1 © 2016 PT KPMG Siddharta Advisory (Registration No: 09.05.1.70.85569), an Indonesian limited liability company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Document Classification: KPMG Confidential

25 October 2016

KPMG Siddharta Advisory

kpmg.com/id

Unlocking the value of Internal Audit The current and future state of Internal Audit in Indonesia

2 © 2016 PT KPMG Siddharta Advisory (Registration No: 09.05.1.70.85569), an Indonesian limited liability company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Document Classification: KPMG Confidential

Introductions – with you today

Gary Chia Partner, Risk Consulting (Head of Financial Services and Regulatory Compliance) KPMG Singapore Tel: +65 6213 2071 Email: [email protected]

Antonius Augusta Partner, Head of Risk Consulting KPMG Indonesia Tel: +62 215740877 Email: [email protected]

James Loh Partner, Risk Consulting (Head of Financial Risk Management) KPMG Indonesia Tel: +62215746308 Email: [email protected]

3 © 2016 PT KPMG Siddharta Advisory (Registration No: 09.05.1.70.85569), an Indonesian limited liability company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Document Classification: KPMG Confidential

Time Topic

0900 - 0915 Welcome and introduction

0915 - 0945 KPMG Indonesia Internal Audit Survey Launch

0945 - 1130 Key survey findings and themes (facilitated discussion)

1130 - 1145 Key takeaways

1145 - 1200 Q&A

What we will discuss

4 © 2016 PT KPMG Siddharta Advisory (Registration No: 09.05.1.70.85569), an Indonesian limited liability company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Document Classification: KPMG Confidential

Objectives of the IA roundtable

• Connect you with a selected group of Internal Audit (IA) professionals

• Engage in insightful conversations about key risks, trends, practices and common challenges

• Share and learn about better practices for internal audit across industries

• Build stronger IA network and community

Survey background

6 © 2016 PT KPMG Siddharta Advisory (Registration No: 09.05.1.70.85569), an Indonesian limited liability company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Document Classification: KPMG Confidential

Cyber security risk

Regulatory risk

Emerging technology risk

Strategic risk

Geopolitical risk

30%

28%

26%

25%

24%

Top 5 key risks that CEOs are most concerned about

Source: 2016 Global CEO Outlook, KPMG International

7 © 2016 PT KPMG Siddharta Advisory (Registration No: 09.05.1.70.85569), an Indonesian limited liability company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Document Classification: KPMG Confidential

Top 10 key IA risks for banking and capital markets

Source: KPMG Internal Audit: Top 10 key risks in 2016, Banking and Capital Markets

8 © 2016 PT KPMG Siddharta Advisory (Registration No: 09.05.1.70.85569), an Indonesian limited liability company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Document Classification: KPMG Confidential

Clarifying the role of IA

Figure 1: The KPMG ‘4 Lines of Defence’ model

Isolated? Findings? Basement?

Checker? Collaborative? Insights? Boardroom?

Business Advisor?

9 © 2016 PT KPMG Siddharta Advisory (Registration No: 09.05.1.70.85569), an Indonesian limited liability company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Document Classification: KPMG Confidential

Recent KPMG Surveys

Background to the KPMG Indonesia IA survey

Figure 2: The KPMG IA Quality Assurance Review (QAR) Framework

10 © 2016 PT KPMG Siddharta Advisory (Registration No: 09.05.1.70.85569), an Indonesian limited liability company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Document Classification: KPMG Confidential

53% 51% represent the Financial Services

Survey demographics are Chief Audit Executives (CAEs)

Chart 1: Role in your organisation Chart 2: Analysis of sector representation

11 © 2016 PT KPMG Siddharta Advisory (Registration No: 09.05.1.70.85569), an Indonesian limited liability company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Document Classification: KPMG Confidential

IA generally adds value but improvements required

Q27. In your view, does IA contribute to improving the quality and effectiveness of governance, risk management, and internal control processes? Q29. Does IA add value to your organisation beyond compliance (e.g. enhancing control environment to mitigate high risk areas, improving efficiency in business process, providing practical recommendations on procedural matters, etc.)?

Chart 3: IA’s contribution Chart 4: IA’s value adding

55% 62% expressed that IA adds value beyond compliance

found their IA effective in contributing to governance, risk management and internal controls

12 © 2016 PT KPMG Siddharta Advisory (Registration No: 09.05.1.70.85569), an Indonesian limited liability company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Document Classification: KPMG Confidential

Key market insights and themes

Risk based aud it ing • To what extent does IA conduct risk based audits?

Integrated assurance • How is IA achieving an integrated assurance approach with risk management,

compliance and other lines of defence?

Technology • To what extent is IA leveraging technology, in terms of data analytics and

additional assurance methods (such as continuous auditing)?

13 © 2016 PT KPMG Siddharta Advisory (Registration No: 09.05.1.70.85569), an Indonesian limited liability company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Document Classification: KPMG Confidential

What is integrated assurance? Coordinated Enterprise Assurance

Compliance – corporate

Internal audit

External audit

Technical evaluation

group

Sustainable development

assurance Corporate

Compliance – product groups

Communities Security

Group Risk

Other

Integrated Assurance: • Coordination of assurance activities • Minimize gaps, maximize overlaps • Coordinated teams where appropriate • Consistency of approach, ratings and

monitoring • Common risk vocabulary and consistent

reporting to executive management and the Board

• Benefits: cost savings (redundant

activities eliminated and common information is shared)

Risk based auditing

15 © 2016 PT KPMG Siddharta Advisory (Registration No: 09.05.1.70.85569), an Indonesian limited liability company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Document Classification: KPMG Confidential

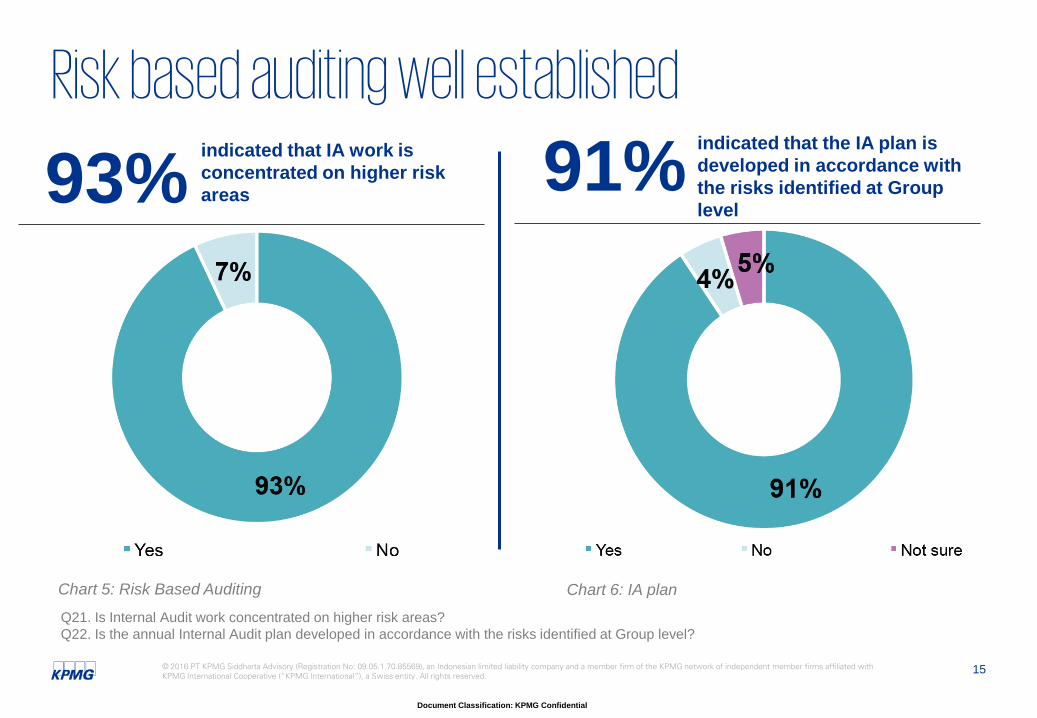

Risk based auditing well established

Chart 5: Risk Based Auditing

93% indicated that IA work is concentrated on higher risk areas

Q21. Is Internal Audit work concentrated on higher risk areas? Q22. Is the annual Internal Audit plan developed in accordance with the risks identified at Group level?

91% indicated that the IA plan is developed in accordance with the risks identified at Group level

Chart 6: IA plan

16 © 2016 PT KPMG Siddharta Advisory (Registration No: 09.05.1.70.85569), an Indonesian limited liability company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Document Classification: KPMG Confidential

What are the current IA priorities?

Chart 7: IA’s current priorities Q8a. Please identify the top three areas on which Internal Audit in your organisation is currently focusing.

Do these results surprise you? What are your current IA priorities?

1st 2nd

3rd Surprising?

17 © 2016 PT KPMG Siddharta Advisory (Registration No: 09.05.1.70.85569), an Indonesian limited liability company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Document Classification: KPMG Confidential

What are the IA priorities in the next 3-5 years?

Chart 8: IA’s future priorities Q8b. Please identify the top three areas on which Internal Audit in your organisation is going to focus on in the next 3-5 years.

Are you experiencing any changes in future IA priorities/expectations?

Joint 1st 2nd

3rd Surprising?

18 © 2016 PT KPMG Siddharta Advisory (Registration No: 09.05.1.70.85569), an Indonesian limited liability company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Document Classification: KPMG Confidential

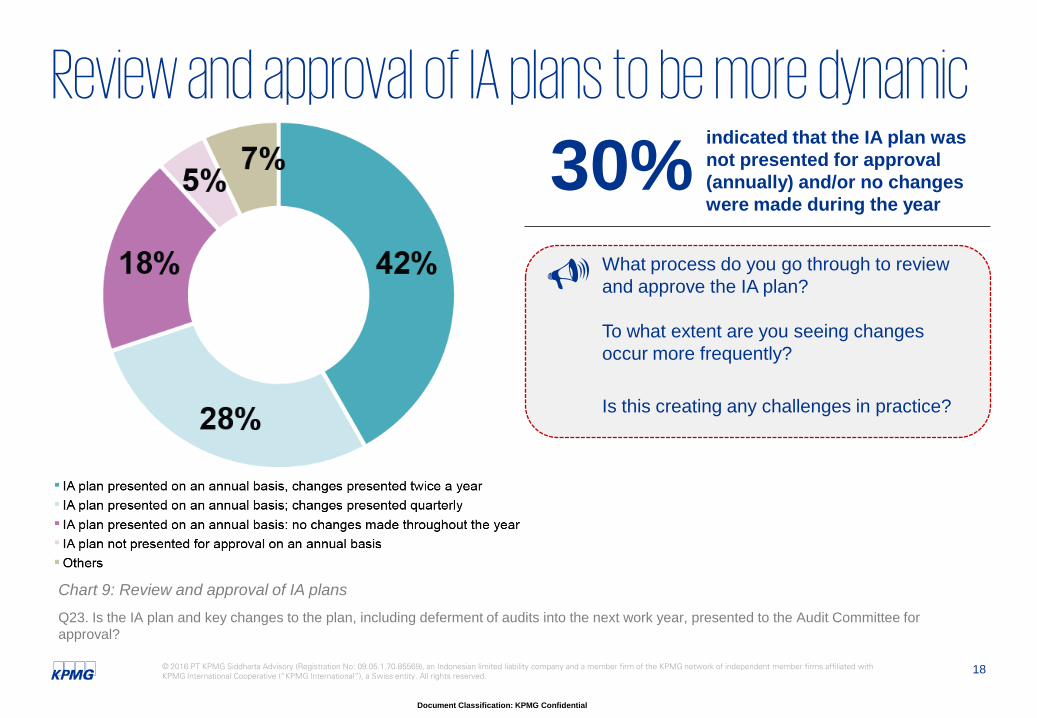

Q23. Is the IA plan and key changes to the plan, including deferment of audits into the next work year, presented to the Audit Committee for approval?

Chart 9: Review and approval of IA plans

Review and approval of IA plans to be more dynamic

30% indicated that the IA plan was not presented for approval (annually) and/or no changes were made during the year

What process do you go through to review and approve the IA plan? To what extent are you seeing changes occur more frequently? Is this creating any challenges in practice?

Integrated assurance

20 © 2016 PT KPMG Siddharta Advisory (Registration No: 09.05.1.70.85569), an Indonesian limited liability company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Document Classification: KPMG Confidential

Q13. If your company has an in-house Internal Audit function, what is its structure?

Chart 10: Structure of IA function

What is the structure of your IA function?

24% indicated a combined IA, Risk Management and Compliance function

How is your IA function currently structured?

21 © 2016 PT KPMG Siddharta Advisory (Registration No: 09.05.1.70.85569), an Indonesian limited liability company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Document Classification: KPMG Confidential

Q12. In your opinion, does IA collaborate well with the Compliance and Risk Management functions in managing the company's risks? Chart 11: IA’s approach to collaboration

41% expressed that IA collaborates well with the Compliance and Risk Management functions all the time

To what extent are there multiple sources of assurance over key risks in your company? How are you achieving integrated assurance with compliance, risk and other lines of defence? Which function takes the lead in driving the integrated assurance approach?

Does your IA collaborate well?

22 © 2016 PT KPMG Siddharta Advisory (Registration No: 09.05.1.70.85569), an Indonesian limited liability company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Document Classification: KPMG Confidential

Q10. In your opinion, is the size and structure of IA appropriate for effective audit coverage across the business areas?

Chart 12: Size and structure of an effective IA

To what extent are the skills of your IA relevant?

30% are confident that their IA possess skills and experience that are appropriate across the business areas

What skill-sets do you look for when recruiting IA personnel? What challenges exist in the market currently to meet these requirements?

23 © 2016 PT KPMG Siddharta Advisory (Registration No: 09.05.1.70.85569), an Indonesian limited liability company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Document Classification: KPMG Confidential

Chart 13: Core competencies ‘ranking Q20. Please rank the following core competencies in your preferred order of importance for Internal Auditors.

Critical competencies for IA to deliver Do these results resonate with you?

Are there other critical competencies you look for? To what extent do you outsource/co-source specialist skills and competencies?

1st

2nd 3rd

Surprising?

24 © 2016 PT KPMG Siddharta Advisory (Registration No: 09.05.1.70.85569), an Indonesian limited liability company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Document Classification: KPMG Confidential

A more structured approach to training is required

Chart 14: Training topics’ ranking Q18. Please select the training topics that you believe are critical to build up your IA capacity. You may choose more than one training topic.

Do you have a formal and structured training program for your IA function? What is the split between on-line vs classroom style training? To what extent has that been reviewed for effectiveness?

1st 2nd 3rd

Technology

26 © 2016 PT KPMG Siddharta Advisory (Registration No: 09.05.1.70.85569), an Indonesian limited liability company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Document Classification: KPMG Confidential

Q32: Does IA leverage on technology (such as data analytics) to increase audit effectiveness and efficiency, and enhance productivity?

Chart 15: Technology leverage

Technology not being leveraged sufficiently by IA

64% do not currently leverage technology to increase IA effectiveness and efficiency

To what extent do you use data analytics on your IA reviews? What systems do you use? What are the key challenges and how do you overcome them?

27 © 2016 PT KPMG Siddharta Advisory (Registration No: 09.05.1.70.85569), an Indonesian limited liability company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Document Classification: KPMG Confidential

Chart 16: Technology leverage for financial and non-financial services

Comparison of FS and non-FS tech usage

65% of financial services responded positively to utilizing data analytics tools compared to only 32% of non-financial services

Q32: Does IA leverage on technology (such as data analytics) to increase audit effectiveness and efficiency, and enhance productivity?

Surprising? How do we leverage technology to provide

additional assurance e.g. continuous monitoring and auditing?

Key takeaways

29 © 2016 PT KPMG Siddharta Advisory (Registration No: 09.05.1.70.85569), an Indonesian limited liability company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Document Classification: KPMG Confidential

Key takeaways

Consider the optimal structure and resourcing model for the IA function to deliver a sufficient coverage in terms of breadth and depth of projects 2

3 4 5

Develop a business case for investing in technology to enhance the depth of analysis and coverage

Establish a better coordination across the providers of assurance (internal and external auditors)

Enhance the skills and experience of the IA function

Establish regular communication between IA and key stakeholders to firm up the key focus areas 1

Question & Answer session

31 © 2016 PT KPMG Siddharta Advisory (Registration No: 09.05.1.70.85569), an Indonesian limited liability company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Document Classification: KPMG Confidential

2013 2015 201

4 2016

Key thought leadership reference points

2014

Copies and more information are available at www.kpmg.com.sg or www.kpmg.com/id

Thank you!

kpmg.com/socialmedia kpmg.com/app

The information contained herein is of a general nature and is not intended to address the circumstances of any particular individual or entity. Although we endeavour to provide accurate and timely information, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. No one should act on such information without appropriate professional advice after a thorough examination of the particular situation. © 2016 PT KPMG Siddharta Advisory, an Indonesian limited liability company and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.