drop shipments and sales tax -...

TRANSCRIPT

Presenting a live 110‐minute teleconference with interactive Q&A

Drop Shipments and Sales Tax Drop Shipments and Sales Tax Navigating Varying State Policies on Registrations and Exemptions

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

THURSDAY, APRIL 26, 2012

Today’s faculty features:

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

Vytenis Kirvelaitis, Director, State and Local Tax Group, Grant Thornton, Chicagoy , , p, , g

Irwin Mittleman, Sales Tax Consultant, Meridian Global Services, New York

Silvia Aguirre, President, Tax Technology Services, Raleigh, N.C.

For this program, attendees must listen to the audio over the telephone.

Please refer to the instructions emailed to the registrant for the dial-in information.Attendees can still view the presentation slides online. If you have any questions, pleasecontact Customer Service at1-800-926-7926 ext. 10.

Conference Materials

If you have not printed the conference materials for this program, please complete the following steps:

• Click on the + sign next to “Conference Materials” in the middle of the left-hand column on your screen hand column on your screen.

• Click on the tab labeled “Handouts” that appears, and there you will see a PDF of the slides for today's program.

• Double click on the PDF and a separate page will open. Double click on the PDF and a separate page will open.

• Print the slides by clicking on the printer icon.

Continuing Education Credits FOR LIVE EVENT ONLY

Attendees must listen to the audio over the telephone. Attendees can still view the presentation slides online but there is no online audio for this program.

Attendees must stay on the line for at least 100 minutes in order to qualify for a full 2 credits of CPE. Attendance is monitored as required by NASBA.

Please refer to the instructions emailed to the registrant for additional information. If you have any questions, please contact Customer Service at 1-800-926-7926 ext. 10.at 1 800 926 7926 ext. 10.

Tips for Optimal Quality

S d Q litSound Quality

For this program, you must listen via the telephone by dialing 1-866-873-1442and entering your PIN when prompted. There will be no sound over the web connection.co ect o .

If you dialed in and have any difficulties during the call, press *0 for assistance. You may also send us a chat or e-mail [email protected] immediately so we can address the problem.

Viewing QualityTo maximize your screen, press the F11 key on your keyboard. To exit full screen, press the F11 key againpress the F11 key again.

Drop Shipments and Sales Tax Seminar

April 26, 2012

Irwin Mittleman, Meridian Global [email protected]

Silvia Aguirre, Tax Technology [email protected]

Vytenis Kirvelaitis, Grant Thornton [email protected]

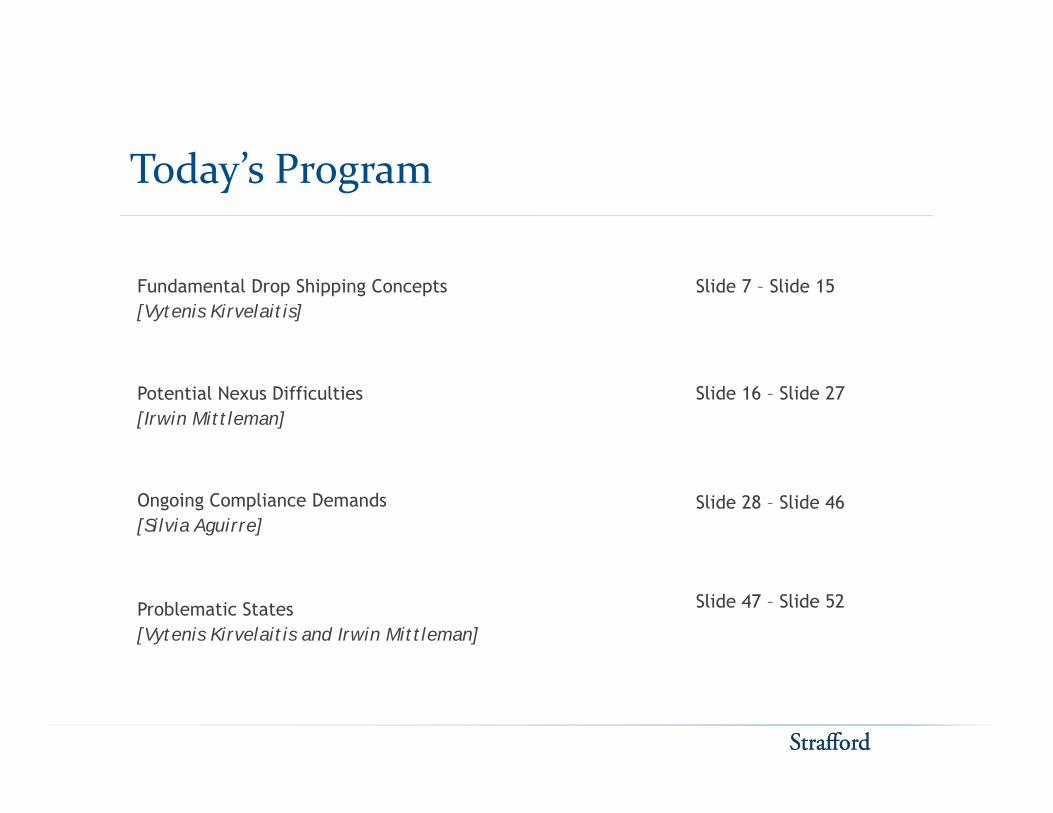

Today’s Program

Fundamental Drop Shipping Concepts[Vytenis Kirvelaitis]

Slide 7 – Slide 15

Potential Nexus Difficulties[Irwin Mittleman]

Slide 16 – Slide 27

Ongoing Compliance Demands[Silvia Aguirre]

Slide 28 – Slide 46

Problematic States[Vytenis Kirvelaitis and Irwin Mittleman]

Slide 47 – Slide 52

FUNDAMENTAL DROP Vytenis Kirvelaitis, Grant Thornton

FUNDAMENTAL DROP SHIPPING CONCEPTS

Wh I A ‘D Shi ’?What Is A ‘Drop Shipment’?

• Drop shipment is a term used to describe a transaction in which a buyer orders an item from a party that then arranges

for the shipment of the item directly to the buyer, from a location other than where the order was received.

• Generally this includes a sale in which the item being • Generally, this includes a sale in which the item being purchased is not already in the retailer’s inventory.

• The item usually arrives at the buyer from another party, such as a wholesaler, distributor or manufacturer.

8

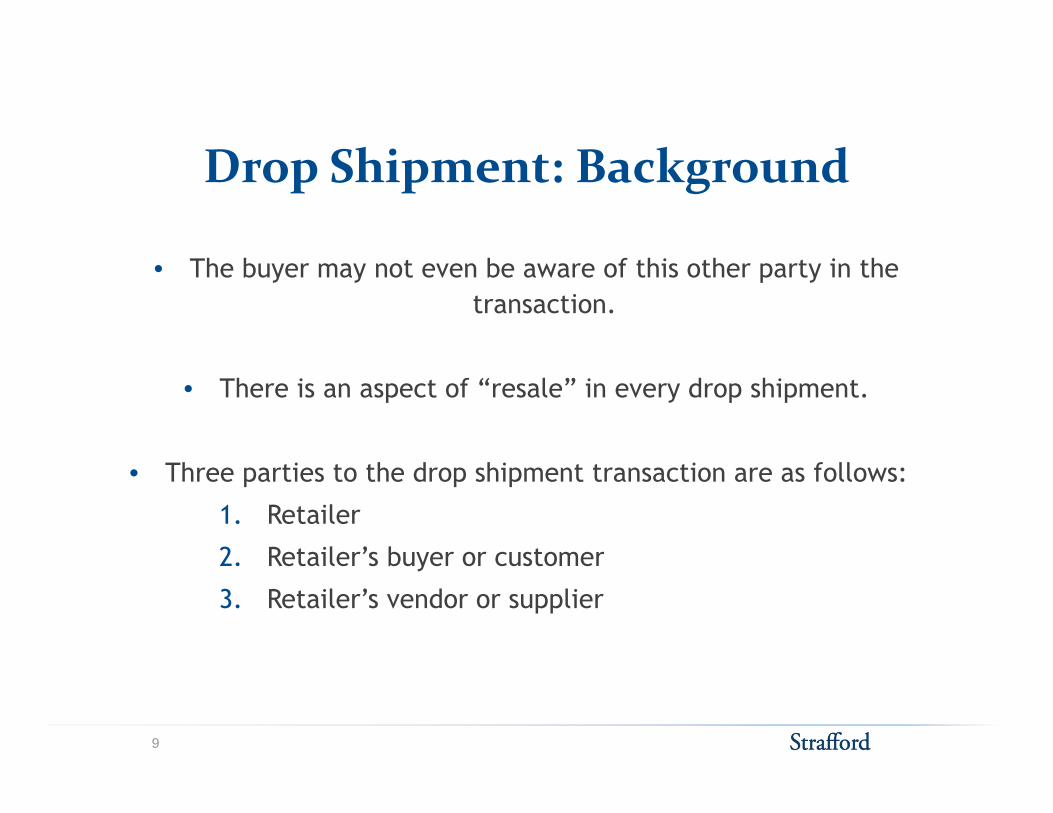

D Shi B k dDrop Shipment: Background

• The buyer may not even be aware of this other party in the transaction.

• There is an aspect of “resale” in every drop shipment.

• Three parties to the drop shipment transaction are as follows:

1. Retailer

2 Retailer’s buyer or customer2. Retailer s buyer or customer

3. Retailer’s vendor or supplier

9

Drop Shipment: Visual

Step 1: Initial order placement Step 2: Subsequent order placement

R il ’Retailer’s Buyer

(Customer)Retailer

(Purchaser)

Retailer’s Vendor or Supplier

(Distributor(Distributor, Manufacturer,

Fulfillment House)House)

Secondary sale (“end user”) Primary sale (“resale”)

10

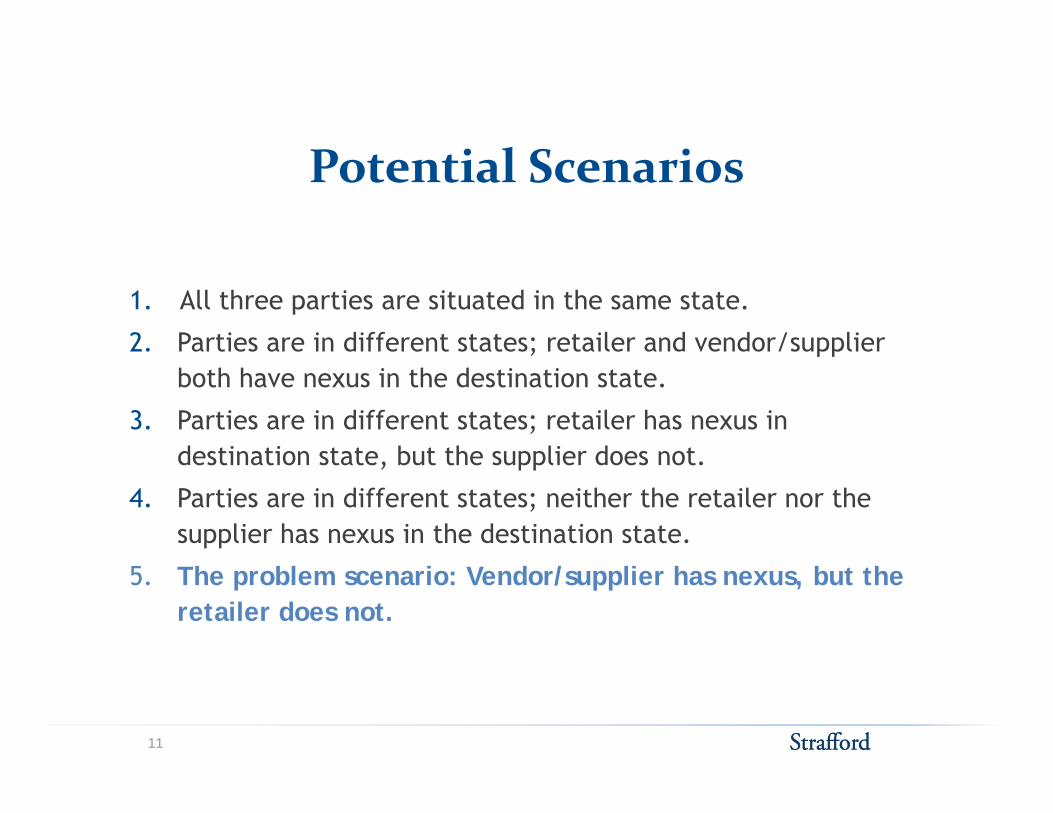

P i l S iPotential Scenarios

1. All three parties are situated in the same state.

2. Parties are in different states; retailer and vendor/supplier ; ppboth have nexus in the destination state.

3. Parties are in different states; retailer has nexus in destination state but the supplier does notdestination state, but the supplier does not.

4. Parties are in different states; neither the retailer nor the supplier has nexus in the destination state.

5. The problem scenario: Vendor/supplier has nexus, but the retailer does not.

11

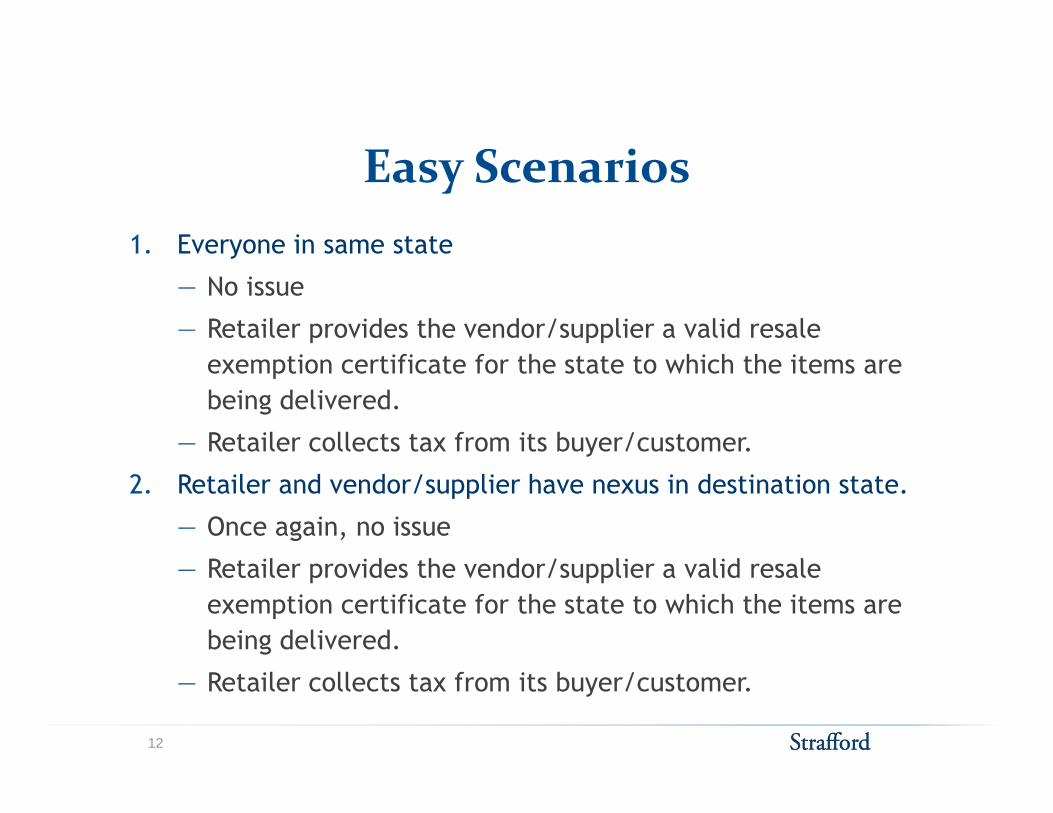

E S iEasy Scenarios1. Everyone in same state1. Everyone in same state

― No issue

― Retailer provides the vendor/supplier a valid resale i ifi f h hi h h i exemption certificate for the state to which the items are

being delivered.

― Retailer collects tax from its buyer/customer.

2. Retailer and vendor/supplier have nexus in destination state.

― Once again, no issue

R t il id th d / li lid l ― Retailer provides the vendor/supplier a valid resale exemption certificate for the state to which the items are being delivered.

― Retailer collects tax from its buyer/customer.

12

I i S iInteresting Scenarios

3 Retailer has nexus in destination state; vendor/supplier does 3. Retailer has nexus in destination state; vendor/supplier does not.

― No need for retailer to provide the vendor/supplier with a l d l f f h dvalid resale exemption certificate for the destination state,

as the vendor/supplier is not registered.

― Retailer collects tax from its buyer/customer.y

4. Neither the retailer nor the vendor/supplier has nexus in the destination state.

No exemption certificate is provided and no tax is charged ― No exemption certificate is provided, and no tax is charged to the buyer/customer.

― Buyer/customer would have an obligation to self-assess use tax on the transaction.

13

P bl S iProblem Scenario

5. Vendor/supplier has nexus in destination state, but the retailer does not.

― Vendor/supplier knows that the sale is for “resale” but is Ve do suppl e ows t at t e sale s o esale but s also aware that the retailer will not be collecting tax on its ultimate sale to its buyer/customer.

Who owes the tax? The buyer/customer?― Who owes the tax? The buyer/customer?

― If yes, can the vendor/supplier expect the customer to self-assess use tax? What documentation is needed?

― Could a state require the vendor/supplier to collect the tax from the retailer’s buyer/customer?

― If yes what is the appropriate tax base?If yes, what is the appropriate tax base?

14

I T K I Mi dIssues To Keep In Mind

• Is the vendor/supplier registered in the destination state?• Is the vendor/supplier registered in the destination state?

• Is the retailer registered in the destination state?

• If the problem scenario exists, what is the destination state’s policy regarding drop shipments?policy regarding drop shipments?

• What documentation needs to be retained by the parties?

• Is the sale to the buyer/customer exempt and if so, how does that affect the destination state's approach to the transaction? that affect the destination state s approach to the transaction?

15

POTENTIAL NEXUS Irwin Mittleman, Meridian Global Services

POTENTIAL NEXUS DIFFICULTIES

Sales Tax Nexus AndSales Tax Nexus AndDrop ShipmentsDrop Shipments

Vendors that utilize drop shippers to avoid holding inventory in a state need to understand that sales tax nexus is a question of in-state activity by themselves, or by their agents.

Nexus-creating activities can include providing services in that state.

Scripto v. Carson (1960) 362 US 207 is still good law to this date.

17

Examples Of NexusExamples Of Nexus--Examples Of NexusExamples Of Nexus--Creating ActivitiesCreating Activities

Salespersons entering a state

Independent agents soliciting on behalf of a business Independent agents soliciting on behalf of a business

Property in a state

Links to a Web site (Amazon nexus)

S t t h ti t l l f Some states have exceptions to general nexus rules for events such as attending trade shows for short periods of time.

18

Assume NothingAssume Nothing Every drop shipment transaction is a three-party

transaction.

Sales tax is basically imposed only on ultimate user transactions.

Even though drop shipments have elements of interstate commerce and the resale exemption, it is important to know the specific state treatment for this type of t titransaction.

19

What Is Amazon Nexus?What Is Amazon Nexus?New York considers New York companies that have links on New York considers New York companies that have links on their Web sites directing customers to the Amazon Web site to be agents of Amazon, and therefore this creates New York nexusYork nexus.

Amazon argues that it does not exercise sufficient control of these New York vendors to create nexusof these New York vendors to create nexus.

There is no final resolution of this dispute.

20

Corporation Tax Nexus AndCorporation Tax Nexus AndDrop ShippersDrop Shippers

Most drop shippers need to be registered for corporation business taxes, because they maintain inventory in the state.

Even if they do not carry inventory in the state, if they own or rent real property in a taxing jurisdiction, that

ld t could create nexus.

21

Pitfalls For The PractitionerPitfalls For The Practitioner

The taxing jurisdictions are getting sophisticated in auditing, and they continually are cross-referencing g, y y gsuppliers and purchasers for registration of the seller.

If the seller is found to be subject to sales tax, then the tax e se e s ou d o be subjec o sa es a , e e abase is the sales price paid to the ultimate purchaser.

California presents special problems for drop shippers; see California presents special problems for drop shippers; see CA Tax Reg. 1706.

22

Practice TipPractice TipPractice TipPractice Tip The tax department of a multi-state company should

review substantive changes to the company Web site.g p y

The tax department should be aware of the minutes of the board of directors, to see if the company might be entering boa d o d ec o s, o see e co pa y g be e e ga new business line.

The tax department should be aware of the states where The tax department should be aware of the states where salespeople and independent contractors are traveling.

23

CCan The Drop Shipper Bean The Drop Shipper BeConsidered Your Agent?Considered Your Agent?gg

If the drop shipper is an affiliated company, then a taxing j i di ti tt t t id it lt jurisdiction can attempt to consider it your alter ego.

Many companies brag about their affiliations on their Web it d f t t lt th i t d t t sites and forget to consult their tax department.

24

Texas Alter Ego NexusTexas Alter Ego Nexus Texas under Tax Law Sect. 151.107 (a) (7) (A) has an alter

ego definition for nexus. It is:

◦ A business that sells a similar line of products,

◦ That is a person with a location in the state,

◦ And that sells the products with a similar business name is subject to the tax.

25

Supplier Is An Agent Of VendorSupplier Is An Agent Of Vendor Tennessee has a regulation, 1230-5-1.96, that specifically

calls an in-state supplier an agent of the out-of-state vendor.

The dealer is held liable for the tax despite the lack of privity between itself and the ultimate customer.

The regulation has language that indicates the state may be willing to make accommodations if made before drop shipments begin.

26

II S D ShiS D ShiIntraIntra--State Drop ShipmentsState Drop Shipments Do not assume that drop shipment rules only concern out- Do not assume that drop shipment rules only concern out

of-state sellers.

Many states have local district sales taxes that might be Many states have local district sales taxes that might be affected by sellers in one district taking orders from in-state sellers and having the product drop shipped into another taxing district. another taxing district.

Texas provides guidance for the correct sales tax rate to be applied in that instance.applied in that instance.

27

ONGOING COMPLIANCE Silvia Aguirre, Tax Technology Services

DEMANDS

Drop ShipmentsDrop Shipments

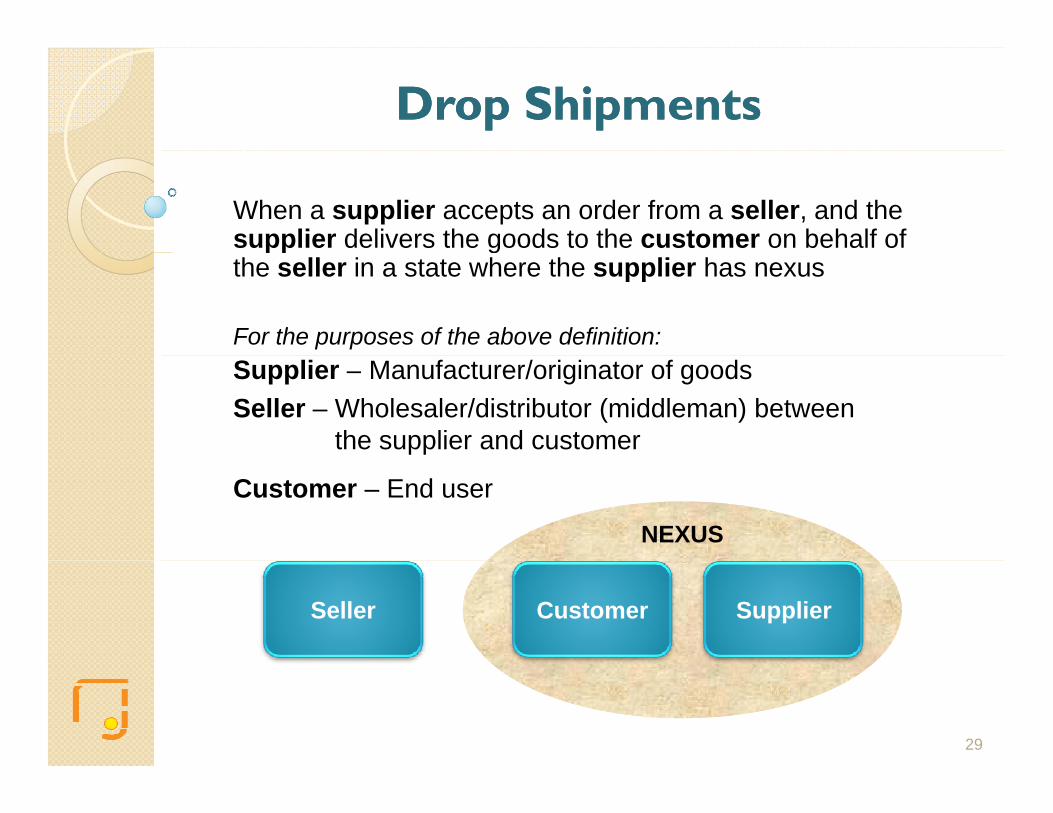

When a supplier accepts an order from a seller, and the supplier delivers the goods to the customer on behalf of pp gthe seller in a state where the supplier has nexus

For the purposes of the above definition:Supplier – Manufacturer/originator of goodsSeller – Wholesaler/distributor (middleman) between

the supplier and customer

Customer – End user

NEXUS

Seller Customer Supplier

29

Drop Shipment: Real World ExamplesDrop Shipment: Real World Examples

Supplier (nexus):

“Why are they not giving me an exemption certificate? It is so simple.”

“Why is the buyer short-paying the tax? Don’t they understand?”

Concerns:• Do you have policies in place for your customer care

personnel, tax department or credit departments to address the concerns of your client?

• Do you know which certificates to accept?

• Can you contact your client’s customer for information?Can you contact your client s customer for information?

30

Drop Shipment: Real World Examples (Cont.Drop Shipment: Real World Examples (Cont.

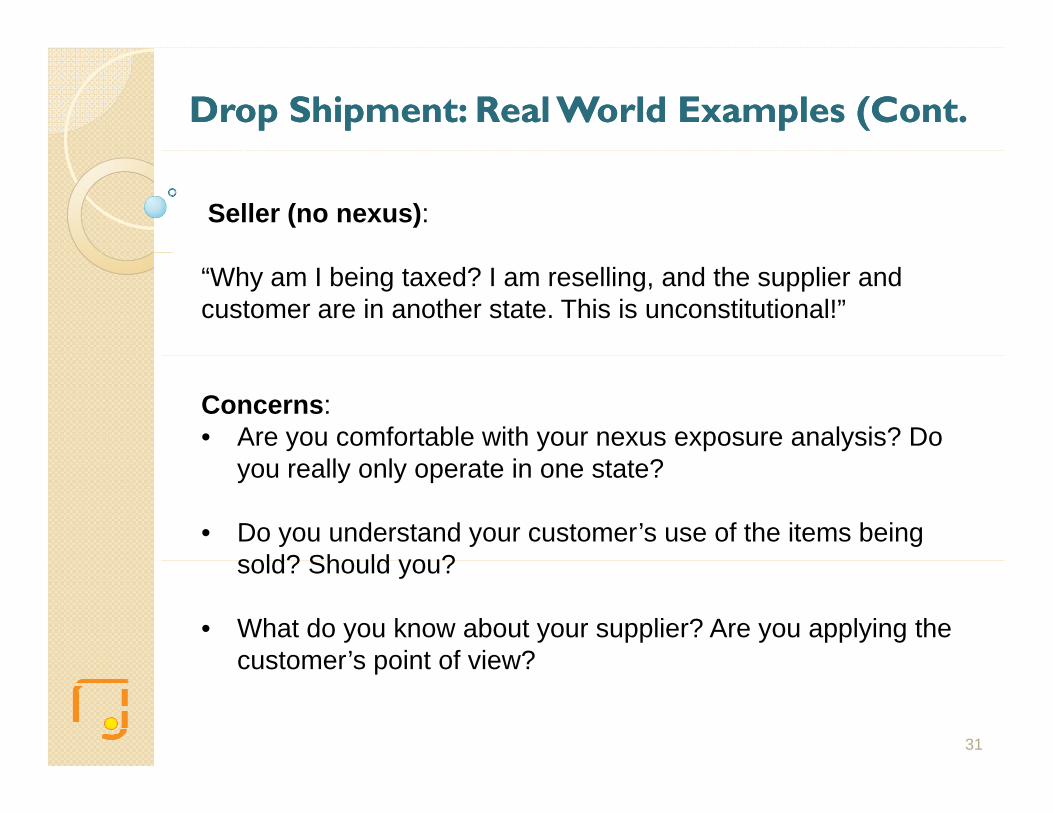

Seller (no nexus):

“Why am I being taxed? I am reselling, and the supplier and customer are in another state. This is unconstitutional!”

Concerns: • Are you comfortable with your nexus exposure analysis? Do

you really only operate in one state?

• Do you understand your customer’s use of the items being sold? Should you?sold? Should you?

• What do you know about your supplier? Are you applying the customer’s point of view?customer s point of view?

31

Drop Shipment: Real World Examples (Cont.)Drop Shipment: Real World Examples (Cont.)

Customer (nexus):

“If I buy it from an out-of-state wholesaler, I do not owe taxes.”

Concern:• Are the items being purchased really tax-exempt? Use tax

probably applies.

32

Exemption Certificate ComplianceExemption Certificate Compliance

Exemption certificates are acceptable if…

Properly completed• Name (buyer and seller)

• Reason of exemption (resale for drop shipments)

• Correct form (SST, MTC, state issued)

Signature/date (at time of sale for best good faith standards)• Signature/date (at time of sale for best good faith standards)

• Blanket/single (for recurring sales)

When there is a drop shipment …

33

Exemption Certificate Compliance (Cont.)Exemption Certificate Compliance (Cont.)

• Some states assume items are for resale, and the seller’s exemption certificate is sufficient.exemption certificate is sufficient.

• Some states require that the customer’s exemption be included with the seller’s exemption certificate to proveincluded with the seller s exemption certificate, to prove resale.

• Some states want you to retain shipping information, in addition to exemption certificates, to prove out-of-state origination.

• Some states tax the sales based on the seller’s price, others based on the supplier’s price.

34

Exemption Certificate Compliance (Cont.)Exemption Certificate Compliance (Cont.)

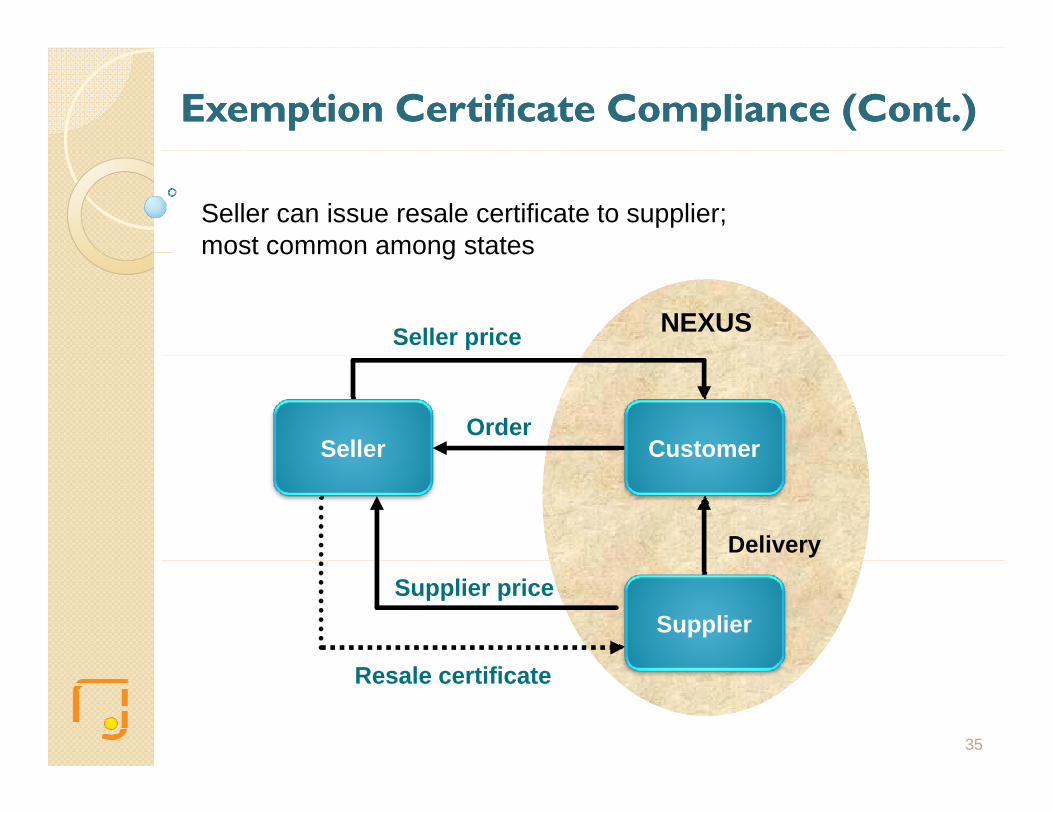

Seller can issue resale certificate to supplier; most common among states

Seller price NEXUS

most common among states

SellerOrder

Customer

Delivery

Supplier priceSupplier

Resale certificate

35

Exemption Certificate Compliance (Cont.)Exemption Certificate Compliance (Cont.)

States that fall under the most common drop shipment categoryAl bAlabamaArkansasArizonaArkansas

New JerseyNew MexicoNew YorkNorth Carolina

Nevada as of 10/1/2007Wisconsin as of 10/1/2009West Virginia as of 12/31/2007

ColoradoGeorgiaIdahoIllinois **

North CarolinaNorth DakotaOhioPennsylvania

** Illinois: A resale number can be obtained without establishing nexus,

IndianaIowaKansasKentucky

yRhode IslandSouth CarolinaSouth Dakota

and/or a written statement that buyer has no nexus should be sufficient. http://12.43.67.2/commission/jcar/admincode/086/086001300B02250R.html

MaineMichiganMinnesotaMissouri

TexasUtahVermontVirginiaNebraska VirginiaWashingtonWyoming

36

Exemption Certificate Compliance (Cont.)Exemption Certificate Compliance (Cont.)

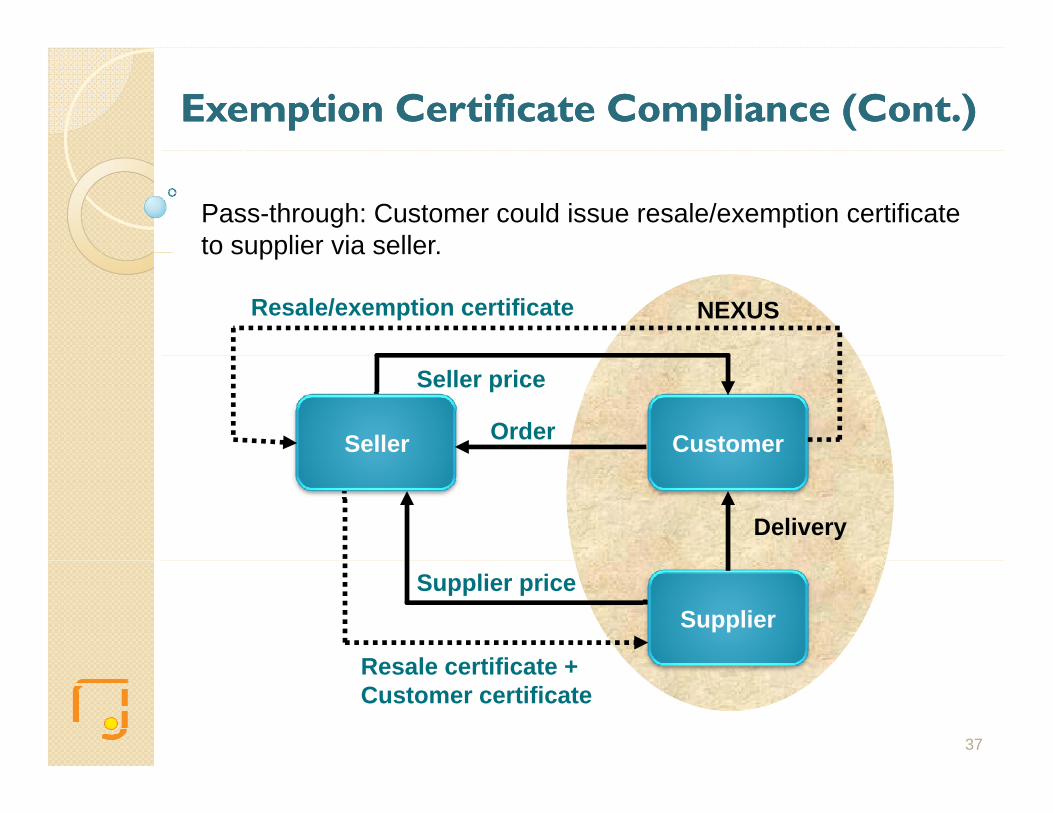

Pass-through: Customer could issue resale/exemption certificate to supplier via seller.

Resale/exemption certificate NEXUS

to supplier via seller.

Seller price

Order CustomerSeller

Delivery

SupplierSupplier price

Resale certificate +Resale certificate +Customer certificate

37

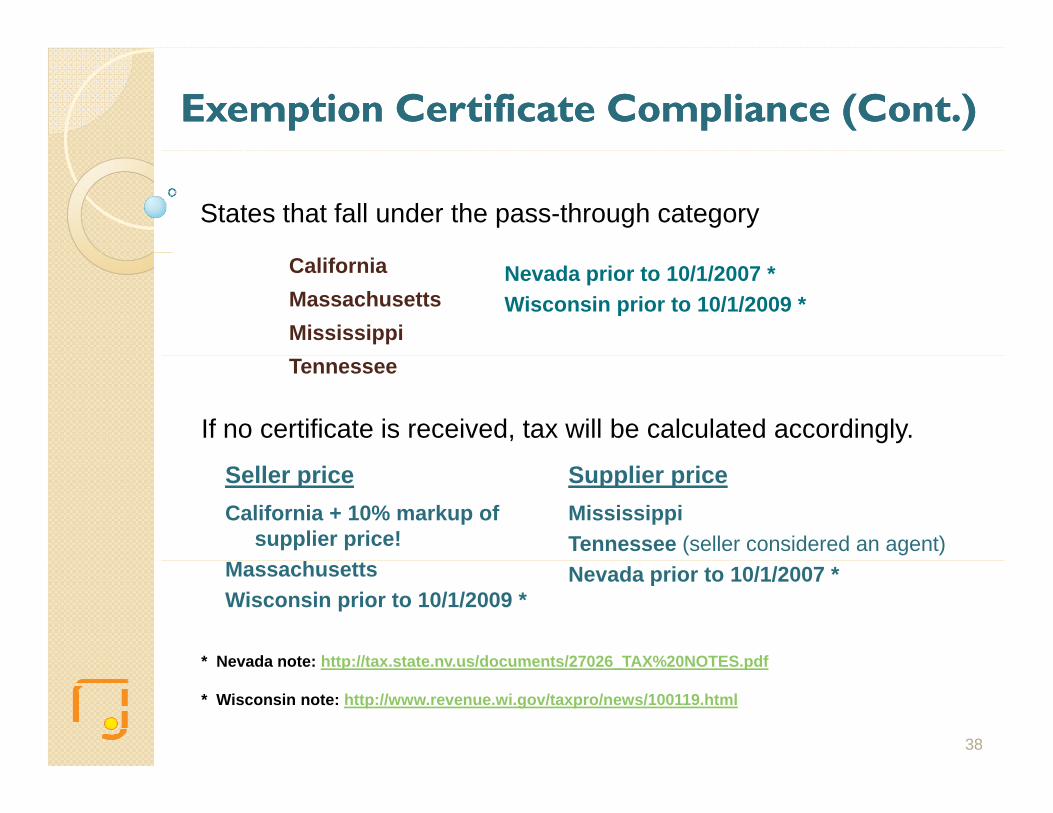

Exemption Certificate Compliance (Cont.)Exemption Certificate Compliance (Cont.)

States that fall under the pass-through category

CaliforniaMassachusettsMississippi

Nevada prior to 10/1/2007 *Wisconsin prior to 10/1/2009 *

Tennessee

If no certificate is received, tax will be calculated accordingly.

California + 10% markup of supplier price!

Seller price Supplier priceMississippiTennessee (seller considered an agent)

MassachusettsWisconsin prior to 10/1/2009 *

Nevada prior to 10/1/2007 *

* Nevada note: http://tax state nv us/documents/27026 TAX%20NOTES pdf Nevada note: http://tax.state.nv.us/documents/27026_TAX%20NOTES.pdf

* Wisconsin note: http://www.revenue.wi.gov/taxpro/news/100119.html

38

Exemption Certificate Compliance (Cont.)Exemption Certificate Compliance (Cont.)

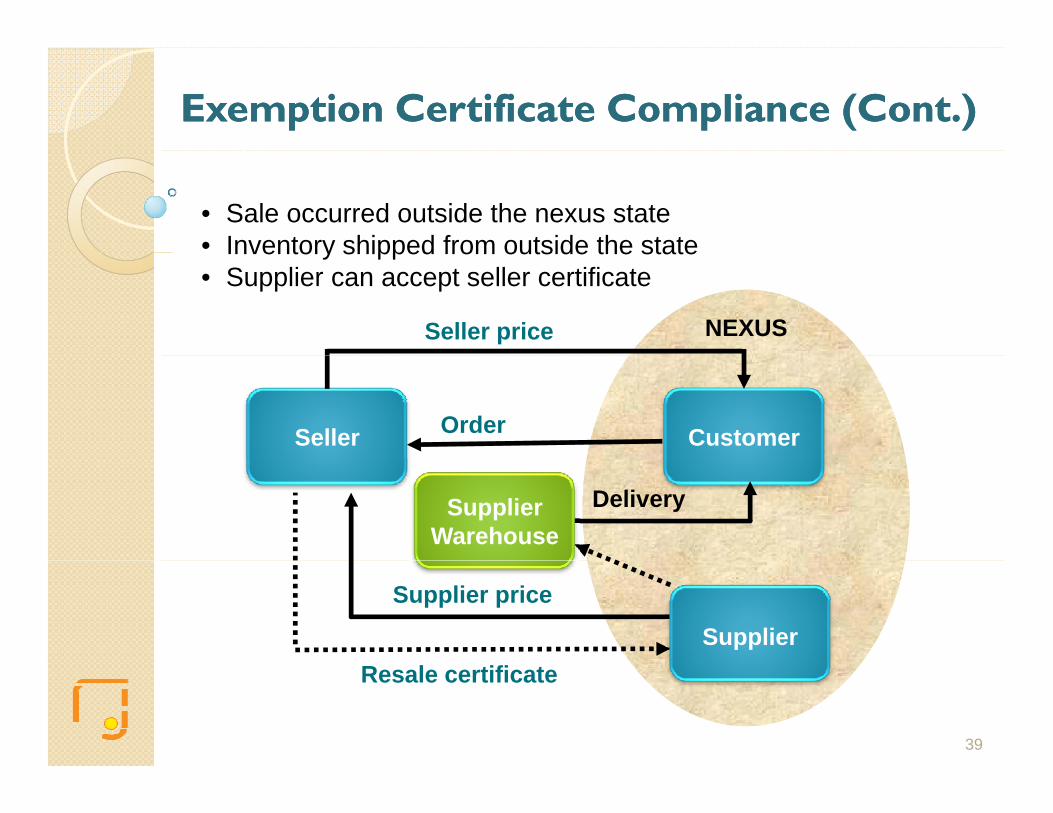

• Sale occurred outside the nexus state• Inventory shipped from outside the state

Seller price NEXUS

Inventory shipped from outside the state• Supplier can accept seller certificate

Order CustomerSeller

DeliverySupplier Warehouse

Supplier price

SupplierResale certificate

39

Exemption Certificate Compliance (Cont.)Exemption Certificate Compliance (Cont.)

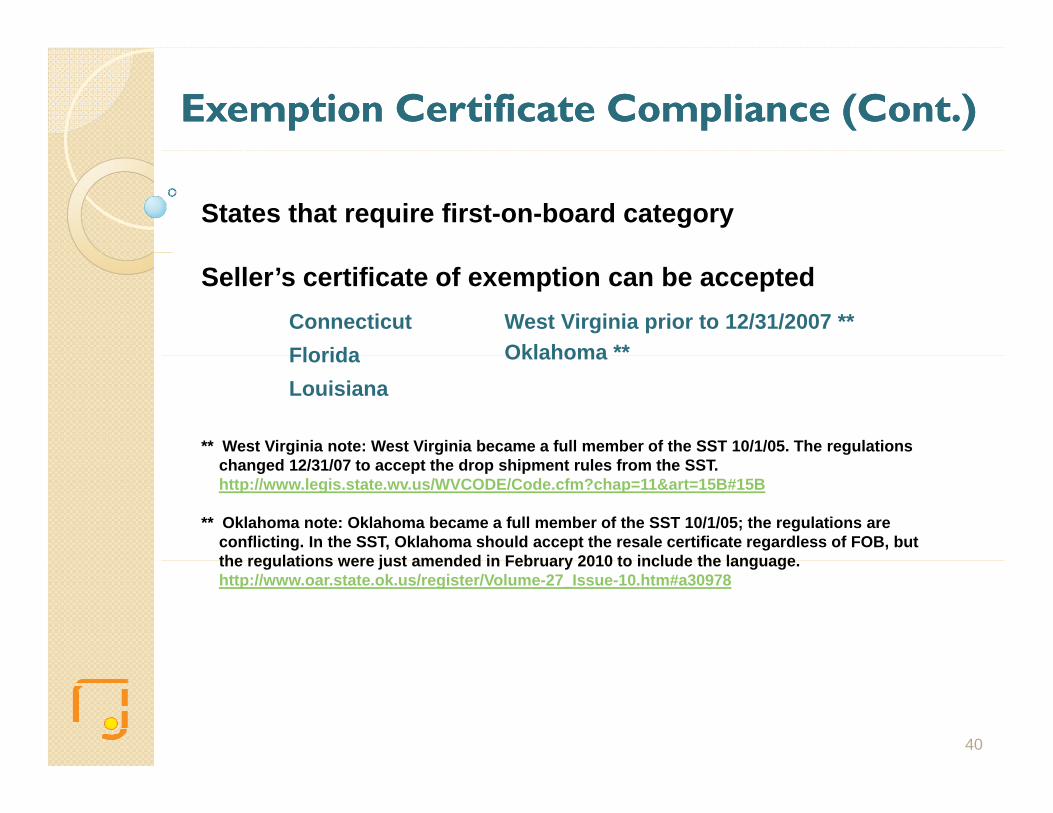

States that require first-on-board category

ConnecticutFlorida

Seller’s certificate of exemption can be acceptedWest Virginia prior to 12/31/2007 **Oklahoma **Florida

Louisiana

** West Virginia note: West Virginia became a full member of the SST 10/1/05. The regulations

Oklahoma

changed 12/31/07 to accept the drop shipment rules from the SST. http://www.legis.state.wv.us/WVCODE/Code.cfm?chap=11&art=15B#15B

** Oklahoma note: Oklahoma became a full member of the SST 10/1/05; the regulations are conflicting. In the SST, Oklahoma should accept the resale certificate regardless of FOB, but the regulations were just amended in February 2010 to include the languagethe regulations were just amended in February 2010 to include the language. http://www.oar.state.ok.us/register/Volume-27_Issue-10.htm#a30978

40

Exemption Certificate Compliance (Cont.)Exemption Certificate Compliance (Cont.)

Taxable transaction

Seller price NEXUS

OrderSeller Customer

Supplier price

Delivery

Tax due to supplier

pp pSupplier

41

Exemption Certificate Compliance (Cont.)Exemption Certificate Compliance (Cont.)

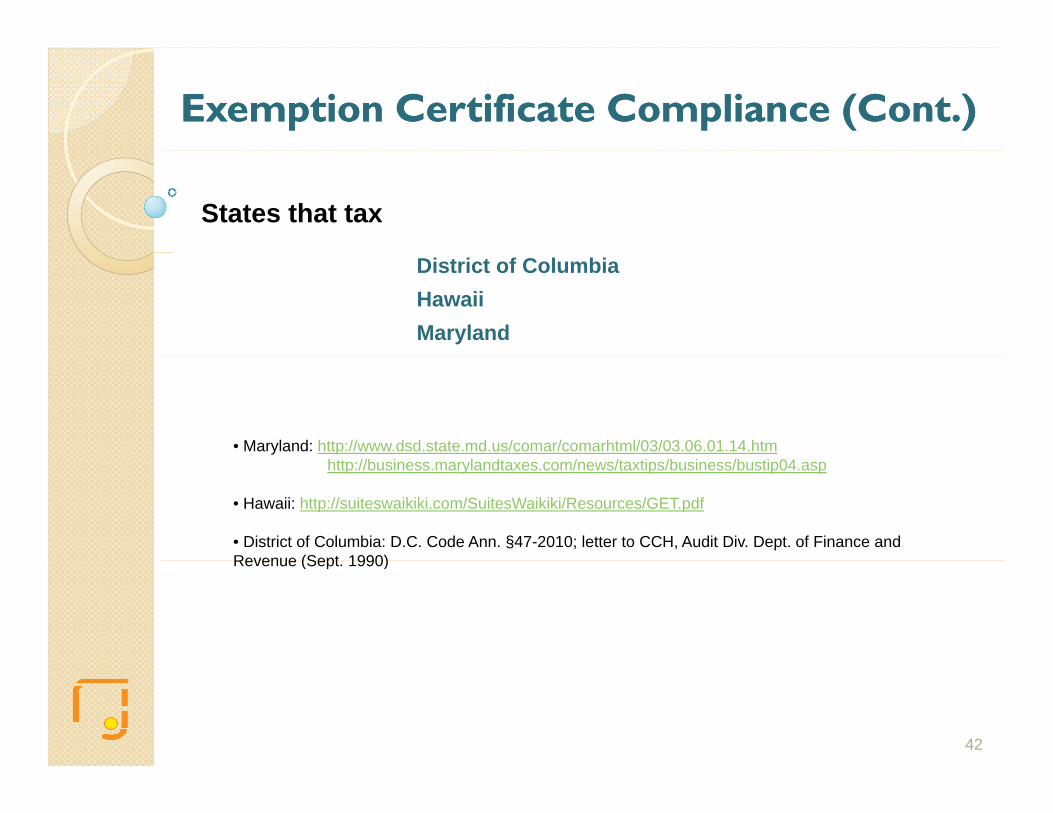

States that tax

District of ColumbiaHawaiiMaryland

• Maryland: http://www.dsd.state.md.us/comar/comarhtml/03/03.06.01.14.htmhttp://business.marylandtaxes.com/news/taxtips/business/bustip04.asp

• Hawaii: http://suiteswaikiki.com/SuitesWaikiki/Resources/GET.pdf

• District of Columbia: D.C. Code Ann. §47-2010; letter to CCH, Audit Div. Dept. of Finance and Revenue (Sept 1990)Revenue (Sept. 1990)

42

SST Drop Ship RuleSST Drop Ship Rule

Sect. 317: Administration of exemptions

A. Each member state shall observe the following provisions when a purchaser claims an exemption:

8. In the case of drop shipment sales, member states must allow a third party vendor (e.g., drop shipper) to claim a resale exemption based on an exemption certificateresale exemption based on an exemption certificate provided by its customer/re-seller or any other acceptable information available to the third party vendor evidencing qualification for a resale exemption, regardless of whether the customer/re-seller is registered to collect and remit sales and use tax in the state where the sale is sourced.

43

State Sales Tax Audits: GeneralState Sales Tax Audits: General

• States are becoming more aggressive in audits.

• Nexus is being redefined in many states.

• Keep organized and track expirations

• Train your staff and keep aware of changing state regulationsTrain your staff and keep aware of changing state regulations.

• Penalties are increasing.

44

Audits: Drop ShipmentAudits: Drop Shipment

Drop shipment audits, from a different point of view

Supplier – sales tax: Exemption certificates were not correctly collected. Tax was not correctly charged. Do you have shipping documents to prove the items came from out of state?

Customer – use tax: Was tax accrued for the items being purchased from the seller, if they were taxable? It is very likely that the auditor will not audit the seller, if no nexus is established. Having said that, the auditor will likely try to find out if the seller should be registered in its state.

Seller – Because the transaction is being scrutinized in two differentSeller – Because the transaction is being scrutinized in two different instances, it might flag your company for audit based on evidence that you might have nexus.

45

Audits: Drop Shipment (Cont.)Audits: Drop Shipment (Cont.)

Double-taxationIf the customer accrues tax, and the buyer pays tax to the supplier, then y p y ppthe state has been paid twice for the same items. This information could be helpful if the customer is being audited, and the items purchased are determined to be taxable and no accrual was in place.

Regulation changes For example, Wisconsin passed legislation to comply with Streamlined Sales Tax Project drop shipment rules. This does not mean you are off the hook; the changes occurred effective Oct. 1, 2009, and the audits cover usually a four-year period. http://www.revenue.wi.gov/taxpro/news/100119.html

Auditors’ educationSometimes, you know might know more than the auditor. For example, the states that recently joined SST have not spent enough time

t i i th i dit f d th i ht b l i SSTretraining their audit force, and they might be relying on non-SST information.

46

Vytenis Kirvelaitis, Grant Thornton

PROBLEMATIC STATES

Vytenis Kirvelaitis, Grant ThorntonIrwin Mittleman, Meridian Global Services

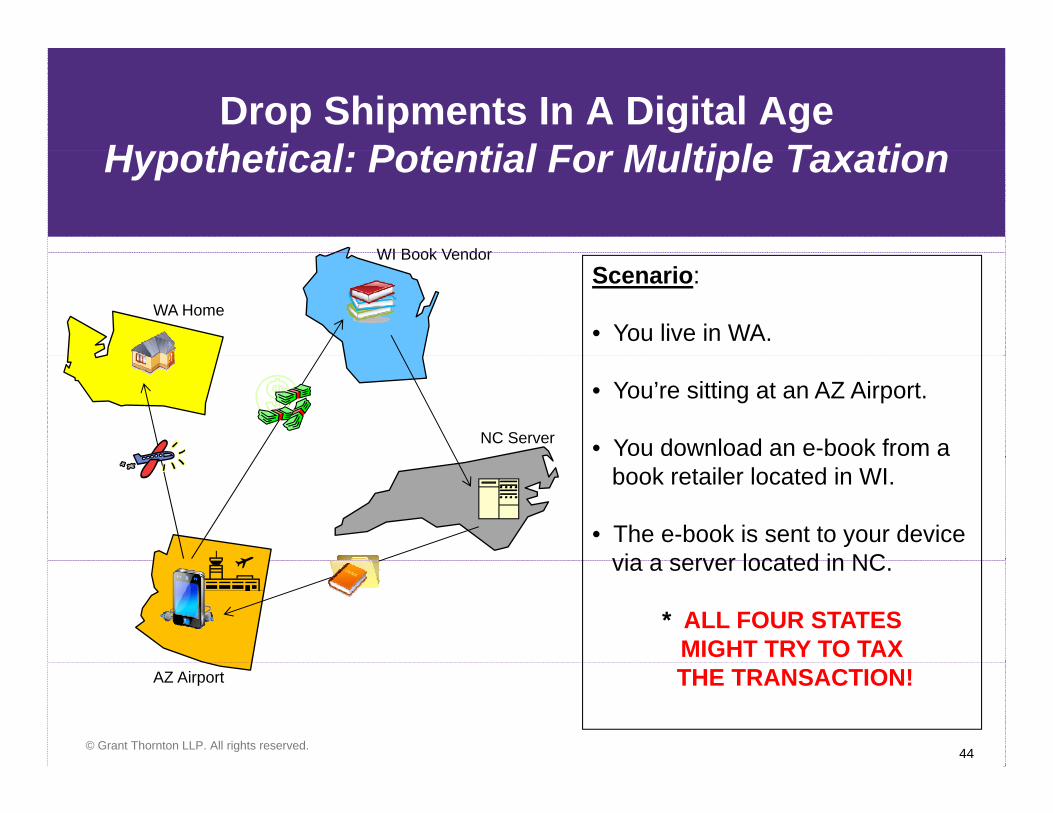

Drop Shipments In A Digital AgeH th ti l P t ti l F M lti l T tiHypothetical: Potential For Multiple Taxation

WI Book VendorScenario:

• You live in WA.

WI Book Vendor

WA Home

• You’re sitting at an AZ Airport.

• You download an e-book from a NC Server

book retailer located in WI.

• The e-book is sent to your device via a server located in NCvia a server located in NC.

* ALL FOUR STATES MIGHT TRY TO TAX

© Grant Thornton LLP. All rights reserved.

THE TRANSACTION!AZ Airport

44

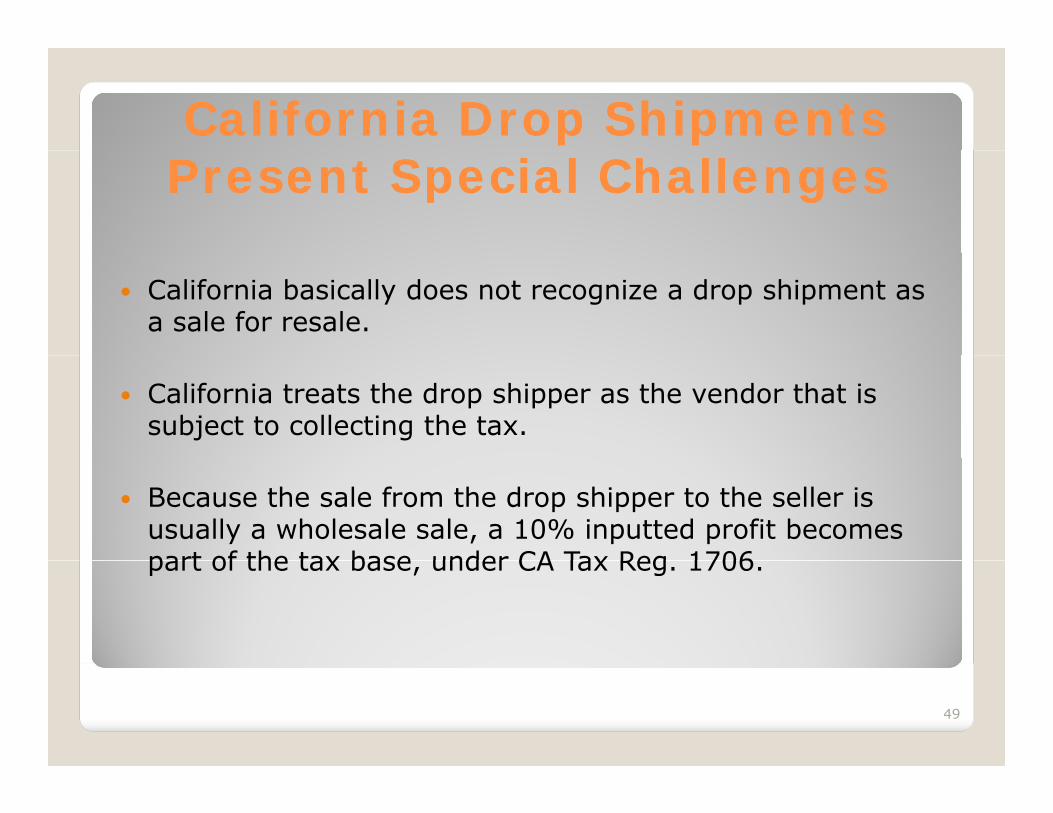

California Drop ShipmentsCalifornia Drop ShipmentsPresent Special ChallengesPresent Special Challenges

California basically does not recognize a drop shipment as a sale for resale.

California treats the drop shipper as the vendor that is subject to collecting the tax.

Because the sale from the drop shipper to the seller is usually a wholesale sale, a 10% inputted profit becomes part of the tax base under CA Tax Reg 1706part of the tax base, under CA Tax Reg. 1706.

49

S h D k G idS h D k G idSouth Dakota GuidanceSouth Dakota Guidance South Dakota holds the supplier liable for the tax if it does South Dakota holds the supplier liable for the tax if it does

not get a resale certificate from the seller.

The resale certificate can be from another state The resale certificate can be from another state.

Failure to get this documentation makes the supplier liable for the tax under Drop Shipments SD Tax Facts May for the tax, under Drop Shipments, SD Tax Facts, May 2011.

50

C i R li 2003C i R li 2003 22Connecticut Ruling 2003Connecticut Ruling 2003--22 An in-state supplier that sells to an out-of-state seller is

making a retail sale under Conn Gen Stat Sect 12making a retail sale, under Conn Gen Stat. Sect. 12-407(a)(3) (A).

D li f d t i C ti t b h lf f t f t t Delivery of product in Connecticut on behalf of out-of-state customers is a retail sale.

Th t i b d th i th t th li i h i The tax is based on the price that the supplier is charging the out-of-state customer, i.e. the wholesale price.

51

M h R liM h R liMassachusetts RulingMassachusetts Ruling TIR 04-26 requires a supplier with nexus in Massachusetts

that sells to a retailer with no nexus in Massachusetts but that sells to a retailer with no nexus in Massachusetts, but that ships to customer in Massachusetts, to collect the tax.

T i i d th t il l t Tax is imposed on the retail sales amount.

The ruling specifically targets Internet sellers that utilize i t t liin-state suppliers.

52