draft merger agreement - homepage | sartorius · translation in english for information purposes...

TRANSCRIPT

Translation in English for information purposes only

PAR-#21077433-v9

Sartorius Stedim Biotech SA

and

VL Finance SAS

DRAFT MERGER AGREEMENT

Dated 18 February 2016

Translation in English for information purposes only

2 PAR-#21077433-v9

TABLE OF CONTENTS

1. FRAMEWORK........................................................................................................................................ 4

1.1. TERMS AND GENERAL CONDITIONS OF THE MERGER ........................................................................ 4

1.2. CHARACTERISTICS OF THE COMPANIES ........................................................................................... 5

1.2.1. Characteristics of the Absorbing Company ............................................................................ 5

1.2.2. Characteristics of the Absorbed Company ............................................................................. 6

1.2.3. Capital links between the Absorbing Company and the Absorbed Company ........................ 7

1.2.4. Common directors and officers .............................................................................................. 7

1.3. REASONS AND PURPOSES OF THE MERGER ....................................................................................... 7

1.4. BASIS OF THE MERGER ..................................................................................................................... 8

1.4.1. Reference financial statements ............................................................................................... 8

1.4.2. Effective date .......................................................................................................................... 8

1.5. VALUATION OF CONTRIBUTED ASSETS AND LIABILITIES .................................................................... 8

1.6. SCRUTINY OF THE CONDITIONS OF THE MERGER .............................................................................. 9

2. CONTRIBUTION – MERGER ......................................................................................................... 9

2.1. PRELIMINARY PROVISIONS ............................................................................................................... 9

2.2. CONTRIBUTION OF THE ABSORBED COMPANY ................................................................................. 9

2.2.1. Assets contributed ................................................................................................................... 9

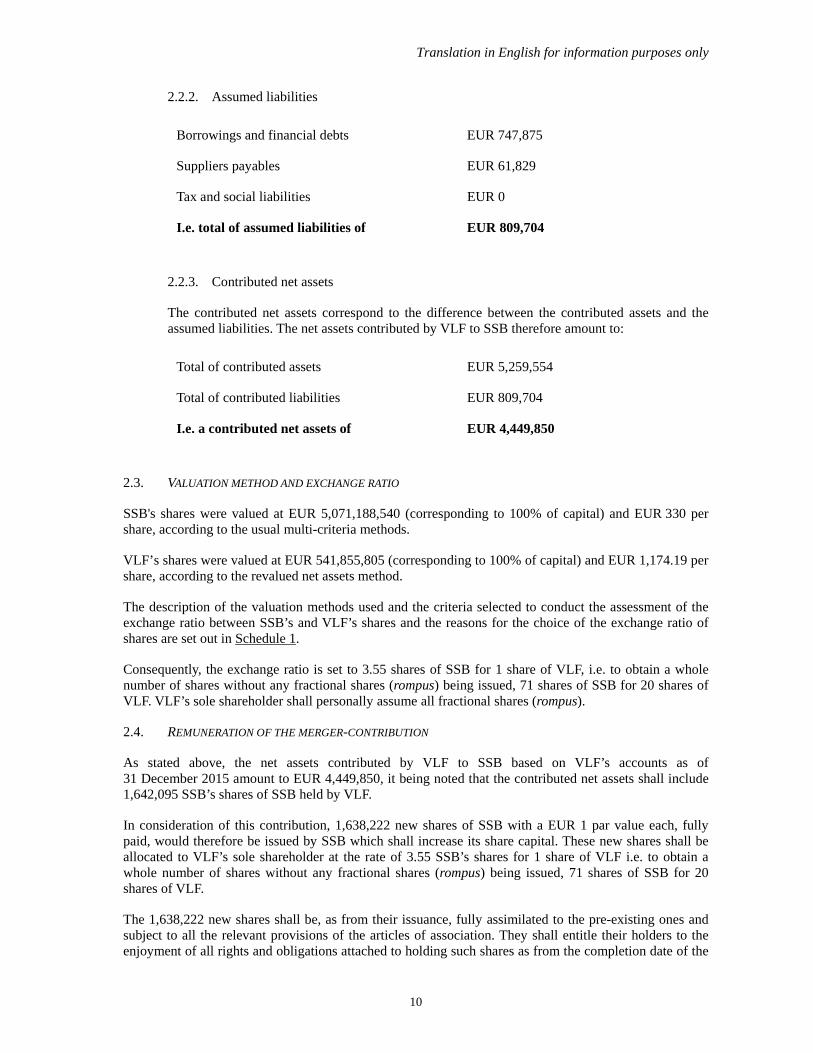

Assumed liabilities ........................................................................................................................10

2.2.2. .....................................................................................................................................................10

2.2.3. Contributed net assets ............................................................................................................10

2.3. VALUATION METHOD AND EXCHANGE RATIO ...................................................................................10

2.4. REMUNERATION OF THE MERGER-CONTRIBUTION ...........................................................................10

2.5. MERGER PREMIUM .........................................................................................................................11

2.6. SHARE CAPITAL DECREASE OF THE ABSORBING COMPANY ..............................................................11

2.7. OWNERSHIP – ENJOYMENT .............................................................................................................12

2.8. DATE OF COMPLETION OF THE MERGER .........................................................................................12

3. CHARGES AND CONDITIONS OF THE MERGER ....................................................................12

4. CONDITIONS PRECEDENT TO THE COMPLETION OF THE MERGER ............................13

5. WINDING-UP OF THE ABSORBED COMPANY ........................................................................14

6. GENERAL REPRESENTATIONS AND WARRANTIES ............................................................14

7. TAX AND SOCIAL REPRESENTATIONS AND WARRANTIES ..............................................15

7.1. GENERAL PROVISIONS ....................................................................................................................15

7.2. REGISTRATION DUTIES ....................................................................................................................15

7.3. CORPORATE TAX .............................................................................................................................15

7.4. VALUE ADDED TAX .........................................................................................................................16

7.5. MAINTAINANCE OF PREVIOUS PREFERENTIAL TAX SCHEMES ...........................................................17

7.6. OTHER TAXES .................................................................................................................................17

8. GENERAL PROVISIONS ........................................................................................................................17

8.1. DISCLOSURE FORMALITIES .............................................................................................................17

8.2. DELIVERY OF DOCUMENTS .............................................................................................................17

8.3. FEES ..............................................................................................................................................17

8.4. ADDRESS FOR SERVICES .................................................................................................................17

8.5. POWERS .........................................................................................................................................17

Translation in English for information purposes only

3 PAR-#21077433-v9

8.6. GOVERNING LAW AND RELEVANT JURISDICTION .........................................................................18

LIST OF SCHEDULES ............................................................................................................................19

SCHEDULE 1 METHOD FOR DETERMINING THE EXCHANGE RATIO .......................................................20

SCHEDULE 2 FINANCIAL STATEMENTS OF SSB AS OF 31 DECEMBER 2015 ...........................................24

SCHEDULE 3 CONSOLIDATED FINANCIAL STATEMENTS OF SSB AS OF 31 DECEMBER 2015 ................25

SCHEDULE 4 FINANCIAL STATEMENTS OF VLF AS OF 31 DECEMBER 2015 ..........................................26

Translation in English for information purposes only

4 PAR-#21077433-v9

DRAFT MERGER BY ABSORPTION AGREEMENT

BETWEEN:

Sartorius Stedim Biotech SA, a société anonyme with a Board of directors organized under the laws of France with an issued share capital of EUR 15,367,238, divided into 15,367,238 of EUR 1 par value each, fully paid, listed on Euronext Paris (Euronext Paris – compartment A – ISIN Code FR0000053266), having its registered office at Avenue de Jouques, zone industrielle Les Paluds, 13400 Aubagne, registered with the trade and companies register of Marseille under number 314 093 352,

Represented hereof by Mr. Joachim KREUZBURG in his capacity of Chairman of the Board of directors and General manager, duly authorized;

Hereinafter “SSB” or the “Absorbing Company”,

ON THE FIRST PART,

AND:

VL Finance SAS, a société par actions simplifiée organized under the laws of France with an issued share capital of EUR 4,614,710, divided into 461,471 shares of EUR 10 par value each, fully paid, having its registered office at Avenue de Jouques, zone industrielle Les Paluds, 13400 Aubagne, registered with the trade and companies register of Marseille under number 377 509 112,

Represented hereof by Mr. Joachim KREUZBURG in his capacity of Chairman, duly authorized;

Hereinafter “VLF” or the “Absorbed Company”,

ON THE SECOND PART,

SSB, together with VLF, are hereinafter referred to as the “Parties” and, each of SSB and VLF individually, as a “Party”.

WHEREAS, FOR PURPOSES OF THE COMPLETION OF THE MERGER BETWEEN SSB AND VLF, BY ABSORPTION OF VLF BY SSB, THE FOLLOWING IS HEREBY STATED, DECLARED AND AGREED:

1. FRAMEWORK

1.1. TERMS AND GENERAL CONDITIONS OF THE MERGER

For purposes of the merger between SSB and VLF, by absorption of the latter by the former, pursuant to the provisions of Articles L. 236-1 et seq. and R. 236-1 et seq. of the French Commercial Code (Code de commerce), VLF shall contribute all of its assets to SSB, provided the latter assumes all of VLF’s liabilities.

Translation in English for information purposes only

5 PAR-#21077433-v9

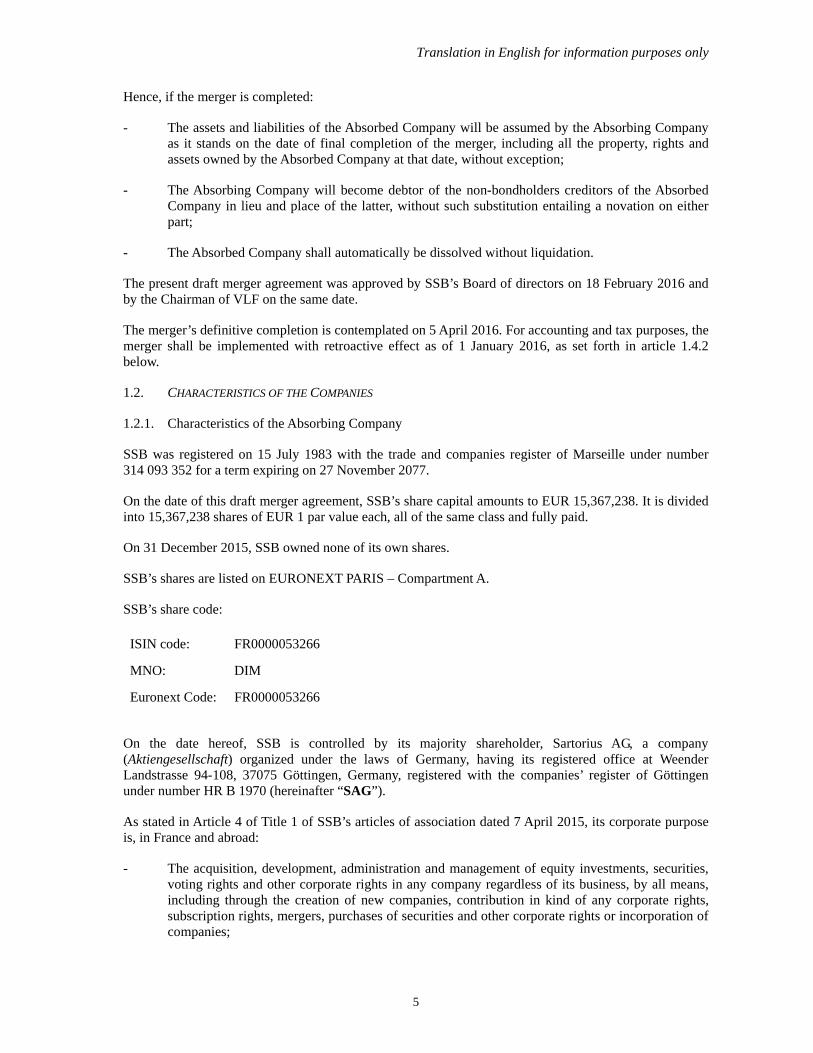

Hence, if the merger is completed:

- The assets and liabilities of the Absorbed Company will be assumed by the Absorbing Company as it stands on the date of final completion of the merger, including all the property, rights and assets owned by the Absorbed Company at that date, without exception;

- The Absorbing Company will become debtor of the non-bondholders creditors of the Absorbed Company in lieu and place of the latter, without such substitution entailing a novation on either part;

- The Absorbed Company shall automatically be dissolved without liquidation.

The present draft merger agreement was approved by SSB’s Board of directors on 18 February 2016 and by the Chairman of VLF on the same date.

The merger’s definitive completion is contemplated on 5 April 2016. For accounting and tax purposes, the merger shall be implemented with retroactive effect as of 1 January 2016, as set forth in article 1.4.2 below.

1.2. CHARACTERISTICS OF THE COMPANIES

1.2.1. Characteristics of the Absorbing Company

SSB was registered on 15 July 1983 with the trade and companies register of Marseille under number 314 093 352 for a term expiring on 27 November 2077.

On the date of this draft merger agreement, SSB’s share capital amounts to EUR 15,367,238. It is divided into 15,367,238 shares of EUR 1 par value each, all of the same class and fully paid.

On 31 December 2015, SSB owned none of its own shares.

SSB’s shares are listed on EURONEXT PARIS – Compartment A.

SSB’s share code:

ISIN code: FR0000053266

MNO: DIM

Euronext Code: FR0000053266

On the date hereof, SSB is controlled by its majority shareholder, Sartorius AG, a company (Aktiengesellschaft) organized under the laws of Germany, having its registered office at Weender Landstrasse 94-108, 37075 Göttingen, Germany, registered with the companies’ register of Göttingen under number HR B 1970 (hereinafter “SAG”).

As stated in Article 4 of Title 1 of SSB’s articles of association dated 7 April 2015, its corporate purpose is, in France and abroad:

- The acquisition, development, administration and management of equity investments, securities, voting rights and other corporate rights in any company regardless of its business, by all means, including through the creation of new companies, contribution in kind of any corporate rights, subscription rights, mergers, purchases of securities and other corporate rights or incorporation of companies;

Translation in English for information purposes only

6 PAR-#21077433-v9

- The direction, animation and the coordination of the activities of its subsidiaries and affiliates; where appropriate, the provision to such subsidiaries and affiliates of all services, either administrative, financial, accounting or legal, the provision of guidance and advice and carrying out or ordering any studies or research required for their development and growth;

- And, generally, any securities, real estate, financial, or civil operations, which may be related, directly or indirectly, to the corporate purpose or any other similar or related corporate purpose or facilitating, directly or indirectly, the achievement of the corporate purpose of the company, its expansion or development.

SSB has closed its latest consolidated financial statements on 31 December 2015, which were approved by the Board of directors on 18 February 2016 and show a profit of EUR 29,311,748.

SSB is managed by a Board of directors, composed on the date of this draft merger agreement of the following members:

- Mr. Joachim KREUZBURG, Chairman of the Board of directors and General manager,

- Mr. Reinhard VOGT, director, Deputy general manager,

- Mr. Volker NIEBEL, director, Deputy general manager,

- Mr. Oscar-Werner REIF, director, Deputy general manager,

- Mr. Bernard LEMAITRE, director,

- Mrs. Liliane de LASSUS (FACHAN), director,

- Mr. Henri RIEY, director,

- Mr. Arnold PICOT, director,

- Mrs. Susan DEXTER, director, et

- Mrs. Anne-Marie GRAFFIN (SALAUN), director.

SSB has appointed as principal independent auditors (i) KPMG S.A of 3 cours du Triangle, Immeuble le Palatin, 92939 Paris La Défense, and (ii) Cabinet DELOITTE ET ASSOCIES of 10 place de la Joliette – Les Docks – Atrium 10.4, 13567 Marseille Cedex.

SSB has appointed as alternate independent auditors (i) BEAS of 7-9 Villa Houssay, 92200 Neuilly-sur-Seine, and (ii) SALUSTRO REYDEL of 3 cours du Triangle, Immeuble le Palatin, 92939 Paris La Défense.

1.2.2. Characteristics of the Absorbed Company

VLF was registered on 9 April 1990 with the trade and companies register of Marseille under number 377 509 112 for a term expiring on 8 April 2089.

On the date of this draft merger agreement, VLF’s share capital amounts to EUR 4,614,710, divided into 461,471 shares of EUR 1 par value each, all of the same class, fully paid, and wholly owned by SAG.

As provided in its articles of association dated 17 December 2015, the corporate purpose of VLF is:

- To hold equity in or control any companies, associations, group or business by purchase, contribution, subscription or any means whatsoever;

Translation in English for information purposes only

7 PAR-#21077433-v9

- Any provision of services in computing technology, management and administration of its subsidiaries or to the benefit of companies in which it would have an interest;

- And, generally, any financial, commercial, industrial, securities or real estate operations, which may be related, directly or indirectly, to the corporate purpose or any other similar or related corporate purpose or facilitating, directly or indirectly, the achievement of the corporate purpose of the company, its expansion or development;

- More specifically, the company's purpose is, in France and abroad, to acquire any shareholding, being majority or not, in industrial or commercial companies that directly or indirectly relate to the sector of manufacturing or selling medical equipment, paramedical, or of materials or products requiring draconian conditions of sterility and microbial safety, and generally manufactured under controlled ambient conditions, to sell them and/or to earn the interests of these investments, to contribute to their development through all advice, financial assistance, as it deems appropriate;

- And more generally, all real estate, securities and financial operations related directly or indirectly to the following activities or likely to facilitate its completion;

- And, if needed, any industrial or commercial operations relating to :

- the creation, the acquisition, the rental, the lease management of any businesses, factories, workshops, relating to any of the aforementioned activities;

- the acquisition, exploitation or sale of all processes, patents and intellectual property rights in respect of such activities.

VLF has closed its latest financial statements on 31 December 2015, which were approved by the Chairman on 18 February 2016 and show a profit of EUR 2,275,208.

VLF is managed by a Chairman, Mr. Joachim KREUZBURG, and a General manager, Mr. Joerg PFIRRMANN.

VLF has appointed Cabinet DELOITTE ET ASSOCIES of 10 place de la Joliette – Les Docks – Atrium 10.4, 13567 Marseille Cedex as principal independent auditor.

VLF has appointed BEAS of 7-9 Villa Houssay, 92200 Neuilly-sur-Seine as alternate independent auditor.

1.2.3. Capital links between the Absorbing Company and the Absorbed Company

At the date hereof, VLF holds 1,642,095 shares out of the 15,367,238 shares forming SSB’s share capital, i.e. about 10.69% of its share capital and about 12.17% of its voting rights.

SSB does not hold any shareholding in VLF’s share capital.

SSB and VLF are both controlled by SAG.

1.2.4. Common directors and officers

Mr. Joachim KREUZBURG, Chairman of VLF, is also Chairman of the Board of directors and General manager of SSB.

1.3. REASONS AND PURPOSES OF THE MERGER

SAG holds directly 100% of the share capital and of the voting rights of VLF.

Translation in English for information purposes only

8 PAR-#21077433-v9

SAG also holds in addition 74.26% of the share capital and 84.55% of the voting rights of SSB:

- directly up to 63.58% of the share capital and 72.39% of voting rights of SSB; and

- indirectly, through VLF, up to 10.69% of the share capital and 12.17% of the voting rights of SSB.

SAG wants to streamline the organization of the Sartorius Group, including the holding of its subsidiaries, and also ensure savings in terms of running costs.

Furthermore, VLF whose only activity is a holding activity, currently owning no more than a sole stake interest, namely 10.69% of SSB’s capital and 12.17% of SSB’s voting rights, its existence is no longer justified.

Thus, the merger would help to reorganize and to simplify the ownership structure of SSB by SAG and get rid of VLF’s specific running costs.

1.4. BASIS OF THE MERGER

1.4.1. Reference financial statements

The terms and conditions of this draft merger agreement are established by the Parties, based on their annual accounts as of 31 December 2015, as respectively stated by the Board of directors of SSB dated 18 February 2016 and by the decisions of the Chairman of VLF dated 18 February 2016 (these accounts, as well as SSB’s consolidated financial statements as of 31 December 2015, are attached hereto as Schedules 2, 3 and 4).

1.4.2. Effective date

Pursuant to the provisions of Article L. 236-4 of the French Commercial Code, the absorption of the Absorbed Company by the Absorbing Company will have retroactive effect for accounting and tax purposes as of 1 January 2016, opening date of the current financial year of such companies.

Accordingly, and pursuant to Article R. 236-1 of the French Commercial Code, the operations performed by the Absorbed Company from 1 January 2016 and until the date of definitive completion of the merger, will be considered as completed by the Absorbing Company, who shall be the only beneficiary of the assets and liabilities with respect to these operations.

Pursuant to Article L. 236-3 of the French Commercial Code, the Absorbed Company shall provide to the Absorbing Company all components of its assets and liabilities as they exist on the date of definitive completion of the merger.

The representatives of the Absorbed Company and the Absorbing Company state that both companies have not, from the accounts settlement date used for the assessment of the assets and liabilities transferred, realized any operation of disposal of the assets or of creation of liabilities beyond those made necessary for the ordinary course of business of the two companies.

1.5. VALUATION OF CONTRIBUTED ASSETS AND LIABILITIES

Pursuant to the provisions of Article 743-1 of Regulation no. 2014-03 of 5 June 2014 of the Accounting regulation authority (Autorité des normes comptables), to the extent that the proposed merger involves companies under common control, the contributions are measured at the net book value, as it appears from the accounts of the Absorbed Company attached as Schedule 4.

Translation in English for information purposes only

9 PAR-#21077433-v9

The assets and liabilities will therefore be contributed, by VLF to SSB, for the value to which they appear in VLF’s annual accounts as of 31 December 2015.

For the calculation of the exchange ratio with regard to SSB, a multi-criteria valuation method was used as recommended by the Autorité des Marchés Financiers (“AMF”) and as specified in Schedule 1.

1.6. SCRUTINY OF THE CONDITIONS OF THE MERGER

Pursuant to Article L. 236-10 of the French Commercial Code, Mrs. Christine BLANC PATIN was appointed as merger auditor by order of Mr. President of the Commercial Court of Marseille dated 7 January 2016, in order to:

- issue a written report on the terms of the merger;

- to assess the value of the contributions in kind made by the Absorbing Company to the Absorbed Company with respect to the merger and, where applicable, to assess the value of the specific benefits contributed to the Absorbing Company, as well as the fairness of the proposed exchange ratio, and to issue the corresponding report.

These reports will be made available to the shareholders of the Absorbing Company and to the sole shareholder of the Absorbed Company, under the conditions and timing set by applicable laws and regulations.

NOW, THEREFORE, HAVING REGARD TO THE AFORESAID, THE PARTIES HEREBY AGREE AS FOLLOWS:

2. CONTRIBUTION – MERGER

2.1. PRELIMINARY PROVISIONS

VLF contributes to SSB, under the ordinary representations and warranties of fact and law in this area, and under the conditions precedent as expressed in article 4 below, all goods, rights and obligations, assets and liabilities, which constitute all its assets and liabilities.

On the reference date of 31 December 2015 which was agreed by mutual consent of the Parties to establish the terms of the merger, the assets and liabilities of VLF include the items listed below, it being specified that this list is only indicative and not exhaustive. The assets and liabilities of VLF shall be contributed to SSB, without exception or condition, as they exist on the date of the definitive completion of the merger, which is hereby accepted by SSB.

2.2. CONTRIBUTION OF THE ABSORBED COMPANY

2.2.1. Assets contributed

Other shareholdings EUR 4,485,395

Other investment securities EUR 676,167

Other receivables EUR 88,186

Cash flow EUR 9,806

I.e. a total of assets contributed of EUR 5,259,554

Translation in English for information purposes only

10 PAR-#21077433-v9

2.2.2. Assumed liabilities

Borrowings and financial debts EUR 747,875

Suppliers payables EUR 61,829

Tax and social liabilities EUR 0

I.e. total of assumed liabilities of EUR 809,704

2.2.3. Contributed net assets

The contributed net assets correspond to the difference between the contributed assets and the assumed liabilities. The net assets contributed by VLF to SSB therefore amount to:

Total of contributed assets EUR 5,259,554

Total of contributed liabilities EUR 809,704

I.e. a contributed net assets of EUR 4,449,850

2.3. VALUATION METHOD AND EXCHANGE RATIO

SSB's shares were valued at EUR 5,071,188,540 (corresponding to 100% of capital) and EUR 330 per share, according to the usual multi-criteria methods.

VLF’s shares were valued at EUR 541,855,805 (corresponding to 100% of capital) and EUR 1,174.19 per share, according to the revalued net assets method.

The description of the valuation methods used and the criteria selected to conduct the assessment of the exchange ratio between SSB’s and VLF’s shares and the reasons for the choice of the exchange ratio of shares are set out in Schedule 1.

Consequently, the exchange ratio is set to 3.55 shares of SSB for 1 share of VLF, i.e. to obtain a whole number of shares without any fractional shares (rompus) being issued, 71 shares of SSB for 20 shares of VLF. VLF’s sole shareholder shall personally assume all fractional shares (rompus).

2.4. REMUNERATION OF THE MERGER-CONTRIBUTION

As stated above, the net assets contributed by VLF to SSB based on VLF’s accounts as of 31 December 2015 amount to EUR 4,449,850, it being noted that the contributed net assets shall include 1,642,095 SSB’s shares of SSB held by VLF.

In consideration of this contribution, 1,638,222 new shares of SSB with a EUR 1 par value each, fully paid, would therefore be issued by SSB which shall increase its share capital. These new shares shall be allocated to VLF’s sole shareholder at the rate of 3.55 SSB’s shares for 1 share of VLF i.e. to obtain a whole number of shares without any fractional shares (rompus) being issued, 71 shares of SSB for 20 shares of VLF.

The 1,638,222 new shares shall be, as from their issuance, fully assimilated to the pre-existing ones and subject to all the relevant provisions of the articles of association. They shall entitle their holders to the enjoyment of all rights and obligations attached to holding such shares as from the completion date of the

Translation in English for information purposes only

11 PAR-#21077433-v9

merger. In particular, they shall give right to any dividend, profit or reserves distribution, as decided by SSB as from such date.

The shares SSB contributed by VLF having been held in the bearer form for more than four (4) years, the new shares of SSB which shall be allocated to the sole shareholder of VLF in the framework of the Merger shall, in compliance with the articles of association of SSB, benefit from a double voting right.

The new shares will be admitted for trading on the regulated market of Euronext Paris - Compartment A.

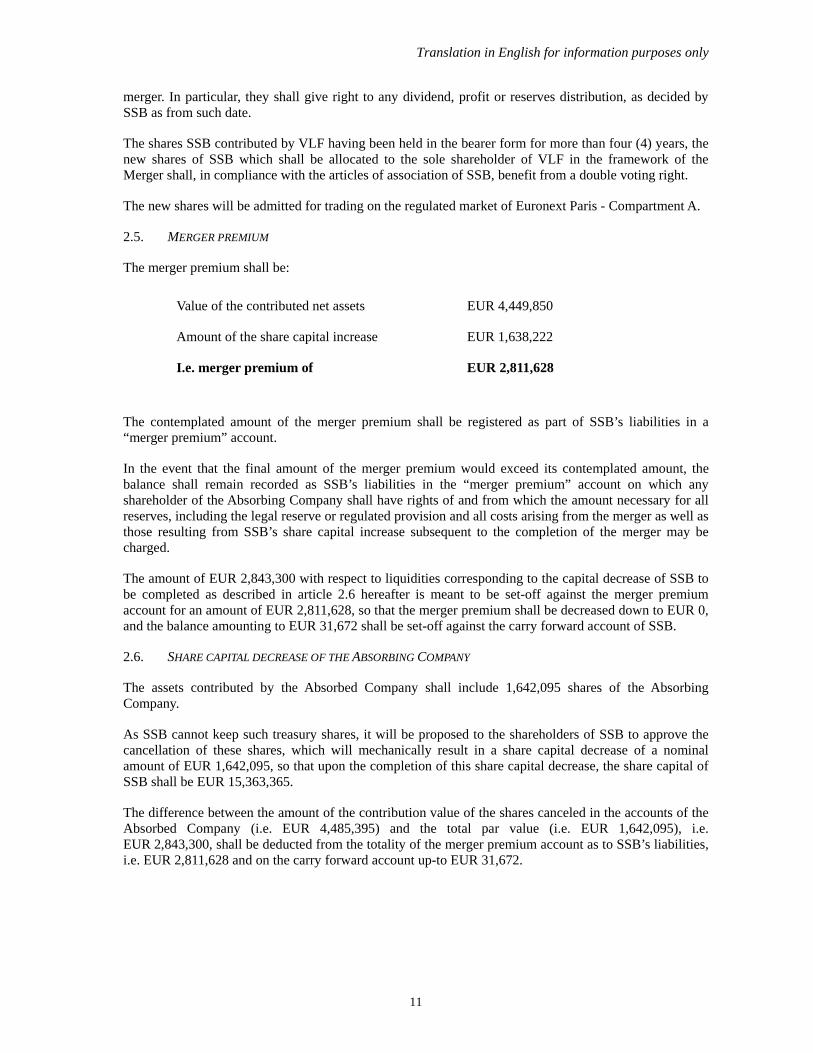

2.5. MERGER PREMIUM

The merger premium shall be:

Value of the contributed net assets EUR 4,449,850

Amount of the share capital increase EUR 1,638,222

I.e. merger premium of EUR 2,811,628

The contemplated amount of the merger premium shall be registered as part of SSB’s liabilities in a “merger premium” account.

In the event that the final amount of the merger premium would exceed its contemplated amount, the balance shall remain recorded as SSB’s liabilities in the “merger premium” account on which any shareholder of the Absorbing Company shall have rights of and from which the amount necessary for all reserves, including the legal reserve or regulated provision and all costs arising from the merger as well as those resulting from SSB’s share capital increase subsequent to the completion of the merger may be charged.

The amount of EUR 2,843,300 with respect to liquidities corresponding to the capital decrease of SSB to be completed as described in article 2.6 hereafter is meant to be set-off against the merger premium account for an amount of EUR 2,811,628, so that the merger premium shall be decreased down to EUR 0, and the balance amounting to EUR 31,672 shall be set-off against the carry forward account of SSB.

2.6. SHARE CAPITAL DECREASE OF THE ABSORBING COMPANY

The assets contributed by the Absorbed Company shall include 1,642,095 shares of the Absorbing Company.

As SSB cannot keep such treasury shares, it will be proposed to the shareholders of SSB to approve the cancellation of these shares, which will mechanically result in a share capital decrease of a nominal amount of EUR 1,642,095, so that upon the completion of this share capital decrease, the share capital of SSB shall be EUR 15,363,365.

The difference between the amount of the contribution value of the shares canceled in the accounts of the Absorbed Company (i.e. EUR 4,485,395) and the total par value (i.e. EUR 1,642,095), i.e. EUR 2,843,300, shall be deducted from the totality of the merger premium account as to SSB’s liabilities, i.e. EUR 2,811,628 and on the carry forward account up-to EUR 31,672.

Translation in English for information purposes only

12 PAR-#21077433-v9

2.7. OWNERSHIP – ENJOYMENT

The Absorbing Company shall own the universality of the assets and liabilities of the Absorbed Company from the date of the completion of the merger. The Absorbing Company shall retroactively benefit from such assets and liabilities as from 1 January 2016.

It is expressly declared that any operation, active and passive, incurred by VLF, between 1 January 2016 and the completion of the merger, shall be regarded as having been implemented by SSB.

VLF’s accounts for that period shall be provided to the Absorbing Company by VLF’s legal representatives.

2.8. DATE OF COMPLETION OF THE MERGER

Subject to the fulfillment of the conditions precedent as described in article 4 below, the merger shall be legally definitively completed after the Combined general meeting of the Absorbing Company approving the merger which is the subject matter of this draft merger agreement, and the share capital decrease of the Absorbing Company referred to in Article 2.6 above.

3. CHARGES AND CONDITIONS OF THE MERGER

The contributed assets are free of all charges and conditions other than those hereby recalled:

3.1. VLF undertakes until the date of completion of the merger, to continue to operate its business with due diligence, and not to do or to allow to be done anything that may cause a depreciation of its valuation.

Moreover, VLF shall not without the prior consent of SSB and until the definitive completion of the merger, do any act of disposal of the contributed assets, sign any agreement, deed or any commitment exceeding the scope of the ordinary course of business, and particularly to enter into any loan in any form whatsoever.

3.2. VLF undertakes to provide SSB with all information and signatures that may be needed, and to provide the necessary support and assistance to ensure the enforceability of the transfer of rights and assets as part of the contribution, as well as the effectiveness of this draft merger agreement towards third parties. It shall especially, upon SSB’s first request, undertake any further actions, reiterative or confirmatory acts regarding these contributions and provide all supporting documents or information and signatures that might be needed at a later stage.

It shall, immediately after the definitive completion of these contributions provided for in this draft merger agreement, provide and deliver to SSB all the assets and rights contributed thereto and all titles and documents of any kind relating therewith.

Where the transmission of certain contracts or certain assets is subject to the approval or the authorization of a co-contracting party or any third party, VLF shall request in due time the necessary authorizations or approvals and shall show evidence of such to SSB on the date of the completion of the merger at the latest. SSB undertakes, if appropriate, to provide assistance to VLF to secure said authorizations or approvals.

VLF shall be in charge of, if necessary and in due time, all notifications, including those required as a result of the existence of any pre-emption rights and of any representations to any administration that would be necessary for the transmission of the assets owned by VLF on the day of completion of the merger.

Translation in English for information purposes only

13 PAR-#21077433-v9

3.3. SSB shall take the assets contributed by VLC at they exist on the date of definitive completion of the merger, and shall not exercise any remedy against VLF, for any reason whatsoever.

SSB shall be substituted to VLF as regards benefit or assumption of all administrative approvals or permissions, of all grants, subsidies, approvals, etc. which have been or may be granted to VLF.

SSB shall fulfill all formalities that may be necessary in order to ensure the transfer of the contributed assets and rights to its benefit, as well as those necessary to ensure the enforceability of this transfer against third parties.

3.4. SSB shall become debtor of VLF’s creditors without such substitution entailing a novation on either part. Pursuant to Article L. 236-14 of the French Commercial Code, VLF’s and SSB’s creditors whose receivable predate the publications referred to in this agreement are entitled to lodge objection within thirty (30) days from the last notice in a legal gazette (journal d’annonces légales) announcing this draft merger agreement.

Where VLF’s or SSB’s creditors lodge objections to the merger in the conditions provided by applicable laws and regulations, the Parties shall consult in good faith to mutually agree on the outcome of such objections, and, as far as possible, to obtain a release.

However, in accordance with applicable laws and regulations, the objection filed by a creditor shall not preclude the completion of the merger.

3.5. SSB shall support and shall pay, from the date of definitive completion of the merger, all taxes, insurance premiums and contributions, and any ordinary or extraordinary encumbrances or charges, which may encumber the contributed assets and rights, and any such encumbrance or charge that are or will be related to the enjoyment or ownership of the contributed assets. It shall assume, where appropriate, the commitments of the Absorbed Company vis-à-vis the administrations with regard to taxes, direct taxes, registration duties and tax on turnover.

3.6. SSB shall be subrogated, as of the date of the definitive completion of the merger, to VLF as to all benefit and liabilities relating to any type of agreement validly binding on the Absorbed Company towards third parties for the operation of the latter’s business.

3.7. SSB shall have full authority, from the definitive completion of the merger, to initiate or pursue all legal actions pending or new, in lieu and place of VLF, as relating to the contributed assets, to give acquiescence to all decisions, and to receive or pay all sums that may be due following any settlement.

3.8. Finally, after completion of the merger, the legal representatives of the Absorbed Company shall, upon first request from the Absorbing Company, provide the latter with all support, signatures and supporting documents and information that might be necessary for the transfer of the assets as part of the merger and the completion of all necessary formalities, given that the Absorbing Company shall bear the costs relating therewith.

4. CONDITIONS PRECEDENT TO THE COMPLETION OF THE MERGER

The merger between the Absorbed Company and the Absorbing Company shall be subject to the fulfillment of the following conditions precedent:

- Filing with the AMF of the document referred to in Article 212-34 of the AMF General Regulations;

Translation in English for information purposes only

14 PAR-#21077433-v9

- Approval by SAG, sole shareholder of the Absorbed Company, of the merger and of the winding-up without liquidation of VLF; and

- Approval by the Combined general shareholders’ meeting of the Absorbing Company of (i) the merger and of the correlative share capital increase, and (ii) of the share capital decrease of the Absorbing Company in the conditions described in article 2.6 hereinabove.

Failing achievement of the aforementioned conditions precedent by 30 June 2016, this merger shall, unless any extension of that period is agreed between the Parties, be considered as null and void, without any right to indemnification for either party.

5. WINDING-UP OF THE ABSORBED COMPANY

Due to the transfer of all the assets and liabilities of VLF to SSB, VLF shall be automatically wound-up upon the definitive completion of the merger, i.e. at the end of the Combined general shareholders’ meeting of the Absorbing Company acknowledging the completion of the merger.

All the liabilities of the Absorbed Company shall be fully transferred to the Absorbing Company and the winding-up of VLF, subsequent to the merger, shall not be followed by any operation of liquidation.

6. GENERAL REPRESENTATIONS AND WARRANTIES

The Absorbed Company represents and warrants that:

6.1. It intends to contribute to SSB, as part of the merger, all the properties forming its corporate assets, without exception or reserve;

6.2. It has never been insolvent or has never been through a process of judicial reorganization or liquidation, and, in general, it has the full capacity to dispose freely of its rights and property;

6.3. It is not currently subject to any known claims or lawsuits, nor to any other event that may give rise to a dispute involving the Absorbed Company or to another measure that might prejudice its legal capacity or the free disposal of its assets;

6.4. It is not currently or may not subsequently be subject to any proceedings that may impede or prevent the exercise of its activities in accordance with applicable laws, regulations and practices;

6.5. All liabilities and charges, and the impairment losses affecting or likely to affect the assets of the Absorbed Company, have been provisioned in the financial statements for amounts that are sufficient to cover the consequences of such events, in respect of which the provisions for risks and charges for depreciation were established;

6.6. It has obtained all contractual authorizations, administrative or other measures as may be necessary to adequately ensure the transfer of assets and of the agreement to be contributed;

6.7. The receivables and securities contributed, and particularly the shares of SSB held by VLF, are free and clear of any security interests, pledges, mortgages, liens or similar or any right that may prevent from using or exercising its rights on its properties;

6.8. Its assets are not threatened by any measures of expropriation or compulsory acquisition;

6.9. All its debts are recorded in the financial statements and there are no circumstances that may cause the payment of default interest, penalties or compensation for default or delay in payment of debts;

Translation in English for information purposes only

15 PAR-#21077433-v9

6.10. It has not entered into any other off-balance sheet arrangements;

6.11. It has no employee;

6.12. It is currently up-to-date with the payment of any taxes and social or parafiscal contributions due, and any other significant obligation to the tax authorities and the relevant social security agencies;

6.13. It is not or has not been subject to any audit or review by the tax authorities or the various social security agencies, it has not received any audit notice, recovery or other dispute with respect to taxes or social security, and there are no circumstances that may result in the implementation of such audit, reorganization or other dispute;

6.14. The assets contributed are free and clear of any encumbrance, pledges, mortgages and liens provided that, if the existence of such encumbrances was revealed on the part of the Absorbed Company, the latter shall obtain a release and a certificate of removal at its own expenses.

6.15. It undertakes to provide and deliver to SSB its documents and accounting books upon the definitive completion of the merger.

7. TAX AND SOCIAL REPRESENTATIONS AND WARRANTIES

7.1. GENERAL PROVISIONS

The undersigned representatives of the two Parties undertake that both of them shall comply with all legal requirements with respect to the statements to be prepared for the payment of corporate income tax and other taxes arising from the definitive completion of this merger, in the framework of what is stated below.

7.2. REGISTRATION DUTIES

The Parties agree that in compliance with Article 816 of the French Tax Code (Code général des impôts), the merger shall be subject to the payment of a fixed registration fee of EUR 500 mentioned in this Article.

7.3. CORPORATE TAX

The Parties, pursuant to article 1.4.2 of this draft merger agreement, have decided to give a retroactive effect to the merger as from 1 January 2016.

Accordingly, and with respect to corporate income tax, the assets and liabilities of VLF shall be contributed to SSB at their net book value as of 1 January 2016 and the profits or losses made since this date by the Absorbed Company shall be included within the taxable income of the Absorbing Company for the year ended 31 December 2016.

The Parties hereby declare that the merger shall be governed by the tax regime provided for in Article 210 A of the French Tax Code.

Corporate incomes or losses incurred by the Absorbed Company from the effective date of the merger, i.e. as from 1 January 2016, shall be included in the taxable profits of the Absorbing Company.

As a result, SSB hereby undertakes to:

- take over as part of its liabilities, provisions which taxation is postponed in the Absorbed Company, including, where appropriate, the regulatory provisions entered in the balance sheet of VLF;

Translation in English for information purposes only

16 PAR-#21077433-v9

- substitute the Absorbed Company for the reintegration of results that were deferred to the imposition, under Article 210 A-3.b. the French Tax Code;

- to calculate the capital gains realized earlier with respect to the sale of non-depreciable capital contribution pursuant to the fiscal value of such assets in the records of the Absorbed Company;

- reintegrate as taxable profits, as provided for by Article 210-A 3.d of the French Tax Code, the capital gains realized, if any, by the Absorbed Company at the moment of the contribution of its depreciable assets;

- enter in its balance sheet items other than capital assets, for their fiscal value in the records of the Absorbed Company, or include in the result of the merger the profit corresponding to the difference between the new value of those items and their fiscal value as recorded in the records of Absorbed Company.

Given that all the contributions are transcribed on the basis of their net book value, the Absorbing Company shall take over in its balance sheet the accounting records of the Absorbed Company (original value, depreciation and amortization) and shall continue to calculate depreciations from the original value of the assets as recorded in the books of the Absorbed Company.

Furthermore, the Absorbing Company and the Absorbed Company also hereby undertake to attach in their income statement a form complying with the template provided by the tax authorities evidencing, for each item contributed as part of the merger, the necessary information regarding the calculation of the taxable income for the subsequent transfer of assets in accordance with Article 54 septies I and Article 38 of Annex III quindecies of the French Tax Code.

The Absorbing Company shall record in its balance sheet, if applicable, the capital gains realized on non-depreciable assets included in the merger, the taxation of which was postponed, in the register provided for by Article 54 septies II of the French Tax Code.

Finally, and from the completion date of the merger, the Absorbing Company shall substitute the Absorbed Company for the implementation of all commitments and tax obligations related to the assets being contributed to it as part of the merger.

7.4. VALUE ADDED TAX

The merger is governed by the tax regime provided for by Article 257 bis of the French Tax Code, which provides for a tax exemption of VAT on supplies of goods and services between entities not liable for VAT and involved in a transfer of a totality of assets and liabilities or part thereof.

The Absorbing Company is deemed to be treated as the successor of the Absorbed Company. It is subrogated in all rights and obligations as to the contributed assets and liabilities.

The Absorbing Company shall proceed, if appropriate, to regularization of rights of deduction to which the Absorbed Company would have been subject to if it had continued to operate the contributed activities.

Furthermore, in accordance with the requirements of Article 287, 5-c of the French Tax Code, the Absorbed Company and the Absorbing Company shall bear the amount free of tax of the contribution on their VAT declaration made in respect of the period in which the merger is carried-out.

Finally, the Absorbed Company shall transfer to the Absorbing Company the VAT credit that it will possibly benefit from the date of its winding-up.

Translation in English for information purposes only

17 PAR-#21077433-v9

7.5. MAINTAINANCE OF PREVIOUS PREFERENTIAL TAX SCHEMES

The Absorbing Company shall assume the benefit and/or the liabilities of all tax-related commitments that may have been previously undertaken by the Absorbed Company on the occasion of previous operations having benefited from a favorable tax regime, regarding registration duties and/or corporate tax, or tax on turnover.

7.6. OTHER TAXES

The Absorbing Company will be subrogated in all the rights and obligations of the Absorbed Company for other tax to which the latter would have been liable.

8. GENERAL PROVISIONS

8.1. DISCLOSURE FORMALITIES

This draft merger agreement will be published in accordance with applicable laws, so that the deadline for creditors to file opposition following this publicity would have expired prior to the Combined general shareholders’ meeting of SSB and to the decisions of the sole shareholder of VLF called to approve this merger. Any objection shall be brought, if appropriate, before the competent Court that will settle their outcome.

The Absorbing Company will fulfill, within the legal deadline, the formalities prescribed by law, and any other formalities necessary to ensure the enforceability of the merger against third parties.

As no liquidation is planned following the winding-up of the Absorbed Company, the legal representative of the Absorbing Company shall also perform on behalf of the Absorbed Company, the formalities subsequent to its winding-up, all powers being conferred to this effect and with right of substitution.

8.2. DELIVERY OF DOCUMENTS

Upon completion of the merger, the original and amended constitutive documents of the Absorbed Company, together with the accounting books, the property titles, statements relating to securities, the supporting documents and information for the ownership of shares, and all agreements, records, papers or other documents relating to property rights, shall be delivered to SSB.

8.3. FEES

The costs, duties and fees associated with the merger together with any accessory or consequential expenses in relation thereto shall be at the Absorbing Company’s expenses.

8.4. ADDRESS FOR SERVICES

The legal representatives of the undersigned companies declare that the address for service regarding the execution of this merger agreement and its consequences, together with any other notice, shall be the registered office of SSB.

8.5. POWERS

All powers are now explicitly granted to:

- the undersigned, representing the companies involved in the merger, with the power to act together or separately, to the effect, if appropriate, to take steps using all complementary or supplementary acts;

Translation in English for information purposes only

18 PAR-#21077433-v9

- the bearer of an original or a copy or excerpt of this draft merger agreement to carry-out all formalities and make all declarations, notifications, all filings, registrations, publications and other necessitated by the merger between SSB and VLF.

8.6. GOVERNING LAW AND RELEVANT JURISDICTION

This draft merger agreement shall be governed by the laws of France, which shall be particularly applicable for all matters relating to its validity, interpretation and effects.

Any dispute concerning the interpretation or execution of this draft merger agreement shall be subject to the exclusive jurisdiction of the Commercial Court of Marseille.

Made in Aubagne On 18 February 2016 In six (6) original copies.

[NOT FOR SIGNATURE]

_________________________________

Sartorius Stedim Biotech SA Represented by Mr. Joachim KREUZBURG Chairman of the Board of directors and General manager

[NOT FOR SIGNATURE]

_________________________________

VL Finance SAS Represented par Mr. Joachim KREUZBURG Chairman

Translation in English for information purposes only

19 PAR-#21077433-v9

LIST OF SCHEDULES

Schedule 1 Method for determining the exchange ratio

Schedule 2 Financial statements of SSB as of 31 December 2015

Schedule 3 Consolidated financial statements of SSB as of 31 December 2015

Schedule 4 Financial statements of VLF as of 31 December 2015

Translation in English for information purposes only

PAR-#21077433-v9

SCHEDULE 1

METHOD FOR DETERMINING THE EXCHANGE RATIO

1. Criteria of assessment of the exchange ratio

The contemplated exchange ratio was determined according to a multi-criteria analysis based on customary and appropriate valuation methods for this type of transaction, while taking into account the respective characteristics of SSB and VLF.

The main features of this multi-criteria analysis are detailed below.

1.1. Valuation of SSB

The selection of methods and references chosen was established taking into account the specificities of SSB, its size, its economic performance and its business segment.

a) Disregarded valuation methods

Net assets value

The method of the net asset value is based on the book value of the assets and liabilities and assumes that the value of the company is based on the historical value of its assets. This method is difficultly relevant for a company like SSB which operates on an innovative and growing market, where the accounting value may be significantly different from the market value.

Revalued net assets

The purpose of this method is to reassess at a market value, the value of assets and liabilities registered in the balance sheet. This method is particularly suitable for a holding company which securities’ value comes from the value of its equity holding and of its real estate portfolio.

This method was discarded for SSB since:

- The fair value of the shares held by SSB would result in a valuation proximate to the valuation determined for SSB itself per the DCF method detailed hereinafter. In fact, the fair value of SSB, in light of its exclusive role as holding company is directly correlated to the valuation of the activities of its affiliates;

- The fair value that would be retained for the valuation of the real estate properties held by SSB would not be representative of the actual value of the company. Indeed, within the operational costs of the Group, part of the costs related to the real estate properties used as registered offices, representing the real estate recorded as assets in the accounts of SSB, are invoiced back to the affiliates and are therefore included in the fair value of the shares of these companies.

As such, the revalued net assets method would not enable to compare the DCF method to a different method permitting to give certainty as to the retained value.

Comparable transaction multiples

The comparable transactions multiples method was discarded given the specificities of the contemplated operation. Indeed, the Merger would be implemented as an internal reorganization for the purposes of administrative and legal simplifications, without any consequence on SSB’s activities.

In this respect, no comparable transaction was identified.

Multiple of stock market comparable

This method was disregarded for the same reasons the comparable transaction multiples was disregarded.

Translation in English for information purposes only

PAR-#21077433-v9

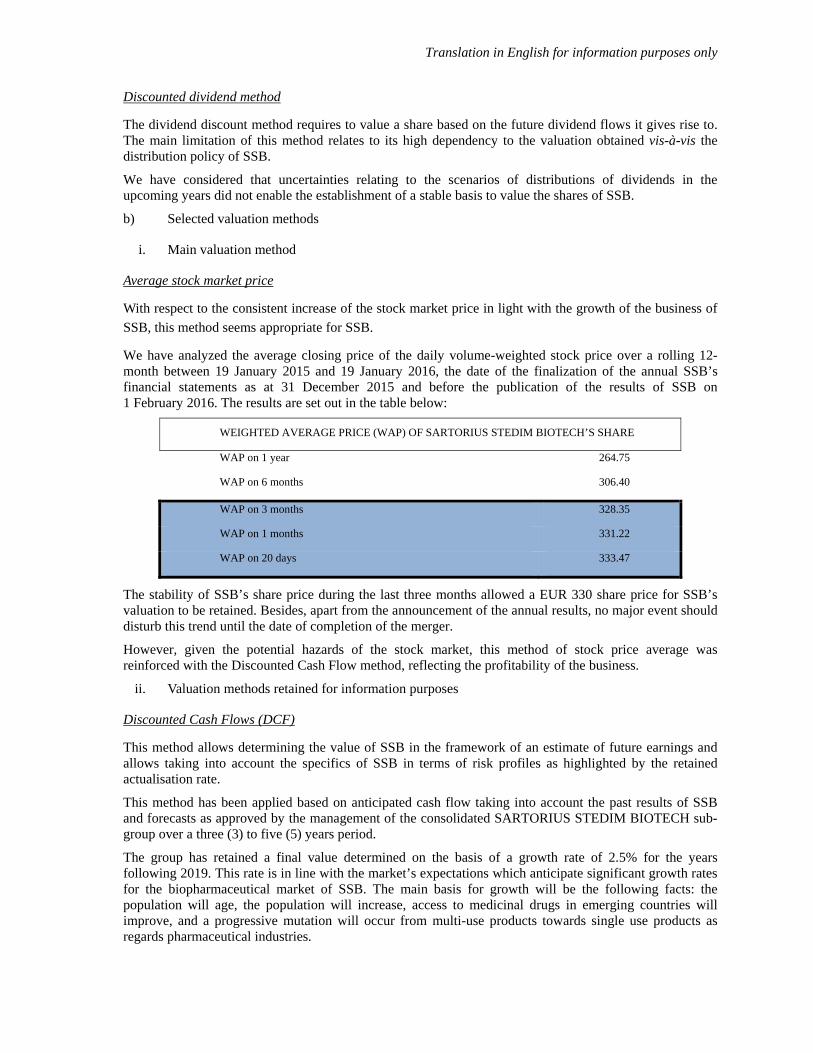

Discounted dividend method

The dividend discount method requires to value a share based on the future dividend flows it gives rise to. The main limitation of this method relates to its high dependency to the valuation obtained vis-à-vis the distribution policy of SSB.

We have considered that uncertainties relating to the scenarios of distributions of dividends in the upcoming years did not enable the establishment of a stable basis to value the shares of SSB.

b) Selected valuation methods

i. Main valuation method

Average stock market price

With respect to the consistent increase of the stock market price in light with the growth of the business of

SSB, this method seems appropriate for SSB.

We have analyzed the average closing price of the daily volume-weighted stock price over a rolling 12-month between 19 January 2015 and 19 January 2016, the date of the finalization of the annual SSB’s financial statements as at 31 December 2015 and before the publication of the results of SSB on 1 February 2016. The results are set out in the table below:

WEIGHTED AVERAGE PRICE (WAP) OF SARTORIUS STEDIM BIOTECH’S SHARE

WAP on 1 year 264.75

WAP on 6 months 306.40

WAP on 3 months 328.35

WAP on 1 months 331.22

WAP on 20 days 333.47

The stability of SSB’s share price during the last three months allowed a EUR 330 share price for SSB’s valuation to be retained. Besides, apart from the announcement of the annual results, no major event should disturb this trend until the date of completion of the merger.

However, given the potential hazards of the stock market, this method of stock price average was reinforced with the Discounted Cash Flow method, reflecting the profitability of the business.

ii. Valuation methods retained for information purposes

Discounted Cash Flows (DCF)

This method allows determining the value of SSB in the framework of an estimate of future earnings and allows taking into account the specifics of SSB in terms of risk profiles as highlighted by the retained actualisation rate.

This method has been applied based on anticipated cash flow taking into account the past results of SSB and forecasts as approved by the management of the consolidated SARTORIUS STEDIM BIOTECH sub-group over a three (3) to five (5) years period.

The group has retained a final value determined on the basis of a growth rate of 2.5% for the years following 2019. This rate is in line with the market’s expectations which anticipate significant growth rates for the biopharmaceutical market of SSB. The main basis for growth will be the following facts: the population will age, the population will increase, access to medicinal drugs in emerging countries will improve, and a progressive mutation will occur from multi-use products towards single use products as regards pharmaceutical industries.

Translation in English for information purposes only

PAR-#21077433-v9

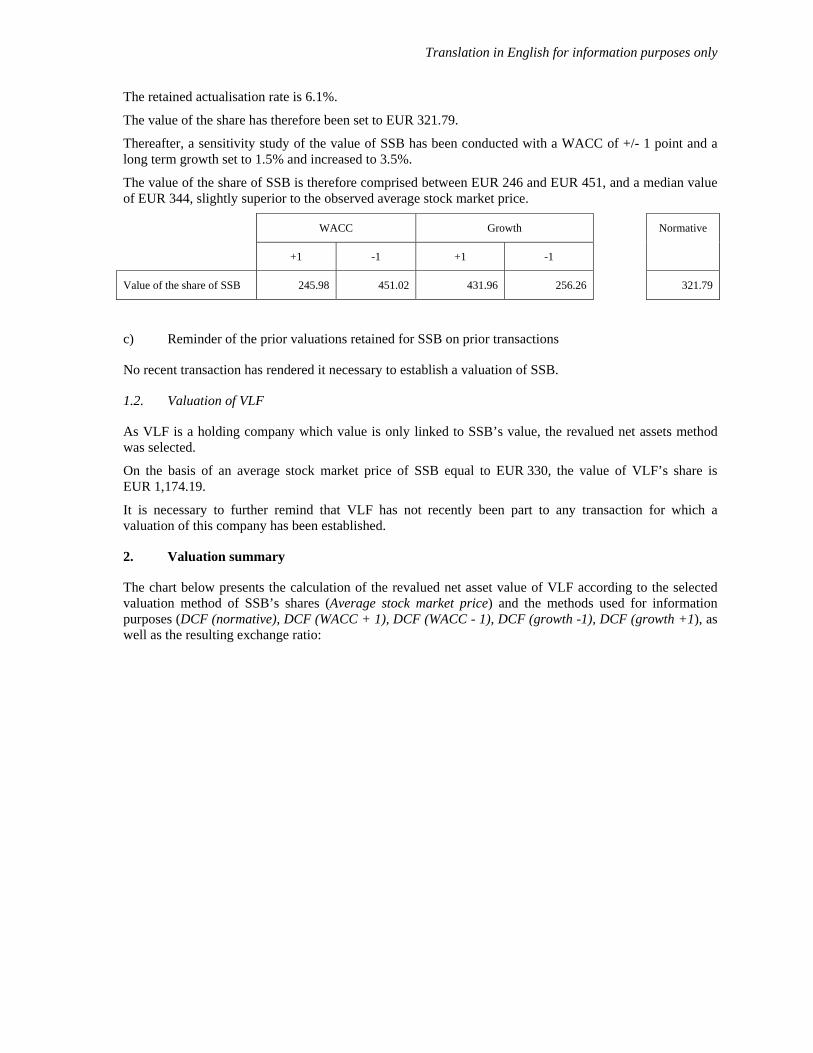

The retained actualisation rate is 6.1%.

The value of the share has therefore been set to EUR 321.79.

Thereafter, a sensitivity study of the value of SSB has been conducted with a WACC of +/- 1 point and a long term growth set to 1.5% and increased to 3.5%.

The value of the share of SSB is therefore comprised between EUR 246 and EUR 451, and a median value of EUR 344, slightly superior to the observed average stock market price.

WACC Growth Normative

+1 -1 +1 -1

Value of the share of SSB 245.98 451.02 431.96 256.26 321.79

c) Reminder of the prior valuations retained for SSB on prior transactions

No recent transaction has rendered it necessary to establish a valuation of SSB.

1.2. Valuation of VLF

As VLF is a holding company which value is only linked to SSB’s value, the revalued net assets method was selected.

On the basis of an average stock market price of SSB equal to EUR 330, the value of VLF’s share is EUR 1,174.19.

It is necessary to further remind that VLF has not recently been part to any transaction for which a valuation of this company has been established.

2. Valuation summary

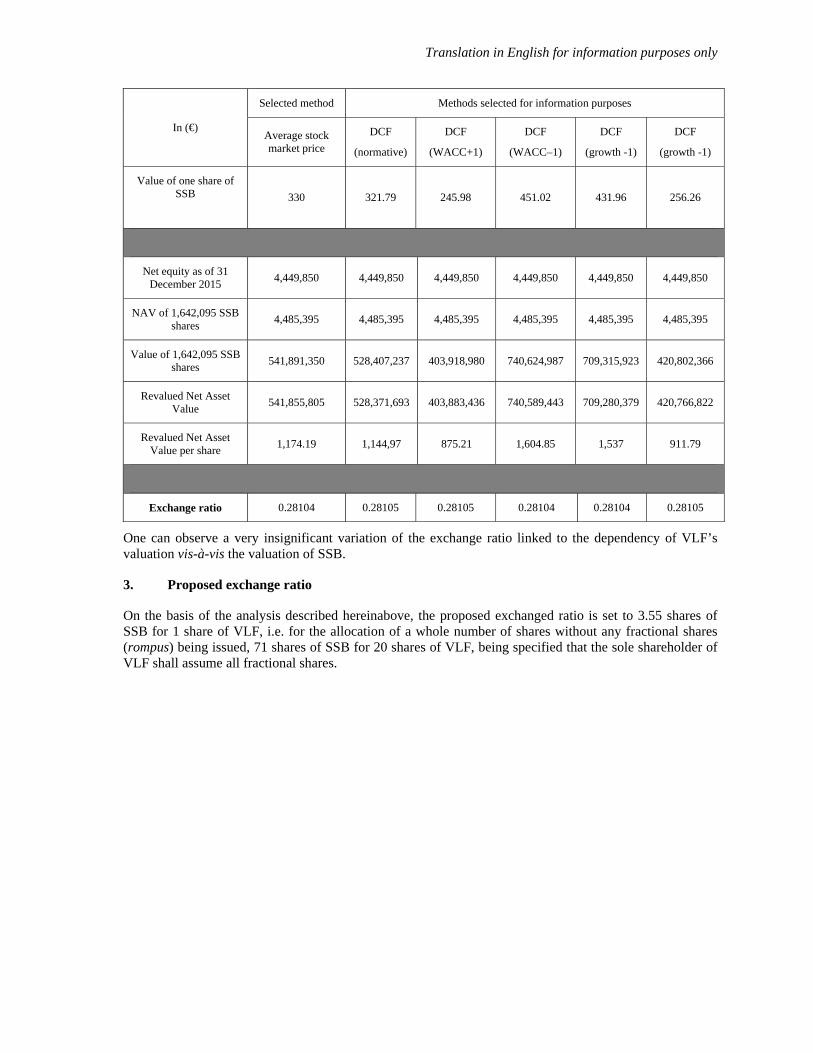

The chart below presents the calculation of the revalued net asset value of VLF according to the selected valuation method of SSB’s shares (Average stock market price) and the methods used for information purposes (DCF (normative), DCF (WACC + 1), DCF (WACC - 1), DCF (growth -1), DCF (growth +1), as well as the resulting exchange ratio:

Translation in English for information purposes only

PAR-#21077433-v9

In (€)

Selected method Methods selected for information purposes

Average stock market price

DCF

(normative)

DCF

(WACC+1)

DCF

(WACC–1)

DCF

(growth -1)

DCF

(growth -1)

Value of one share of SSB

330 321.79 245.98 451.02 431.96 256.26

Net equity as of 31 December 2015

4,449,850 4,449,850 4,449,850 4,449,850 4,449,850 4,449,850

NAV of 1,642,095 SSB shares

4,485,395 4,485,395 4,485,395 4,485,395 4,485,395 4,485,395

Value of 1,642,095 SSB shares

541,891,350 528,407,237 403,918,980 740,624,987 709,315,923 420,802,366

Revalued Net Asset Value

541,855,805 528,371,693 403,883,436 740,589,443 709,280,379 420,766,822

Revalued Net Asset Value per share

1,174.19 1,144,97 875.21 1,604.85 1,537 911.79

Exchange ratio 0.28104 0.28105 0.28105 0.28104 0.28104 0.28105

One can observe a very insignificant variation of the exchange ratio linked to the dependency of VLF’s valuation vis-à-vis the valuation of SSB.

3. Proposed exchange ratio

On the basis of the analysis described hereinabove, the proposed exchanged ratio is set to 3.55 shares of SSB for 1 share of VLF, i.e. for the allocation of a whole number of shares without any fractional shares (rompus) being issued, 71 shares of SSB for 20 shares of VLF, being specified that the sole shareholder of VLF shall assume all fractional shares.

Translation in English for information purposes only

PAR-#21077433-v9

SCHEDULE 2

FINANCIAL STATEMENTS OF SSB AS OF 31 DECEMBER 2015

Translation in English for information purposes only

PAR-#21077433-v9

SCHEDULE 3

CONSOLIDATED FINANCIAL STATEMENTS OF SSB AS OF 31 DECEMBER 2015

Translation in English for information purposes only

PAR-#21077433-v9

SCHEDULE 4

FINANCIAL STATEMENTS OF VLF AS OF 31 DECEMBER 2015