Urban Infrastructure Investment

Mechanisms, Possibilities, and Special Financing Vehicles

Infrastructure Development Finance Company Ltd.

2

Structure Background Current financing mechanisms Strengths and weaknesses of current

mechanisms New possibilities:

– Pooled Finance initiatives, Viability Gap Funding, Urban Funds

Bringing private capital into Urban Infra

Background

4

Galloping Urbanization Urban Population was 26% in 1991 likely to

increase to 36% in 2011– Rate of urban population growth likely to be

almost thrice that of total population growth

Urbanization picks up after reaching 25% according to international experience

Economic reforms and globalization will make cities primary wealth creators

5

India’s economic growth has been led by urban areas

India has become increasingly urban– 1981: 23 per cent, 1991: 26%, 2001: 29 per cent

Economic growth led by urban areas : industrial and service sectors accounted for – 1981 : 62 % of GDP– 2001: > 75% of GDP

More urbanized states recorded high growth rates– Tamil Nadu, Maharashtra, Karnataka, Gujarat, Delhi-Haryana

At the local level, larger cities in faster growing states have grown rapidly– Chennai, Hyderabad, Mumbai, Bangalore

6

Demand Supply Gap

Annual investment needs in Urban Infrastructure are about Rs. 400 billion*

as against an availability of Rs. 50 billion, (excluding new mass transit and

township development projects)

*give or take a few hundred billion!

7

Urban Infrastructure… Needing large investments in…

– Urban Transport– WatSan

– Desalination– Reuse of “pre-loved” water

– Solid Waste collection, transportation & disposal– Almost all States looking at SEZ development

(main developer as well as component developers) with private sector participation

– Investments are being actively sought even for the ‘traditional’ industrial area developments which now include Biotech parks, hardware parks, and so on

8

74th Constitutional Amendment

Introduces fundamental changes in system of urban governance– provides for regular and fair conduct of

elections through State Election Commissions– provides a framework for assignment of

appropriate civic functions (as per 12th Schedule of Constitution)

– States required to constitute State Finance Commissions to improve municipal finances

Current Financing Mechanisms

10

Government Funding Virtually the entire investment,

construction, operating, and maintenance is by government– Direct budgetary devolution (tax-payer

money)– Debt raised against government

guarantees, (and “letters of comfort”)– Financing primarily by HUDCO and LIC

11

Local Authority Funding After the 74th Amendment, there is

increasingly, funding generated by the ULB– Escrowing revenues such as property tax,

entry tax/ octroi– Selling/ securitizing land

12

Multilateral/ Bilateral Funding

World Bank, ADB, DFID…– Based on reform agenda– Fairly detailed appraisals done– Sectoral or project-wise– Generally addresses needs of urban poor

However, for commercial loans, based on Government of India Guarantees as security…

13

Private Sector Interest? Urban Infrastructure, has not yet found

investor interest in the absence of clear directions on various aspects - Risk, social/ political, Regulatory, cost recovery mechanisms, etc.

Various attempts are being made to convert Urban Service (water, waste-water, Solid waste, etc) into ‘Bankable projects’– This is likely to open a new area for

investments– And a new breed of ‘Operating’ companies to

provide these services

Strength & Weakness

…Of current Financing Mechanisms

15

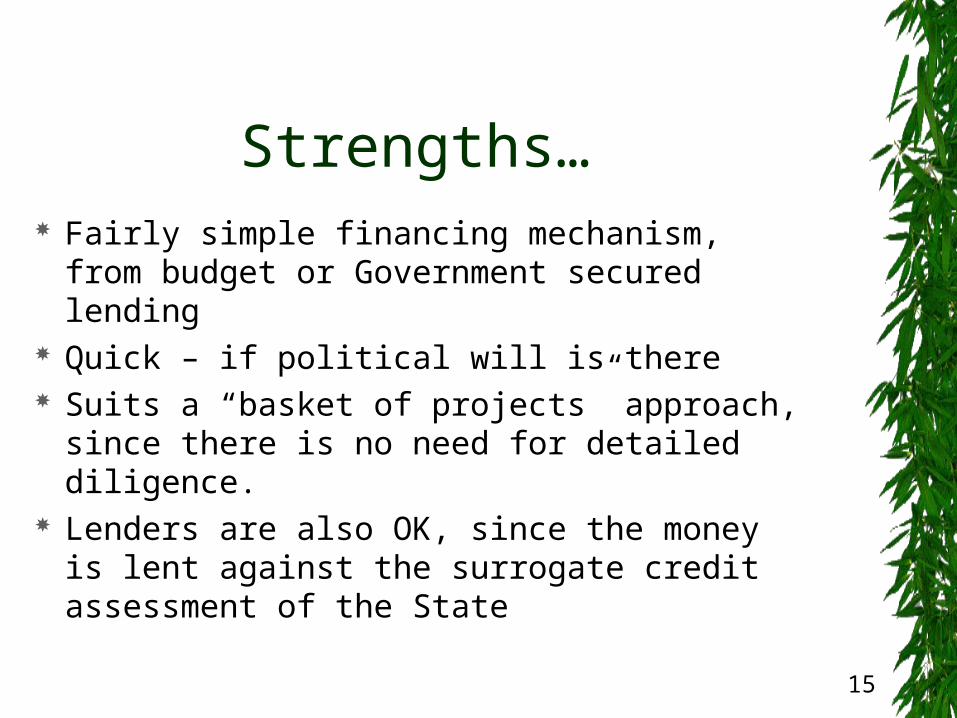

Strengths… Fairly simple financing mechanism, from

budget or Government secured lending Quick – if political will is there Suits a “basket of projects” approach, since

there is no need for detailed diligence. Lenders are also OK, since the money is

lent against the surrogate credit assessment of the State

16

Weakness… Practically no diligence on the project

financials– Viability, user-charge recovery, and such minor

issues are non-critical, high gestation period for loan sanction

Financial requirements are increasing way beyond direct budgetary/ guarantee capacity

State budget deficits and statutory guarantee limits constraining State Gov. funding capacity

No impetus to reform

Future Possibilities

& Some Progress Stories

18

Beginnings well made… May not be complete “success stories”, but:

– Tamil Nadu Tirupur, Alandur, TNUDF Pooled Finance

– Municipal Bond issues Ahmedabad, Hyderabad, Nashik

– Sukhthankar Committee, Maharashtra– Urban infrastructure funds – IFCG, Feedback U-

Fund and MUIF– BATF in Bangalore– Water O&M PSPs (attempts!) in Pune, Goa,

Bangalore, Hyderabad

19

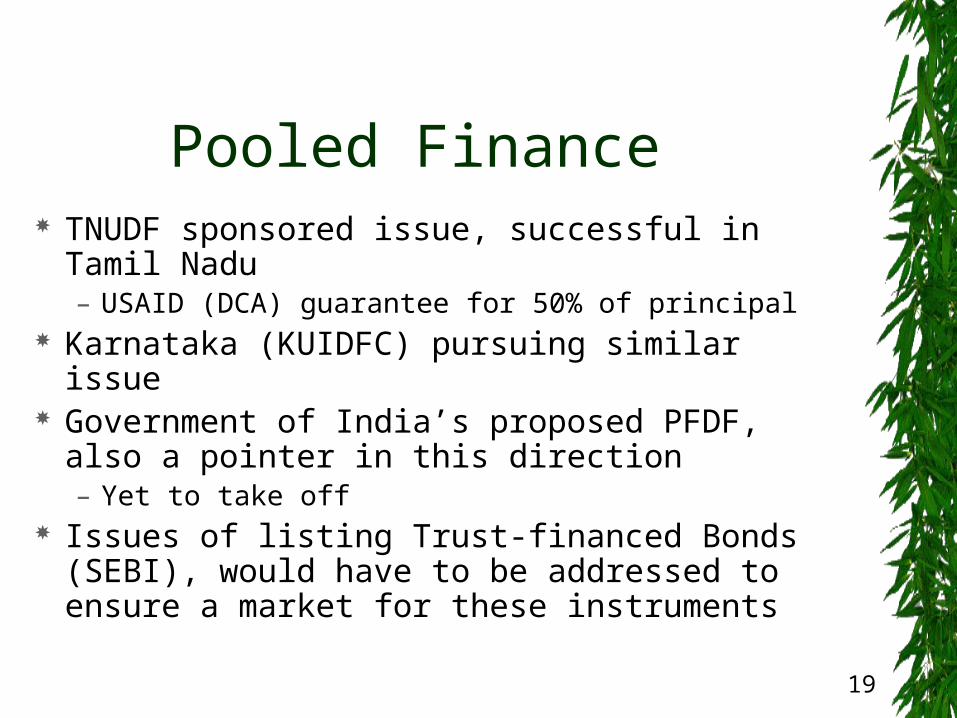

Pooled Finance TNUDF sponsored issue, successful in

Tamil Nadu– USAID (DCA) guarantee for 50% of principal

Karnataka (KUIDFC) pursuing similar issue Government of India’s proposed PFDF, also

a pointer in this direction– Yet to take off

Issues of listing Trust-financed Bonds (SEBI), would have to be addressed to ensure a market for these instruments

20

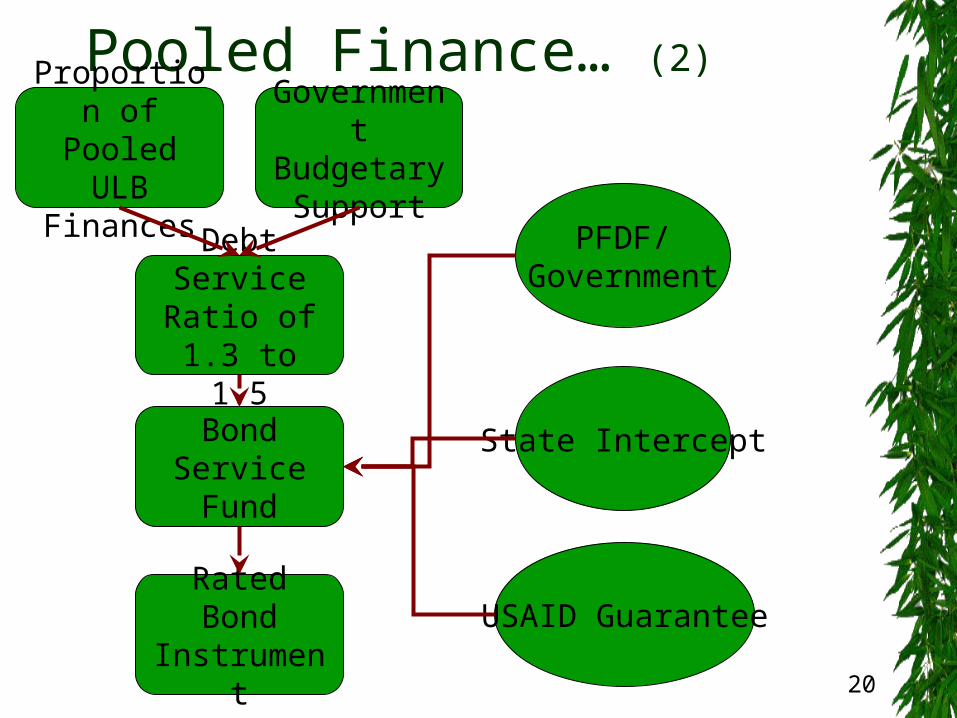

Pooled Finance… (2)Proportion of Pooled ULB

Finances

Government Budgetary Support

Debt Service Ratio of 1.3

to 1.5

PFDF/Government

Bond Service Fund

State Intercept

USAID GuaranteeRated Bond Instrument

21

Viability Gap Funding Proposed by Government of India

– To “Prop-up” marginally viable projects– Established and clear guidelines for

allocation Problem may be in the lack of developed and

structured projects, that are eligible to claim this assistance

Also will take time to disseminate info/ capability to the ULB level

22

Capital Market Access Bond issues of Ahmedabad,

Hyderabad, BMP, Nashik etc., have not led to large-scale replication– Issues of market appetite, end-use– Limited number of ULBs which can

access financing on a standalone basis– Pooled Finance seems a more

appropriate structure for small ULBs

23

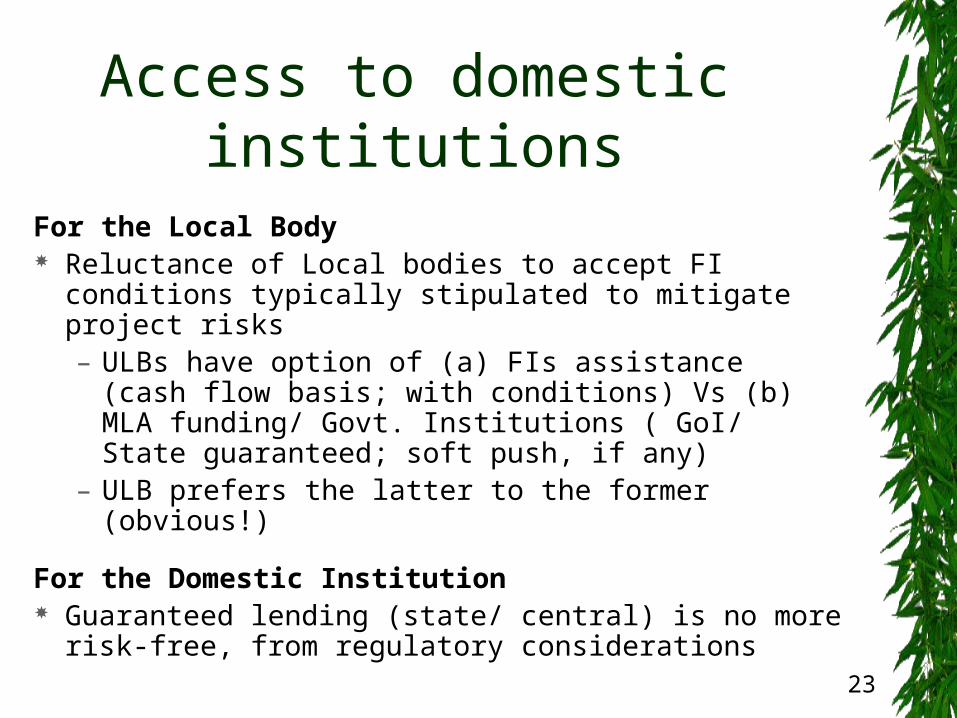

Access to domestic institutions

For the Local Body Reluctance of Local bodies to accept FI conditions

typically stipulated to mitigate project risks– ULBs have option of (a) FIs assistance (cash flow

basis; with conditions) Vs (b) MLA funding/ Govt. Institutions ( GoI/ State guaranteed; soft push, if any)

– ULB prefers the latter to the former (obvious!)

For the Domestic Institution Guaranteed lending (state/ central) is no more risk-

free, from regulatory considerations

24

Earmarked Urban Funds The CCF, URIF, PFDF, IFCG and MUIF

were envisaged by GoI/ State Govt., 3 years ago– Did not take off very well

Too small a corpus, too long a wish-list of reform interventions sought

Proposal to consolidate the existing Central Govt. funds (Mega City, IDSMT, etc.), to make them better oriented to the proposed end-use

Bringing Private Capital

---into Urban Infrastructure

26

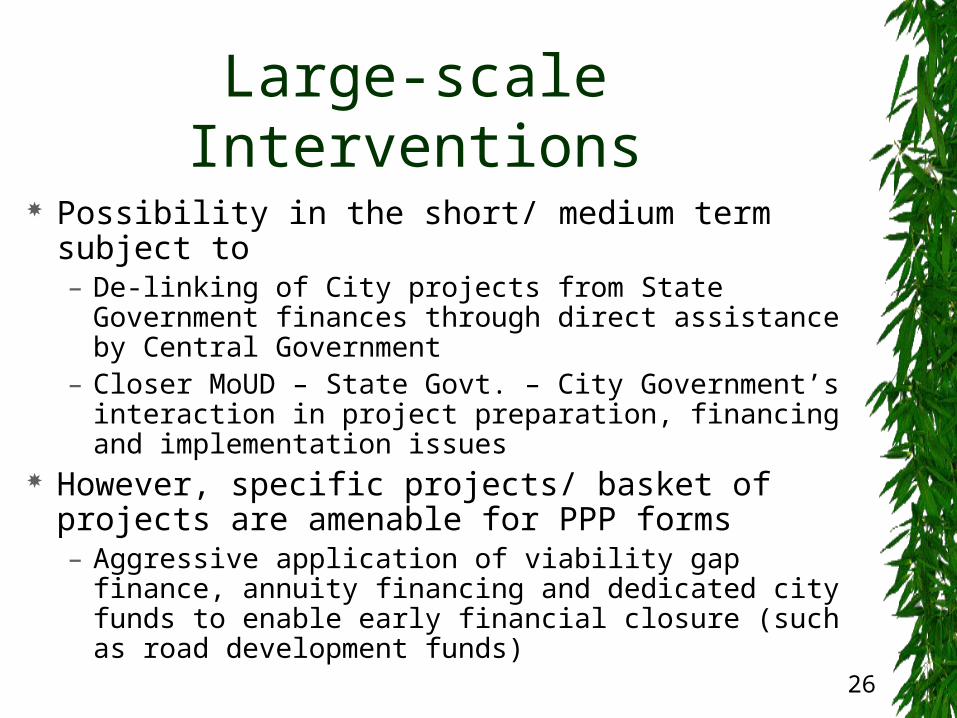

Large-scale Interventions Possibility in the short/ medium term subject to

– De-linking of City projects from State Government finances through direct assistance by Central Government

– Closer MoUD – State Govt. – City Government’s interaction in project preparation, financing and implementation issues

However, specific projects/ basket of projects are amenable for PPP forms– Aggressive application of viability gap finance,

annuity financing and dedicated city funds to enable early financial closure (such as road development funds)

Conclusions

& Way Forward

28

Reasons to be optimistic Realization of need for improvement of

Urban Services, and concurrently, the finance needed for doing so

Various precedents are being tried and tested, and experience is maturing– But yet a long way to go

29

Conducive Macro-economic Policies

0

100

200

300

400

East Asia andPacif ic

Europe andCentral Asia

Latin Americaand the

Caribbean

Middle Eastand North

Africa

South Asia Sub-SaharanAfrica

Investment in Infrastructure Projects with Private Participation by Region, 1991-2001, $ Billion.

Source : World Bank WP 5, 2003

30

Fiscal policy – Tax policy

–Widening of tax bases–User charges

– Policy of fiscal transfers – decentralization of powers and finances

Fiscal Policies

31

Making Local Governments Credit Worthy– Make property taxes more buoyant– Make subventions from higher levels less discretionary – Decentralize more services – Freeing Property markets (ULCRA, DDA and even in

China’s SEZs) Making Urban Infrastructure Projects

Commercially viable– There is a need for many borrowers, investors and

intermediaries– Urban infrastructure projects will require credit

enhancement

Capacity Building For ULBs

32

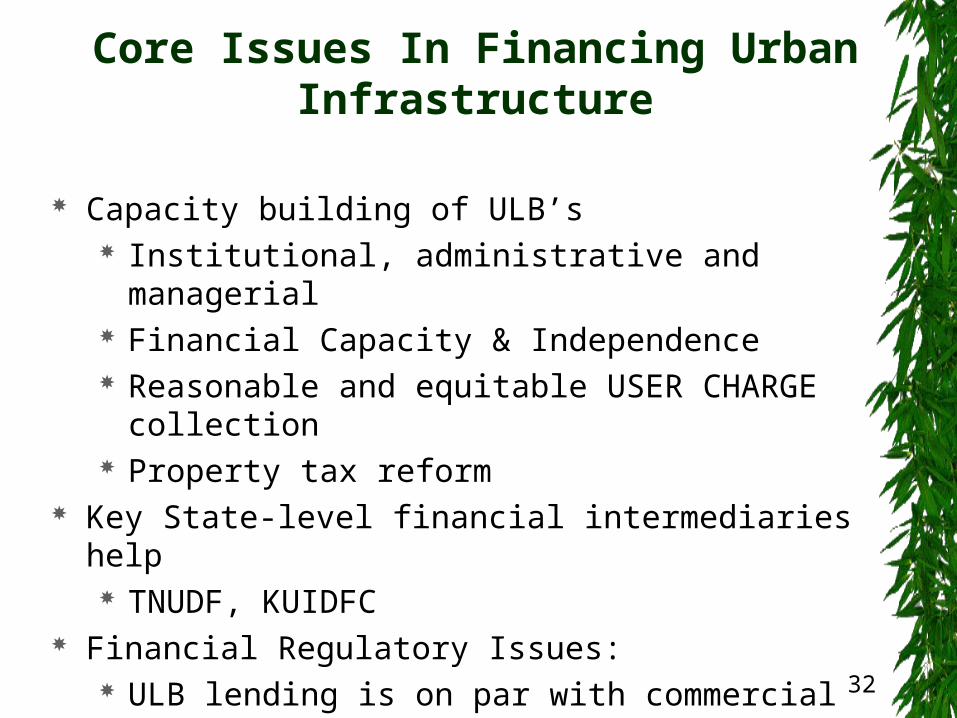

Capacity building of ULB’s Institutional, administrative and managerial Financial Capacity & Independence Reasonable and equitable USER CHARGE collection Property tax reform

Key State-level financial intermediaries help TNUDF, KUIDFC

Financial Regulatory Issues: ULB lending is on par with commercial lending, for

accounting, prudential norms, and provisioning Efficient Service Provision – PSP as appropriate

Core Issues In Financing Urban Infrastructure

33

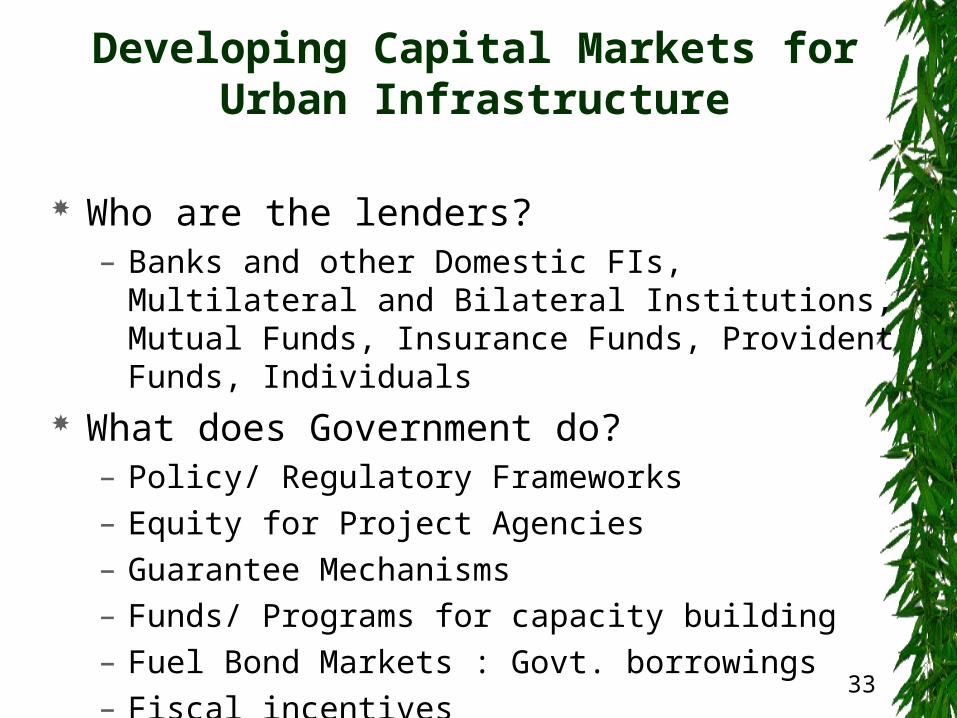

Who are the lenders?– Banks and other Domestic FIs, Multilateral and

Bilateral Institutions, Mutual Funds, Insurance Funds, Provident Funds, Individuals

What does Government do?– Policy/ Regulatory Frameworks– Equity for Project Agencies– Guarantee Mechanisms– Funds/ Programs for capacity building– Fuel Bond Markets : Govt. borrowings– Fiscal incentives

Developing Capital Markets for Urban Infrastructure

34

Conclusions Cities have coped reasonably well in the past

– But under stress now: Challenges faced by huge investment and O&M requirements

– No reason why the problem cannot be addressed in the future

Clear policy and regulatory frameworks needed Local capacities must be strengthened

Decentralization to be actually implemented Mobilize and leverage all resources possible

including private investment/ PPPs

Thank You