dynamics of socio-economic systems: a physics perspective

TRANSCRIPT

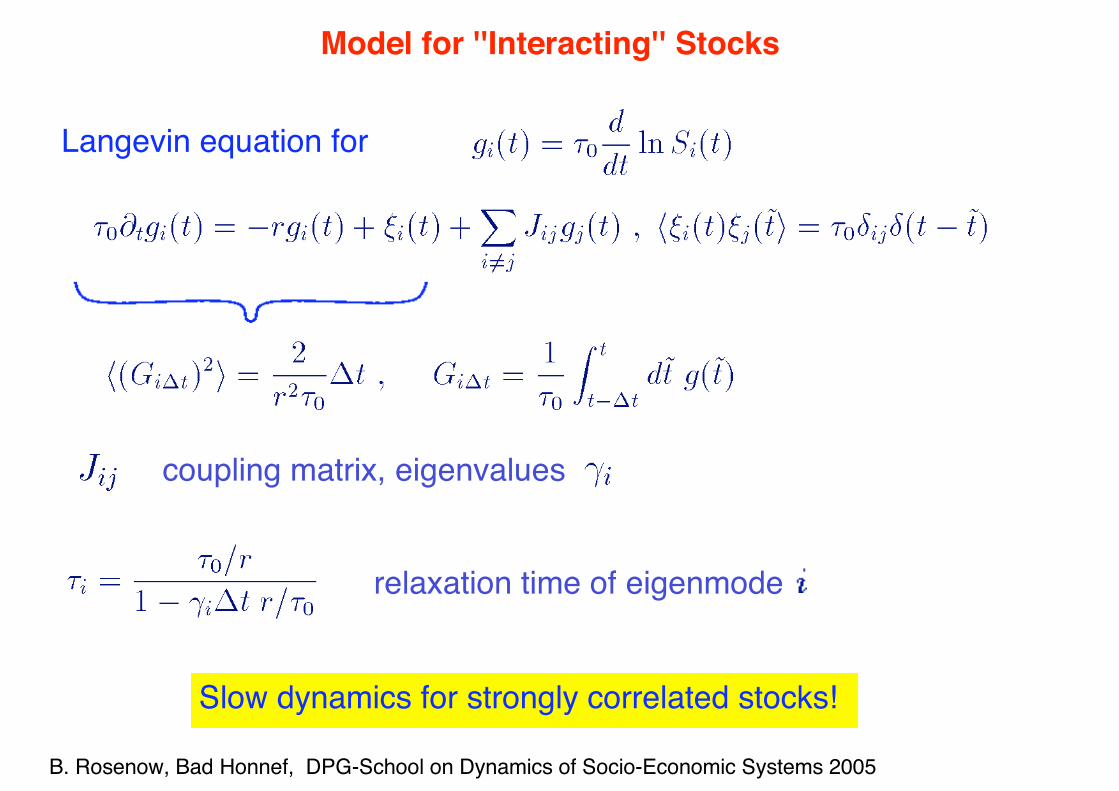

B. Rosenow, Bad Honnef, DPG-School on Dynamics of Socio-Economic Systems 2005

Lecture I:Random Matrix Theory for Financial Markets

Bernd Rosenow Harvard University

References: V. Plerou, P. Gopikrishnan, B. Rosenow, L. Amaral, and

H.E. Stanley, PRL 83, 1473 (1999).

P. Gopikrishnan, B. Rosenow, V. Plerou, and H.E. Stanley,

Phys. Rev. E 64, R035106 (2001).

V. Plerou et al., Phys. Rev. E 65, 066126 (2002).

B. Rosenow et al, Europhys. Lett. 59, 500 (2002).

Dynamics of Socio-Economic Systems: A Physics Perspective,September 19, 2005

Related work: L. Laloux, P.Cizeau, J.-P. Bouchaud and M. Potters, PRL. 83, 1469 (1999)

B. Rosenow, Bad Honnef, DPG-School on Dynamics of Socio-Economic Systems 2005

statistical mechanics!

many constituents

complex interactions

stock prices as macroscopic variables

Stock Market

B. Rosenow, Bad Honnef, DPG-School on Dynamics of Socio-Economic Systems 2005

Outline

• Description of cross-correlations in the stock market – analysis

with random matrix theory (RMT)

• Autocorrelations of correlated modes

• Time dependence of cross-correlations

• Application: optimal investments in the stock market

B. Rosenow, Bad Honnef, DPG-School on Dynamics of Socio-Economic Systems 2005

Long Term Capital Management

past correlations = future correlations?

NOT ALWAYS !

LTCM loss: 2,5 Milliarden $

B. Rosenow, Bad Honnef, DPG-School on Dynamics of Socio-Economic Systems 2005

Correlations and Interactions

stock pricechanges

stock market 1994-97

data points

1000 companies, i = 1,...,1000

t = 30 min

Correlations betweencompanies measured by

What to do with this huge (1,000,000 entries) matrix?

B. Rosenow, Bad Honnef, DPG-School on Dynamics of Socio-Economic Systems 2005

Nuclear Physics

Model calculationsfail!

Wigner: single energy levels not so important, study statistical properties

assumptions: real symmetric random Hamiltonian

prediction: distribution ofnearest neighbor distances s

s

B. Rosenow, Bad Honnef, DPG-School on Dynamics of Socio-Economic Systems 2005

Stock Market

s

eigenvalues of

no free parameter!

conclusion: up to now,

nuclear physics = economy

B. Rosenow, Bad Honnef, DPG-School on Dynamics of Socio-Economic Systems 2005

Eigenvalue Distribution

Compare eigenvalues of C to those of a random matrix R constructedfrom i.i.d. time series

agreement randomness deviations information

length of time series

number of time series

Laloux et al., '99, Plerou et al., '99

B. Rosenow, Bad Honnef, DPG-School on Dynamics of Socio-Economic Systems 2005

Computer Simulation with Octave

M = randn(400,200) generates 200 i.i.d. time series of length 400

C = corrcoef(M) calculates correlation coefficients

d = eig(C) calculates eigenvalues of C

x = linspace(0,5,500)

y = linspace(0,0,500)

for i=1:200, y= y + normal_pdf(x,d(i),0.001); end

y = y./200

plot(x,y)

B. Rosenow, Bad Honnef, DPG-School on Dynamics of Socio-Economic Systems 2005

Distribution of Eigenvector Components

RMT-prediction for distribution

Laloux et al., '99,Plerou et al., '99

B. Rosenow, Bad Honnef, DPG-School on Dynamics of Socio-Economic Systems 2005

Market Mode

Example: perfectly correlated returns

Construct portfolio

from eigenvector

and compare it to

S&P500 portfolio

Strong common component in stock prices: market

B. Rosenow, Bad Honnef, DPG-School on Dynamics of Socio-Economic Systems 2005

Industry Sectors

Construct map of the industry

Eigenvector has contribution

from industry

B. Rosenow, Bad Honnef, DPG-School on Dynamics of Socio-Economic Systems 2005

Interpretation of Deviating Eigenvectors

B. Rosenow, Bad Honnef, DPG-School on Dynamics of Socio-Economic Systems 2005

Model for stock price fluctuations

imbalance of supply and demand

noise correlator

return on microscopic time scale

with

dynamics of supply and demand

B. Rosenow, Bad Honnef, DPG-School on Dynamics of Socio-Economic Systems 2005

Model for ''Interacting'' Stocks

Langevin equation for

Slow dynamics for strongly correlated stocks!

coupling matrix, eigenvalues

relaxation time of eigenmode

B. Rosenow, Bad Honnef, DPG-School on Dynamics of Socio-Economic Systems 2005

Autocorrelation function

Power law correlations reminiscent of critical spin systems

Detrended fluctuation analysis:

• detrended fluctuation function

• without autocorrelations

• implies power law

correlations

Power Law Correlations

B. Rosenow, Bad Honnef, DPG-School on Dynamics of Socio-Economic Systems 2005

Are Correlations Stable?

period A period B

01/94 06/94 01/95

How to compare

eigenvectors and ?

(market) is very stable

stable for

980

990

B. Rosenow, Bad Honnef, DPG-School on Dynamics of Socio-Economic Systems 2005

Dynamics of the Correlation Strength

daily returns of 422 CRSP stocks, 1962-96

B. Rosenow, Bad Honnef, DPG-School on Dynamics of Socio-Economic Systems 2005

Optimal Investments

•One stock: return , risk

•Diversification into N stocks

•Optimal investment minimizes

interaction random field

Lagrange multipliers fix total return and total invested capital

B. Rosenow, Bad Honnef, DPG-School on Dynamics of Socio-Economic Systems 2005

Practical Implementation

estimation period A testing period B

01/94 06/94 01/95

• actually realized values

• three different estimates for

i) historical matrix

ii) filtered correlation matrix

iii) standard assumption

B. Rosenow, Bad Honnef, DPG-School on Dynamics of Socio-Economic Systems 2005

Accuracy of Risk Forecast

0.5 1 1.5 2 2.5 3

10

20

30

40

50

0.5 1 1.5 2 2.5 3

10

20

30

40

50

0.5 1 1.5 2 2.5 3

10

20

30

40

50

B. Rosenow, Bad Honnef, DPG-School on Dynamics of Socio-Economic Systems 2005

Risk Reduction

1.4 1.5 1.6 1.7 1.8 1.9 2

10

20

30

40

50

(Filtered)C

//(Control)C

Does RMT prediction work best?

construct

and transform back to original basis 1 10 20 30 40 50 60

1.5

1.52

1.54

1.56

1

1

1

1

Number of eigenvalues

Ris

k %

B. Rosenow, Bad Honnef, DPG-School on Dynamics of Socio-Economic Systems 2005

Random Ferromagnet

Futures Market: deposit coupled equations for signs

S. Galluccio et al., Physica A 257, 449 (1998)

• Spin glass problem for historical

• Random ferromagnet for filtered

only has large components, all other have

0

50

100

150

200

250

300

350

0 100 200 300 400 500 600 700 800 900 1000

line 1line 2

N s

0 500 1000

100

200

300

Rank of eigenvector

B. Rosenow, Bad Honnef, DPG-School on Dynamics of Socio-Economic Systems 2005

Conclusions

• meaningful correlations described by large eigenvalues of C

• portfolios defined by deviating eigenvectors have power law

autocorrelations

• correlations change in time

• Random matrix theory helps to reduce risk of optimal portfolios