dynamic product positioning in differentiated product - source

TRANSCRIPT

Dynamic Product Positioning in Di¤erentiated Product

Markets: The E¤ect of Fees for Musical Performance Rights

on the Commercial Radio Industry

Andrew Sweeting�

Duke University and NBER

January 2011

Abstract

This article investigates how product positioning decisions in the radio industry would be

a¤ected if, as has recently been proposed, music stations have to pay fees for musical performance

rights. A rich dynamic model, which captures many features of the industry such as multi-

station ownership, economies of scope and both vertical and horizontal product di¤erentiation,

is formulated, estimated and (approximately) re-solved for di¤erent levels of fee, by applying

the method of parametric policy function iteration in the context of a dynamic game. The

estimated model predicts that fees could have substantial e¤ects on product positioning. For

example, if music stations have to pay 10% of their revenues as performance fees - which would

be consistent with the fees currently paid by cable and satellite providers - the number of music

stations would fall by 11% over a 15 year period. The article also considers how industry

characteristics such as heterogeneous listener tastes, multi-station ownership and substantial

repositioning costs a¤ect the size and speed of adjustment.

�Please send comments to [email protected]. I would like to thank Jerry Hausman, Igal Hendel, Aviv Nevo, AmilPetrin, Ariel Pakes, Rob Porter, Steve Berry, Pat Bayer, Peter Arcidiacono, Kate Ho, Allan Collard-Wexler, PaulEllickson, Arie Beresteanu, three referees and seminar participants for valuable comments. I would like to thankthe National Association of Broadcasters and the Center for the Study of Industrial Organization at NorthwesternUniversity for �nancial support. All errors are my own.

1

1 Introduction

While we have many tools to help us understand static pricing decisions in di¤erentiated product

markets, we know relatively little about what determines the set of products that are o¤ered. This

is unfortunate because this margin may be more important for consumer welfare and government

policies often intentionally or unintentionally a¤ect �rms�incentives to sell particular types of prod-

uct. For example, gasoline taxes, fuel e¢ ciency standards and trade policies a¤ect the incentives

of domestic automakers to produce particular types of vehicles (Berry et al. (1993)), while taxes,

labelling and advertising restrictions increasingly a¤ect the incentives of �rms making or selling food

and beverages to o¤er healthier products (Wang (2010)). The e¤ects of these policies will likely

depend on industry characteristics such as consumers� tastes for variety, ownership concentration

and the costs that �rms have to incur to develop new products or reposition their existing ones.

In most settings, accurately predicting a policy�s e¤ects will also require a dynamic model because

�rms will typically expect to sell products for several years, and their incentives to develop particular

types of products may depend on how their competitors might change their assortment decisions in

response.1

This article estimates a dynamic oligopoly model of the broadcast radio industry to understand

how the set of available products would be a¤ected by proposed legislation that would levy potentially

large performance rights fees on music stations.2 Historically, broadcast stations in the United States

have paid fees to the owners of composition rights (i.e., composers and music writers), but not the

owners of performance rights (musicians, performers and record labels), based on the argument that

owners of performance rights bene�t from increased sales of recordings and concert tickets when their

music is played on the radio. However, this position is anomalous as cable, satellite and internet

stations pay both types of fees, as do broadcast stations in most other countries. Under pressure

from the recording industry, legislation has been introduced into both houses of Congress (H.R. 848

and S. 379, 111th Congress), with support from the Obama Administration and members of both

1Of course, dynamics may be less important when assortment or positioning change frequently (e.g., Mazzeo et al.(2009) and Fan (2010)).

2Some earlier work has focused on vertical di¤erentiation. For example, Aguirregabiria et al. (2007) and Macieira(2007) estimate a dynamic models where �rms choose product quality but, unlike in the current paper, there is nosystematic horizontal di¤erentiation. Beresteanu et al. (2010) estimate a dynamic game with two types of grocery�rm that make capacity choices in each market, but �rms are unable to choose their type.

2

major political parties, to require commercial broadcast stations to pay for performance rights.3 The

broadcast radio industry also provides an excellent setting for studying �rms�positioning decisions

as we are able to observe the formats of several thousand stations in di¤erent local markets, and,

even in the absence of performance fees, changes in demand and competition lead to many observed

format switches in the data.

While the proposed legislation left the level of fees to be determined by negotiation or, in the

absence of agreement, by copyright judges, precedent suggests that these fees, charged as a % of

revenues, would be much larger than the 2-3% fees typically paid for composition rights. For example,

copyright judges recently determined that satellite radio company XM Sirius should pay 7-8% of its

total subscription revenues (including those for non-music programming) for performance rights for

2010-12, a fee level which included a discount recognizing the fact that satellite radio was struggling

to become established.4 Companies providing audio programming on cable pay 15% of revenues.5

Some experts on media law have predicted that copyright judges might approve fees as high as 25%

of revenues for broadcast music radio stations.6 Not surprisingly, the broadcast radio industry has

argued that fees at this level would have devastating e¤ects. One of its principal arguments has been

that even small fees would cause many stations to switch to non-music programming, which could

have the perverse e¤ect of harming the music industry if performers do bene�t from airplay.7 As

these types of fee have never been levied before and the radio industry in the US is quite di¤erent

from the radio industries in the rest of the world, where public broadcasters or content regulations

are much more important, it is impossible to evaluate this claim based on historical experience alone.

The substantive aims of this article are therefore to predict how station format decisions would

3The House Judiciary Committee voted for the draft bill 21-9 with the no votes coming primarily from Republicanmembers who wanted further study of the e¤ects of the legislation on the broadcast radio and music industries. Forexample, Lamar Smith, the ranking Republican member, asked that �the parties agree to have a third party entityconduct an objective study of the economic impact of royalty payments on performing artists and radio stations.�(ThePerformance Rights Act, Hearing Before the Committee on the Judiciary, House of Representatives, 111th Congress,1st session on HR 848, March 10, 2009, Statement of Lamar Smith). The Government Accountability O¢ ce made itsreport (US GAO (2010)) to Congress in August 2010.

4Federal Register vol. 75, p. 5513 (2010-02-03).5Federal Register vol. 75, p. 14075 (2010-03-24).6See for example, http://www.broadcastlawblog.com/2010/03/articles/music-rights/copyright-royalty-board-

approves-settlement-for-sound-recording-royalty-rates-for-new-subscription-services-any-hints-as-to-what-a-broadcast-performance-royalty-would-be/ (accessed December 5, 2010).

7For example, the National Association of Broadcasters Radio Board Chairman, Steven Newberry, stated beforethe House Judiciary committee that �the number of stations playing music would dramatically decrease�because ofthe Act (The Performance Rights Act, Hearing Before the Committee on the Judiciary, House of Representatives,111th Congress, 1st session on HR 848, March 10, 2009, Oral Testimony of Steven Newberry).

3

change under di¤erent fee levels, and to understand how important features of the industry, such as

consumers tastes for variety and multiple station ownership, in�uence the e¤ects of fees.

To achieve these substantive goals, I formulate and estimate a rich dynamic discrete choice game

where radio companies choose their stations�formats. The model allows for many important features

of the industry including: horizontal (format) and vertical (quality) di¤erentiation between stations,

heterogeneity in listeners� tastes for di¤erent types of programming and in advertisers�values for

di¤erent types of listeners, multiple station ownership and economies of scope from operating similar

stations, and the existence of costs to changing station formats. Many of these features may a¤ect

how the industry responds when performance fees are introduced. For example, repositioning costs

may a¤ect how many music stations want to switch formats and the speed of adjustment, while

heterogeneity in listeners�tastes a¤ect how listeners are redistributed across stations when a music

station switches to a non-music format. If many listeners have a strong preference for music pro-

gramming, the audience of the remaining music stations will increase, reducing their incentives to

move.

Under the assumption that future innovations in station quality are unknown when format choices

are made, I can consistently estimate static models describing listener and advertiser tastes in a �rst

stage. The results show that heterogeneity in the tastes of each group are important. I estimate

the remaining parameters of the model, which describe station repositioning costs and economies

of scope, by combining Aguirregabiria and Mira�s (2007, AM hereafter) Nested Pseudo-Likelihood

(NPL) procedure with parametric policy function iteration (PPI), assuming that the �rms�value

functions can be accurately approximated using a particular function of the state variables. I also

use the PPI approach to re-solve the model in order to predict what would happen for di¤erent

levels of fee, for di¤erent parameters and ownership structures. PPI has been used to approximately

solve and estimate the parameters of rich dynamic single agent models in the economics literature

(Benitez-Silva et al. (2005), Nevo and Hendel (2006)) and dynamic programming problems outside

of economics (Bertsekas (2010)), but it has not been used to solve dynamic games where multiple

agents interact. To provide evidence that these methods can be used e¤ectively in the game context,

I present extensive Monte Carlo results using a simpli�ed, but still quite rich, version of my model

that can be solved exactly. I use the example to show that my estimation procedure can recover

the parameters without signi�cant bias and that when PPI is used to perform a counterfactual

4

experiment, both the short-run and long-run e¤ects of format-speci�c fees on product positioning

can be predicted accurately.

The estimated parameters indicate that format repositioning costs are quite large especially for

stations with many listeners, which re�ects the value of stations�relationships with existing listeners

and advertisers, as many of these relationships are lost when a station changes formats. As a result,

the format structure of the industry evolves quite slowly when fees are introduced. For example, a

fee equal to 10% of revenues is predicted to reduce the number of music stations by 6.1%, 9.9% and

11.0% after 5, 10 and 15 years respectively relative to the no fee case, while music radio audiences

would fall by 4.7%, 5.6% and 5.9% over the same time period. If listeners had more homogenous

tastes for di¤erent types of programming, more stations would switch to non-music programming

when fees are introduced and the declines in the number of people listening to music radio would be

larger. Lower repositioning costs would cause a similar long-run adjustment to happen more quickly.

Multi-station ownership, a common feature of the modern radio industry, tends to lead to a faster

adjustment than independent ownership, as independent owners may delay moving in the hope that

one of their competitors will pay the repositioning cost and restore the pro�tability of the remaining

music stations.

1.1 Related Literature

The paper is related to both the methodological literature on the solution and estimation of dynamic

discrete choice models, and the growing literature on understanding product positioning and the

e¤ects of ownership consolidation in the commercial radio industry.

1.1.1 Dynamic Games

I consider a discrete time, dynamic game with a very rich state space (re�ecting station characteristics,

station ownership and local market characteristics), where �rms simultaneously make discrete choices

about how to arrange their stations across formats for the next period. I estimate the parameters

of the model using �rms�choices in an environment with no performance rights fees, and then re-

solve the model to see how the industry would change if fees are imposed. Following most of the

dynamic games literature, I make assumptions that allow me to consistently estimate the parameters

describing listeners�and advertisers�tastes in a �rst stage, with the remaining parameters estimated

5

using the dynamic model.

Aguirregabiria and Nevo (2010) provide a review of the literature on estimating dynamic games.

Several papers, including Pakes et al. (2007), Bajari et al. (2007), Pesendorfer and Schmidt-Dengler

(2008) and Arcidiacono and Miller (2010), have proposed two-step methods for estimating games

which may be too complicated to solve even once.8 However, these methods su¤er from �nite sample

biases in large games and they do not provide a method for performing counterfactuals. AM�s NPL

procedure, imposes more of the structure of the model during estimation which can substantially

reduce bias (Kasahara and Shimotsu (2009)), and application of the iterative procedure with �xed

parameters, which corresponds to policy function iteration, provides a natural approach to re-solve

the model. However, the NPL algorithm has only been used to estimate games with a relatively

small number of discrete states (e.g., Aguirregabiria and Ho (2009)). In my setting, the state space

required to model the industry in a plausible way is too rich to approximate it with a small number of

states, and many of the state variables are naturally continuous.9 I therefore assume that �rms�value

functions can be accurately approximated using a linear parametric function of the state variables,

and a simulation method for numerically integrating over future states. The method of �parametric

policy function iteration�, generalized to a game setting, can then be used to approximately solve the

game, and the method can also be used as a step within an iteration of the NPL estimation procedure.

I present Monte Carlo evidence that these methods can work well, even with quite simple functions

of the state variables, using a simpli�ed version of my model which can be solved exactly. The

application of various approximation methods in the context of single-agent dynamic programming

problems has been an active area of research outside of economics (see, for example, Bertsekas (2010),

Bertsekas and Yu (2007) and Bertsekas and Io¤e (1996) which contains an application to the game

Tetris with over 2200 states), and some degree of approximation will always be necessary when state

variables are continuous (Benitez-Silva et al. (2000)).10

8Some counterfactuals can be assessed using forward simulation and the estimated choice probabilities. Forexample, Benkard et al. (2010) use this approach to simulate the e¤ects of additional mergers in the airline industry.

9Nevo and Rossi (2008) suggest a method, implemented by Macieira (2007), for reducing the size of the state spacewhen there are multi-product �rms and consumers�preferences can be represented by a pure logit model, so that theydo not have systematic preferences for particular types of horizontally di¤erentiated product. This approach cannotbe used here where horizontal di¤erentiation is important.10Bertsekas (2010) and Ma and Powell (2009) discuss various convergence results for approximate dynamic program-

ming algorithms where the underlying problem is a contraction, which is not the case for a dynamic game. As notedby Benitez-Silva et al. (2000) accurate approximation of the value function will depend on payo¤s being a smoothfunction of the state variables. Keane and Wolpin (1994) provide an approach to using simulation and interpolationto solve and estimate �nite horizon dynamic programming models that has been widely applied in the labor literature.

6

The possible existence of multiple equilibria may a¤ect both the estimation of dynamic games

(Pesendorfer and Schmidt-Dengler (2008) and Su and Judd (2010)) and the simulation of counterfac-

tuals where it is impossible to know for sure which equilibrium would be played when the parameters

are changed. I discuss issues concerning equilibrium selection when presenting the empirical results

and counterfactuals.

1.1.2 Product Positioning in the Radio Industry

Several recent articles have examined the e¤ects of ownership consolidation on product positioning

and pricing in the radio industry, looking at the period of rapid ownership consolidation that followed

the 1996 Telecommunications Act. Berry andWaldfogel (2001) and Sweeting (2010) provide evidence

on how owners within local markets tend to di¤erentiate their stations, focusing on �ner classi�cations

in programming than are used here. Using my coarser programming classi�cation, owners have a

tendency to cluster their stations, consistent with the existence of economies of scope. O�Gorman

and Smith (2008) and Mooney (2010a) estimate static models to estimate economies of scope from

operating stations in the same market and economies of scope from operating similar stations in

di¤erent markets respectively, �nding evidence that both can be large. I estimate economies of scope

from operating multiple stations in the same format in the same market and in di¤erent markets using

a dynamic model. Jeziorski (2009) considers the e¤ects of mergers on future product positioning

using forward simulation using conditional choice probabilities estimated from the existing data.

That approach is not possible for counterfactuals that are unlike changes observed in the data.

I use a reduced form revenue function to estimate stations�revenues as a function of demographics,

station ownership and competition. Mooney (2010b) and Jeziorski (2010) estimate static structural

models of the radio advertising market to investigate the e¤ects of consolidation on the advertising

market, �nding evidence that consolidation leads to either slightly more or slightly less commercials

being played respectively. The estimated coe¢ cients of my revenue function also indicate small

e¤ects of ownership. A more restrictive modelling assumption in the current article is that owners

are assumed to treat the current ownership, but not format, structure of the industry as �xed when

they take forward looking decisions about how to position their stations. This assumption is clearly

imperfect because station transactions occur in the data. However, I focus on the years 2002-2005,

when the rapid consolidation that followed the 1996 Act had come to an end. At the cost of additional

7

computation, it would be possible to incorporate a model of endogenous ownership changes within

the current framework.

1.2 Format Switching: An Example

To readers who are not familiar with the radio industry, it may not be obvious what factors lead

stations to change formats and why format changes can be expensive, so I now provide an example

based on the experience of one (anonymous) company that I have spoken to. In 2007 the �rm owned

an FM Adult Contemporary station and an FM Country station in one mid-sized local market, with

annual revenues of around $10 million and $4 million respectively. The Country station had a

relatively weak signal, which could not be upgraded due to potential interference with other stations,

so when another station moved into Country, the �rm decided that it would need to switch the

Country station to a di¤erent format. Its �rst action was to hire consultants to evaluate its options

based on local tastes and current competition, and they recommended switching to either Religious

or Sports programming. The �rm then spent six months investigating each of these possibilities,

including negotiating for possible syndication rights in each format. At this point the �rm chose

Sports, even though it could not initially secure its preferred syndication rights, moving the station

approximately 3 months after the decision was taken. During these three months, it played Rock

music, which Country listeners tend to dislike, in order to reduce the number of complaints that would

be made when it �nally moved into Sports and to confuse competitors about the �rm�s intentions.

The �rm also replaced all of the station�s on-air sta¤, all of its advertising sales sta¤ (because Sports

stations appeal to di¤erent advertisers than Country) and hired a new general manager for the

station. Once the station switched to Sports, it aired fewer commercials for several months while

it developed a new base of advertisers, a feature which I will capture by allowing a �rm�s revenues

per listener to fall for one period following a format switch. The �rm expected that the station

would have more listeners than before its switch after 6 months (in reality it took 2 years to meet

this target), and that it would take �at least two years for the move to pay for itself�.

1.3 Outline

The paper is structured as follows. Section 2 describes the data and Section 3 presents the model.

Section 4 explains how the model is approximately solved using a parametric approximation to the

8

value function and parametric policy function iteration. Section 5 describes the estimation procedure.

Monte Carlo results are presented in the Appendix. Section 6 presents the coe¢ cient estimates,

and Section 7 describes the counterfactual experiments. Section 8 concludes.

2 Data

This section describes the data used to estimate the model, and some stylized facts that motivate

the rest of the analysis. The data is taken from BIAfn�s MediaAccessPro database (BIA Financial

Network (2006)) unless otherwise noted.

2.1 Sample Markets, Periods and Stations

I estimate the model using data from a sample of local radio markets. Consistent with industry

practice, I use the local geographic markets de�ned by the Arbitron Company for estimating station

audiences, and in many cases these markets correspond to Metropolitan Statistical Areas. The

sample markets were chosen using three criteria. First, I exclude markets where stations based in

other Arbitron markets have more than a combined 6% share of commercial radio listening in order

to avoid modelling how much revenues stations derive from each market.11 Second, I exclude the

ten largest radio markets from the sample. These markets have as many as 49 commercial stations

each, and including them raises the computational burden signi�cantly as well as introducing some

additional concerns about variation in tastes across markets.12 Third, I use markets which were

surveyed by Arbitron in every Spring and Fall quarter from Spring 2002 to Spring 2005, the ratings

periods used in estimation.13 In my model, a period will be one of these six month periods. The

�nal sample consists of 102 markets, ranging in size from Caspar, WY (with 55,000 people aged 12

and above in 2002) to Atlanta, GA (3.4 million). Based on BIAfn�s estimates, these markets had

advertising revenues of approximately $5.5 billion in 2004.

11Stations typically derive most of their revenues from their home market, as local, but not regional or national,advertisers primarily value local residents.12For example, New York City historically has had no Country music stations even though based on some format

classi�cations this is the most popular format in the US. In contrast, smaller markets close to New York, such asAlbany, which are included in the sample, have a distribution of stations across formats which is much more similarto the rest of the US.13I use the Spring and Fall quarters for all markets, even though Arbitron also collects data in the Winter and

Summer quarters in larger markets.

9

BIAfn lists each station�s on air date and indicates whether it was active each quarter. De novo

entry and permanent exit in the broadcast radio industry are rare. During the sample only one

station closes permanently, which re�ects the fact that licences are scarce, and it is much easier to

buy an existing, if struggling, station than to receive an entirely new license from the FCC.14 55

stations (approximately 0.09 stations per market per quarter) begin operating during the sample,

while 40 stations go temporarily o¤-air before returning. As entry and exit are not important

phenomena in this industry, I simplify the model by assuming that �rms optimize treating the set of

stations that will operate in the future as �xed, although some of these stations may go temporarily

o¤-air (located in the �Dark�format). If it was important, a model of the entry and exit process

could be added to the model at the cost of additional computation.

A limitation of the data is that market share information is not available for non-commercial

stations and commercial stations that fail to meet Arbitron�s minimum ratings standard (MRS,

which typically requires 0.3% of radio listening) in a given quarter. I focus my analysis on non-

marginal commercial stations by excluding all non-commercial stations (approximately 18% of all

stations) and active stations that fail to meet the MRS in at least 4 sample periods (approximately

3% of the commercial stations). This means that the �rms in my model will ignore the current

and future existence of these stations. These deletions leave a sample of 2,378 stations, or 16,543

station-market-period observations.

2.2 Station Audiences and Revenues

During the period of the data, Arbitron estimated the audiences of commercial stations using diaries

completed by a sample of listeners. A station�s reported market share (the AQH in industry jargon)

is the station�s share of radio listening by people aged 12 and above during an average quarter hour

in a broadcast week of Monday to Sunday 6am to midnight. Consistent with industry practice, any

listening by people younger than 12 is ignored for the rest of the paper. These market shares are

converted into shares of the time potentially available for radio listening by using Arbitron�s APR

number, which measures the average proportion of time that people spend listening to radio during

the broadcast week, and an assumption that each person has at most 6 hours per day to listen to

14More generally, exit in the radio industry often occurs for non-economic reasons such as the death of a stationowner or the revocation of a license by the FCC due to breaches of FCC regulations.

10

the radio, compared with average realized listening of 2 hours per day.15 The outside good in the

demand model will include time spent listening to non-commercial stations and stations which are

dropped because they are too small, as well as time spent not listening to the radio. I impute market

shares for stations which are included in the sample, but fail to meet the MRS in a particular quarter,

by assuming that their AQH shares were 10 percent below the smallest AQH share which Arbitron

did report for the market in that quarter.

AQH shares are averages across demographics, and demographic-speci�c shares may di¤er sig-

ni�cantly across formats which appeal to di¤erent types of listener. Identi�cation of di¤erences

in listener tastes across demographics is aided by using average listening patterns for di¤erent de-

mographic groups reported in Arbitron�s 2003-2006 Radio Today publications, which are based on

Arbitron�s surveys in the Spring quarter of the preceding year in a known subset of markets. Data

on the proportion of each market�s population which is in each of 18 mutually exclusive demographic

groups (the product of three age categories (12-24, 25-49 and 50 plus), two gender categories and

three ethnic racial/categories (black, white and Hispanic)) are calculated for each quarter from the

US Census�s County Population Estimates, aggregated to the market level using Arbitron�s market

de�nitions.16

BIAfn estimates annual station advertising revenues using a proprietary formula.17 These es-

timates are available for 96% of station-years in the sample. BIAfn�s revenue numbers are widely

cited within the industry, so they are likely to be useful for approximating how revenues per listener

di¤er across markets and across di¤erent types of listener, which is how they are used here.

2.3 Station Formats and Observed Characteristics

I model stations as either being o¤-air or being located in exactly one active format per quarter.

Modelling programming in discrete formats is consistent with industry practice, although exact pro-

15The APR number is not reported in MediaAccessPro. However, I was able to collect it from M Street�s STARdatabase for 2002 and Spring 2003 and BIAfn were able to provide me with these numbers from Fall 2004. The APRsfor Fall 2003 and Spring 2004 were interpolated which is a reasonable approach as they change very slowly over time.16The County Population Estimates are calculated for July each year. I choose to assign these to the Spring quarter

and use linear interpolation to �nd estimates for the Fall. My estimation of the process by which demographics evolveexplicitly addresses the fact that I only observe demographics every other period.17About 80% of radio advertising revenues come from local (as opposed to regional or national) advertisers. Unfor-

tunately very little is known about how station ownership has a¤ected the balance of local and national advertisingor how this may a¤ect BIAfn�s revenue estimates.

11

Table 1: Format AggregationIncluding BIAfn Number of Station-Quarters

Aggregated Format Format Categories AM Stations FM Stations1 AC/CHR/Rock Adult Contemporary, 64 5,944

Contemporary Hit Radio,Rock, AOR/Classic Rock

2. Country Country 233 1,8073. Urban Urban, Black Gospel (part of Religious) 616 1,155

4. News/Talk News, Talk, Sports 2,551 2565. Spanish Spanish-language 490 514

6. Other Programming Oldies, Easy Listening, Classical, Jazz, 972 1,893Big Band, Variety, Religious (non-Gospel)

gramming categorizations di¤er across sources.18 MediaAccessPro lists a very speci�c format for

each station - there are several hundred of these and they are based on the station�s own description

- and also places each station in one of twenty format categories. To reduce the number of choices

available for each station, I aggregate these 20 categories into the six active formats listed in Table 1.

While this aggregation results in an unbalanced distribution of stations across formats, it was chosen

because it captures important di¤erences in programming tastes across demographics. For example,

Urban and Spanish programming appeal strongly to black and Hispanics respectively, and markets

with very low black or Hispanic populations often have no stations in these formats. News/Talk

stations attract more male listeners, while stations in the Other Programming format attract older

listeners. Most AM stations are in the News/Talk format and very few are in contemporary mu-

sic formats as signal quality is less important for non-music programming. The largest category

(�AC/CHR/Rock�) contains formats which are broadly popular across all markets and attract largely

white audiences under 50. To perform the counterfactual, I assume that performance fees would

be levied on stations in the �rst three formats. This will not be exactly correct as some Spanish-

language and Other Programming stations which primarily play music would also have to pay fees

(stations which only play limited amounts of music were exempted in the draft legislation). However,

it may be straightforward for these stations to switch to less musical programming while maintaining

audiences with similar demographics, so I use this simpli�cation in order to retain a relatively simple

18A music station may play (say) a Country music song without being in the Country format. A format re�ects theoverall programming genre of the station. A relatively small number of commercial stations do truly mix formats (e.g.,talk in the morning, music in the afternoon) and for these stations I base my categorization on the format reportedby MediaAccessPro.

12

format structure. Stations observed as o¤-air are placed in the non-active �Dark�format, and I place

stations that enter during the data into the Dark format in the period before they are �rst on-air.19

Stations in the same market-format can have quite di¤erent market shares. I allow for these

di¤erences to be explained by several observable variables, speci�cally AM band*format interactions,

the proportion of the market�s population covered by the station�s signal (interacted with the station�s

band), an �out of market�dummy for whether the station is based outside the geographic boundaries

of the local market (e.g., in the surrounding countryside) and a dummy for whether the station has

an imputed share in one or more periods. With the exception of the format interactions, �rms treat

these characteristics as permanent and �xed. While this ignores the possibility of physical capital

investment, it is a reasonable approximation to the data where less than 1% of stations change signal

strength or tower height between 2002 and 2006. MediaAccessPro provides data on current and

historical station ownership. I assign ownership to the �rm that owns the station at the end of the

period.

2.4 Summary Statistics and Stylized Facts

Table 2 contains summary statistics on the market and station variables. The sample markets di¤er

widely in their populations, racial composition, total revenues and number of stations. Average

revenues per capita also vary across markets (mean $68.20, standard deviation $16.59, minimum

$34.76, maximum $116.97). On average, a �rm operates 2.5 stations, with the number varying from

1 to 8. Market shares and revenues also di¤er signi�cantly across stations within a market: in both

cases, within-market standard deviations are greater than between market standard deviations. For

this reason it is important to allow for both observed and unobserved heterogeneity in station quality.

The top section of Table 3 provides some summary statistics on format switching, based on the

sample markets. The years 2002-5 are used in estimation, but the table shows statistics for 1996�

2000 and 2001 as a comparison. Throughout the decade, 3-4% of stations switch formats per period.

The switching rates are similar across small and large markets, even though average station revenues

are almost 4.5 times larger in the large market group. This suggests that format repositioning costs

may also be larger in larger markets. Independent stations are slightly more likely to switch than

19This treatment will obviously a¤ect the estimated level of costs for moves from Dark to active formats. However, itshould not directly a¤ect the estimates of the costs of switching between active formats which are key for the analysis.

13

Table2:SummaryStatistics

MarketCharacteristics

Variable

Observations

Mean

Std.Dev.Min.

Max.

(market-periods)

Numberofstationsinmarket

714

23.2

5.8

1138

Numberofdi¤erentstationownersinmarket

714

9.4

3.2

318

Population(12andabove,inmillions)

714

0.733

0.747

0.055

3.683

Proportionofpopulationblack

714

0.119

0.124

0.002

0.502

ProportionofpopulationHispanic

714

0.091

0.130

0.005

0.793

Combinedlisteningtosamplestations(%

oftotalmarket20)

714

37.2

3.5

24.9

47.9

BIAfnEstimatedAnnualMarketAdvertisingRevenues(2002-2005,$m.)

408

53.5

66.0

3.9

403.7

StationCharacteristics

Variable

Observations

Mean

Std.Dev.Min.

Max.

(station-periods)

Marketshare(includesdarkstations)

16,543

1.6%

1.4%

011.3%

BIAfnEstimatedAdvertisingrevenues(station-year2002-2004,$000s)

6,413

2,438

3,702

2545,550

Dummyforstationlocatedoutsidemarketboundaries

16,543

0.061

0.240

01

DummyforAMband

16,543

0.299

0.458

01

Proportionofmarketcoveredbysignal(outofmarketstationsexcluded)21

15,526

0.786

0.358

0.003

1.1

Dummyforstationhasimputedmarketshareinatleastonequarter

16,543

0.147

0.354

01

Thetotalmarketincludestheoutsidegoodofnotlisteningtoradioandlisteningtonon-commercialandcommercialnon-samplestations.Market

de�nitionallowsforeachindividualtospendupto6hourslisteningtotheradiobetween6amandmidnight.

Signalcoverageisde�nedrelativetothemarketpopulationandIcapitat1.1toaddressoutliersthatappearedtodistortthedemandestimates.

14

Table3:SummaryStatisticsonFormatSwitchingandOwnership

FormatSwitching 1996-2000

2001

2002

2003

2004

2005

FormatSwitchingRate(perstation-quarter)

4.0%

3.4%

3.0%

3.7%

2.9%

3.4%

FormatSwitchingRateinMarketswith2001Population>1million

3.3%

3.9%

2.7%

3.4%

2.5%

4.3%

FormatSwitchingRateinMarketswith2001Population

�1million

4.3%

3.1%

3.2%

3.8%

3.1%

2.9%

Mean(Std.Dev.)MarketShareforSwitchingStation

50.4%

45.8%

54.3%

67.0%

56.6%

63.5%

as%ofmarketaverageshare

(51.8%)

(50.8%)(52.9%)(70.8%)(52.0%)(53.1%)

SwitchingRateforIndependentStations

4.8%

5.4%

4.2%

4.1%

3.9%

4.0%

SwitchingRateforStationsinLocalClusterswith2-3Stations

4.0%

3.5%

2.4%

3.0%

2.3%

2.0%

SwitchingRateforStationsinLocalClustersof>3Stations

3.4%

2.6%

2.8%

3.8%

2.8%

3.2%

Ownership

1996-2000

2001

2002

2003

2004

2005

%ofStationsA¤ectedByOwnershipChanges

16.1%

17.2%

5.8%

5.8%

6.1%

4.6%

MeanLocalMarketOwnershipConcentration(HHI,audienceshares)

0.249

0.274

0.276

0.275

0.286

0.287

ProbabilitythatTwoRandomlyChosenStationsareintheSameFormat:

StationsinSameLocalMarketwithDi¤erentOwners

0.20

0.21

0.22

0.22

0.21

0.21

StationsinSameLocalMarketwithSameOwner

0.28

0.28

0.29

0.29

0.29

0.29

StationsinDi¤erentLocalMarketswithDi¤erentOwners

0.20

0.21

0.22

0.21

0.21

0.21

StationsinDi¤erentLocalMarketswithSameOwner

0.27

0.28

0.28

0.29

0.29

0.28

15

Figure 1: Distribution of Year-to-Year Changes in Market Share (Listeners) for Switching and Non-Switching Stations

3 2 1 0 1 2 3 4 50

0.2

0.4

0.6

0.8

1

1.2

1.4

Share Change in One Year (Percentage Point)

Ker

nel D

ensi

ty E

stim

ate

Switching StationNonSwitching Station

stations owned by multi-station �rms.

The bottom section of the table provides some additional information about ownership. During

the sample years, fewer stations changed ownership than in earlier years. Randomly selected pairs

of stations owned by the same �rm are more likely to be in the same format, which suggests that

economies of scope may be realized by operating similar stations. This is true whether one looks at

pairs of stations in the same market or di¤erent markets, suggesting that economies of scope from

operating similar stations may exist at both levels.

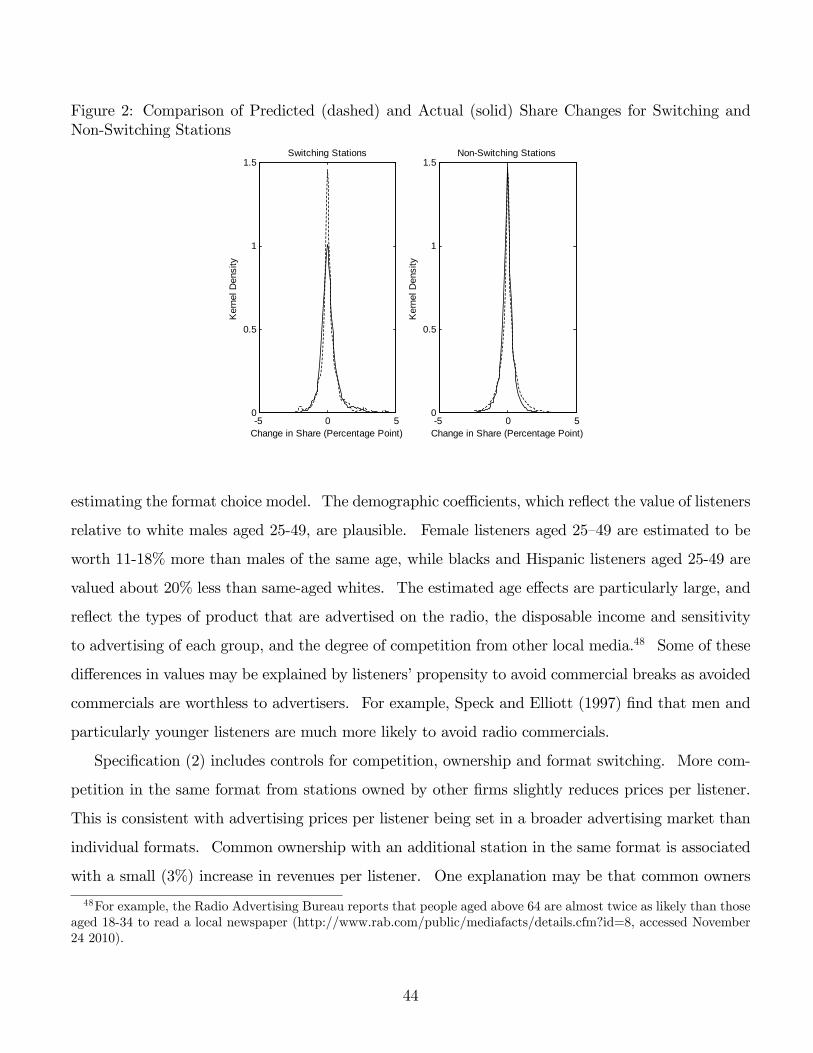

Figure 1 shows how the market shares of stations which switch formats change in the following

year, compared with stations that do not switch. Switching stations tend to gain listeners, and the

average gain is 32% of the average pre-switch market share. It is also interesting to note that few

switching stations experience large declines in market shares. This fact favors a model where station

quality can be predictably transferred across formats, rather than a model where stations receive

completely new, and unpredictable, draws on quality when they switch.

Table 4 shows the frequency with which switches are made between pairs of active formats. In all

formats, stations are much more likely to remain than to switch. Stations leaving News/Talk, Other

Programming or Spanish are more likely to switch to another non-music format, which re�ects the

16

Table 4: Format Switching Matrixformat in period t+ 1

AC Country Urban/Gospel News/Talk Other Prog. SpanishAC/CHR/Rock 0.975 0.004 0.005 0.003 0.009 0.002

format Country 0.013 0.963 0.003 0.007 0.005 0.006in period Urban/Gospel 0.007 0.003 0.974 0.008 0.005 0.003

t News/Talk 0.003 0.003 0.001 0.982 0.006 0.004Other Programming 0.023 0.007 0.006 0.014 0.941 0.006

Spanish 0.003 0.002 0.001 0.008 0.004 0.982

behavior of AM stations, but otherwise there are few obvious patterns. In estimation I will assume

that the cost of switching between any pair of active formats is the same, although this cost may

vary across stations and markets.

3 Model

In this section I describe the empirical model, and discuss the rationale for some of the restrictive

assumptions that I make.

3.1 Overview and Notation

Stations are observed in a set of local markets m = 1; :::;M; and play an in�nite horizon discrete

time game with periods t = 1; :::;1. A market has observable characteristics Xmt which include

population size, demographic composition based on 18 age-gender-race/ethnicity groups, population

growth rates and the value of each listener to advertisers. The players are a set of �local �rms�

o = 1; :::O. o owns a set of stations So in a particular local market m(o). As noted in the

Introduction, �rms optimize assuming that the current period�s ownership structure will remain the

same in the future so that any ownership changes that occur would be unexpected surprises. Stations

owned by the same company (e.g., Clear Channel) in di¤erent local markets will be controlled by

separate players in my game, but I explain below how I allow for cross-market economies of scope to

a¤ect format choices. Each station has observable characteristics Xst. Characteristics such as signal

coverage and whether the station is located outside market boundaries will be treated as �xed while

the band-format interactions can vary with format choices. Each station also has a one-dimensional

17

level of time-varying quality �st that is orthogonal to these observed characteristics. Xst and �st

capture vertical di¤erentiation between stations.

The set of players and stations are assumed to remain the same over time, so that there is no

new entry, permanent exit or changes in ownership. Each period local �rms generate revenues by

selling their stations�audiences to advertisers, and pay �xed costs so that their stations can operate.

Station audiences are determined by the size and demographic make-up of the market, station quality

characteristics (vertical di¤erentiation) and station programming formats (horizontal di¤erentiation).

There are F = 0; 1; :::; 6 discrete formats, where format 0 is the Dark (temporarily o¤-air) format.

Each station is in exactly one format each period, where Fst is a vector which indicates the format

of station s. To describe economies of scope from operating stations in the same format, F o;m(o)ft will

be a count of the number of local stations that o has in format f , and F o;m0

ft will be a count of the

number of stations in format f and market m0 that have the same corporate owner as o. The Xmt,

Xst; �st and ownership and format variables in all markets are observed by all �rms andMt denotes

these features of the state space at time t.

In the game, �rms choose the formats of their stations for the next period (they are not able

to take any other type of action). Aot denotes the discrete set of actions (next period choices)

available to o, and aot the chosen action. To place a limit on the size of the choice sets, I assume

that each �rm can move at most one station per period. Each possible action is associated with

a private information, iid payo¤ shock "ot(aot; �"o(Mt)). These shocks will be distributed Type

1 extreme value with location parameter 0 and scale parameter �"o(Mt) which can depend on o�s

observed characteristics. Market demographics and the �sts, which are continuous state variables,

evolve stochastically over time according to AR(1) processes and �rms cannot a¤ect how they evolve,

except that �st can change discretely when a format switch is made. Advertising values and listener

preferences are assumed to stay the same over time.

3.2 Timing

Within each period t; the timing of the game is as follows:

1. �rms observeMt;

2. �rms pay �xed costs Co(Mt)�C for the current period (i.e., a function of state variables that

18

are linear in parameters). These costs are a¤ected by local and cross-market economies of

scope;

3. �rms observe the private information shocks "ot to their payo¤s from each choice and simulta-

neously and irreversibly make their choices aot;

4. �rms receive revenuesP

s2So Rs(Mtj ), pay any repositioning costsWo(aot;Mt)�W and receive

the payo¤ shock "ot(aot; �"o(Mt)) associated with their format choices. are parameters of

the static listener demand system and advertising revenue functions. These parameters can

be estimated separately from the various � parameters that are estimated using the dynamic

model. A �rm�s total current period payo¤s are therefore

�ot(aot;Mt; �; ) + "ot(aot; �"o(Mt)) (1)

=Xs2So

Rs(Mtj )| {z }Period t Advertising Revenues

� Co(Mt)�C| {z }

Fixed Operating Costs

�Wo(aot;Mt)�W| {z }

Repositioning Costs

+ "ot(aot; �"o(Mt))| {z }

Payo¤ Shock For aot

5. Mt evolves to Mt+1, re�ecting �rms�format choices, and the stochastic evolution of market

demographics and station qualities.

3.3 Components of the Per-Period Payo¤ Function

I now describe each component of the payo¤ function.

3.3.1 Station Revenues (Rs(Mtj ))

A station�s revenues are determined by a listener demand model, which determines howmany listeners

a station has in each demographic group, and a revenue function, which determines the value of each

listener to the station.

Listener Demand A station�s audience in each of 18 demographic groups is determined by a

static, discrete choice random coe¢ cients logit model as a function of the state variables in its own

market. Each consumer i in this market chooses at most one station, and i�s utility if she listens to

19

non-Dark station s is

uist = Xst S + Fst(

F + Fi ) + �st + "List (2)

= �st(Fst; Xst; S; F ; �st) + Fst

Fi + "List (3)

where �st is the �mean utility�of the station for a consumer with baseline demographics (white, male,

aged 12-24) and "List is an iid logit shock to individual preferences. Xst and �st are assumed to enter

the preferences of all consumers in the same way. �st allows stations with the same observed charac-

teristics to have di¤erent market shares, and while it is orthogonal to observed market characteristics,

the values of �st can be backed out from the estimated demand model. F are the average format

tastes of baseline consumers. Individual deviations from these preferences are

Fi = FDDi + �vFi (4)

where the �rst term re�ects systematic demographic preferences (additively separable age, ethnicity

and gender e¤ects) and vFi is a vector of draws from independent standard normals. The parameter

� determines the heterogeneity in format preferences within a demographic group, and it is assumed

to be the same across formats. A consumer receives utility of "Li0t if she chooses the outside good

(i.e., she does not listen to one of the commercial radio stations in my model).

This is a rich speci�cation, but it makes two signi�cant simpli�cations. First, consumers are

assumed to choose at most one station, whereas in reality people listen to several stations for di¤erent

lengths of time during a period (ratings quarter). This is a common simpli�cation when using

aggregate data (e.g., Nevo (2001)) and it can be rationalized as a representation of consumers�

preferences during shorter time periods, which are aggregated to give period market shares. This

representation is adequate if stations and advertisers are indi¤erent between audiences of the same

size made up of either a few people who listen a lot, or a lot of people who listen a little, and this

is consistent with average quarter hour (AQH) shares being the ratings number that are most used

by advertisers. Second, the model is entirely static, whereas listening habits might make shares

adjust slowly to quality or format changes. This simpli�cation seems reasonable given my focus on

major format changes, which are likely to cause any listener to change her habits, and six-month

time periods, which are likely to be longer than the time required for listeners to adjust.

20

Revenues Per Listener I assume that station s�s revenues for a listener with demographics Dd

are determined by a parametric function

rsmt(Dd) = m(1 + Ysmt Y )(1 +Dd d) (5)

where m is a market �xed e¤ect and d allows listeners with di¤erent characteristics to be more

or less valued by advertisers. In order to allow for format switching and market structure to a¤ect

revenues, the variables in Y include the number of other stations that the �rm has in the format, the

number of other stations in the format and a dummy variable for whether the station switched formats

in the previous period. I also allow for revenues per listener to depend on the station�s aggregate

market share, as work in the broadcast television industry has shown that larger stations achieve

higher revenues per viewer per minute of commercial time (Fisher et al. (1980)). Total station

revenues Rs(Mtj ) are calculated by multiplying the number of listeners in each demographic group

by these prices.

3.3.2 Repositioning Costs (Wo(aot;Mt)�W )

A local �rm has to pay a repositioning cost when it moves a station to a new format. I allow

repositioning costs to depend on whether the potential move is between active formats or to or from

the Dark format, total market revenues22, the revenues of the station being moved and whether the

station switched formats in the previous period. Because I estimate a cost for all possible moves, it

is not possible to also estimate a common �xed cost that stations pay to be active.23

3.3.3 Fixed Costs and Economies of Scope (Co(Mt)�C)

I assume that active stations pay �xed costs. The level of costs that is common across formats is

not identi�ed, but, using the positioning decisions of multi-station �rms, I can estimate the value of

22Speci�cally this variable equals market revenues per percentage point of radio listening during the years that themarket is observed in the data. Results using total population are similar, but I prefer the revenue measure as itshould also re�ect some di¤erences in input prices across markets, as well as population.23One could assume that the cost of switching to Dark is zero and then estimate the �xed cost of being active.

However, switches to Dark are rare, so that estimated �xed costs could be negative. Instead, I estimate a cost ofswitching to Dark which can be interpreted as a re�ection of the fact that when a station goes o¤-air it will lose thegoodwill of all of its existing listeners and advertisers, not just those who would leave the station if it switched to adi¤erent active format.

21

economies of scope that arise when a �rm operates several stations in the same format. For local

market economies of scope, I allow each station�s �xed costs to fall linearly with the number of other

stations that the local �rm has in the same format. These should re�ect e¢ ciencies achieved in pro-

gramming and selling commercials to advertisers with similar preferences. Cross-market economies

of scope are modelled with a non-linear speci�cation because the number of a¢ liated stations in other

markets can be very large (maximum in the data is 232). I assume that a local �rm is rewarded (by

the corporate owner) for the contemporaneous externality that its format con�guration has for local

�rms in other markets, and, taking this into account, o�s total bene�t from cross-market economies

of scope is proportional to24

Xf

0BBBBBB@Fo;m(o)ft log

�1 + F oft � F

o;m(o)ft

�| {z }cost reduction for local �rm�s own stations

+

Xj 6=m(o)

F o;jft

�log(1 + F oft � F o;jft )� log(1 + F oft � F o;jft � F

o;m(o)ft )

�| {z }

externality on stations in other markets with the same corporate owner

1CCCCCCA (6)

where F o;m(o)ft is the number of stations o has in format f in its own market in period t, and F oft =

Fo;m(o)ft +

P8j 6=m(o) F

o;jft is the total number of stations across markets in format f with the same

corporate owner.

3.3.4 Payo¤ Shocks ("ot(aot; �"o(Mt)))

Firms receive iid (across �rms and over time) private information shocks to their payo¤s from each

possible format choice, including keeping stations in the same format. These shocks are drawn from

a Type 1 extreme value distribution with location parameter 0 and scale parameter �"o(Mt): The

scale parameter is identi�ed in my setting because revenues are treated as observed and all costs are

assumed to be �xed. I allow the scale parameter to depend on both a constant and the revenues of

the local �rm in the current period.25 The revenue e¤ect should be identi�ed by how much �rms

24See Aguirregibiria and Ho (2009) for an alternative, and still fairly simple, way to model network externalities,applied to the airline industry. Note that I calculate this function based on only the sample markets.25It is important to allow for the scale of the payo¤ shocks to vary across �rms because �rms have quite di¤erent

expected future revenues depending on the size of the market and the number and quality of stations owned. With noscaling, choice probabilities exceptionally close to 0 or 1 tend to be predicted for either high or low revenue �rms. Ihave also experimented with allowing the scale of the shocks to also depend directly on the number of stations owned.Unfortunately the pseudo-likelihood minimization procedure often performed poorly in this case.

22

with di¤erent revenues tend to switch and how predictable their chosen format switches are (based

on predicted future values).26 The interpretation of these payo¤ shocks are factors that a¤ect the

format choices of �rms that are not captured by expected revenues or costs. For example, the �rm

described in Section 1.2 was attracted to Sports partly because the �rm had some non-radio interests

in managing sports facilities so it knew more about the types of advertisers that might be attracted

to a Sports station. The assumptions that payo¤ shocks are private information and independent

over time (serial independence) are necessary for tractability. The example does provides anecdotal

support for the private information assumption by illustrating how �rms may want to keep their

intentions hidden from competitors.27

3.4 Evolution of the State Variables

At the end of period t, the state variables evolve for the following period. Station formats change

deterministically with �rms�choices. Unobserved station quality is assumed to evolve according to

an AR(1) process with normally distributed innovations that are iid across stations

�st = ���st�1 + ��st if Fst = Fst+1 (7)

= ���st�1 + ��st � � if Fst 6= Fst+1 (8)

where ��st � N(0; �2v�): The � term allows for a change in station quality when it changes format.

An important assumption, which allows consistent �rst-stage estimation of the demand model when

format choices are endogenous to qualities, is that no �rm knows the v�st+1 innovations when they

make format choices in period t, so that there can be no selection into di¤erent formats based on

these innovations. In contrast, there can be selection based on the prior level of the �s. I show that

this model of quality innovations allows me to match the distribution of observed share changes in the

data. If it was assumed that �rms knew the innovations in quality when choosing these formats, it

would be necessary to adopt a di¤erent approach to estimation of listener demand, possibly involving

26Note that I assume that repositioning costs vary with the current revenues of the station that would be moved(which can therefore di¤er across choices), not the current total revenues of the �rm (that are common across choices).27A standard objection to the private information assumption in static models (e.g., Seim (2006)) is that it can lead

to �rms experiencing ex-post regret, because, for example, more �rms choose the same location than was expected.However, in my model the rate of switching is relatively low and in the data it is relatively rare for two �rms in thesame market to make switches that would have a large impact on the expected pro�tability of each other�s switch. Ina dynamic model �rms are also able to quickly reverse choices that turn out to be particularly sub-optimal.

23

the joint estimation of the demand and format choice models which would create an exceptionally

large computational burden.

While listener demand depends on 18 mutually exclusive age-gender-ethnic/racial groups it is

cumbersome to model the evolution of each of these groups independently. Instead, I model the

growth rate for each ethnic/racial group (white, black and Hispanic) and assume that the same

growth rate applies to each of the associated age-gender groups. I assume that for ethnic group e

log

�popmetpopmet�1

�= � 0 + � 1 log

�popmetpopmet�1

�+ umet (9)

which allows population growth for particular groups to have the serial correlation that we observe in

the data.28 This particular speci�cation also lets me address the problem that population estimates

are annual.

3.5 Value Functions and Equilibrium Concept

Following the empirical literature on dynamic games, I assume that �rms play a stationary and

anonymous pure strategy Markov Perfect Nash Equilibrium (MPNE).29 A stationary Markov Perfect

strategy �o is a mapping from (Mt; "ot) to actions aot that does not depend on t; and � is the set

of strategies for all �rms in all states. V �o (Mt; "ot) de�nes a �rm�s value in a particular state when

it uses an optimal strategy and other �rms use strategies de�ned in �. Dropping notation for the

parameters, by Bellman�s optimality principle

V �o (Mt; "ot) = max

aot2Aot

24 �(aot;Mt) + "ot(aot;Mt)+

�RV �o (Mt+1)g(Mt+1jaot;��o;Mt)dMt+1

35 (10)

28Alho and Spencer (2005), Chapter 7 discuss the application of time series models, including AR(1) to demographicgrowth rates. Models with additional lag terms would complicate the state space of the dynamic model.29With continuous states it is an assumption that a pure strategy MPNE exists. Dorazelski and Satterthwaite

(2010) show the existence of a pure strategy MPNE for a model with discrete states when the random component ofpayo¤s has unbounded support. Conceptually it would be possible to convert my model into one with an exceptionallylarge number of discrete states using an arbitrarily �ne discretization. A similar argument is made in Jenkins et al.(2004).

24

where � is the discount factor. The choice-speci�c value function v�o (aot;Mt) de�nes o�s expected

payo¤ from choosing aot excluding the idiosyncratic shock component "ot(aot;Mt)

v�o (aot;Mt) = �(aot;Mt) + �

ZV �o (Mt+1)g(Mt+1jcot;��o;Mt)dMt+1 (11)

It follows that o�s optimal strategy ��o in state (Mt; "ot) when other �rms use ��o is

��o(Mt; "ot;��o) = arg maxaot2Aot

[v�o (aot;Mt) + "ot(aot;Mt)] (12)

Strategies will form a MPNE when, in all states, the strategy of each �rm maximizes its value given

the strategies of other �rms.

3.6 Discussion of the Assumptions

Several assumptions deserve some additional comment.

Time E¤ects. When estimating the listener demand and revenue models I allow for time

e¤ects as, during the sample period, there is a downward trend in radio listenership (which began

in the late 1980s) and an upward trend in revenues per listener. Unfortunately it is di¢ cult to

include persistent trends in in�nite horizon dynamic games because existing solution methods assume

stationarity. Therefore I assume that �rms expect that the current value of the time e¤ects will

remain �xed in the future (so, for example, �rms in Spring 2003 assume that the Spring 2003 values

of the time e¤ect of listener demand and per listener revenues will persist into the future and the

�rms in Spring 2004 assume that the Spring 2004 values will persist into the future). This is a

simpli�cation but it is consistent with the fact that total revenues, which is what �rms care about,

were stable during the sample period changing by no more than 2% from year-to-year, because the

trends in listenership and revenues per listener roughly cancelled out.30 ;31

30The Radio Advertising Bureau estimates annual industry revenues from 2002 to 2006 of $19.4 bn., $19.6 bn., $20.0bn. and $20.1 bn (personal correspondance, November 29, 2010).31Given my counterfactual, it is important that these trends are common across formats. This appears to be the

case in the data. For example, based on Arbitron�s Radio Today reports time spent listening between 2001 and 2005fell by 4.9% for the population as a whole, 5.1% for black listeners and 3.5% for Hispanic listeners who were beingserved by many more Spanish language stations over this period. When I regress station revenues per listener onformat dummies, market dummies, year dummies and year*format interactions, the coe¢ cients on the year*formatinteractions are jointly insigni�cant (p-value 0.3142) which suggests that revenues per listener were changing in asimilar way across formats over time.

25

Entry and Exit. As noted in Section 2, de novo entry and exit are very rarely observed, and

the issuing of new licenses is complicated by spectrum constraints in most markets, so I choose not

to include these margins in my model (although stations can go o¤-air temporarily). Of course, very

large fees might cause some stations to exit rather than switch to non-music programming. However,

even when industry revenues dropped dramatically after 2008, the FCC still reported excess demand

for broadcast licenses (US GAO (2010), p. 25).

One Move Per Period. The current model assumes that a local �rm can only move at most

one station per period in order to limit the number of choices available to a particular �rm. While

99.5% of �rm-period observations satisfy this constraint, there are 28 observations where �rms move

two stations and 1 observation where a �rm moves 3 stations.32 These observations are ignored

when calculating the pseudo-likelihood as part of the estimation process, and it is assumed that all

other local �rms optimize assuming that other �rms can only move one station at once. Relaxing

this restriction in the dynamic model with seven formats would be very burdensome, but I have

investigated how allowing each �rm to make two moves, rather than one move, a¤ects the results in

a two-period version of the model where �rms only care about their revenues in the following period.

The only signi�cant change is that the estimates of local economies of scope increase by around 10%,

which is sensible as 9 out of the 28 two move observations involve a �rm moving two stations to the

same format at the same time.

Coordination Across Local Firms with the Same Corporate Owner. I assume that

format choices are made by local �rms, but that each �rm is compensated for how its current format

con�guration a¤ects the �xed costs of �rms in other markets. This provides a relatively simple

way to allow for cross-market economies of scope to a¤ect format choices, without modelling a single

decision maker who controls many stations simultaneously. However, it does assume that local �rms

with the same corporate owner do not know each others " draws, so that they cannot coordinate their

simultaneous choices. Instead, �rms have expectations about what their sister �rms will choose in

the same way that they have expectations about their competitors.

32There are 364 �rm-market observations where exactly one station is moved.

26

4 Approximately Solving the Model using Parametric Pol-

icy Function Iteration (PPI)

Finding an exact solution to the proposed model, which has many asymmetric players and a rich state

space that is a mixture of continuous and discrete variables is beyond the current literature.33 Instead,

I employ the technique of �parametric policy function iteration�(PPI) to compute an approximate

solution. This section describes how I use PPI to solve the model, and brie�y describes the related

Monte Carlo experiments that are detailed in the Appendix. Estimation is described in the next

section.

Following AM, it is convenient to express �rms�strategies in probability space. De�ne P � as the

probabilities that actions are chosen prior to the "s being revealed when �rms use strategies �

P �o (aot;Mt) =

ZI(�o(Mt; "ot) = aot)hot(Mt; "ot)d"ot (13)

where hot("ot) is the pdf of the vector of shocks "ot and I(�o(Mt; "ot) = aot) is an indicator for action

aot being chosen. Equilibrium strategies �� imply equilibrium choice probabilities P �. At P �, we

can express ex ante (i.e., before the "s are revealed) value functions as

V P �

o (Mt) = e�o(Mt; P�) + �

ZV P �

o (Mt+1)g(Mt+1jP �;Mt)dMt+1 (14)

where e�o(Mt; P�t ) are o�s expected �ow pro�ts for strategies P � and state Mt. In terms of the

within-period timing detailed above, expected �ow pro�ts are calculated from stage 3 in the current

period to stage 2 in the following period, so they include next period�s expected �xed costs (which

will depend on the actions chosen in the current period). For describing estimation later, it is useful

33To understand the size of the state space, suppose that cross-market e¤ects are ignored and consider a marketwith 20 stations, with time-varying station quality discretized to 5 levels and 25 discretized states describing marketdemographic composition. Then, the number of possible states for this market would be greater than 3.8e31, and be-cause stations di¤er in some permanent characteristics the number of states could not be reduced using exchangeability(Gowrisankaran (1999)).

27

to express e�o(Mt; P�ot) as

e�(Mt; P�ot) =

Xaot2Aot

P �ot(aotjMt;��o)

0BBB@P

s2So Rs(Mtj )�Wo(aot;Mt)�W�

�RCo(aot;Mt+1)�

Cg(Mt+1jP �;Mt)dMt+1

+e(aot; P�ot; �

"o(Mt))

1CCCA (15)

where e(aot; P �ot; �"ot(Mt)) = �"o(Mt)({ � log(P �(aotjMt;��o))) is the expected value of the " associ-

ated with choice aot. { is Euler�s constant. Note that e only depends on o�s own choice probabilities

in the current period, and not the strategies of other �rms or o�s own strategy in future periods.

Fixed costs in the next period can depend on the choices of other �rms in di¤erent markets because

of national economies of scope.

Stacking states and �rms, equation (14) can be expressed in matrix form as

V P � = e�(P �) + �EP �VP � (16)

where EP � is the Markov operator corresponding to policies P �; and for a particular state and �rm

EP �VP �

o (Mt) =

ZV P �

o (Mt+1)g(Mt+1jP �;Mt)dMt+1 (17)

Holding P � �xed, equation (16) has a unique solution for V P � de�ned by the linear equations

V P � = [I � �EP � ]�1e�(P �) (18)

Policy iteration seeks to solve for equilibrium policies and values by iterating two steps (Judd

(1998), Rust (2000)). At iteration i, in the �rst step (policy valuation), (15) and (18) are applied to

calculate values V P i associated with probabilities P i that may not be optimal. In the second step

(policy improvement), values V P i are used to update P i by computing choice-speci�c value functions

vPi

o (aot;Mt) = �(Mt; aot) + �

ZV P i

o (Mt+1)g(Mt+1jP i;Mt; aot)dMt+1 (19)

where g(Mt+1jP i;Mt; aot) is the probability of transitioning toMt+1 when o chooses aot. P i+1 is

calculated using formulae implied by the Type 1 extreme value distribution of the "s where the scale

28

parameter is �"o

P i+1ot (aotjMt; Pi) =

exp

�vP

io (aot;Mt)�"o(Mt)

�P

a0ot2Aotexp

�vPio (a0ot;Mt)

�"o(Mt)

� (20)

For V P s and P s that constitute a �xed point of these equations, the associated strategies will con-

stitute a Markov Perfect Nash equilibrium. Similarly, for any Markov Perfect Nash equilibrium

strategies, the V P s and P s will form a �xed point. For a game, there may be multiple solutions and

convergence of policy iteration is not guaranteed. Practical implementation of policy iteration with

continuous states requires a choice of N discrete states at which to evaluate V and P and, typically, a

method for approximating the integrals by choosing an additional set of statesMt+1 for eachMt.34

Parametric Policy Function Iteration (PPI).

To apply parametric policy iteration I make the further assumption that the value function can

be approximated using a linear combination of K basis functions describing the state variables

V P �

o (Mt) 'KXk=1

�k�ko(Mt) (21)

so that equation (14) can be expressed as

KXk=1

�k�ko(Mt) ' e�(Mt; P�ot) + �

Z KXk=1

�k�ko(Mt+1)g(Mt+1jP �;Mt)dMt+1 (22)

The solution to the value function for given choice probabilities now requires �nding K � coe¢ cients

rather than values for V at each state. When the equations (22) are stacked into matrix form for N

states

�� = e�(P �) + �E�� (23)

where � is the matrix of basis functions and E� is a matrix where element (j; k)

E�j;k =

Z�ko(Mt+1)g(Mt+1jP �;Mt)dMt+1 (24)

34The integration method must specify the discrete set of statesMt+1 for eachMt at which to evaluate V , a methodfor approximating V (Mt+1) given the estimates of V at the N points, and a rule for weighting the V (Mt+1) estimatesthat are calculated to approximate the integral.

29

if row j is associated with �rm o and stateMt. For the overidenti�ed case (N > K), b� can be foundusing the OLS estimator

b� = ((�� �E�)0(�� �E�))�1(�� �E�)0e�(P �) (25)

The iterative procedure now consists of the following steps for a given initial set of choice probabilities

P i:

1. at a given set of N states, calculate �; and use (24) to calculate the matrix E� and the vectore�(P i). Details of the approximate integration procedure are provided below;2. create matrices (�� �E�) and use (25) to calculate b�;3. use b� to calculate the choice-speci�c value functions for each choice

vPi

o (aot;Mt) = �(Mt; aot) + �KXk=1

��Z�ko(Mt+1)g(Mt+1jP i;Mt; aot)dMt+1

� b�k� (26)

4. use formulae (20) to calculate updated choice probabilities P 0; and calculate P i+1 = P 0 +

(1 � )P i, where the weights can vary (from 0.1 to 1) depending on how well the choice

probabilities appear to be converging. In practice, weights equal to 1 work �ne close to the

�nal values.

5. repeat steps 1-4 until the maximum di¤erence between P i and P 0 is small enough (less than

1e� 5).

Integration.

An e¢ cient procedure is required to perform the integrations. In particular it would very com-

putationally expensive to calculate entirely new matrices of variables each time a choice probability

changes: in my setting this would require solving a random coe¢ cient demand model. Instead, I

calculate matrices for many sets of moves by other �rms in advance, and reweight these matrices as

the choice probabilities change. Speci�cally suppose that for a given state inMt, I consider a set of

H statesMh;t+1 created by considering all possible combinations of moves by the current �rm, a set

of S� draws for innovations in � and market demographics (which do not depend on �rm choices),

30

S�o;m moves by other �rms in the same local market, and S�o;�m moves by other �rms with the same

corporate owner in di¤erent local markets. The integralR�ko(Mt+1)g(Mt+1jP �;Mt)dMt+1 is then

approximated byHXh=1

�ko(Mh;t+1)g(Mh;t+1jP �;Mt)PHh0=1 g(Mh0;t+1jP �;Mt)

A similar integration is used to calculate a �rm�s expected �xed costs in the following period. To

be accurate this integration procedure requires that the moves S�o;m and S�o;�m are those that are

likely to be made. I choose these moves by �rst solving (or estimating when the parameters are being

estimated) a model where �rms assume that all other �rms�formats will remain �xed forever. This

is a single agent model that can be solved quickly. The choice probabilities implied by this model are

then used to select the set of S�o;m moves by other �rms which are most likely. In estimating and

solving the model for the counterfactual I use S� = 50, S�o;m = 500 and S�o;�m = 100.35 To make

computation with this many simulations feasible I assume that variables describing cross-market

factors enterPK

k=1 �k�ko(Mt) completely separably from the variables describing a �rm�s situation

within its own market. It is also possible to repeat the procedure by drawing a new set of states

S�o;m and S�o;�m that re�ect the choice probabilities of a solved game.

Speci�cation of the Parametric Function.

It is necessary to specify the variables used in the parametric approximation of the value function

and the initial set of N states at which the value function is evaluated. The N states used are

the ones that are observed in the data (a total of 6,075, one for each local �rm-period observation).

These points will, of course, represent the types of states that are likely to be observed given �rms�

equilibrium strategies. In the Monte Carlo described in the Appendix, using additional states, which

increases the computational burden, gives, at most, a small improvement in performance.

There are 151 variables used in the parametric approximation that can be divided into 6 groups (a

full list and code to calculate them is available). The �rst group describe market characteristics: the

proportion black and proportion Hispanic in the market�s current population, market population and

market average revenues per market share point, and several interactions between these variables.

The second group contains measures of the quality of stations owned by the �rm: sums of exp(�st)