driving force nov/dec 2012

DESCRIPTION

New York Independent Automobile Dealers Association Magazine for November and December 2012TRANSCRIPT

NOVEMBER/DECEMBER 2012

• BE ON THE LOOKOUT FOR OPEN RECALLS• TECHNOLOGY’S GROWING ROLE IN POST-RECESSION MARKET• COMPLIANCE OVERDRIVE

inside

BHPH Sales vs. Collection Is it really a battle, or are they one and the same?

PRSRT StandardU.S. Postage

PAIDDALLAS, TEXASPermit No. 2079

V i s i t u s a t w w w . n e w y o r k i a d a . o r g

T H E N E W Y O R K

N E W Y O R K I N D E P E N D E N T A U T O M O B I L E D E A L E R S A S S O C I A T I O N

DRIVING FORCEPage 14

NY_1112.indd 1 10/17/12 10:14 AM

NY_1112.indd 2 10/17/12 10:14 AM

NY_1112.indd 3 10/17/12 10:14 AM

T H E N E W Y O R K D R I V I N G F O R C E NOVEMBER/DECEMBER 2012

4

w w w . n e w y o r k i a d a . o r g

WHAT’S NEW

MAGAZINE CONTENTS

ADVERTISERS INDEX

06 Join Your Independent Dealers Association08 Government Report10 Technology’s Growing Role12 Look Out for Open Recalls14 BHPH Success: Sales vs. Collection16 Money Matters18 Compliance Overdrive

OFFICE

ADESA .............................................Inside Front CoverAlly ............................................................................9Auto Use .................................................................16AutoTrader.com .........................................Back CoverCorry Auto Dealers Exchange ..................................17Dealer Center ..........................................................13Dealer Services Corp. ...............................................5 Dodah.com .............................................................15Manheim New York .........................Inside Back Cover Protective ...............................................................11STARS GPS ..............................................................3Voisys ......................................................................18Westlake Financial ....................................................7

inside

NATIONAL INDEPENDENT AUTOMOBILE DEALERS ASSOCIATIONWWW.NIADA.COM • WWW.NIADA.TVNIADA HEADQUARTERS: 2521 BROWN BLVD. • ARLINGTON, TX 76006-5203 PHONE (817) 640-3838FOR ADVERTISING INFORMATION CONTACT: TROY GRAFF (800) 682-3837 OR [email protected] New York Driving Force is published bi-monthly by the National Independent Automobile Dealers Association Services Corporation, 2521 Brown Blvd., Arlington, TX 76006-5203; phone 817-640-3838.Periodicals postage paid at Dallas, TX and at additional offices. POSTMASTER: Send address changes to NIADA State Publications, 2521 Brown Blvd., Arlington, TX 76006-5203. The statements and opinions expressed herein are those of the individual authors and do not necessarily represent the views of New York Driving Force or the National Independent Automobile Dealers Association. Likewise, the appearance of advertisers, or their identification as members of NIADA, does not constitute an endorsement of the products or services featured. Copyright (c) 2011 by NIADA Services, Inc. All rights reserved.

STATE MAGAZINE MGR./SALES Troy Graff • [email protected] Andy Friedlander • [email protected] DIRECTOR Christy Haynes • [email protected] Nieman Printing

4

FOR INFORMATION ON HOW TO BECOME A MEMBER OF THE NYIADA, PLEASE CONTACTPAULA FRENDEL (855) 694-2324 [email protected]

www.niada20groups.comNIADA 20 Groups are designed for NIADA’s independent dealers as they do business today – retail, BHPH or a little bit of both.

FREE Dealer Education on www.niada.tv• Waking the Economy Up from a Bad Dream • Automotive Outlook: Back from the Brink, Now

for the Golden Age • Protecting Our American Dream

Studies Say Consumers Interested in Alternative PowertrainsAccordingtotwonewstudies,driverswantandwillpayformorefuel-efficientcars,

including hybrids and plug-in cars.Ford Motor Co. hired Penn Schoen Berland to con duct a study that found seven in

10 dri vers are tak ing steps to reduce gaso line con sump tion. A quar ter of them told researchers that if they had an extra $1,000 avail able at the time of their next vehi cle pur chase, they would pre fer a hybrid over a con ven tion ally pow ered vehicle.

In another study con ducted by Phoenix Mar ket ing Inter na tional, a solid major-ity of Amer i can motorists say they’re now will ing to con sider some form of alter na tive propulsion, whether it’s hybrid, pure battery-electric or some thing else even more radical.

The study found con sumers in the lux ury mar ket more open to alter na tive tech nolo-gies by a mar gin of three-to-one. For main stream prod uct seg ments, the margin of those willing to consider alternatives was closer to two-to-one. Car buyers under 40 years old are even more inter ested – only 10 percent of them are not open to cleaner or more fuel-efficientpowertraintechnology.

F U N FAC T

NY_1112.indd 4 10/17/12 10:14 AM

NY_1112.indd 5 10/17/12 10:14 AM

T H E N E W Y O R K D R I V I N G F O R C E NOVEMBER/DECEMBER 2012

6

w w w . n e w y o r k i a d a . o r g

N U M B E R S M AT T E R . T H E Y G I V E U S P OW E R . W E A R E P OW E R F U L A S A G RO U P A N D N O T S O M U C H A S I N D I V I D UA L S .

Join your Independent Dealers Association NowIt’s 3 a.m., and I am writing this blurb before

we start a day that includes getting 700 units in and ready for auction this Thursday and Friday on the wholesale side, putting out fires on the after-auction side, a bunch of meetings dealing with project management on the technology side, hiring new people, timelines/ prioritization of projects, and dealing with an ongoing IRS audit (six months into it on five separate companies/entities).

So why do I want every dealer in the country to join his independent dealers association?

I’m sure you’re saying, “Who gives a rat’s back end what time it is, what you’re doing and why you want me to join?”

You can’t BS me. I know you.OK, here’s the deal. I’ll pay. You got it, I’ll pay,

so it costs you zippo to join.You’re too cheap to pull up a couple hundred

out of your pocket? No sweat, I’ll pay.Read on and I’ll tell you why you are going to

join your dealers association, at no additional cost to you.

If you haven’t joined until now, or you belonged before and never saw the value and quit, or you say you’re too busy, or you are apathetic, or you don’t know why you should because you can’t see what’s in it for you, or are so cheap you don’t want to reach in your pocket for a couple of shekels because you can’t see the value because you are too busy to stop and understand, I’m paying for you.

Ready to pay attention?Numbers matter. They give us power. We

are powerful as a group and not so much as individuals. Together we generate billions of dollars in revenue and support businesses way bigger than ourselves. We employ hundreds of thousands of people. We spend big money.

Think about it. We spend billions in workers comp, trucking, recon products, insurance of all kinds, at auctions, with financial institutions, at body shops, at dealerships, at bid lots, on parts, making keys, at ports, on advertising (all kinds of advertising), on accountants and lawyers, with website designers and computer programmers, in gas, on tolls, renting/buying properties to run our businesses, on taxes, zoning and 1,147 other important things too boring to mention, helping make all of those entities bigger and better – which, in general, helps the economy move.

We are the grass roots of free enterprise. Start with an idea – um, I want to buy something and sell it for little more. Good idea, right? Ever have that idea? Why?

Because if you do it enough times it will liberate you. You become a free spirit responsible only (initially) to yourself and your family. Work is no longer work because you are doing it for yourself.

If you haven’t experienced it you obviously

aren’t a used car dealer. It’s what drives us to get up early and go to bed late. It is the definition of freedom in my world.

So enough nauseous rambling. Here is the point, and why I’ll pay your fee to join. You can’t wait to see how I’m going to close you, can you? You’re going to love it.

Ever hear of Consumer Reports? Ever hear of dealer financing?

Start with Consumer Reports. You know what it does. It rates things.

If we all belong to a nonprofit organization, what do you think that organization can do for us? Rate things, all things. We will rate auctions, truckers, financial institutions, recon shops, insurance companies, accountants, lawyers, bid lots, politicians, auction policies, products, sellers at auctions and captive sellers at auctions by name brand. Why you can even rate us to be sure what we say is true.

It gets better than that. They can rate us, and with that rating we can bargain with them. Everybody wants to sell us something. Let’s use the organization to rate them so we all know what others in our group have experienced.

What about forming our own dealers financial institution that lends only to us? Sounds silly? Not too silly. Don’t forget, the average dealer is paying up to 25 percent interest on the money he borrows from financial services. Do the math. It isn’t a beef, it’s a fact.

If dealers are able and willing to pay that, wouldn’t it be better for us, the dealers’ body, to have ownership in the entity that is able to charge usury rates with near-zero exposure?

Sound silly? Use a few hours of road time traveling to your next auction or bid lot thinking about it. I have. For four decades.

Not only is it true and the concept correct, but the solution is in hand. We’ve set up a financial institution we all can own shares in, and have total transparency into the operations of, and not only control who and how we lend, but leverage peer pressure to ensure borrowers are kept in check to the point they will pay our bank back what they have borrowed before they pay the food bill at home.

Peer pressure is a powerful thing. Look at your 9-year-old kids if you don’t think so. More on request – or in our next article.

So why join, and why join a nonprofit? Join because it gives us weight, power, bargaining power, influence and possibilities we don’t have as individuals. We become a franchise of our own, helping guide our own destiny.

Why a non-profit? Because there is no special interest to squelch the message or distort the intent of the goals. If we all belong, think about the consumer report. That baby will have power to make things happen, for our benefit, period.

It is the ultimate form of free speech, and

baby, I love freedom and free speech. I prefer death over lack of freedom, and that is no exaggeration.

We have been given this organization to connect and take advantage of our freedom. It feels good, but it’s going to feel better when we have 50,000 independent dealers who belong to and enjoy the benefits you get from being part of our organization.

So, I’ll pay for your subscription. How? I’ll take $20 off the purchase of every car I sell you until we hit the amount it costs you to join your state’s independent auto dealers association.

I am inviting any branch to come to the auction and use the table in my lanes to advertise and sign up dealers willing to join your organization. You are also welcome to use any of my facilities to promote, sign up and educate any dealer with an interest in becoming a member. I’ll pay.

Our goal is to increase membership to include everybody, no exceptions. That translates, in our region, to 30,000 dealers.

I sell 500-700 units a week. I sell 80 percent of my cars to independent dealers like you. On a good day at Manheim, I have about 1,000 dealers online and another 2,500 in the lanes. That’s one auction on one day. So 30,000 dealers is not an unrealistic number. There is no doubt in my mind we can get everybody in, and I am willing to share the cost because I think the end game is big.

A consumer report function puts real power in the organization. It won’t work unless we have everybody in. But when we have everybody in, it won’t just work, it will be to our benefit. Not small – big, real big, huge, massive. You won’t only be free, you will feel the power of free and big, real big.

Many entities have us as customers, clients, doormats, etc., and make us do dances for them while we are their customer. It doesn’t sound right to me. Feels worse. But not bad enough to give up my freedom for a roof, not close.

But I know that with a united voice and agenda, we not only can keep our freedom, we can cause others who make us dance to their music instead dance to our collective music. Like it or not, sir, numbers matter.

Beyond that, a lending facility, owned by dealers, is not only possible but ready to fly.

We can have an influence on our future. We just have to use our collective power and brain to our advantage.

Sell Well,Robert Hollenshead

BY ROBERT HOLLENSHEADROBERT HOLLENSHEAD, FOUNDER OF HOLLENSHEAD AUTO SALES, INC., OF MANHEIM, PA., CALLS HIMSELF THE LARGEST INDEPENDENT WHOLESALE CAR DEALER IN HISTORY, WITH ANNUAL REVENUES APPROACHING $500 MILLION.

NY_1112.indd 6 10/17/12 10:14 AM

NY_1112.indd 7 10/17/12 10:14 AM

T H E N E W Y O R K D R I V I N G F O R C E NOVEMBER/DECEMBER 2012

8

w w w . n e w y o r k i a d a . o r g

A R U N D OW N O F S O M E O F T H E L AT E S T G OV E R N M E N TA L I S S U E S A N D AC T I V I T Y A F F E C T I N G T H E U S E D CA R I N D U S T RY

Government ReportHere’s a rundown of some of the

latest governmental issues and activity affecting the used car industry from Sante Esposito of Federal Advocates and NIADA legislative/regulatory/compliance counsel Shaun Petersen.

Consumer Financial Protection Bureau

Procedural rules to establish supervisory authority over certain nonbank covered persons based on risk determination: The CFPB says it canassertjurisdictionoveranyfinancialentity that otherwise is not covered underthedefinitionofa“largermarketparticipant” if the CFPB has reasonable cause to believe such an entity is posing a risk to the market.

That proposed procedural rule has the potential to impact our members that are nototherwisedefinedaslargermarketparticipants.

The procedural rules outline the processunderwhichtheCFPBwouldfindan entity to be a risk and the process by which that entity is entitled to challenge the proposed determination before being subject to the CFPB’s supervision. If the CFPBstaffhas“reasonablecause”tobelieve the entity is a risk, the deputy director will send a written notice to the entity explaining the why the bureau believes that risk exists.

It will then provide an opportunity for the entity to respond in writing and to participate in an informal telephone hearing between the CFPB staff and the assistant director. The response from the entity would include any written information the CFPB could and should consider.

After the informational hearing, the assistant director would submit a written proposed order to the director of the CFPB to bring the entity under the supervisory oversight of the CFPB. If the determination is made to supervise the entity, the CFPB will do so for a minimum of two years and can make a petition to be relieved of that obligation after that time, but only once annually.

We reviewed these proposed rules and found several concerns we asked the CFPB to consider through comments submittedtoit.Ourfirstsignificantconcern was the lack of clarity from the

bureau as to the type of conduct the bureaubelievesis“reasonablecause”tofindanentitytobearisk.Theproposedruledoesnotdefine“reasonablecause”or provide any framework of conduct the bureau believes would create the risk.

We asked the CFPB to revise the rule to providethisdefinition.WealsoaskedtheCFPB to limit the risk to inappropriate or undisclosedfinancialrisktotheconsumerso the scope of misconduct the bureau would attempt to regulate is not overly broad.

Second, we raised concerns about the information used to make that determination. Presumably, much of the information will be made on consumer complaints, but the rules do not specify the information the bureau will use in making its risk determination. We asked the bureau to address that.

We also pointed out what we considered an unfair process, notwithstanding the CFPB’s attempt to keep it informal. The procedures proposed in the draft rule would not allow entity potentially subject to conduct to exercise discovery and examine the same material the CFPB reviewed in making its determination. The rule would not allow an entity to depose witnesses, review documents, ask interrogatories of either consumer complainants or CFPB staff as to what formsthebasisofthe“reasonablecause.”

We believe it is patently unfair to be placed at such a disadvantage when compared to the CFPB staff, which has access to consumers or other information in making its determination. An entity should be provided the same level of access in order to properly defend itself.

We also asked the CFPB to consider allowing an entity the opportunity to rebut the assistant director’s recommendation to the director beforetheDirectormakeshisfinalrecommendation.

Regulation Z: The CFPB has proposed a number of changes to Reg Z in the mortgage arena. While it does not directly affect the automotive industry, it could be an indicator for proposed regulations in the near future.

The proposed mortgage regulation would require prompt crediting of payments on mortgage loans and prompt response time for payoff amount inquiry.

Reg Z already requires higher-price mortgage lenders to look at the consumer’s ability to repay the loan before lending. The CFPB amended the regulation to expand its scope to any credit transaction secured by a dwelling. That rule becomes effective Jan. 21.

The CFPB is proposing changes to thedefinitionof“financecharge”inamortgage transaction by eliminating certain exclusions that were not otherwise considered when calculating an APR. The CFPB has invited comments on the proposed changes to be submitted by Nov. 6. We will analyze the proposed change for any potential impact if something similar wasadoptedintheautofinancesector.

Rental CarsA month after Rep. Lois Capps

(D-Calif.) introduced H.R. 6094, which prohibits the rental of motor vehicles under a safety recall until the defect or noncompliance is remedied, Sen. Barbara Boxer (D-Calif.) introduced S. 3502, the Raechel and Jacqueline Houck Safe Rental Car Act of 2012, with Sen. Feinstein (D-Calif.) as cosponsor.Thebill,amodificationofasimilar

bill introduced by Sen. Boxer in 2011, requiresnotificationbycarrentalcompanies to renters about any defect or noncompliance regarding the rented vehicle at issue, as well as imposing limitations on sales, leases or rentals by rental companies, holding rental companies to the same standard of responsibility as dealers with respect to various vehicle inspection, investigation and records requirements, and authorizing the Department ofTransportationtostudy“theeffectiveness of the amendments made by [the bill] and other related activities of rental companies.”

Federal Trade CommissionThe FTC recently held a roundtable

discussion about the issues facing consumers and businesses relating to onlinemarketingandprivacy,specificallyregarding mobile devices and social media websites. The roundtable was used as afact-findingtoolforpotentialfuturelegislation.

BY SHAUN K. PETERSEN AND SANTE ESPOSITO

NY_1112.indd 8 10/17/12 10:14 AM

NY_1112.indd 9 10/17/12 10:14 AM

T H E N E W Y O R K D R I V I N G F O R C E NOVEMBER/DECEMBER 2012

10

w w w . n e w y o r k i a d a . o r g

T H E P O P U L A R I Z AT I O N O F S M A R T P H O N E S A N D T H E W H I R LW I N D O F A P P S H AV E E M P OW E R E D T H E I N D U S T RY

Growing Role of Technology in Post-Recession MarketHeading into the fourth quarter of

2012, industry leaders continue to point to market trends that forecast the end of the recession. As a result of increased availabilityofrental,fleetandnewcartrades at auction and continued strong new car sales, the industry will see nearly one million more vehicles in the market in 2012.

The current challenge for many independent car dealers is sourcing the right inventory as wholesale used car prices decline. The industry continues to stabilize since the peak of the recession. However, the lasting effects of the recession will continue to impact the market as we once knew it.

The extreme market conditions brought on by the recession have produced a unique set of challenges for the independent used car dealer. With sharply climbing gas prices since 2007 and 2008, the market had experienced a negative impact on large truck and SUV sales. Overall used car supplies dropped substantially with the removal of more than 750,000 units by the Cash for Clunkers program.

Those market changes resulted in artificiallyhighusedcarprices,whichmade sourcing vehicles even more difficultfortheaverageusedcardealer.Whilethedifficultmarketforcedoutmanydealersduringthepastfiveyears,a new crop of dealers has recently emerged. Those dealers are turning to technology to drive their businesses and maintain a competitive edge.

The reliance on technology has increasedsignificantlyintheautomotivesector. This permanent change has helped dealers in all areas of their business. Sourcing inventory is one of the major avenues in which dealers are using technology to assist in their “newbusiness”flow.Manydealersare turning to consumer direct online

portals and wholesale online platforms to supplement purchases at traditional auction facilities.

In addition, the popularization of handheld smartphone devices and the whirlwind of available apps have empowered the industry to source, assess, value and purchase inventory from the tools in the palms of our hands. In fact, the market is rife with smartphone app solutions for every step in the life cycle of a used car.

Choosing the right products and services can take some time, but trying to run a dealership operation without the right tools to stay ahead of the competition takes even more time.

With sourcing issues easing in 2012 and used car prices continuing to stabilize, the rest of the year should produce new opportunities for dealers. But staying on top of local price trends isamusttoensureprofitmarginsstaystrong and overall sales increase.

Speculating on inventory levels and pricing heading into tax season can hurt some dealers if consumer demand and pricesdropsharply.Marketfluctuations,softer prices and macroeconomic factors are all challenges dealers could face in the next few months.

Technology can help dealers stay on top of those trends.

Partnering with technology-based companies that are positioned to forecast market trends and adapt according to industry needs should be an integral part of a dealer’s success in the post-recession marketplace. Dealers should look to align with companies that not only offertechnologyproductsthatfittheirbusiness needs and scale of operations, but that also back their products with superior customer service.

Tech solutions should allow dealers tobemoreefficientandeffectivesotheycan focus on core dealership operations.

Dealers should look for solutions that focus on turning inventory faster while increasingprofitmargins.

Today’s technology can provide dealers the real-time data needed to do just that — appraisal tools, real-time reporting, markettrendsonspecificvehiclesanddays’ supply. All are things a successful dealerwillfindimportantasawaytostayon top of market conditions.

Additionally, a technology platform that requires dealers to make large-scale changes to their business operations might not be the right choice for all dealers. Technology solutions should enhance a dealer’s successful business practices and provide a consistent means to providing market data.

As we enter a more technologically-driven marketplace, the resilience, determination and entrepreneurial drive of used car dealers continues to inspire companies like DSC to provide the right products and services backed with superior customer service. Since 2005, Dealer Services Corporation has worked to bring innovative technology solutions to our dealer and auction partners to makefloorplanfinancingaseamlessbusiness solution.Withstateoftheartandindustry-first

technology offerings like the myDSC virtualofficeandtheDSCUnplugged™mobile smartphone application, DSC provides the support today’s dealers look for in a business partner. DSC is proud to serve independent car dealers and looks forward to long partnerships with its customers in navigating the post-recession market.

BY BRIAN GEITNERBRIAN GEITNER IS PRESIDENT AND CO-FOUNDER OF DEALER SERVICES CORPORATION, THE LARGEST INDEPENDENT INVENTORY FINANCE PROVIDER FOR USED AUTOMOBILES, AND HAS MORE THAN 20 YEARS OF EXPERIENCE IN THE AUTO FINANCE INDUSTRY. FOR MORE INFORMATION ABOUT DSC, VISIT WWW.DISCOVERDSC.COM.

NY_1112.indd 10 10/17/12 10:14 AM

Growing Role of Technology in Post-Recession Market

NY_1112.indd 11 10/17/12 10:14 AM

T H E N E W Y O R K D R I V I N G F O R C E NOVEMBER/DECEMBER 2012

12

w w w . n e w y o r k i a d a . o r g

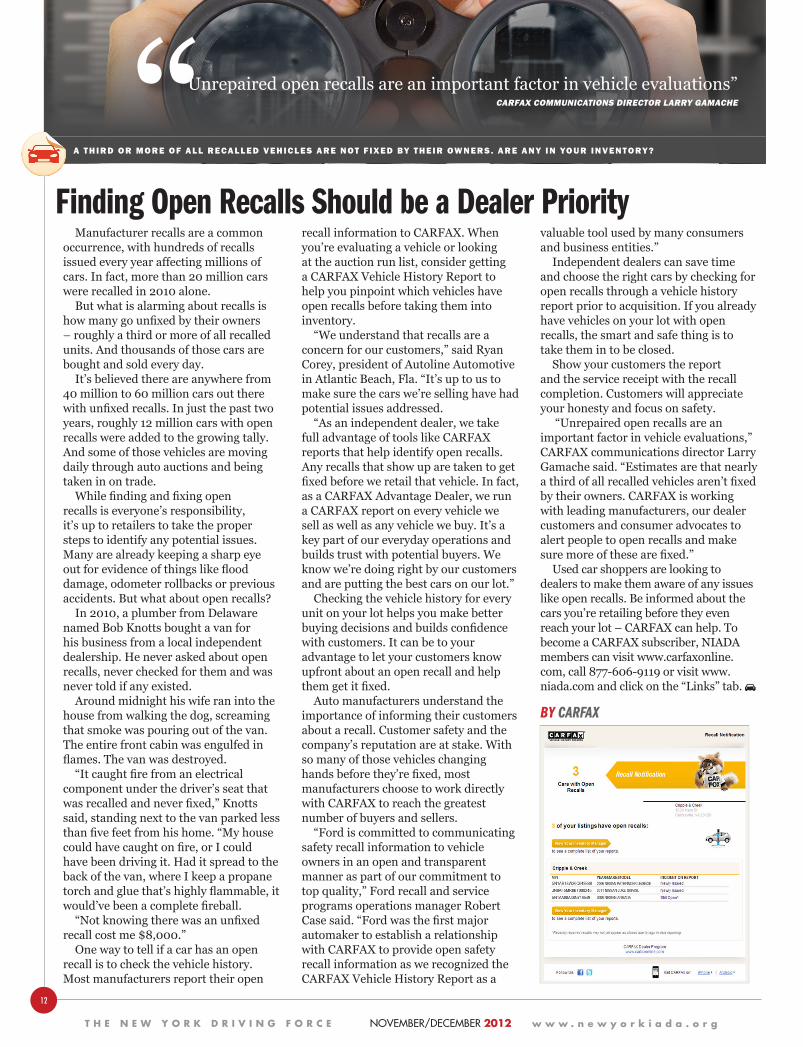

A T H I R D O R M O R E O F A L L R E CA L L E D V E H I C L E S A R E N O T F I X E D BY T H E I R OW N E R S . A R E A N Y I N YO U R I N V E N T O RY ?

Finding Open Recalls Should be a Dealer PriorityManufacturer recalls are a common

occurrence, with hundreds of recalls issued every year affecting millions of cars. In fact, more than 20 million cars were recalled in 2010 alone.

But what is alarming about recalls is howmanygounfixedbytheirowners– roughly a third or more of all recalled units. And thousands of those cars are bought and sold every day.

It’s believed there are anywhere from 40 million to 60 million cars out there withunfixedrecalls.Injustthepasttwoyears, roughly 12 million cars with open recalls were added to the growing tally. And some of those vehicles are moving daily through auto auctions and being taken in on trade.Whilefindingandfixingopen

recalls is everyone’s responsibility, it’s up to retailers to take the proper steps to identify any potential issues. Many are already keeping a sharp eye outforevidenceofthingslikeflooddamage, odometer rollbacks or previous accidents. But what about open recalls?

In 2010, a plumber from Delaware named Bob Knotts bought a van for his business from a local independent dealership. He never asked about open recalls, never checked for them and was never told if any existed.

Around midnight his wife ran into the house from walking the dog, screaming that smoke was pouring out of the van. The entire front cabin was engulfed in flames.Thevanwasdestroyed.“Itcaughtfirefromanelectrical

component under the driver’s seat that wasrecalledandneverfixed,”Knottssaid, standing next to the van parked less thanfivefeetfromhishome.“Myhousecouldhavecaughtonfire,orIcouldhave been driving it. Had it spread to the back of the van, where I keep a propane torchandgluethat’shighlyflammable,itwould’vebeenacompletefireball.“Notknowingtherewasanunfixed

recall cost me $8,000.”One way to tell if a car has an open

recall is to check the vehicle history. Most manufacturers report their open

recall information to CARFAX. When you’re evaluating a vehicle or looking at the auction run list, consider getting a CARFAX Vehicle History Report to help you pinpoint which vehicles have open recalls before taking them into inventory.“Weunderstandthatrecallsarea

concern for our customers,” said Ryan Corey, president of Autoline Automotive inAtlanticBeach,Fla.“It’suptoustomake sure the cars we’re selling have had potential issues addressed.“Asanindependentdealer,wetake

full advantage of tools like CARFAX reports that help identify open recalls. Any recalls that show up are taken to get fixedbeforeweretailthatvehicle.Infact,as a CARFAX Advantage Dealer, we run a CARFAX report on every vehicle we sell as well as any vehicle we buy. It’s a key part of our everyday operations and builds trust with potential buyers. We know we’re doing right by our customers and are putting the best cars on our lot.”

Checking the vehicle history for every unit on your lot helps you make better buyingdecisionsandbuildsconfidencewith customers. It can be to your advantage to let your customers know upfront about an open recall and help themgetitfixed.

Auto manufacturers understand the importance of informing their customers about a recall. Customer safety and the company’s reputation are at stake. With so many of those vehicles changing handsbeforethey’refixed,mostmanufacturers choose to work directly with CARFAX to reach the greatest number of buyers and sellers.“Fordiscommittedtocommunicating

safety recall information to vehicle owners in an open and transparent manner as part of our commitment to top quality,” Ford recall and service programs operations manager Robert Casesaid.“Fordwasthefirstmajorautomaker to establish a relationship with CARFAX to provide open safety recall information as we recognized the CARFAX Vehicle History Report as a

valuable tool used by many consumers and business entities.”

Independent dealers can save time and choose the right cars by checking for open recalls through a vehicle history report prior to acquisition. If you already have vehicles on your lot with open recalls, the smart and safe thing is to take them in to be closed.

Show your customers the report and the service receipt with the recall completion. Customers will appreciate your honesty and focus on safety.“Unrepairedopenrecallsarean

important factor in vehicle evaluations,” CARFAX communications director Larry Gamachesaid.“Estimatesarethatnearlyathirdofallrecalledvehiclesaren’tfixedby their owners. CARFAX is working with leading manufacturers, our dealer customers and consumer advocates to alert people to open recalls and make suremoreofthesearefixed.”

Used car shoppers are looking to dealers to make them aware of any issues like open recalls. Be informed about the cars you’re retailing before they even reach your lot – CARFAX can help. To become a CARFAX subscriber, NIADA members can visit www.carfaxonline.com, call 877-606-9119 or visit www.niada.comandclickonthe“Links”tab.

BY CARFAX

“Unrepaired open recalls are an important factor in vehicle evaluations” CARFAX COMMUNICATIONS DIRECTOR LARRY GAMACHE

NY_1112.indd 12 10/17/12 10:15 AM

NY_1112.indd 13 10/17/12 10:15 AM

T H E N E W Y O R K D R I V I N G F O R C E NOVEMBER/DECEMBER 2012

14

w w w . n e w y o r k i a d a . o r g

I S I T R E A L LY A B AT T L E , O R A R E T H E Y O N E A N D T H E SA M E ?

BHPH Success: Sales vs. CollectionThe very last thing I wish to do is start

an article by upsetting the salesperson who is out on the front line of a Buy Here-Pay Here dealership every day.

But let’s be honest. Selling a vehicle to customers with terrible credit scores, not much (if any) money down and/or an abnormal quality of life is not a terribly complicatedordifficulttask.

The objective here is to get you, the dealer principal or general manager of a BHPH operation (no matter what the size), to reposition your thought process and put your priority and focus on the collection process – not the sales procedures – at your store. You need to invest your time as well as your dollars on training your salespeople,andallpersonnel,inthe“artof the collection.”

Let’s look at the entire process from the point of the typical BHPH customer. I have always contended you must always treat them as impulse or emotional buyers, even though they are credit-challenged.

They all still have the following major concerns: vehicle year, make and model; overall pricing structure; weekly, bi-weekly, or monthly payment; and mileage and overall condition of the vehicle.

Obviously there are many more issues associated with the average BHPH transaction at your dealership. But in general, when it comes right down to it, there is no price negotiating and no negotiating of the interest rate, and most of the time the dealership tells the customer which vehicle he or she can purchase that day. The salesperson does not have to overcome all the major objections listed above, and many more, as he or she wouldwhenfacingaconventionalfinancecustomer.

In most instances, the dealer is not overlyconcernedwithback-endprofits,oreven if any aftermarket products are sold, becausehewillbefinancingalltheextrasanyway. The only big objective left is the ever-important down payment. In reality, Mr. Dealer, you are the bank or lending institution and you solely determine what amount you will accept to proceed with the sale. Donotmisunderstand–first,youmust

always make a sale, and all the factors priortothataredefinitelyimportant,suchasfirstimpressions,cleanlinessofyourfacility, attitude of salespeople, dealership reputation and vehicle selection, etc.

What I am trying to get across is that havingafirst-ratequalitycollectionsystemin place will have a much greater effect on yourprofitsinaBHPHoperationthanagood selling process.

The real fact of the matter is you will notevenstarttomakeaprofitinmostcases until you are somewhere well into the age and depth of the note. So you have an obligation to convince each and every one of your customers that it is vitally important (and in their best interest) to make all payments on time as agreed.

Thus, this all-important and high-priority task now becomes the responsibility of your collectors.

So think with me here. Now your collectors become your salespeople.

Allow me to ask you honestly: Have you ever considered your collectors as salespeople?Thecollectorsmust“sell”oneach

and every contact why your customers must maintain their payment schedules as agreed and why they must maintain constant open communication at all times with their personal collector – whoops, I meantheir“salesperson.”

With a lot of small BHPH stores, the collectionprocessisleftuptoofficepersonnel and basically passed off under the category of a clerical job within the officeoperationsofthedealership.

Do you as the dealer principal or decision-maker contribute hands-on involvement on a daily basis to your own established collection process? Do you have a complete and through understanding of all your collection policies and procedures? Do your collectors (salespeople) exercise the proper attitude and demeanor when it comes to collecting on each and every personal contact?

Because I do business on a daily basis with BHPH dealers all over the United States, from single-point operations that sell 10-15 units a month to BHPH dealers with 65 million dollars worth of notes on the street, it jumps out at me that collections is the single most important process with the most direct effect and instant impact on whether or not you are successful as a BHPH dealer.

Many experts and consultants have thousands of ideas on how you can be successful in a conventional retail used car dealership. But with a BHPH operation, Mr. Dealer, you ain’t in the car business – you

areinthefinancebusiness.Youmustknowand understand the separation of the two entirely different operations and concepts.

If you are a current BHPH dealer or are considering getting into that part of our industry, the key to being successful is not rocket science. There are no magic pills you can take to establish and maintain a great BHPH operation with a professional and productive collection process.

Good collecting skills go hand and hand with good sales skills. Or are they both the same?

A negative and confrontational sales call or a bad retail experience out in front of the storereallytranslatesinto“nosaletoday.”A negative and confrontational collection callcanresultin“nomoney”foryoutoday, which can ultimately turn into an expensive repossession and/or a possible charge-off.

Both situations cost you money right now.I hope you I’ve helped you get the point

loudandclearandfindtheanswertothequestion: Is sales versus collection really a battle, or are they one in the same?

Prioritizing collections over sales sounds like it is out of proper sequence in the entire process, but really, it is not.

So, Mr. BHPH Dealer, why not take the necessary time and money to educate and train your collectors as salespeople as well as collectors?

Your answer should be that it just sounds like good old simple common sense.

BY ROD A. HEASLEYROD HEASLEY IS EXECUTIVE VICE PRESIDENT OF PERITUS PORTFOLIO SERVICES , A SOUTHLAKE, TEXAS-BASED SPECIALTY FINANCE COMPANY THAT SPECIALIZES IN THE PURCHASING OF OPEN BANKRUPTCY ACCOUNTS. HE HAS MORE THAN 30 YEARS’ EXPERIENCE IN THE RETAIL AUTOMOTIVE SALES INDUSTRY AND IS A NOTED WRITER AND SPEAKER ON THE SUBJECT. HE CAN BE REACHED AT [email protected] OR 866-8315954, EXT. 5.

NY_1112.indd 14 10/17/12 10:15 AM

NY_1112.indd 15 10/17/12 10:15 AM

T H E N E W Y O R K D R I V I N G F O R C E NOVEMBER/DECEMBER 2012

16

w w w . n e w y o r k i a d a . o r g

Congress enacted the federal Bankruptcy Code in 1978, and it has been amended several times since. The procedural aspects are governed by bankruptcy rules and the local rules of each bankruptcy (BK) court. There are 90 BK courts – one in every federal judicial district in the country.Thecourtofficialwiththedecision-

making power in each district is a United States bankruptcy judge. Much of BK process is administrative and conducted away from the courthouse. In Chapter 7 and 13 cases, the ones that affect dealers and lien holders, the process is carried out by a trustee.

What’s the Difference?The consumer bankruptcies that affect you

mostwillbefiledasChapter7orChapter13.Chapter 7 – liquidation: A chapter

7casedoesnotinvolvethefilingofaplan

of repayment, as in chapter 13. Instead, the trustee gathers and sells the debtor’s nonexempt assets and uses the proceeds to pay holders of claims (creditors) in accordance with the provisions of the Bankruptcy Code.

Chapter 13 – wage earner plan: Chapter 13 offers individuals a number of advantages over Chapter 7 liquidation, including an opportunity to save their homes from foreclosure.ByfilingunderChapter13,individuals

can stop foreclosure proceedings and may cure delinquent mortgage payments over time, though they must still make all mortgage payments that come due during the Chapter 13 plan on time.

Chapter 13 allows individuals to reschedule secured debts, other than a mortgage for their primary residence, and extend them over the life of the plan. That

could lower the payments. Chapter 13 also has a special provision that protects third parties who are liable with the debtor on “consumerdebts,”aprovisionthancanprotect co-signers.

Chapter 13 acts like a consolidation loan under which the individual makes payments to a trustee, who then distributes payments to creditors.

Any individual, even if self-employed or operating an unincorporated business, is eligible for Chapter 13 relief as long as the individual’s unsecured debts are less than $360,475 and secured debts are less than $1,081. A corporation or partnership cannot be a Chapter 13 debtor.

How Chapter 13 Works AChapter13casebeginsbyfiling

a petition with the bankruptcy court serving the area where the debtor has a

Understanding Your Customer’s Chapter 13 Bankruptcy

T H E F I R S T O F A T H R E E - PA R T S E R I E S O N T H E B A S I C S O F B A N K R U P T C Y P RO C E D U R E S A N D W H AT I T M E A N S T O D E A L E R S / L I E N H O L D E R S .

MONEY MATTERS

NY_1112.indd 16 10/17/12 10:15 AM

NOVEMBER/DECEMBER 2012 T H E N E W Y O R K D R I V I N G F O R C E

17

w w w . n e w y o r k i a d a . o r g

residence. Unless the court orders otherwise, the debtor must also file schedules of assets and liabilities, a schedule of current income and expenditures, a schedule of contracts and unexpired leases, and a statement of financial affairs.

When an individual files a Chapter 13 petition, an impartial trustee is appointed to evaluate the case and serve as a disbursing agent, collecting payments from the debtor and making distributions to creditors. The bankruptcy clerk gives notice of the bankruptcy case to all creditors whose names and addresses are provided by the debtor.

Between 21 and 50 days after the debtor files the petition, the trustee will hold a meeting of creditors. The debtor, the trustee and those creditors who wish to attend will then come to court for a hearing on the repayment plan.

The debtor must file a repayment plan with the petition or within 14 days after the petition is filed. The plan must be submitted for court approval and must provide for payments of fixed amounts to the trustee on a regular basis, typically biweekly or monthly. The trustee then distributes the funds to creditors according to the terms of the plan, which can offer creditors less than full payment on their claims.

If the debtor wants to keep the collateral securing a particular claim, the plan must provide that the holder of the secured claim receive at least the value of the collateral. If the obligation underlying the secured claim was used to buy the collateral – such as a car loan – and the debt was incurred within certain time frames before the bankruptcy filing, the plan must provide for full payment of the debt, not just the value of the collateral.

If the court confirms the plan, the trustee will distribute funds received under the plan “as soon as is practicable.”

Making the Plan WorkOnce the court confirms the plan, the debtor

must make the plan succeed by making regular payments to the trustee either directly or through payroll deduction, which requires living on a fixed budget for a prolonged period. While confirmation of the plan entitles the debtor to retain property as long as payments are made, the debtor cannot incur new debt without consulting the trustee.

Next: The basics of Chapter 7 filings.

Note: The information presented should not be cited or relied upon as “legal authority” and should not be used as a substitute for reference to the U.S. Bankruptcy Code and the Federal Rules of Bankruptcy Procedure.

BY ROD HEASLEY ROD HEASLEY IS EXECUTIVE VICE PRESIDENT OF PERITUS PORTFOLIO SERVICES , A SOUTHLAKE, TEXAS-BASED SPECIALTY FINANCE COMPANY THAT SPECIALIZES IN THE PURCHASING OF OPEN BANKRUPTCY ACCOUNTS.

Dealer’s Charity Event Ready to RollSanta’s Toy Run, a three-day racing event benefiting children’s charities, is coming up Nov.

30-Dec. 2 at Road Atlanta in Braselton, Ga.The event is run by Circle Heart Racing, a racing team dedicated to raising money to help

children in North Georgia and nationwide. Circle Heart was founded by Ron and Debbie Rigdon, owners of Ron’s Auto Sales in Lawrenceville, Ga., who were honored for their charitable work as the winners of the 2012 NIADA Manheim National Community Service Award.

Santa’s Toy Run will benefit five children’s charities. Admission to the event is free with the donation of a toy or gift card, and fans can also purchase full-speed race car ride-alongs and pledge donations for completed laps.

Circle Heart Racing has provided assistance to some 2,000 area children in the past six years. Last year’s Toy Run collected more than 1,500 toys and a raised record $9,000 in donations. For more information on how you can help, visit www.santastoyrun.org.

G I V I N G B AC K

NY_1112.indd 17 10/17/12 1:45 PM

T H E N E W Y O R K D R I V I N G F O R C E NOVEMBER/DECEMBER 2012

18

w w w . n e w y o r k i a d a . o r g

BY CHIP ZYVOLOSKICHIP ZYVOLOSKI IS A SENIOR ATTORNEY FOR INDIRECT LENDING AT WOLTERS KLUWER FINANCIAL SERVICES. FOR MORE INFORMATION, VISIT WWW.WOLTERSKLUWERFS.COM/INDIRECT.

The year’s end is a time of reflection.When it comes to auto finance and compliance

challenges, the story can sound similar from year to year. There are usually a handful of new regulations facing dealers and lenders that have made a big impact on the industry over the previous 12 months.

But this year doesn’t really fit the mold. That’s because 2012 arguably hasn’t been as much about new regulation as about the additional scrutiny of regulators enforcing laws that have been in place for some time.

That has been particularly evident in the areas of state-specific forms, model language and loan documentation.

Some recent examples suggest a trend that state regulators are taking a closer look at existing motor vehicle retail sales financing authority and transaction documentation:

New Mexico: Since 2009, a New Mexico attorney general’s regulation has required creditors to provide a summary or a translation of English-language transaction documents in consumer sales negotiated in a language other than English. Its coverage is very broad and

somewhat difficult to understand.This year, the New Mexico attorney general

proposed additional changes to the regulation. After receiving comments, the AG acknowledged issues with the proposed changes and with the existing regulation itself. As a result, it pulled back the changes and repealed the existing regulation to allow for further study.

Michigan: Years ago, the Michigan Department of Licensing and Regulatory Affairs, Office of Financial and Insurance Regulation (OFIR) said bad check charges are not allowed in motor vehicle retail contracts in spite of statutory authority that seems to allow it.

This year, the OFIR published a letter saying bad check charges cannot be collected on retail motor vehicle sales contracts unless the contract contains a bad check charge provision, indirectly reversing its prior position. The OFIR now holds that bad check charges are allowed as long as they are specifically authorized in the retail contract.

Montana: The Montana late charge authority is a bit ambiguous and has been that way for many years. Because of the ambiguity, there were vastly different interpretations in the marketplace. In response to a request, the Montana Division of Banking and Financial Institutions recently published a letter clarifying its interpretation of the state statute.

The apparently heightened state scrutiny might be just a coincidence. It could also be that states are demonstrating their diligence and control to the public and to the new federal Consumer Financial Protection Bureau (CFPB).

The CFPB regulates dealers who don’t routinely assign their financing contracts to unaffiliated third parties. For the most part, that means the CFPB regulates Buy Here-Pay Here dealers. The Federal Trade Commission (FTC) continues to regulate the rest of the auto sales and finance industry.

The net result is there are two federal regulators in the auto finance marketplace. It’s possible states are more actively clarifying and enforcing their existing laws and regulations in an effort to maintain a level of control over the auto finance industry – hoping to minimize federal oversight.

In addition to reflecting on the year that has been, it’s also time to think about what might lie ahead. What will the new regulatory environment look like in 2013?

Many thought the CFPB would have done a lot of regulatory change in auto financing by now, but that hasn’t been the case. One reason is it has been focused on real estate financing practices and disclosures. The CFPB also seems to be carefully studying the consumer finance marketplace – and even consumers – to lay a solid foundation for its regulatory oversight.

The CFPB’s strategic plan for 2013-18 notes one of its strategies is to “develop and maintain an efficient fact-based approach to developing, evaluating, revising and finalizing regulations.”

“Fact-based” is a key term. We have seen the

CFPB asking good questions and conducting extensive research on areas it is tasked with overseeing. For example, the CFPB tested draft real estate disclosure documents with consumers in shopping malls.

The Dodd Frank Act requires the CFPB to research and provide policy guidance on whether arbitration provisions should be allowed in consumer credit (non-real estate) transactions. To start that process, the CFPB published a request for suggestions, data sources and strategies to study the issue.

It’s also clear the CFPB is not afraid to take a fresh approach to presenting transaction information to consumers. For example, the CFPB published a proposed rule in July regarding integrated mortgage disclosures under RESPA and the Truth in Lending Act. Leading up to the proposed rule, it published a number of drafts trying various new disclosure formats and designs.

That was one of the first significant proposed rules from the CFPB, and the planning process involved extensive research and solicitation of industry and consumer feedback. As a result, the proposed rule and explanatory materials are more than 1,000 pages.

The upside is the CFPB is trying practical, consumer-tested ways to present information so average consumers can understand key transaction terms. The downside is the volume of information in the proposal is overwhelming.

It’s hard to know when the CFPB will complete its foundation-building and begin proposing new regulations or revising existing ones that affect the consumer auto finance industry. It’s likely big changes will come to the market. It’s just unclear when.

While we’re in this waiting period, dealers might feel there are a lot of variables out of their control, but the focus needs to be on the areas you can control.

Since a number of states seem to be focused on clarifying and enforcing existing requirements, dealers should review and button down compliance documentation and processes to make sure they are satisfying those requirements.

Additionally, reviewing and tightening transaction standards and communication within the dealership is key. Make sure your sales and finance teams are describing financing terms and options, vehicle features, and add-on products and services in a correct and consistent manner. Educate your buyers and be direct and honest about each element of a transaction and the risks each party is assuming.

Investing in those areas can go a long way toward maintaining compliance now and preparing for what lies ahead.

C O M P L I A N C E OV E R D R I V E

Out with the Old and In with the New?

NY_1112.indd 18 10/17/12 10:15 AM

NOVEMBER/DECEMBER 2012 T H E N E W Y O R K D R I V I N G F O R C E

19

w w w . n e w y o r k i a d a . o r g

NY_1112.indd 19 10/17/12 10:16 AM

NY_1112.indd 20 10/17/12 10:16 AM