e r s t e g r o u p aafbr conference bucharest, november 2010 outlook on the cee region financial...

TRANSCRIPT

E R S T E G R O U P

AAFBR ConferenceBucharest, November 2010

Outlook on the CEE Region Financial Markets & Debt

Fritz Mostböck, CEFAHead of Group Research

E R S T E G R O U P

BucharestNovember 2010

AAFBR Conference2

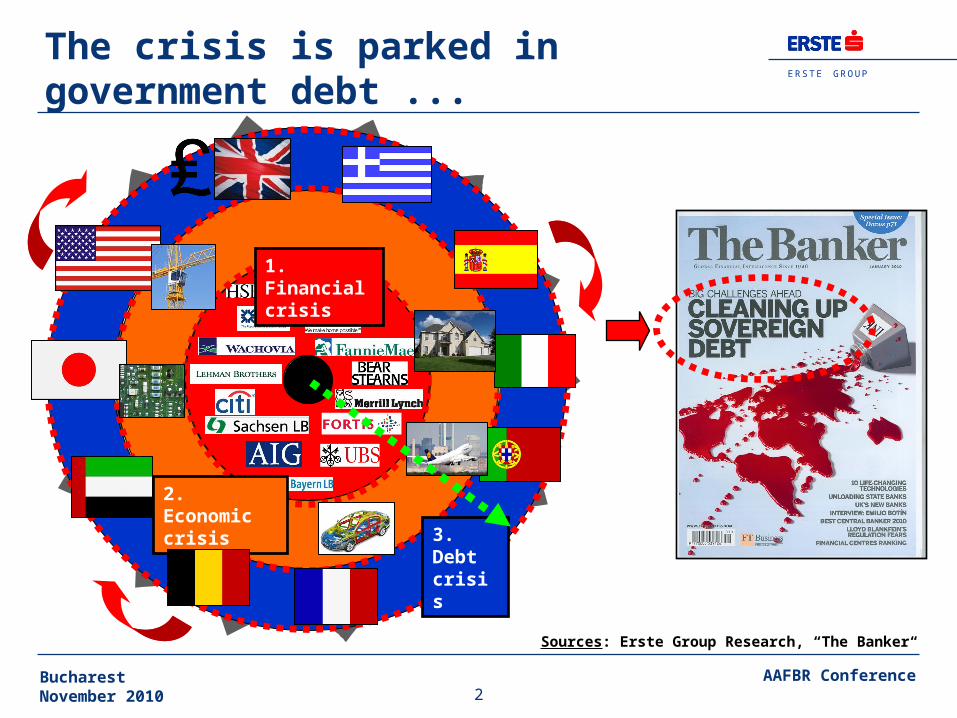

The crisis is parked in government debt ...

Sources: Erste Group Research, “The Banker“

2. Economic crisis

1. Financial crisis

3. Debt crisis

E R S T E G R O U P

BucharestNovember 2010

AAFBR Conference3

CEE: economy andgovernment debt

E R S T E G R O U P

BucharestNovember 2010

AAFBR Conference4

-18

-13

-8

-3

2

7

12

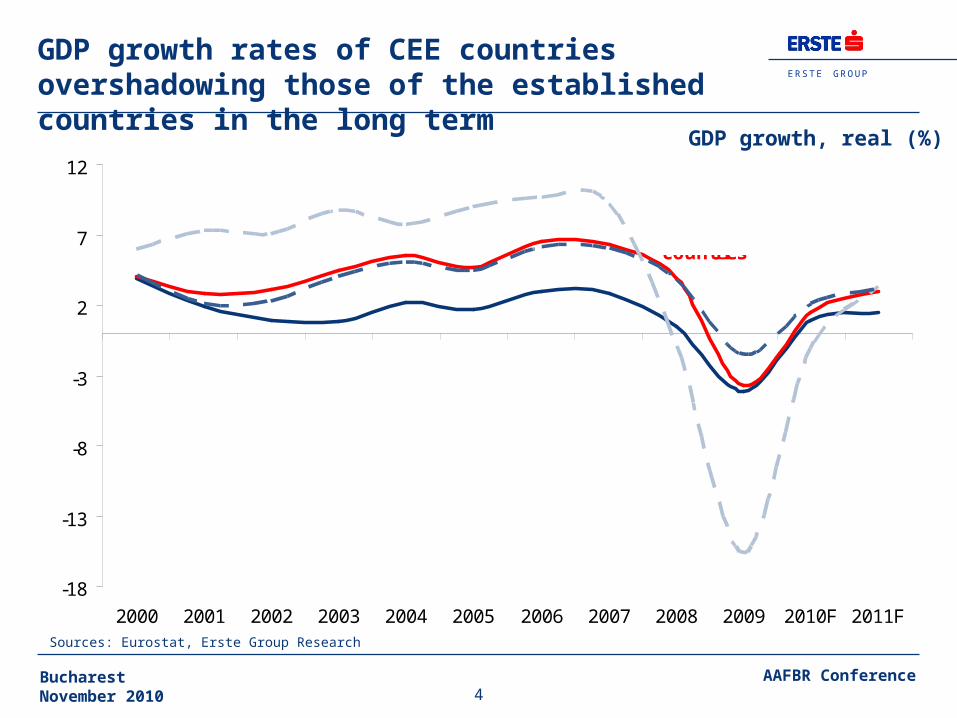

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010F 2011F

Euro Area

New EU membercountries

Baltics

Baltics

CEE4

Sources: Eurostat, Erste Group Research

GDP growth, real (%)

GDP growth rates of CEE countries overshadowing those of the established countries in the long term

E R S T E G R O U P

BucharestNovember 2010

AAFBR Conference5

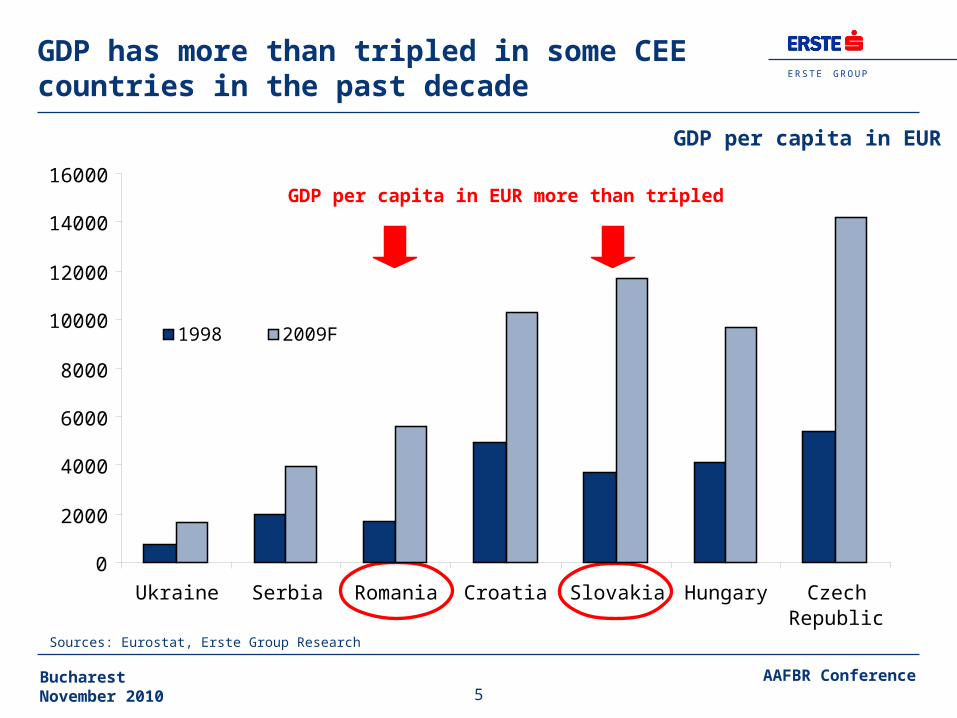

GDP has more than tripled in some CEE countries in the past decade

Sources: Eurostat, Erste Group Research

GDP per capita in EUR

0

2000

4000

6000

8000

10000

12000

14000

16000

Ukraine Serbia Romania Croatia Slovakia Hungary CzechRepublic

1998 2009F

GDP per capita in EUR more than tripled

E R S T E G R O U P

BucharestNovember 2010

AAFBR Conference6

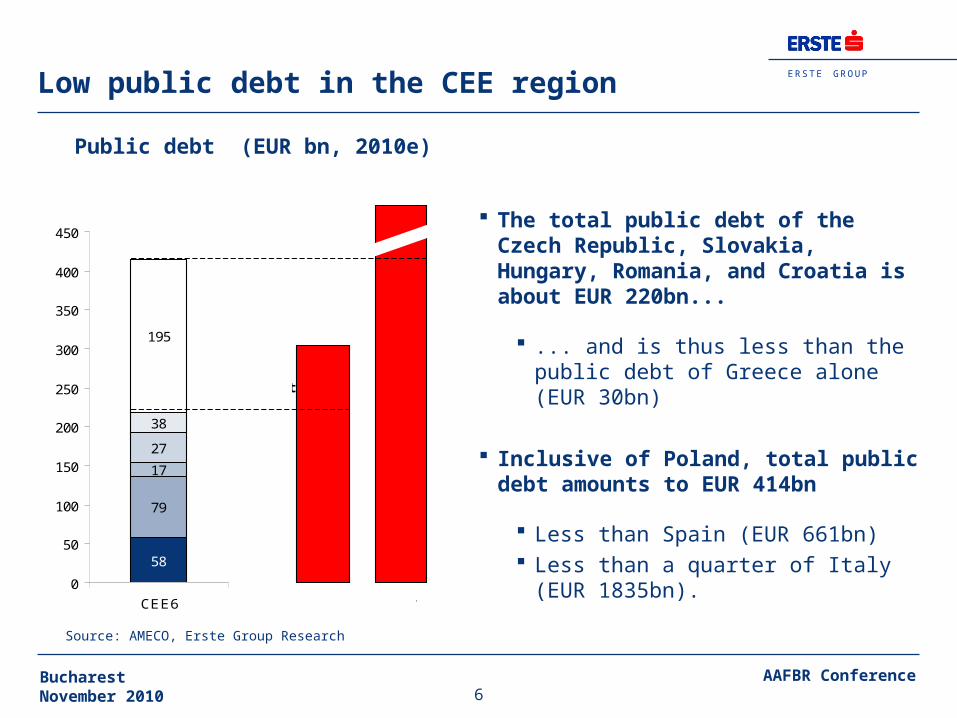

Source: AMECO, Erste Group Research

Public debt (EUR bn, 2010e)

Low public debt in the CEE region

The total public debt of the Czech Republic, Slovakia, Hungary, Romania, and Croatia is about EUR 220bn...

... and is thus less than the public debt of Greece alone (EUR 30bn)

Inclusive of Poland, total public debt amounts to EUR 414bn

Less than Spain (EUR 661bn) Less than a quarter of Italy (EUR

1835bn).

17

58

79

27

38

195

0

50

100

150

200

250

300

350

400

450

CEE6 Greece Italy

1835

300

CZ

HU

HR

SKRO

PLPublic debt excl. Poland is considerbably below the debt of Greece

CEE6 public debt is less than a quarter of Italy's

E R S T E G R O U P

BucharestNovember 2010

AAFBR Conference7

In terms of GDP, public debt is low and certainly (well) below the Eurozone average

All CEE countries except Hungary have maintained their aggregate debt below 60% of GDP

Hungarian debt is below the Eurozone average

The share of government bonds held outside the respective countries is relatively low in the CEE region

in CEE6 it accounts for about a quarter of public debt or 22-23% of GDP

In Greece the share accounts for two thirds of public debt or 90% of GDP

Public debt (in % of GDP, 2010e)

Sources: AMECO, JEDH, Erste Group Research

10

8,5

6,6

5

6,3

7,3

4

6,1

7,5

125118

9994

8685

7784

79

7979

70

6566

5551

574242

374040

3017

9.4

5.2

5

10

8.5

6.6

11.7

8

11.8

4

5

4.7

9.8

6.3

7.3

4

4.7

6.1

7.5

4.8

5.5

5.3

7.8

2.8

0 20 40 60 80 100 120 140

GreeceItaly

BelgiumUSA

Portugal

EurozoneIrland

FranceUK

HungaryGermany

Austria

SpainNetherlands

Poland

FinlandCroatia

SloveniaSlovakia

SerbiaUkraine

Czech Republic

RomaniaBulgaria

Debt Deficit

Euro Areaaverage (2010E)

Maastrichtlimit

E R S T E G R O U P

BucharestNovember 2010

AAFBR Conference8

Recovery clearly noticeable, but base level and speed are very mixed

Source: Erste Group Research

q/q GDP growth (%)

Differentiation between the various countries is therefore crucial, PL, CZ, and SK ahead, H and RO with a time lag / flatter development.

-2

-1.5

-1

-0.5

0

0.5

1

1.5

2

Hungary Romania Czech Republic Poland Slovakia

2Q09

3Q09

4Q09

1Q10

2Q10

Q310e

Q410e

E R S T E G R O U P

BucharestNovember 2010

AAFBR Conference9

Substantially lower cost of labour and solid growth of productivity

Cost of labour (inclusive of social

contributions) in CEE account for half

of those in Spain and a third of those in

Germany

This relation has even improved as a

consequence of the depreciation of

local currencies

ROE much higher in CEE because of

lower unit cost of labour

0 10 20 30 40 50

Romania

Poland

Hungary

Slovakia

CzechRepublic

Croatia

Portugal

Greece

Spain

Germany

2010

2009

2008

2007

Nominal compensation per employee (EUR ‘000)

Sourceds: AMECO, Erste Group Research

E R S T E G R O U P

BucharestNovember 2010

AAFBR Conference10

A glimpse at the growth figures

Sources: Eurostat, Erste Group Research

After the slump in GDP growth from 4% to -3.7% in 2009, we seem to be seeing a slight recovery in 2010 to +1.9% (EMU +1.6%), which should speed up to +2.9% (EMU +1.3%) in 2011.

The 2010 recovery has mainly come on the back of foreign trade

This contribution will subside in 2011, and the economic activity in the Eurozone should remain moderate

However, private consumption in the CEE region should record a clear rebound next

year

Risk factors Weaker Eurozone economy Stronger negative effects of the budget consolidation than anticipated

GDP growth (base scenario,%)

2009 2010 2011 2012

Croatia -5.8 -1.5 1.5 2.5

Czech Republic -4 2.2 2.0 2.8

Hungary -6.3 0.9 2.6 3.1

Poland 1.8 3.3 3.7 4.4

Romania -7.1 -3.0 1.2 2.3

Serbia -3 1.3 3.0 3.8

Slovakia -4.7 4.1 4.0 4.5

Ukraine -15.1 4.3 4.5 6.0

CEE8 - weighted average -3.7 1.9 2.9 3.1

Eurozone -4.1 1.6 1.3 1.6

E R S T E G R O U P

BucharestNovember 2010

AAFBR Conference11

Ytd performance equity markets

6,4%

35,3%-

8,2%

16,7%

30,6%

3,9%

0,9%-

7,3%

13,1%-

11,7%

1,8%-

9,9%-

8,0%-

9,4%-

27,0%

15,4%

11,6%

9,1%

24,4%

DOW JONES

NIKKEI 225

FTSE 100

DAX 30

CAC 40

IBEX 35

MIB INDEX

PORTUGAL

ATHEN 20

IRELAND

OMX COPENHAGEN

OMX STOCKHOLM

ATX

BUDAPEST (BUX)

WARSAW WIG

ROMANIA BET

UKRAINE PFTS

ISE ISTANBUL

PRAGUE PX

Source: Bloomberg, performances in local currencies as of 3rd, Nov 2010

International

Westeuropa

CEE

PIIGS Countries

Strong evidence for a link

between government debt and

YTD performance on the equity

markets

Investors are clearly

differentiating

The country approach is gaining

importance again relative to the

regional or sector approach

Debt will continue to burden

financial markets

E R S T E G R O U P

BucharestNovember 2010

AAFBR Conference12

CDS spreads have come back to normal levels, but Hungary and Romania are grappling with domestic (political) problems

Sources: Bloomberg, Erste Group Research

Sovereign credit default swaps (bps)

0

100

200

300

400

500

600

700

800

900

1000

Jan-

07

Mar

-07

May

-07

Jul-0

7

Sep

-07

Nov

-07

Jan-

08

Mar

-08

May

-08

Jul-0

8

Sep

-08

Nov

-08

Jan-

09

Mar

-09

May

-09

Jul-0

9

Sep

-09

Nov

-09

Jan-

10

Mar

-10

May

-10

Jul-1

0

Sep

-10

0

500

1000

1500

2000

2500

3000

3500

4000

4500

5000

Czech RepublicPolandHungaryRomaniaUkraine (rhs)Croatia

E R S T E G R O U P

AAFBR ConferenceBucharest, November 2010

Outlook on the CEE Region Financial Markets & Debt

Fritz Mostböck, CEFAHead of Group Research