ebtc is a programme co-funded by the european union...

TRANSCRIPT

EBTC is a programme co-funded by the European Union and coordinated by

the Association of European Chambers of Commerce and Industry

Overview Of indian BiOtech

Market assOciated with

cliMate change

INDEX

Authors: Gautam Khurana, Mg. Partner, Akash Chauhan, Sr. Associate, Abhishek Hans,

Associate, India Law Offices

The report has been compiled based on an in-house research and various sources,

including the Department of Biotechnology (DBT), Ministry of New and Renewable

Energy (MNRE), Ministry of Environment & Forests (MEF), Federation of Indian

Chambers of Commerce & Industry (FICCI), Confederation of Indian Industries (CII),

The Energy and Research Institute (TERI) and many private researches.

S.No. Index Page

1.

2.

3.

4.

5.

6.

Overview of the Indian Biotech Market 2011

Overview of Indian Biotech associated with Climate Change; Strengths and Weaknesses

Opportunities in India

Government Initiative

Intellectual Property Rights

Future Opportunities – New Business Model

8

33

74

89

114

120

www.ebtc.eu EuropEan BusinEss and TEchnology cEnTrE

5ovErviEw of indian BioTEch MarkET associaTEd wiTh cliMaTE changE

Executive Summary Biotechnology sector in India is witnessing exponential growth and plays a pivotal role in the

Indian economy. In the year 2009-2010, the Indian biotech industry breached EUR 2,218.58

Million mark with a staggering growth of 17% over the previous year.

Amongst the various disciplines of Biotechnology, Bio-Agri emerges as the winner recording a

growth rate of 37% followed by Bio-Services at 28% and BioIndustrial at 16%. Exports accounted

for 53% share with 5% growth over FY 2008-09 and Domestic accounted for 47% share with 34%

growth over FY 2008-09.

Government Organisation and Autonomous Bodies

To provide an impetus to the Biotech sector in India the Government established The Department

of Science and Technology (DST), the Department of Biotechnology (DBT), and Health Biotech

Science Cluster (HBSC) under the Ministry of Science and Technology. Apart from these,

autonomous organisations like TERI (The Energy and Research Institute) play a significant role in

the development of Biotech Sector.

Biotechnology and Environment

Indian policies have always had provisions for Climate change. According to the International

Energy Agency, India is set to become the third largest emitter of greenhouse gases by the year

2015. India has set voluntary targets to reduce the intensity of carbon emissions by 20-25% by

2020 and plans to meet these challenges with combined forces of Public and Private Partnerships.

Biotechnology has an enormous potential to offer eco-friendly, efficient, economically viable, and

unique options for in-situ waste treatment and degradation of the potentially hazardous toxic

waste into harmless/ relatively less harmful by-products. Certain technologies developed with the

efforts of the DBT and other bodies are: Industrial Effluent Treatment, Paper and Pulp Mill Effluent

Treatment, Oilzapper Technology, Chemo biochemical process, Biosensor for Detection of Pesticide

Residues, Detection of Pathogens in Drinking Water, Biosurfactants from Wastes, and Bioscrubber

for Removal of Odours from Industrial Emissions.

www.ebtc.eu EuropEan BusinEss and TEchnology cEnTrE

7ovErviEw of indian BioTEch MarkET associaTEd wiTh cliMaTE changE

The National Policy on Biofuels was initiated in 2009 to promote the use of renewable energy

resources as alternate fuels for transportation vehicles with a target of 20% biofuel blending

(Ethanol Blending Programme-EBP) by the year 2017.

National Bio-diesel Mission (NBM), since 2003, has been promoting Jatropha curcas as the ideal

tree-borne oilseed for producing bio-diesel on wastelands. The Planning Commission of India has

targeted covering 11.2-13.4 million hectares of land under Jatropha cultivation by the end of 11th

Five Year Plan (2011-12). According to the industry sources the government is in the process to

devise an ethanol purchase price for the EBP.

The Ministry of New and Renewable Energy is implementing a biomass power programme with the

objective of harnessing grid quality power from biomass resources through various conversion

technologies along with optimising power generation from bagasse produced in sugar mills.

New Legislation and Regulation

The GoI has drafted the Seed Bill 2010 that seeks to repeal and replace existing Seeds Act, 1966

but is presently pending for an approval of Parliament. The Bill seeks to regulate the production,

quality of seeds for sale, import and export, distribution and sale of seeds, and addressing other

seed-related matters.

Most recently, the National Green Tribunal Act, 2010 has evolved establishing a National Green

Tribunal which shall have the jurisdiction over all substantial questions relating to environment and

power to provide relief and compensation to the victims of pollution and other environmental

hazards.

Public-Private Partnership

The public-private partnerships are increasing with several business houses acquiring approval for

projects to bolster R&D efforts and focus on innovative and eco-friendly products. The initiatives

taken by Bill & Melinda Gates Foundation and DBT Small Business Innovation Research Initiative

(SBIRI) are examples of collaborations between the industry and the government.

EuropEan BusinEss and TEchnology cEnTrE www.ebtc.eu

8 ovErviEw of indian BioTEch MarkET associaTEd wiTh cliMaTE changE

Recently in March 2011, SG Biofuels, a US based bioenergy crop Company using breeding and

biotechnology to develop elite hybrid seeds of Jatropha, has extended operations in India.

Advantage in India

India offers a lot of advantages in the field of Biotechnology, including investments, Outsourcing

Opportunity, Low Manufacturing Cost, High Quality and Technical Capability, Quality Manpower,

Climate Condition, and Innovative Product Market.

Carbon Credit

India is actively promoting ‘Clean Development Mechanism’ (CDM) to achieve the targets as per

the Kyoto Protocol and save Carbon Credits. The country has entered into CDM projects with

companies investing in Windmill, Bio-gas, Bio-diesel, and Co-generation and these companies are

are generating Carbon Credits to be sold later to developed nations. The GoI has further

constituted the National Clean Development Mechanism Authority for the purpose of protecting and

improving the quality of environment in terms of the Kyoto Protocol.

Government Initiative

The Indian Government announced the Jawahar Lal Nehru National Solar Mission (JLNNSM) in

2010 to generate 20,000 MW of grid connected solar energy by 2022. Recently, Cleantech

Switzerland entered into an agreement with the Confederation of Indian Industry (CII) to explore

business opportunities in the clean energy sector for both Indian and Swiss entities.

The Government has also proposed the establishment of the National Biotechnology Regulatory

Authority (NBRA) for regulatory approval. In July 2008, the DBT introduced the National

Biotechnology Regulatory Act, which would establish the NBRA as an empowered body to approve

genetically modified crops, food, recombinant biologics, like DNA, vaccines, recombinant gene

therapy products, and recombinant and transgenic plasma-derived products, such as clotting

factors, veterinary biologics and industrial products.

www.ebtc.eu EuropEan BusinEss and TEchnology cEnTrE

9ovErviEw of indian BioTEch MarkET associaTEd wiTh cliMaTE changE

The Eleventh Five Year Plan has allocated EUR 1015.62 Million for Department of Biotechnology. In

February 2009, DBT implemented a new scheme “BIPP” for enhancing the scope of public-private

partnership.

The Small Business Innovation Research Initiative (SBIRI) is the new scheme launched by the

department to boost public-private-partnership effort in the country. The scheme brings together

users and producers of technology creating direct focus and a sense of urgency for producing

defined results that can only be produced by the private sector engagements.

A National Mission called “Green India” has been launched to enhance ecosystem services. An

initial corpus of over EURO 1 Billion has been earmarked for the programme through the

Compensatory Afforestaion Management and Planning Authority (CAMPA) to commence the work.

The programme will be scaled up to cover all remaining degraded forest land.

Government of India has designed a National Mission on Enhanced Energy Efficiency (NMEEE),

which is one out of eight missions planned under the National Action Plan on Climate Change.

International Collaboration

The Department of Biotechnology has been introducing joint proposals and maintaining

international collaborations with countries like EU, Australia, Canada, USA, and Japan. Some are as

follows:

NEW INDIGO, the Initiative for the Development and Integration of Indian and European Research

aims at strengthening the multilateral science and technology cooperation between EU and India.

Department of Biotechnology has also partnered with UK based Wellcome Trust (WT) to a three-

tier fellowship programme on biomedical research at postdoctoral level.

Namaste is a collaborative small or medium-scale focused research project between European

Commission and Department of Biotechnology, India. The project Namaste EU was launched on 1

February, 2010 while Namaste India was launched on 26 March, 2010 for 3 years duration.

EuropEan BusinEss and TEchnology cEnTrE www.ebtc.eu

10 ovErviEw of indian BioTEch MarkET associaTEd wiTh cliMaTE changE

An MoU for cooperation in the area of Biotechnology and Biological Sciences between DBT and

BBSRC, UK has been signed. Areas identified are Food Biotechnology, Vaccines for communicable

and non communicable diseases, Diagnostics for infectious and non-infectious diseases, Bioprocess

engineering and down stream processing, and Exchange of information on technology transfer.

Taxation Benefit

1. As per Section 10AA – Special Economic Zone, Income Tax Act 1961, the profit and gain

derived from export of goods and services shall be exempted.

2. Any expenditure on scientific research (except cost of land and building), on in-house

research, and development facility as approved by the prescribed authority shall be allowed a

deduction of a 200%.

3. Full exemption from basic custom duty is being provided to bio-polymer/bio-plastics (HS Code

39139090) used for manufacture of bio-degradable agro mulching films, nursery plantation &

flower pots.

4. As per Notification No. 4/2007-Central Excise, excise duty on Bio-Diesel (Alkyl esters of long

chain fatty acids obtained from vegetable oils) is exempted.

5. Full exemption from excise duty on all items of machinery, required for initial setting up of a

project for the generation of power using non-conventional materials, namely, agricultural,

forestry, agro-industrial, industrial, municipal and urban waste, bio waste or poultry litter.

Intellectual Property

World Intellectual Properties Organization (WIPO) was formed in 1967 which ensures IPR

protection amongst its member countries worldwide. Trade Related Aspects of Intellectual Property

Rights (TRIPS) is an international agreement administered by the World Trade Organization (WTO)

that sets down minimum standards for many forms of intellectual property (IP) regulation as

applied to nationals of other WTO Members.

Intellectual property being an intangible property includes 'patents', 'trade secrets', 'copyrights'

and 'trademarks'. Under biotechnology, processes and products are most important examples of

intellectual property. In 1967, WIPO was formed to centralise the world’s patent and copyright

information. The Trade Related Aspects of Intellectual Property Rights (TRIPS) agreement

www.ebtc.eu EuropEan BusinEss and TEchnology cEnTrE

11ovErviEw of indian BioTEch MarkET associaTEd wiTh cliMaTE changE

introduced intellectual property law into the international trading system for the first time in 1994.

Biotechnology Patent Facilitating Cell (BPFC) was set up in 1999 to create awareness and

understanding about Intellectual Property Rights (IPRs) among scientists and researchers.

New Business Model

Collaborative R&D: Indian companies can partner with foreign players to enter into collaborative

R&D efforts as an initial step towards developing an R&D focus.

New revenue streams: Revenues from patent licensing and litigation can re-define existing

business models completely, and shift them to a higher value-generation plane.

Emerging business Opportunities: India will become a highly lucrative option for contract

research once strong IP protection legislation is introduced.

Capturing the Indian Market: Indian companies can introduce entry barriers for foreign players

in the Indian market by using IP to protect their own innovations.

EuropEan BusinEss and TEchnology cEnTrE www.ebtc.eu

12 ovErviEw of indian BioTEch MarkET associaTEd wiTh cliMaTE changE

1: Overview of the Indian Biotech Market 2011

1.1. Introduction BIOTECHNOLOGY is a wide term covering a broad range of scientific applications being used for

various sectors. The term is inter-related with other disciplines and technologies like systems

biology, synthetic biology, bioinformatics and nanotechnology, whose convergence will lead to

improved future products and technologies.

Indian Government is embracing biotechnology as the next driver of innovation and economic

growth. Biotechnology is already beginning to usher in complex, rapidly emerging and far-reaching

novel changes in several areas, particularly food and nutrition security, healthcare and

environmental sustainability.

The private sector with several home-grown companies has performed well. This has strongly

impacted the promotion of low cost vaccines and other useful healthcare products and forced a

price reduction on various bioproducts of MNCs.

The Year 2010 - 2011 was considered the ‘Year of Recovery for Indian Economy’ after the global

downturn in 2009 and a slow recovery in the Q1 2010. Unlike the biotech sectors worldwide, the

global recession has left the Indian biotech industry untouched due to its less reliance on investors’

capital. India’s biotech industry has blossomed in recent years as domestic companies have grown

aggressively in a liberalized intellectual property (IP) regime and as companies worldwide have

sought to seize opportunities from India’s large, skilled workforce, lower manufacturing and

research costs.

1.2. India Biotechnology Sector – Emerging India’s biotechnology sector has flourished in the recent years with a steady pace. The domestic

companies have shown a marked growth due to the liberalized regime in terms of intellectual

property (IP). Also, both the domestic and global companies have made use of the advantages

www.ebtc.eu EuropEan BusinEss and TEchnology cEnTrE

13ovErviEw of indian BioTEch MarkET associaTEd wiTh cliMaTE changE

offered and have benefited from the large and skilled Indian workforce in addition to the low

manufacturing costs.

Currently, India holds a two percent share in the global market. In the year 2010 – 2011, the

revenue for Indian biotechnology industry touched an astounding figure of EUR 2,343.75 Million.

This figure is estimated to reach EUR 10.2 billion by the year 2015, indicating a robust growth for

the Indian biotech industry. This, however, implies that the industry would have to grow at about

30% year-on- year with increased government initiatives.

A consistent double digit growth has been recorded for the industry over the last decade with the

average revenue growth figures being greater than 20%. The Indian Economy has witnessed a

sharp growth in deals involving outsourcing, technology transfer and entry of foreign players to tap

the burgeoning Indian biotechnology market.

The Government of India has introduced a number of important legislations in order to support and

promote the growth of biotechnology industry in the country. However, several organisations are

involved in regulating the development of biotechnology in the country which has often led to an

overlap of functions. In order to streamline the regulatory process, the Government has proposed

the establishment of the National Biotechnology Regulatory Authority (NBRA) to provide a

consistent mechanism for regulatory approval.

1.3. Evolution of Indian Biotech Sector

EuropEan BusinEss and TEchnology cEnTrE www.ebtc.eu

14 ovErviEw of indian BioTEch MarkET associaTEd wiTh cliMaTE changE

1.4. Market Overview

Amount in EUR Million

Particular / Year 02 -03 03-04 04-05 05-06 06-07 07-08 08-09 09-10

€ € € € € € € €

BioPharma 279.68 430 557.81 735.62 933.28 1077.96 1231.71 1379.53

BioServices 21.09 42.96

20.31

66.40 112.50 172.18 245.62 322.18 412.34

BioAgri 18.3 51.56 93.43 144.68 187.65 233.43 302.5

BioIndustrial 36.71 37.18 50 58.59 61.71 64.06 74.68 88.12

BioInformatics 11.71 12.5 15.62 18.75 22.65 29.68 34.37 36.09

Total 366.37 542.95 741.39 1018.89 1334.5 1604.97 1896.37 2218.58

Particular / Year 10-11 11-12

€ €

Expected Market (Biotech) 2343.75 2765.62

www.ebtc.eu EuropEan BusinEss and TEchnology cEnTrE

15ovErviEw of indian BioTEch MarkET associaTEd wiTh cliMaTE changE

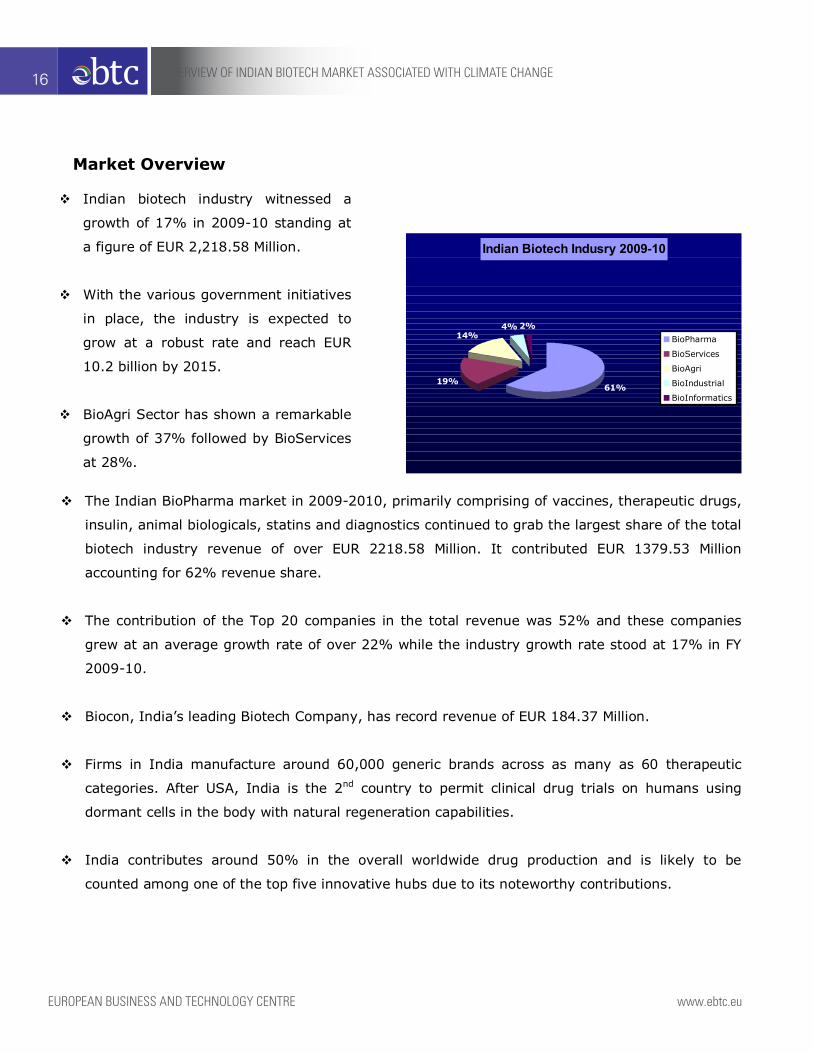

Market Overview

The Indian BioPharma market in 2009-2010, primarily comprising of vaccines, therapeutic drugs,

insulin, animal biologicals, statins and diagnostics continued to grab the largest share of the total

biotech industry revenue of over EUR 2218.58 Million. It contributed EUR 1379.53 Million

accounting for 62% revenue share.

The contribution of the Top 20 companies in the total revenue was 52% and these companies

grew at an average growth rate of over 22% while the industry growth rate stood at 17% in FY

2009-10.

Biocon, India’s leading Biotech Company, has record revenue of EUR 184.37 Million.

Firms in India manufacture around 60,000 generic brands across as many as 60 therapeutic

categories. After USA, India is the 2nd country to permit clinical drug trials on humans using

dormant cells in the body with natural regeneration capabilities.

India contributes around 50% in the overall worldwide drug production and is likely to be

counted among one of the top five innovative hubs due to its noteworthy contributions.

Indian Biotech Indusry 2009-10

61%19%

14%4% 2%

BioPharma

BioServices

BioAgri

BioIndustrial

BioInformatics

Indian biotech industry witnessed a

growth of 17% in 2009-10 standing at

a figure of EUR 2,218.58 Million.

With the various government initiatives

in place, the industry is expected to

grow at a robust rate and reach EUR

10.2 billion by 2015.

BioAgri Sector has shown a remarkable

growth of 37% followed by BioServices

at 28%.

EuropEan BusinEss and TEchnology cEnTrE www.ebtc.eu

16 ovErviEw of indian BioTEch MarkET associaTEd wiTh cliMaTE changE

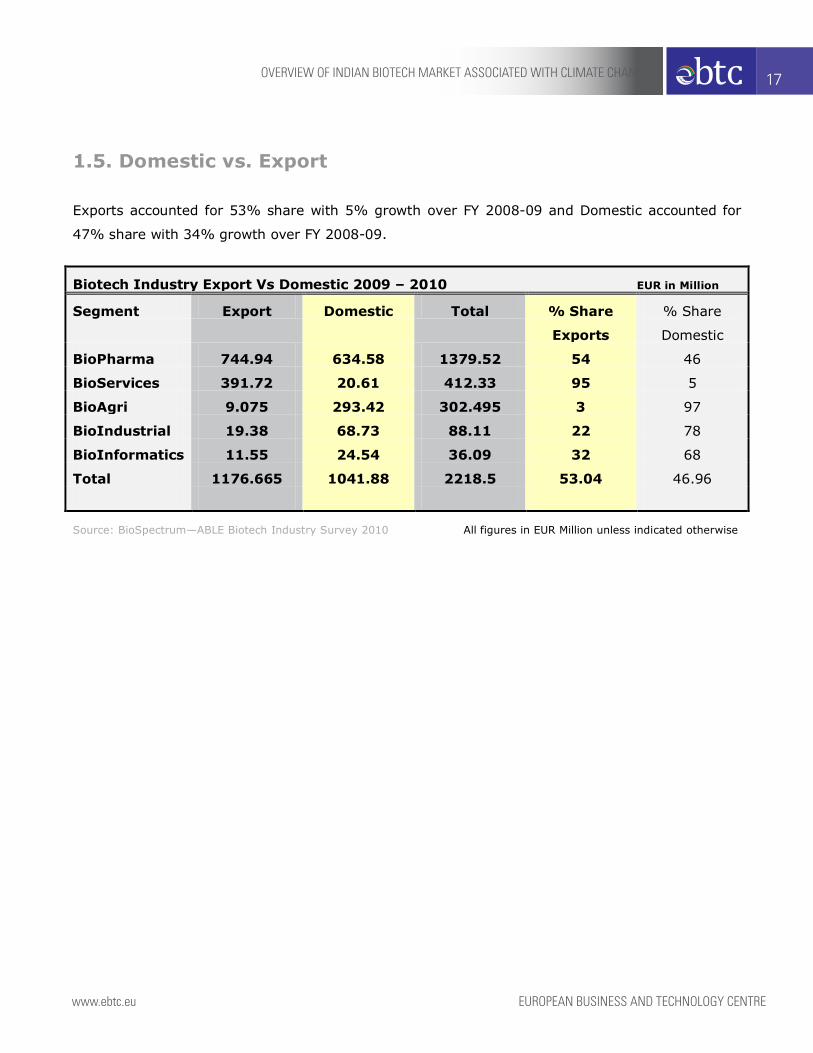

1.5. Domestic vs. Export Exports accounted for 53% share with 5% growth over FY 2008-09 and Domestic accounted for

47% share with 34% growth over FY 2008-09.

Biotech Industry Export Vs Domestic 2009 – 2010 EUR in Million

Segment Export Domestic Total % Share

Exports

% Share

Domestic

BioPharma 744.94 634.58 1379.52 54 46

BioServices 391.72 20.61 412.33 95 5

BioAgri 9.075 293.42 302.495 3 97

BioIndustrial 19.38 68.73 88.11 22 78

BioInformatics 11.55 24.54 36.09 32 68

Total 1176.665 1041.88 2218.5 53.04 46.96

Source: BioSpectrum—ABLE Biotech Industry Survey 2010 All figures in EUR Million unless indicated otherwise

www.ebtc.eu EuropEan BusinEss and TEchnology cEnTrE

17ovErviEw of indian BioTEch MarkET associaTEd wiTh cliMaTE changE

1.6. Key Market Segment

Vaccines

Diagnostic

Therapeutic

CRO

CMO

Hybrid Seeds

Biofertilisers

Biopesticides

Industry Enzymes

Biotechnology

BioPharma

BioServices

BioAgri

BioIndustrial

BioInformatics

Database Services

Biotech Software Services

Integrated Research

Application Software

EuropEan BusinEss and TEchnology cEnTrE www.ebtc.eu

18 ovErviEw of indian BioTEch MarkET associaTEd wiTh cliMaTE changE

1.6.1. BioPharmaceutical

The key ingredients of the Indian BioPharma market primarily include vaccines, therapeutic drugs,

insulin, animal biologicals, statins, and diagnostics. These are nothing but medical drugs used for

therapeutic or diagnostic purposes using biotechnology.

Majority of the biotech industry’s revenue comes from this segment. It contributed EUR 1,379.53

Million, accounting for 62% market share.

The last year sale figure for Vaccines was EUR 312.5 Million which advanced to an estimated sale

of EUR 340.62 Million; setting a new benchmark. The Total sales from the human vaccine business

stood at EUR 273.43 Million over EUR 242.18 Million for the year 2008- 2009. Animal Vaccines

witnessed a marginal decline with sales dipping down from EUR 70.31 Million to EUR 67.18 Million.

The vaccine market will push the biopharma segment growth by 10-13% in the next 5 years.

The diagnostic market touched EUR 312.5 Million in FY 2009-2010. Its share in the total BioPharma

market stands at 20-22%. On the other hand, the therapeutics market had a 15% market share in

FY 2009-2010.

The market size of Oral Diabetes Drugs and Insulin (including analogs) is estimated to be EUR

242.18 Million and EUR 95.62 Million, respectively. In the near future, Biogenerics segment will

spur quick growth for Indian players, especially with the US ready to establish a biogenerics

(biosimilars) pathway by the year 2013. In India, Erythropoietin (EPO) clocked a sales of EUR

14,960, c-GSF—EUR 7,480, interferon– EUR 14,960 and streptokinase EUR 10,880.

Currently, at least 25 Indian players are functional in the domestic market in this segment with

over 50 products already on sale. Some of the well-known companies that have taken initiatives in

the field include Glenmark, Cipla and Lupin Pharma.

www.ebtc.eu EuropEan BusinEss and TEchnology cEnTrE

19ovErviEw of indian BioTEch MarkET associaTEd wiTh cliMaTE changE

Top 20 BioPharma Companies by Revenue (2009-10)

*bio spectrum estimates All figures in EUR Million unless indicated otherwise

Source : BioSpectrum—ABLE Biotech Industry Survey 2010

1.6.2. BioServices

Clinical research and contract research organisations (CRO) are two main components of

BioServices. However, to some extent it also includes custom manufacturing. Today, BioServices

Revenue Rank 2010

Company 2009-10 2008-09 % Change over 2008-09

1 Biocon 184.37 142.55 29.34

2 Serum Institute of India*

132.81 174.06 -23.7

3 Panacea Biotec 109.87 93.30 17.76

4 Reliance Life Sciences

70.31 - -

5 NovoNordisk 53.43 51.56 3.64

6 Shantha Biotech 52.22 38.59 35.32

7 Indian Immunologicals

42.63 36.16 17.89

8 Bharat Biotech 42.44 37.66 12.7

9 Eli Lilly 29.21 25.62 13.85

10 Bharat Serums 27.34 21.87 25

11 Haffkine Biopharma

26.40 - -

12 Cadila Healthcare 23.04 14.64 57.4

13 GlaxoSmithkline 19.27 13.04 47.75

14 Intervet India 19 - -

15 Intas Biopharma 17.96 13.94 28.82

16 Themis Medicare 17.51 15.23 14.99

17 Concord Biotech 17.45 8.14 114.27

18 Venkateshwara Hatcheries*

14.06 - -

19 Aventis Pharma 10.67 5.62 89.83

20 Dr Reddy's Laboratories

9.76 6.25 56.25

EuropEan BusinEss and TEchnology cEnTrE www.ebtc.eu

20 ovErviEw of indian BioTEch MarkET associaTEd wiTh cliMaTE changE

also covers areas like data management, clinical trials, site management, bio equivalence and

toxicology studies apart from catering to the pharma industry for knowledge process outsourcing.

BioServices segment recorded a 28% growth in 2009-10 over the previous year’s total segment

revenue of EUR 322.18 Million. Over 90 percent of the total revenue of this segment comes from

exports.

The Top 10 CROs form 60% of the total segment revenue of EUR 412.34 Million.

Several companies have started contract research and clinical research services in India and

considering the potential for growth the number is expected to grow further.

Indian service industry is, decidedly, set to take the collaboration growth highway.

Top 10 Service Companies by Revenue (2009-10)

Rank 2010

Company 2009-10 2008-09 % Change over 2008-09

1 Quintiles India * 58.59 - - 2 Syngene

International 39.37 35.09 12.2

3 Jubilant Organosys

38.95 37.81 3.02

4 Sirco Clinpharm 23.43 43.75 -46.43 5 Lambda

Therapeutic Resarch*

22.65 4.68 383.33

6 Veeda Clinpharm 17.18 - - 7 Ecron Acunova 15.15 - - 8 Vimla Labs 13.81 12.75 8.36 9 Anthem

Biosciences 8.28 5.05 63.88

10 Max Neeman International

6.25 2.34 166.67

*Bio Spectrum Estimates All figures in EUR Million unless indicated

otherwise

Source: BioSpectrum—ABLE Biotech Industry Survey 2010

www.ebtc.eu EuropEan BusinEss and TEchnology cEnTrE

21ovErviEw of indian BioTEch MarkET associaTEd wiTh cliMaTE changE

1.6.3. BioAgri

Agri-biotech includes hybrid seeds and transgenic crops, biopesticides and biofertilisers. In the FY

2009-2010, Agri biotech was the third largest contributor to the Indian biotech industry with a

turnover of EUR 302.5 Million. It accounted for around 14% of the total biotech revenue. BioAgri

registered a 37% growth over last year and emerged as the fastest growing segment of biotech

industry.

The Bt cotton cultivation in India covers almost 8.4 million hectares of land. In India, there has

been a dramatic increase in the number of companies selling Bt cotton seeds over the last eight

years after the first commercialization in 2002. At present, there are more than 30 companies in

the country marketing Bt cotton seeds.

Nuziveedu Seeds is acclaimed as the largest Bt cotton seeds seller which sold 70 lakh packets

generating a revenue of EUR 74.50 Million followed by the second largest seller - Rasi Seeds with a

sale value of EUR 56.05 Million. Nuziveedu holds a leading market share of 25% while Rasi Seeds

stands second holding a market share of 19%. Some of the other prominent players include Ajeet

Seeds and Ankur Seeds selling 1.2-2 Million packets each in FY 2009-10.

In 2009 alone, a total of 28 Million seed packets, containing 450 grams were sold. Out of the total

seeds sold, around 87% were Bollgard II and 13% were Bollgard I. In addition to this, an

estimated figure of at least 2 Million packets of spurious seeds was sold illegally to the farmers

particularly in the state of Gujarat. The pricing of Bollgard I and Bollgard II cotton seeds was kept

as EUR 10.15 and EUR 11.71 respectively in most of the regions, however, the pricing in North

(especially Punjab, Haryana and, Rajasthan) was kept as EUR 11.85 for Bollgard I and EUR 14.45

for Bollgard II.

Nine states were involved in the sale of the “Bollgard” Bt cotton seeds - Andhra Pradesh, Tamil

Nadu, Karnataka, Gujarat, Madhya Pradesh, Maharashtra, Haryana, Punjab, and Rajasthan. From

the nine aforesaid states, Maharashtra leads the sale charts selling almost 9 Million packets in the

region followed by the South (7.5 million packets) and North (4.5 million packets). The northern

market is primarily ruled by Shriram Bioseeds.

EuropEan BusinEss and TEchnology cEnTrE www.ebtc.eu

22 ovErviEw of indian BioTEch MarkET associaTEd wiTh cliMaTE changE

A region wise split reveals Northern India as the producer of the highest yield of Bt cotton. The

approval of MLS 9124 was an important breakthrough in the year 2009. The type was developed

indigenously by Metahelix Life Sciences. It comprises a synthetic cry 1C gene. Another significant

development was the release of two cotton hybrids namely MH 5124 and MH 5174 expressing the

synthetic cry 1C gene (MLS 9124).

Region Production

North 600 kg per hectare

West 516 kg per hectare

Central 472 kg per hectare

South 595 kg per hectare

Top 10 BioAgri Companies by Revenue (2009-10) Rank 2010

Company 2009-10 2008-09 % Change over 2008-09

1 Nuziveedu Seeds

74.50 70.15 6.07

2 Rasi Seeds 56.05 58.68 -4.48 3 Mahyco 48.75 32.98 47.78 4 Monsanto* 39.84 53.90 -26.09 5 Krishidhan

Seeds 20.81 9.88 110.64

6 Ankur Seeds 17.10 12.55 36.28 7 Ajeet Seeds* 16.09 - - 8 Nath Seeds 13.28 7.57 75.26 9 J K

Agrigenetics* 5.46 4.06 34.62

10 Bayer CropScience*

3.51 - -

*BioSpectrum

Estimates All figures in EUR Million unless

indicated otherwise

Source: BioSpectrum—ABLE Biotech Industry Survey 2010

www.ebtc.eu EuropEan BusinEss and TEchnology cEnTrE

23ovErviEw of indian BioTEch MarkET associaTEd wiTh cliMaTE changE

1.6.4. BioIndustrial

The BioIndustry primarily comprises enzyme manufacturing and marketing companies. In India,

enzymes are still used on a limited scale but India surely holds a considerable growth potential.

The industrial enzyme consumption in India is principally in the detergents market (40%), followed

by the starch market (25%). Lately, enzymes have found wide applications in food,

pharmaceutical, diagnostic, and chemical processing industries.

Novozymes is a leading player in this segment holding over 50% market share followed by

Advanced Enzyme Technologies holding 25-30% market share.

The Indian companies are experiencing a substantial growth, and are thus focusing more on R&D

due to which new applications are being discovered. However, the global enzyme industry in India

still has a long road to be covered.

Top 10 BioIndustrial Companies by Revenue (2009-10) Rank 2010

Company 2009-10 2008-09 % Change over 2008-09

1 Novozymes South Asia*

41.87 39.06 7.2

2 Advanced Enzymes

18.90 13.84 36.57

*BioSpectrum

Estimates All figures in EUR Million unless

indicated otherwise

Source : BioSpectrum—ABLE Biotech Industry Survey 2010

1.6.5. BioInformatics

BioInformatics entails the creation and advancement of databases, algorithms, computational and

statistical techniques, and theory to solve formal and practical problems arising from the

management and analysis of biological data. Basically, it involves construction of databases on

genomes, protein sequences, and modeling complex biological processes, including systems

biology.

EuropEan BusinEss and TEchnology cEnTrE www.ebtc.eu

24 ovErviEw of indian BioTEch MarkET associaTEd wiTh cliMaTE changE

BioInformatics accounts for the smallest segment of the biotech Industry, holding a mere 2%

share in the overall industry. In the year 2009-2010, it recorded a sluggish 5% growth over 2008-

09 as compared to the 16% growth in FY 2008-09.

The pure-play BioInformatics companies in India include Strand Genomics, Ocimum Biosolutions,

SysArris, CytoGenomics and Molecular Connections. Majority of these companies are small- to-

medium enterprises based in Bangalore, Hyderabad, Pune, etc.

Rank 2010

Company 2009-10 2008-09 % change over 2008-09

1 Ocimum Biosolutions

6.46 7.43 -12.97

2 Strand Life Sciences

5.46 5.46 0

*BioSpectrum Estimates

All figures in EUR Million unless indicated otherwise

Source : BioSpectrum—ABLE Biotech Industry Survey 2010

1.7. Top Biotech Cluster and Cities

Particular Amount Percentage

Maharashtra Mumbai 480.625 35.04

Pune 186.25

Karnataka Bangalore 446.40 20.12

Andhra Pradesh Hyderabad 348.43 15.71

NCR NCR 317.18 14.30

Gujarat Ahmedabad 160.15 7.92

Others Others 270.46 6.91

Source : BioSpectrum—ABLE Biotech Industry Survey 2010

All figures in EUR Million unless indicated otherwise

www.ebtc.eu EuropEan BusinEss and TEchnology cEnTrE

25ovErviEw of indian BioTEch MarkET associaTEd wiTh cliMaTE changE

This increased the share of the Western region in the overall revenue by 3% over FY 2008-09

giving it a lead of 6% over the Southern cluster.

Southern region is counted as India’s largest Biotech cluster with the highest number of biotech

companies - 172 in number (West has 137 companies) which made a revenue of EUR 865.26

Million in the FY 2009-10 accounting for 39% of the total revenue. Further, Karnataka state

government has plans to set up around five new biotech parks involving an investment of EUR

171.87 Million. Andhra Pradesh is also launching a MedTech Valley at Shameerpet in Hyderabad

stretching across 1,200 acres of land.

The Kerala State Industrial Development Corp (KSIDC) has announced setting up state-of-the-art

life science park worth EUR 46.87 Million at Thonnakkal in Thiruvananthapuram spanning across

260 acres.

The Northern biocluster – National Capital Region (NCR) houses the Top 3 biotech companies that

contribute around 15% of the total industry revenue. The Northern cluster is famous for its

research institutes and government bodies. A 200 acre Health Biotech Science Cluster (HBSC) is

being developed at Faridabad and would include Translational Health Science & Technology

Institute (THSTI), Regional Center for Biotechnology (RCB), Center for Vaccinology, Molecular

Medicine Center, Center for Diagnostics, Biotech Park, Center for Health Science Technology,

Maharashtra35%

Karnataka20%

Andhra Pradesh16%

NCR14%

Gujarat8%

Other7%

Among the biotech clusters in India, the

Western cluster continues to dominate

the industry with a 46 percent share in

the overall revenue of EUR 2218.58

Million. The companies in the Western

region, 137 in number, churned out a

whopping amount of EUR 1036.09

Million in the FY 2009-10.

EuropEan BusinEss and TEchnology cEnTrE www.ebtc.eu

26 ovErviEw of indian BioTEch MarkET associaTEd wiTh cliMaTE changE

Center for Platform Technologies, UNESCO Center, Incubator and a Center for Animal Model for

Clinical Advances. The first initiative in this regard came with the recent inauguration of a

temporary THSTI lab at Gurgaon, which will later be shifted to Faridabad once the infrastructure is

ready.

In addition to the above, Lucknow also has a biotech park. Rajasthan State industrial Development

& Investment Corporation (RIICO) has also taken an initiative to set up three Biotech Parks at

Sitapura-Jaipur and Chopanki, Bhiwadi (Alwar), and Borandi. A biocluster at Mohali (Punjab), a

biotech park at Chandigarh (Punjab), and at Nalagarh in Himachal Pradesh are also proposed.

1.8. Major Deals • Four Deals have been completed in 2010

• In June 2010, Piramal Healthcare Ltd. acquired Canadian biotechnology company

Biosyntech, Inc for EUR 2.85 Million.

M&A (Period: January 1, 2010 to October 31, 2010)

Deal Type Number of Deals Deal Value (EUR Million)

Inbound 2 16.49

Outbound 1 2.85

Domestic 1 -

Foreign Direct Investment (Period: November 2000 to August 2010)

Sector Amount of FDI Inflow (EUR Million) Drugs and pharmaceuticals 1,239.36

Deal Summary

Deal Type Acquirer Acquirer’s Country

Target Name Target Country

Completion Date

www.ebtc.eu EuropEan BusinEss and TEchnology cEnTrE

27ovErviEw of indian BioTEch MarkET associaTEd wiTh cliMaTE changE

Inbound Sequoia

Capital India Invest

Mauritius

Celon Laboratories Ltd

India 5th October 2010

Inbound Telematic& Biomedica

Italy

MNE Technologies Pvt Ltd

India 31st March 2010

Outbound Piramal Healthcare Ltd

India

Bio Syntech, Inc

Canada 21st June 2010

Domestic Anu's Laboratories Ltd.

India

Stilbene Chemicals Ltd

India 16th April 2010

1.9. Government / Organisation

Government of

India

Ministry of Science

& Technology

Ministry Of Health

Ministry of

Environment & Forest

Ministry of New &

Renewable

Ministry of Agriculture

Ministry of Human

Resource and Development

Departments of Biotechnology

Departments of

Environment, Forest & Wildlife

Indian Council of Medical Research

Indian Council of

Agricultural Research

Recombinant DNA Advisory

Committee (RDAC)

Regulatory Committee on

Genetic Manipulation

(RCGM)

Institutional Biosafety

Committee (IBSC)

Genetic Engineering Approval Committee

(GEAC)

Department of Science & Technology

Department

of Atomic Energy

DSIR

EuropEan BusinEss and TEchnology cEnTrE www.ebtc.eu

28 ovErviEw of indian BioTEch MarkET associaTEd wiTh cliMaTE changE

1.9.1. Government of India In 1986, the Department of Biotechnology (DBT) was set up by the Government of India under the

Ministry of Science and Technology. The DBT has established ‘Centres of Excellence’ which

generate skilled manpower and support the R&D efforts within the country. Before DBT, the

National Biotechnology Board (NBTB) was established in 1982 to promote biotechnology products

and processes.

1.9.2. Department of Biotechnology The Biotechnology department was established with the vision to create innovative technologies

and tools that can address the existing issues in food production, agriculture productivity,

environmental sustainability, nutrition security, and health care by launching new products and

services at affordable prices and generating employment opportunities that eventually give India a

global competence in the emerging bio-economy.

The functions of the department of Biotechnology are as follows:

1. Human Resource Development, biotech product development and value chain processing.

2. Establishing the required facilities and infrastructure for biotechnology for research purpose.

3. Orienting the sectoral R&D programmes towards the emerging and development areas of

agriculture, vaccines and diagnostics, biofuels and bioenergy, stem cell biology, etc.

4. Establishing centres of excellence and encouraging innovative thinking.

5. Launching Grand Challenge Programmes on breeding crops.

6. Encouraging young Indian scientists/ scientists from abroad to take up research in Indian

universities and institutions.

7. Establishing new institutions for critical areas holding national importance.

8. Promoting interaction between academia and industry and the development of both

products and processes.

9. Introducing major public-private partnership programmes for research on futuristic

technologies and also providing assistance to SMEs and other big industries.

10. Establishing superior mechanisms and institutional framework for facilitating stakeholder

communication.

www.ebtc.eu EuropEan BusinEss and TEchnology cEnTrE

29ovErviEw of indian BioTEch MarkET associaTEd wiTh cliMaTE changE

Objective Action

Ensure availability of adequate human

resource at all levels

Different fellowships and HRD & R&D

schemes

Engage public-private partnerships Launching healthcare & agricultural

projects at the right time: public-private

partnerships.

Promote basic and translational research Undertaking genomic crop research

Establish new centres of excellence and

technology platforms

Increasing the biodesign capacity to

produce improved medical devices

1.9.3. Department of Science & Technology (DST) May 1971 was the year of establishment of Department of Science & Technology (DST). It was

founded with the purpose of promoting new areas of Science & Technology and also to act in the

capacity of a nodal department for coordinating, organising and promoting S&T activities in India.

The department has responsibilities for particular projects and programmes towards:

1. Policy formulation for Science and Technology.

2. Promoting new avenues in the field of Science and Technology with increased emphasis on

upcoming trends and areas.

3. Futurology.

4. Approving the Grants-in-aid for the Scientific Associations, Scientific Bodies and Scientific

Research Institutions and also supporting their cause.

5. Matters related to domestic technology; especially promoting ventures for commercialization of

a technology that does not fall under Department of Scientific and Industrial Research.

6. Matters related to capacity building for institutional Science and Technology.

7. Promoting Science and Technology at a grass-root level.

8. Applying Science and Technology for the benefit of weaker and disadvantaged sections of the

society.

EuropEan BusinEss and TEchnology cEnTrE www.ebtc.eu

30 ovErviEw of indian BioTEch MarkET associaTEd wiTh cliMaTE changE

1.9.4. National Biotechnology Regulatory Authority The Department of Biotechnology (DBT) has been assigned the responsibility of establishing the

National Biotechnology Regulatory Authority (NBRA) as per the directives of the Indian

Government. The NBRA will function as a self-directed, independent, and professionally led body

offering a single-window mechanism for obtaining a biosafety clearance for the genetically modified

processes and products.

The National Biotechnology Regulatory Bill, 2008 seeks to safeguard the health and safety of the

people and to regulate the safe development and deployment of biotechnology products and

processes.

The new legislation is expected to provide an opportunity to consolidate and enhance the efficiency

and effectiveness of biotechnology regulation, increase collaboration with state governments in this

area, promote public confidence in the regulatory system, and facilitate international trade.

The Indian Government has also given a green signal to the National Biotechnology Development

Strategy. The strategy, besides using the available opportunities in manufacturing and services

also lays a strong platform for innovation using technology for sustainable industrial growth and

long-term benefits.

1.9.5. Council of Scientific and Industrial Research (CSIR) The Council of Scientific and Industrial Research undertakes research in different fields of science

and technology through a network of national institutes and laboratories in different parts of the

country. It gives special importance to applied research with an equal emphasis on utilising the

results thereof.

Currently, there are 38 research institutes, including five research laboratories at regional level.

Some institutes have established survey field stations for experimental purpose in order to

enhance their research activities. At present, 39 such survey field stations are operating and are

attached to 16 laboratories. The CSIR laboratories are set up for the advancement of Indian

science and industry and for catering to the societal needs for food, fuel, roads, etc. However,

www.ebtc.eu EuropEan BusinEss and TEchnology cEnTrE

31ovErviEw of indian BioTEch MarkET associaTEd wiTh cliMaTE changE

some laboratories look after specific problems which are of interest for particular industries, for

example, biotechnology, drugs & pharmaceuticals, marine chemicals, scientific instruments, etc.

There are yet other laboratories concerned with research in aerospace science and engineering,

mechanical engineering, metrology, oceanography, electrochemistry, geophysics, experimental

medicine, and toxicology.

Having completed more than 63 years of existence, CSIR today is the country’s largest holder of

intellectual property rights (IPR) on patents.

1.9.6. Indian Council of Medical Research (ICMR) The Indian Council of Medical Research (ICMR), New Delhi, is undoubtedly one of the oldest bodies

in the world for medical research. It formulates, coordinates, and promotes biomedical research in

India.

Formerly known as the Indian Research Fund Association (IRFA), it was founded in 1911 by the

Indian Government specifically for coordinating/ sponsoring medical research in the country. Post

independence, IRFA saw major changes in the organisation, activities and a wider functional

expansion. In 1949 IRFA was renamed as the Indian Council of Medical Research (ICMR).

The research priorities of the Council coincide with the priorities of National health. All its efforts

are directed at reducing the disease rate and promoting the population’s well-being and health.

The Union Health Minister presides over the Governing Body of the Council. Scientific Advisory

Board provides scientific/ technical assistance to the Governing Body of the Council and includes

eminent experts with a varied background in biomedical disciplines. The Board is further assisted

by a series of Scientific Advisory Committees, Scientific Advisory Groups, Task Forces, Steering

Committees, Expert Groups, etc., these monitor and assess the Council’s research activities.

EuropEan BusinEss and TEchnology cEnTrE www.ebtc.eu

32 ovErviEw of indian BioTEch MarkET associaTEd wiTh cliMaTE changE

The ICMR is not merely involved in research activities, it also promotes the manpower

development in biomedical research through (i) Research Fellowships (ii) Short-Term Visiting

Fellowships (iii) Short-Term Research Studentships and (iv) Various Workshops and Training

Programmes organised by ICMR Institutes and Headquarters.

The Council also gives an opportunity to the retired medical teachers and scientists by offering the

position of Emeritus Scientist to take up/ continue with the biomedical research on specific topics.

The Council also confers prizes and awards on the Indian scientists. Currently, there are 38 awards

that the Council gives away for significant contribution. Out of these 38 awards, 11 awards are

exclusively meant for young scientists who are below 40 years of age.

The burgeoning population and the increasing count of infectious diseases have become a priority

to be dealt with using medical research for several decades. Apart from dealing with these issues

the current trends have increasingly intensified the research on emerging health problems. This

has also sparked and revived the research on Herbal Remedies or Traditional Medicine adopting a

disease-oriented approach. The Council is keeping a watch on new diseases and also looking into

the new aspects of existing diseases; the growing network of Surveillance Centres for AIDS in the

different Indian States in 1986 is a good example.

1.9.7. Indian Council of Agricultural Research (ICAR) An autonomous organisation, the Indian Council of Agricultural Research (ICAR) falls under the

ambit of Department of Agricultural Research and Education (DARE), Ministry of Agriculture,

Government of India. Originally addressed as Imperial Council of Agricultural Research, the

organisation came into existence on 16 July, 1929 as a registered society under the Societies

Registration Act, 1860 in accordance with the report of the Royal Commission on Agriculture. ICAR

is headquartered at New Delhi.

An apex body, the Council is responsible for guiding, co-coordinating, and managing education and

research in different fields of agriculture throughout the country, including fisheries, horticulture,

and animal sciences. The Council has a widespread network of 97 ICAR institutes and 47

www.ebtc.eu EuropEan BusinEss and TEchnology cEnTrE

33ovErviEw of indian BioTEch MarkET associaTEd wiTh cliMaTE changE

agricultural universities across the length and breadth of the country and is hailed as one of the

largest national agricultural systems in the world.

A pioneer of the Green Revolution in agriculture, the ICAR has played a crucial role in the

subsequent agricultural developments in the country by promoting research and technology that

has enabled India to increase its food grain production by 4 times, production of

horticultural crops by 6 times, production of milk by 6 times, production of eggs by 27

times, and production of fish by 9 times (inland 17 times and marine 5 times), since 1950-

51.

1.9.8. University Grant Commission (UGC) UGC has a broader spectrum of responsibilities and duties towards universities. It has the onus of

providing leadership in professions, politics, administration, industry, and commerce. The UGC has

been entrusted the responsibility of meeting the growing demands of higher education, technical

and professional knowledge and literacy and scientific fields. It also inspires the country to achieve

the freedom from disease, want, and ignorance in a short span of time by applying and developing

scientific and technical knowledge.

UGC has a unique identity of being India’s one and only grant-giving agency which shoulders two

major responsibilities of providing funds and determining, coordinating, and maintaining higher

standards in higher educational institutes.

1.9.9. Department of Scientific and Industrial Research (DSIR) The Department of Scientific and Industrial Research (DSIR) is an undertaking of the Ministry of

Science and Technology. It was announced through a Presidential Notification, dated January 4,

1985 (74/2/1/8 Cab.) contained in the 164th Amendment of the Government of India (Allocation of

Business) Rules, 1961. The Department of Scientific and Industrial Research (DSIR) takes care of

the activities related to technology promotion, development, utilisation and technology transfer at

an indigenous level.

EuropEan BusinEss and TEchnology cEnTrE www.ebtc.eu

34 ovErviEw of indian BioTEch MarkET associaTEd wiTh cliMaTE changE

The primary purpose of DSIR is to promote industrial R&D, support small and medium industrial

units in developing state-of-the art international level technologies of high commercial potential,

facilitate commercialization of lab-scale R&D at a rapid pace, increase the percentage of technology

intensive exports out of the overall exports, enhance capabilities related to industrial consultancy &

technology management and introduce a user-friendly information network to assist industrial and

scientific research in India. It also plays a key role in linking the industrial establishments and

scientific laboratories for transferring technologies through National Research Development

Corporation (NRDC) and encourages investment in R&D through Central Electronics Limited (CEL).

1.9.10. UNESCO and other similar organisations The United Nations Educational, Scientific and Cultural Organization (UNESCO) is a

specialized United Nations agency that contributes to and promotes international collaboration

through education, science, and culture.

UNESCO achieves its objectives through education, natural sciences, social and human sciences,

culture, communication, and information. It also sponsors programs on literacy, technical, and

teacher-training; international science; promotion of independent media, freedom of press;

regional and cultural history projects; promotion of cultural diversity; international cooperation

agreements to preserve the (World Heritage Sites), and the human rights. UNESCO also strives to

bridge the global digital divide.

The Government of India and UNESCO jointly established the Regional Centre for research, training

and education in biotechnology sponsored by UNESCO. Also, by next year a UNESCO Regional

Centre for Biotechnology will be set up in Faridabad, Haryana.

The UNESCO Regional Centre for Biotechnology is a unique platform for interdisciplinary research,

training, and education to furnish human resources required at the biotech interface of medicine,

chemistry, physics, and engineering. Its objective also includes empowerment of human resources

for the varied biotech needs and seeking innovative and context-specific biotechnology solutions.

www.ebtc.eu EuropEan BusinEss and TEchnology cEnTrE

35ovErviEw of indian BioTEch MarkET associaTEd wiTh cliMaTE changE

1.9.12. Health Biotech Science Cluster (HBSC) Even though the life sciences industry in India has progressed with the upcoming research centers,

academic institutes, and development of healthcare industry, the growth is still confined.

Faridabad, Bangalore, and Mohali have decided to host biotech science clusters where all such

ideas can bear fruits. These clusters include an exclusive Health Biotech Science Cluster (HBSC)

being developed by the Department of Biotechnology. The HBSC will be built on a 200 acre stretch.

It will foster ground-breaking conceptual research for biotech-related sciences, initially focusing on

health biotechnology. The Translational Health Science Technology Institute (THSTI) and UNESCO

Regional Center for Biotechnology (URCB) will be housed as the founding institutes in this cluster.

To begin with, they will operate from Udyog Vihar, Gurgaon. Faridabad is where the first phase of

work will begin on the 40-acre land. The permanent laboratories will be set up in the coming three

years.

The second phase of the cluster will see the presence of a number of related centers which are still

at a conceptual stage. Center for Vaccinology, Center for Diagnostics, Center for Health Science

Technology, Center for Platform Technologies, Center for Animal Model for Clinical Advances,

Biotech Park, Incubator, Molecular Medicine Center, and National center for Biodesign are likely to

be a part of the cluster in the second phase.

1.9.13. All India Biotech Association (AIBA) All India Biotech Association (AIBA) was founded in 1994 as a non- profit Society to serve as the

top-most Forum at national level for representing the interests of the people engaged in different

areas of Biotechnology. The primary purpose of AIBA is to promote and protect the overall

interests of Biotechnology as a science, industry, profession & trade. The Southern Chapter of AIBA

started functioning at Hyderabad in August, 1999. The core objectives of AIBA are as

follows:-

• Promoting and protecting the overall interests of Biotechnology.

• Collecting all the relevant information to safeguard the interests of the constituent members for

activities related to Biotechnology.

EuropEan BusinEss and TEchnology cEnTrE www.ebtc.eu

36 ovErviEw of indian BioTEch MarkET associaTEd wiTh cliMaTE changE

• Subscribing and promoting the goals and objectives of an Association/ society that shares the

same objectives as those of the Association and encouraging a Government Policy or any

Association for improving the laws related to Biotechnology.

• Coordinating and assisting its constituent members for research, manufacturing, and

professional and export promotion activities.

• Sponsoring business and study teams, undertaking research, and market surveys.

• Settling the disputes arising within the Association objectives.

• Advising/ representing the local public bodies and Central and State Governments for all the

matters related to biotechnology.

• Awarding individual persons and institutions for their exceptional contributions to meet the

objectives of the society.

1.9.14. Ministry of New and Renewable Energy (MNRE) The Ministry of New and Renewable Energy (MNRE) is allocated the following subjects or business:

1. Research/ promotion of Biogas and related programmes;

2. Commission for Additional Sources of Energy (CASE);

3. Application, development and production of Solar Energy, including Solar Photovoltaic devices;

4. Programmes for research and promotion of improved chulhas;

5. Indian Renewable Energy Development Agency (IREDA);

6. All aspects related to hydel projects which are small, mini or micro-level and have a capacity lower than 25 MW;

7. Research and promotion of fresh sources of renewable or non-conventional energy and related programmes;

8. Tidal energy;

9. Integrated Rural Energy Programme (IREP);

10. Geothermal Energy;

11. Bio-fuels: (i) Establishing National Bio- fuels Development Board and fortifying the current mechanism of the institutes; (ii) National Policy; (ii) Promotion, demonstration and research on transport, stationary and other applications; and (iv) overall coordination.

www.ebtc.eu EuropEan BusinEss and TEchnology cEnTrE

37ovErviEw of indian BioTEch MarkET associaTEd wiTh cliMaTE changE

2. Overview of Indian Biotech associated with Climate Change; Strengths and Weaknesses

2.1. Indian Biotech Sector - Climate Change Climate change is a hot topic for discussion and a key government agenda on a global scale. India

too cannot escape the damaging effects of global warming. With majority of India’s population

residing in the rural areas, the poor cannot afford to fend for themselves against the devastating

effects of global warming. The National Action Plan commented on the Climate Change stating that

India’s population is closely knitted and economically dependent on the natural resources and

climate dependent sectors like agriculture, water and forestry and thus needs an honest adaptive

approach and capacity to combat the climatic changes. According to the International Energy

Agency, India is set to become the third largest emitter of greenhouse gases by the year 2015.

India is still at a developing stage and so it can not really afford to face the dangers arising out of

climate change. Also, more than a quarter of the country’s population lives below the poverty line,

which makes it essential to reduce the vulnerability of the masses to the severe impacts of climate

change. Knowing this, and the fact that by the year 2030 the primary energy demand will be

doubled implies that the Indian government has already initiated significant mitigation measures

by framing new laws and introducing green business codes: incentives for promoting renewable

energy/ energy efficiency, and adaptation techniques making agriculture more resistant against

the impact of climatic changes have been suggested. In an effort to cut down the intensity of

carbon emissions by 20-25%, India has also set voluntary targets for itself with a deadline of

2020. Despite of all the measures and the public acknowledgement about recognising climate

change as a pressing problem for India, policymakers still struggle to locate the required resources

and the necessary expertise to be able to address the climate-related issues and find workable

resolutions.

To overcome the menacing challenges of climate change it has become necessary for the private

sector to step in and play a critical role.

EuropEan BusinEss and TEchnology cEnTrE www.ebtc.eu

38 ovErviEw of indian BioTEch MarkET associaTEd wiTh cliMaTE changE

A recent study indicates that by the year 2017, the green spending in India may touch a figure of

EUR 102 Billion. This in turn will usher huge business opportunities. India stands a fair enough

chance to be the world leader in the “Go-Green” drive harnessing the resources as well as the

expertise of private investors and enterprises. The country already has a large market for green

and low-carbon goods and is still at an expansion stage.

Similarly, investments look promising with an increased number of Indian enterprises and their top

management taking pains to control their percentage of carbon emission. This is a deciding factor

for most of the financial institutions for investing their capital. Currently, investors are well-versed

with the available opportunities in the market and the Indian private sector has executed low-

carbon projects utilising different sources for investment, for example, self-financing, venture

capital, private equity investment and carbon finance, if available.

There is still a lot to be done to speed-up the process. Financial incentives can play a critical role in

bringing individuals and institutions on board. To mitigate the climate change impact, a regulatory

environment which is crystal clear and reliable is the need of the hour. Investors have a never-

ending appetite to fund green and clean technologies like renewable energy, but this is possible

only if they are assured about their investment decisions being safe with a secure legal framework

in place. It is essential to analyse and inspect how the financial market expertise can be utilised to

develop unique financing techniques. For that matter, London can enter a partnership with India

where India’s green drive and entrepreneurial talent can be linked with London’s expertise

regarding financial innovations and its image as the main hub for carbon financing.

Climate change brings its own set of challenges for each and every individual and there is surely no

easy way out, however, if the government along with the private investors work in a coordinated

manner and take prompt actions the same challenges can actually be transformed into big-time

opportunities for the Indian businesses building a new path that leads to a sustainable and cleaner

planet.

www.ebtc.eu EuropEan BusinEss and TEchnology cEnTrE

39ovErviEw of indian BioTEch MarkET associaTEd wiTh cliMaTE changE

2.2. Role of Various Ministries and Autonomous Institutions

Department of Biotechnology: Environmental Biotechnology – Programmes

Biotechnology has an enormous potential to offer eco-friendly, efficient, economically viable and

unique options for in-situ waste treatment and degradation of the potentially hazardous toxic

waste into harmless/ relatively less harmful byproducts. The Department of Biotechnology has

given a significant thrust to programmes on treatment of industrial effluents, mining spoil dumps,

development of biosensors for detection of pollutants, ecorestoration of degraded ecosystems, and

use of molecular markers to characterise biodiversity. All such programmes have been pushed and

conceived by eminent scientists who have headed the task force on Environmental Biotechnology

and Biodiversity Conservation over the last few years.

Achievements

Around 65 projects were sanctioned during the review period. As many as 45 projects have been

finished while 50 are still under process. The projects cover some prime areas like treatment of

industrial effluents especially paper and pulp industry, electroplating, distillery, oil refineries, dye

industry, tannery, etc., use of isozymes/ molecular markers like RFLP, RAPD for characterisation of

biodiversity, ecorestoration of degraded lands and mine spoil dumps. Developing programmes

based on the needs of the users has also reflected in the Department’s efforts.

Efforts are being made to change the research leads obtained from completed/ ongoing projects

into technologies and then demonstrating them at the site of user industries. A lot of emphasis is

laid on involving the user industry right from the start to validate the process on site for a smooth

technology transfer. The standard technologies developed in the labs are being upgraded and

transferred to industries for large scale exploitation. Several attempts were made to spot out the

priority areas and many brainstorming sessions were also held for gap areas to create integrated

R&D proposals. The brainstorming session details are as below:

• Degradation of pesticides held in May, 1999 at ITRC, Lucknow

• Biodiversity Conservation held on Sept, 16, 2000 at NEHU, Shillong

• Biodegradation of Textile and Dye Industry wastewater treatment on 19th July, 2001 at

Sardar Patel University, Anand

EuropEan BusinEss and TEchnology cEnTrE www.ebtc.eu

40 ovErviEw of indian BioTEch MarkET associaTEd wiTh cliMaTE changE

• Conservation and Genetic Enhancement of Cryptogamic Plants for Pollution abatement on

28-29th December, 2001 at NBRI, Lucknow

• Metabolic Engineering for Environmental amelioration at Thapar Institute, Patiala on 8-

9th April, 2002

Some of the important achievements are as follows:

1) Establishing a laboratory for conservation of endangered animal species CCMB, Hyderabad

2) Pesticide degradation network programmes

3) Programme to conserve the biodiversity of North-Eastern Region

4) Conservation programmes and programmes to make use of lower plants as pollution

indicators

5) Molecular biology programmes for environmental amelioration

6) Ecorestoration of degraded ecosystems, including mine dumps

7) Afforestation of Mangroves by applying biotechnological and classical tools

Environmental Biotechnology – Technology / Treatment

The standard technologies developed at laboratory scale due to the efforts of the Department have

been upgraded to pilot level, demonstrated on the industry site, and transferred. Some of the

noteworthy technologies are as below:

1) Industrial Effluent Treatment: Microbial Treatment of Cassava Starch Factory Waste Water;

Central Tuber Crops Research Institute (CTCRI), Thiruvananthapuram has introduced a

standard technology for degradation of waste water from starch factory.

2) Paper and Pulp Mill Effluent Treatment: GB Pant University of Agriculture and Technology

has invented a pilot scale technology for treating the effluent of paper and pulp mills. The

technology was demonstrated at Shyam dyeing company, Sanganer. For treating the waste

of 3 units, a common effluent treatment plant has been established having a capacity of

treating textile wastewater up to 35,000 litre/ day. Sardar Patel University, Anand has

developed bench scale sequential anaerobic-aerobic treatment system comprising anaerobic

up flow film bioreactor and fluidized bed bioreactor for treating reactive dye industry

effluent.

www.ebtc.eu EuropEan BusinEss and TEchnology cEnTrE

41ovErviEw of indian BioTEch MarkET associaTEd wiTh cliMaTE changE

3) Oilzapper Technology has been developed for Treatment of Oily Sludge and Bioremediation

of Crude Oil Spills. The technology has been developed by TERI, New Delhi and has been

demonstrated in several refineries viz., Bharat Petroleum Corporation Ltd., Guwahati

Refinery, Assam; Digboi Refinery, Assam; Kandla Terminal, Gujarat; Barauni Refinery,

Bihar; Bharat Petroleum Corporation Ltd., Maharashtra; and Hindustan Petroleum

Corporation Ltd.

4) A chemo biochemical process has been developed by Microbial Desulphurisation of Fossil

Fuels and Biogas NEERI, Nagpur for desulphurisation of gaseous stream which contains

hydrogen sulphide. The process has been successfully demonstrated at Vam Organic

Chemicals Ltd., Gajraula on a pilot scale with a capacity of 100 Nm3 / hr to check the

techno-economic feasibility of the process for large scale application. The same process has

also been demonstrated at Mathura Refinery.

Biosensor / Biosurfactant / Bioscrubber

1) Biosensor for Detection of Pesticide Residues: A biosenser has been developed by the Visva

Bharti University, Shantiniketan for detecting and estimating organophosphates like

carbamate residues and Metacid in the environment. The sensor is constructed and

designed as per the ability of these two pesticides to inhibit the activity of

acetylcholinesterase (AchE); an indispensable enzyme responsible for normal neural

transmission. The biosensor is portable, simple, and capable of providing quick data in the

field for measuring the trace concentration residues of these pesticides. The biosensor is

similar to a pH paper which changes colour depending on the contamination level. Lower

contamination level is indicated by a greater intensity of the yellow colour while a higher

contamination level is indicated by a decreasing intensity of the same.

2) Detection of Pathogens in Drinking Water: A user-friendly colour based detection system

has been developed by NEERI, Nagpur for the presence of E.coli (up to 500 cells) in

drinking water. Attempts are being made to enhance the sensitivity of the test by

decreasing the pathogen load and extending the test to Vibrio and Salmonella.

EuropEan BusinEss and TEchnology cEnTrE www.ebtc.eu

42 ovErviEw of indian BioTEch MarkET associaTEd wiTh cliMaTE changE

3) Biosurfactants from Wastes: Two microorganisms have been isolated from oil-contaminated

soils by NEERI, Nagpur, which produce biosurfactants. It has also introduced a standard

and cost-effective technology for production of biosurfactants from low-cost substrates like

distillery and whey waste without any additional carbon source. It is an extremely

ecofriendly substitute for synthetic surfactants.

4) Bioscrubber for Removal of Odours from Industrial Emissions: Microbial cultures that can

degrade different odourants in industrial emissions have been isolated and characterised by

NEERI, Nagpur which biotransform odourants into secondary products or change them to

water and carbon dioxide. A pilot plant is being set up in Bhartiagram at M/s Jubilant

Organosys Ltd. (JOL). Details of patents filed or granted:

A total of 12 patents have been filed for the Department of Biotechnology supported

projects, their details are as follows:

o Four patents on biocatalyst preparation process in order to eliminate DDT residues

from soil and contaminated sites, industrial effluent, an increased DDT degradation,

and degradation of HCH by microbial formulation by CFTRI, Mysore.

o One Indian Patent filed by Centre for Biochemical Technology, Delhi (presently

known as IGBD) to improve the process for simultaneous biogas production mainly

containing methane and biofertiliser using high rate biomethanation of Palm Oil Mill

Effluent.

o Two Indian patents filed by IIT, Kharagpur on pollution-free gaseous fuel production

and developing a hydrogen production process with high rate and yield.

o One Indian patent filed by TERI, New Delhi on oil refinery waste biodegradation.

o Two Indian patents filed by NEERI, Nagpur on biosurfactant preparation process for

oil recovery and biosurfactant from distillery waste.

o One Indian patent by NEERI, Nagpur on a novel odour monitoring unit.

o One Indian patent filed by Visva Bharati University, Shantiniketan on biosensor for

detecting pesticide residues.

www.ebtc.eu EuropEan BusinEss and TEchnology cEnTrE

43ovErviEw of indian BioTEch MarkET associaTEd wiTh cliMaTE changE

2.3. Bio Energy (R & D) – 11th Five Year Plan It is proposed to take up focused R&D projects in the area of bio-energy resource identification and

biomass conversion to energy through combustion, pyrolysation, atmospheric and high pressure

gasification, plasma, bio-methanation and Biogas.

1. Bio-energy Resource

Resource Atlas for Bio-energy covering crop residues, forest residues, MSW, industrial wastes etc.

2. Biomass Conversion

a. Development of MW-scale fluidized bed biomass gasifiers, hot gas clean up system,

and optimum integration of the system.

b. Development of poly-generation facilities, gasifier systems based on charcoal /

pyrolysed biomass, and establishing the concept of a Bio-refinery.

c. Raising efficiency of atmospheric gasification to 25-30% along with cooling systems,

complete tar decomposition, and safe disposal of wastes in commercial production.

d. Raising system efficiency of small (upto 1 MW) combustion and turbine technologies

to 20% plus and laying down standards for various bio-energy components,

products, and systems.

e. Design and Development of high rate anaerobic co-digestion systems for biogas/

synthetic gas production, and of systems to couple with Stirling engine and turbines.

3. Bio-energy Utilisation

a. Design and development of equipment for waste segregation; engines, Stirling

engine and micro-turbine for biogas/ producer gas/ bio-syngas; direct gas-fired

absorptive chillers, driers, stoves, etc.; and improvement in biomass furnaces,

boilers etc. Development of driers for MSW and industrial wastes.

b. Improved design and development of processes/ de-watering device for drying of

digested slurry, and Pelletisation/ Briquetting technology for RDF.

c. Improving/ upgrading biogas and syngas quality.

EuropEan BusinEss and TEchnology cEnTrE www.ebtc.eu

44 ovErviEw of indian BioTEch MarkET associaTEd wiTh cliMaTE changE

4. Bio-Fuels

a. Develop technology for production of ethanol from sweet sorghum and sugar beet.

b. Developed technology for production of ethanol from ligno-cellulosic materials (rice

straw, etc.) and other agricultural and forestry residues.

c. Study petrol engine performance (using more than 10% blend of ethanol & petrol),

physico-chemical properties of potential non-edible oils for production of bio-diesel,

and undertaking engine modifications.

d. Developing bio/heterogeneous catalyst and chemical/catalyst conversion processes.

e. Alternate use of bio products, data generation & production of bio-diesel from all

possible feed-stocks.

f. Response of different available additives and their dosages on the bio-diesel.

g. Effect of bio-diesel on corrosion, stability, and engine modifications for using more

than 20% bio-diesel as blend with diesel.

h. Engine performance/ emissions based on different feed-stock based bio-diesels.

i. Toxicological studies and test to check adulteration and design and develop bio-liquid

fuel engines.

j. Development of second-generation bio-liquid fuels and related applications.

5. Bio-Gas

a. Studies in the field of micro-biology, bio-chemistry and engineering for increasing

the biogas yield by at least a factor of two, especially at low and high temperatures;

b. Reduction in the capital cost of biogas plants; development of materials and

techniques amenable for local level fabrication to reduce the time of installation;

c. Diversification of feed stocks to use alternate biomass wastes and cattle dung for

household biogas plants and sustained biogas production methods for winters.

d. Value added products using biogas slurry manure, development of biogas micro

turbines and engines, and cleaning and bottling of biogas;

e. Local power grids compatible with dual fuel engines and gas engines/turbines;

f. Corrosion-resistant paints and sealants for biogas plant components;

g. Portable biogas lantern and advanced bio-reactor techniques in institutional biogas

plants based on cattle dung for improving efficiency;

www.ebtc.eu EuropEan BusinEss and TEchnology cEnTrE

45ovErviEw of indian BioTEch MarkET associaTEd wiTh cliMaTE changE

h. Removal of hydrogen sulphide from biogas produced in Night-soil based biogas

plants, other treatment methods for effluent from Night-soil based biogas plants;

i. Field trials, demonstration of new models/ products, set design and appliances

standards/ specifications and on-site waste water treatment for small & medium

communities (500-5000 people).

2.4. Policy and programme: ‘India’s Biofuel Policy The National Policy on Biofuels was approved by the Government of India (GOI) on December 24,

2009. The biofuel policy promotes an increased use of renewable energy resources as alternate

fuels for transport fuels supplementation (diesel and gasoline for vehicles). It also suggests a

target of 20% biofuel blending (bio-ethanol and bio-diesel) by the year 2017.

At present, the government is finding it hard to implement the compulsory blending of 5% ethanol

in petrol (gasoline) due to the inadequate supply of sugar molasses in the year 2009/10 and

2008/09 due to the overall low production of sugarcane crop in India. As a consequence, India had

to import around 280 million liters of ethanol in CY 2009 to cope up with the increasing demand for