earthquake microinsurance for …icrm.ntu.edu.sg/newsnevents/doc/mirt_froums/documents...kornelius...

TRANSCRIPT

Kornelius Simanjuntak

General Insurance Association of IndonesiaApril 2011

1

EARTHQUAKE MICROINSURANCE FOR INDONESIA

Earthquake Risk in Indonesia

2

World’s and Indonesia’s EarthquakeEpicenter Map for Earthquake withMagnitude > 5.5 (1964 – 2010)

Almost 20% of Damageable andtsunamigenic Earthquake Occurred inIndonesia.

Earthquake occurrences in Indonesia formagnitude more than 5,0.

Overall, it is rising in number since year of2000.

Histogram: Number of Earthquake in Indonesia from 1965 to April 2009.

EARTHQUAKE HAZARD IN INDONESIA

ECONOMIC LOSSES AND HUMAN CASUALTIES DUE TO EARTHQUAKE 2004 – 2010

Huge losses …… Unprepared communities !!

EVENT DATE PROVINCE MAG. DEATH TOLL

DAMAGED HOUSES

ECONOMIC LOSSES

(Billion IDR)

INSURED LOSSES

(Billion IDR)

Letusan Gunung Merapi 25/10 and 05/11/10 Yogyakarta - 275 2,200 7,300 TBA

Gempa & Tsunami Mentawai 25/11/10 Sumatera Barat 7.7 450 720 NA TBA

Gempa Papua 16/6/10 Papua 7,1 17 3,422 800 16.85

Gempa Aceh 7/4/2010 Aceh 7,2 (USGS 7.7) - Hundreds NA 0.57

Gempa Jambi 1/10/2009 Jambi 7 N.A N.A N.A 0.26

Gempa Padang 30/9/2009 Sumatera Barat 7,6 1,117 279,472 23,000 1,475.59

Gempa Tasikmalaya 2/9/2009 Jawa Barat 7,3 81 225,051 8,790 45.81

Gempa Talaud 11/2/2009 Sulawesi Utara 7,2 1 1,400 NA 0.05

Gempa Manokwari 4/1/2009 Papua Barat 7,6 4 6,200 300 4.94

Gempa Gorontalo 17/11/2008 Gorontalo 7.3 4 2,300 400 0.69

Gempa Sumbawa 7/8/2008 Nusa Tenggara Barat 6,6 - 1,000 NA 7.14

Gempa Bengkulu 12 and 13/09/2007 Bengkulu 8,4 dan 7,9 25 59,000 1,500 55.21

Gempa Padang 6/3/2007 Sumatera Barat 6,2 68 43,000 1,470 38.08 Gempa & TsumaniPangandaran 17/7/2006 Jawa Barat 6,8 683 2,500 550 2.43

Gempa Yogyakarta 27/5/2006 Yogyakarta 5,9 5,716 414,000 31,000 325.37

Gempa dan tsunami Aceh 26/12/2004 Aceh 9,3 220,000 120,000 45,000 629.31

Source : BNPB, Bappenas, Media, World Bank, UNDP, MAIPARK

POST-DISASTER SPENDING 2001 - 2007

SOURCE: MINISTRY OF FINANCE, REPUBLIC OF INDONESIA

-

200

400

600

800

1,000

1,200

1,400

2001 2002 2004 2005 2006 2007

67 4 15

176

1,278

1,112

In Million USD

PRE-DISASTER SPENDING 2001-2007

-

50

100

150

200

250

300

2001 2002 2004 2005 2006 2007

62

97 114

136

232

262

SOURCE: MINISTRY OF FINANCE , REPUBLIC OF INDONESIA

In Million USD

8

The increasing tendency of government spending in pre- and post-disaster reliefalready create heavy burden to the state

budget.

It is therefore imperative that Indonesia should be able to perform more efficiently in

risk management performances.

Until now, all responsibility to finance the rehab-recon is in the Government

Society of all level should be made eager to prepare themselves against disaster

9

Microinsurance as a tool for homeowners and even the low

income to protect themselves against disaster risk

Insurance through its risk transfer mechanism provide a better alternative in disaster risk

financing

10

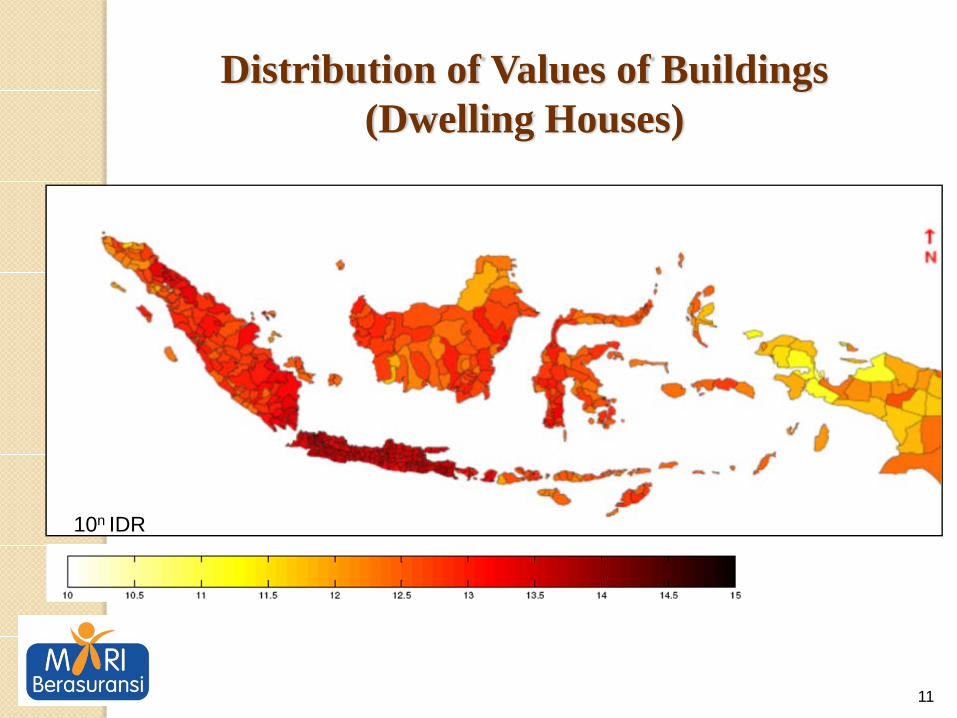

Indonesia Insurance Exposure 2008

Source : PT Asuransi MAIPARK Indonesia

11

Distribution of Values of Buildings(Dwelling Houses)

10n IDR

12

Value of Indonesia BuildingOverlayed with EQ events (1599 – Present)

Shallow EQIntermediate EQDeep EQ

10n IDR

Insurance penetration 2% of GDPInsurance bureau of Indonesia (2010)

13

Only 1,2% of Insured properties have EQ cover

PT. Asuransi MAIPARK Indonesia (2008 – 2010)

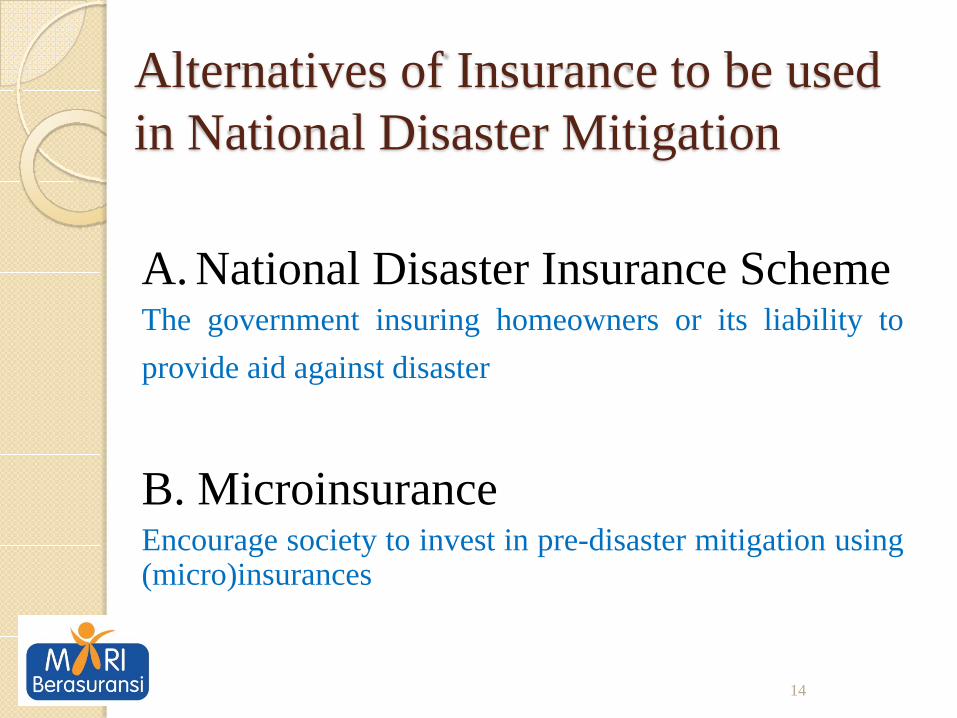

Alternatives of Insurance to be used in National Disaster Mitigation

14

A. National Disaster Insurance SchemeThe government insuring homeowners or its liability toprovide aid against disaster

B. MicroinsuranceEncourage society to invest in pre-disaster mitigation using(micro)insurances

15

A. National Disaster Insurance Scheme

16

A. National Disaster InsuranceScheme; Earthquake

- Government work together with InsuranceIndustry (PPP)

- Providing insurance cover for allhomeowners/householders in the country (orselected areas)

- Protection for state budget

NATIONAL EARTHQUAKE INSURANCE SCHEME

Features of Required Earthquake Insurance Scheme:

◦ The crux of the matter:Quick response to asses the damage (within two weeks after the area is “declared” accessible)Quick claims payment (two weeks after assessment)

• Deployment of nation wide insurance network necessary

• Strong local and international capacity needed

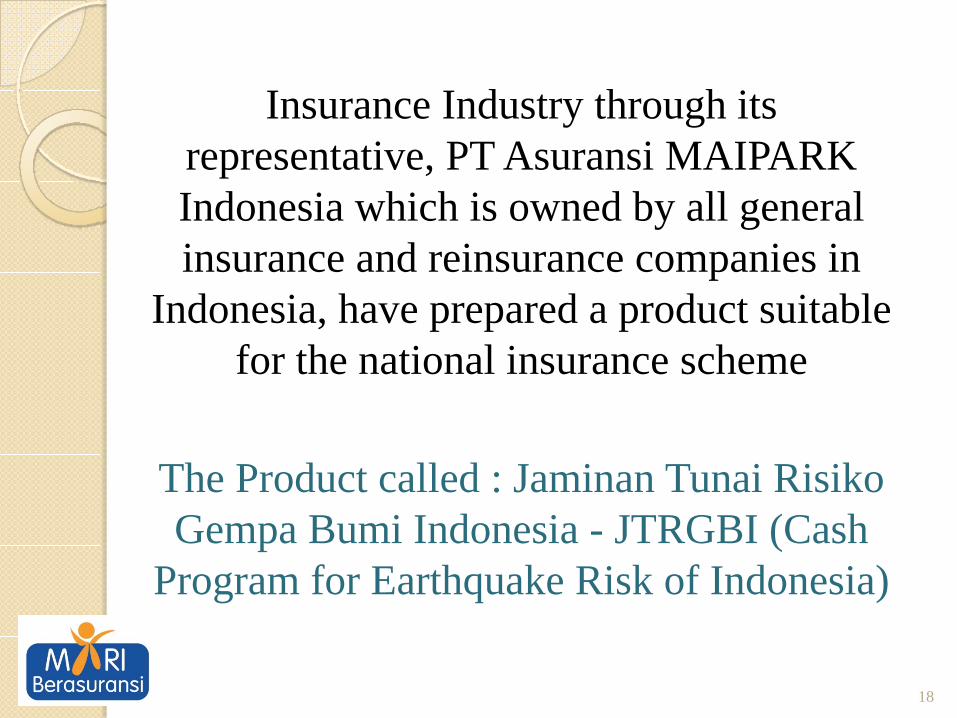

Insurance Industry through its representative, PT Asuransi MAIPARK Indonesia which is owned by all general insurance and reinsurance companies in

Indonesia, have prepared a product suitable for the national insurance scheme

The Product called : Jaminan Tunai RisikoGempa Bumi Indonesia - JTRGBI (Cash

Program for Earthquake Risk of Indonesia)

18

19

JAMINAN TUNAI RISIKO GEMPA BUMI INDONESIA (JTRGBI)

The Insured = The Government (central and/or local Government)

Insurer = General Insurance Industry represented by MAIPARK

JTRGBI low cost, simple administration, quick claim payment

20

Risks Covered :• Earthquake• Volcanic Eruption• Tsunami• Fire Following Earthquake

Insurable Property :All tax-registered dwelling houses in therelated administrative area

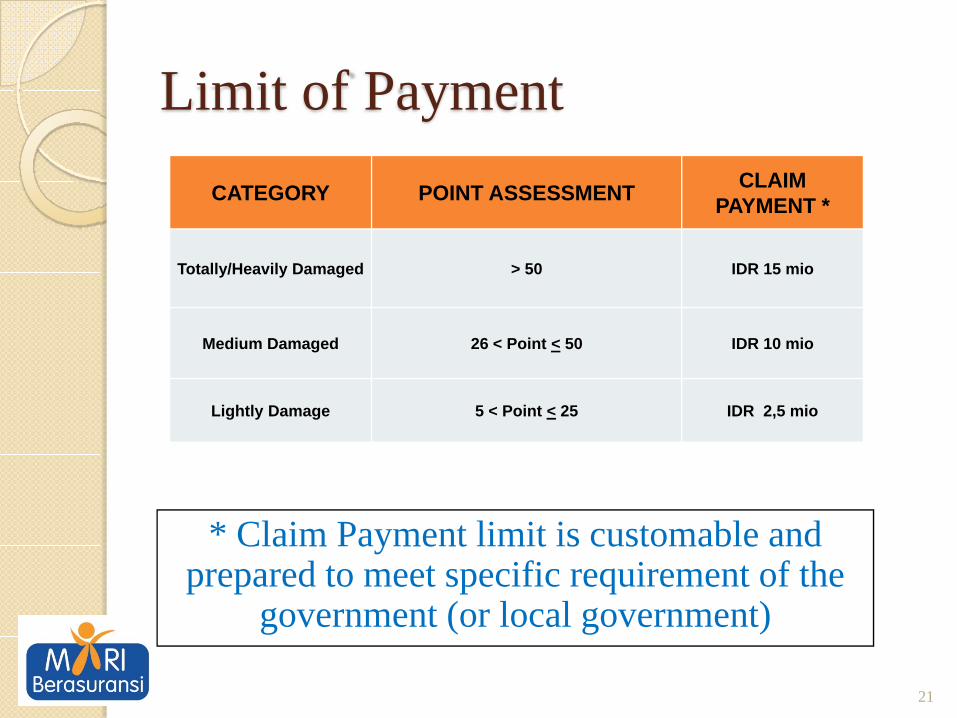

Limit of PaymentCATEGORY POINT ASSESSMENT CLAIM

PAYMENT *

Totally/Heavily Damaged > 50 IDR 15 mio

Medium Damaged 26 < Point < 50 IDR 10 mio

Lightly Damage 5 < Point < 25 IDR 2,5 mio

21

* Claim Payment limit is customable and prepared to meet specific requirement of the

government (or local government)

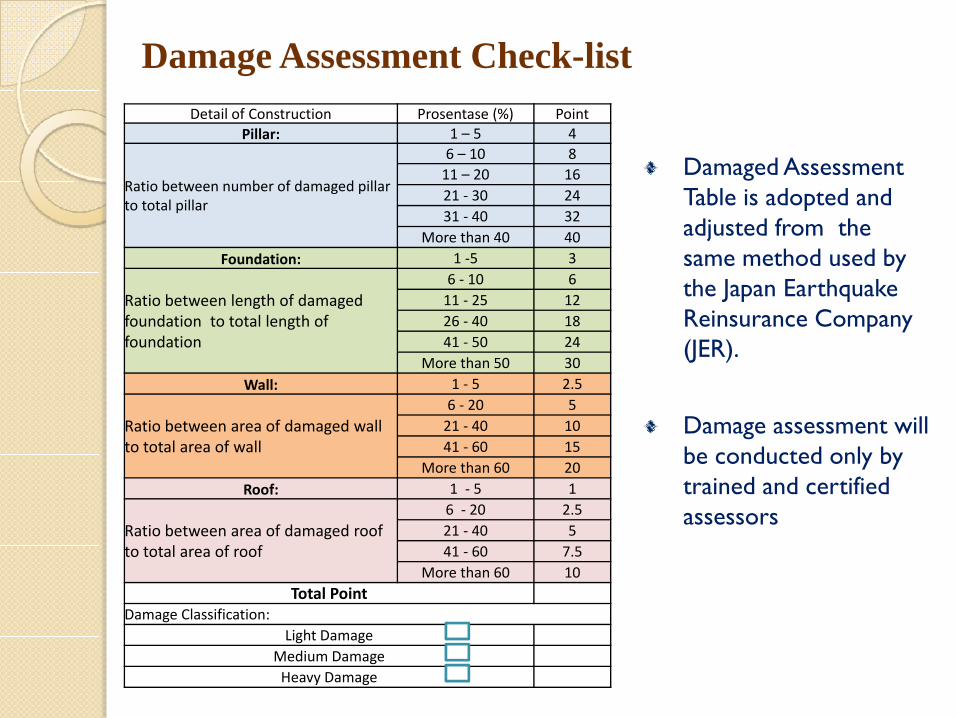

Detail of Construction Prosentase (%) PointPillar: 1 – 5 4

Ratio between number of damaged pillar to total pillar

6 – 10 811 – 20 1621 ‐ 30 2431 ‐ 40 32

More than 40 40Foundation: 1 ‐5 3

Ratio between length of damaged foundation to total length of foundation

6 ‐ 10 611 ‐ 25 1226 ‐ 40 1841 ‐ 50 24

More than 50 30Wall: 1 ‐ 5 2.5

Ratio between area of damaged wall to total area of wall

6 ‐ 20 521 ‐ 40 1041 ‐ 60 15

More than 60 20Roof: 1 ‐ 5 1

Ratio between area of damaged roof to total area of roof

6 ‐ 20 2.521 ‐ 40 541 ‐ 60 7.5

More than 60 10Total Point

Damage Classification:Light Damage

Medium DamageHeavy Damage

Damaged Assessment Table is adopted and adjusted from the same method used by the Japan Earthquake Reinsurance Company (JER).

Damage assessment will be conducted only by trained and certified assessors

Damage Assessment Check-list

Alternative of Claim Payout Basis

1. Indemnity Basis2. Parametric Insurance Method

23

24

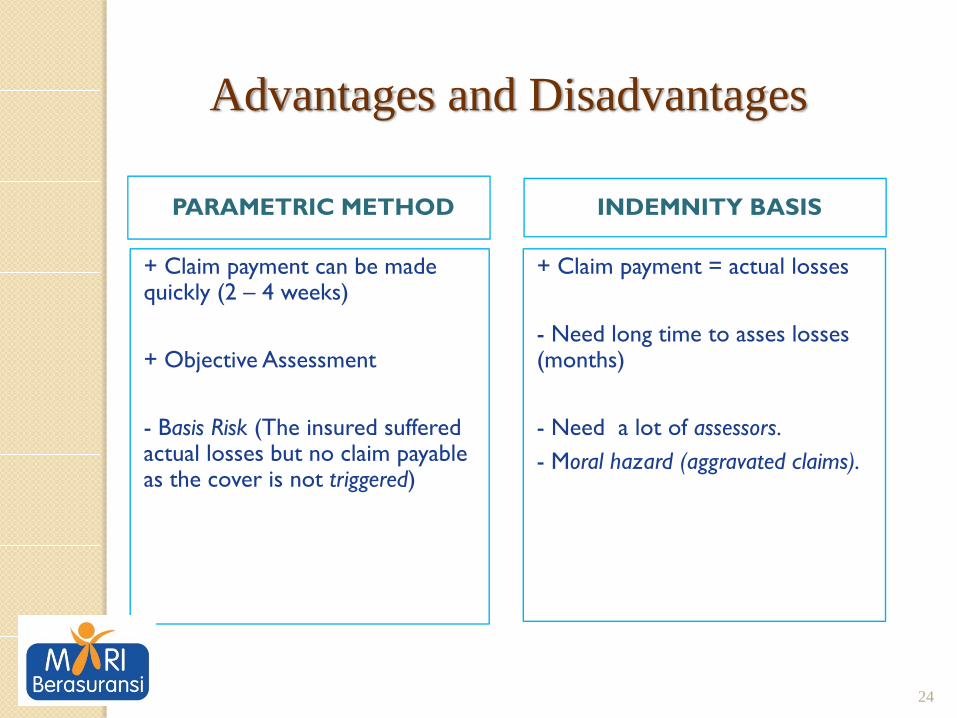

+ Claim payment = actual losses

- Need long time to asses losses (months)

- Need a lot of assessors.- Moral hazard (aggravated claims).

Advantages and Disadvantages

INDEMNITY BASIS

+ Claim payment can be made quickly (2 – 4 weeks)

+ Objective Assessment

- Basis Risk (The insured suffered actual losses but no claim payable as the cover is not triggered)

PARAMETRIC METHOD

25

JTRGBI; Loss Assessment

Satellite Imagery and/or Cat Model calculation of first/Interim payment

Quick Assessment by certified assessors calculation of final claim payment

Bantul EQ 2006 - Before Bantul EQ 2006 - After

Satellite Imagery Assessment

CATASTROPHE MODEL

=EARTHQUAKE LOSS

SIMULATOR

Loss Assessment Using Cat. Model

28

Survey Gempa Bengkulu 12 September 2007

Loss Assessment through Field Survey

29

Claim Payment

Combined method allows insurer to make very quick claimpayment

First/Interim payment will be available within 3 weeks afterdisaster. The calculation based on satellite imagery and Cat.Modeling

Final calculation of claim will be based on field lossassessment by certified assessors, and claim will be payablewithin 3 months after the disaster affected area declared tobe accessible

30

Claim Payment

Claim payment will be addressed to the Government as the insured

Claim payment received by the Government distributed to the victims as cash aid for rehabilitation and reconstruction program

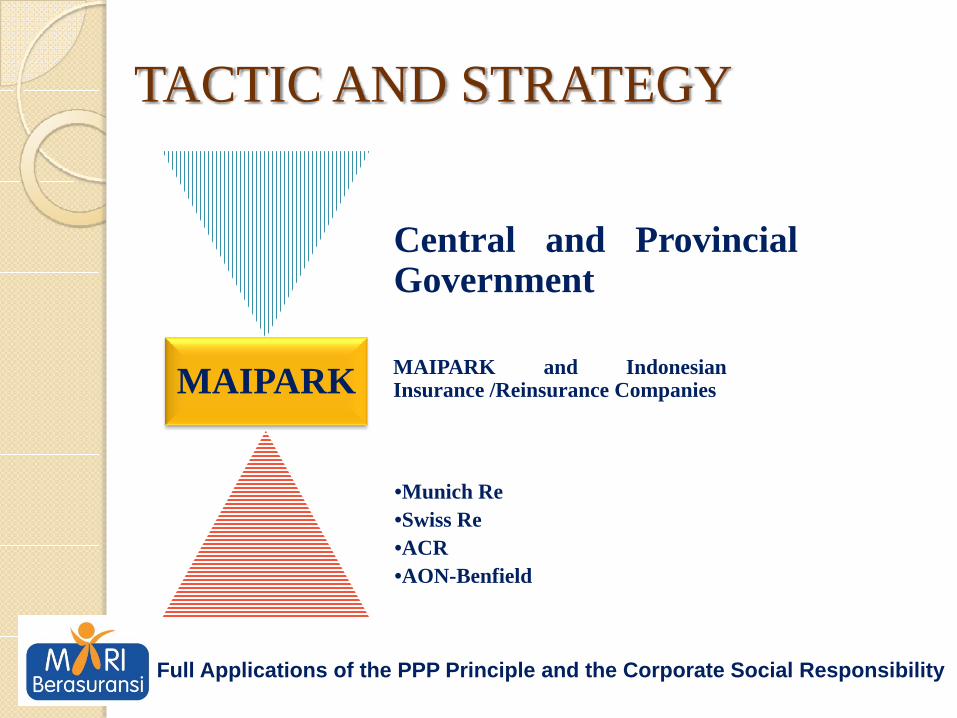

MAIPARK

Central and ProvincialGovernment

MAIPARK and IndonesianInsurance /Reinsurance Companies

•Munich Re•Swiss Re•ACR•AON-Benfield

A Full Applications of the PPP Principle and the Corporate Social Responsibility

TACTIC AND STRATEGY

PROGRESSMAIPARK has been in involved in discussions on DwellingHouse Earthquake Insurance Scheme between Government,World Bank and Asian Development Bank since severalyears ago.

Earthquake Insurance Scheme on dwelling houses has beenintensively discussed between Indonesia General InsuranceAssociation (AAUI) and National Agency for DisasterManagement - BNPB (since 2007)

The implementation of EQ insurance scheme was delayeddue to the Government lack of legal basis to use statebudget to buy commercial insurance

PROGRESS …………….… continued

At this time, MAIPARK and AAUI are having intensivediscussions with the Ministry of Finance to prepare aCatastrophe Insurance Scheme to protect state budgetholistically and integratedly (not only dwelling houses)

MAIPARK cooperates with AONBenfield, Munich Re, andSwiss Re to prepare the scheme.

34

B. Microinsurance

35

Microinsurance is insurance characterized by :

low premium and affordable insurance productslow caps or low coverage limits, as a basiccoversold as part of atypical risk-pooling andmarketing arrangementsdesigned to service low-income people andbusinesses not served by typical social orcommercial insurance schemes.

What risks are they concerned about?Country Priority risk

Uganda Illness, death, disability, property loss, risk of loanMalawi Death, food insecurity, illness, educationPhilippines Death, old age, illnessViet Nam Illness, natural disaster, accidents, livestock diseaseIndonesia Illness, children’s education, poor harvestLao P.D.R. Illness, livestock disease, deathGeorgia Illness, business losses, theft, death, retirement income

Ukraine Illness, disability, theftBolivia Illness, death, property loss (including crop loss in rural

areas)Adapted from Cohen and Sebstad (2006)

Disaster risk is not on their priority !!

37

AvailableAffordableAcceptableSustainable for insuring agency

Required feature of Microinsurance

38

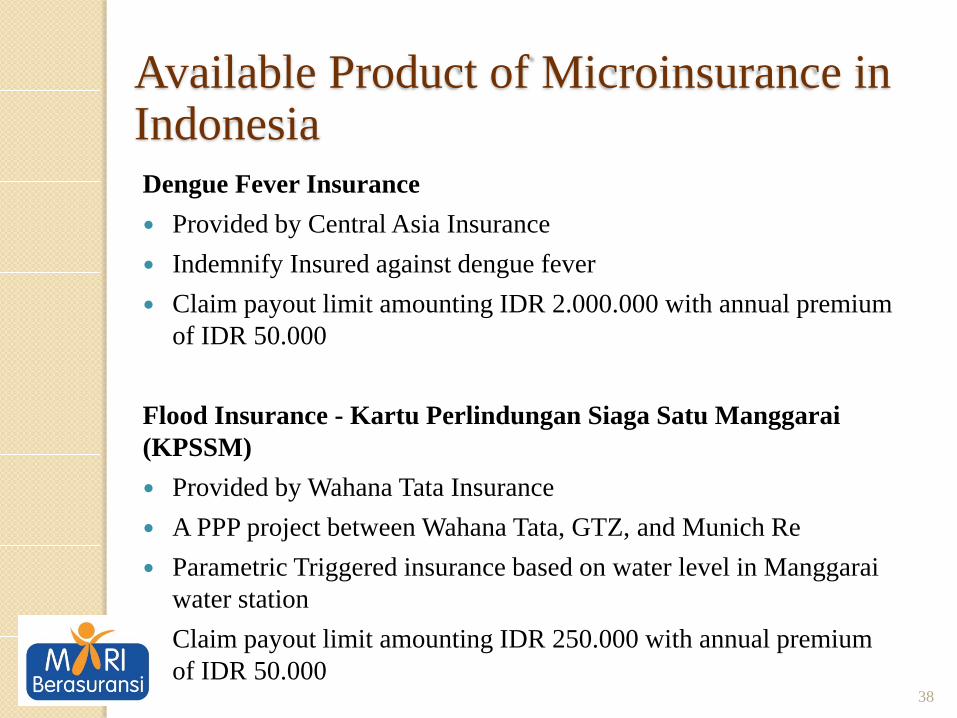

Available Product of Microinsurance in IndonesiaDengue Fever Insurance

Provided by Central Asia InsuranceIndemnify Insured against dengue feverClaim payout limit amounting IDR 2.000.000 with annual premium of IDR 50.000

Flood Insurance - Kartu Perlindungan Siaga Satu Manggarai(KPSSM)

Provided by Wahana Tata InsuranceA PPP project between Wahana Tata, GTZ, and Munich ReParametric Triggered insurance based on water level in Manggaraiwater stationClaim payout limit amounting IDR 250.000 with annual premium of IDR 50.000

39

EQ Microinsurance – New Product

A new Earthquake Insurance Product is being developed. Targeting low income societyAs a basic insurance cover for the low-income society

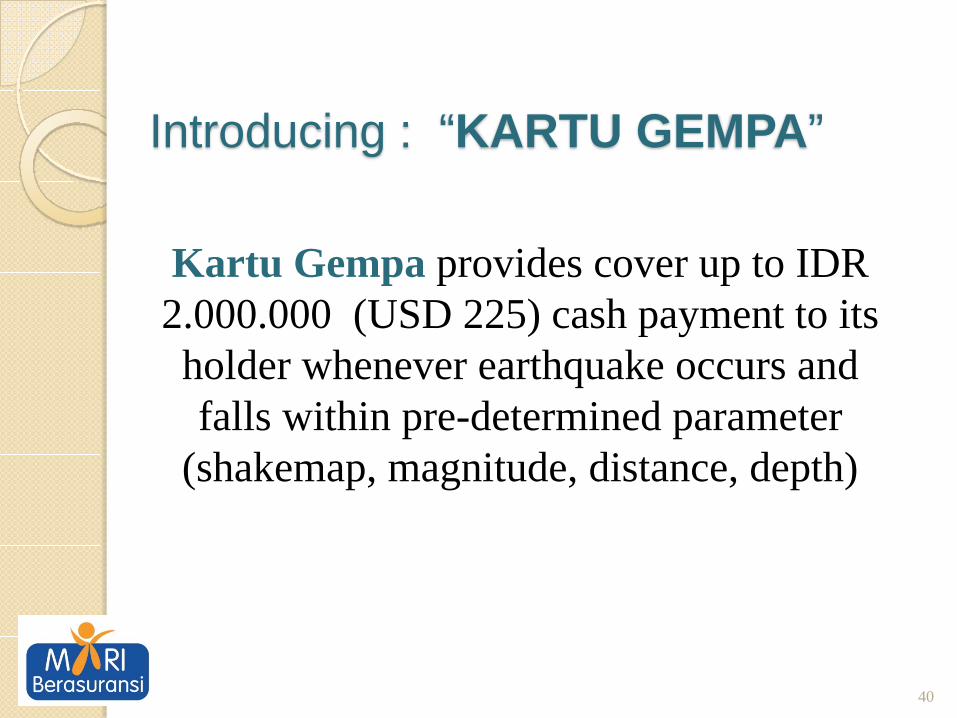

Introducing : “KARTU GEMPA”

Kartu Gempa provides cover up to IDR 2.000.000 (USD 225) cash payment to its holder whenever earthquake occurs and falls within pre-determined parameter

(shakemap, magnitude, distance, depth)

40

Introducing : “KARTU GEMPA”

41

The InsuredHome owners/householders

CoverageEarthquake (EQ)

Triggering parameter (shakemap, magnitude, distance, depth) is still under research

Product Specification “KARTU GEMPA”

PremiumRetail price for a voucher of KARTU GEMPA is +/- IDR 100.000 (USD 11) …. Fix price is still under researchCover effective for one year periodHomeowner is allowed to have max 5 units KARTU GEMPA

42

Cash payment of IDR 2.000.000 (USD 225) per KARTU GEMPABenefit will be paid if an earthquake occurs and reach the triggering parameterPre-determined Parametric Trigger Max benefit per homeowner is IDR 10.000.000)

43

Benefit

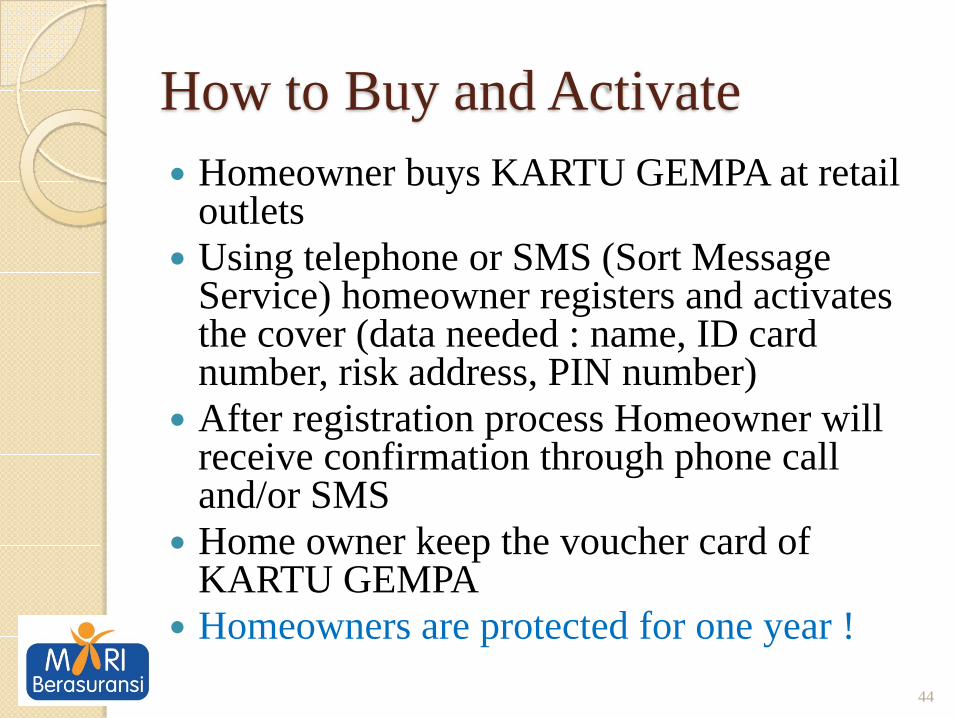

How to Buy and Activate Homeowner buys KARTU GEMPA at retail outletsUsing telephone or SMS (Sort Message Service) homeowner registers and activates the cover (data needed : name, ID card number, risk address, PIN number)After registration process Homeowner will receive confirmation through phone call and/or SMSHome owner keep the voucher card of KARTU GEMPA Homeowners are protected for one year !

44

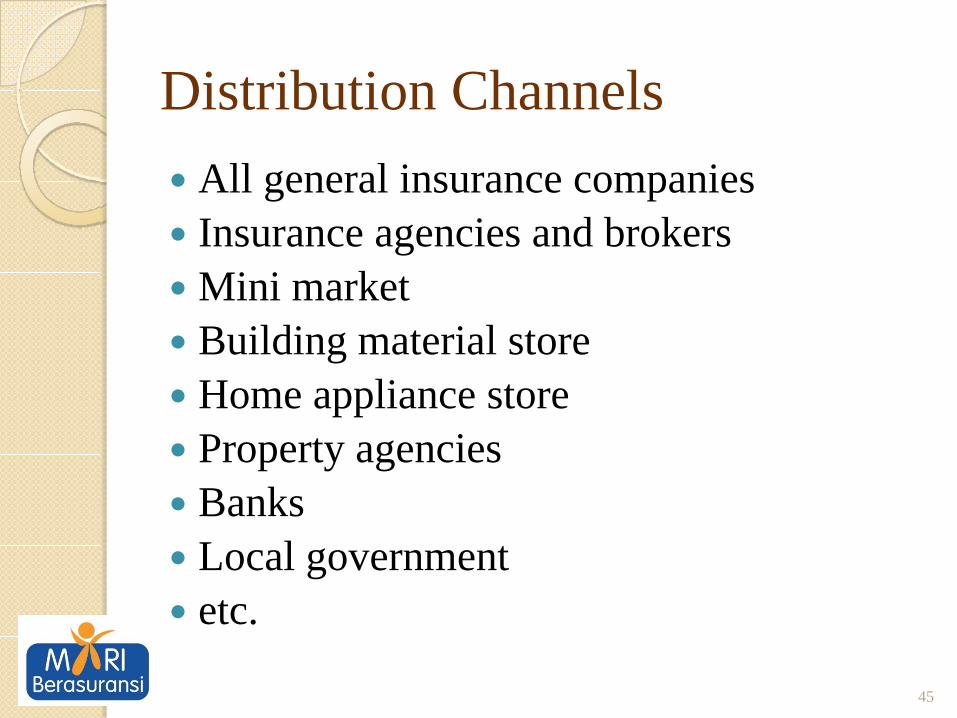

Distribution ChannelsAll general insurance companiesInsurance agencies and brokersMini marketBuilding material storeHome appliance storeProperty agenciesBanksLocal governmentetc.

45

Claim PaymentCash payment will be paid If an earthquake occur and hit the triggering parameter (based on official report from USGS and/or BMKG – Meteorological, Climatological and Geophysical Agency of Indonesia)Homeowner notifies insurance company through phone call and/or SMS, or otherwise Insurance company will inform homeowner when claim is payable due to an earthquakePayment will be made within 2 weeks after disaster

46

TERIMA KASIHTHANK YOU

47