Unit 3 - Investing: Unit 3 - Investing: Making Money Work for YouMaking Money Work for You

Mr. Vogel

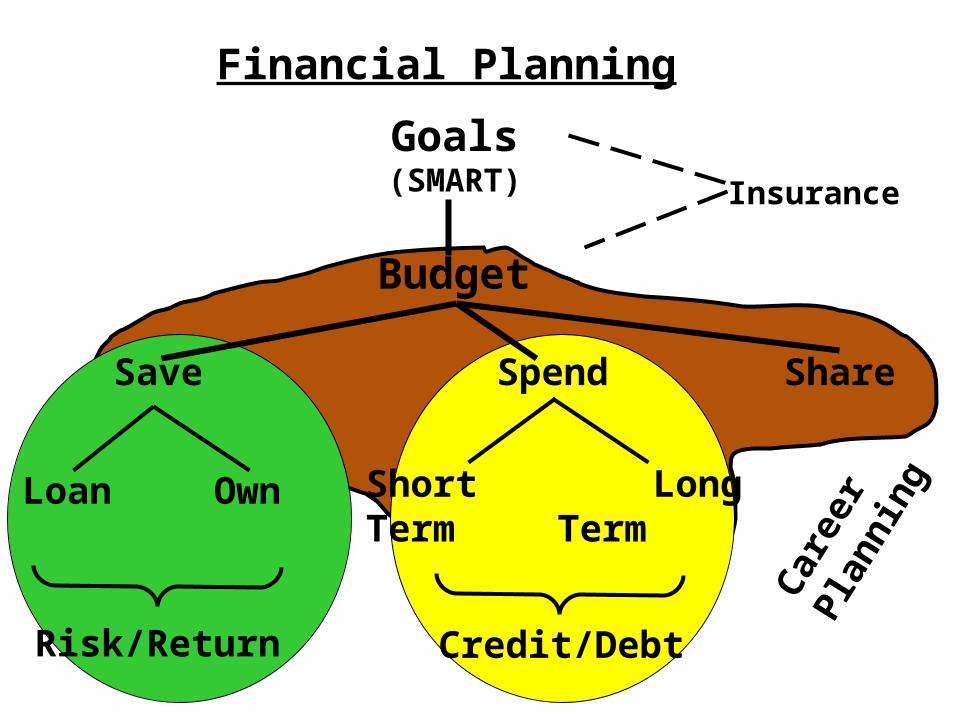

Financial Planning

Goals(SMART)

Budget

Save Spend Share

Loan Own Short LongTerm Term

Risk/Return Credit/Debt

Car

eer

Plan

ning

Insurance

Credit/Debt - Review

Is it part of your Plan (Budget) ???

Use Emergency Fund for your emergencies

Use Insurance for any catastrophies

Concept of Compounding – time and interest rate

T I M E

You areHERE

T I M E

T I M E

T I M E

T I M E

T I M E

T I M E

T I M E

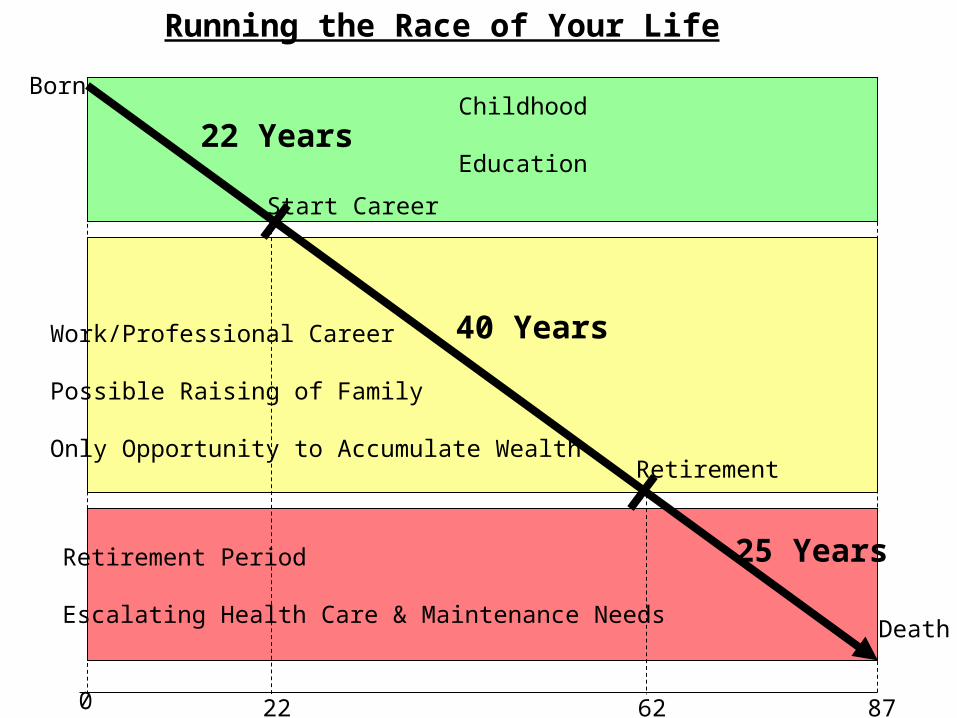

Born

Start Career

Retirement

Death

0 22 62 87

22 Years

40 Years

25 Years

Childhood

Education

Work/Professional Career

Possible Raising of Family

Only Opportunity to Accumulate Wealth

Retirement Period

Escalating Health Care & Maintenance Needs

Running the Race of Your Life

10 20 30 40 50 60 70

Ag e

18

Age

28

10 Years

Invested$20,000

Age

31

Age

65

35 Years

Invested$70,000

$276,474

$361,418

At Age 65

Assumptions: Save $2,000 per year Compound Interest @ 7%

The Advantage of Starting Early to Save

______+$85K

Save Age 18 to 65$60/wk ($2880/yr)$1,000,000 !!!!!

If you “wait until later” you will NEVER catch up

Saving & Investing

Saving IS Important !

Investing IS Important!

While they are “related” -

They are Quite Different

Saving is for meeting your Short Term goalsEmergency Fund, Major Purchases

Investing is for meeting your Long Term goalsNet Worth for retirement years

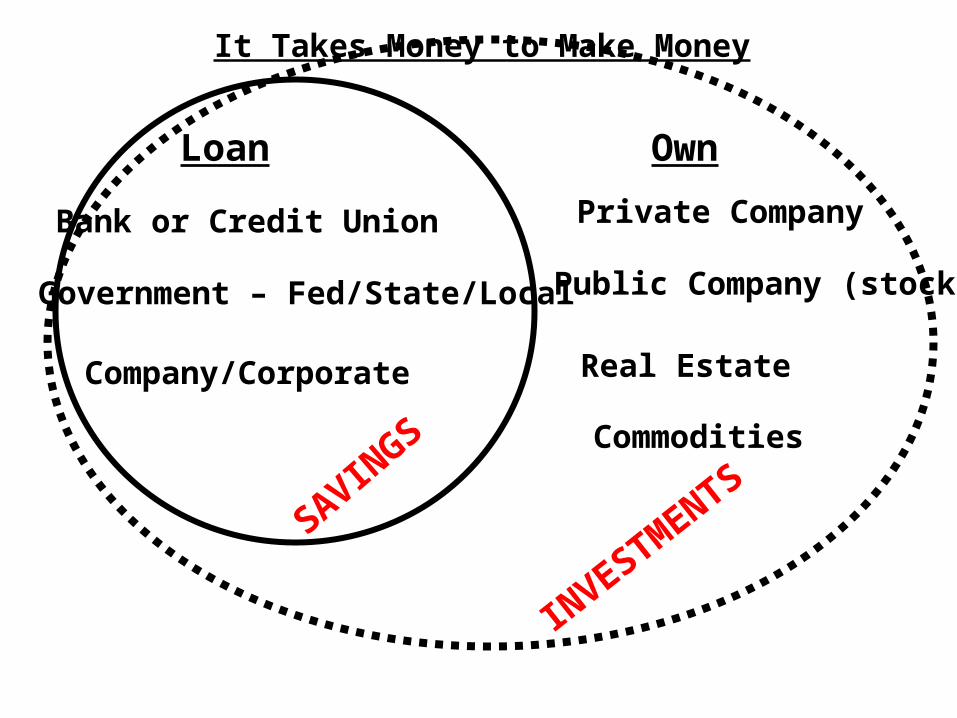

It Takes Money to Make Money

Loan Own

Bank or Credit Union

Government – Fed/State/Local

Company/Corporate

Private Company

Public Company (stock)

Real Estate

Commodities

SAVINGS

INVESTM

ENTS

FinancialPlanningPyramid

PennyStock

Commo- dities

CollectiblesSpeculative Stock / Bonds /Mutual Funds

RealEstate

Blue-ChipCommonStock

GrowthMutual Funds

High-GradeConvertible

Bonds

High-GradePreferred

Stock

BalancedMutual Funds

High-GradeCorporate Bondsor Mutual Funds

High-GradeMunicipal Bondsor Mutual Funds

Money MarketAccounts

or Mutual Funds

Certificatesof Deposit

U.S. SavingsBonds

Insured Savings / Checking Accounts

TreasuryIssues

Highest RiskHighest RiskHighest EarningsHighest Earnings

Lower Lower RiskRisk

Lower Lower EarningsEarnings

NEFE High School Financial Planning ProgramNEFE High School Financial Planning ProgramUnit Three – Investing: Making Money Work for YouUnit Three – Investing: Making Money Work for You

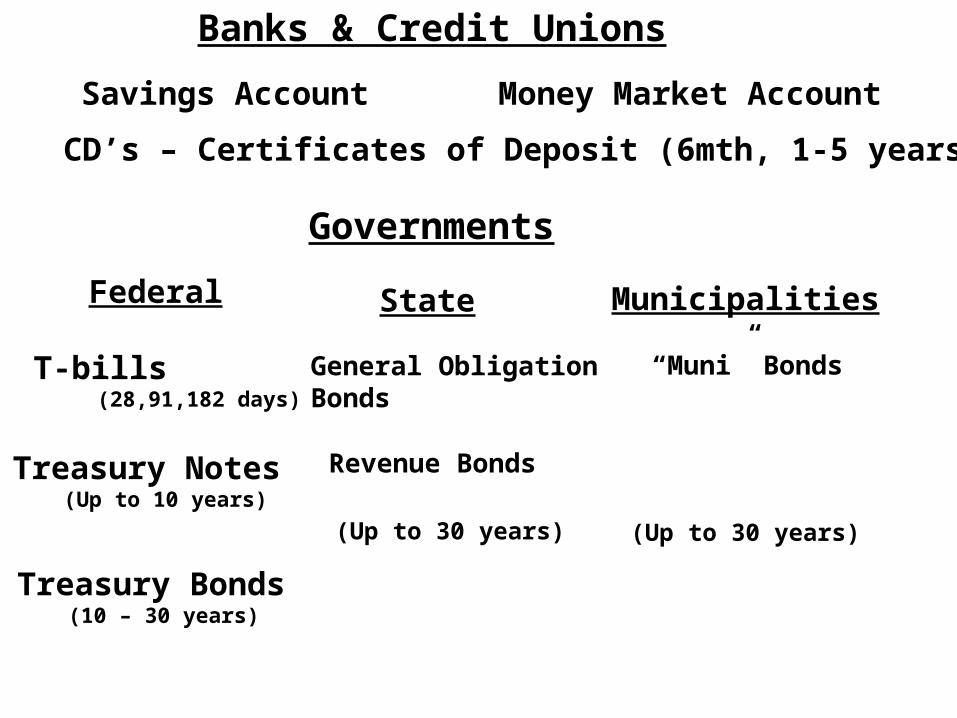

Banks & Credit Unions

Savings Account Money Market Account

CD’s – Certificates of Deposit (6mth, 1-5 years)

Governments

Federal

T-bills (28,91,182 days)

Treasury Notes (Up to 10 years)

Treasury Bonds (10 – 30 years)

State

General ObligationBonds

Revenue Bonds

(Up to 30 years)

Municipalities

“Muni” Bonds

(Up to 30 years)

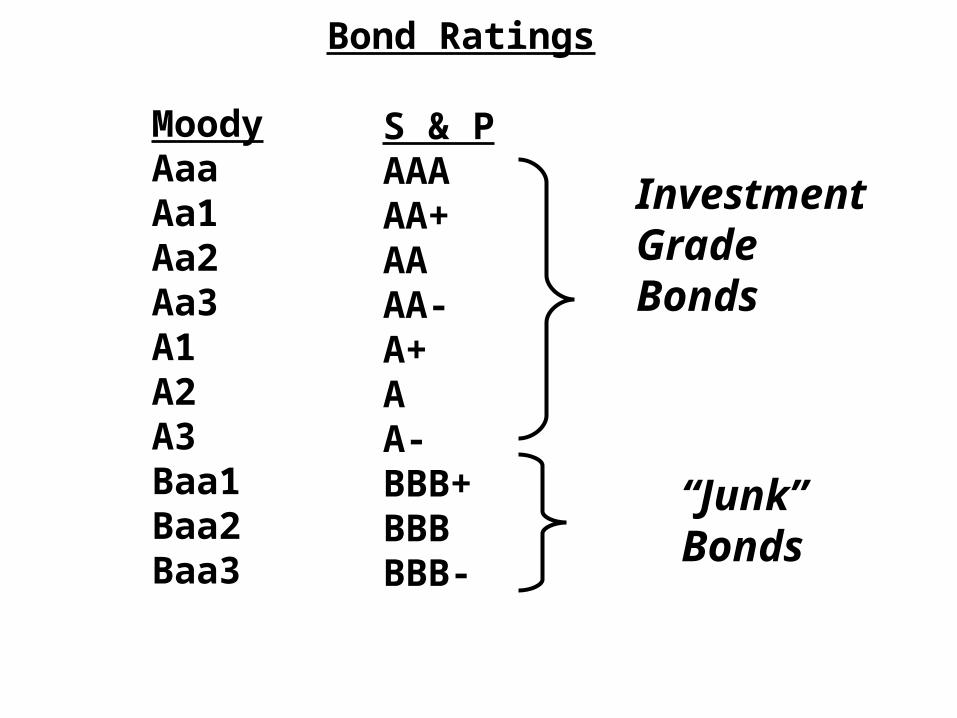

Bond Ratings

MoodyAaaAa1Aa2Aa3A1A2A3Baa1Baa2Baa3

S & PAAAAA+AAAA-A+AA-BBB+BBBBBB-

InvestmentGrade Bonds

“Junk”Bonds

Public Company

President/CEO (Management)

Board of Directors (Owners)

Sales/Revenue - Less CostsOperating Profit - Less Interest - Less TaxesNet Income

RetainedEarnings

DividendsPay OffDebt

Corporate Bonds (Debt)

Rei

nves

t in

the

Bus

ines

s

LoanInterest on the Bonds

OwnStock DividendsStock Price Appreciation

Stock HoldersElect BoardMembers

Stock Certificate Example

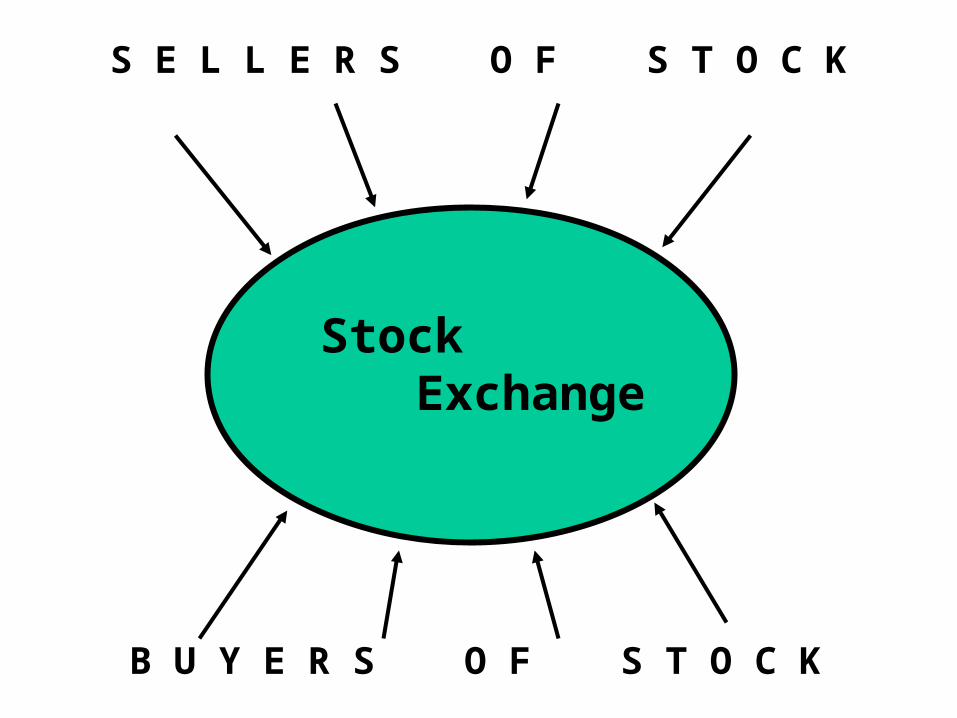

StockExchange

S E L L E R S O F S T O C K

B U Y E R S O F S T O C K

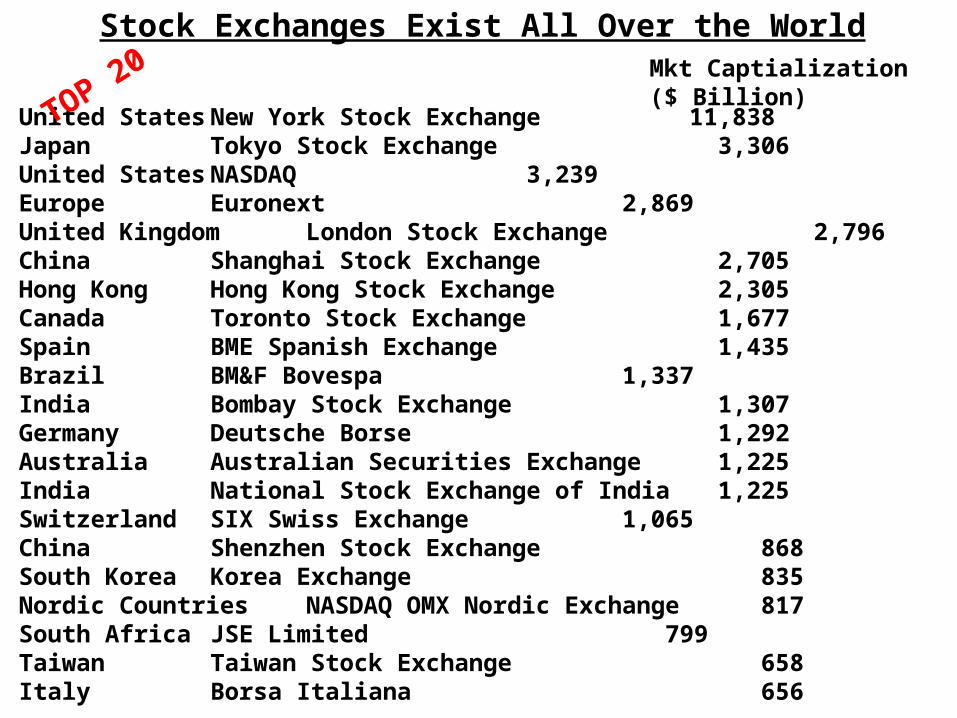

United States New York Stock Exchange 11,838Japan Tokyo Stock Exchange 3,306United States NASDAQ 3,239Europe Euronext 2,869United Kingdom London Stock Exchange 2,796China Shanghai Stock Exchange 2,705Hong Kong Hong Kong Stock Exchange 2,305Canada Toronto Stock Exchange 1,677Spain BME Spanish Exchange 1,435Brazil BM&F Bovespa 1,337India Bombay Stock Exchange 1,307Germany Deutsche Borse 1,292Australia Australian Securities Exchange 1,225India National Stock Exchange of India 1,225Switzerland SIX Swiss Exchange 1,065China Shenzhen Stock Exchange 868South Korea Korea Exchange 835Nordic Countries NASDAQ OMX Nordic Exchange 817South Africa JSE Limited 799Taiwan Taiwan Stock Exchange 658Italy Borsa Italiana 656

Stock Exchanges Exist All Over the WorldMkt Captialization($ Billion)TOP 20

-60

-40

-20

0

20

40

60

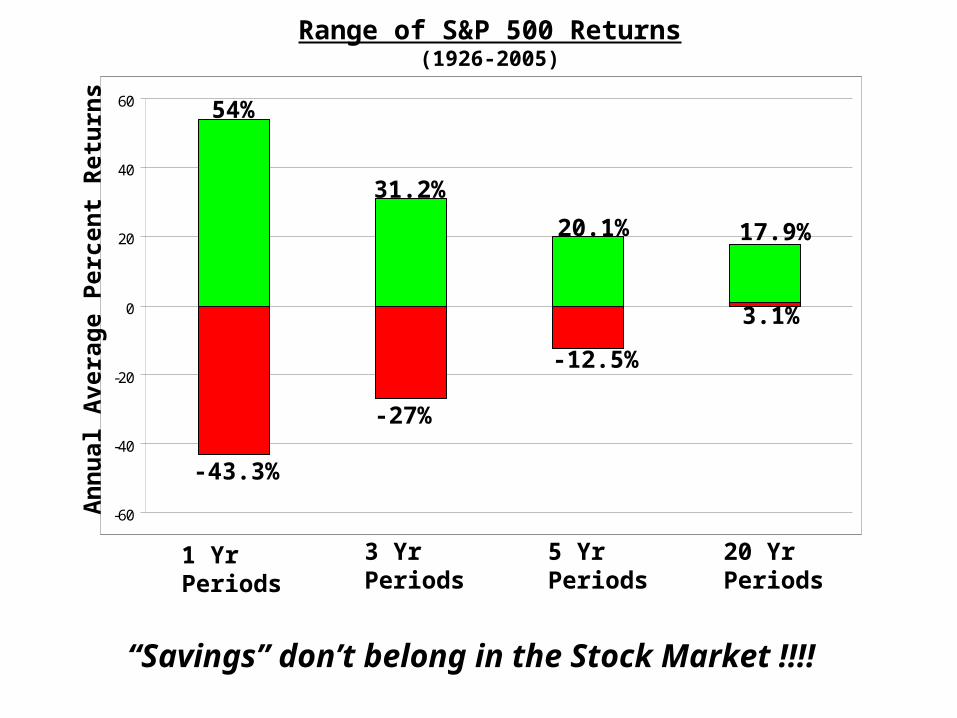

Range of S&P 500 Returns(1926-2005)

1 YrPeriods

3 YrPeriods

5 YrPeriods

20 YrPeriods

54%

-43.3%

31.2%

-27%

20.1%

-12.5%

17.9%

3.1%

An

nual

Ave

rage

Per

cent

Ret

urn

s

“Savings” don’t belong in the Stock Market !!!!

-8

-6

-4

-2

0

2

4

6

8

10

1 2 3 4 5

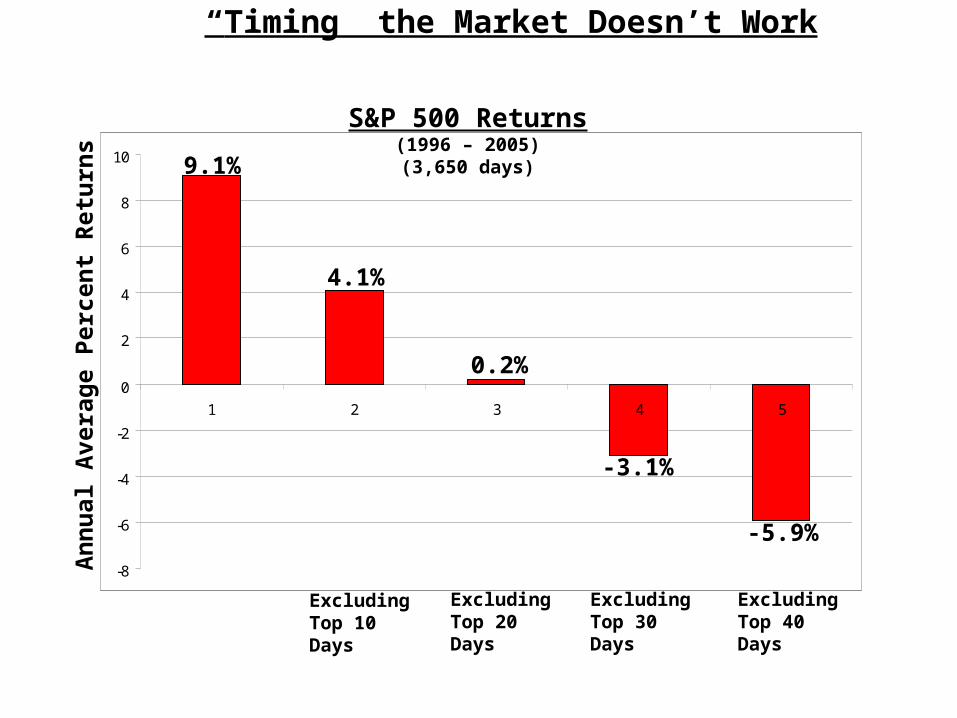

S&P 500 Returns(1996 – 2005)(3,650 days)9.1%

4.1%

0.2%

-3.1%

-5.9%

An

nual

Ave

rage

Per

cent

Ret

urn

s

ExcludingTop 10Days

ExcludingTop 20Days

ExcludingTop 30Days

ExcludingTop 40Days

“Timing” the Market Doesn’t Work

Mutual Fund

Diversification – Stocks & Bonds

Mutual Funds

Spreads Your Risk Any ONE Stock/Bond can Fail or Default Personally managing large numbers of investments gets “messy”

Convenient/Affordable Way to Hold a Large Portfolio of Investments Can Have Hundreds of Positions in a Portfolio Minimum Investment can be Quite Low (e.g. $1,000)

You Can Find a Fund for Every Investment Interest Over 6000 Funds Exist Today Their Operating Rules are Covered in the Prospectus

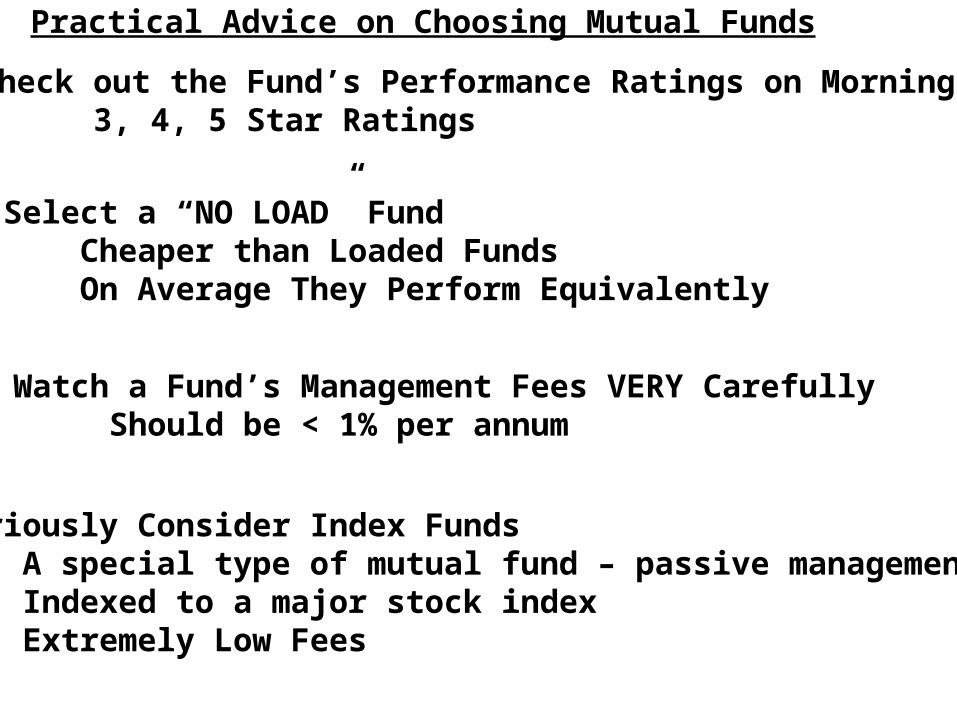

Practical Advice on Choosing Mutual Funds

Check out the Fund’s Performance Ratings on Morningstar 3, 4, 5 Star Ratings

Select a “NO LOAD” Fund Cheaper than Loaded Funds On Average They Perform Equivalently

Watch a Fund’s Management Fees VERY Carefully Should be < 1% per annum

Seriously Consider Index Funds A special type of mutual fund – passive management Indexed to a major stock index Extremely Low Fees

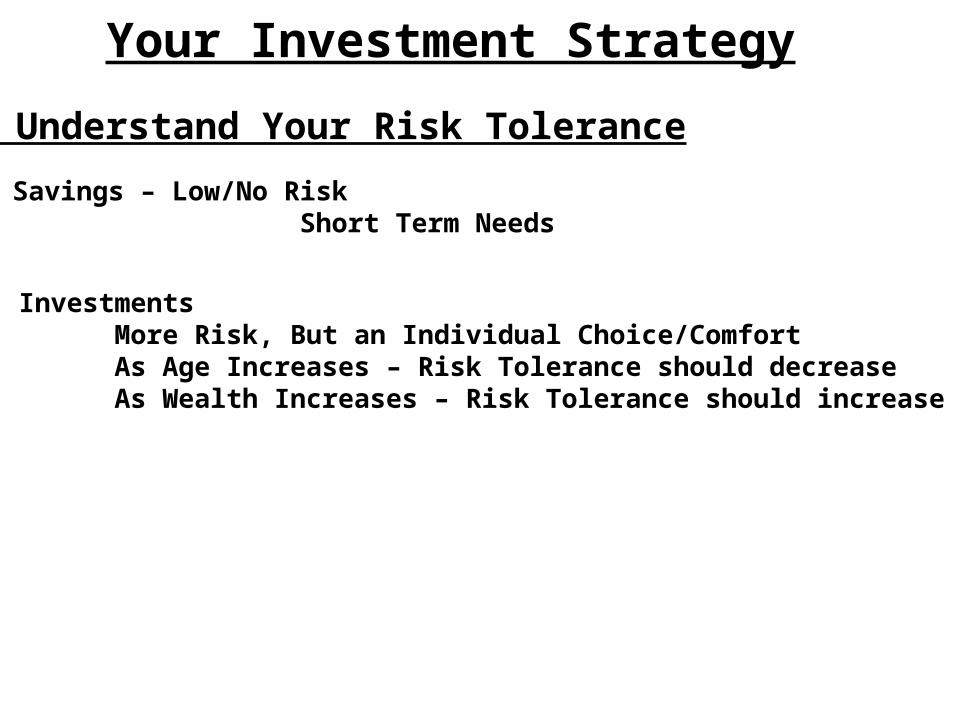

1. Understand Your Risk Tolerance

Savings – Low/No Risk Short Term Needs

Investments More Risk, But an Individual Choice/ComfortAs Age Increases – Risk Tolerance should decreaseAs Wealth Increases – Risk Tolerance should increase

Your Investment Strategy

Bonds

S.T. Investments

Dom. Stocks

Foreign Stocks

50%

30%

14%6%

Conservative

40%

10%

35%

15%

Balanced

25%

5%

49%

21%

Growth

15% 0%

60%25%

Aggressive

Annual Returns (1926-2008)

Average

Best 12 Months

Worst 12 Months

Best 5 Years

Worst 5 Years

6.06%

31.06%

(17.67%)

16.79%

(0.37%)

7.85%

76.57%

(40.64%)

22.06%

(6.18%)

8.73%

109.55%

(52.92%)

27.23%

(10.43%)

9.31%

136.07%

(60.78%)

31.91%

(13.78%)

2. Select Asset Allocation That Matches Your Risk Target

3. Choose Individual Investments

Consider Mutual Funds or Index Funds – Diversification

Check out performance with 3rd Parties – e.g. Morningstar

Remember: “No Loads” perform as well as “Load” funds

Wherever possible, Index Funds are you least expensive choice

4. Track and Readjust as needed

Keep your asset allocations proportioned correctly

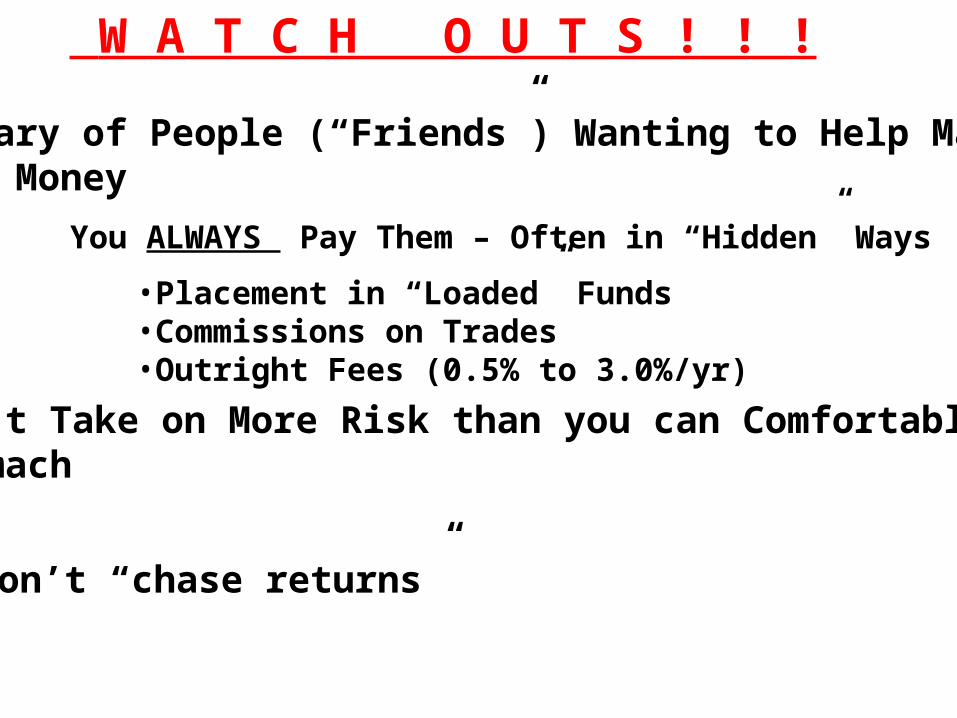

W A T C H O U T S ! ! !

Be Wary of People (“Friends”) Wanting to Help ManageYour Money

You ALWAYS Pay Them – Often in “Hidden” Ways

•Placement in “Loaded” Funds•Commissions on Trades•Outright Fees (0.5% to 3.0%/yr)

Don’t Take on More Risk than you can ComfortablyStomach

Don’t “chase returns”

Special “Deals” You Should Never Pass Up(Tax Sheltered Investments)

401K’s, 403b’s, Self Directed IRA’sMoney Goes IN BEFORE TaxesPossible “Company Match”Money Compounds without Taxes!Money OUT is Taxed as IncomeStart Withdrawls Age 59.5 to 70.5

Roth IRA’sMoney Goes IN AFTER TaxesMoney Compounds without Taxes!Money OUT is Tax FREE !!!!!!!!!Start Withdrawls Age 59.5No Mandatory Withdrawls – can be passed to next generation

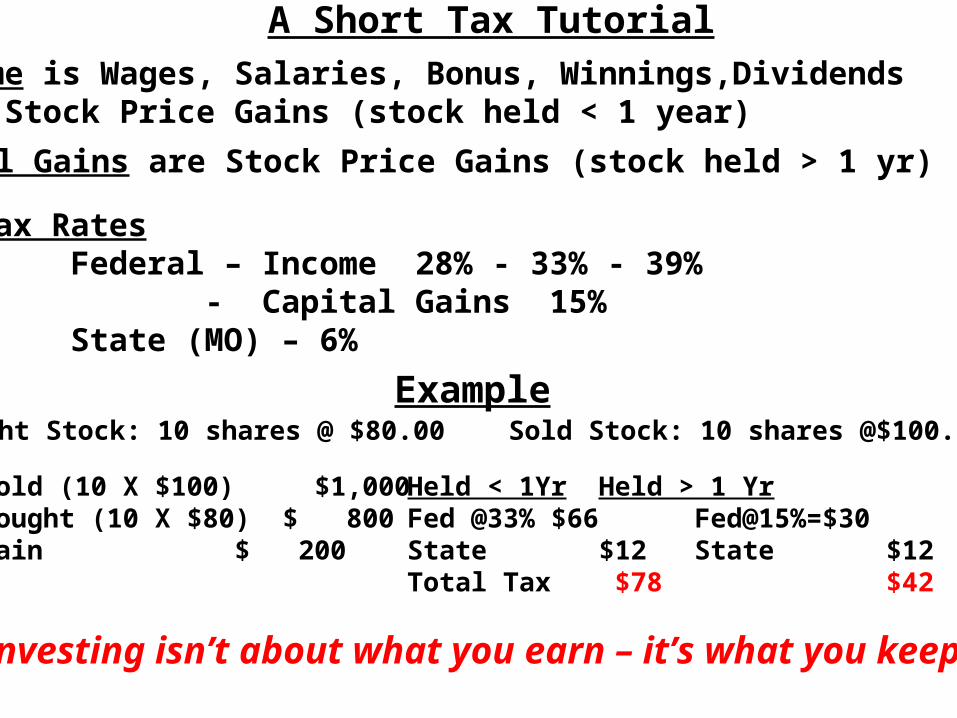

A Short Tax Tutorial

Tax RatesFederal – Income 28% - 33% - 39%

- Capital Gains 15%State (MO) – 6%

Income is Wages, Salaries, Bonus, Winnings,Dividends & Stock Price Gains (stock held < 1 year)

Capital Gains are Stock Price Gains (stock held > 1 yr)

ExampleBought Stock: 10 shares @ $80.00 Sold Stock: 10 shares @$100.00

Sold (10 X $100) $1,000Bought (10 X $80) $ 800Gain $ 200

Held < 1Yr Held > 1 YrFed @33% $66 Fed@15%=$30State $12 State $12Total Tax $78 $42

Investing isn’t about what you earn – it’s what you keep!

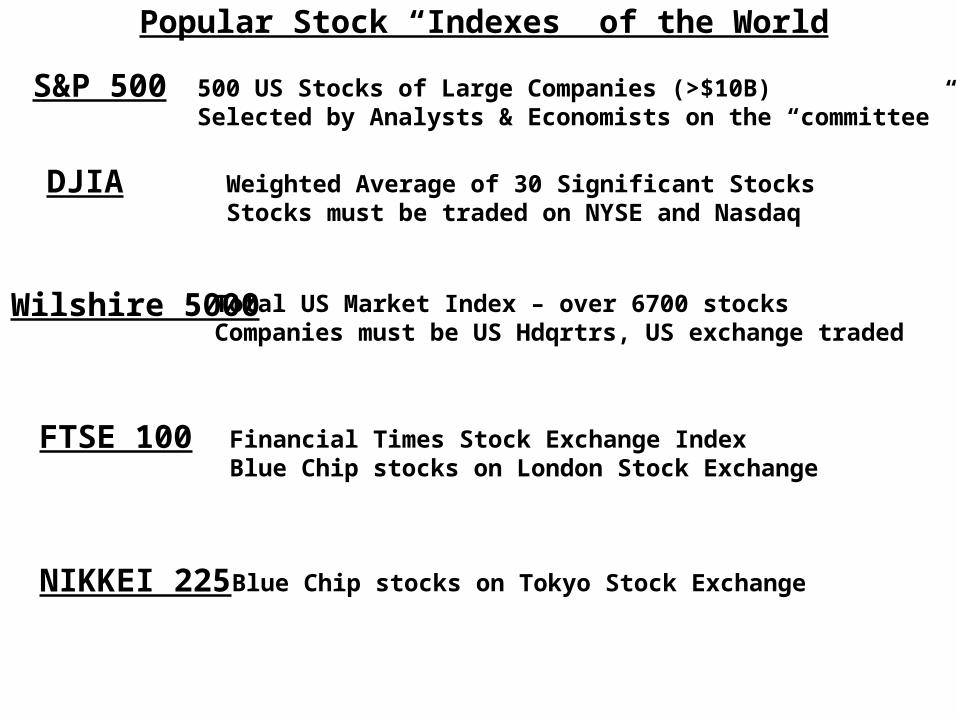

Popular Stock “Indexes” of the World

S&P 500 500 US Stocks of Large Companies (>$10B)Selected by Analysts & Economists on the “committee”

DJIA Weighted Average of 30 Significant StocksStocks must be traded on NYSE and Nasdaq

Wilshire 5000 Total US Market Index – over 6700 stocksCompanies must be US Hdqrtrs, US exchange traded

FTSE 100 Financial Times Stock Exchange IndexBlue Chip stocks on London Stock Exchange

NIKKEI 225 Blue Chip stocks on Tokyo Stock Exchange