WHAT IS A ROBS? (Rollovers as Business Start-ups)

Legal Arrangement involving a C-Corporation Utilized Prohibited Transaction Exemptions

(in Employment Retirement Income Securities Act (ERISA) and Internal Revenue Code (IRC))

Enables Entrepreneur to Provide Capital from Qualified Retirement Plan to: Start New Business

Purchase Existing Business Refinance Existing Business

WITHOUT TRIGGERING TAXABLE EVENT

One of the more popular funding strategies to purchase a new business 10% of the franchises sold in the U.S. utilized retirement plan rollovers as part of the funding Why was this created? How does this work? What are the benefits?

401 (K) - IRA ROLLOVER FUNDING

1974 Congress creates IRA’s allowing Americans to save for their retirement tax deferred

1980 401(k)’s were established increasing the amount Americans could save tax deferred

Most Americans have the bulk of their savings in their Retirement Plan

Withdrawal of savings incurs taxes and penalties

WHY RETIREMENT PLAN FUNDING IS NEEDED

Here is an example of the tax implications for someone withdrawing $200,000 from their retirement plan

10% early withdrawal penalty

30% state and federal taxes

Leaves the individual with $120,000 of the $200,000

WHAT IF I WANT TO WITHDRAW THE MONEY ?

The process begins with the establishment of a new corporation. MUST be a C-Corporation Will become the sponsor of a new qualified retirement plan

ESTABLISH A NEW CORPORATION

DESIGN A QUALIFIED RETIREMENT PLAN

Next, a qualified retirement plan is designed for the new company. The design of this plan uses specific features that are right for you and your business. These features will be determined usually during an up-front needs assessment

ADOPT THE PLAN & ROLLOVER FUNDS

The new company then adopts the qualified retirement plan.

The company’s new retirement plan will be designed to allow rollovers from most other types of retirement plans. This will allow you – and your company’s employees – the option to rollover your current retirement funds… tax-deferred and penalty-free.

Roth IRAs and Inherited IRAs do not qualify – Most Employers require employment termination prior to using retirement funds. *Other plans may qualify

401(k) Plans 407 Plans (Government agencies) Cash Balance Plans Employee Stock Ownership Money Purchase Plans SEPs

403(b) Plans Annuity Plans Defined Benefits Plans IRAs Rollover Plans SIMPLE Plans

TYPES OF PLANS THAT QUALIFY

DIRECT THE INVESTMENTS & STOCK PURCHASE

You then direct how these funds are to be invested. The Plan design allows rollover contributions to be invested in the stock of the new company that sponsors the retirement plan.

The plan then purchases stock in the new company.

FOR EXAMPLE

For example, suppose you have $250,000 in an existing retirement plan and you require $150,000 to purchase a new business. Using the Rainmaker process, you can roll the entire $250,000 into your new company’s retirement plan. You would then direct $150,000 of the rollover to be invested in company stock.

Your new company ends up with $150,000 in cash that it can use for any legitimate business purpose, including payroll, rent, marketing, supplies, salaries, furniture and fixtures, and more. The plan ends up with company stock valued at $150,000.

DIVERSIFY REMAINING INVESTMENTS

Just like other qualified plans, rollovers, wage deferrals or employer contributions can be invested in other investment options such as stocks, bonds and mutual funds giving plan participants the ability to diversify their portfolios. Your financial advisor can assist you to determine what other types of investments to offer through your company’s new plan.

No Loan payments Current credit score not a factor Does not affect one’s debt ratio or credit rating Can be used as capital injection for SBA

Saves money Builds wealth Reduces emotional and financial concerns Can take a salary

WHAT ARE THE BENEFITS ?

IN SUMMARY…..

TO ROB OR NOT TO ROB?

Employer Securities(Personally Owned)

IRS -Thank You!!

$120,000

$80,000

Qualified EmployerSecurities (in Plan)

YOUR Other Tax DeferredInvestments

$120,000

$80,000

With ROBS Plan Without ROBS Plan

Employer Securities(Personally Owned)

IRS -Thank You!!

$120,000

TO ROB OR NOT TO ROB?

Qualified EmployerSecurities (in Plan)

YOUR Other Tax DeferredInvestments

$120,000

$80,000

With ROBS Plan Without ROBS Plan

REPORTING C-Corporation

Must File Annual Form 1120 All Other Tax/Withholding Filing Requirement (Federal, State & Local)

Must be Kept in Good Standing with State

REPORTING Plan

Annual 5500 (not 5500 EZ) Annual Summary Annual Report (SAR) Quarterly PPA Statements to Participants

Documents and Summary Plan Descriptions (SPD) must be kept current Participant Fee Disclosures

Forms 1099-R and 945 related to Distributions

HOW WE CAN DO WHAT WE DO Plan Asset Rules

Generally, when a plan invests in stock of a company that is not publicly traded nor issued by an investment company (e.g. Mutual Fund)

BOTH Issued Stock

AND Underlying Assets of Company

Are Considered PLAN ASSETS

HOW WE CAN DO WHAT WE DO Exception to General Rule

Entity is an “Operating Company” OR

Plan Owns Less than 25% of Entity

“Operating Company” – Primarily Involved in the Production or Sale of a Product or Service

HOW WE CAN DO WHAT WE DO Result

Your Corporate Assets are NOT Plan Assets!

HOW WE CAN DO WHAT WE DO Prohibited Transaction (“PT”) Exemption

Plan Purchasing or Selling Employer Securities to a Related Party is NOT a “PT” if:

“Eligible Individual Account Plan” (401(k) and Profit Sharing Plans meet requirement)

No Commission is Paid

If Transaction is for “Adequate Consideration”

HOW WE CAN DO WHAT WE DO “Adequate Consideration”

Agreed Upon Price when Buyer and Seller are “arms-length”

Otherwise, Based on Independent Appraisal

Result – if Plan is involved in the sale or purchase of Employer Securities with the C-Corp and Independent Appraisal is Required

www.simplenumbers.me

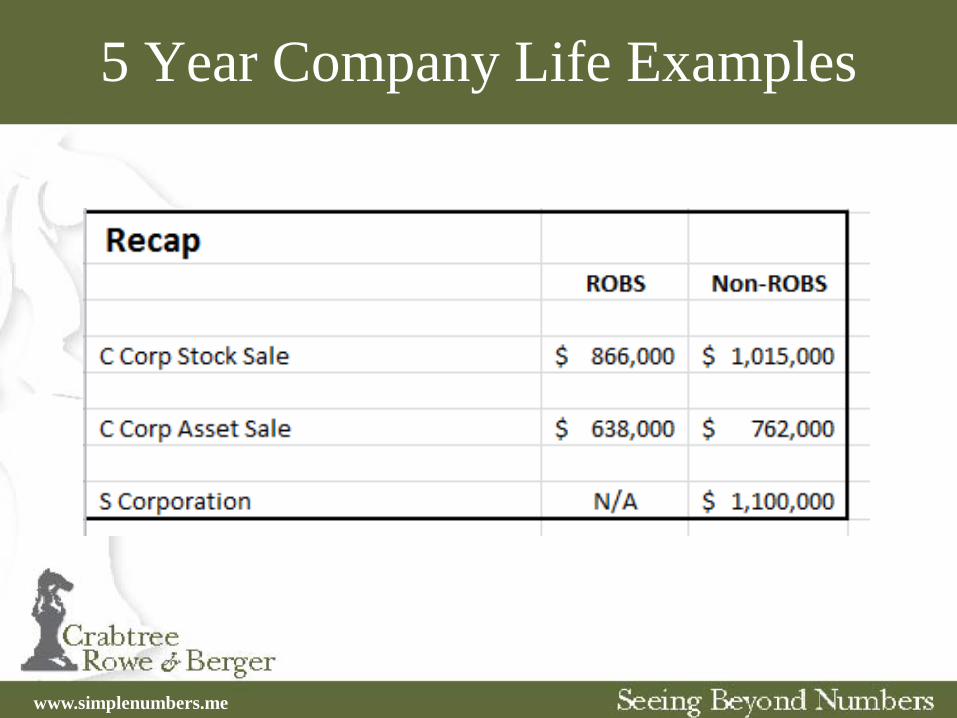

5 Year Company Life Examples

• C Corporation – Stock Sale (ROBS and Non-ROBS) – Asset Sale (ROBS and Non-ROBS)

• S Corporation

www.simplenumbers.me

5 Year Company Life Examples

www.simplenumbers.me

5 Year Company Life Examples

www.simplenumbers.me

5 Year Company Life Examples

www.simplenumbers.me

5 Year Company Life Examples

www.simplenumbers.me

5 Year Company Life Examples

www.simplenumbers.me

Roth Conversion

• Can convert shares over time • Need available cash to pay the tax • Will need stock appraisal

(recommend 2 appraisals) • Do not recommend if you need to

access funds before age 59 ½

www.simplenumbers.me

Key Takeaways • Capital is better than debt for start up • ROBS is a good option to consider over

debt if: – You stick to the rules! – Do not distort wages, profits or valuations – Run your business like you invested in

someone else's company – You can avoid an asset sale (consider giving

reps and do not agree to 381(a) adjustment in a C Corp stock sale)