eastern europe and south caucasus initiative …

TRANSCRIPT

OECD

EASTERN EUROPE AND SOUTH CAUCASUS INITIATIVE

SETTING-UP THE CONDITIONS TO ESTABLISH A CREDIT GUARANTEE SCHEME FOR AGRIBUSINESS SMEs IN UKRAINE Phase I

Third Task Force meeting Task Force on a Credit Guarantee Scheme Kyiv, 10th February, 2015

CONFIDENTIAL – NOT FOR DISTRIBUTION

Key decisions of this Task Force meeting

1- Key directions

1. Initial approval of primary characteristics

I. Basic objectives and eligibility criteria II. Coverage rate III. Guarantee fees IV. Credit Guarantee Scheme type

2. Validate bank screening methodology

3. Approve proposal to limit tendering process to 2 or 3 banks

4. Approve funding mobilisation approach & nomination of CGS IG representative to coordinate 2 – Project management 1. Approve creation of CGS Implementation Group

2. Approve the project next steps and timeline

FOR APPROVAL

2

CONFIDENTIAL – NOT FOR DISTRIBUTION

1. Brief overview of the Project

2. Presentation of pre-feasibility study findings

(2.1) Presentation of results of pre-feasibility study

(2.2) Primary characteristics for the scheme

‒ Objectives & eligibility criteria ‒ Coverage rate ‒ Service fees ‒ Credit Guarantee Scheme type

(2.3) Bank selection methodology for the scheme

‒ Current banking system context for a CGS in Ukraine ‒ Introduction of bank partner screening methodology

3. Introduction of next phase: feasibility study & secondary characteristics

4. Next steps and timeline

3

Agenda

CONFIDENTIAL – NOT FOR DISTRIBUTION

The Credit Guarantee Scheme project emerged as a key recommendation of the SCS project, and is geared towards increasing access to finance for agri-SMEs in Ukraine

Aim 1: to increase access to finance for agribusiness SMEs Aim 2: to set up a scheme which is anchored to the local context & which is duplicable

4

(1) Brief project overview

CONFIDENTIAL – NOT FOR DISTRIBUTION

The project is in the diagnostic phase, & the pre-feasibility study has been completed

Phase I

1. Pre-feasibility study

Introduction to CGS & case studies

Best practices & lessons learnt

Primary characteristic recommendations

Presentation of partner-bank screening methodology

Identification of potential partner banks

2. Feasibility study • Recommendations on secondary

characteristics – Governance & management – Registration form – Type of guarantee – Leverage rate – Risk management approach – Loan duration – Bank interest rate reduction – Counter-guarantee

5

(1) Brief project overview

CONFIDENTIAL – NOT FOR DISTRIBUTION

Key directions for a credit guarantee scheme have already been approved

International donor-funded scheme

Farms 100-2000ha

Piloted in 4 Ukrainian regions

Ra

tio

na

le

< 100 ha: Too small for significant productivity improvements

> 2000ha: High average funding requirements, threat to sustainability

High agricultural productivity

Low bank loan rates to agriculture

Low state support to agriculture

Limited public funding

Technical complexity of CGS

Demonstration effect

Targeted SMEs

represent 26% of agribusiness SMEs in

Ukraine

Estimated credit of UAH 15bn required

IFIs & bilateral donors

Share

Funding gap

Source

TAR

GET

FU

ND

ING

6

(1) Brief project overview

CONFIDENTIAL – NOT FOR DISTRIBUTION

1. Brief overview of the Project

2. Presentation of pre-feasibility study findings

(2.1) Presentation of results of pre-feasibility study

(2.2) Primary characteristics for the scheme

‒ Objectives & eligibility criteria ‒ Coverage rate ‒ Service fees ‒ Credit Guarantee Scheme type

(2.3) Bank selection methodology for the scheme

‒ Current banking system context for a CGS in Ukraine ‒ Introduction of bank partner screening methodology

3. Introduction of next phase: feasibility study & secondary characteristics

4. Next steps and timeline

7

Agenda

CONFIDENTIAL – NOT FOR DISTRIBUTION

Based on the findings of the pre-feasibility study, several key recommendations have been made on the CGS’s primary characteristics & the selection of partner banks

P R I M A R Y C H A R A C T E R I S T I C S

Recommendation Suggested further analysis

Objectives & eligibility criteria

Scheme should achieve the objectives of financial & economic additionality &

sustainability whilst targeting agri-SMEs with 100-2000 ha of land in Cherkassy, Poltava,

Vinnytsia & Kharkiv.

• More detailed eligibility criteria required • Are there specific financing needs by

segment, which can be targeted whilst ensuring sustainability?

Coverage rate Scheme should provide 50-60% coverage

rate on average

• Should coverage rate be variable? • Is 50-60% acceptable to all banks which are

active in agribusiness SME lending?

Service fees Scheme should charge service fees of

around 2%, potentially upfront & annual • Are both upfront & annual fees required?

Type of CGS Scheme should be an internationally-funded

public/private model

• How would such a scheme be registered under Ukrainian legislation?

• Funds located in or outside Ukraine? • Is the legal & regulatory framework

compatible with features of the scheme?

B A N K S E L E C T I O N M E T H O D O L O G Y

Pre-screening Banks screened based on eligibility,

relevance & quality

Limited tender 2-3 banks out of 3-5 to initially participate

in the scheme • Tendering process best practices • Criteria for due diligence process

8

(2.1) Pre-feasibility study findings: results

CONFIDENTIAL – NOT FOR DISTRIBUTION

The methodology for developing these recommendations is based on country-specific conditions in Ukraine as well as OECD best practice

P R I M A R Y

B A N K S E L E C T I O N M E T H O D O L O G Y

OBJECTIVES & ELIGIBILITY

COVERAGE RATE TYPES OF FEES TYPE OF CGS

ELIGIBILITY

Define aims & target group

Define % of risk shared with lender

Define % of loan amount charged as service fee

Define broad organisational structure

for guarantee issue

Pre-feasibility study Pre-feasibility study Pre-feasibility study Pre-feasibility study

RELEVANCE QUALITY

Define which banks have sufficient capacity, interest & experience to participate

Define which banks can currently commit to active participation

Encourage self-selection & ensure that partner banks can meet the defined

objectives of the CGS

Questionnaire Questionnaire Questionnaire

9

(2.1) Pre-feasibility study findings: results

Pre-feasibility study

Questionnaire

Pre-feasibility study

Questionnaire

Feasibility study

Due diligence process

CONFIDENTIAL – NOT FOR DISTRIBUTION

These recommendations have been developed alongside an analysis of inherent & external project risks, in order to mitigate against them

Risks Mitigation Measures

Inherent

External

1. Technical complexity of CGS

2. Level of funding

3. Scheme buy-in from banks

4. Moral hazard

5. Lending technical capacity

1. Limited banking sector liquidity

2. Hryvnya depreciation

3. Legal & regulatory environment

1. Limited tendering process

2. Analysis to determine localisation & specificity of funds

3. In-depth legal assessment

1. CGS oversight working group; high-level political representative (high-level champion)

2. Donor mobilisation strategy

3. Attractiveness of risk-sharing; dialogue with banks

4. Careful scheme design; in-built evaluation mechanisms; oversight; capacity building

5. Bank screening; technical assistance (if funds)

10

(2.1) Pre-feasibility study findings: results

CONFIDENTIAL – NOT FOR DISTRIBUTION

1. Brief overview of the Project

2. Presentation of pre-feasibility study findings

(2.1) Presentation of results of pre-feasibility study

(2.2) Primary characteristics for the scheme

‒ Objectives & eligibility criteria ‒ Coverage rate ‒ Service fees ‒ Credit Guarantee Scheme type

(2.3) Bank selection methodology for the scheme

‒ Current banking system context for a CGS in Ukraine ‒ Introduction of bank partner screening methodology

3. Introduction of next phase: feasibility study & secondary characteristics

4. Next steps and timeline

11

Agenda

CONFIDENTIAL – NOT FOR DISTRIBUTION

In-line with OECD best practice, initial primary characteristics of the scheme have been defined to achieve the core objectives of a CGS – additionality & sustainability

Objectives of a CGS Description Method

Financial additionality

Increased access to finance for agri-SMEs (outreach & loan volume)

More appropriate risk assessment and client outreach is conducted by banks

Economic additionality

Improved production techniques and higher farm productivity

The targeted group accesses more appropriate/cheaper financing for working capital & investment

Sustainability The scheme covers its own costs (operating & otherwise), as it pursues the objectives of its mission

The CGS operates in-line with prudent risk management & best practice

COVERAGE RATE

TYPES OF FEES

TYPE OF CGS

ELIGIBILITY Credit Guarantee Schemes are usually targeted at SMEs (export-oriented, high-growth or rural). Best practice targets a segment of borrowers to ensure additionality, but is not overly-restrictive Coverage rates should reflect the tradeoff between attractiveness & moral hazard, i.e. sufficiently share credit risk whilst ensuring that banks still undertake adequate screening & monitoring processes. Several best-practice schemes link coverage rates to risk exposure, e.g. Chile provides 80% coverage for small borrowers & 50% coverage for medium borrowers

Fees should be high enough to cover administrative costs, whilst being low enough to ensure that the scheme is used. Best practice usually links fees to risk exposure

Most Credit Guarantee Schemes in OECD countries are public models. However since public schemes usually require annual budgetary appropriations, donor-funded models are often adopted in developing & emerging economies to secure funding

12

(2.2) Pre-feasibility study findings: primary characteristics

CONFIDENTIAL – NOT FOR DISTRIBUTION

The Ukrainian CGS will be targeted at a segment of agribusiness SMEs that are perceived to have high potential & sustainable financing costs

Objectives & eligibility

The aim is generally to increase loan access by lowering collateral requirements &/or interest rates for underfinanced firms

OECD: targeted at export-oriented, high-growth or rural SMEs. UKR: agribusiness SMEs with 100-2000ha of land, located in Cherkassy, Poltava, Kharkiv & Vinnytsia

Description Policy advice

Mission statement:

“The Ukrainian Agribusiness Guarantee Scheme is an independent credit guarantee instrument that aims to support agricultural SMEs in rural areas and is working under the regulation of the National Bank of

Ukraine. Its long term aim is to create a liquid credit market for bankable agribusiness SME projects that promote productivity growth in the sector.”

- approved at CGS Task Force meeting 1, June 2014

Eligibility criteria will further be defined with the results of the questionnaire, in-line with the 3 CGS objectives: financial additionality; economic additionality; & sustainability

13

(2.2) Pre-feasibility study findings: primary characteristics FOR DISCUSSION

Objectives & eligibility

CONFIDENTIAL – NOT FOR DISTRIBUTION

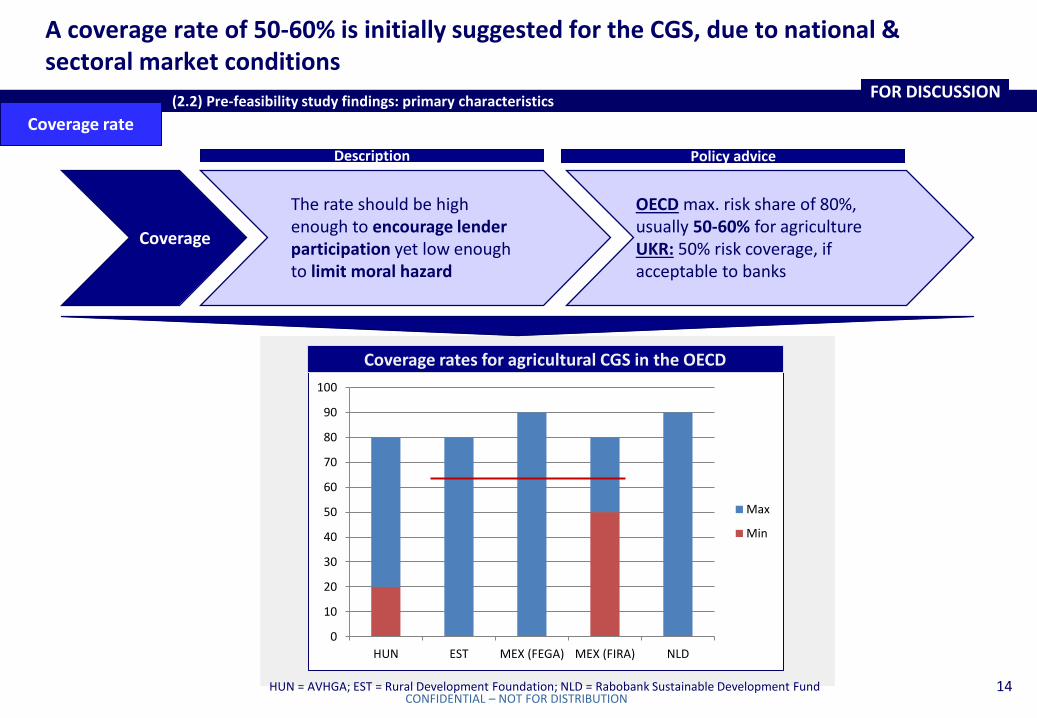

A coverage rate of 50-60% is initially suggested for the CGS, due to national & sectoral market conditions

Coverage

The rate should be high enough to encourage lender participation yet low enough to limit moral hazard

OECD max. risk share of 80%, usually 50-60% for agriculture UKR: 50% risk coverage, if acceptable to banks

0

10

20

30

40

50

60

70

80

90

100

HUN EST MEX (FEGA) MEX (FIRA) NLD

Max

Min

Coverage rates for agricultural CGS in the OECD

Description Policy advice

HUN = AVHGA; EST = Rural Development Foundation; NLD = Rabobank Sustainable Development Fund 14

(2.2) Pre-feasibility study findings: primary characteristics FOR DISCUSSION

Coverage rate

CONFIDENTIAL – NOT FOR DISTRIBUTION

Risk-adjusted upfront & annual fees of around 2% are initially recommended for the CGS; to be further defined in the feasibility study

Fees

OECD: fees are generally around 1-2% of the loan value, & are risk-adjusted UKR: guarantee fee of around 2%, paid by the bank

Fees should be high enough to cover administrative costs yet low enough to ensure adequate lender & borrower participation

Guarantee fees for agricultural CGS in the OECD

0

1

2

3

4

5

6

7

HUN EST MEX (FEGA) NLD

Max

Av

Min

HUN = AVHGA; EST = Rural Development Foundation; NLD = Rabobank Sustainable Development Fund

Risk-adjusted fees usually based on: • Coverage ratio • Borrower risk • Loan amount • Composition of

fund portfolio

To be further investigated in feasibility study

15

(2.2) Pre-feasibility study findings: primary characteristics FOR DISCUSSION

Description Policy advice

Service fees

CONFIDENTIAL – NOT FOR DISTRIBUTION

An internationally-funded & publically/privately-governed scheme is recommended as the most appropriate model type for Ukraine, based on the following assessment

PUBLIC

PRIVATE

PUBLIC/PRIVATE

INTERNATIONAL DONOR

1. Risk of failure due to limited PPP experience & low experience with CGS

2. Private operator needs to be selected. Needs to develop a strong selection methodology

1. Strong demonstration effect, if successful 2. Possible under existing regulatory environment 3. Highest level of operational efficiency 4. Can be easily sold/expanded, if viable

1. High price of capital, if investment is even possible

2. Commercial pressure (re ROI, etc.) will quickly shift CGS focus away from development goals

3. Requires sufficient capital & credibility

1. Allows for combination of mixed CGS funding (grant & commercial) with much-needed technical assistance & international know-how

2. Offers broad range of opportunities for future development (depending of IFIs & donors)

1. Chance of reduced ownership, if no private partner

2. Largely driven by policy goals, which may reduce commercial viability

1. No exit strategy possible — funds managed by Ukrainian government institution(s)

2. Annual budgetary commitment required for continuation

3. Limited replicability

PROS CONS

1. Ongoing Ukrainian government support after establishment

2. Regulation exists for organisational form 3. Full accountability with NBU

1. Positive aspects from both public & private models, if sufficient support from both sides

2. Highest likelihood of long-term sustainability

16

(2.2) Pre-feasibility study findings: primary characteristics FOR APPROVAL

CGS type

CONFIDENTIAL – NOT FOR DISTRIBUTION

Potential typology for a CGS: Private/public (international) model

17

CONFIDENTIAL – NOT FOR DISTRIBUTION

Potential typology for a CGS: Private/public (local) model

18

CONFIDENTIAL – NOT FOR DISTRIBUTION

1. Brief overview of the Project

2. Presentation of pre-feasibility study findings

(2.1) Presentation of results of pre-feasibility study

(2.2) Primary characteristics for the scheme

‒ Objectives & eligibility criteria ‒ Coverage rate ‒ Service fees ‒ Credit Guarantee Scheme type

(2.3) Bank selection methodology for the scheme

‒ Current banking system context for a CGS in Ukraine ‒ Introduction of bank partner screening methodology

3. Introduction of next phase: feasibility study & secondary characteristics

4. Next steps and timeline

19

Agenda

CONFIDENTIAL – NOT FOR DISTRIBUTION

A methodology for selecting partner banks has been developed, in order to limit the scheme’s risk exposure

Quality check Limited tender

3-5 Initial group of CGS

partner banks

Relevance check Pre-selection

7-10 Based on quantitative

questionnaires and qualitative interviews

Eligibility check Initial screening

17/43 Check based on positive

(e.g. history of sustainable agricultural

lending, presence in pilot regions) and

negative criteria (e.g. transparency & stability)

(2.3) Pre-feasibility study findings: bank selection methodology

20

CONFIDENTIAL – NOT FOR DISTRIBUTION

Agribusiness SMEs are facing important constraints in accessing credit due to the high conservatism of Ukrainian banks

CGS can increase credit to agribusiness SMEs by incentivising banks to increase lending

In Dec ‘14-Jan ’15 the NBU & the OECD distributed a questionnaire to 17 banks in Ukraine

Agricultural SMEs are perceived as risky

High collateral requirements

High interest rates

Cap on interest rate: no loan offer, even at a high interest rate

Loans provided to creditworthy SMEs

Banks are conservative

Lower interest rates

Lower collateral requirements

CG

S lo

wer

s ri

sk

This questionnaire will allow us to fine-tune various elements of the scheme

Eligibility criteria

Risk assessment processes

Lending volume to agricultural SMEs

Duration of loans to agricultural SMEs

Denominations of loans offered to agricultural SMEs

Purpose of loans provided to agricultural SMEs

Service fees / coverage rate Interest rates charged on loans to agricultural SMEs

NPL rates of loans to agricultural SMEs

21

(2.3) Pre-feasibility study findings: bank selection methodology

CONFIDENTIAL – NOT FOR DISTRIBUTION

The Ukrainian banking system is currently facing highly challenging conditions

Deposit outflows were extremely high in 2014

And loan quality deteriorated

-10

-5

0

5

10

15

20

Q1 '13 Q2 '13 Q3 '13 Q4 '13 Q1 '14 Q2 '14 Q3 '14

%

NPLs to total gross loans ROE

in UAH in USD in EUR in UAH in USD in EUR

-21,4% -38,4% -36,1% -2,4% -26,4% -13,8%Source: Forbes.ua

Funds of individuals Funds of legal entities

Deposit outflow from banks in Ukraine in 2014

Banks in Ukraine are strongly negatively affected by recent developments, such as:

• the strong depreciation of the hryvnya in combination with an emerging black market for foreign currency,

• the significant outflow of deposits from the banking system

Furthermore, massive restructurings are currently taking place, which are expected to result later in 2015 in very high NPL levels for the banking sector

Source: Forbes ua

22

Source: NBU

(2.3) Pre-feasibility study findings: bank selection methodology

CONFIDENTIAL – NOT FOR DISTRIBUTION

These conditions, combined with the structural nature of the banking system, have created high credit risk & liquidity constraints across the banking sector as a whole

To be successful in the current context, the CGS needs to carefully select partners banks

High costs of capital • Massive deposit outflows trigger higher

competition among banks which are offering high deposit rates

• Banks tend to be conservative • Few banks active on lending market

• Currency depreciation

• High rate of NPLs in banking sector

• Potentially high recapitalisation needs1

• Prospects for investors remain uncertain

• Further consolidation likely

Banks mainly finance existing customers

Increased administrative pressure on banks from NBU

1 Confirmed by NBU stress test of largest 40 banks

Current context Outcome

23

• Difficulty to find

investors

• Risk exposure must be under control

• Sound bank selection process required

Implications for CGS

(2.3) Pre-feasibility study findings: bank selection methodology

CONFIDENTIAL – NOT FOR DISTRIBUTION

In order to counter these risks, the CGS must control its risk exposure by screening & limiting the number of partner banks

Multi-stage selection process to identify solid partners for a CGS

Capacity, interest & experience to engage in agricultural

SME lending is limited

Bank selection process starts with initial

screening of around 40 banks that are known for

interest in SME &/or agricultural finance

– Conducted jointly with NBU

Due to uncertainty over the country’s economic prospects, a

limited no. of eligible banks may be able / willing to

mobilise funding

Country risks in Ukraine are high. Guarantee risk

exposure must be low

A relevance check will assess current capacities &

short-term strategy of pre-selected banks, as well

as interest in using a CGS

Final quality checks will allow for the final selection of

the most suitable partner banks & also serve

as basis for the application of a risk-based pricing model

1.

2.

3.

Country conditions Response in methodology

24

(2.3) Pre-feasibility study findings: bank selection methodology

CONFIDENTIAL – NOT FOR DISTRIBUTION

A bank selection methodology has been developed & applied to commercial banks in Ukraine, in collaboration with the NBU, in order to identify eligible partner banks

Positive criteria Negative criteria

1.

2.

3.

4.

5.

6.

7.

8.

Strategy • Includes a focus on SME finance

Activities • Already engages in agricultural finance

Products • Already has specific products for agricultural SMEs

Presence • Has a presence in the selected pilot regions

Relevance • Relevant agricultural portfolio size

Quality • Has developed quality indicators for agricultural lending

Standing with NBU • Has good standing with NBU & good market reputation

Recent portfolio developments • Promising trends in terms of growth, etc.

1 Eligibility check 43/17

Negative criteria

Concerns regarding integrity, transparency & stability Foreign state-ownership

1.

2.

25

(2.3) Pre-feasibility study findings: bank selection methodology FOR APPROVAL

CONFIDENTIAL – NOT FOR DISTRIBUTION

The second stage of the process will be to ensure that eligible banks are relevant for the scheme, given the current financial environment in Ukraine

2 Relevance check 17/10

1. Qualitative interviews with bank management Quantitative data gathering (through OECD/NBU questionnaire)

Assessment of interest in agricultural SME lending and participation in CGS, via:

2.

26

Progress 1. Interviews were conducted with

10 pre-selected banks in Nov ‘14, to get an overview of key issues & potential banking partners

2. Questionnaire distributed to around 17 banks in December 2014. It requests key indicators over time (e.g. loan volumes)

Next steps 1. Upon approval of bank selection

methodology, remaining interviews will be undertaken to discuss medium-term strategic plans & attitudes towards a CGS

2. Questionnaire results will be analysed in February 2015, in order to determine lending market characteristics for agri-SMEs by pre-screened banks

(2.3) Pre-feasibility study findings: bank selection methodology FOR APPROVAL

CONFIDENTIAL – NOT FOR DISTRIBUTION

Once eligible partners have been chosen, the scheme will be opened to 3-5 partner banks via a limited tendering process. Following this, final membership may be initially limited to 2-3 banks, given the current financial situation in Ukraine

Tendering process 1. Limited tender — only open to eligible & relevant banks 2. Transparent 3. Demanding

Annual review and tender renewal 1. Selection of add. partner banks 2. Monitoring / quality checks 3. Knowledge sharing 4. Review of pricing

Due diligence process Assessment of bank:

1. Policies 2. Procedures 3. Processes 4. Concrete lending results 5. Future targets

Technical support to be provided by NBU or international experts

The quality assessment will also provide information for the application of a risk-based pricing model.

3 Quality check 3-5

27

(2.3) Pre-feasibility study findings: bank selection methodology FOR APPROVAL

CONFIDENTIAL – NOT FOR DISTRIBUTION

In conclusion, the OECD suggests approval of the following primary characteristics for a Credit Guarantee Scheme in Ukraine

P R I M A R Y C H A R A C T E R I S T I C S

Recommendation Suggested further analysis

Objectives & eligibility criteria

Scheme should achieve the objectives of financial & economic additionality &

sustainability whilst targeting agri-SMEs with 100-2000 ha of land in Cherkassy, Poltava,

Vinnytsia & Kharkiv.

• More detailed eligibility criteria required • Are there specific financing needs by

segment, which can be targeted whilst ensuring sustainability?

Coverage rate Scheme should provide 50-60% coverage

rate on average

• Should coverage rate be variable? • Is 50-60% acceptable to all banks which are

active in agribusiness SME lending?

Service fees Scheme should charge service fees of

around 2%, potentially upfront & annual • Are both upfront & annual fees required?

Type of CGS Scheme should be an internationally-funded

public/private model

• How would such a scheme be registered under Ukrainian legislation?

• Funds located in or outside Ukraine? • Is the legal & regulatory framework

compatible with features of the scheme?

B A N K S E L E C T I O N M E T H O D O L O G Y

Pre-screening Banks screened based on eligibility,

relevance & quality

Limited tender 2-3 banks out of 3-5 to initially participate

in the scheme • Tendering process best practices • Criteria for due diligence process

28

(2.1) Pre-feasibility study findings: results FOR APPROVAL REMINDER

CONFIDENTIAL – NOT FOR DISTRIBUTION

1. Brief overview of the Project

2. Presentation of pre-feasibility study findings

(2.1) Presentation of results of pre-feasibility study

(2.2) Primary characteristics for the scheme

‒ Objectives & eligibility criteria ‒ Coverage rate ‒ Service fees ‒ Credit Guarantee Scheme type

(2.3) Bank selection methodology for the scheme

‒ Current banking system context for a CGS in Ukraine ‒ Introduction of bank partner screening methodology

3. Introduction of next phase: feasibility study & secondary characteristics

4. Next steps and timeline

29

Agenda

CONFIDENTIAL – NOT FOR DISTRIBUTION

During the next phase of the project we will make recommendations on secondary characteristics for the scheme

P R I M A R Y

S E C O N D A R Y

GOVERNANCE MANAGEMENT REGISTRATION FUNDING RISK

MANAGEMENT TYPE OF

GUARANTEE

Define strategic governance of the

scheme & ownership

Define operational management

structures

Define legal & regulatory framework

Define funding source & fund

location

Define procedures for overseeing & mitigating risks

Define how guarantees are

extended

Feasibility study Feasibility study Legal consultation Questionnaire Questionnaire Questionnaire

Feasibility study Feasibility study Feasibility study Feasibility study

30

(3) Introduction of next phase: feasibility study

CONFIDENTIAL – NOT FOR DISTRIBUTION

1. Brief overview of the Project

2. Presentation of pre-feasibility study findings

(2.1) Presentation of results of pre-feasibility study

(2.2) Primary characteristics for the scheme

‒ Objectives & eligibility criteria ‒ Coverage rate ‒ Service fees ‒ Credit Guarantee Scheme type

(2.3) Bank selection methodology for the scheme

‒ Current banking system context for a CGS in Ukraine ‒ Introduction of bank partner screening methodology

3. Introduction of next phase: feasibility study & secondary characteristics

4. Next steps and timeline

31

Agenda

CONFIDENTIAL – NOT FOR DISTRIBUTION

The OECD recommends the establishment of a CGS implementation group

Governmental “CGS Implementation Group”

Composition Tasks Timeframe

Based on expertise & seniority, 1 member from

• MoF

• NBU

• MoE

• MoA

Discussions on selection of members during: • February 2015 To be established by: • Early March 2015

• Suggest strategic direction

• Engage with donors (one focal point)

• Engage with team managing the scheme

32

(4) Next steps & timeline FOR APPROVAL

… with support from OECD

CONFIDENTIAL – NOT FOR DISTRIBUTION

There is a need to approach potential donors, to determine interest & availability of funding, in collaboration with a representative from the MoF or MoE

Suggested list of potential multilateral donors Suggested list of potential bilateral donors

EBRD

IFC

World Bank

Sweden

Germany

UK

UKR legislation

Financing gap

Requisite start-up capital for financial services in Ukraine: ₴3m

The OECD (2012) estimated the financing gap in pilot regions at ₴ 15bn. At a leverage rate of 5x, ₴3bn required

EIB / EIF

EU

France

US

Administrative costs should be covered by guarantee fees; but start-up capital should initially come from international donors

The OECD recommends that these discussions are led with the MoF/MoE representative from the CGS implementation group

33

(4) Next steps & timeline

Max

Min

CONFIDENTIAL – NOT FOR DISTRIBUTION

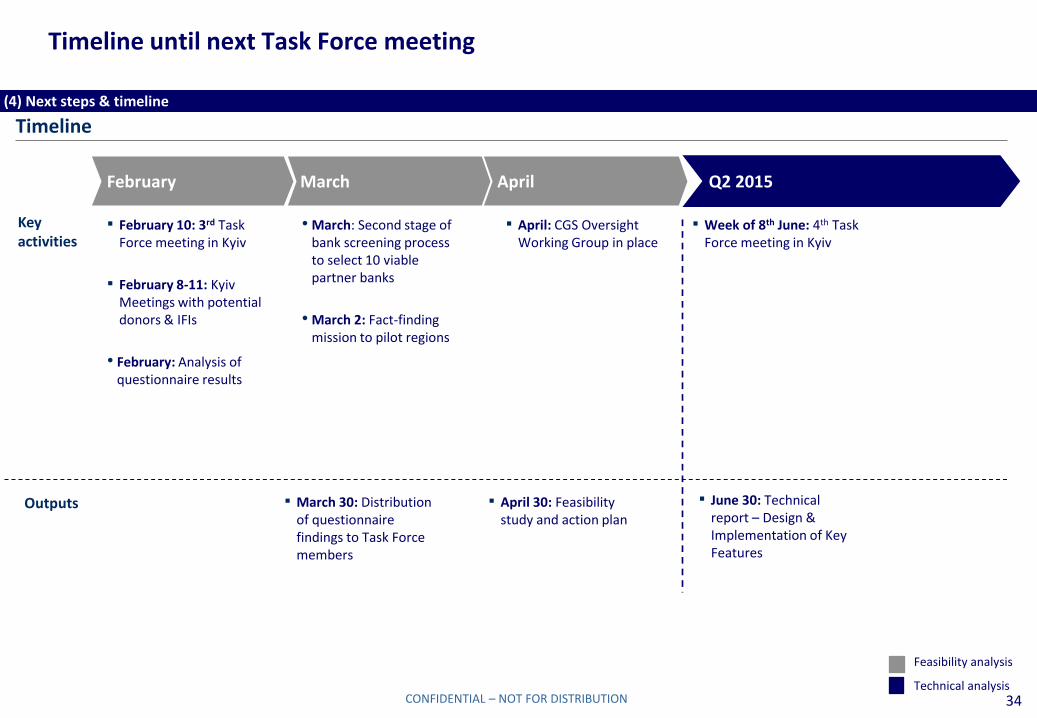

Timeline until next Task Force meeting

Timeline

February March April Q2 2015

Key activities

Outputs ▪ April 30: Feasibility study and action plan

▪ June 30: Technical report – Design & Implementation of Key Features

▪ February 10: 3rd Task Force meeting in Kyiv

▪ February 8-11: Kyiv Meetings with potential donors & IFIs

• February: Analysis of questionnaire results

• March: Second stage of bank screening process to select 10 viable partner banks

• March 2: Fact-finding mission to pilot regions

Feasibility analysis

Technical analysis 34

▪ March 30: Distribution of questionnaire findings to Task Force members

▪ April: CGS Oversight Working Group in place

(4) Next steps & timeline

▪ Week of 8th June: 4th Task Force meeting in Kyiv

CONFIDENTIAL – NOT FOR DISTRIBUTION

Key decisions of this Task Force meeting

1- Key directions

1. Initial approval of primary characteristics

I. Basic objectives and eligibility criteria II. Coverage rate III. Guarantee fees IV. Credit Guarantee Scheme type

2. Validate bank screening methodology

3. Approve proposal to limit tendering process to 2 or 3 banks

4. Approve funding mobilisation approach & nomination of CGS IG representative to coordinate 2 – Project management 1. Approve creation of CGS Implementation Group

2. Approve the project next steps and timeline

FOR APPROVAL

35

TF Proposals to be submitted to the

OECD-Ukraine Co-ordination Council

CONFIDENTIAL – NOT FOR DISTRIBUTION

ORGANISATION FOR ECONOMIC CO-OPERATION AND DEVELOPMENT

Antonio Somma Head of Programme OECD Eurasia Competitiveness Programme Tel: + 33 1 45 24 93 90 Email: [email protected]

Contact details

Gabriela Miranda Project Manager Ukraine OECD Eurasia Competitiveness Programme Tel: + 33 1 45 24 95 01 Email: [email protected]

Annie Norfolk Beadle Policy Analyst OECD Eurasia Competitiveness Programme Tel: + 33 1 85 55 64 01 Email: [email protected]

Audrey Vergnes Project Coordinator OECD Eurasia Competitiveness Programme Tel: + 33 1 85 55 64 13 Email: [email protected]

36