Jonathan Jachym, Executive Director, Government Relations

US and EU Derivatives Regulatory Reform Update LBMA/LPPM Precious Metals Conference Rome 1 October 2013

1

© 2013 CME Group. All rights reserved

• Regulatory Landscape • Global overview and update

• EU legislative and regulatory structure

• Key EU legislative files

• Updates on US and EU Derivatives Regulation • Clearing

• Reporting

• Trading

• Commodity Derivatives: Key Regulatory Drivers

Presentation Overview

2

© 2013 CME Group. All rights reserved

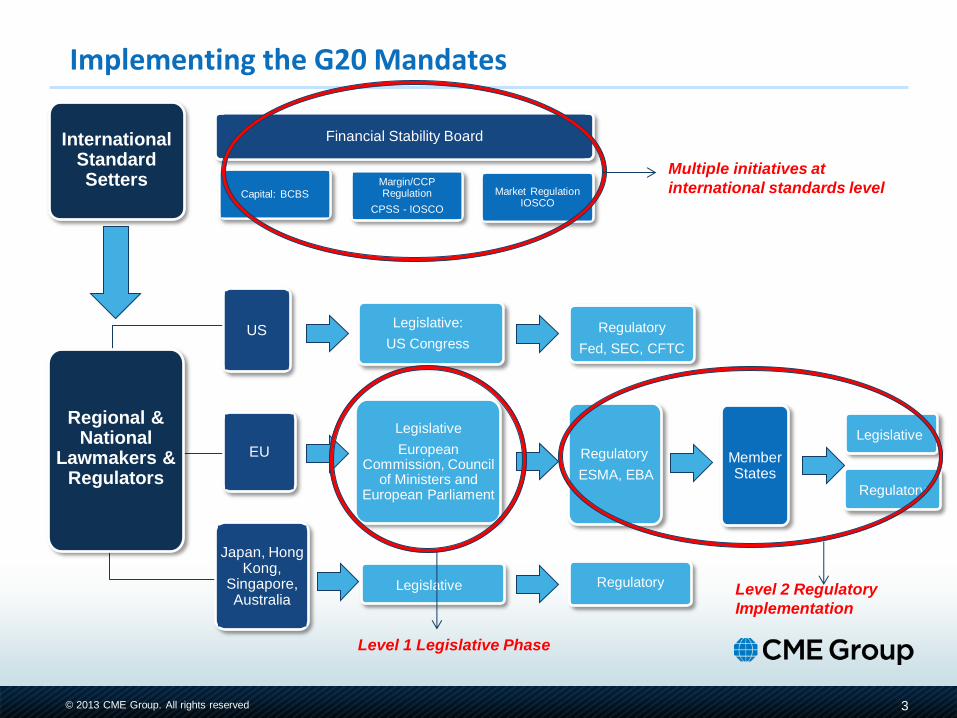

Implementing the G20 Mandates

Margin/CCP Regulation

CPSS - IOSCO

Capital: BCBS

Legislative:

US Congress

Regulatory

ESMA, EBA

Legislative

European Commission, Council

of Ministers and European Parliament

Legislative Regulatory

Member States

Legislative

Regulatory

EU

Regional & National

Lawmakers & Regulators

US

Japan, Hong Kong,

Singapore, Australia

Regulatory

Fed, SEC, CFTC

Market Regulation IOSCO

Financial Stability Board International Standard Setters

Level 2 Regulatory

Implementation

Level 1 Legislative Phase

Multiple initiatives at

international standards level

3

© 2013 CME Group. All rights reserved

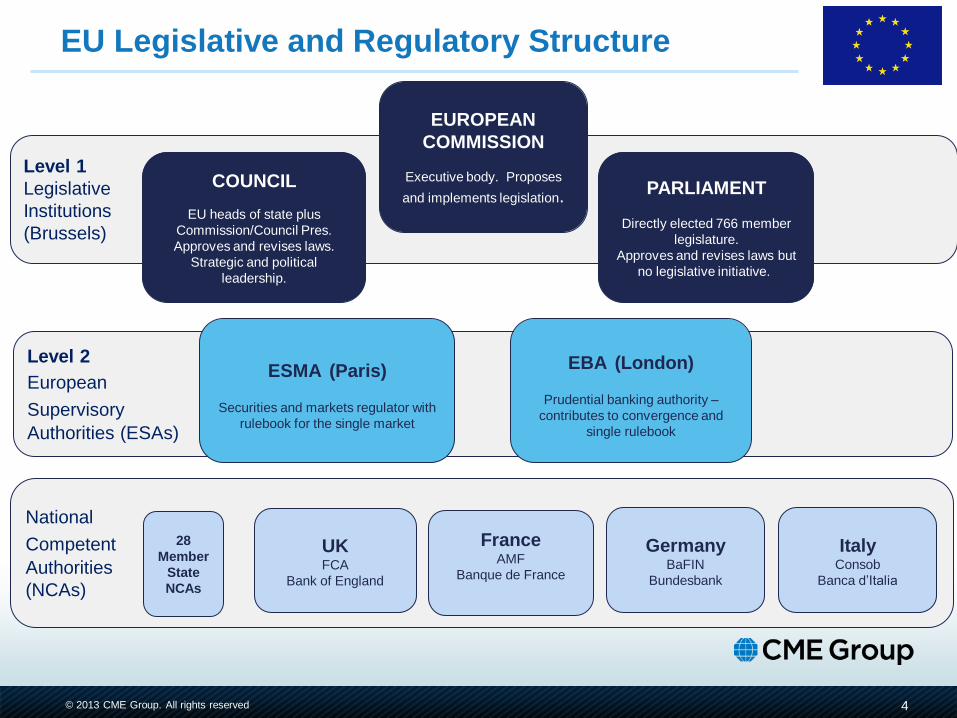

EU Legislative and Regulatory Structure

PARLIAMENT

Directly elected 766 member

legislature.

Approves and revises laws but

no legislative initiative.)

COUNCIL

EU heads of state plus

Commission/Council Pres.

Approves and revises laws.

Strategic and political

leadership.

EUROPEAN

COMMISSION

Executive body. Proposes

and implements legislation.

Germany BaFIN

Bundesbank

France AMF

Banque de France

UK FCA

Bank of England

Level 1

Legislative

Institutions

(Brussels)

Level 2

European

Supervisory Authorities (ESAs)

National

Competent Authorities

(NCAs)

ESMA (Paris)

Securities and markets regulator with

rulebook for the single market

EBA (London)

Prudential banking authority –

contributes to convergence and

single rulebook

28

Member

State

NCAs

Italy Consob

Banca d’Italia

4

© 2013 CME Group. All rights reserved

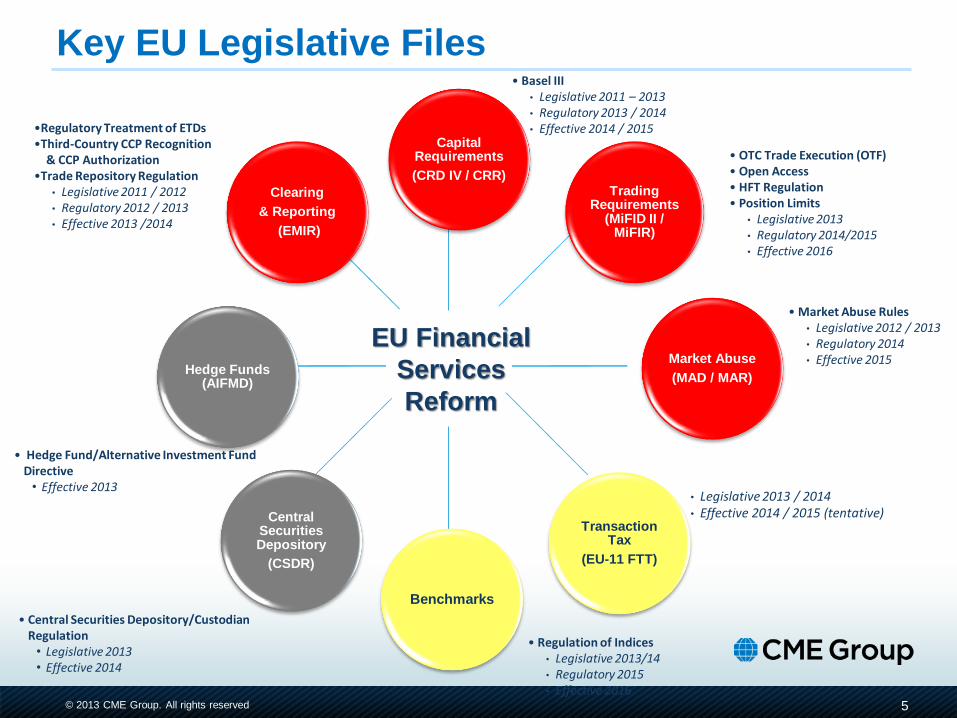

Transaction Tax

(EU-11 FTT)

Trading Requirements

(MiFID II / MiFIR)

Benchmarks

Capital Requirements

(CRD IV / CRR)

Market Abuse

(MAD / MAR)

Central Securities Depository

(CSDR)

Hedge Funds (AIFMD)

Clearing

& Reporting

(EMIR)

Key EU Legislative Files

• Legislative 2013 / 2014 • Effective 2014 / 2015 (tentative)

• OTC Trade Execution (OTF) • Open Access • HFT Regulation • Position Limits

• Legislative 2013 • Regulatory 2014/2015 • Effective 2016

• Regulation of Indices • Legislative 2013/14 • Regulatory 2015 • Effective 2016

• Basel III • Legislative 2011 – 2013 • Regulatory 2013 / 2014 • Effective 2014 / 2015

• Market Abuse Rules • Legislative 2012 / 2013 • Regulatory 2014 • Effective 2015

•Regulatory Treatment of ETDs •Third-Country CCP Recognition & CCP Authorization •Trade Repository Regulation

• Legislative 2011 / 2012 • Regulatory 2012 / 2013 • Effective 2013 /2014

EU Financial

Services

Reform

• Central Securities Depository/Custodian Regulation • Legislative 2013 • Effective 2014

• Hedge Fund/Alternative Investment Fund Directive • Effective 2013

5

© 2013 CME Group. All rights reserved

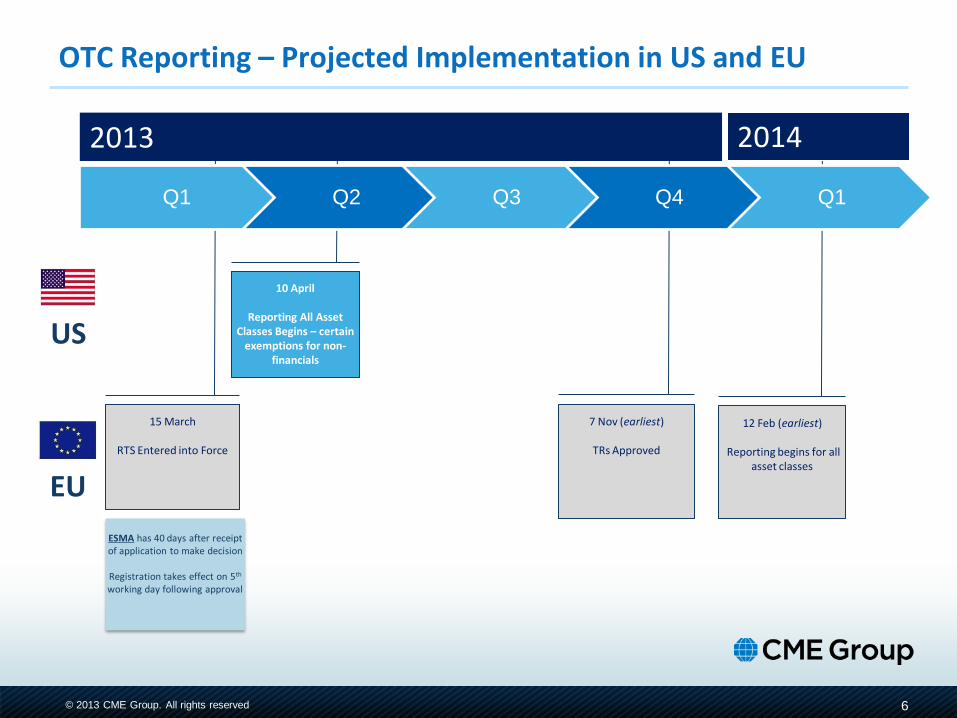

12 Feb (earliest)

Reporting begins for all asset classes

10 April

Reporting All Asset Classes Begins – certain

exemptions for non-financials

OTC Reporting – Projected Implementation in US and EU

7 Nov (earliest)

TRs Approved

15 March

RTS Entered into Force

2013 2014

US

EU

Q1 Q2 Q3 Q4 Q1

ESMA has 40 days after receipt of application to make decision

Registration takes effect on 5th working day following approval

6

© 2013 CME Group. All rights reserved

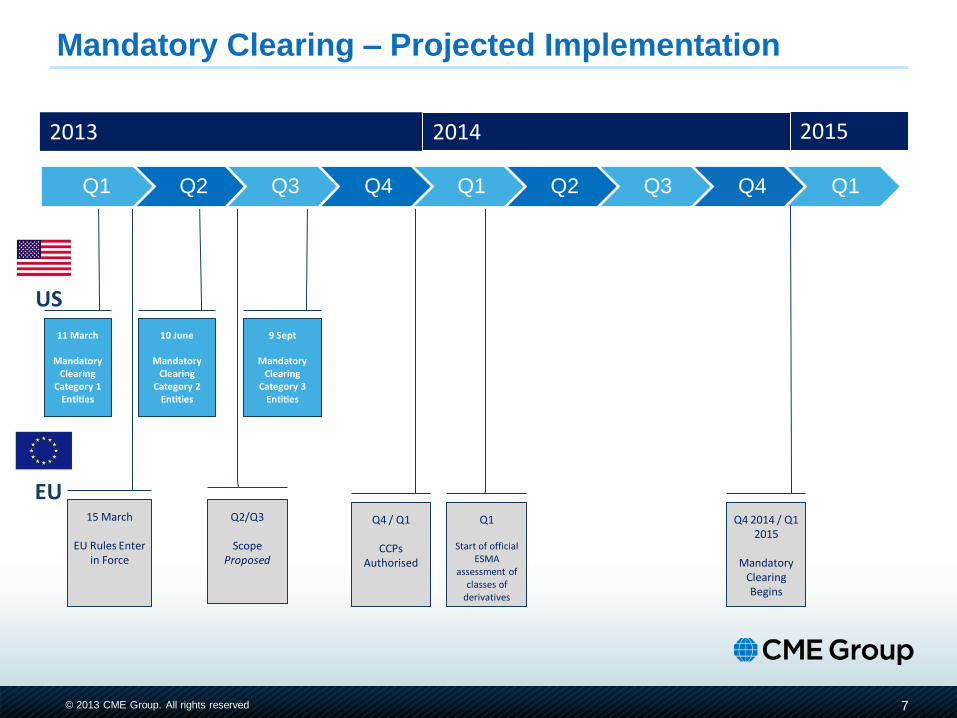

Q2/Q3

Scope Proposed

15 March

EU Rules Enter in Force

2013 2014

11 March

Mandatory Clearing

Category 1 Entities

10 June

Mandatory Clearing

Category 2 Entities

US

EU

9 Sept

Mandatory Clearing

Category 3 Entities

Q4 / Q1

CCPs Authorised

Q1

Start of official ESMA

assessment of classes of

derivatives

Mandatory Clearing – Projected Implementation

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1

2015

Q4 2014 / Q1 2015

Mandatory

Clearing Begins

7

© 2013 CME Group. All rights reserved

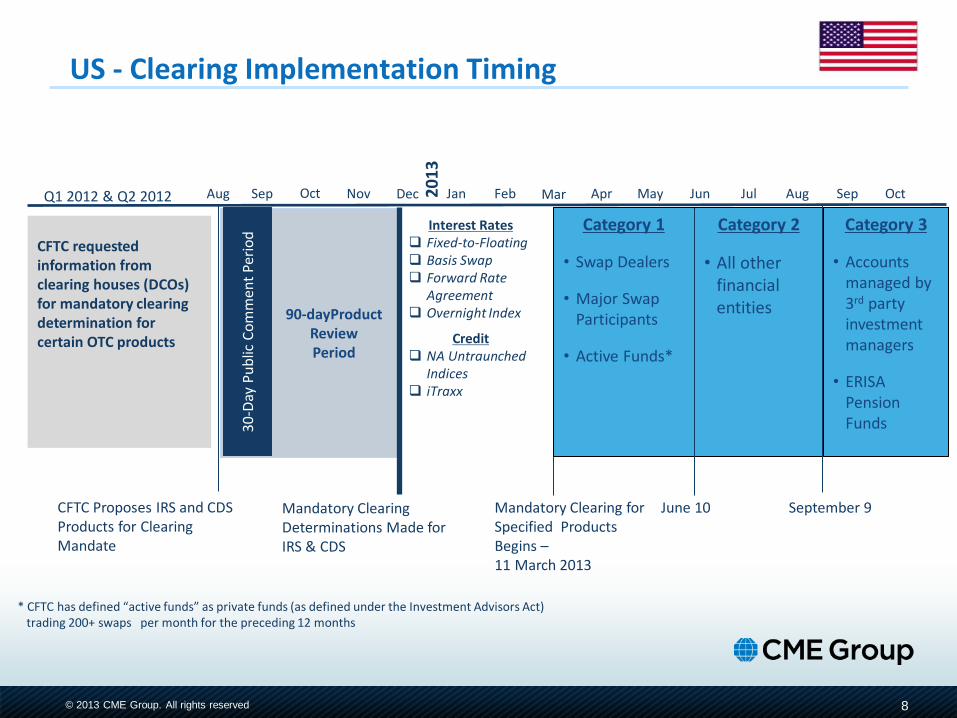

Interest Rates Fixed-to-Floating Basis Swap Forward Rate

Agreement Overnight Index

Credit NA Untraunched

Indices iTraxx

CFTC Proposes IRS and CDS Products for Clearing Mandate

Mandatory Clearing Determinations Made for IRS & CDS

CFTC requested information from clearing houses (DCOs) for mandatory clearing determination for certain OTC products

Category 2

• All other financial entities

Category 3

• Accounts managed by 3rd party investment managers

• ERISA Pension Funds

Category 1

• Swap Dealers

• Major Swap Participants

• Active Funds*

90-dayProduct Review Period

30-D

ay P

ub

lic C

om

me

nt

Peri

od

Q1 2012 & Q2 2012

Mandatory Clearing for Specified Products Begins – 11 March 2013

Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct 20

13

* CFTC has defined “active funds” as private funds (as defined under the Investment Advisors Act) trading 200+ swaps per month for the preceding 12 months

June 10 September 9

US - Clearing Implementation Timing

8

© 2013 CME Group. All rights reserved

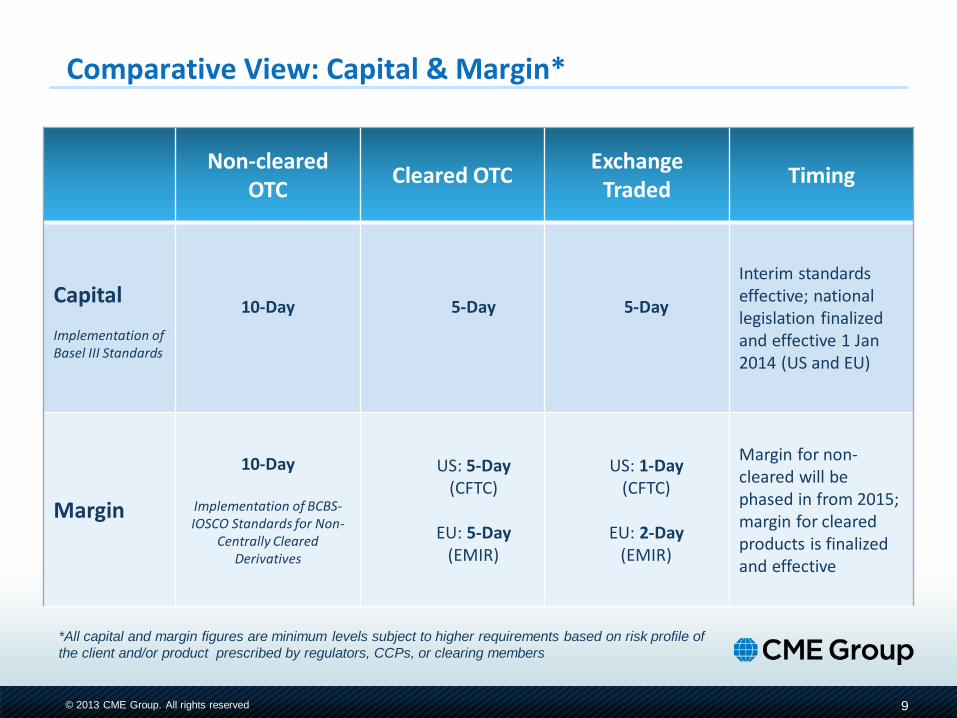

Non-cleared OTC

Cleared OTC Exchange

Traded Timing

Capital Implementation of Basel III Standards

10-Day

5-Day

5-Day

Interim standards effective; national legislation finalized and effective 1 Jan 2014 (US and EU)

Margin

10-Day

Implementation of BCBS-IOSCO Standards for Non-

Centrally Cleared Derivatives

US: 5-Day

(CFTC)

EU: 5-Day (EMIR)

US: 1-Day (CFTC)

EU: 2-Day

(EMIR)

Margin for non-cleared will be phased in from 2015; margin for cleared products is finalized and effective

Comparative View: Capital & Margin*

*All capital and margin figures are minimum levels subject to higher requirements based on risk profile of

the client and/or product prescribed by regulators, CCPs, or clearing members

9

© 2013 CME Group. All rights reserved

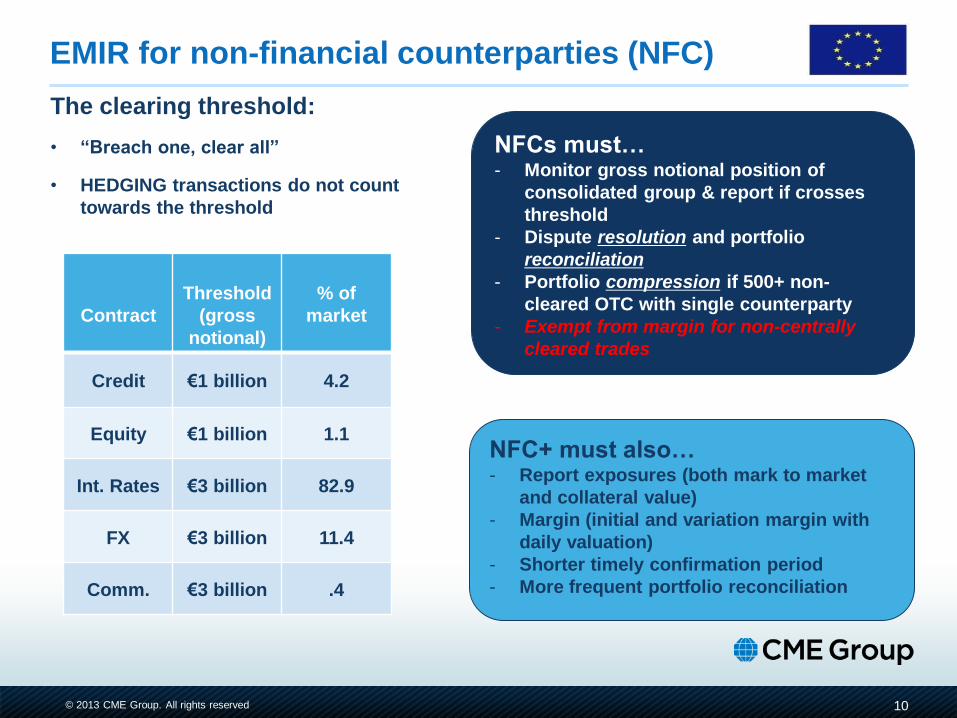

EMIR for non-financial counterparties (NFC)

The clearing threshold:

• “Breach one, clear all”

• HEDGING transactions do not count

towards the threshold

Contract

Threshold

(gross

notional)

% of

market

Credit €1 billion 4.2

Equity €1 billion 1.1

Int. Rates €3 billion 82.9

FX €3 billion 11.4

Comm. €3 billion .4

NFCs must… - Monitor gross notional position of

consolidated group & report if crosses

threshold

- Dispute resolution and portfolio

reconciliation

- Portfolio compression if 500+ non-

cleared OTC with single counterparty

- Exempt from margin for non-centrally

cleared trades

NFC+ must also…

- Report exposures (both mark to market

and collateral value)

- Margin (initial and variation margin with

daily valuation)

- Shorter timely confirmation period

- More frequent portfolio reconciliation

10

© 2013 CME Group. All rights reserved

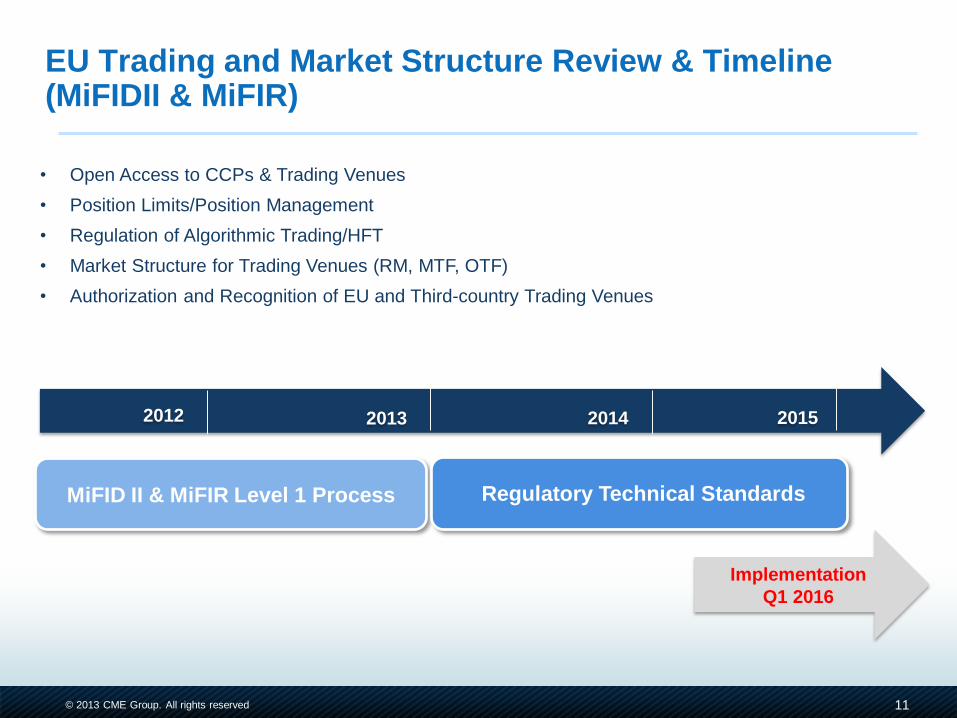

11

2013 2015 2014 2012

MiFID II & MiFIR Level 1 Process Regulatory Technical Standards

• Open Access to CCPs & Trading Venues

• Position Limits/Position Management

• Regulation of Algorithmic Trading/HFT

• Market Structure for Trading Venues (RM, MTF, OTF)

• Authorization and Recognition of EU and Third-country Trading Venues

EU Trading and Market Structure Review & Timeline (MiFIDII & MiFIR)

Implementation

Q1 2016

11

© 2011 CME Group. All rights reserved

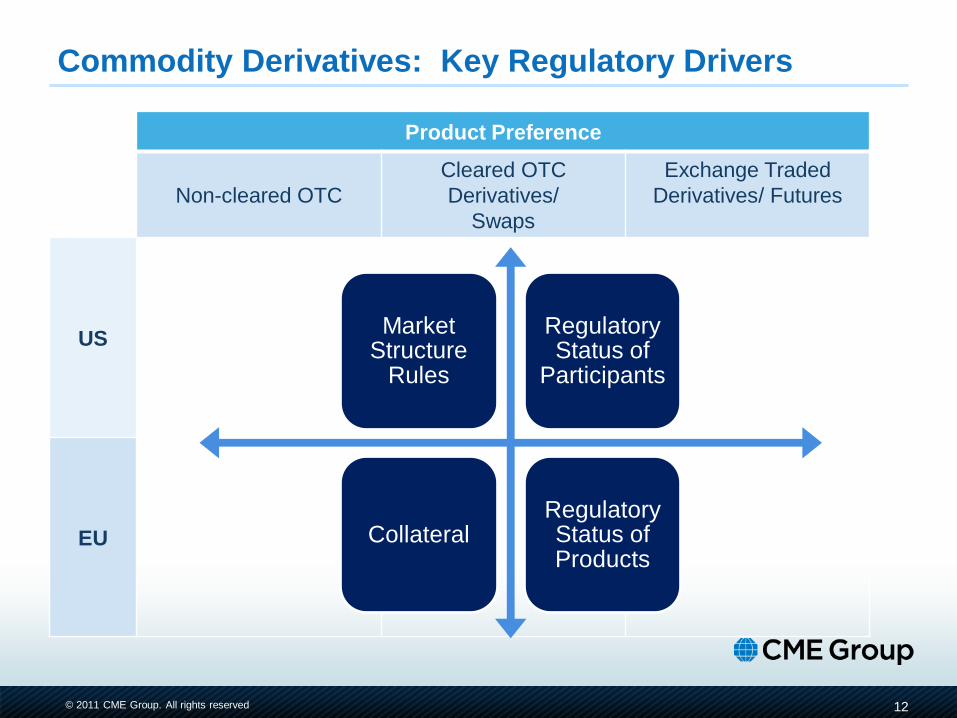

Commodity Derivatives: Key Regulatory Drivers

Product Preference

Non-cleared OTC

Cleared OTC

Derivatives/

Swaps

Exchange Traded

Derivatives/ Futures

US

EU

Market Structure

Rules

Regulatory Status of

Participants

Collateral Regulatory Status of Products

12