driving enterprise value presents: international … financial reporting standards: strategies for...

TRANSCRIPT

International Financial Reporting

Standards:Strategies For Adopting a Single Set of Standards

Driving Enterprise Value Presents:

D.J. Gannon, Deloitte & Touche LLP

Joel Osnoss, Deloitte & Touche LLP

February 20, 2008

Copyright © 2008 Deloitte Development LLC. All rights reserved.

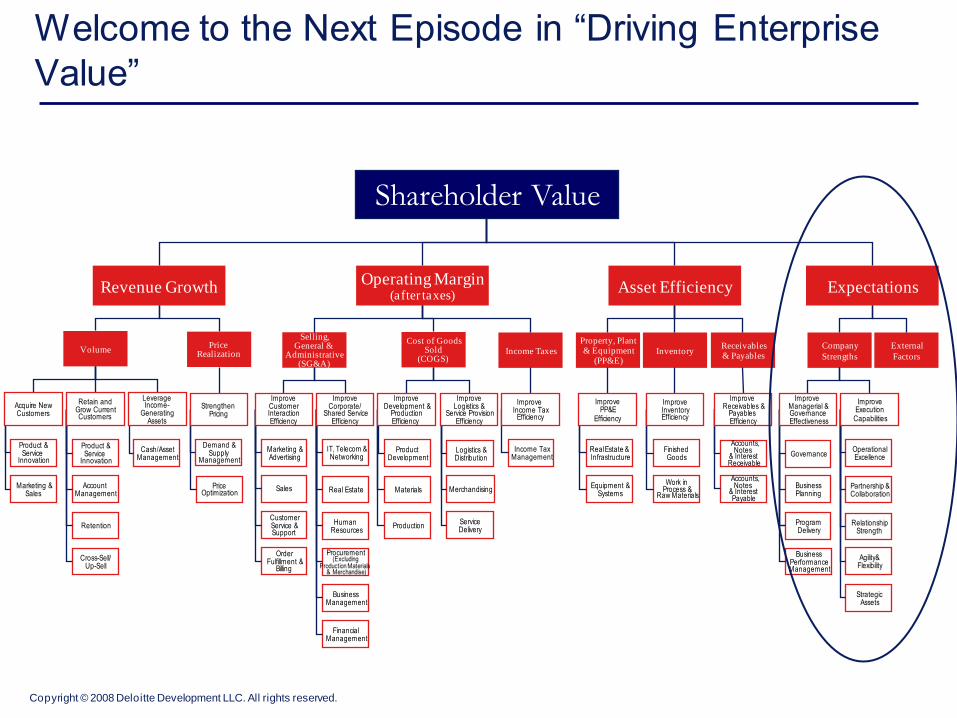

Shareholder Value

Revenue GrowthOperating Margin

(after taxes)Asset Efficiency Expectations

VolumePrice

Realization

Selling,General &

Administrative(SG&A)

Cost of GoodsSold

(COGS) Income Taxes

Property, Plant& Equipment

(PP&E)Inventory

Receivables& Payables

Company

Strengths

External

Factors

Product &Service

Innovation

Marketing &Sales

Product &Service

Innovation

Retention

AccountManagement

Cross-Sell/Up-Sell

Cash/AssetManagement

Demand &Supply

Management

PriceOptimization

IT, Telecom &Networking

Real Estate

Human Resources

Procurement(Excluding

Production Materials & Merchandise)

Business Management

Financial Management

Finished Goods

Work inProcess &

Raw Materials

OperationalExcellence

Partnership &Collaboration

RelationshipStrength

StrategicAssets

Accounts,Notes

& Interest Receivable

Accounts,Notes

& Interest Payable

Equipment &Systems

RealEstate & Infrastructure

Agility&Flexibility

BusinessPlanning

Governance

Program Delivery

BusinessPerformanceManagement

Logistics &Distribution

Merchandising

ServiceDelivery

ImproveDevelopment &

ProductionEfficiency

Product Development

Materials

Production

Income TaxManagement

ImproveCorporate/

Shared ServiceEfficiency

Marketing &Advertising

Sales

CustomerService &Support

OrderFulfillment &

Billing

Retain andGrow CurrentCustomers

Strengthen Pricing

LeverageIncome-

GeneratingAssets

ImproveInventoryEfficiency

ImproveExecution

Capabilities

Improve Income Tax

Efficiency

Improve Managerial &GovernanceEffectiveness

ImprovePP&E

Efficiency

ImproveLogistics &

Service ProvisionEfficiency

Improve Receivables &

Payables Efficiency

ImproveCustomerInteractionEfficiency

Acquire NewCustomers

Welcome to the Next Episode in “Driving Enterprise

Value”

Copyright © 2008 Deloitte Development LLC. All rights reserved.

Agenda

• IFRS background and update

• Why are U.S. companies considering IFRS?

• A case study

• Final thoughts

IFRS Background and Update

Copyright © 2008 Deloitte Development LLC. All rights reserved.

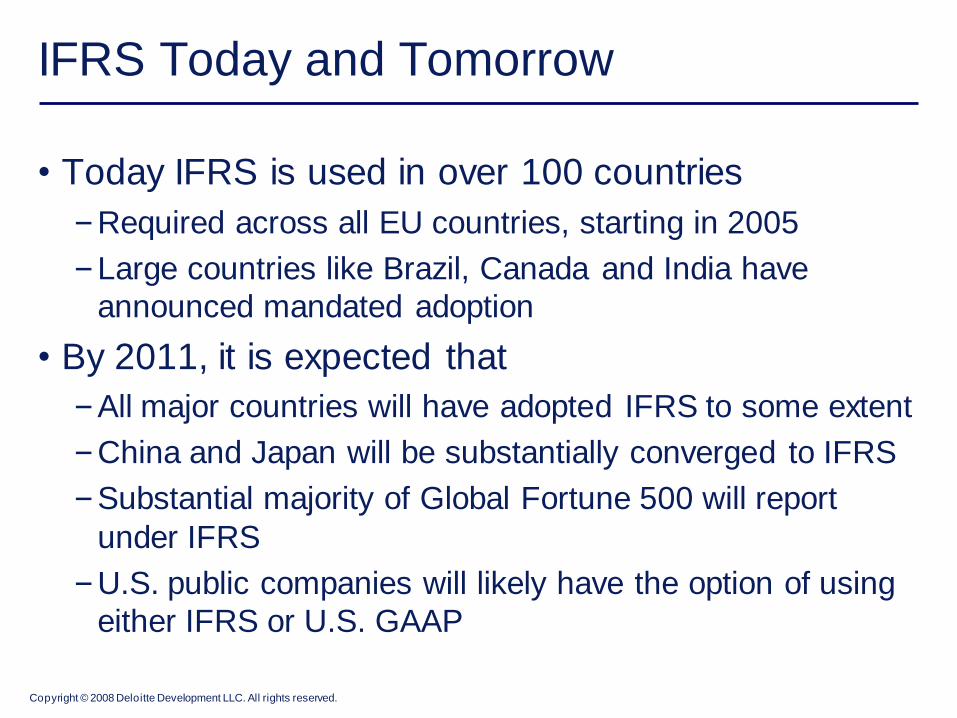

IFRS Today and Tomorrow

• Today IFRS is used in over 100 countries

–Required across all EU countries, starting in 2005

–Large countries like Brazil, Canada and India have

announced mandated adoption

• By 2011, it is expected that

–All major countries will have adopted IFRS to some extent

–China and Japan will be substantially converged to IFRS

–Substantial majority of Global Fortune 500 will report

under IFRS

–U.S. public companies will likely have the option of using

either IFRS or U.S. GAAP

Copyright © 2008 Deloitte Development LLC. All rights reserved.

Regulatory Developments

• Ongoing evolution of regulatory practices around

the globe

–Movement towards mutual recognition of financial

reporting frameworks

• Greater scrutiny of IFRS financials

–Presentation and disclosure are significant areas of focus

across industries

–Focus on understanding judgments used and

assumptions made in applying IFRS

• Greater cooperation on IFRS application issues

–SEC/CESR work plan

Copyright © 2008 Deloitte Development LLC. All rights reserved.

Principles-based Approach

• Greater emphasis will be on interpretation and

application of principles

• Need to assess the “substance” of transactions

–Evaluate whether the accounting presentation reflects the

“economic reality”

–Companies will need to do a “reality check”

• Renewed focus on use of professional judgment

• Greater use of fair value as a measurement basis

• Comparability versus uniformity

Copyright © 2008 Deloitte Development LLC. All rights reserved.

Poll Question #1

Principles-based judgments should play a more

important role in the application of accounting and

financial reporting standards than adherence to

bright-line rules.

–Strongly agree

–Agree

–Neither agree nor disagree

–Disagree

–Strongly disagree

–Don’t know / not applicable

Why Are U.S. Companies Considering

IFRS?

Copyright © 2008 Deloitte Development LLC. All rights reserved.

Drivers of Interest in IFRS

• Industries dominated by non-U.S. companies

–Financial services, pharmaceuticals, energy & resources,

certain technology and manufacturing sectors

• Fear of “the other guy” adopting

• Cross-border M&A transactions

–Acquisitions of foreign companies using IFRS

–Targets of foreign companies using IFRS

– Investments in joint ventures

Copyright © 2008 Deloitte Development LLC. All rights reserved.

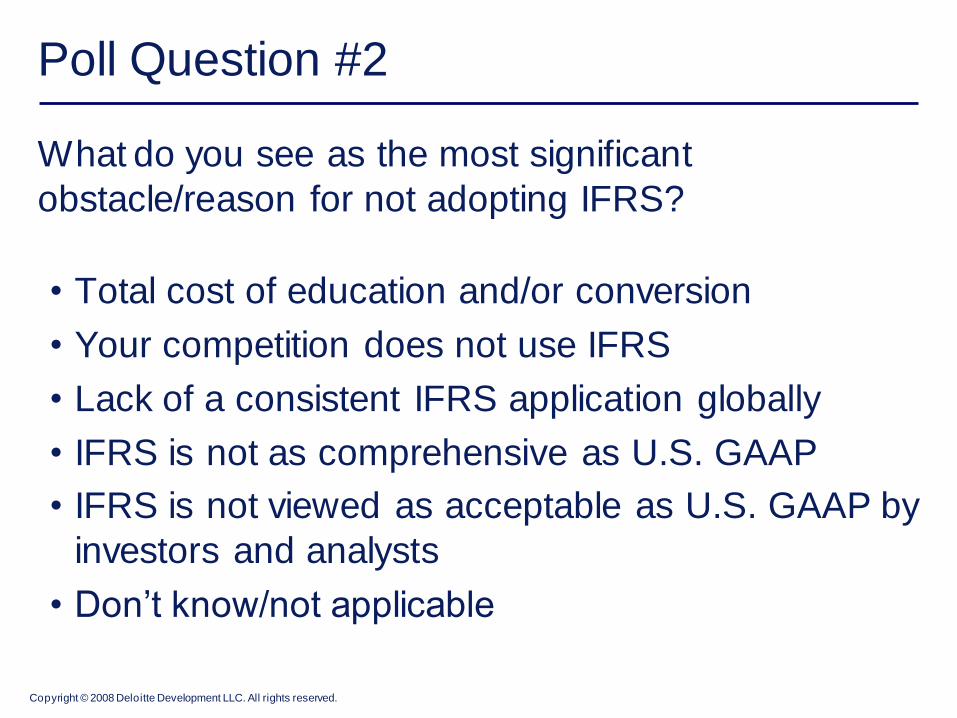

Poll Question #2

What do you see as the most significant

obstacle/reason for not adopting IFRS?

• Total cost of education and/or conversion

• Your competition does not use IFRS

• Lack of a consistent IFRS application globally

• IFRS is not as comprehensive as U.S. GAAP

• IFRS is not viewed as acceptable as U.S. GAAP by

investors and analysts

• Don’t know/not applicable

Copyright © 2008 Deloitte Development LLC. All rights reserved.

You May Already Be Using IFRS

• Your subsidiaries may already file IFRS financials

–More countries are considering IFRS

–Publicly available financial information

–More disclosure than before

• Are you tracking statutory reporting?

–Who is ensuring accuracy and consistency?

• IFRS is inevitable in the U.S.

–Consider building the foundation now if there is a

business case

A Case Study

Copyright © 2008 Deloitte Development LLC. All rights reserved.

Poll Question #3

Your company has centralized visibility over statutory reporting requirements that govern non-U.S. subsidiaries.

• Strongly agree

• Agree

• Neither agree nor disagree

• Disagree

• Strongly disagree

• Don’t know/not applicable

Copyright © 2008 Deloitte Development LLC. All rights reserved.

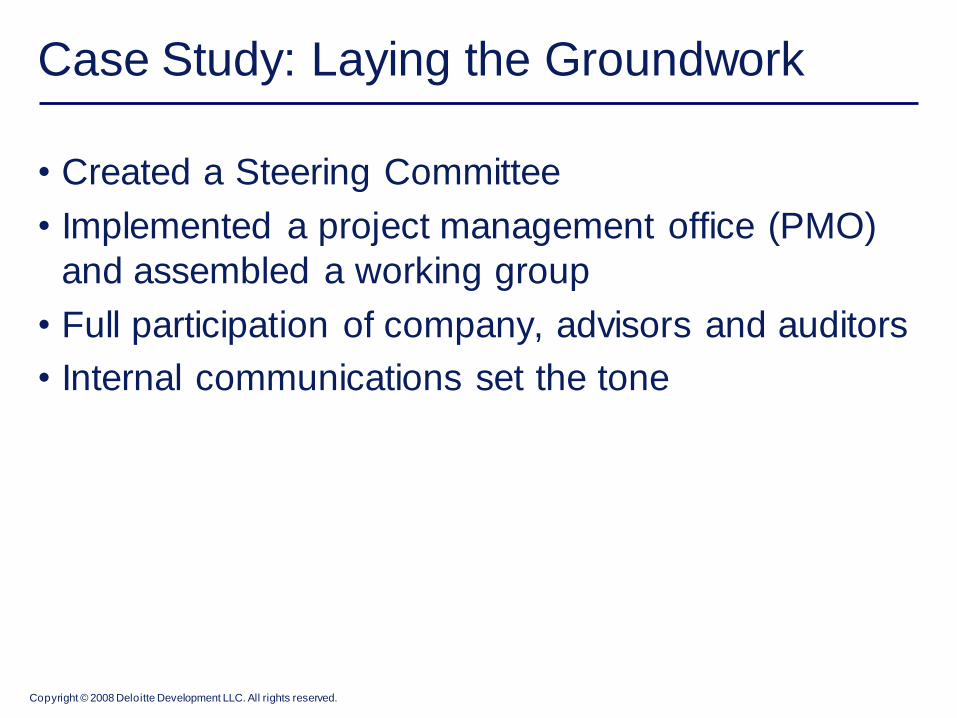

Case Study: Laying the Groundwork

• Created a Steering Committee

• Implemented a project management office (PMO)

and assembled a working group

• Full participation of company, advisors and auditors

• Internal communications set the tone

Copyright © 2008 Deloitte Development LLC. All rights reserved.

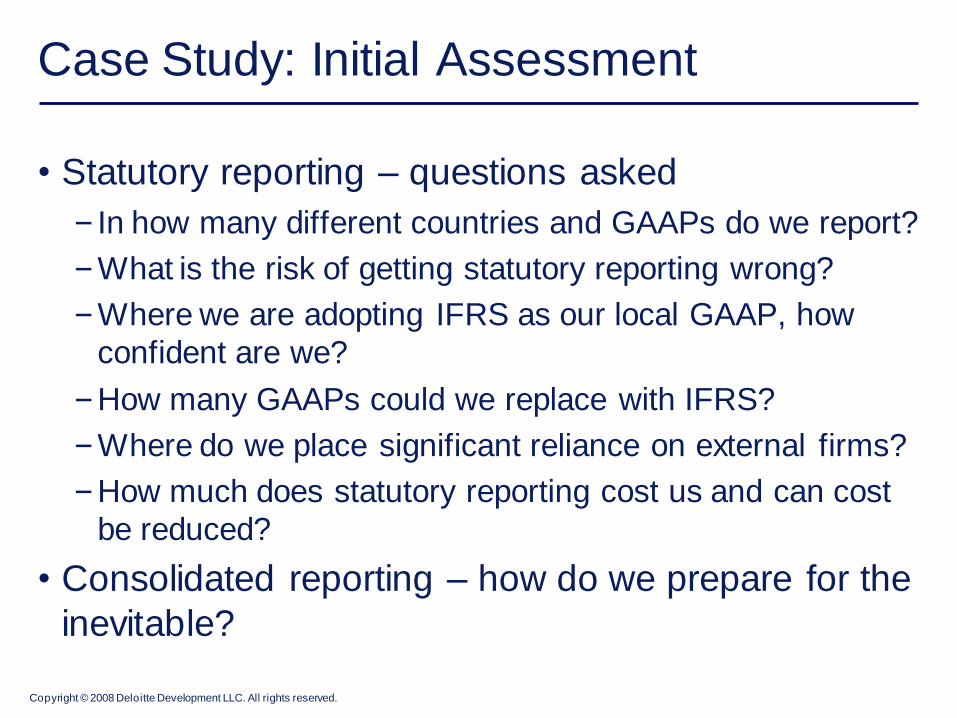

Case Study: Initial Assessment

• Statutory reporting – questions asked

– In how many different countries and GAAPs do we report?

–What is the risk of getting statutory reporting wrong?

–Where we are adopting IFRS as our local GAAP, how

confident are we?

–How many GAAPs could we replace with IFRS?

–Where do we place significant reliance on external firms?

–How much does statutory reporting cost us and can cost

be reduced?

• Consolidated reporting – how do we prepare for the

inevitable?

Copyright © 2008 Deloitte Development LLC. All rights reserved.

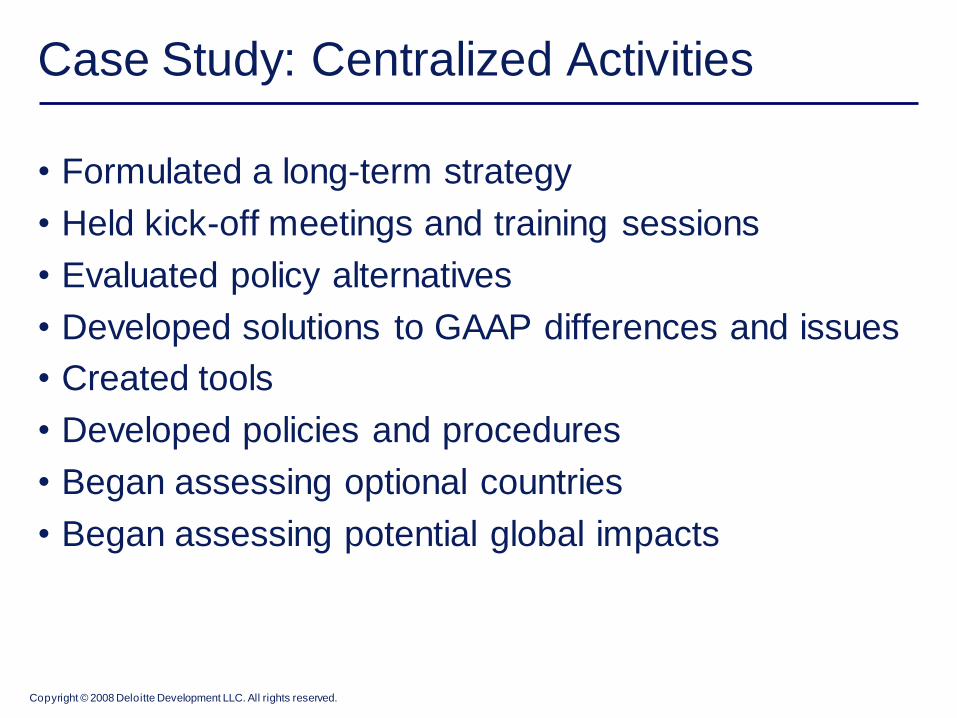

Case Study: Centralized Activities

• Formulated a long-term strategy

• Held kick-off meetings and training sessions

• Evaluated policy alternatives

• Developed solutions to GAAP differences and issues

• Created tools

• Developed policies and procedures

• Began assessing optional countries

• Began assessing potential global impacts

Copyright © 2008 Deloitte Development LLC. All rights reserved.

Case Study: What Was Learned

Challenges Benefits

• Uncertain future enforcement

• Cultural bias and other change

management challenges

• Possible effects on tax structures and

covenants

• IFRS: more complex and restrictive than former local statutory GAAPs

– Statutory reports in many countries can be

accessed by the public

• Standardized and improved

accounting and reporting policies

• Availability and more efficient usage of resources

• Improved controls

– Statutory reports often prepared

based on manual conversion from

U.S. GAAP

• Better cash management

– Consistent standard across

countries can help improve cash

flow planning

Copyright © 2008 Deloitte Development LLC. All rights reserved.

Poll Question #4

If given a choice between U.S. GAAP and IFRS for

U.S. reporting purposes, your company would

consider adopting IFRS.

• Strongly agree

• Agree

• Neither agree nor disagree

• Disagree

• Strongly disagree

• Don’t know/not applicable

Copyright © 2008 Deloitte Development LLC. All rights reserved.

Final Thoughts

• IFRS has become a dominant force globally and is

coming, sooner or later, to the U.S.

• Global transition to IFRS has current implications

for statutory reporting obligations of MNCs

–Requirements to report under IFRS for statutory reporting

–Opportunities to use IFRS for statutory reporting

–Local GAAP may be substantially the same as IFRS

• IFRS can significantly improve global reporting

processes

• A significant number of U.S. companies are

planning for the adoption of IFRS

Copyright © 2008 Deloitte Development LLC. All rights reserved.

Poll Question #5

Your company has an adequate number of personnel

who collectively have a level of IFRS knowledge

sufficient to convert to and maintain IFRS financial

statements.

• Strongly agree

• Agree

• Neither agree nor disagree

• Disagree

• Strongly disagree

• Don’t know/not applicable

Questions & Answers

Join us March 19th at 3PM ET as

our Driving Enterprise Value series

presents:

Mergers and Acquisitions: What

CFOs Should Consider Asking

Before the Deal Is Done

Copyright © 2008 Deloitte Development LLC. All rights reserved.

Thank you for joining

today’s webcast.

To request CPE credit,

click the link below.

Copyright © 2008 Deloitte Development LLC. All rights reserved.

Contact Information

D.J. Gannon

Deloitte & Touche LLP [email protected]

Joel Osnoss

Deloitte & Touche LLP [email protected]

Copyright © 2008 Deloitte Development LLC. All rights reserved.

The information contained in this publication is for general purposes only and is not

intended, and should not be construed, as legal, accounting, or tax advice or

opinion provided by Deloitte to the reader. This material may not be applicable or

suitable for, the reader’s specific circumstances of needs. Therefore, the

information should not be used as a substitute for consultation with professional accounting, tax, or other competent advisors. Please contact a local Deloitte

professional before taking any action based upon this information.

Copyright © 2008 Deloitte Development LLC. All rights reserved.

About Deloitte

Deloitte refers to one or more of Deloitte Touche Tohmatsu, a Swiss Verein, and its network of member

firms, each of which is a legally separate and independent entity. Please see www.deloitte.com/about for a detailed description of the legal structure of Deloitte Touche Tohmatsu and its member firms. Please see

www.deloitte.com/us/about for a detailed description of the legal structure of Deloitte LLP and its subsidiaries.

Copyright © 2008 Deloitte Development LLC. All rights reserved.

A member firm ofDeloitte Touche Tohmatsu