draft sensitivity case results and assumptions · • ev 1% penetration rate per year of the...

TRANSCRIPT

DRAFT Sensitivity Case Results and Assumptions

November 5, 2010

Disclaimer – This presentation, prepared by ICF under contract with RGGI, Inc., is designed to support ongoing evaluation of state RGGI programs. The opinions, data and analysis contained in this report do not necessarily reflect those of RGGI, Inc. or any of the RGGI Participating States.

2

The following slides present select projections from the latest RGGI Reference Case and draft sensitivity cases, based on assumptions in place as of November 1st .

These projections are draft and may change as ICF makes refinements based on state review and input.

The RGGI States specified 6 sensitivities for analysis:1. Higher Load Growth

2. Lower Load Growth

3. Higher Natural Gas Prices & Lower Oil Prices

4. Lower Natural Gas Prices

5. High Emissions Combination

6. Low Emissions Combination

This presentation describes the sensitivity assumptions and results for each related pair of cases (Load Growth, Fuel Prices and Combinations).

The sensitivity case results are shown as compared to the Reference Case and then as compared to each other.

The final section contains the proposed specifications for a Regulatory Sensitivity Case, which has not yet been analyzed.

RGGI SENSITIVITY RESULTS

2

DRAFT RGGI Sensitivity Case Results

3

RGGI SENSITIVITY RESULTS

3

RGGI CO2 EmissionsReference Case and All Sensitivity Cases The chart shows historical and projected CO2 emissions for the RGGI states.

0

20

40

60

80

100

120

140

160

180

200

2005 2010 2015 2020 2025 2030

CO2

Emis

sion

s (M

MTo

ns)

Reference HighDemand

LowDemand

High Gas/Low Oil

LowGas

HighCombo

LowCombo

RGGI Cap

Historical Projected

LOAD GROWTH SENSITIVITY CASES

5

RGGI SENSITIVITY RESULTS

5

DRAFT RGGI Sensitivity Case SpecificationsLoad Growth Sensitivity CasesSensitivity Run Category of Change Components Assumptions

1HIGH LOAD

Higher load growth • Economy • Weather • Additional load, e.g. Electric Vehicles

• Higher economic growth• EV 1% penetration rate per year of the

current fleet. The forecast is 1.6% and 2.4% higher than the reference case in 2020 and 2030, respectively.

• Weather proposal-10% increase over normalized weather

• Includes reference case energy efficiency estimates

• Above is estimated to result in average annual growth rate of 1.3% per year

2LOW LOAD

Lower load growth • Increased Energy Efficiency• State by state calculation of more

aggressive EE targets than reference case

6

The chart shows total firmly planned (“Firm”) and economic capacity additions by type and total retirements projected by IPM.

RGGI SENSITIVITY RESULTS

6

RGGI Cumulative Capacity Changes by 2030Reference Case and Load Growth Sensitivity Cases

-20

-10

0

10

20

30

40

50

Reference HighDemand

LowDemand

Capa

city

Add

ition

s (G

W)

Other

Solar

Biomass

Wind

Gas

Nuclear

Firm Renew.

Firm Conv.

Other Retire

Firm Retire

7

RGGI SENSITIVITY RESULTS

7

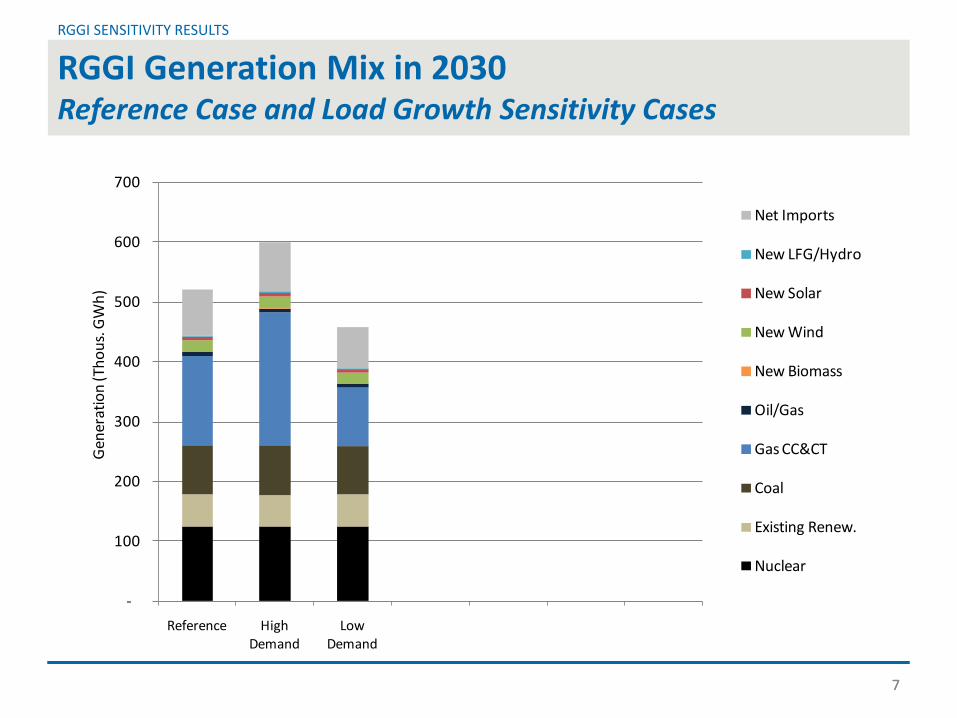

RGGI Generation Mix in 2030Reference Case and Load Growth Sensitivity Cases

-

100

200

300

400

500

600

700

Reference HighDemand

LowDemand

Gen

erat

ion

(Tho

us. G

Wh)

Net Imports

New LFG/Hydro

New Solar

New Wind

New Biomass

Oil/Gas

Gas CC&CT

Coal

Existing Renew.

Nuclear

8

RGGI SENSITIVITY RESULTS

8

RGGI CO2 EmissionsReference Case and Load Growth Sensitivity Cases The chart shows historical and projected CO2 emissions for the RGGI states.

0

20

40

60

80

100

120

140

160

180

200

2005 2010 2015 2020 2025 2030

CO2

Emis

sion

s (M

MTo

ns)

Reference HighDemand

LowDemand

RGGI Cap

Historical Projected

FUEL PRICE SENSITIVITY CASES

10

RGGI SENSITIVITY RESULTS

10

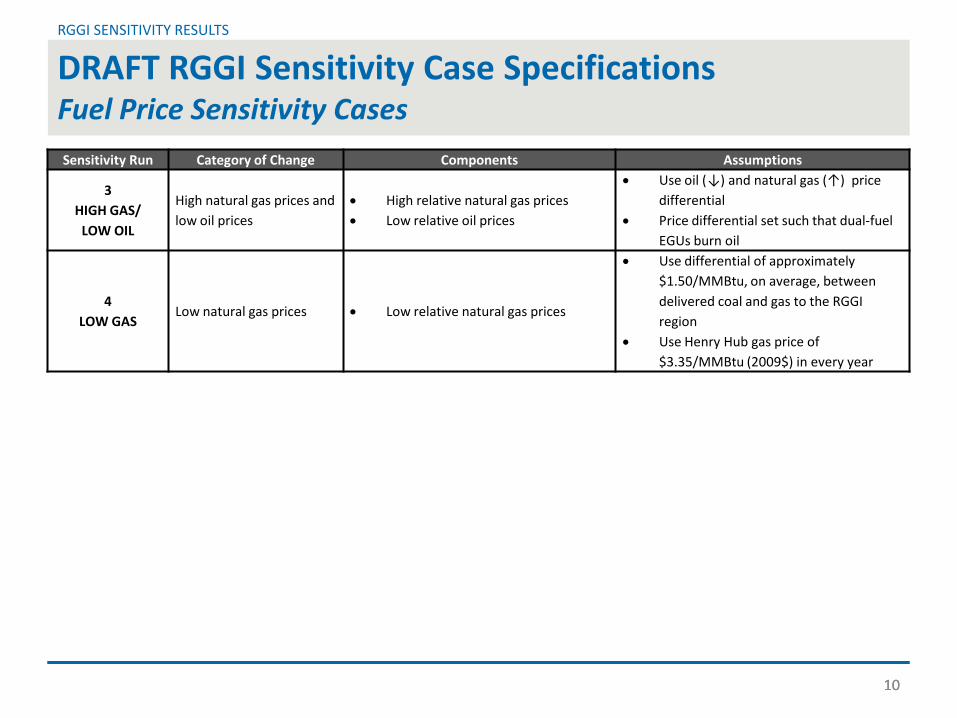

DRAFT RGGI Sensitivity Case SpecificationsFuel Price Sensitivity CasesSensitivity Run Category of Change Components Assumptions

3HIGH GAS/

LOW OIL

High natural gas prices and low oil prices

• High relative natural gas prices• Low relative oil prices

• Use oil (↓) and natural gas (↑) price differential

• Price differential set such that dual-fuel EGUs burn oil

4LOW GAS

Low natural gas prices • Low relative natural gas prices

• Use differential of approximately $1.50/MMBtu, on average, between delivered coal and gas to the RGGI region

• Use Henry Hub gas price of $3.35/MMBtu (2009$) in every year

Fuel Price Sensitivity CasesNatural Gas and Oil Price Assumptions

RGGI SENSITIVITY RESULTS

11

Natural Gas Prices at Henry Hub 0.3%S Resid to New York City

0

2

4

6

8

10

12

14

16

18

2005 2010 2015 2020 2025 2030

2009

$/M

MBt

u

Historical Projected

0

2

4

6

8

10

12

14

16

18

2005 2010 2015 2020 2025 2030

2009

$/M

MBt

u

Historical Reference High Gas/Low Oil

LowGas

Historical Projected

12

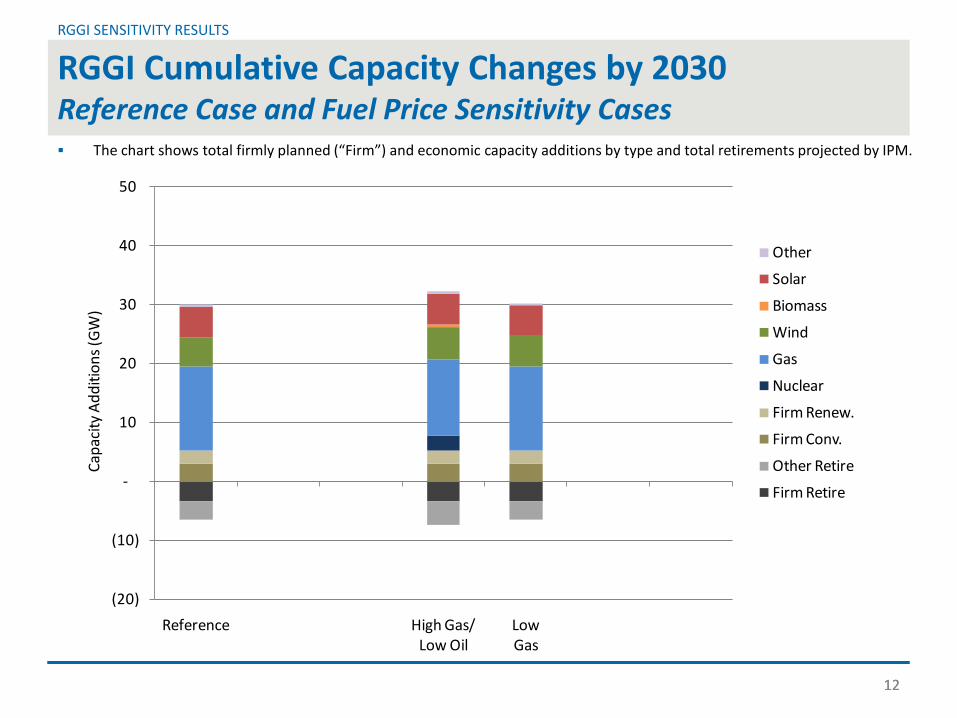

The chart shows total firmly planned (“Firm”) and economic capacity additions by type and total retirements projected by IPM.

RGGI SENSITIVITY RESULTS

12

RGGI Cumulative Capacity Changes by 2030Reference Case and Fuel Price Sensitivity Cases

(20)

(10)

-

10

20

30

40

50

Reference High Gas/Low Oil

LowGas

Capa

city

Add

ition

s (G

W)

Other

Solar

Biomass

Wind

Gas

Nuclear

Firm Renew.

Firm Conv.

Other Retire

Firm Retire

13

RGGI SENSITIVITY RESULTS

13

RGGI Generation Mix in 2030Reference Case and Fuel Price Sensitivity Cases

-

100

200

300

400

500

600

700

Reference High Gas/Low Oil

LowGas

Gen

erat

ion

(Tho

us. G

Wh)

Net Imports

New LFG/Hydro

New Solar

New Wind

New Biomass

Oil/Gas

Gas CC&CT

Coal

Existing Renew.

Nuclear

14

RGGI SENSITIVITY RESULTS

14

RGGI CO2 EmissionsReference Case and Fuel Price Sensitivity Cases The chart shows historical and projected CO2 emissions for the RGGI states.

0

20

40

60

80

100

120

140

160

180

200

2005 2010 2015 2020 2025 2030

CO2

Emis

sion

s (M

MTo

ns)

Reference High Gas/Low Oil

LowGas

RGGI Cap

Historical Projected

EMISSIONS COMBINATION SENSITIVITY CASES

16

RGGI SENSITIVITY RESULTS

16

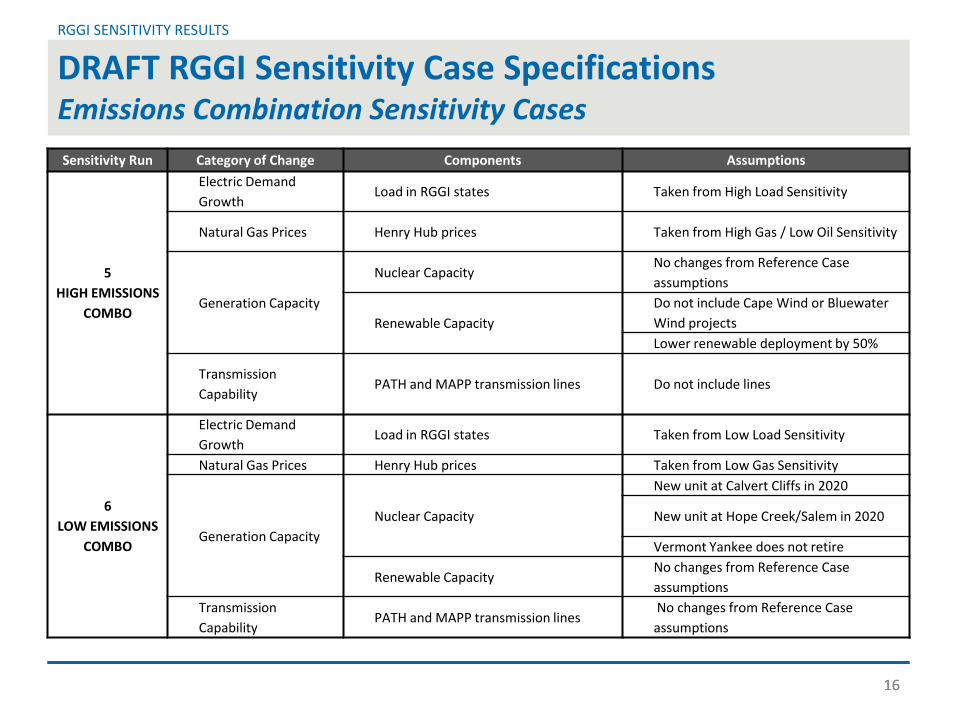

DRAFT RGGI Sensitivity Case SpecificationsEmissions Combination Sensitivity CasesSensitivity Run Category of Change Components Assumptions

5HIGH EMISSIONS

COMBO

Electric Demand Growth

Load in RGGI states Taken from High Load Sensitivity

Natural Gas Prices Henry Hub prices Taken from High Gas / Low Oil Sensitivity

Generation Capacity

Nuclear CapacityNo changes from Reference Case assumptions

Renewable CapacityDo not include Cape Wind or Bluewater Wind projectsLower renewable deployment by 50%

Transmission Capability

PATH and MAPP transmission lines Do not include lines

6LOW EMISSIONS

COMBO

Electric Demand Growth

Load in RGGI states Taken from Low Load Sensitivity

Natural Gas Prices Henry Hub prices Taken from Low Gas Sensitivity

Generation CapacityNuclear Capacity

New unit at Calvert Cliffs in 2020

New unit at Hope Creek/Salem in 2020

Vermont Yankee does not retire

Renewable CapacityNo changes from Reference Case assumptions

Transmission Capability

PATH and MAPP transmission linesNo changes from Reference Case assumptions

17

The chart shows total firmly planned (“Firm”) and economic capacity additions by type and total retirements projected by IPM.

RGGI SENSITIVITY RESULTS

17

RGGI Cumulative Capacity Changes by 2030Reference Case and Emissions Combination Sensitivity Cases

(20)

(10)

-

10

20

30

40

50

Reference HighCombo

LowCombo

Capa

city

Add

ition

s (G

W)

Other

Solar

Biomass

Wind

Gas

Nuclear

Firm Renew.

Firm Conv.

Other Retire

Firm Retire

18

RGGI SENSITIVITY RESULTS

18

RGGI Generation Mix in 2030Reference Case and Emissions Combination Sensitivity Cases

-

100

200

300

400

500

600

700

Reference HighCombo

LowCombo

Gen

erat

ion

(Tho

us. G

Wh)

Net Imports

New LFG/Hydro

New Solar

New Wind

New Biomass

Oil/Gas

Gas CC&CT

Coal

Existing Renew.

Nuclear

19

RGGI SENSITIVITY RESULTS

19

RGGI CO2 EmissionsReference Case and Emissions Combination Sensitivity Cases The chart shows historical and projected CO2 emissions for the RGGI states.

0

20

40

60

80

100

120

140

160

180

200

2005 2010 2015 2020 2025 2030

CO2

Emis

sion

s (M

MTo

ns)

Reference HighCombo

LowCombo

RGGI Cap

Historical Projected

ALL SENSITIVITY CASES

21

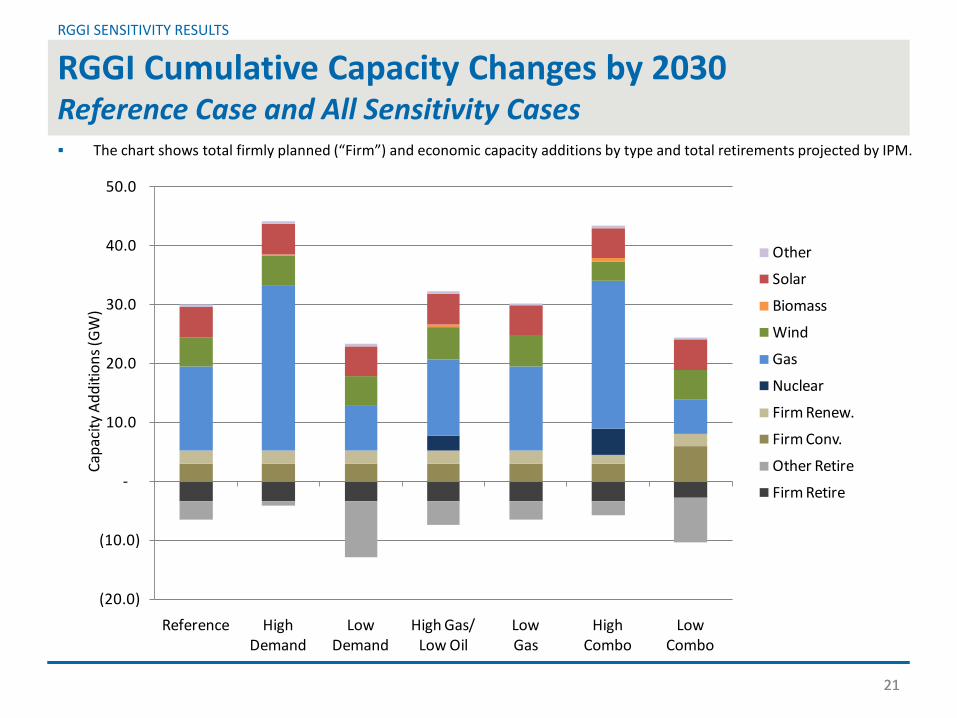

The chart shows total firmly planned (“Firm”) and economic capacity additions by type and total retirements projected by IPM.

RGGI SENSITIVITY RESULTS

21

RGGI Cumulative Capacity Changes by 2030Reference Case and All Sensitivity Cases

(20.0)

(10.0)

-

10.0

20.0

30.0

40.0

50.0

Reference HighDemand

LowDemand

High Gas/Low Oil

LowGas

HighCombo

LowCombo

Capa

city

Add

ition

s (G

W)

Other

Solar

Biomass

Wind

Gas

Nuclear

Firm Renew.

Firm Conv.

Other Retire

Firm Retire

22

RGGI SENSITIVITY RESULTS

22

RGGI Generation Mix in 2030Reference Case and All Sensitivity Cases

-

100

200

300

400

500

600

700

Reference HighDemand

LowDemand

High Gas/Low Oil

LowGas

HighCombo

LowCombo

Gen

erat

ion

(Tho

us. G

Wh)

Net Imports

New LFG/Hydro

New Solar

New Wind

New Biomass

Oil/Gas

Gas CC&CT

Coal

Existing Renew.

Nuclear

23

RGGI SENSITIVITY RESULTS

23

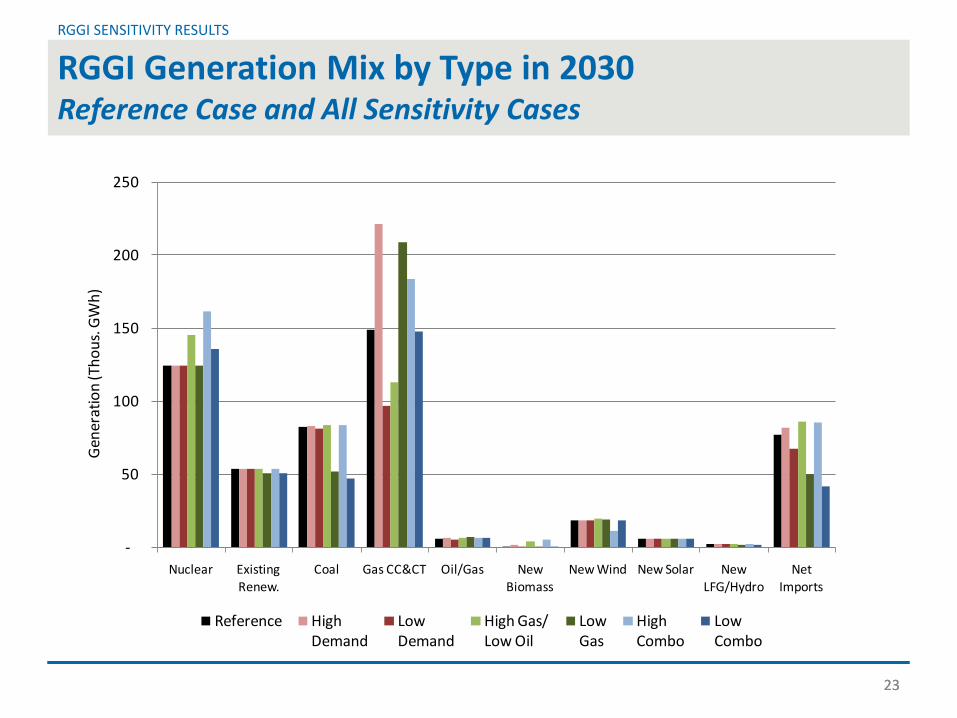

RGGI Generation Mix by Type in 2030Reference Case and All Sensitivity Cases

-

50

100

150

200

250

Nuclear Existing Renew.

Coal Gas CC&CT Oil/Gas New Biomass

New Wind New Solar New LFG/Hydro

Net Imports

Gen

erat

ion

(Tho

us. G

Wh)

Reference HighDemand

LowDemand

High Gas/Low Oil

LowGas

HighCombo

LowCombo

24

RGGI SENSITIVITY RESULTS

24

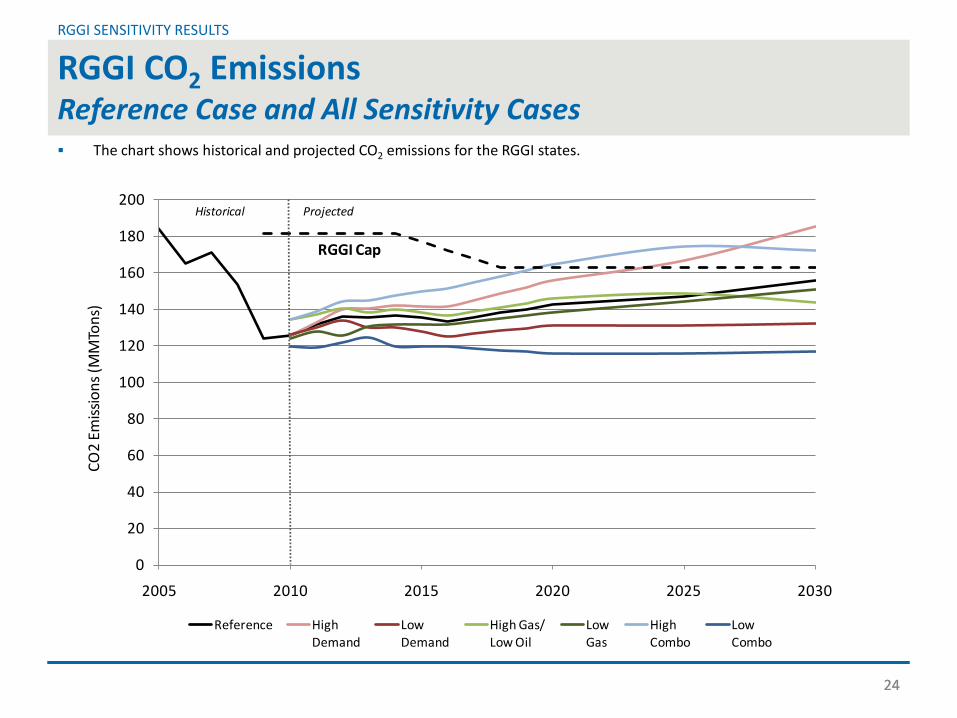

RGGI CO2 EmissionsReference Case and All Sensitivity Cases The chart shows historical and projected CO2 emissions for the RGGI states.

0

20

40

60

80

100

120

140

160

180

200

2005 2010 2015 2020 2025 2030

CO2

Emis

sion

s (M

MTo

ns)

Reference HighDemand

LowDemand

High Gas/Low Oil

LowGas

HighCombo

LowCombo

RGGI Cap

Historical Projected

25

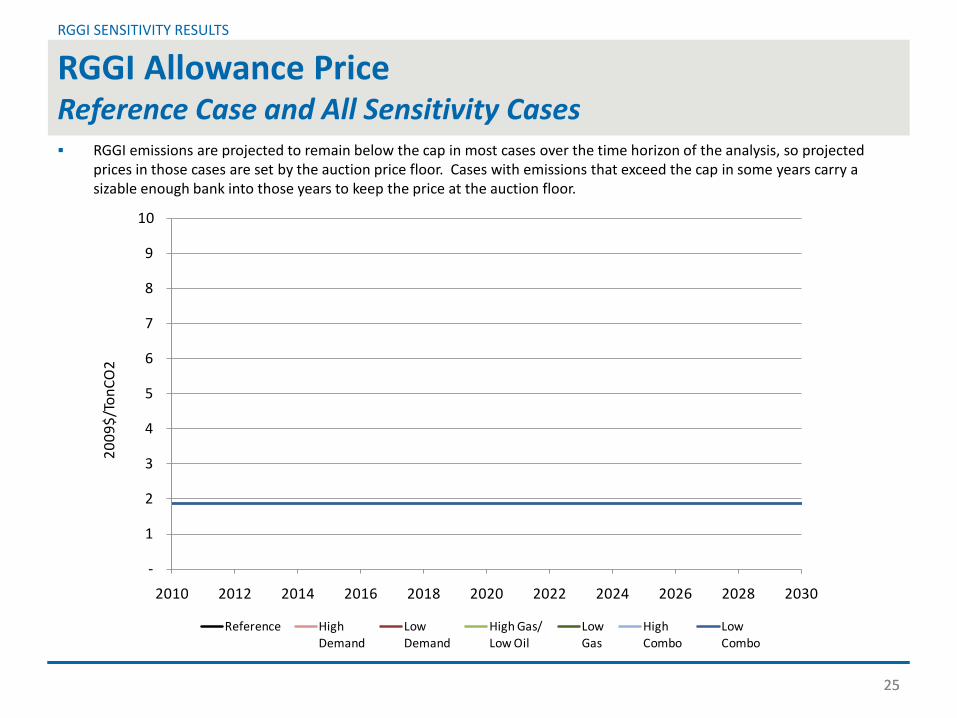

RGGI emissions are projected to remain below the cap in most cases over the time horizon of the analysis, so projected prices in those cases are set by the auction price floor. Cases with emissions that exceed the cap in some years carry a sizable enough bank into those years to keep the price at the auction floor.

RGGI SENSITIVITY RESULTS

25

RGGI Allowance PriceReference Case and All Sensitivity Cases

-

1

2

3

4

5

6

7

8

9

10

2010 2012 2014 2016 2018 2020 2022 2024 2026 2028 2030

2009

$/To

nCO

2

Reference HighDemand

LowDemand

High Gas/Low Oil

LowGas

HighCombo

LowCombo

26

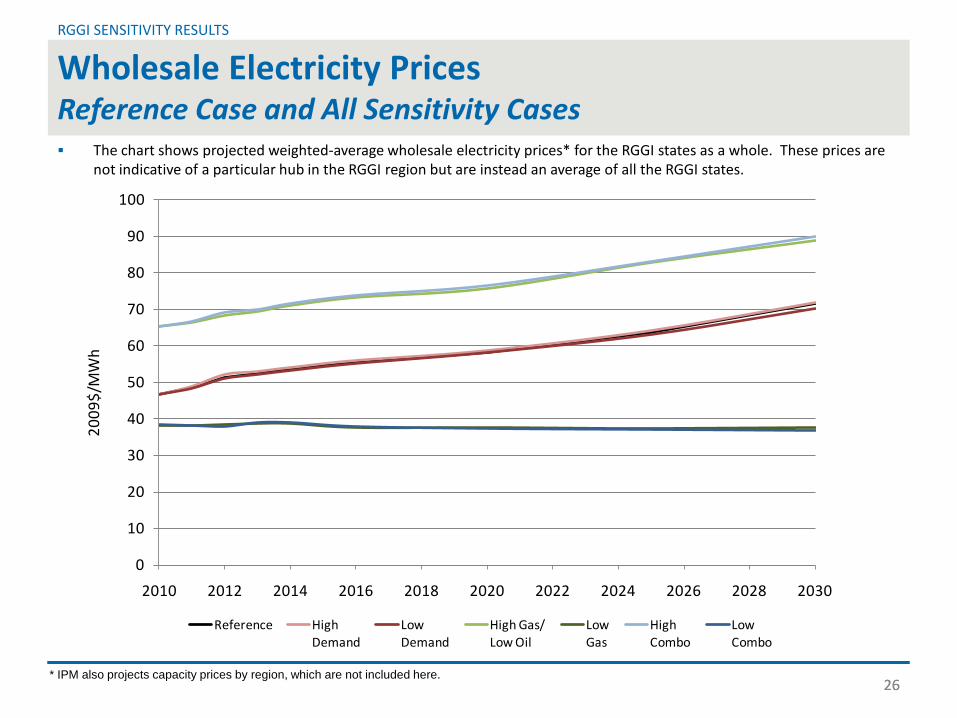

The chart shows projected weighted-average wholesale electricity prices* for the RGGI states as a whole. These prices are not indicative of a particular hub in the RGGI region but are instead an average of all the RGGI states.

RGGI SENSITIVITY RESULTS

26

Wholesale Electricity PricesReference Case and All Sensitivity Cases

* IPM also projects capacity prices by region, which are not included here.

0

10

20

30

40

50

60

70

80

90

100

2010 2012 2014 2016 2018 2020 2022 2024 2026 2028 2030

2009

$/M

Wh

Reference HighDemand

LowDemand

High Gas/Low Oil

LowGas

HighCombo

LowCombo

PROPOSED REGULATORY SENSITIVITY

28

RGGI SENSITIVITY RESULTS

28

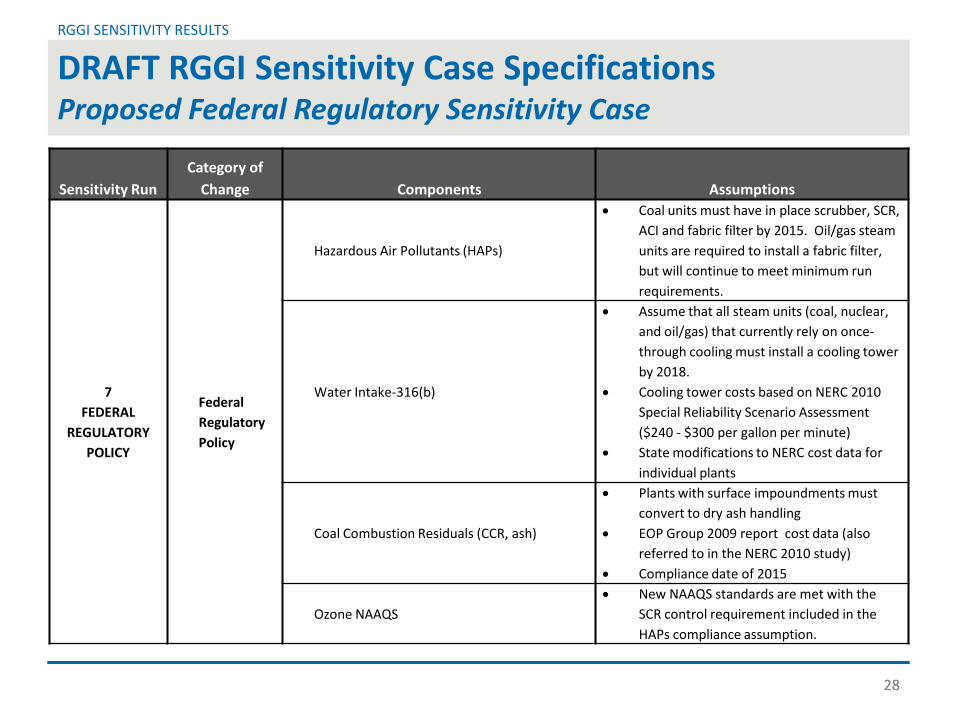

DRAFT RGGI Sensitivity Case SpecificationsProposed Federal Regulatory Sensitivity Case

Sensitivity RunCategory of

Change Components Assumptions

7 FEDERAL

REGULATORY POLICY

Federal Regulatory Policy

Hazardous Air Pollutants (HAPs)

• Coal units must have in place scrubber, SCR, ACI and fabric filter by 2015. Oil/gas steam units are required to install a fabric filter, but will continue to meet minimum run requirements.

Water Intake-316(b)

• Assume that all steam units (coal, nuclear, and oil/gas) that currently rely on once-through cooling must install a cooling tower by 2018.

• Cooling tower costs based on NERC 2010 Special Reliability Scenario Assessment ($240 - $300 per gallon per minute)

• State modifications to NERC cost data for individual plants

Coal Combustion Residuals (CCR, ash)

• Plants with surface impoundments must convert to dry ash handling

• EOP Group 2009 report cost data (also referred to in the NERC 2010 study)

• Compliance date of 2015

Ozone NAAQS• New NAAQS standards are met with the

SCR control requirement included in the HAPs compliance assumption.