earnings management in thailand: effects on … · earnings management, financial reporting...

TRANSCRIPT

EARNINGS MANAGEMENT IN THAILAND: EFFECTS ON FINANCIAL REPORTING RELIABILITY, STAKEHOLDER ACCEPTANCE AND CORPORATE TRANSPARENCY

Phaithun Intakhan, Mahasarakham University, Thailand

Phapruke Ussahawanitchakit, Mahasarakham University, Thailand

ABSTRACT

The objective of this paper is to examine the effects of earnings management on corporate transparency of Thai-Listed Company via financial reporting reliability and stakeholder acceptance as mediator also social-minded awareness as the moderator. Moreover, this study tests ethical executive behavior, accountant’s CSR-based practice, outstanding corporate culture, and intense regulation force as the restraining of earnings management and uncertainty business environment as the antecedent. Earnings management consists of four dimensions: 1) unreasonable change in accounting policy, 2) wealth transfer misrepresentation, 3) information distortion, and 4) corporate based concern of accounting choice. Thai-listed firms as the population and sample. The questionnaire is used to collect data. The results show the negative relationship among earnings management, financial reporting reliability, stakeholder acceptance and corporate transparency. Moreover, social-minded awareness is the moderator on the relationship among financial reporting reliability, stakeholder acceptance, and corporate transparency. In addition, four restraining of EM has significant direct effect on EM. Surprisingly, uncertainty business environment is not antecedent of EM. Potential discussion is competently implemented in the study. Research implication, future research directions and conclusion will be presented.

Keywords: Earnings Management, Financial Reporting Reliability, Stakeholder Acceptance, Corporate Transparency, Ethical Executive Behavior, Accountant’s CSR-based Practice, Outstanding Corporate Culture, Intense Regulation Force, Uncertainty Business Environment, Social-Minded Awareness 1. INTRODUCTION Accounting numbers, especially earnings an important summary statistic of a firm’s performance are used to help stakeholders in many ways not only external users use them to evaluate stock prices (Ball and Brown, 1968; Beaver, 1972) but also internal managers use them for strategic planning, monitoring, controlling, and performance measurement. Thus, the quality of earnings is so important due to the fact that qualitative characteristics of financial statements consist of understandability, relevance, reliability and comparability (IASB, 2001). During two decades, earnings are managed from numerous incentives including market incentive and influenced the stock market, executive’s compensation, decreased the likelihood of violating lending agreements, and avoided intervention by government regulators (Healy and Wahlen, 1999; Sevin and Schroeder, 2005; Spear, 2007). It can be more serious and harmful activities because earnings management (hereafter EM) does not only directly affect the overall integrity of financial reporting but also affect resource allocation in an economy (Rath and Sun, 2008). Then, earnings management can mislead financial reporting users. EM focus on short-term benefit, but long-term firm confronts with real economic situation to pass to go bankrupt in the end such as in the case of Enron, WorldCom, and Xerox that impacts to transparency, capital market trust, accounting professional acceptance, regulator role and standard-setters. With regard to past research, EM has been widely studied in the context of developed countries such as the United States of America, The United Kingdom, and the European Union. There were very a few researches studied in the context of developing countries, especially Thailand. Moreover, Thailand was well-known for its scandal about EM. The case of Picnic Corporation Public Company had hidden its over income changing accounting method about payment term of gas container with gas filling factory. In addition, the company was executed for lending money to other companies, but it did not really do so. So it distorted information in financial reporting and made it vague, unclear, and affecting the users’ decision making.

JOURNAL OF INTERNATIONAL FINANCE AND ECONOMICS, Volume 9, Number 3, 2009 1

The concept of EM has long been studied both in economic and behavioral issues. The majority focus in economy, only a few researches focus on behavior. Prior researches concentrated to provide empirical evidence on the existence and motivation of their practice (Matsunaga and Park, 2001; Othman and Zeghal, 2006) the frequency, pervasiveness, and magnitude of earnings management (Bauwhede and Willekens, 2003; Erickson and Wang, 1999) restraining earnings management (Van Caneghem, 2002; Wasley and Wu, 2006) the market consequence of earnings management (Beneish, 1997; Dechow et al., 1996; Sloan, 1996), and ethics and perception (Cohen et al., 2000; Elias, 2002; Fischer and Rosenzweig, 1995;).However, past research focuses on accounting manipulation such as change or choice accounting policy, operating manipulation such as delay repairing assets, and classification shifting such as shifting from core item to special item. . The disadvantage point of prior researches is that they have omitted the reflection of earnings management that is information distortion and wealth transfer misrepresentation. Balsam et al. (2003) stated that manager reports affect SFAS No. 123 to footnote instead of recognition to expense which change in material information that influence stakeholder so it is the information distortion. This dissertation tries to capture the intent of activity. Information distorting refers to changing in the form, meaning of information within financial reporting and off balance sheet that including concealment and representing imperfect significant information that influences on stakeholders’ decision making. Consequently, wealth transfer misrepresentation refers to intent or actions that managers focus on private gain more than on maximized firm value and corporate sustainability so that this dissertation captures intent earnings management use in four dimensions which encompass: 1) unreasonable change in accounting policy, 2) wealth transfer misrepresentation, 3) information distortion and 4) corporate based concern of accounting choice. Moreover, Healy and Wahlen (1999); Spear (2007) suggested that future research should identify the financial and operate characteristics of the firm found to be engaging in earnings management and answering the question what factors limit earnings management. Hence, four research questions are presented in this paper. Firstly, the key research question is how earnings management affects financial reporting reliability, stakeholder acceptance and corporate transparency. Secondly, how the impacts of executive ethical behavior, accountant’s corporate social responsibility (hereafter CSR)-based practice outstanding corporate culture, intense regulation force, and uncertainty business environment on EM are. Thirdly, how the performance implications (corporate transparency) of financial reporting reliability, stakeholder acceptance and EM are on corporate transparency. Lastly, how social-minded awareness moderator affects the relationships among financial reporting reliability, and stakeholder acceptance to corporate transparency. To answer four research questions, six objectives are provided as follows: 1) to examine the role of EM on Financial reporting reliability, stakeholder acceptance and corporate transparency; 2) to investigates the relationship among financial reporting reliability and stakeholder acceptance on corporate transparency; 3) to test the moderating effect (social-minded awareness) which influence the relationship among financial reporting reliability, stakeholder acceptance and corporate transparency; 4) to determine four restraining─ ethical executive behavior, accountant’s CSR-based practice, outstanding corporate culture and intense regulation force limiting EM; 5) to compare which one of the four restraining is more influence than another and; 6) to determine the antecedent (uncertainty business environment) that causes EM. This paper has theoretical implication that encompasses to test agency theory and positive accounting theory and adds literature of earnings management in terms intent of manager. Consequently, this work tries to capture the technique of earning management that is information distortion and intent of manager to wealth transfer misrepresentation. Further, this paper investigates the concept of corporate culture, ethical of executive, accountant’s CSR-based practice, and intense regulation force to limit earnings management. In the context of practical contribution, the results of this dissertation provide contribution not only to regulators but also to educators for concerning about ethical and code of conduct. Moreover, the regulators can use the evidence to apply the methods limitation or to reduce EM. The remainder of this paper is organized as follows. The next section presents the theoretical foundation. Literature review, and hypothesis development is indicated in the followed section. The fourth section explains the research design, data collection and variable measurements of all constructs in the study.

JOURNAL OF INTERNATIONAL FINANCE AND ECONOMICS, Volume 9, Number 3, 2009 2

The fifth section presents the results and discussion. The sixth section shows the implication of this research, limitation and suggestion for future research. The conclusion is highlighted in the last section. 2. THEORETICAL FOUNDATION Agency theory (Jensen and Meckling, 1976) and positive accounting theory (Watts and Zimmerman, 1986) can explain existing earnings management. In context of agency theory, the relationship among various parties in the firm is the principle and agent. Principle (shareholder) needs to employ agent (manager) to manage corporation to achieve the objective that the principle must pay the benefit for agent based on contract and performance. Accounting information is made by agent to communicate financial position, performance and change in financial position to principle that existence information asymmetry and lead to the moral hazard problem. It can imply that managers may distort some damaging information, may divert corporate resources for themselves, or may signaling positive factor effect self-interest. Positive accounting theory perspective states manager manipulation accounting number through three hypotheses political cost hypothesis, bonus plan hypothesis and the debt covenant hypothesis. The bonus plan hypothesis indicates that managers are more likely to shift future earnings to current period to ensure their bonus or their compensation. The debt covenant hypothesis suggests that firms with face debt covenant, managers are more likely to engage in income-increase to reduce the likelihood of violating lending agreements. Finally, the political cost states that managers are more likely to engage in income-decreasing to reducing political cost such as, avoiding large tax payment. 3. LITERATURE REVIEW AND HYPOTHESIS DEVELOPMENT With regard to the literature review on EM and supporting with the Agency Theory and Positive Accounting Theory, this paper proposes a conceptual model to empirical testing in the topic “Earnings Management in Thailand: Effects on Financial Reporting Reliability, Stakeholder Acceptance and Corporate Transparency”. This paper provides relevant literature review to four sections. First, the integrative review of EM and shift to behavior context are presented. Second, it explains negative consequence of EM (corporate transparency, financial reporting reliability and stakeholder acceptance). Third, it illustrates the association among financial reporting reliability, stakeholder acceptance and corporate transparency and tests social-minded awareness moderator effects on the relationship among financial reporting reliability, stakeholder acceptance and corporate transparency. Finally, the restraining and antecedence of earnings management are illustrated. The full conceptual model is presented in Figure 1. 3.1 Earnings Management The concept of EM has been studied for a long time since at least the 1960s. Xiong (2006) and Rath and Sun (2008) classified EM research focus on three groups. First, earlier capital market focus (1960s-1970) those academic researches emphasized on the influence of accounting choice on capital market. However, there was inconsistency between Mechanistic Hypothesis and Efficient Market Hypothesis. Mechanistic Hypothesis states that users can be misled by firm’s accounting discretion but, EMH states that users cannot be misled by accounting discretions because users are not foolish. They can find other information for decision making. Thus, this inconsistency leads to the question why firms manipulate accounting number. Watt and Zimmerman (1986) tried to answer the question they developed PAT and shift EM research focus on internal contractual incentive (1980-1990). They focused on the conflict of interest among other contracts within firms. This group found evidence why firms change or choice accounting policy based on three major hypotheses: bonus plan, debt covenant, and political cost. It is not clear about the objective of EM and also it is unclear whether manager use judgment in financial reporting and in structuring transaction for maximize their compensation or they signal the firms prospect to outside investors (Rath and Sun, 2008). Therefore, the researches shift back to capital market again and up to date. Current researches try to capture intent of manager to manipulate accounting number for influence stock price or meet analysis forecast. EM is a major topic in accounting research, but the definition of EM is inconsistency Yaping (2006) separates the definition of EM into four approaches: management intention, quality of reported earnings information, management reporting discretion, and accounting standard application. In terms of

JOURNAL OF INTERNATIONAL FINANCE AND ECONOMICS, Volume 9, Number 3, 2009 3

H5, H6

H7a - b

H8a - d

H9 –H13

management intent, EM is a purposeful intervention in the external financial reporting process, with management intent of obtaining some private gain. The main problem of this approach is that intention of manager is unobservable. In terms of the quality of reported earnings information, EM is the manipulation of reported earnings so that they do not accurately represent economic earnings at every point in time. The significant puzzle is no one knows a firm’s underlying or information asymmetry. In addition, in terms of management reporting discretion EM is the strategic exercise of management discretion over accounting numbers with or without restrictions. Finally, EM is the practice of firms’ misapplying accounting standards and it also is the process of taking deliberate steps within the bounds of accounting standard so as to bring reported earnings to a desired level. To sum, from the details of definition earnings management is that the distinctive features consist of EM are manipulated on purpose and intentionally, and EM not only use accounting technique but also real business decision.

This paper focuses on management intention. A lot of academic researches define EM in terms of intent of managers. However, the population reference is earnings management occurs when manager use judgment in financial reporting and in structuring transaction to alter financial reports to either mislead some stakeholders about the underlying economic performance of the company or to influence contractual outcomes that depend on reported accounting numbers (Healy and Wahlen, 1999). Misleading some stakeholders is the key assigned EM to inimical and harmful. Moreover, in terms of judgment of manager based on this definition that can separates into two types. The first is accounting manipulate such as choices accounting policy among GAAP. The second is operating manipulate such as delay repair some equipment implying that holding cash flow. This dissertation defines EM as intention, distortion, or omission of significant information which serves to increase or to decrease earnings that does not indicate real economic circumstance of the firm and also mislead some stakeholders to change

Figure 1: Earnings Management In Thailand: Effects On Financial Reporting Reliability, Stakeholder

Acceptance And Corporate Transparency

H1

H2

Ethical Executive Behavior

Accountant’s CSR-based

Practice

Outstanding Corporate

Culture

Intense Regulation

Force

Stakeholder Acceptance

Uncertainty Business

Environment

Financial Reporting Reliability

Social-Minded Awareness

Corporate Transparency

Earnings Management

H4

H5

H6, H7

H3

H8

H12

H11

H10

H9

JOURNAL OF INTERNATIONAL FINANCE AND ECONOMICS, Volume 9, Number 3, 2009 4

their determination. Based on this definition, intention of manager is impossible to be measured directly and difficult to operationalize them directly (Xiong, 2006; Yaping, 2006). However, this paper tries to measure EM by indirect measurement that is tendency of manager to the reflection of EM. This paper measures EM by using four dimensions which reflect EM encompass: unreasonable change in accounting policy, wealth transfer misrepresentation, information distortion, and corporate based concern of accounting choice. All dimensions are developed from Agency Theory, Positive Accounting Theory, and relevance literature review and can be explained as below. 3.1.1 Unreasonable Change in Accounting Policy The first dimension to measure EM is unreasonable change in accounting policy. It refers to inconsistently or unreasonably change in accounting principle, accounting estimates, or the reporting entity. This dimension tries to capture intention of manager to exercise accounting accruals and operationalize from the most popular to measure EM in term of using secondary data. It’s the discretionary total accruals method (Dechow et al, 1995) which presumes that managers fundamentally depend on their discretion over certain accounting accruals as a means of managing earnings. Jones (1991) provides total accruals into two types: discretionary, and non-discretionary. Discretionary accruals are the management that determined, but non-discretionary are economically determinant (Xiong, 2006). Managers can use their judgment over accounting methods such as, changing in accounting policy (such as a new valuation inventory method), estimating related to discretionary accruals (such as a doubtful accounts receivable), and moving up the timing of recognizing accruals. Total accruals methods use discretionary accruals as a proxy of EM implies that if the discretionary accruals are high, the level of EM is high too. When the firms want to increase or decrease earnings, managers can exercise their judgment pass accounting policy or accounting methods. Hence, the change in accounting policy is not reasonable because the process does not follow conditions of accounting standard.

According to IAS 8, firms can change accounting policy, accounting methods, or estimate related to discretionary accruals when (a) required by an IFRS legislates new standard or an Interpretation or (b) results in the financial statement providing more relevant and reliable information about the entity’s financial position, financial performance or cash flow. Therefore, managers who change accounting policy and don’t follow the IAS 8 is the unreasonable change and lending to inconsistency, and unnatural of accounting policy. It showed that managers use judgment to ensure the level of earning to meet the target and EM is occurred. Inconsistency and unnatural accounting policy or accounting methods will damage financial reporting reliability and stakeholder acceptance which will discussed as below: The IASB’s Framework for the preparation and presentation of financial statements mention four qualitative characteristics of financial statement which consists of understandability, reliability and comparability (IASB, 2001). The reliability is related to financial information which is free from both error and intentional misstatement, faithfully delineates what is a purpose to represent. The concept of reliability is affected by the use of estimation and by uncertainties. These uncertainties consist of two components: exercise discretionary in preparing financial statement, and disclosure. 3.1.2 Wealth Transfer Misrepresentation The second dimension to measure EM is wealth transfer misrepresentation. It refers to intent or actions that manager focuses on private gain more than focuses on maximize firm value and corporate sustainability. Private gain is the benefit from his work and receives from the firm such as bonus, compensation and image of manager. Maximized firm value depends on many factors such as investment in profitability project and reduces conflicts and pressure among stakeholders. Transfer wealth from other contracting parties can be separated into two types: manager transfers wealth from firms, and manager transfers wealth for firms. According to Watt and Zimmerman (1990), accounting number, especially earning or bottom line transaction are used for performance measurement. It causes wealth to be transferred from shareholder to manager. Similarly, Schipper and Vincent (2003) assumed that earnings result in wealth transfer to manager from other parties if earnings are used as an indicator of manager’s performance. Transfer wealth from other contract parties may be debt holders to shareholder by avoiding the violation of debt covenants (Watt and Zimmerman, 1990; (Smith, 1993). Moreover, Yaping (2006) suggested that wealth transfer from investor (i.e. potential) to shareholder is the basis of the SEC’s strong obstruction earnings management activity. Therefore, if manager intends to transfer

JOURNAL OF INTERNATIONAL FINANCE AND ECONOMICS, Volume 9, Number 3, 2009 5

wealth from other parties to maximize private gain, he can use aggressive or conservative accounting, signaling and financial motives, and take “a big bath” for misleading stakeholder and achieving the target of earnings. 3.1.3 Information Distortion The third dimension to measure EM is information distortion. It refers to change in form, meaning of information within financial reporting and off balance sheet including conceals and represent imperfect significance information that influence on stakeholder’s decision making. This dimension tries to capture intent of manager disclose imperfect of information in financial reporting such as, not frankly reporting information. Moreover, change in form or meaning is important and misleads judgment of stakeholder. Balsam et al. (2003) find evidence that manager report affect of SFAS No. 123 to footnote instead of recognizing the expense which change in material information that influences stakeholder. Moreover, timeliness of information disclosure is used to manipulate or mislead financial reporting user. The disclosure should reduce the information asymmetry between insider and outsider and can affect stock price, perceive image of stakeholder to the firms. Therefore, management may use disclosure for signaling stakeholder to wrong decision making. Empirical evidence suggests that managers delay the disclosure of bad news relative to good news (Kothari et al., 2009) and timeliness of firm’s voluntary disclosure of good vs. bad news depend on firms size and the degree of news (Tucker and Zarowin, 2006). In addition, Ismail and Chandler (2005) investigated companies that tend to defer the reporting of exceptional items to the final quarter. It implies that it delays bad news and affects earnings in the first three quarterly reports which are considered to be misstated, overstatement bias. Thus, delaying bad news but leaking good news to investors may be deceiving investors to wrong route judgment. 3.1.4 Corporate Based Concern of Accounting Choice According to GAAP, management can also use accounting choice to make financial reporting and that may increase informative for uses or mislead users. Managers can exercise in financial reporting consistent with GAAP. Agency costs, information asymmetries, and externalities affecting non-contracting parties are the incentive to drive corporate concern of accounting choice (Fields et al., 2001). An accounting choice is any decision whose primary purpose is to influence the output of accounting system in a particular way, including not only financial statement published in accordance with GAPP, but also tax returns, internal decision making and regulatory filings (Fields et al., 2001). The last dimension to measure EM is corporate based concern of accounting choices. It refers to the concentration of firm to use ambiguity or alternative in Generally Accepted Accounting Principle (GAPP) or accounting standard to manipulate accounting data that aims to provide temporarily increase earnings. Judgment based on GAAP such as forecast lives and salvage values of plant and equipment, losses from bad debts and asset impairments. Manager can choose among accounting standard for reporting the same transaction such as the accelerated depreciation methods or the straight-line methods weighted average or FIFO inventory valuation methods. Changing inventory valuation methods can explain that from FIFO to LIFO in periods of increasing price, reduces earnings because the product that was sold most recently will appear in “cost of goods sold” and present in income statement. The oldest will appear on the balance sheet under “inventory. That activity is with-in GAPP earnings management. 3.1.5 Earnings Management and Financial Reporting Reliability Financial reporting reliability occurs when information in financial statement is both from material error and bias. If management is concerned to use ambiguity or alternative of GAAP for obtaining to reduce agency cost and reduce externality affecting, the information does not represent events and transaction faithfully. For example, if the management is concerned for the compensation and bonus, they are more likely to choose accounting choice for increasing earnings or reducing expenditure, for example, management is more likely to choose capital leases instead of operation leases. As a result, the cost in records to the assets as a replacement for recognize to expenditure and increase earnings. Daily (2001) noted that if firms choose questionable accounting practice to meet expectation of shareholders, analysts and manager compensation, then they will get the attention of the regulators such as, SEC, implying that regulators who see some indicators to represent firms may mislead financial users through accounting choice that impact not only free form material error and bias but also faithfulness of transaction and events.

JOURNAL OF INTERNATIONAL FINANCE AND ECONOMICS, Volume 9, Number 3, 2009 6

Prior researches use the concept of financial reporting quality more than financial reporting reliability and the main link for good financial reporting quality is corporate governance (Klein, 2002) implying that when the firms have good corporate governance it is more effectiveness in monitoring the corporate financial accounting process. Corporate governance has four foundations – management, the audit committee, the external auditor, and the internal audit department. Therefore, if the firms don’t keep on the way of good corporate governance, that allows an opportunity for the firms to manipulate accounting process and the risk of accounting error and the practice of earnings management which damage financial reporting quality through financial reporting reliability. Moreover, Akers et al., (2007) state that if management does not try to manipulate earnings, there is an increased earnings quality. The earnings data is more reliable because it is free from unreasonable change in accounting policy such as deferring expenses or accelerating revenues to bring about desired short-term earnings results. The absence of earnings management does not occur. In addition, the authors noted that if management does not manipulate earnings, earnings in financial reporting are reliable. Nevertheless management manipulates earnings; the financial reporting may weaken reliability. The misrepresentation is the key to capture intention of manager’s tendency to manipulate accounting information because if they do not want more private gain they should present the information faithfully. Managers can transfer wealth from firm (bonus plan hypothesis) or for firm (debt covenant, and political cost hypothesis). Moreover, mangers can transfer wealth misrepresentation from other situation such as equity offering. Many of academic researches investigate incentive to increase reported income in the context of stock offering. Information asymmetry among manager-owner-investor is the key to explain the events. Managers who want to misrepresent the wealth among stakeholders are more likely to choose accounting policy than to increase short-term earnings, and to distort information to present external. Those activities influence the quality of financial reporting because they do not provide information about the financial position, performance and changes in financial position of firms and may mislead judgment’s financial users. Reliability is one of the qualities of financial reporting that depends on judgment of users to be prudent on uncertainties such as assets or income which are not overstated, and liabilities or expenses are not understated. The availability of information is alleged to be a key determinant of the efficiency of users’ decision-making and influences the growth in an economy (Bushman et al., 2003). Accounting information is importing key of information that is mandated by regulators for available stakeholders. When the financial reporting does not represent events and transaction faithfully such as delaying bad news (Kothari et al, 2009), changing in form or meaning which is important and misleads judgment of stakeholder (Balsam et al., 2003) and deferring the reporting of exceptional items to the final quarter (Ismail and Chandler, 2005). Therefore, the financial reporting is likely to be unreliable, then the first hypothesis is proposed as bellow: Hypothesis 1: The higher the level of earnings management is, the lower the financial reporting reliability will be. 3.1.6 Earnings Management and Stakeholder Acceptance This dissertation defines stakeholder acceptance as perceive admittedly organization governance, honesty of group or individual who can affect or is affected by the achievement of the corporate objective. Many academic researches noted that EM is immoral and unethical activities (Akers, et al., 2007; Brown, 1999). It can mislead financial statement user and is more serious and harmful activities (Ziv, 1998). Moreover, earnings management behavior is a concern of standard-setters, regulators and the accounting profession. EM not only influences a firm’s owner, it also affects other stakeholders. Hence, when the firms represent inconsistency of accounting policy or change in accounting policy and do not keep on GAAP that affects the overall integrity of financial reporting. It impacts the perception of stakeholders to view the poor image of the firm and impacts business process. Beneish (1997) finds that firms really violate GAAP and have negative earnings for two years after the disclosure of the GAAP violation and the stock market responses negatively when the firms are accused allegation of EM by the financial press or SEC.

JOURNAL OF INTERNATIONAL FINANCE AND ECONOMICS, Volume 9, Number 3, 2009 7

The indicator of wealth transfer misrepresentation may be based on motivation of managers such as, compensation or bonus. Managers’ manipulation reported earnings to increase their compensation (Gaver and Austin, 1995; Healy, 1985; Holthausen et al., 1995). Summers and Sweeney (1998) noted that managers who mislead stakeholders may possess low personal ethics, misleading include transfer wealth from firms to private gain through compensation. Beneish (1999) explored the punishment of managers who manipulate accounting information after the EM is discovered. He noted that managers penalties by reputation losses, employment and monetary damage. That even shows that stakeholder does not accept the EM activity because this actions are unethical. Financial users attempt to price protect them against EM and their ability enhances when firms distort material information, delay bad news, or disclose supplementary balance sheet and/or cash flow statement. As described early, if the stakeholder acceptance about information distortion, they may connect with firms, buy and sell stocks of the firm. But stakeholders do not accept the information distortion; the stakeholder may do business with firms or the reaction for negative stock prices. Baber et al., (2006) used supplementary financial disclosure to proxy of EM and investigate stock price reaction to this activity. The results show that the negative relationship between security price reactions and EM indicator are stronger when supplementary balance sheet and cash flow statement is disclosed along with earnings than when such information is not disclosed. That result represents the investors who do not accept the information distortion. When the firms are more concerned of accounting choice, the extreme case is the fraud second by violating GAAP or accounting standard. The consequence accuses of firms with more concerns of accounting choice. Their cost of capital may be higher because the institution questionable ethical standards (Kaplan, 2001) that represent EM are not acceptable from other parties. In addition, the firms face alleged inventory or receivable overstatement impact on accounting choice for 70 percent of all enforcement, which the average stock price reaction to announcements of these enforcement action is declined 13 percent (Feroz et al., 1991). Moreover, the consequence of EM may be that firms face higher cost of capital after being identified as having manipulated earnings, a less of analysis following, and increase in short interest (Dechow and Skinner, 2000). That indicates the unacceptability of EM though reduces the credibility of the firm’s management process and punished by other stakeholder. According to aforementioned, all four dimensions integrated as EM. Hence, when firm is more concern with level of earnings and focus on short private gain more than long term benefit. Firm may manipulate earnings and that affects stakeholder acceptance leading to the hypothesis as below: Hypothesis 2: The higher the level of earnings management is, the lower the stakeholder acceptance will be. 3.1.7 Earnings Management and Corporate Transparency Corporate transparency is defined as the acceptance of stakeholders from administration’s transparency feature concentration on rules, regulations and presenting fact information with correctness and timeliness (Bushman et al., 2003). The concept of corporate governance states that corporate governance can be improving financial reporting quality. Nevertheless weakness in governance can give opportunities of EM and damage financial reporting quality, financial statement fraud, and weaker internal control (Dechow et al., 1996; Beasley, 1996; shah et al., 2009). This implies that EM damages fair and true of financial reporting information that the major data to present outside publicly. EM reduces transparency obscuring the true earnings of company. Moreover, the corporate transparency is destroyed by EM because when the firms accuses of regulator such as SEC. The image of the firm is tarnished and can be affecting to transparency of firm. This leads to the hypothesis as below: Hypothesis 3: The greater the degree of earnings management is, the lower the corporate transparency will be. 3.2 Mediating Effects of the Relationship 3.2.1 Financial Reporting Reliability and Corporate Transparency Financial reporting reliability refers to information in financial statement which is free from material error and bias and can be depended upon by users to represent events and transactions faithfully (IASB,

JOURNAL OF INTERNATIONAL FINANCE AND ECONOMICS, Volume 9, Number 3, 2009 8

2001). Corporate transparency can remain when firms keep on code of ethics disclosures (Richard and Catherine, 2005) which implies that firms should present free from material error and bias the information to outside. Specially, the financial reporting because it is in order to provide information about the financial position, performance and change in financial position. In addition, the meaning of reliability is affected by the use of estimates and by uncertainties associated with items recognized and measured in financial statement. Firm has a reliability of financial reporting which user reduced uncertainty of all items in financial reporting that can reduce information asymmetry between manager and shareholders. Therefore, transparency is to encourage companies to fully disclosure information about their process, practice as well as financial reporting quality one which is the reliability. This leads to the related hypothesis as below: Hypothesis 4: The greater the financial reporting reliability is, it is more likely that the higher the corporate transparency will be. 3.2.2 Stakeholder Acceptance and Corporate Transparency Stakeholder acceptance refers to perceive admittedly organization governance of group or individual who can affect or can be affected by the achievement of the corporate objective (Kuratko et al., 2007). Stakeholder acceptance depends on many factors such as firm’s concern wealth of all stakeholders. Firms want to be an acceptance from many stakeholders who may follow up to meet their expectation. To date, stakeholders have a main role to pressure firms to care social and environment. The concept of CSR is the one that launched for regulator in order to protect many stakeholders from firm taking advantage. One of stakeholders wants fairness and availability of information to present to them. It implies that firms with pressure from stakeholder and want acceptance form them may present fairness and availability of information which affects corporate transparency. This leads to the related hypothesis as below: Hypothesis 5: The greater the stakeholder acceptances are, it is more likely that the higher the corporate transparency will be. 3.4 Moderating Effects of the Relationship Social-minded awareness refers to perceived responsibility and accountability that a business confronts with many stakeholders through social and environment. It also refers to policies, practices, and activities to present a good member of a social (Unerman and O'Dwyer, 2007). This concept permits firms to fully disclosure information about their responsibility to social that include process, practice, policies as well as financial reporting. This implies that the relation between financial reporting reliability and corporate transparency is strengthened because firms have awareness to responsibility and accountability of social and fully present information free form both bias and error. Moreover, the relation between stakeholder acceptance and corporate transparency is strengthened because firms are aware of stakeholder pressure to request for all important information to reduce mistake in decision making and fully present information faithfully. This leads to the related hypothesis as below: Hypothesis 6: The more the social-minded awareness is, the stronger the positive relationship between financial reporting reliability and corporate transparency is. Hypothesis 7: The more the social-minded awareness is, the stronger the positive relationship between stakeholder acceptance and corporate transparency is. 3.5 Restraining of Earnings Management EM is serious and harmful activities because earnings management not only directly affects the overall integrity of financial reporting but also affects resource allocation in an economy (Rath and Sun, 2008). Then, EM can mislead financial reporting users. According to Healy and Wahlen (1999), they suggest future research to respond to what factors limit earnings management. It can be a new tract of EM and the researcher tries to answer this question. Based on definition of EM, it occurs when manager exercises judgment around accounting policy and transaction for decision making. This paper reviews literature of

JOURNAL OF INTERNATIONAL FINANCE AND ECONOMICS, Volume 9, Number 3, 2009 9

the prior research that relates to the way to limit EM, external and internal factors. In terms of external factor, that includes the regulator role, and external auditing. Internal factor is business ethics, corporate governance practice, and CSR concept. Many academic researches focus on the role of regulators to limit EM because they have power and authority to limit alternative of accounting choice and accounting change through the accounting standard. 3.5.1 Ethical Executive Behavior and Earnings Management Executive behavior is the top power of the organizational which plays not only in the role of leader but also their behavior that influences of the organization. For example, the executive has more leadership that can help the members to follow and keep on the organization objectives. In terms of ethics, it refers to moral standard of right and wrong in conduct, judgment and behavior. Hence, Ethical executive behavior is defined as actions consistent with accepted standard of good conduct or behavior that conforms to be generally accepted for top manager that including trustworthiness, responsibility, respect, comparison fairness and citizenship. According to a recent research which noted that earnings management occurs when manager exercise discretionary accrual, manipulate business transaction that can mislead financial reporting user so that earnings management is immoral and unethical (Akers, et al., 2007; Brown, 1999). In addition, earnings management behavior is a concern of standard-setters, regulators and the accounting profession (Elias, 2002). However, not all companies manage earnings leading to the question why some managers choose earnings management while others do not. Many researchers may answer that they use the ethics. Prior research investigated the concept of ethics to earnings management. Greenfield et al., (2008) examined ethical orientation and professional commitment on earnings management. The results show that participants with higher level of ethics and professional commitment seem to be less likely to engage in earnings management. Consistent with Huang et al., (2008) who suggests ethical management and corporate governance reduce the abnormal accruals. As mentioned earlier, the managers have high level of ethics such as, trustworthiness, responsibility, respect they do not accrual management and represent financial reporting faithfulness. This leads to the related hypothesis as below: Hypothesis 8: The greater the level of ethical executive behaviors is, the lower the level of earnings management will be. 3.5.2 Accountants’ CSR-based Practice and Earnings Management Accountants play the important role for preparing financial reporting and they are keys to make financial reporting quality. CSR is the way of managing corporate by concern the impact of activities and customers, suppliers, employees, shareholders, communities, and other stakeholders as well as the environment. It also includes activities such as incorporating social aspects into products and manufacturing processes, adopting progressive human resources practices, achieving improved environment-friendly (McWilliams et al., 2006; Prior et al., 2008). The concept of CSR is for sustainability, performance, competitive advantage and survival of the firms (Orlitzky et al., 2003; Waddock and Graves, 1997) Accountant’s CSR-based practice refers to degree or procedure of accountant that keeps on accounting standard and concern code of conduct, legal, ethical, responsibilities to third parties about integrity of accounting information. Prior research, for example Prior et al (2008) examined EM and CSR in multi-nation panel sample of 593 firms from 26 countries between 2002 and 2004 they found that EM practices have a positive impact of a CSR. It was different from Chih et al., (2008) investigated whether the CSR-related EM of 1653 corporations in 46 countries. The results show that the relationship depends on their proxy of EM for example, when EM is proxied by earnings smoothing, an increase in CSR mitigates earnings smoothing but when EM is proxied by earnings aggressiveness, an increase in CSR increase earnings aggressiveness. However, this paper explains the relationship among accountant’s CSR-based practice and EM that when accounting plays the role of preparing financial information such as, book keeping, considering vouchers which socially responsible. It does not distort or manipulate earnings, hence it conducts on EM. Moreover, CSR-based practice not only focuses in short term earnings but also concerns good future relationship with all stakeholders. Accountant keeps work within accounting

JOURNAL OF INTERNATIONAL FINANCE AND ECONOMICS, Volume 9, Number 3, 2009 10

standard or GAAP and keeps on professional conduct and that practice can mitigate EM. This leads to the hypothesis as below: Hypothesis 9: The higher the level of accountants’ CSR-based practices is, the lower the level of earnings management will be. 3.5.3 Outstanding Corporate Culture and Earnings Management The concept of corporate organizational culture is the main theme in academic research. Many researchers defined organization culture in many different way for example; Gordon (1991) defined as “an organization specific system of widely share assumption and values that give rise to typical behavior”. It influences the corporate memberships in order to create and gain commitment. To clearly defined Ussahawanitchakit (2002) described that as a pattern of an organization-specific system of assumption, value, beliefs, artifacts, behavioral norms, and expectations shared by the organization’s members. Outstanding corporate culture refers to company’s strategy which focuses on concept of sustainability (e.g. continuous improvement, concentration on stakeholder and social, keep on concept of corporate governance, and building customer satisfaction). Corporate culture affects corporate ethical values and practice that affects member’s attitudes toward acts of organization, strategic and accounting process. It can help firms to achieve good performance and competitive advantage (Christensen and Gordon, 1999). The concept of culture has been less studied in terms of EM. Prior research use nation culture based on Hofstede’s (1984, 1991) to examine perception of EM across countries. The results show that the Power Distance and Masculinity dimension are associated with the perception of operating manipulation decision. Individuals in high Masculinity or low Masculinity countries perceived operating manipulations less favorable the individuals in Low power Distance or high Masculinity countries (Geiger et al., 2006). In addition, Ussahawanitchakit (2002) provided a conceptual framework systematic explanation for the relationships among organizational culture, environmental characteristics and earnings management. The author noted that earnings management diminished by organization culture. He provided four cultures characteristic: bureaucratic, clan, entrepreneurial, and market cultures and proposes the negative relationship to earnings management. In summary, outstanding corporate culture can help firms to achieve good performance, sustained competitive advantage and survival in the business. Firms that have stronger culture may be able to reduce earnings management well. Thus, outstanding corporate culture is likely to impact the degree of earnings management. This leads to hypothesis as below: Hypothesis 10: The higher the strength of outstanding corporate cultures is, the lower the degree of earnings management will be. 3.5.4 Intense Regulation Force and Earnings Management Regulations influenced not only on organization process but also manager’s behavior. In the business environment, regulations have important role and they can give opportunity to firms’ management accounting number (Kao et al., 2009) or prevent the level of EM (Patrice, 2007) and lead to significant benefit in terms of increase financial reporting transparency and improve the comparability of financial reporting that improves the quality of financial reporting (Ewert and Waggenhofer, 2005). Prior research focused on whether the mandatory introduction of new standard that had an impact on earnings quality, and more precisely on earnings management. Jeanjean and Stolowy (2008) investigated the effect of the mandatory introduction of IFRS standards on earnings quality and limiting EM. They selected three countries, namely, Australia, France, and UK to test the phenomena. The results show that the level of EM did not decline after the introduction of IFRS and they noted that accounting standard alone does not improve earnings quality and prevent EM and they point out to the strict and enforcement from institution. This paper uses the level of enforcement of regulation to prevent EM. Intense regulation force refers to pressure, attention and concentration of the set of regulator rule that includes law, regulation and their implementation, and accounting standard that strong effect to firms. As mentioned above, when firms perceived the level of enforcement of regulations they may fear penalty and do not conduct on EM. This leads to the related hypothesis as below:

JOURNAL OF INTERNATIONAL FINANCE AND ECONOMICS, Volume 9, Number 3, 2009 11

Hypothesis 11: The higher the strength of intense regulation forces is, the lower the degree of earnings management will be. 3.6 Antecedent of Earnings Management The literature reviews on motivation or existence of EM are separated into three periods. First, academic researches focus on capital market and then academic researches change to within firms context and to date shift back to capital market again. The first period focuses on the influence of accounting choice on the capital market. The Mechanistic hypothesis proposes that stock price is associated with change or choice in accounting policy. Summarizing earnings is important for investors because earnings increasing may impact to abnormal return (Ball and Brown, 1968). It represents the accounting information particularly earning is which the information content. The interaction between earnings and stock price can certainly drive management towards manipulated earnings. The second period is shifting to contractual with in firms. Academic research focuses on managers trying to meet their expectation contracting in the firm for their bonus, debt covenant and reduce political cost by exercise discretion over accounting number. Much empirical evidence supports the three major hypothesis of PAT. For example, Healy (1985), Holthausen et al (1995), Gavor et al (1995) found that firms with pay bonus awards are more likely to use discretionary accruals to increase report earnings than firms to pay salary with no bonus. The results are consistency not only at firm level but also at business unit level (Guidry et al., 1999; Healy, 1999). Moreover, some papers use pay-performance, earnings-based compensation for proxy of incentive and the results show that firms use judgment for exercise accruals accounting than other firms (Levine and Hughes, 2005; Murphy, 2000; Shuto, 2007). In terms of lending contract the research investigates whether firms that face with lending contract the more likely to be manage earnings. For example, Sweeney, 1994 investigate a sample of 130 firms in US that actually violated a lending covenant. The results show that covenant violators made income increase earnings management, but these typically took place after the violation. Holthausen (1981) found that firms used to change depreciation methods from another to straight-line for meeting their dividend constraint. The example represents lending contract that is the incentive for manager to manipulation accounting policy. The properly political cost firms have incentive to reducing earnings for avoiding the pressure from regulator such as, governmental regulations and tax laws. For example, Jones (1991) studied EM during an inquiry of the International Trade Commission form 23 firms in 5 industrial sectors. The results show that managers made income-decreasing earnings management accounting choice during the period. In addition, Haw et al (2005.) tried to answer firms escaping from governmental interference. They studied income-increase earnings management in China as a response to governmental regulations. Moreover, earnings management for large tax avoidance is investigated income-decreasing which earnings management used to reduce large tax avoidance because accounting number is the basis for calculating tax payment (Johnston and Rock, 2005; Monem, 2003). In summary, political cost is the strong incentive for firms to manage their earnings. This paper shifts from previous paradigm, capital market and contractual incentive within firms to business environmental because an organization’s environmental uncertainty may induce greater variability in reported earnings; managers have motivation to reduce this variability. In this paper uncertainty business environment can be defined as the degree or variability to which an internal and external business’ environment can be predicted. Internal includes culture, policy and process. External includes social, legal, political and economic situation. The important objective of management is to maintain uncertainty of all business function. Earnings are the accounting number and summary statistic of a firm’s performance. Therefore, managers have incentive to manipulate report earnings and use their judgment in financial reporting. This implies that manager may exercise in all accounting policy and accounting methods to smooth their earnings for reducing uncertainty business environment. This leads to the following hypothesis as below: Hypothesis 12: The greater the degree of uncertainty business environments is, the more likely that the higher earnings management will be.

JOURNAL OF INTERNATIONAL FINANCE AND ECONOMICS, Volume 9, Number 3, 2009 12

4. RESEARCH DESIGN 4.1 Population and Sample Thai-listed firms are population and sample of this study because they are one of the emerging capital markets. The Stock Exchange of Thailand has been of interest to not only local investors but also to international investors. However, the information about the characteristic of stock market are a little. Key informant is accounting director or accounting controller or chief financial officer of each of Thai-listed firms. Database has been from The Stock Exchange of Thailand website: http://www.set.or.th. Based on this database, it shows 547 listed firms as of April 5, 2009. The twenty one provident and mutual funds, which non-listed firms, are excluded. Thus, the samples are remained 526 firms. 4.2 Data Collection This dissertation uses the questionnaire as an instrument to collect data from key participants similarly to Bruns and Merchant (1990); Clikeman and Henning (2000); Elias (2002); Kaplan (2001); Merchant and Rockness (1994);and Greenfield et al., (2008). The strength of these surveys is that they normally are able to examine a broader and more representative set of decision, settings, and actors. As mentioned above, a multi-item method to examine questions about EM is generally accepted (Libby and Seybert, 2008). The questionnaire is constructed by each of constructs’ definition and related literature and that designed on a five-point Likert scale. Before using to collect data, two academic experts verify and modify the instrument. Then, the pre-test technique is done by other sample in order to that the questionnaire is correctly measured of all construct. Questionnaires are sent to key participants of Thai listed company to provide data for this study via mail. Each package of instrument consists of a questionnaire and cover letter containing an explanation of the research as well as instructions for completing the data. Length of time for collect data is about 1 month. With regard to the questionnaire mailing, four mails were undeliverable because the changing address, the valid mailing was 522 firms, from which 97 responses were received and usable. Hence, the effective response rate was approximately 18.60 percent. 4.3 Test of Non-Response Bias To clearly non-response bias, this paper use t-test technique to compare early and late responses. The first half of received data is treated as early response and the half is treated as lately responses. The results shows that no significant imply that no different between early and lately responses. 4.4 Variable Measurements For study the EM as well as its consequences, antecedent, and restrains, all variables were obtained from the data collection. The variables measurements of dependent, independent, moderator, mediators are described as follow: 4.4.1 Dependent Variable Corporate transparency is measured using three items indicating firms present clearly information, and keep on the rule of business operation. 4.4.2 Independent Variables Unreasonable change in accounting policy is measured using three items asking key informant about how often change in accounting policy, and adjusts accounting principle back and forward. Wealth transfer misrepresentation is measured using four items indicating administrators concern about their private gain by not consideration priority, using information asymmetry advantage to transfer wealth for itself.

JOURNAL OF INTERNATIONAL FINANCE AND ECONOMICS, Volume 9, Number 3, 2009 13

Information distortion is measured by four items investigation firms change accounting structure such as core expense to other expense. In addition, asking respondent how often conflict with Certified Public Accountant (CPA) about accounting policy or addition disclosure. Corporate based concern of accounting choice is measured by four items exploration the level of firms applies the accounting standard for make earnings in order to have good performance. 4.4.3 Mediator Variables Financial reporting reliability is measured by four items. The scaling concerning information in financial reporting is materialized, natural, prepared based on standard. Stakeholder acceptance is measured by four items indicating firms were mentioned by stakeholder about its fairness, frankness, honesty, and responsibility to stakeholder as well as society. 4.4.4 Moderator Variable Social-minded awareness is measured by four items indicating social expects business using good governance, produce qualified goods or service, maintain environment, and responsibility to their stakeholder. 4.4.5 Restraining Variables Ethical executive behavior is measured by four items indicating the management persist in administration correctly, emphasize to the fairness in performance evaluation, and support and encourage their employee to follow rules, regulation. Accountant’s CSR-based practice is measured by four items asking the respondent about the level of the responsibility to the society of the accountant, the level of emphasis on professional ethics. Outstanding corporate culture is measured by four items investing firms give emphasis to the improvement continuously, aim to build up sustainable and emphasis to work clearly and can be checked in order to build up reliability for employees. Intense regulation force is measured by four items exploring the strictly, continuously of regulation and regulator. Moreover, the questionnaire concerned punishment, and altered and improved of regulation. 4.4.6 Antecedent Variable Uncertainty business environment is measure by four items exploring the level of uncertainty of economic, political status, technology and the competitors. 4.5 Reliability and Validity In order to clearly validity and reliability, cronbarch’s Alpha is used to prove the multi-item in order to measure the reliability of data. An alpha coefficient should be higher than 0.70 (Nunnally an Bernstein, 1994), to make sure internal consistency and the stability of instrument. For testing the validity, factor analysis is used to prove construct validity. The factor loading of each construct should present a value higher than 0.5 in order to ensure that construct validity of this study is tapped by items, as theorized (Hair et al., 2006). The results for factor loading and Cronbach’s alpha for multiple item scale are shown in Table 1. Table 1 show all variables have factor loading score between 0.520 – 0.965 implying that there is the construct validity. Moreover, the Cronbach’s alpha coefficients for each key variable are shown between 0.714 – 0.937. Therefore, the reliability of all variables is accepted. .

JOURNAL OF INTERNATIONAL FINANCE AND ECONOMICS, Volume 9, Number 3, 2009 14

Table 1: Results Of Factor Loadings And Cronbach Alpha Coefficients

Variables

Factor Loading

Cronbach’s Alpha

Earnings management (EM) Unreasonable Change in Accounting Policy (URA) Wealth Transfer Misrepresentation (WTM) Information Distortion (ID) Corporate Based concern of Accounting Choice (CBA) Financial Reporting Reliability (FRR) Stakeholder Acceptance (SA) Corporate Transparency (CT) Social-Minded Awareness (SMA) Ethical Executive Behavior (EEB) Accountant’s CSR-based Practice (ACP) Outstanding Corporate Culture (OCC) Intense Regulation Force (IRF) Uncertainty Business Environment (UBE)

0.709 – 0.917 0.781 – 0.863 0.629 – 0.857 0.774 – 0.962 0.829 – 0.869 0.677 – 0.911 0.879 – 0.905 0.916 – 0.963 0.788 – 0.906 0.883 – 0.901 0.855 – 0.965 0.889 – 0.927 0.812 – 0.912 0.520 – 0.810

0.863 0.761 0.714 0.879 0.855 0.780 0.910 0.937 0.866 0.915 0.934 0.919 0.869 0.711

4.6 Statistical Techniques Ordinary least squares (OLS) regression analysis is chosen to estimate coefficients affecting the influence of EM on financial reporting reliability, stakeholder acceptance and corporate transparency because all constructs are the metric scales. In order to meet this objective, the following equations are tested as below:

Equation 1: FRR = 1 - 1EM + 1 Equation 2: FRR = 2 - 2URA - 3WTM - 4ID - 5CBA + 2 Equation 3: SA = 3 - 6EM + 3 Equation 4 SA = 4 - 7URA - 8WTM - 9ID - 10CBA + 4 Equation 5 CT = 5 - 11EM + 5 Equation 6 CT = 6 - 12URA - 13WTM - 14ID - 15CBA + 6 Equation 7 CT = 7 + 16FRR + 17SA + 7 Equation 8 CT = 8 + 18FRR + 8 Equation 9 CT = 9 + 19SA + 9 Equation 10 CT = 10 + 20FRR + 21SMA + 22(FRR x SMA) + 10 Equation 11 CT = 11 + 23SA + 24SMA + 25(SA x SMA) + 11 Equation 12 EM = 12 - 26EEB - 27ACP - 28OCC - 29IRF + 30UBE + 12 Equation 13 EM = 13 - 31EEB + 13 Equation 14 EM = 14 - 32ACP + 14 Equation 15 EM = 15 - 33OCC + 15 Equation 16 EM = 16 - 34IRF + 16 Equation 17 EM = 17 + 35UBE + 17

Where; EM = Earnings Management CT = Corporate transparency URA = Unreasonable change in accounting policy SMA = Social-minded awareness WTM = Wealth transfer misrepresentation EEB = Ethical executive behavior ID = Information distortion ACP = Accountant’s CSR-based practice CBA = Corporate based concern of accounting choice OCC = Outstanding corporate culture FRR = Financial reporting reliability IRG = Intense regulation force SA = Stakeholder acceptance UBE = Uncertainty business environment

5. RESULTS AND DISCUSSION Descriptive statistics and correlation matrix for all variables are presented in table 2. To clearly multicorlinearlity problem, Variance Inflation Factor (VIF) is used to ensure the multicorlineraity problem

JOURNAL OF INTERNATIONAL FINANCE AND ECONOMICS, Volume 9, Number 3, 2009 15

and VIFs that well below the criterion of 10 (Neter, Wasserman, and Kutner, 1985). The results showed that VIFs range from 1.025 – 5.024, well below the cut-off, implying that all independent variables are not correlated with each other. Therefore, there is no multicolinearity problem in this study.

Table 2: Descriptive Statistics and Correlation Matrix Variables EM UCA WTM ID CBC FRR SAT CT SMA EEB ACP OCC IRF UBE Mean Standard deviation EM UCA WTM ID CBA FRR SA CT SMA EEB ACP OCC IRF UBE

1.583 0.566 1.000 .709** .857** .917** .883** .-.394** -.244* -.173 -.393** -.318** -.357** -.315** -.220* -.114

1.917 0.812 1.000 .469** .549** .467** -.219* -.091 -.055 -.287** -.159 -.151 -.160 -.207* -.156

1.618 0.682 1.000 .719** .681** -.316** -.176 -.122 -.352** -.274** -.342** -.264** -.208* -.083

1.250 0.531 1.000 .792** -.375** -.214* -.140 -.392** -.249 -.302** -.273** -.167 -.090

1.546 0.736 1.000 -.403** -323** -.252* -.294** -.377** -.388** -.350** -.172 -.069

4.415 0.673 1.000 .695** .653** .529** .642** .688** .670** .244* .159

4.103 0.656 1.0000 .914** .547** .779** .681** .774** .271** .127

4.082 0.688 1.000 .490** .740** .622** .716** .182 .136

4.121 0.653 1.000 .576** .561** .610** .477** .117

4.273 0.560 1.000 .782** .858** .301** .107

4.479 0.559 1.000 .818** .369** .096

4.270 0.641 1.000 .390** .067

3.696 0.640 1.000 .298

3.221 0.646 1.000

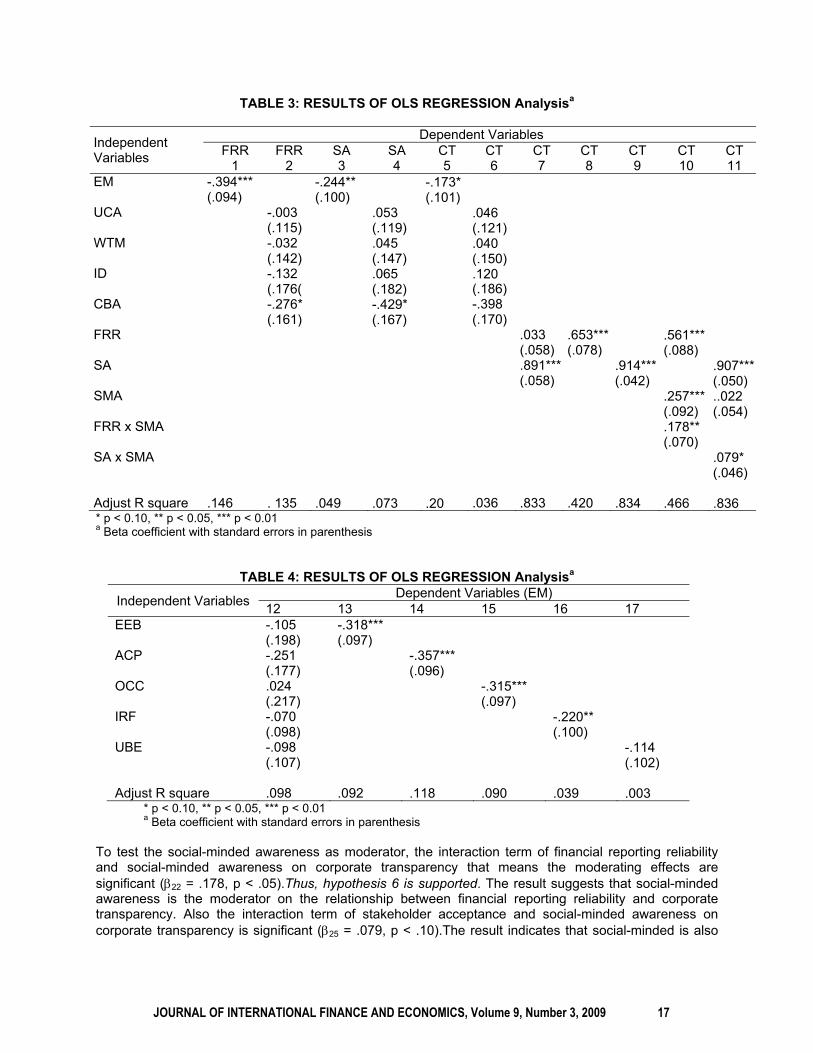

* Correlation is significant at the 0.05 level (2-tailed) * Correlation is significant at the 0.01 level (2-tailed) Table 3 presents the results of OLS regression analysis. As the first equation indicates that EM is negatively related with financial reporting reliability (1 = -.394, p < .01). Firms with higher degree of EM tend to have lower financial reporting reliability. Hence, hypothesis 1 is supported. In addition, the result shows that only one dimension of EM: corporate based concern of accounting choice has negative effect to financial reporting reliability (5 = -.276, p < .10). It indicates that the corporate based concern of accounting choice more influence on financial reporting reliability than other dimension. On the other hand, each of four dimensions separately affects the financial reporting reliability at higher significant level (all of them are investigated with one by one the results show negative sign at p < .01 but do not show in the table). Next, the third model presents that EM is negatively related with stakeholder acceptance (6 = -.244, p < .01). Firms which have the higher degree of EM tend to have lower stakeholder acceptance because EM is immoral and unethical that activity does not accept from stakeholder. Therefore, hypothesis 2 is supported. Moreover, the result shows that only one dimension of EM: corporate based concern of accounting choice has negative effect to stakeholder acceptance (10 = -.429, p < .10). However, each of four dimensions separately negative affects to stakeholder acceptance and the most have significant except unreasonable change in accounting policy is not significant. These results imply that if change in accounting policy within limit of standard (with in GAAP EM), stakeholder can be accepted. Predictable results in table 3, EM is negatively related with corporate transparency (11 = -.173, p < .10). Firms with high level of EM tend to have lower corporate transparency. Hence, hypothesis 3 is supported. Nevertheless, the results show that all dimensions have negative impact on corporate transparency but not significant. The reasonable discussions, the responses of this study are little and have effect on the power of test. To investigate the relationship among financial reporting reliability, stakeholder acceptance and corporate transparency models 7 – 9 are examined. Financial reporting reliability has positive impact on corporate transparency (18 = .653, p < .01). Then, hypothesis 4 is supported. The result indicates that firm with financial reporting is free form material error and bias gaining the higher level of transparency. In addition, stakeholder acceptance has positive relationship with corporate transparency (19 = .914, p < .01) Hence, hypothesis 5 is also supported. It implies that firms have the higher level of stakeholder acceptance they have gain corporate transparency.

JOURNAL OF INTERNATIONAL FINANCE AND ECONOMICS, Volume 9, Number 3, 2009 16

TABLE 3: RESULTS OF OLS REGRESSION Analysisa

Independent Variables

Dependent Variables FRR FRR SA SA CT CT CT CT CT CT CT

1 2 3 4 5 6 7 8 9 10 11 EM UCA WTM ID CBA FRR SA SMA FRR x SMA SA x SMA Adjust R square

-.394*** (.094) .146

-.003 (.115) -.032 (.142) -.132 (.176( -.276* (.161) . 135

-.244** (.100) .049

.053 (.119) .045 (.147) .065 (.182) -.429* (.167) .073

-.173* (.101) .20

.046 (.121) .040 (.150) .120 (.186) -.398 (.170) .036

.033 (.058) .891***(.058) .833

.653*** (.078) .420

.914***(.042) .834

.561***(.088) .257***(.092) .178** (.070) .466

.907***(.050) ..022 (.054) .079* (.046) .836

* p < 0.10, ** p < 0.05, *** p < 0.01 a Beta coefficient with standard errors in parenthesis

TABLE 4: RESULTS OF OLS REGRESSION Analysisa

Independent Variables Dependent Variables (EM)

12 13 14 15 16 17 EEB ACP OCC IRF UBE Adjust R square

-.105 (.198) -.251 (.177) .024 (.217) -.070 (.098) -.098 (.107) .098

-.318*** (.097) .092

-.357*** (.096) .118

-.315*** (.097) .090

-.220** (.100) .039

-.114 (.102) .003

* p < 0.10, ** p < 0.05, *** p < 0.01 a Beta coefficient with standard errors in parenthesis

To test the social-minded awareness as moderator, the interaction term of financial reporting reliability and social-minded awareness on corporate transparency that means the moderating effects are significant (22 = .178, p < .05).Thus, hypothesis 6 is supported. The result suggests that social-minded awareness is the moderator on the relationship between financial reporting reliability and corporate transparency. Also the interaction term of stakeholder acceptance and social-minded awareness on corporate transparency is significant (25 = .079, p < .10).The result indicates that social-minded is also

JOURNAL OF INTERNATIONAL FINANCE AND ECONOMICS, Volume 9, Number 3, 2009 17

the moderator which affects on the relationship between stakeholder acceptance and corporate transparency. Therefore, hypothesis 7 is also supported. In table 4 presents the examination of four restraining: ethical executive behavior, accountant’s CSR-based practice, outstanding corporate culture, and intense regulation force and uncertainty business environment as antecedent. All of four variables are the restraining of EM because they have negative effects: ethical executive behavior (31 = -.318, p < .01) consistent with Greenfield et al (2008) who state that manager with higher level of ethics and professional commitment seems to be less likely to engage in EM. Similar with Huang et al., (2008) who suggest ethical management and corporate governance reduction of abnormal accruals that means EM. Thus, hypothesis 8 is supported. Model 14 suggests Accountant’s CSR-based practice has negative relation with EM (32 = -.357, p < .01) consistent with Chih et al., (2008) who found CSR concept mitigate EM. Thus, hypothesis 9 is supported. For the role of outstanding corporate culture, the result shows the negative affects (33 = -.315, p < .01) consistent with Ussahawanitchakit (2002) who proposes the negative relationship between EM and organizational culture. Hence, hypothesis 10 is supported. Intense regulation force has negative affects on EM (34 = -.220, p < .05) consistent with Jeanjean and Stolowy (2008) who found the effects of the mandatory new standard (IFRS) limiting EM. Thus, hypothesis 11 is supported. According to models 13 – 16, accounting CSR-based practice has high beta coefficient (32 = -.357, p < .01) than others. It implies that accounting CSR-based practice is the most effective to restrain EM. However more surprisingly, uncertainty business environment is not significant (35 = -.114, p > .10). Hence, hypothesis 12 is not supported. This result implies that in this paper the uncertainty business environment focuses on economy, political, technology and competitor firms may use another technique to reduce the uncertainty such as improvement product or service, and investment in the technology. 6. IMPLICATION OF THE RESEARCH 6.1 Theoretical Implication and Future Directions for Research The objective of this paper is to investigate an intelligence of EM that has a significant direct negative impact on financial reporting reliability, stakeholder acceptance and corporate transparency. The study offers important theoretical contribution that is one of the first known studies to link among EM, financial reporting reliability, stakeholder acceptance and corporate transparency of Thai-listed firms. Next, this study aims at the first studies to treats social-minded awareness as the moderator under the context of Thailand. Moreover, this research also examines the ethical executive behavior, accountant’s CSR-based practice, outstanding corporate culture, and intense regulation force to restraining EM. 6.2 Practical Implication EM is significant and negatively associated with financial reporting reliability, stakeholder acceptance, and corporate transparency. Thus, firms which require building good image about transparency, building admire from stakeholder should avoid EM. In addition, financial reporting reliability and stakeholder acceptance are positively related with corporate transparency. Hence, Firms which build transparency should concern about accounting process in order to construct financial reporting free from material error and bias. Further, the results of this paper show that outstanding corporate culture is significant and negatively related with EM. Firms which concern the good reputation should support or encourage the concept of outstanding corporate culture such as concept of sustainability and concept of corporate governance in order to restrain EM. 6.3 Institution Implication Another implication for regulator, this study helps institution to determine and explain the methods to limitation EM. According to the results of this study, the force of regulator has negative effect on EM. Thus, regulator should be altered, improve the rule or standard in order to limit EM activity. Moreover, the ethics of manager and accountant is so important that education institute should be establishing beliefs, norms, ethic to students in order to solve problem in the long term.

JOURNAL OF INTERNATIONAL FINANCE AND ECONOMICS, Volume 9, Number 3, 2009 18

7. LIMITATIONS AND FUTURE RESEARCH DIRECTIONS This study focuses on the affect of EM on financial reporting reliability, stakeholder acceptance, and corporate transparency. Moreover, four dimensions of EM separately affect financial reporting reliability and stakeholder acceptance. Nevertheless, when four dimensions include at the one model, they do not influence on financial reporting reliability and stakeholder acceptance. Hence, these four dimensions should be integrated as EM that has more powerful influence on financial reporting reliability and stakeholder acceptance. However, future research should use other techniques such as structural equation model to test each of four dimensions for more description on how direct and indirect effects. With the regard to model 10, social-minded awareness is significant for testing moderating effect between financial reporting reliability and corporate transparency. Therefore, the future study should use social-minded awareness to the independent variable. In addition, this paper also investigates the antecedent of EM: uncertainty business environment but this variable is not significant. According to the results, the need for future research is apparent. Further, this research is chosen the financial reporting reliability to dependent variable of EM thus; future research should be choosing other qualitative characteristics of financial statements such as understandability, and comparability as the dependent variable. This study has several limitations, firstly the variable measures are new scale development, and future research wishes to explore the scale by different approaches in order to understanding of EM, financial reporting reliability, stakeholder acceptance and corporate transparency. Secondly, only the questionnaire is used to collect the data by mail survey. Thus, the empirical validity may be limited by biases. 8. CONCLUSION According to the important of accounting data, especially earnings which motivate firms to manipulate accounting number in order to mislead stakeholder decision making that means EM. It can be more serious and harmful activities because EM not only directly affect the overall integrity of financial reporting but also affect resource allocation in an economy. EM focus on short-term benefit, but long-term firm confronts with real economic situation to pass to go bankrupt in the end such as case of Enron, WorldCom, and Xerox that has impact on transparency, capital market trust, accounting professional acceptance, regulator role and standard-setters. This study investigates how EM affects financial reporting reliability, stakeholder acceptance and corporate transparency via social-minded awareness as moderator. EM consists of four dimensions: unreasonable change in accounting policy, wealth transfer misrepresentation, information distortion and corporate based concern of accounting choice. The overall results show the significant negative relationship among EM on financial reporting reliability, stakeholder acceptance, and corporate transparency. Moreover, the findings also indicate that social-minded awareness is the moderator of the relationship between financial reporting reliability and corporate transparency and between stakeholder acceptance and corporate transparency. Besides, four restraining variables; ethical executive behavior, accountant’s CSR-based practice, outstanding corporate culture, and intense regulation force have the negatively direct effect to EM. Surprisingly, uncertainty business environment is not the antecedent of EM that needs future research to apparently reconfirm. This study suggests that regulator should be improving the regulation and using the rule strictly. Moreover, education institute should be establishing beliefs, norms ethic in order to solve problem in the long term. REFERENCES: Akers, Mark D., Giacomino, Don E. and Bellovary, Jodi L., "Earnings management and Its Implications

Educating the Accounting Profession", The CPA Journal, Vol. august, 2007. Baber, William R., Chen, S. and Kang, S., "Stock Price Reaction to Evidence of Earnings Management:

Implications for Supplementary Financial Disclosure", Review of Accounting Studies, Vol. 11, 2006, 5-19.

Ball, Ray.J. and Brown, Philip, "An empirical evaluation of accounting income number", Journal of Accounting Research, Vol. 6, 1968, 159-178.