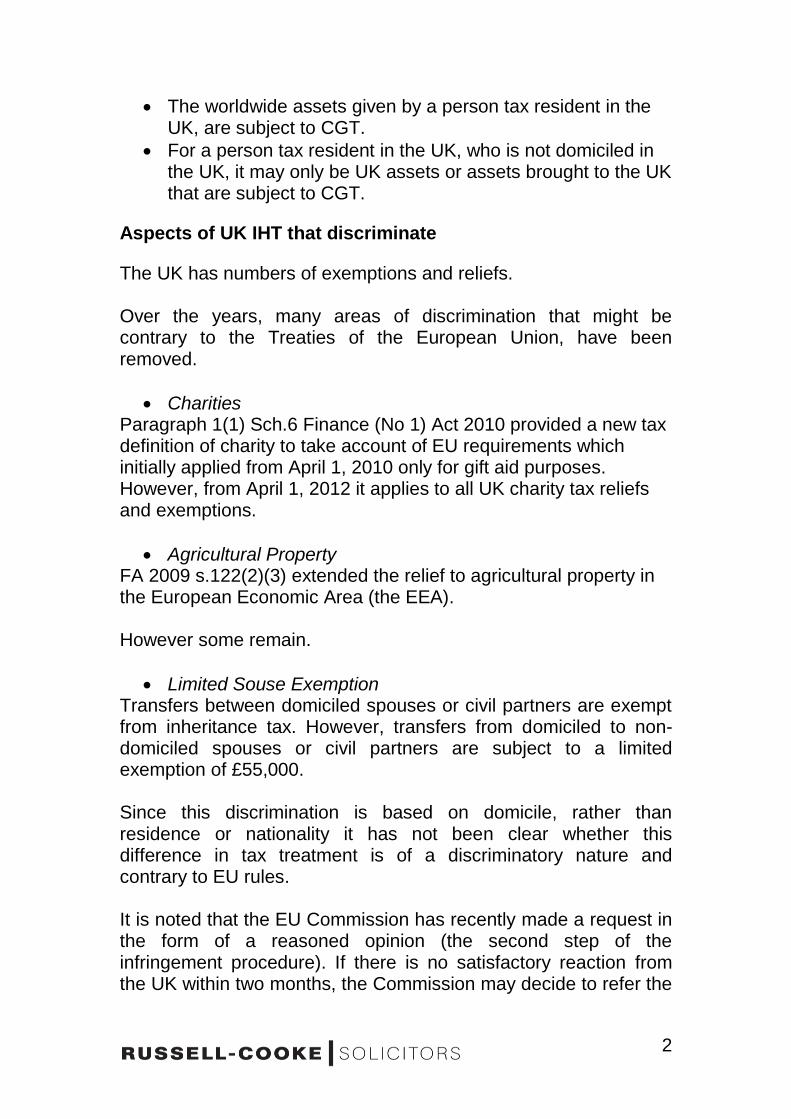

The worldwide assets given by a person tax resident in the UK, are subject to CGT.

For a person tax resident in the UK, who is not domiciled in the UK, it may only be UK assets or assets brought to the UK that are subject to CGT.

Aspects of UK IHT that discriminate

The UK has numbers of exemptions and reliefs. Over the years, many areas of discrimination that might be contrary to the Treaties of the European Union, have been removed.

Charities Paragraph 1(1) Sch.6 Finance (No 1) Act 2010 provided a new tax definition of charity to take account of EU requirements which initially applied from April 1, 2010 only for gift aid purposes. However, from April 1, 2012 it applies to all UK charity tax reliefs and exemptions.

Agricultural Property FA 2009 s.122(2)(3) extended the relief to agricultural property in the European Economic Area (the EEA). However some remain.

Limited Souse Exemption Transfers between domiciled spouses or civil partners are exempt from inheritance tax. However, transfers from domiciled to non-domiciled spouses or civil partners are subject to a limited exemption of £55,000. Since this discrimination is based on domicile, rather than residence or nationality it has not been clear whether this difference in tax treatment is of a discriminatory nature and contrary to EU rules. It is noted that the EU Commission has recently made a request in the form of a reasoned opinion (the second step of the infringement procedure). If there is no satisfactory reaction from the UK within two months, the Commission may decide to refer the

3

matter to the Court of Justice of the European Union. (Reference: IN/2010/2111). The UK has already started to consult as to proposed changes to the law to increase the limit from £55,000 to £325,000 and allow a surviving spouse/civil partner to elect for treatment as if they were domiciled in the UK. Since, there would still be differences between domiciled and non-domiciled spouses, it is not clear that the proposed changes would not still be of a discriminatory nature and contrary to EU rules.

Heritage Property ss.30–35A of the Inheritance Tax Act 1984 provides for the conditional exemption of works of art, houses of historic or architectural interest and qualifying land, which are designated by the UK Revenue as being of outstanding national, scientific, historic or artistic interest. Many of the detailed provisions would seem to be contrary to EU rules. For example, an undertaking must be given that a work or art will be kept permanently in the United Kingdom.

Mismatches of Classification for Taxation

If a usufruct is classified in the UK as a settlement within the relevant property regime for Inheritance Tax purposes, but classified in a civil law jurisdiction as a valid gift which splits value, there will be very different tax consequences in each jurisdiction.

The Impact of Succession Law

Immovable property in England & Wales and worldwide movable property of persons domiciled in England & Wales can be transferred without restriction subject to the provisions of the rules protecting dependents – Inheritance (Provision for Family & Dependents) Act 1975. Immovable property elsewhere and moveable property of persons domiciled elsewhere is subject to the succession law of another state. From a UK perspective:

4

A person domiciled in England & Wales can leave movables to a spouse or civil partner or to charity and they will receive it exempt from IHT

A person domiciled in France, but deemed domiciled in the UK, with 3 children must leave ¾ of his cash and shares to them and they will be subject to IHT at 40% if not protected by the double tax treaty. There is no option. The Succession Regulation (EU) No 650/2012 will enable some citizens from 17 August 2015, to choose the succession law of their nationality to apply, and this will provide an additional choice in some circumstances.

Unilateral and Double Tax Treaty Relief

The fact that different states may use common law domicile, deemed domicile, civil law domicile, tax residence, habitual residence, nationality or situs of either the donor (or the deceased) on the one hand or the donee (or heir or beneficiary) on the other, means that either some assets are not taxed at all, or some assets are taxed twice or more Some of these problems are resolved by double tax treaties, but there are very few of these, and they themselves create differences and discriminate between EU nationals The USA treaties with the UK and with France are examples. If a French resident moves to UK with assets in USA

USA/F treaty ceases to apply since no longer French resident

USA/UK treaty does not apply until UK resident for 17 years and becomes UK deemed domiciled If a UK domiciled person moves to France with assets in USA

US/UK treaty continues to apply since still UK domiciled or deemed domiciled

US/ F treaty also applies since French resident Where there is no double tax treaty, unilateral relief is available. However this only helps when the same taxpayer is taxed in a similar way at the same time in relation to particular property.

5

If property is taxed in France on death A but not in the UK, and taxed in the UK but not in France on death B, unilateral relief is of no assistance.

Unilateral relief is not available for foreign tax paid on property regarded as situated solely in the UK.

Draft Commission Recommendation

Although EU legislation creating harmonised rules across the EU would be the best solution for citizens, it is appreciated that the politically acceptable policy options are limited. We welcome the draft Recommendation’s proposal for Member States to amend their existing law to provide:

a more limited tax base for inheritance tax

clearer rules for unilateral relief

tie breaker rules

We look forward to working with the Commission to assist in the implementation of the Recommendation and further moves to reduce discrimination and multiple taxation in the European Union.

Tackling EU cross-border inheritance tax obstacles

Bert Zuijdendorp

Directorate General for Taxation and the Customs Union European Commission

Members of the

European Union

Candidate countries

• The Subsidiarity Principle - laws are adopted at the most appropriate level

• The Proportionality Principle - a measure is well adapted and no more than is necessary to meet the purpose

• Unanimity in Council for proposals for tax legislation, but "enhanced cooperation" to ensure that one Member State cannot block the progress

• Art. 115 of the TFEU approximation of those rules of Member States that directly affect the establishment or functioning of the internal market

General background

Citzen Focused Approach In Taxation

• Re-launch of the Single Market

• A report on 20 most frequently encountered problems faced by EU citizens – published in September 2011

• "The Single Market through the lens of the people" - (http://ec.europa.eu/commission_2010-2014/barnier/headlines/news/2011/09/20110926_en.htm

• Cross-border inheritance tax problems, as well as other tax problems, identified among the top 20 list of problems

• More focus on citizens in tax policy – double taxation as well as double non-taxation and tax evasion should be avoided

Cross-border inheritance tax issues

Double taxation

Discrimination

• Commission

Recommendation for a

broader and more flexible

application of existing

national measures to

relieve double taxation of

cross-border inheritances

• Commission Staff Working

Paper with a set of principles

for non-discriminatory

inheritance taxation, based

on EU case law

• Increase in relevant court

cases and complaints

• 0.5 % of total tax revenues in the EU

• In 8 new Member States this share comes to a negligible amount of 0.05%

Double taxation problems

• Which private law to apply? Draft Regulation on cross-border successions for a single connecting factor

• Significant differences in Member States’ private laws Civil law vs. Common law

Transfer of assets

• Which taxes on death? Inheritance tax, stamp duties, etc.

• Death taxes: Enormous variety of rules Different taxable person/event

Different personal nexus rules

Location rules

Diverging definitions of terms

High rates on not related heirs

Limitations to existing tools to eliminate the double taxation of inheritances • Limitations of existing domestic provisions to relieve double taxation, e.g.:

Taxes and persons covered

Assets covered

Timing issues

• Limitations of bilateral tax conventions

There are only 33 bilateral inheritance tax treaties between Member States out of possible 351

The OECD Model Tax Convention on estates, inheritances and gifts not updated since 1982

Solutions

Double taxation:

• Commission

Recommendation for a

broader and more flexible

application of existing

national measures to

relieve double taxation of

cross-border inheritances

Discrimination

• Commission Staff

Working Paper with a set of

principles for non-

discriminatory inheritance

taxation, based on EU case

law

Recommendation regarding relief for double taxation on inheritances • Minor changes to Member States' national inheritance tax double tax relief measures to make them more coherent with each other

• Setting order of taxing rights and relief for previous taxation in cases where several Member States claim taxing rights over the same inheritance.

• Member States with the closest links to the property, to the deceased or to the heir takes precedence over other Member States in terms of taxing rights.

• Suggesting solutions to cases where an heir or a deceased has personal links to more than one Member State (e.g. resident in one of the States and domiciled in another).

Principles for non-discriminatory inheritance tax systems

No discrimination including as regards:

• Geographical location of assets e.g. different valuation methods

• Residence of heir or deceased/donor e.g. lower personal tax allowances

• Businesses (e.g. tax allowances available only if employees are local)

Conclusion

• Speedy and proportionate solutions proposed

• The Commission has launched discussions with Member States

• The Commission will publish an evaluation report in 3 years time and may take follow-up action

• The Commission continues to tackle discrimination via infringement actions

Questions?

http://ec.europa.eu/taxation_customs/taxation/personal_tax/inheritance/

index_en.htm

European Economic and Social Committee

Opinion

Tackling cross-border inheritance tax obstacles

within the EU

Vincent Farrugia – EESC Rapporteur

Consultative mechanism

• On 15 December 2011, the Commission decided to consult

the EESC, under Article 304 of the Treaty on the Functioning

of the European Union (TFEU)

• The Section for Economic and Monetary Union and Economic

and Social Cohesion, which was responsible for preparing the

Committee's work on the subject, adopted its opinion on 4

September 2012

• At its 483rd plenary session, held on 18 September 2012, the

EESC adopted the opinion by 135 votes to 1 with 11

abstentions

The Commission tackling a real problem for citizens

• The number of EU citizens moving between MS increased

from 3 million in 2005 to 12.3 million in 2010, and cross-

border real estate ownership in the EU increased by up to

50%

• EU citizens who inherit assets across national MS borders are

frequently faced with taxation in two or more different MS (i.e.

double or multiple taxation) and tax discrimination

• EU Member States revenues from inheritances taxes account

for less than 0.5% of total tax receipts, with cross-border

cases alone accounting for far less

EESC in agreement with the Commission’s approach

• The EESC is in favour of removing such obstacles, and

welcomes the Commission’s approach that:

• recognises the problems which impinge especially on citizens and small

business, but have a very limited dimension in terms of national fiscal

performance

• suggests ways in which MS would grant tax relief in cases of multiple

taxation

• respects the tax sovereignty of individual MS while calling for better

interfacing of national tax systems

More effective measures to achieve the final aims

• practical mechanisms that would ensure the efficient

interfacing of national tax systems while encouraging MS to

operate double/multiple taxation relief mechanisms in a more

effective and flexible manner

• using legislative mechanisms to effectively eliminate such

taxation problems of EU citizens

Going further

• looking into distortionary effects arising from differences in the

computation of the inheritance tax base by different national

tax jurisdictions, by setting common principles based on fair

net asset valuations and which safeguard the business entity

unit

• actively promoting more effective, efficient and citizen-friendly

taxation systems, with the least possible burden

An in depth analysis

• studying the issues which impinge on EU citizens arising out

of global cross-border inheritance taxes

• studying the possibility of simplifying inheritance taxation in

cross border situations through a system which imposes

taxation once at a sole point of taxation determined by the

location of the asset

EU Taxation Observatory

• The EU Taxation Observatory, whose creation under the

auspices of the Commission has been suggested in previous

EESC Opinions dealing with multiple and discriminatory

taxation

• The Observatory would contribute to the more effective

resolution of inheritance tax obstacles on an ongoing basis

through research and investigations and provide fora for

consultation, collaboration and agreement between different

national tax jurisdictions.

Tackling Cross-Border IHT Problems Bruxelles, 12 November 2012

Expert’s response to Commission proposals

Academic perspective

Prof. Guglielmo Maisto

Catholic University of Piacenza

Maisto e Associati

© Guglielmo Maisto 2012 1

Main tax obstacles in cross-border inheritances

• Different taxable persons

• Different taxes on death

– None

– Inheritance tax

– Estate tax

– Income tax or capital gains tax

– Combination of taxes

– Characterisation of taxes (fees)

• Different tax connecting factors

• Different tax base computation

• Few bilateral IHT DTCs signed between Member States 2

European Commission’s response to tax law issues

• Commission package on inheritance tax

– Proposed solutions for eliminating double IHT

1. Order of priority of taxing rights

2. Improvement of existing domestic double taxation relief

systems

© Guglielmo Maisto 2012 3

First EC solution: Order of priority of taxing rights

1. Rules on the order of priority of taxing rights

i. Immovable property and movable property of a PE

– Priority: State of Situs

ii. Other kinds of movable property – Priority: exclusive right to tax for State of personal link

iii. Deceased and heir with personal link to different Member States

– Priority: State of deceased

iv. Multiple personal link of a single person (either heir or deceased)

– Closer link based on criteria contained in DTCs

© Guglielmo Maisto 2012 4

First EC solution: Order of priority of taxing rights - Issues

• Priority of situs for immovable property

(AGREED… BUT)

Rules on location of immovable assets may vary in MS

• e.g. real estate companies and other structures

Provide guidance on rules of situs of

immovable assets

© Guglielmo Maisto 2012 5

First EC solution: Order of priority of taxing rights - Issues

• Exclusive taxing right to State of personal link

for movable property

(AGREED)

It solves the problems deriving from conflicting situs rules

• e.g. debt claims

6

Deceased

(creditor)

Heir

(debtor)

Situs for the

D. State Situs for the

H. State

First EC solution: Order of priority

of taxing rights - Issues

• Taxing right to State of the deceased vs State

of the heir

(AGREED)

Most Member States link worldwide taxation to personal

connection of the deceased

Tax policy rationale

© Guglielmo Maisto 2012 7

First EC solution: Order of priority

of taxing rights - Issues

• Definition of “closer personal link”

(AGREED… BUT)

DTCs tiebreaker rules are unclear (“centre of vital interest”)

‒ Interpretation issues faced by tax administrations and courts

MAPs are not a satisfactory solution

‒ Experience on MAPs regarding income “tax residence” is not positive

‒ MAPs available only under DTCs

EU definition of “closer link” ‒ e.g. VAT Regulation 282/2011 on transfer of vehicles upon change of

residence

© Guglielmo Maisto 2012 8

First EC solution: Order of priority of

taxing rights - Issues

• Legal instrument to adopt taxing right

priority rules

Recommended rules can only be adopted by Member

States through legislation

Legislative changes are likely to take a long time,

presumably longer than the 3-year monitoring period

© Guglielmo Maisto 2012 9

Second EC solution: Relief system

• “1.1. … Member States can apply measures, or

improve existing measures, to relieve double or

multiple taxation caused by the application of

inheritance taxes by two or more Member

States”

(AGREED… BUT)

© Guglielmo Maisto 2012 10

Second EC solution: Relief system - Issues

• Weaknesses of domestic relief systems

still remain

Some Member States have no unilateral relief

Some Member States have “poor” domestic IHT relief

provisions

Some Member States have relief limitations

© Guglielmo Maisto 2012 11

Second EC solution: Relief system – Issues: No relief

• Some Member States have no unilateral

relief

– e.g. Poland*

* The Polish Minister of Finance does have a general competence to decide to refrain from collecting taxes for a specified group of taxpayers. Source: Commission Staff Working Paper Impact Assessment, SEC(2011) 1489 final, 15 December 2011

© Guglielmo Maisto 2012 12

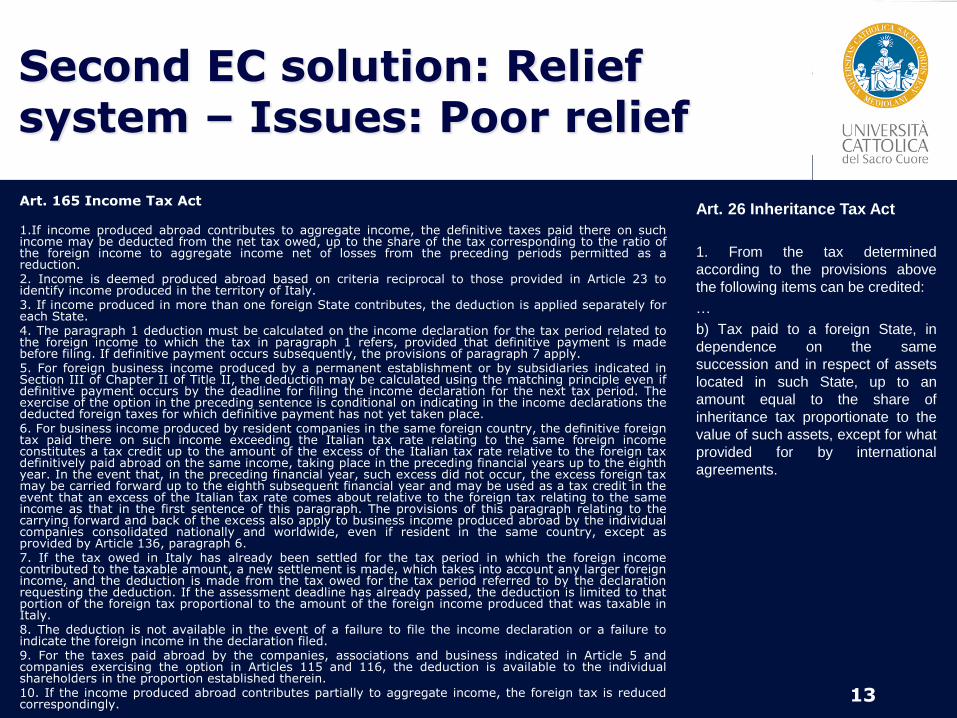

Second EC solution: Relief system – Issues: Poor relief

13

Art. 165 Income Tax Act 1.If income produced abroad contributes to aggregate income, the definitive taxes paid there on such income may be deducted from the net tax owed, up to the share of the tax corresponding to the ratio of the foreign income to aggregate income net of losses from the preceding periods permitted as a reduction. 2. Income is deemed produced abroad based on criteria reciprocal to those provided in Article 23 to identify income produced in the territory of Italy. 3. If income produced in more than one foreign State contributes, the deduction is applied separately for each State. 4. The paragraph 1 deduction must be calculated on the income declaration for the tax period related to the foreign income to which the tax in paragraph 1 refers, provided that definitive payment is made before filing. If definitive payment occurs subsequently, the provisions of paragraph 7 apply. 5. For foreign business income produced by a permanent establishment or by subsidiaries indicated in Section III of Chapter II of Title II, the deduction may be calculated using the matching principle even if definitive payment occurs by the deadline for filing the income declaration for the next tax period. The exercise of the option in the preceding sentence is conditional on indicating in the income declarations the deducted foreign taxes for which definitive payment has not yet taken place. 6. For business income produced by resident companies in the same foreign country, the definitive foreign tax paid there on such income exceeding the Italian tax rate relating to the same foreign income constitutes a tax credit up to the amount of the excess of the Italian tax rate relative to the foreign tax definitively paid abroad on the same income, taking place in the preceding financial years up to the eighth year. In the event that, in the preceding financial year, such excess did not occur, the excess foreign tax may be carried forward up to the eighth subsequent financial year and may be used as a tax credit in the event that an excess of the Italian tax rate comes about relative to the foreign tax relating to the same income as that in the first sentence of this paragraph. The provisions of this paragraph relating to the carrying forward and back of the excess also apply to business income produced abroad by the individual companies consolidated nationally and worldwide, even if resident in the same country, except as provided by Article 136, paragraph 6. 7. If the tax owed in Italy has already been settled for the tax period in which the foreign income contributed to the taxable amount, a new settlement is made, which takes into account any larger foreign income, and the deduction is made from the tax owed for the tax period referred to by the declaration requesting the deduction. If the assessment deadline has already passed, the deduction is limited to that portion of the foreign tax proportional to the amount of the foreign income produced that was taxable in Italy. 8. The deduction is not available in the event of a failure to file the income declaration or a failure to indicate the foreign income in the declaration filed. 9. For the taxes paid abroad by the companies, associations and business indicated in Article 5 and companies exercising the option in Articles 115 and 116, the deduction is available to the individual shareholders in the proportion established therein. 10. If the income produced abroad contributes partially to aggregate income, the foreign tax is reduced correspondingly.

Art. 26 Inheritance Tax Act

1. From the tax determined

according to the provisions above

the following items can be credited:

…

b) Tax paid to a foreign State, in

dependence on the same

succession and in respect of assets

located in such State, up to an

amount equal to the share of

inheritance tax proportionate to the

value of such assets, except for what

provided for by international

agreements.

Second EC solution: Relief system – Issues: Limited relief

• Some Member States have relief limitations – Credit only for taxes levied on certain foreign assets (e.g. Belgium

(real estate), Denmark (real estate and business assets of a PE), Greece (movable assets), the Netherlands (real estate and business assets of a PE)*

– Narrow definition of foreign creditable taxes (e.g. in UK, Germany and France probate fees and stamp duties - such as Portuguese Stamp Duty - are not creditable*; in Finland IHT levied by foreign local authorities are not creditable**)

* Source: Commission Staff Working Paper Impact Assessment, SEC(2011) 1489 final, 15 December 2011 ** Source: General report for the 2010 Rome IFA Congress, “Death as a taxable event and its international ramification”, Cahiers de

droit Fiscal international, Vol 95b, 2010.

© Guglielmo Maisto 2012 14

Possible remedies to improve domestic relief

EU Model for double taxation relief provision or

practice to be adopted by Member States

Substantial simplification and reduction in potential

conflicts of interpretation

Persuasive EU guidance better than domestic legislative

change (current generic relief provisions should make it

possible)

A condition of reciprocity would mitigate Member States’

resistances to amend domestic double taxation relief

resulting in revenue loss

© Guglielmo Maisto 2012 15

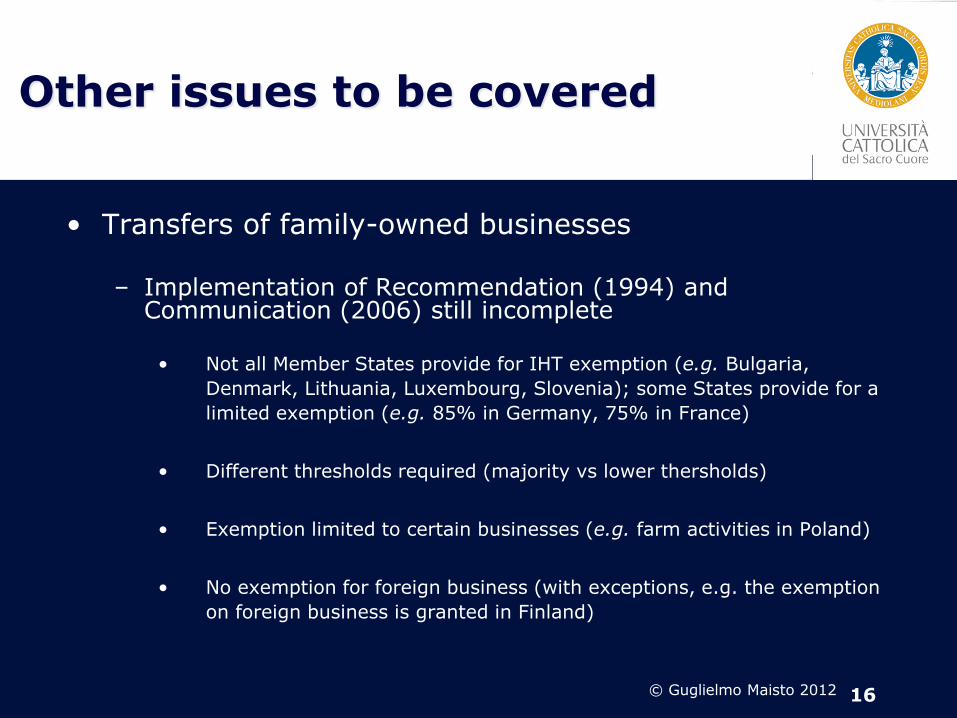

Other issues to be covered

• Transfers of family-owned businesses – Implementation of Recommendation (1994) and

Communication (2006) still incomplete

• Not all Member States provide for IHT exemption (e.g. Bulgaria,

Denmark, Lithuania, Luxembourg, Slovenia); some States provide for a

limited exemption (e.g. 85% in Germany, 75% in France)

• Different thresholds required (majority vs lower thersholds)

• Exemption limited to certain businesses (e.g. farm activities in Poland)

• No exemption for foreign business (with exceptions, e.g. the exemption

on foreign business is granted in Finland)

© Guglielmo Maisto 2012 16

Conclusion

• Relying on soft law is a good solution

• Not relying on treaty law is also a good solution

• Definition of “closer personal link” is desirable (cf. VAT Regulation)

• Model tax relief practice is desirable and should have priority on a model tax relief provision

• Reciprocity condition may be considered

© Guglielmo Maisto 2012 17

Double taxation under Belgian inheritance tax law

Alain VAN GEEL

Taxes applicable upon the death of person

Subjective link used by Belgian inheritance Tax Code is :

residence of the deceased

link with f.e. the heir is not relevant

Belgian resident

« He who at the time of his death has fixed his domicile or the centre of

his fortune within the realm » art. 1, 2nd al. Belgian InhTC

13/11/2012 2

Taxes applicable upon the death of person

Belgium is the resident State

estate/inheritance tax, due upon the death of a resident on all

(worldwide) assets, irrespective of the residence of the recipient heir or

legatee

federal vs. regional taxes

the fiscal residence of the deceased determines the applicable legislation

(of the Flemish Brussels or Walloon Region)

– place where the deceased had actual residence in last 5 years prior to decease

– if he resided in more than one region = region where he resided the most

the rate of tax is determined per heir or legatee

inheritance taxes are regional taxes but are levied by the federal State

– till the end of 2014

13/11/2012 3

Taxes applicable upon the death of person

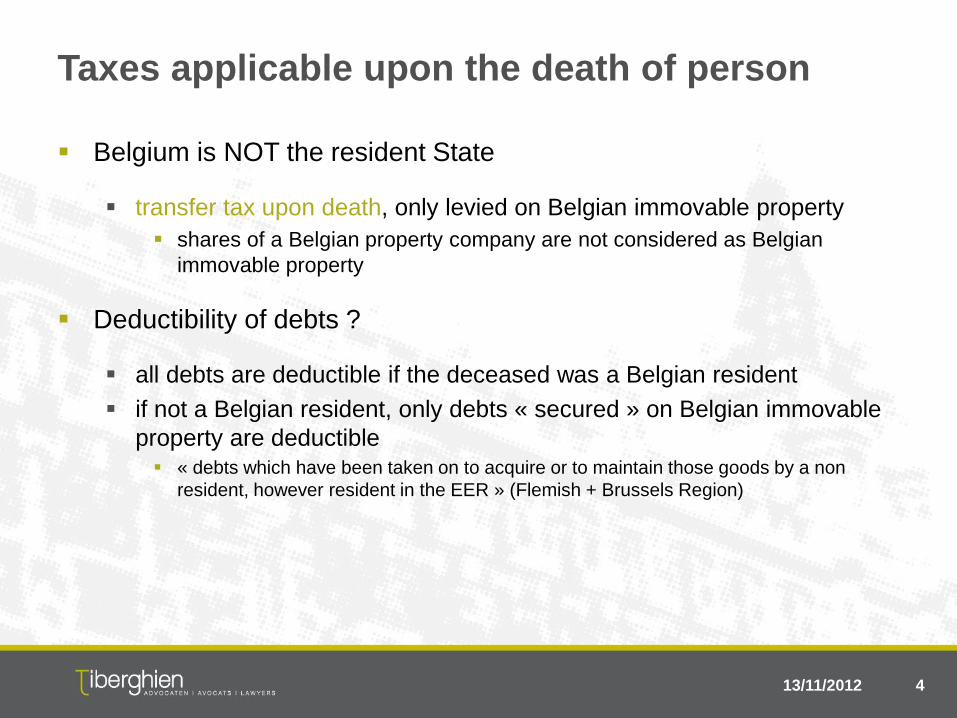

Belgium is NOT the resident State

transfer tax upon death, only levied on Belgian immovable property

shares of a Belgian property company are not considered as Belgian

immovable property

Deductibility of debts ?

all debts are deductible if the deceased was a Belgian resident

if not a Belgian resident, only debts « secured » on Belgian immovable

property are deductible « debts which have been taken on to acquire or to maintain those goods by a non

resident, however resident in the EER » (Flemish + Brussels Region)

13/11/2012 4

Avoidance of double inheritance taxation under

treaties ?

Belgium has only two inheritance tax treaties, both dating from

before the 1960 OECD model

with France (1960)

with Sweden (1959)

13/11/2012 5

Avoidance of double inheritance taxation under

Belgian domestic law ?

How to avoid double taxation ?

the excemption method

the credit method

Belgium does not use the excemption method

Belgium uses the credit methode but only in specific situations

13/11/2012 6

Avoidance of double inheritance taxation under

Belgian domestic law ?

For movable assets

no avoidance of double inheritance tax possible

not even a deduction o foreign inheritance taxes from the taxable base

however, if

foreign tax is levied on the heirs personally (inheritance tax) : no

foreign tax is levied on the estate as a whole (estate tax) : yes

Conclusion : may result in double inheritance taxation

f.e. Belgian resident holds at his time of death :

shares of German, Greek or US company ?

cash on a spanish bank account ?

13/11/2012 7

Avoidance of double inheritance taxation under

Belgian domestic law ?

For immovable property

all foreign taxes on the estate are creditable, both inheritance and

estate taxes but only if they have been really paid

excemption not equal to payment

creditable to what extent ?

the credit is

– calculated per heir, not for the entire estate

– limited to the part of the Belgian inheritance tax corresponding to the foreign real

estate, calculated according to Belgian rules

13/11/2012 8

Avoidance of double inheritance taxation under

Belgian domestic law ?

For immovable property

Conclusion : application of this method by Belgian tax administration may

result in insufficient tax relief and thus in double taxation

f.e. in cases with diverging valuations of assets

valuation of usufruct in France / the Netherlands >< Belgium

the so called « parental division » in the Netherlands

13/11/2012 9

Avoidance of double inheritance taxation under

Belgian domestic law ?

Belgian resident (Dutch nationality)

Two children

Spanish resident

German resident

Moved into Belgium from the Netherlands less than 10 years ago

If he should die, inheritance taxes levied by ?

the Netherlands : yes (fiction)

Spain : yes (residence of one of the children)

Germany : yes (residence of one of the children)

Belgium : yes (residence of the deceased)

Quid tax credit ?

13/11/2012 10

Suggested solutions

To conclude (more) inheritance tax treaties ?

similar to the model of the existing treaties with Sweden / France ?

not realistic - those models are insufficient in our actual world

would take a lot of (too much ?) time to conclude

a mutilateral agreement will be required since inheritance taxes are

regional taxes still levied by the federal state

impossible, probably for political reasons

To include estate and inheritance taxes in the existing income tax

double taxation agreements ?

why not ?

since f.e. capital gains taxes and taxes on capital can be included in

those agreements

European initiative ?

13/11/2012 11

Brussels Office

Tour & Taxis

Havenlaan 86C / 419

B-1000 Brussels

Tel +32 (0)2 773.40.00

www.tiberghien.com

Antwerp Office

Minerva Building

Karel Oomsstraat 47/5

B-2018 Antwerpen

Tel +32 (0)3 443.20.00

www.tiberghien.com

Luxembourg Office

44, rue de la Vallée

L-2661 Luxembourg

Tel +352 27 47 51 11

www.tiberghien.com

Alain VAN GEEL

13/11/2012 12

FRANCE

Droits de mutation à titre gratuit

Patrick Delas

Avocat au Barreau de Paris

Solicitor (England & Wales)

Russell-Cooke LLP

Généralités

• La France applique des droits de

donation et de succession connus sous

le terme générique de « droits de mutation

à titre gratuit » (DMTG).

Redevable des droits

• Le donataire ou héritier/légataire en fonction du lien de parenté avec le donateur/défunt.

• En matière de donations, le donateur peut prendre à sa charge le paiement des droits sans que le paiement constitue une donation supplémentaire.

Exonérations • Totale:

– Successions entre époux ou partenaires d’un PACS ou équivalent étranger (mais pas en matière de donations) (CGI art. 796-O bis)

– Etat, collectivités territoriales, établissements public d’enseignement

– Associations reconnues d’utilité publique dont les ressources sont affectées à l’assistance, l’environnement ou la protection des animaux ou associations déclarées dont les ressources sont affectées à la recherche médicale ou scientifique désintéressée (CGI art. 795, 2°)

– Fonds universitaires, établissements d’enseignement supérieur (CGI art. 796-O)

• Partielle:

– Transmission d’entreprises (sous condition d’engagement de conservation des parts sociales) (CGI art. 787 B)

– Bois et forêts / Biens ruraux (CGI art. 793)

Territorialité

• Essentiellement en fonction du domicile du défunt ou du donateur et du lieu de situation des biens et depuis 1999 du domicile de l’héritier ou du donataire. Le tout sous réserve des conventions internationales (CGI art. 750 ter).

CGI art. 750 ter

• i) Défunt ou donateur domicilié en France : tous les biens situés en France ou hors de France sont imposables (CGI art. 750 ter 1°).

• ii) Défunt ou donateur non-domicilié en France : – Donataire/héritier non-domicilié en France : seuls les biens

situés en France sont imposables (CGI art. 750 ter 2°).

– Donataire/héritier domicilié en France (6/10 années) : tous les biens situés en France ou hors de France sont imposables (CGI art. 750 ter 3°).

La notion de domicile • La détermination du domicile fiscal obéit aux mêmes règles que

pour l’établissement de l’impôt sur le revenu (CGI art. 4 B).

• Est domicilié en France le contribuable qui avait en France au jour de décès ou de la donation :

– Son foyer (lieu où les époux et les enfants résident habituellement)

– Le lieu de son séjour principal (présence effective de plus de 6 mois)

– Le centre de ses intérêts économiques

• Le domicile fiscal se confond en pratique avec la résidence.

Pluralité de domiciles

• En cas de pluralité de domiciles (deux Etats revendiquent le domicile du défunt/donateur), les conventions fiscales signées par la France s’efforcent de résoudre le conflit autour des critères successifs suivants :

– Le foyer d’habitation permanent

– Le centre des intérêts économiques

– Le lieu de séjour habituel

– La nationalité

Biens considérés comme situés en France

• Biens qui ont leur assise matérielle en France : immeubles, fonds de

commerce.

• Créances sur un débiteur situé en France.

• Actions de sociétés dont l’actif consiste à + de 50% en des immeubles situés en France (prépondérance immobilière).

• Depuis 1999, immeubles détenus indirectement c’est à dire appartenant à une personne morale elle-même détenue directement ou indirectement à plus de 50% par le donateur/défunt, son conjoint, ses ascendants/descendants ou ses frères/sœurs que cette personne morale soit prépondérance immobilière ou non (CGI Art. CGI Art. 750 ter 2°).

• Les dispositions ci-dessus sont sous réserve des conventions internationales.

Liste des conventions

Pays Successions Donations

Allemagne * *

Autriche * *

Belgique *

Espagne *

Finlande *

Italie * *

Portugal * *

Royaume-Uni *

Suède * *

Jeu des conventions

• Les conventions règlent la double imposition de la façon suivante :

• Par la définition du domicile du donateur/défunt de sorte à ce qu’il ne soit domicilié que dans un seul Etat (de ce point de vue les conventions ne prennent pas en compte le domicile du donataire/héritier privant la France d’appliquer l’article 750 ter al. 3, sauf en cas de donations en l’absence de traité).

Jeu des conventions

• Par la répartition du droit d’imposer entre les Etats : – Les immeubles sont imposables dans l’Etat de leur situation.

Note: les conventions signées par la France permettent d’appliquer la notion de prépondérance immobilière mais pas celle de détention indirecte de l’art. CGI 750 ter 2 al. 2

– Les biens meubles rattachés à l’établissement stable d’une

entreprise sont imposables dans l’Etat où se trouve l’établissement stable.

– Les autres biens meubles sont imposables dans l’Etat où le donateur/défunt est domicilié.

Jeu des conventions

• Par la mise en place de règles de répartition des dettes:

– Les dettes garanties par des biens immobiliers sont

déduites de la valeur de ces biens.

– Les dettes afférentes à un établissement stable sont déduites de la valeur ce cet établissement stable.

– Les autres dettes sont déduites de la valeur des autres biens dont l’imposition est réservée à l’Etat de domicile.

• Par l’exonération ou l’imputation (crédit) d’impôt.

L’art. CGI 784 A

• En l’absence de convention, il existe cependant un mécanisme d’élimination des doubles impositions prévu par l’article CGI 784 A qui prévoit la possibilité d’imputer sur les DMTG dus en France l’impôt acquitté à l’étranger (Concerne les DMTG et l’ISF mais pas l’IR).

• Cependant, seuls sont imputables les DMTG perçus à l’occasion de la donation ou du décès (et non par exemple l’impôt sur la plus-value au Royaume-Uni en cas de donation).

• En outre, seuls sont pris en compte les impôts étrangers sur les biens étrangers c’est à dire qui ne sont pas situés en France en vertu de la législation française. Il n’y a donc pas de crédit d’impôt au titre de l’article CGI 784 A dans le cas ou des valeurs mobilières considérées comme situées en France par la loi française, domicile du défunt, ont été imposées à l’étranger où elle étaient déposées.

• Lorsqu’il est imputable le crédit d’impôt est plafonné au montant de l’impôt français.

Taux d’imposition

• Ligne directe Abattement 100,000 EUR par parent et par enfant, puis :

Valeur transmise

%

Jusqu’à 8,072 5

de 8,072 à 12,109 10

de 12,109 à 15,932

15

de 15,932 à 552,324

20

de 552,324 à 902,838

30

de 902,838 à 1,805,677

40

Au-delà de 1,805,677

45

Epoux (ou partenaires pacsés)

Valeur transmise

%

Jusqu’à 8,072 5

de 8,072 and 15,932 10

de 15,932 and 31,865 15

de 31,865 à 552,324 20

de 552,324 and 902,838 30

de 902,838 and 1,805,677 40

Au-delà de 1,805,677 45

• Succession : Exonération totale. • Donations : Abattement de 80,724 EUR, puis :

Frères et sœurs

• Abattement de 15,932 EUR, puis:

Valeur transmise

%

Jusqu’à 24,430

35

Au-delà de 24,430

45

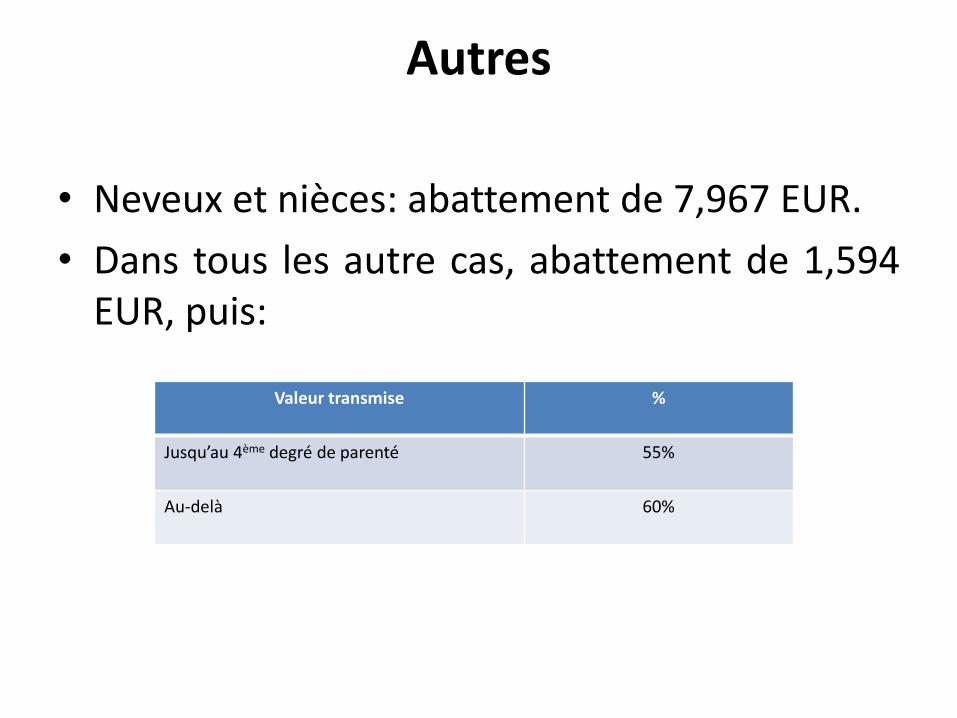

Autres

• Neveux et nièces: abattement de 7,967 EUR.

• Dans tous les autre cas, abattement de 1,594 EUR, puis:

Valeur transmise

%

Jusqu’au 4ème degré de parenté

55%

Au-delà

60%

Exemple de difficulté

• Donation d’un immeuble situé au Royaume-Uni au profit d’un résident français avec prise en charge des droits de donation par le donateur.

• L’impôt sur la plus-value dû au Royaume-Uni n’est pas imputable sur les droits de donation dus en France.

Exemples de difficultés

• D’une manière générale la France prend soin de la compatibilité européenne de sa législation en prévoyant par exemple que les exonérations applicables aux transmissions de parts de sociétés faisant l’objet d’un engagement de conservation ne soient pas réservées aux sociétés françaises (RM Bobe AN-31-10-2006).

• Cela dit, la mise en œuvre pratique est souvent délicate et matière à interprétation notamment quant à l’exonération des dons et legs au profit d’associations étrangères (notamment charities du Royaume-Uni qui sont en général constituées sous forme de sociétés commerciales).

GERMANY

Dr. Daniel Lehmann, Attorney-at-Law, Partner

Rölfs RP Steuerberatungsgesellschaft GmbH,

Rölfs RP Rechtsanwaltsgesellschaft GmbH

Brussels, 12 November 2012

2145851

Unlimited Taxability

7 – 30%

1. Current Infringement case

page 2

Tax Rates

500,000 (spouse)

400,000 (children, each)

200,000 (grandchildren, each)

Close Relatives

Tackling Cross-Border Inheritance Tax Problems: GERMANY

Tax

Allowances

30 / 50%

Tax Rates

20,000 each

Unrelated Persons

Tax

Allowances

Limited Taxability

7 – 30%

Tax Rates

2,000 each

Close Relatives

Tax

Allowances

30 / 50%

Tax Rates

2,000 each

Unrelated Persons

Tax

Allowances

• Opt-in Option to unlimited taxation

available for EU/EEA residents

No practical experience with investors who were deterred

from limited taxability

2. Definition of Tax Residency

page 3 Tackling Cross-Border Inheritance Tax Problems: GERMANY

Many cases where investors were deterred from becoming

unlimited taxable in Germany

• Unlimited Gift/Inheritance Taxability, if

• either decedent / donor or

beneficiary / donee is resident in Germany

• tax residence: Availability of Sleeping Lot suffices

(e.g. Guest Room, Hunting Lodge, Secondary Home…)

• Only Double Taxation Treaties on Gift and Inheritance

Tax with • Denmark (Gift and Inheritance Tax)

• Greece (Inheritance Tax only)

• Sweden (Gift and Inheritance Tax)

• Switzerland (Inheritance Tax only)

• USA (Gift and Inheritance Tax)

Potential Foreign Buyers

of Private Residential

Property in Germany are

less concerned about

higher Tax Charge on

German Property due to

lower Personal Tax

Allowances

than

having to pay German

Inheritance Tax on the

Worldwide Estate.

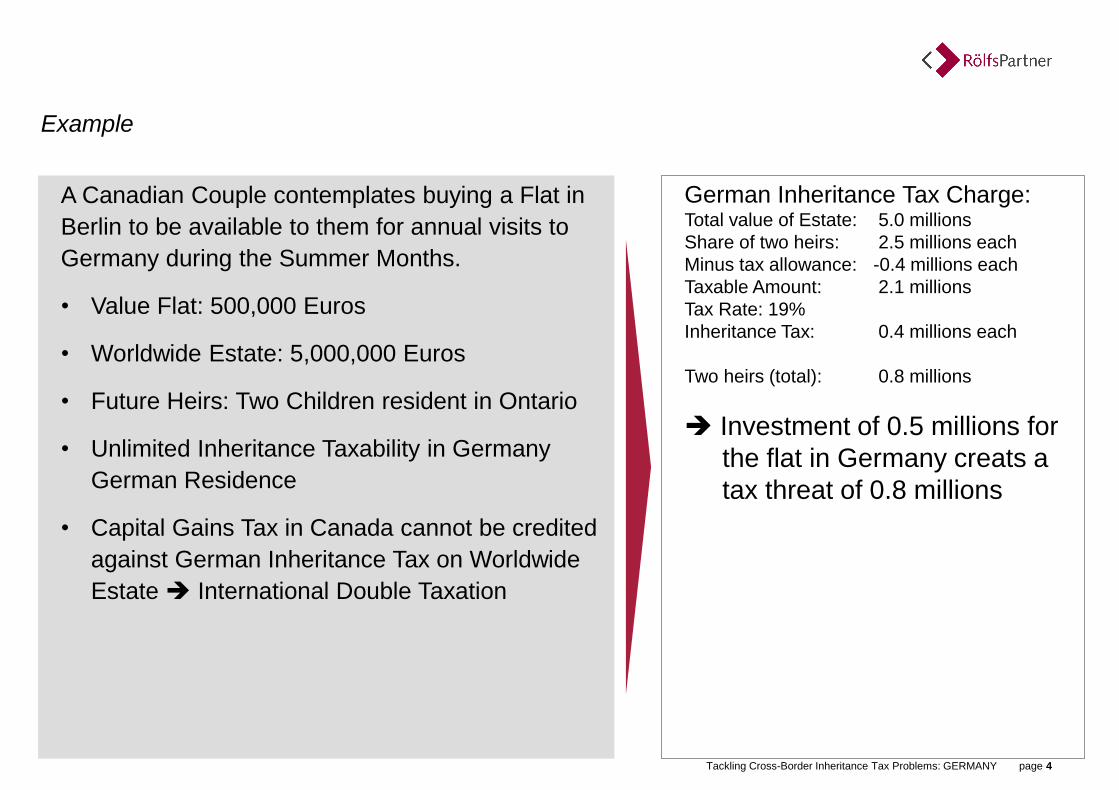

Example

page 4 Tackling Cross-Border Inheritance Tax Problems: GERMANY

A Canadian Couple contemplates buying a Flat in

Berlin to be available to them for annual visits to

Germany during the Summer Months.

• Value Flat: 500,000 Euros

• Worldwide Estate: 5,000,000 Euros

• Future Heirs: Two Children resident in Ontario

• Unlimited Inheritance Taxability in Germany

German Residence

• Capital Gains Tax in Canada cannot be credited

against German Inheritance Tax on Worldwide

Estate International Double Taxation

German Inheritance Tax Charge: Total value of Estate: 5.0 millions

Share of two heirs: 2.5 millions each

Minus tax allowance: -0.4 millions each

Taxable Amount: 2.1 millions

Tax Rate: 19%

Inheritance Tax: 0.4 millions each

Two heirs (total): 0.8 millions

Investment of 0.5 millions for

the flat in Germany creats a

tax threat of 0.8 millions

National Definition of Domestic Assets only

Definition of Domestic Asset

page 5 Tackling Cross-Border Inheritance Tax Problems: GERMANY

Example:

• No German Tax Credit for Foreign Inheritance Tax on Foreign Bank Account

(see EuGH, matter „Block“, C-67/08):

• German decedent owned a Spanish Bank Account. Spanish Inheritance Tax could not be

credited against German Tax Charge.

Dr. Daniel Lehmann

Attorney-at-Law

Partner

RölfsPartner

Nymphenburger Str. 3 b

80335 Munich

tel.: +49 89 55066-295

fax: +49 89 55066-130

www.roelfspartner.de

Deutschland

Dr. Daniel Lehmann, Rechtsanwalt, Partner Rölfs

RP Steuerberatungsgesellschaft GmbH,

Rölfs RP Rechtsanwaltsgesellschaft GmbH

Brüssel, 12. November 2012

2145851

Unbeschränkte Steuerpflicht

7 – 30%

1. Aktuelles Vertragsverletzungsverfahren gegen Deutschland

page 2

Steuersätze

500.000 (Ehepartner)

400.000 (Kinder, jeweils)

200.000 (Enkel, jeweils)

Nahe Verwandte

Tackling Cross-Border Inheritance Tax Problems: GERMANY

Freibeträge

30 / 50%

Je 20,000

Nicht Verwandte

Beschränkte Steuerpflicht

7 – 30%

Steuersätze

Je 2.000

Nahe Verwandte

Freibeträge

30 / 50%

Je 2.000

Nicht Verwandte

• Auf Antrag Besteuerung als unbeschränkt

Steuerpflichtiger für EU/EWR-Ansässige

Steuersätze

Freibeträge

Steuersätze

Freibeträge

Keine praktische Erfahrung mit ausländischen Investoren, die

durch geringen Freibetrag abgeschreckt wurden

2. Definition der steuerlichen Ansässigekeit

page 3 Tackling Cross-Border Inheritance Tax Problems: GERMANY

Viele Fälle ausländischer Investoren, die durch Risiko der

unbeschränkten Steuerpflicht in Deutschland abgeschreckt

wurden

• Unbeschränkte Schenkung- und Erbschaftsteuerpflicht,

wenn entweder Erblasser/Schenker oder

Erbe/Beschenkter in Deutschland ansässig ist

• Steuerliche Ansässigkeit (Wohnsitz): Verfügbarkeit einer

Übernachtungsgelegenheit genügt (z.B. Gästezimmer,

größere Jagdhütte, Ferienhaus, Zweitwohnung…)

• DBA für Erbschaften und Schenkungen nur mit Dänemark (Erbschaften und Schenkungen), Griechenland (nur

Erbschaften), Schweden (Erbschaften und Schenkungen), Schweiz (nur

Erbschaften), USA (Erbschaften und Schenkungen)

Ausländische Investoren

in private

Wohnimmobilien werden

weniger durch niedrige

Freibeträge als durch das

Risiko abgeschreckt, in

Deutschland

unbeschränkt (Erbschaft-)

steuerpflichtig zu werden

mit der Folge, deutsche

Erbschaftsteuer auf ihren

weltweiten Nachlass

auszulösen.

Beispiel (echter Fall!)

page 4 Tackling Cross-Border Inheritance Tax Problems: GERMANY

Ein kanadisches Ehepaar möchte eine

Eigentumswohnung in Berlin kaufen, die sie für

jährliche Urlaubsaufenthalte während der

Sommermonate nutzen möchten.

• Kaufpreis Eigentumswohnung: 500.000 Euro

• Nachlasswert weltweit: 5.000.000 Euro

• Künftige Erben: Zwei Kinder in Ontario

• Unbeschränkte Erbschaftsteuerpflicht in

Deutschland aufgrund deutschen Wohnsitzes

(wegen Eigentumswohnung in Berlin)

• Capital Gains Tax in Kanada kann nicht auf

deutsche Erbschaftsteuer angerechnet werden.

Es besteht kein Doppelbesteuerungsabkommen

mit Kanada auf dem Gebiet der Erbschaftsteuer

Folge: Echte Doppelbesteuerung

Deutsche Erbschaftsteuerbelastung: Nachlasswert: 5,0 Millionen Euro

Anteil von zwei Erben: 2,5 Millionen Euro (je)

Abzüglich Freibetrag: -0,4 Millionen Euro

Steuerpflichtig: 2,1 Millionen Euro

Steuersatz: 19%

Erbschaftsteuer: 0,4 Millionen Euro

Insg. (zwei Erben): 0,8 Millionen Euro

Investition: 0,5 Mio. Euro

führt zu

ErbSt von: 0,8 Mio. Euro.

Zum Vergleich:

Bei beschränkter Steuerpflicht

(niedriger Freibetrag) nur

ErbSt. von: 0,05 Mio. Euro

Das steuerliche Inlandsvermögen wird nur von den nationalen Rechtsordnungen definiert

Definition des steuerlichen Inlandsvermögens

page 5 Tackling Cross-Border Inheritance Tax Problems: GERMANY

Beispiel:

• Bankkonten sind aus deutscher Steuersicht kein Inlandsvermögen.

Folge: Kein Steuerabzug der ausländischen Erbschaftsteuer auf ausländisches

Bankkonto ( echte Doppelbesteuerung)

(vgl. EuGH, Rechtssache „Block“, C-67/08): In Deutschland ansässiger Erblasser

hinterließ ein spanisches Bankkonto. Spanische Erbschaftsteuer kann nicht auf deutsche

Erbschaftsteuer angerechnet werden.

Dr. Daniel Lehmann

Rechtsanwalt

Partner

RölfsPartner

Nymphenburger Str. 3 b

80335 München

Tel.: +49 89 55066-295

Fax: +49 89 55066-130

www.roelfspartner.de

Notary Doctor Annalise Micallef

Key issues in the inheritance tax area &

suggested solutions

Introductory Remarks:

The unfortunate reality of parallel taxation: a breach of the

postulate of fiscal justice albeit no obligation on Member

States to eliminate double taxation (The Block Case)

A situation not solely restricted to pan-European cases: to be

considered in view of the internal market and the free

movement of capital

Predictions of greater mobility in the future : the urgent

need to tackle this issue

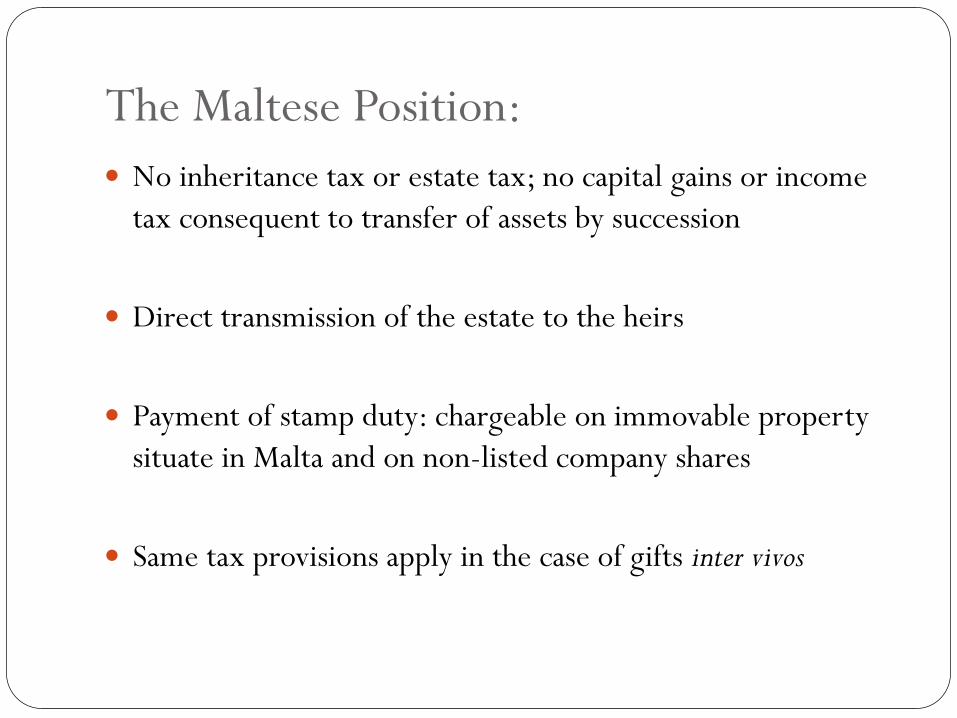

The Maltese Position:

No inheritance tax or estate tax; no capital gains or income

tax consequent to transfer of assets by succession

Direct transmission of the estate to the heirs

Payment of stamp duty: chargeable on immovable property

situate in Malta and on non-listed company shares

Same tax provisions apply in the case of gifts inter vivos

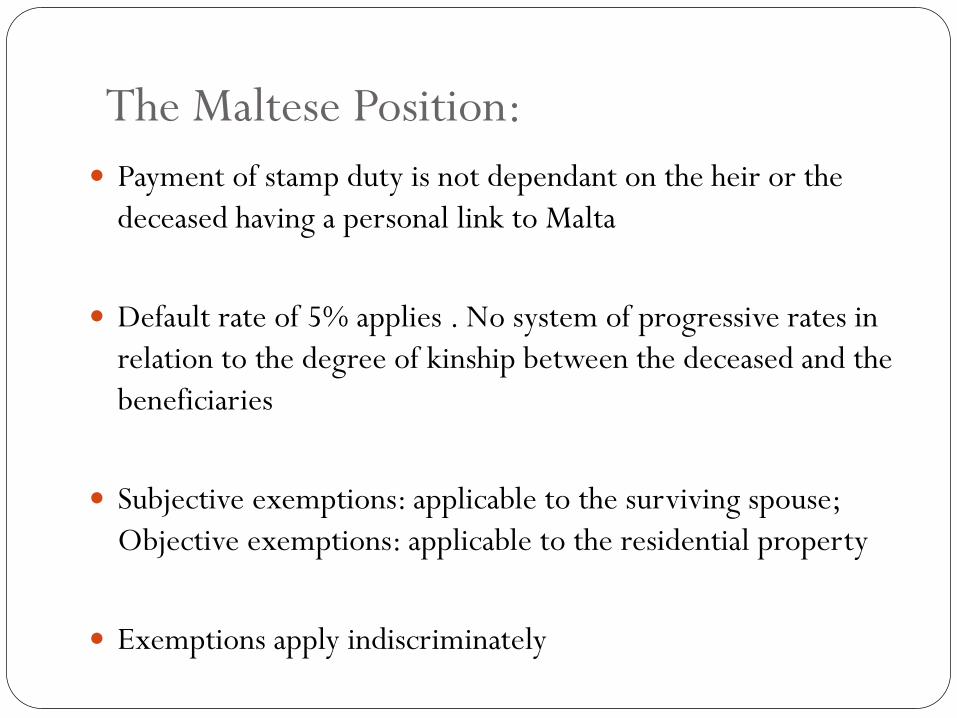

The Maltese Position:

Payment of stamp duty is not dependant on the heir or the

deceased having a personal link to Malta

Default rate of 5% applies . No system of progressive rates in

relation to the degree of kinship between the deceased and the

beneficiaries

Subjective exemptions: applicable to the surviving spouse;

Objective exemptions: applicable to the residential property

Exemptions apply indiscriminately

The Maltese Position:

Value of assets for tax purposes are based on the market value

– no account of debts or mortgages burdening the same

Extensive network of double taxation treaties : none dealing

with inheritance tax issues, nor bilateral agreements

concerning the same.

Considerations:

The Recommendation as a welcome adjunct to the Regulation 650/2012

Tandem effort to strengthen the mobility of citizens across of the internal market

Does the private law governing the succession in terms of Regulation 650/2012 lay the basis for the applicable taxing provisions in terms of the Commission Recommendation?

Are we truly moving towards a unitary regulation of succession?

Considerations:

An order of primacy is established that respects the inderogable right of each Member State to lay down its taxation rules – also establishing a mechanism for resolution of multiple taxation

Practical problems of taxes of a different nature being credited against each other

On a macroeconomic level, revenue from inheritance tax not significant - not diminish the magnitude of the problem for the protagonists thereof.

Notary Doctor Annalise Micallef

Micallef & Associates, Malta

A solution to the problem of multiple

taxation?

TACKLING CROSS-BORDER INHERITANCE

TAX PROBLEMS

Experts’ response to the European Commission’s proposals

Brussels conference, 12 November 2012

Session 2 – Member States’ private sector experts – key issues in the

inheritance tax area & suggested solutions: Spain

1

INDEX

Session 2 – Member States’ private sector experts – key issues in the inheritance

tax area & suggested solutions: Spain

1. Overview: Social and economic factors in context 3

2. Spanish Inheritance Tax: Technical Overview 5

3. The European Commission Recommendation regarding relief for double

taxation of inheritances 8

4. The Commission Staff Working Paper on Non-Discriminatory Inheritance Tax

systems 11

2

1. Overview: Social and economic factors in context

3

Session 2 – Member States’ private sector experts – key issues in the inheritance tax area &

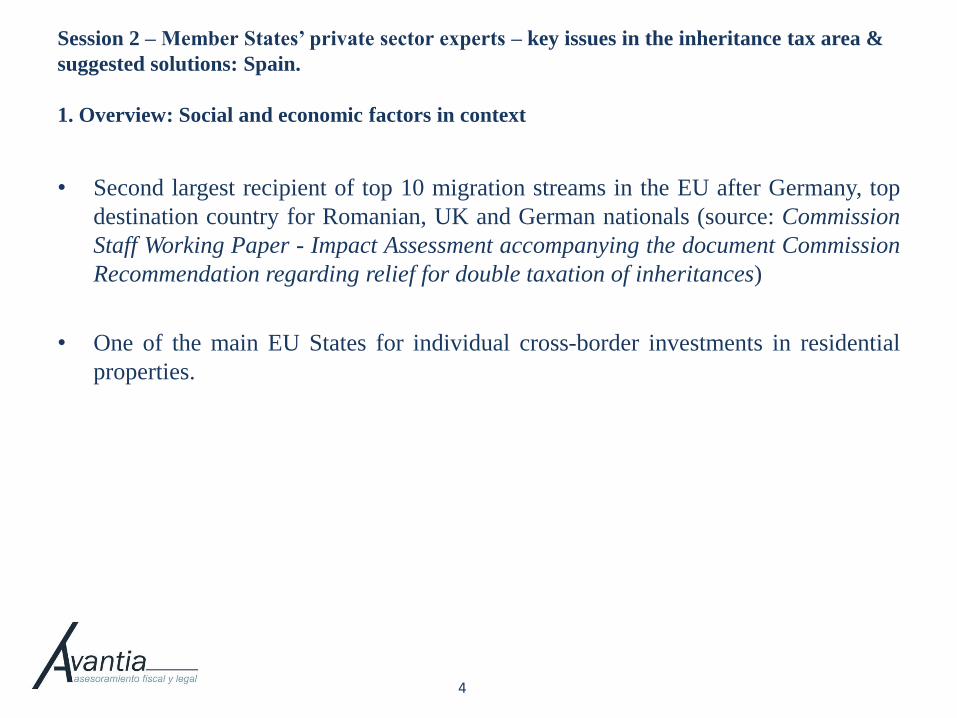

suggested solutions: Spain.

1. Overview: Social and economic factors in context

• Second largest recipient of top 10 migration streams in the EU after Germany, top

destination country for Romanian, UK and German nationals (source: Commission

Staff Working Paper - Impact Assessment accompanying the document Commission

Recommendation regarding relief for double taxation of inheritances)

• One of the main EU States for individual cross-border investments in residential

properties.

4

2. Spanish Inheritance Tax: Technical Overview

5

Session 2 – Member States’ private sector experts – key issues in the inheritance tax area &

suggested solutions: Spain

2. Spanish Inheritance Tax: Technical Overview

• Imposed on heir.

• Very limited number of Double Tax Treaties covering this tax: France, Greece and

Sweden.

• Complex interaction between national and regional laws:

– Practical effect: potentially discrimination against non-residents, currently sub-

iudice at the European Court of Justice (ECJ): (case C-127/12 – European

Commission vs. Kingdom of Spain), based on the fact that non-residents may

not benefit from significant inheritance tax reductions for intra-family

successions and other tax benefits granted by regional laws.

6

Session 2 – Member States’ private sector experts – key issues in the inheritance tax area &

suggested solutions: Spain

2. Spanish Inheritance Tax: Technical Overview

• Further potential discrimination against cross-border inheritances of SMEs: current Revenue interpretation of the provisions of the Spanish Inheritance Tax law blocks the application of Business Property relief (95% reduction in chargeable value) where the deceased is non-resident (Rulings V1076-11, of 27 April 2011, V0561-07, of 16 March 2007, V2099-09 of 22 September 2009, V0130-10, of 27 January 2010 and V2331-10 of 27 October 2010).

• Limitations in unilateral tax relief, granted by means of a double tax credit:

(i) Limitations in scope

(ii) Time limitations for claims

• Technical uncertainties leaving taxpayers exposed to double or multiple taxation on successions involving instruments or arrangements alient to Spanish law, particularly trusts and similar arrangements:

– Some clarification through rulings on particular cases but still incomplete, uncertain and largely subjective.

7

3. The European Commission Recommendation regarding relief for

double taxation of inheritances

8

Session 2 – Member States’ private sector experts – key issues in the inheritance tax area &

suggested solutions: Spain

3. The European Commission Recommendation regarding relief for double taxation of

inheritances

• Would materially improve the existing situation if adopted consistently and coherently by all Member States: implementation and enforceabilty will be key:

– Particularly relevant as there is no ECJ case law backing at present.

• Further elaboration might be required on certain aspects, including:

(i) Further elaboration of the "closer personal link" tie break provisions suggested in order to determine the State which should grant tax relief, including the point in time or period of time over which tests should be applied.

(ii) Considering the inclusion of a recommendation on how to tackle potential double or multiple taxation on arrangements or instruments commonly used in successions in one Member State but not recognised by the laws of the taxing State (such as trusts): eg by specifically identifying most such common misalignments and including a specific recommendation to Member States to address them through Mutual Agreement procedures.

9

Session 2 – Member States’ private sector experts – key issues in the inheritance tax area &

suggested solutions: Spain

3. The European Commission Recommendation regarding relief for double taxation of

inheritances

(iii) Easing tax relief claims by formulating recommendations regarding the

production and validation of formal means of proof of taxes paid by virtue of

inheritance in one or more Member States with a view to facilitating tax relief

claims in the taxing Member State and avoid double or multiple inheritance

tax charges due to mismatching formalities.

10

4. The Commission Staff Working Paper on Non-Discriminatory

Inheritance Tax systems

11

Session 2 – Member States’ private sector experts – key issues in the inheritance tax area &

suggested solutions: Spain

4. The Commission Staff Working Paper on Non-Discriminatory Inheritance Tax systems

• Again, would materially improve the existing situation if adopted consistently and

coherently by all Member States: implementation and enforceability will be key:

– On the positive side, the ECJ has been proactive on this matter and existing

case law provides strong and clear guidance and thus a clearer picture to

taxpayers.

– On the other hand, this matter is more likely to face stronger covert or "soft"

resistence from Member States, so it may mean facing the need to adopt some

EU-wide legislation going forward.

12

Session 2 – Member States’ private sector experts – key issues in the inheritance tax area &

suggested solutions: Spain

4. The Commission Staff Working Paper on Non-Discriminatory Inheritance Tax systems

• In the meantime, the EU should continue to proactively guard taxpayers from

breaches of EU law concerning discrimination in the Inheritance Tax area; for

Spain, this would mean specifically:

(i) The pending ECJ resolution of the current case C-127/12 – European

Commission vs. Kingdom of Spain.

(ii) Detecting and preventing other potential areas of discrimination such as the

current unavailability of Business Property relief to SMEs where the deceased

is non-resident according to current Spanish Revenue practice.

13

Patricia García Mediero

Partner

Avantia Asesoramiento Fiscal y Legal, S.L.

www.avantiaasesoramientofiscalylegal.com

14