Proceedings of the Fifth Asia-Pacific Conference on Global Business, Economics, Finance

and Social Sciences (AP16Mauritius Conference) ISBN - 978-1-943579-38-9

Ebene-Mauritius, 21-23 January, 2016. Paper ID: M627

1 www.globalbizresearch.org

Triple Bottom Line Reporting and Auditing in Mauritius-

Perspectives of Academics and Professionals in

Financial Services and Tourism Sector

Ramen. M,

Department of Accounting and Finance,

Faculty of Law and Management,

University of Mauritius, Mauritius.

E-mail: [email protected]

Seechurn. M,

Department of Accounting and Finance,

Faculty of Law and Management,

University of Mauritius, Mauritius.

Jugurnath. B,

Department of Accounting and Finance,

Faculty of Law and Management,

University of Mauritius, Mauritius.

___________________________________________________________________________

Abstract This paper heuristically addresses the three aspects of TBL reporting and auditing and

scrutinizes the possible introduction of TBL reporting and auditing in financial services and

tourism sector. Questionnaires were designed and sent to a targeted sample to collect data on

this subject matter; a sample of professionals and academics was used to elicit their

perspectives, thereby distinction between non practitioners and practitioners was made.

Analysis is principally based on the evaluation of identified drivers, barriers, potential

benefits and recommendations for the implementation of TBL reporting and auditing.

However, this research calls for further empirical research into other sectors with a wider

sample size. It is worth mentioning that this paper is highly original as it is the first study

providing insights of TBL in Mauritius.

___________________________________________________________________________

Keywords: Triple Bottom Line (TBL) Reporting and Auditing, academics, professionals,

drivers, barriers, benefits, sustainability, transparency, Social/Environmental/Financial

Reporting and auditing

Proceedings of the Fifth Asia-Pacific Conference on Global Business, Economics, Finance

and Social Sciences (AP16Mauritius Conference) ISBN - 978-1-943579-38-9

Ebene-Mauritius, 21-23 January, 2016. Paper ID: M627

2 www.globalbizresearch.org

1. Introduction

In 21st century business era, it would not be wise to evaluate the health performance of an

organization through financial reporting solely. Nowadays, stakeholders are claiming for non-

financial information along with financial information for better accountability and

transparency of business activities (Samyet al., 2009). Hence, the phenomenon concept of

Triple Bottom Line (TBL) reporting and auditing somehow bridges the gap between

stakeholders’ demands and corporate activities. Moreover, as first coined by John Elkington

in the late 1990’ Triple Bottom Line Accounting is a viable approach to measurement of

sustainability.

Figure 1: The 3 aspects of Tripple Bottom Line SVN, Balle, B Corporation, elephant journal, 2013.

[Online] available at http://www.elephantjournal.com/2008/11/triple-bottom-line-business-networks-

svn-balle-b-corporation/ [Accessed 8 April 2013]

The third millennium observes a growing adoption of TBL reporting and auditing by

companies, yet it is still in its infancy. This interest has been triggered by a number of factors

namely environmental concerns such as Global Warming, Ozone Depletion, Climate Change,

Deforestation, among others; Social concerns like Corporate Social Responsibility, Health

and safety, Employment of people with disabilities, benefits to employees (health insurance,

special loans for children studies, housing), among others; And Economic scandals including

Enron, WorldCom, Barings Bank, Tyco International.

In Mauritius companies have recently laid emphasis on TBL activities due to

stakeholders’ concerns, who seeks for transparency and sustainability mainly. Scandals such

as White dot, Medpoint, CT Power have triggered the need for TBL. Moreover, corporate

firms are increasingly engaging in social activities being blood donations, HIV/AIDS, drug,

diabetes awareness campaigns and educational sponsorships programs for needy students

(ProjetSourire by IBL). Government of Mauritius also contributed to the conceptualisation of

TBL by making mandatory CSR and promoting the project of ‘Maurice Ile Durable’. In

addition, National Economic and Social Council (NESC) and Federation of disable people

have recently launched programs to educate and guide employers to employ and care for

disable people.

Proceedings of the Fifth Asia-Pacific Conference on Global Business, Economics, Finance

and Social Sciences (AP16Mauritius Conference) ISBN - 978-1-943579-38-9

Ebene-Mauritius, 21-23 January, 2016. Paper ID: M627

3 www.globalbizresearch.org

2. Literature Review

2.1 Triple Bottom Line Reporting and Auditing

2.1.1 Definition of TBL Reporting

Sumanta Dutta SSRN, (2011) pointed out that TBL Reporting reflects a more

comprehensive mechanism that integrates the traditional financial information along with

non-financial information, which can help firm in enhancing economic value addition, besides

putting it on a firm financial footing

2.1.2 The Need for TBL Reporting

TBL reporting is closely associated with disclosure transparency which is related to

strong corporate governance (Beekes and Brown, 2006). G100 guide TBL reporting (2003)

states that companies protect and enhance their reputation by communicating three spheres

being environmental, social and economic. In addition, according to Baret&Lougee (2006)

and Wallace (2008), sustainability as a strategy seeks long-term improvements in corporate

competitiveness.

According to Simnettet al. (2009) TBL may be conducted when their benefits exceed

their costs. Firstly, TBL information may position employees as an ‘employer of choice,’

whereby employee loyalty, reduction in staff turnover and retention of shall be attained.

Secondly, enhance attractiveness of investment on the market as investors are increasingly

considering TBL aspects in their investment decisions. Thirdly, organizations succeed in

obtaining a differentiated position in the market place as a preferred supplier through TBL

reporting.

2.1.3 Initiatives for TBL Reporting

Several initiatives have been declared such as South Africa’s King report in 2002

suggesting that every South African company report annually on its social, transformation,

ethical, safety, health and environment policies and practices. MP Linda Perham’s (UK June

2002) seeks to establish a new regulatory body for corporate, social and environmental

standards (Hayward, 2002). Moreover, International Integrated Reporting Committee (IIRC)

pictures a concise, clear, consistent and comparable integrated reporting Framework

reflecting the reporting of financial and non-financial information (Brand, 2010)

2.1.4 Definition of TBL Auditing

In its broad sense, TBL auditing is just an in-depth assessment and measurement of how

to report on the financial, social and environmental aspects of an organization was carried out

to determine the firm sustainability and viability (Business Dictionary).

2.1.5 The Need for TBL Auditing

According to the study by Basri and McAvoy(2000)TBL Audit promotes transparency

of companies, whereby auditors shall give reasonable assurance that reporting on economic,

social and environment has been conducted fairly and truly evaluated for decision-making.

Proceedings of the Fifth Asia-Pacific Conference on Global Business, Economics, Finance

and Social Sciences (AP16Mauritius Conference) ISBN - 978-1-943579-38-9

Ebene-Mauritius, 21-23 January, 2016. Paper ID: M627

4 www.globalbizresearch.org

2.2 Environmental Reporting and Auditing

2.2.1 Definition of Environmental Reporting and Auditing

As per Edu et al. (2009) “environmental information is used to disclose the impact of

corporate activities on the natural environment to stakeholders of the corporate entity or

organization.” Environmental Auditing is regarded as the independent, objective, strategic

and systematic audit(ICC, 1991)to identify problems, improve compliance, improve corporate

image and give reasonable assurance on credibility and reliability of environmental reported

information(Simnett et al.,2009; Darnall et al., 2009).

2.2.2 Drivers for environment reporting and auditing

Legitimacy Theory

Today a legitimate organization is one which is in conformity with social norms, values

and expectations. Organizations legitimacy increases when their adaptations result in

homogeneity with other organizations in its environment (Baker and Rennie, 2006).

Institutional Isomorphism: Normative, Coercive and Mimetic Forces

Normative forces relate to what techniques should be used to make companies more eco-

friendly in their activities. Coercive forces refer direct pressures exercised by Legislation and

Regulations while indirect forces occur from a change in community concern, adverse media

publicity “fear Factor”.

Good Corporate Governance

As stated part 5 of section 7 Integrated Sustainability Reporting of Corporate Governance

Report (2003), “Every Company should regularly report to its stakeholders on its policies

and practices as regards to ethics, environment, health and safety and social issues.”

Stakeholders’ Pressures

Environmental crises have raised public and stakeholder awareness of the impact that

corporate activity can have on the environment and the need for appropriate disclosure on

such matters (Dillard et al., 2005)

Comply with Standards

Regarding Environmental Reporting Standards IAS 1 Presentation of financial statements

requires the recognition of environment assets, environment liabilities and environmental

expenses.ISA 32, 39, IFRS 7 and IFRS 9 on financial instruments deal with present and future

risks of hedge accounting, the measurement of environmental derivatives and the treatment of

other financial elements that occur as a result of environmental impacts (Barbuet al., 2011).

On the other hand, for environmental auditing, businesses may adopt the ISO

14001(appendix2). IAS 37 (IASB, 2005) requires companies to recognize and measure

contingent liabilities which may have a legal obligation or a constructive obligation

depending on company’s policy. In addition, IAS 8 (IASB, 2003) requires disclosure in

accounting policies, changes and estimates and errors. Similarly, ISA720 (IFAC, 2012)

Proceedings of the Fifth Asia-Pacific Conference on Global Business, Economics, Finance

and Social Sciences (AP16Mauritius Conference) ISBN - 978-1-943579-38-9

Ebene-Mauritius, 21-23 January, 2016. Paper ID: M627

5 www.globalbizresearch.org

imposes a limited duty on auditors to read and understand disclosures made anywhere in

financial statements. Hence, auditors need to verify the “truth and fairness” of environmental

disclosures in financial statements.

2.2.3 Barriers to Environmental Reporting and Auditing.

Professional Competence: Reliance on Experts/Management Advisors

A lack of expertise and competence represent a serious challenge to the accounting

profession’s ability. KPMG (2005) argue that the measurement of social and environmental

performance is rather a complex task, thus Accountants and auditors use professional

judgement. They may seek advice of an expert or rely on management with respect to the

recognition and measurement of the consequences of environmental matters in the financial

report (ICANZ, 2001). However, by doing so, the auditor’s independence maybe

compromised. Familiarity threat may also be an issue as the auditor shall be working closely

with client management on evaluating environmental issues.

Consistency & Comparability

The relative absence of environmental reporting standards has contributed to the

generation of reports that are not consistent across organizations. This has affected the

comparability and verifiability of environmental reports among organizations (Wallace,

2000). In this context, users of accounts are unable to use information in decision making.

Lack of Regulators

Environmental reporting is basically a voluntary disclosure (Shivaji and Subramaniam,

2008) as it does not materially impact the financial statements.

2.3 Social Reporting and Auditing

2.3.1 Definition of Social Reporting?

Social reporting is a mechanism facilitating transparency, empowering stakeholders to

hold organizations accountable for all related social matters. This form of transparency grants

stakeholders negotiating power and allows true collaborate governance to develop around

particular firms and issues (Hess, 2007).It encompasses both internal and external social

reporting.

Internal Social Reporting

Companies need to ensure that their employees are working in a safe and secured

environment. In Mauritius, the Occupational Health and Safety Act 2005 makes provisions

for hazard free work environments. Being a statutory regulation, companies are bound to

appoint an Occupational Health and Safety (OHS) officer to carry out assessment and

reporting on health and safety conditions prevailing in the organization under certain

condition. Moreover, according to the Training and Employment of Disabled Persons Act

1996companies should employ 3% staff with disabilities thus engaging in diversification of

staffs.

Proceedings of the Fifth Asia-Pacific Conference on Global Business, Economics, Finance

and Social Sciences (AP16Mauritius Conference) ISBN - 978-1-943579-38-9

Ebene-Mauritius, 21-23 January, 2016. Paper ID: M627

6 www.globalbizresearch.org

External Social Reporting

Many authors defined CSR in different ways, yet all heed towards the notion that

businesses are expected to discharge duty towards the society. According to Finance Act 2009

in Mauritius CSR contribution is a legal requirement. As from January 2012 companies

should contribute 2% of their chargeable income for tax purposes.

2.3.2 Definition of Social Auditing?

Social auditing involves the understanding, verifying, measuring, and monitoring of social

programs or services being carried out by companies (Anupekkonenand Sadashiva,2010).

Moreover, a social audit helps to narrow the gaps between vision and reality, between

efficiency and effectiveness (PARTAS, 2010).

2.3.3 Drivers of Social Reporting and Auditing

Legitimacy Theory

Legitimacy theory points out that companies engage in CSR reporting in order to be

accepted by society and maintain existence and “license to operate” as a legitimate entity.

Grayet al. (1995).

Institutional Isomorphism: Normative, Coercive and Mimetic Forces

Normative Force: Social reporting is becoming a norm. Stakeholders like local

communities, the public in general and social activists seek sponsorships in programs being

undertaken. Programs such as “AnouBouzé” are platforms which invite companies to

contribute to social activities.

Coercive Force: Direct pressures exercised by law such as mandatory CSR contribution,

health and safety assessment reports. Indirect pressures are exerted by media attention.

Consequences of negative media attention brings along bad image of company, loss of

goodwill and stakeholders’ loss, while positive media attention shall improve companies

image and act as an indirect way of advertising for the company(KPMG, 2004).

Mimetic Forces: Since 2007 Rogers Ltd has been contributing massively in the fight of HIV/

AIDS and today other companies are following the same trend like SBM which regularly

engages in Blood donation programs throughout the island.

Stakeholder Activism

Stakeholders may seek social reporting and auditing for decision-making and assessment

of human factor in a business. Moreover, social auditing values the voice of stakeholders

including marginalized/ poor groups whose voices are rarely heard (PARTAS, 2010).

International Guidance

Recently, the institute for social and ethical Accountability proposed AA1000s standards

for social auditing (Accountability, 2002) which describe that social accounting and auditing

should be multi-perspective, comprehensive, comparative, regular, verified and disclosed.

Proceedings of the Fifth Asia-Pacific Conference on Global Business, Economics, Finance

and Social Sciences (AP16Mauritius Conference) ISBN - 978-1-943579-38-9

Ebene-Mauritius, 21-23 January, 2016. Paper ID: M627

7 www.globalbizresearch.org

Besides, ISO 26000 (2010) has been put in place to provide guidance to companies on how to

operate in a socially responsible manner. It assists companies in translating principles into

effective actions and shares social best practices globally. The GRI is probably the most

successful attempt to date, at standardising the reporting of social and environmental

information globally (Adams and Frost, 2007). Where firms are investing massively in any

program dealing either with internal or external reporting, it has to be reflected in accounts

under the concept of “true and fair”. Accordingly, auditors under ISA720 (IFAC, 2012) have

an obligation to consider all material matters and gather concrete evidence on the issue.

2.3.4 Barriers to Social Reporting and Auditing

Reliance on Work of an Expert/Management Advisors

The OHS officer has an obligation to report all hazards identified. The auditor is not an

expert and will have to rely on expert (OHS officer) or management (HR Personnel) for social

audit. Reliance is worthy when:

No familiarity or advocacy threats exist to ensure objective reporting on issues.

People involved in social auditing should have professional competence.

Availability of sources of information from external parties for reliability.

Requirements checklists of OHS should be structured, pertinent and proper.

2.4 Financial reporting and auditing

2.4.1 Definition of Financial Reporting

Broadly defined, Financial Reporting is the systematic recording, measuring and

presentation of financial data occurring during an accounting period. Wild, Shaw

&Chiappetta (2009) define Financial Reporting as the communication of financial

information useful for making investment, credit and other business decisions. Well-

established standards and policies are put in place to ensure that financial information are true

and fair, complete, relevant, understandable, consistent, comparable, adequate and reliable

(IASB conceptual framework, 2001).

2.4.2 The Need for Financial Reporting

Financial reporting is conducted in view to give useful information to users of accounts

about the financial position and trend in performance of companies(IASB Framework,

2001).According to Accounting Simplified (2012), IFRS Framework (2010) firstly help

management in assessing financial position of company and decision-making; Secondly,

enable shareholders in assessing risks and returns of their investment and ultimately take

investment decision; Thirdly, illustrate economic performance of firm whereby potential

investors assess the viability of investing in business. Moreover, financial statements help

financial lenders to decide whether it would be wise to provide finance to company based on

the solvency of business. Suppliers and creditors shall assess the liquidity and

Proceedings of the Fifth Asia-Pacific Conference on Global Business, Economics, Finance

and Social Sciences (AP16Mauritius Conference) ISBN - 978-1-943579-38-9

Ebene-Mauritius, 21-23 January, 2016. Paper ID: M627

8 www.globalbizresearch.org

creditworthiness of business to pay its obligation as and when it falls due. Besides, Customers

want to ensure that business will continue to provide product in the future, hence financial

statements is used to assess current and future existence of business. On the other hand,

employees shall use financial statements to assess company’s profitability and future

existence for job security, while for competitors it is a platform to compare and contrast

performance and accordingly improve competitiveness. Also, Government shall use financial

figures to determine correct tax charge and keep record of firm’s economic performance.

2.4.3 What is Financial Auditing?

In a broad sense financial auditing is the evaluation of truth and fairness of final accounts

from an independent party. The financial statement audit has never been more important. In

today's business environment there is more scrutiny and scepticism of a company's financial

statements than ever before. Investors have lost faith in corporate governance and reporting

and they expect more: greater reliability, more oversight and clear evidence of internal

controls (PWC website accessed on Dec, 2012).

2.4.4 The Need for Financial Auditing

As per ISA 200 (IFAC, 2004) objectives and general principles governing an audit of

financial statements, the primary aim of an audit is to enable the auditor to express an opinion

on whether the final accounts are prepared in all material respects, in accordance with an

identified financial reporting framework. Furthermore, according to ISA 540(IFAC,

2009)Auditing accounting estimates, including fair value accounting estimates and related

disclosures and ISA 450 (IFAC, 2009) Evaluation of misstatements identified during the

audit, auditors enhance credibility and reliability by giving reasonable assurance that those

final accounts reflect a true and fair view of business financial position. This means that the

Final accounts are free from material misstatements and that estimates and disclosures are

reasonable. For this to be achieved, auditors shall collect evidences, which should be

sufficient, appropriate, adequate and relevant during a time period (ISA 500 Audit evidence

IFAC, 2008).In addition, the auditor shall ensure the assertions of Management when

preparing the final accounts (see appendix) by conducting Observation, Inspection, External

confirmation, Recalculation, Reperformance, Analytical procedures and Inquiry. Moreover,

auditing of final accounts aims to assess going concern of business, as such ISA 570 (IFAC,

2008) states the auditor is required to consider whether there are events related to business

risks which may cast significant doubts on the entity’s ability to continue as a going concern.

Moreover, auditors have to obtain sufficient appropriate audit evidence regarding the

appropriateness of management’s use of going concern assumption in preparing financial

statements. Examples of big scandals ongoing concern are Enron, WorldCom, MF Global and

Lehman.

Proceedings of the Fifth Asia-Pacific Conference on Global Business, Economics, Finance

and Social Sciences (AP16Mauritius Conference) ISBN - 978-1-943579-38-9

Ebene-Mauritius, 21-23 January, 2016. Paper ID: M627

9 www.globalbizresearch.org

2.4.5 Auditors Opinion

ISA 700 (IFAC, 2004) requires auditors to form an opinion on financial statements,

which are of 2 types:

Unqualified opinion: Financial Statements are in compliance with generally accepted

standards and they give a true and fair view of business. However, unqualified report may

contain ‘Emphasis of Matter’ (ISA 706 IFAC, 2007) is due to doubt; uncertainties which

do not affect the reliability of the statement but are matters that the auditor believes

deserve special attention.

Qualified opinion: Where uncertainty arises due to lack of records and evidence rendering

financial statements not credible, auditors shall express a qualified opinion or a disclaimed

opinion. Moreover, auditors may react similarly in cases of disagreements such as

inappropriate accounting policies, inadequate and misleading disclosures.

3. Methodology

3.1 Research Questions A set of clear, measurable, relevant, specific, and achievable objectives have been set for

this study. These include:

To evaluate awareness of TBL Reporting and Auditing;

To measure the willingness and reluctances of academics and professionals to adopt

TBL reporting and auditing;

To assess the efficiency of current regulators and frameworks in Mauritius in

providing necessary support for such implementation;

To analyse the potential benefits of conducting TBL reporting and auditing.

3.2 Modelling Volatility

A descriptive and exploratory approach has been adopted to carry out this study. To

gather primary data, 2surveys have been carried out. Secondary data was mainly obtained

from accounting and auditing journals, websites, publications and books. 35 respondents out

of 75, from each targeted groups namely professionals and undergraduates in accounting and

auditing field was collected. Professionals included accountants, clerks, auditors and trainees,

while academics included lecturers and graduates. Academics were mainly from UOM in

accounting and auditing field, while targeted professionals were from Hotel industry,

Business Process Outsourcing and Financial Services providers, Audit firms. Time factor was

a significant limitation as the period during which questionnaires were sent was the peak

season for accountants and auditors were involved in finalization of final accounts and filling

of annual VAT return.

3.3 Data

Questionnaires were self-administered to respondents in order to gather the maximum

information required. Data was collected, coded and analysed on SPSS version 16.0. Testing

Proceedings of the Fifth Asia-Pacific Conference on Global Business, Economics, Finance

and Social Sciences (AP16Mauritius Conference) ISBN - 978-1-943579-38-9

Ebene-Mauritius, 21-23 January, 2016. Paper ID: M627

10 www.globalbizresearch.org

of data was completed through descriptive statistics, combination of charts of mode, mean,

median and standard deviation derived from frequency testing and cross-tabulation testing.

Secondly, inferential statistics was used for more complex and explicit testing.

4. Results and Discussion

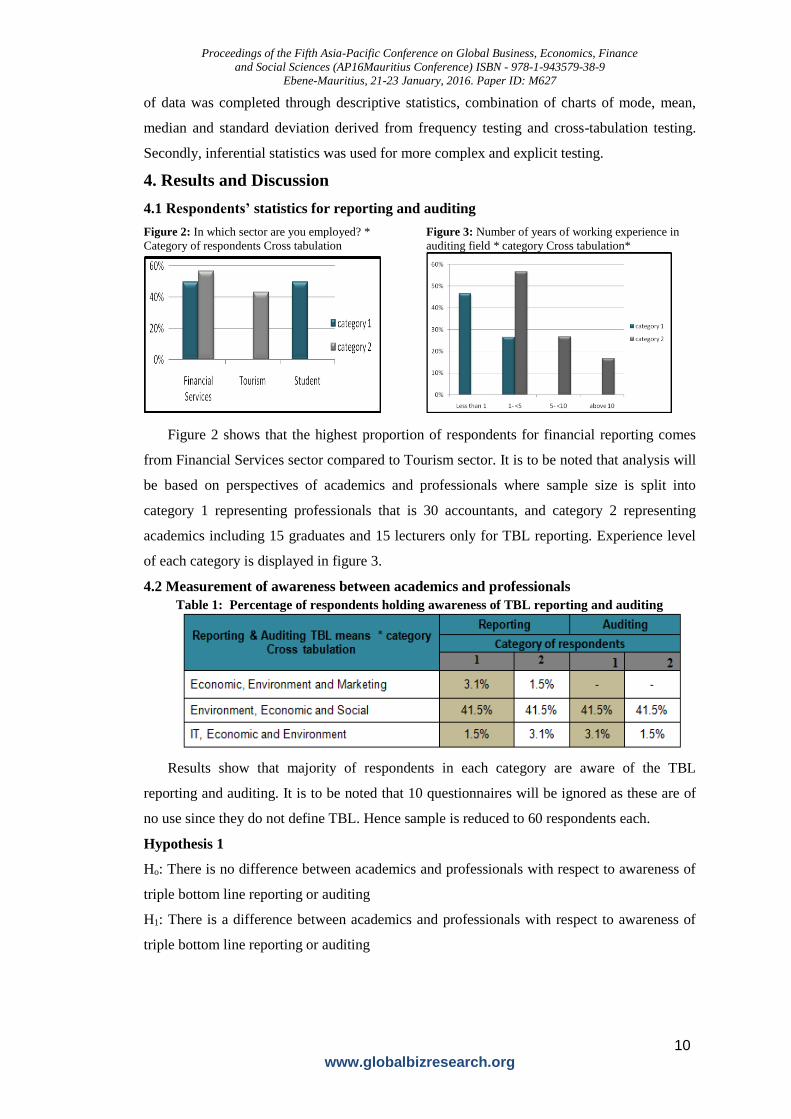

4.1 Respondents’ statistics for reporting and auditing

Figure 2: In which sector are you employed? * Figure 3: Number of years of working experience in

Category of respondents Cross tabulation auditing field * category Cross tabulation*

Figure 2 shows that the highest proportion of respondents for financial reporting comes

from Financial Services sector compared to Tourism sector. It is to be noted that analysis will

be based on perspectives of academics and professionals where sample size is split into

category 1 representing professionals that is 30 accountants, and category 2 representing

academics including 15 graduates and 15 lecturers only for TBL reporting. Experience level

of each category is displayed in figure 3.

4.2 Measurement of awareness between academics and professionals

Table 1: Percentage of respondents holding awareness of TBL reporting and auditing

Results show that majority of respondents in each category are aware of the TBL

reporting and auditing. It is to be noted that 10 questionnaires will be ignored as these are of

no use since they do not define TBL. Hence sample is reduced to 60 respondents each.

Hypothesis 1

Ho: There is no difference between academics and professionals with respect to awareness of

triple bottom line reporting or auditing

H1: There is a difference between academics and professionals with respect to awareness of

triple bottom line reporting or auditing

Proceedings of the Fifth Asia-Pacific Conference on Global Business, Economics, Finance

and Social Sciences (AP16Mauritius Conference) ISBN - 978-1-943579-38-9

Ebene-Mauritius, 21-23 January, 2016. Paper ID: M627

11 www.globalbizresearch.org

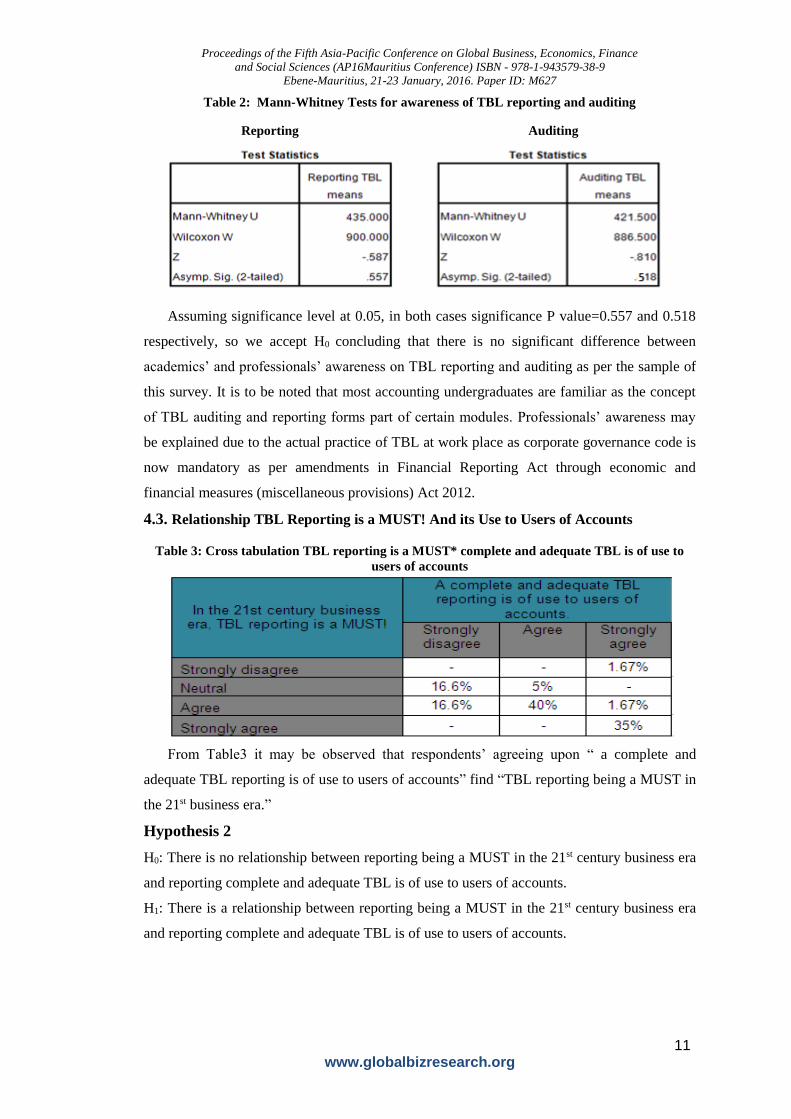

Table 2: Mann-Whitney Tests for awareness of TBL reporting and auditing

Reporting Auditing

Assuming significance level at 0.05, in both cases significance P value=0.557 and 0.518

respectively, so we accept H0 concluding that there is no significant difference between

academics’ and professionals’ awareness on TBL reporting and auditing as per the sample of

this survey. It is to be noted that most accounting undergraduates are familiar as the concept

of TBL auditing and reporting forms part of certain modules. Professionals’ awareness may

be explained due to the actual practice of TBL at work place as corporate governance code is

now mandatory as per amendments in Financial Reporting Act through economic and

financial measures (miscellaneous provisions) Act 2012.

4.3. Relationship TBL Reporting is a MUST! And its Use to Users of Accounts

Table 3: Cross tabulation TBL reporting is a MUST* complete and adequate TBL is of use to

users of accounts

From Table3 it may be observed that respondents’ agreeing upon “ a complete and

adequate TBL reporting is of use to users of accounts” find “TBL reporting being a MUST in

the 21st business era.”

Hypothesis 2

H0: There is no relationship between reporting being a MUST in the 21st century business era

and reporting complete and adequate TBL is of use to users of accounts.

H1: There is a relationship between reporting being a MUST in the 21st century business era

and reporting complete and adequate TBL is of use to users of accounts.

Proceedings of the Fifth Asia-Pacific Conference on Global Business, Economics, Finance

and Social Sciences (AP16Mauritius Conference) ISBN - 978-1-943579-38-9

Ebene-Mauritius, 21-23 January, 2016. Paper ID: M627

12 www.globalbizresearch.org

Chi-Square Tests

Value df Asymp. Sig. (2-sided)

Pearson Chi-Square 66.395a 6 .000

a. 7 cells (58.3%) have expected count less than 5. The minimum expected count is .17.

Chi Square value= 66.395 and P value = 0.000 < 0.05, therefore we accept H1it is confirmed

that there is a very strong relationship between the TBL reporting being a MUST in the 21st

century business era and reporting complete and adequate TBL is of use to users of accounts.

This may be true as to stakeholders concerns about the environment and social aspect has

increased the past decades.

4.4 Reporting and Auditing are 2sides of the same coin

Figure 4: Reporting and Auditing are the two sides of the same coin; hence TBL Reporting

should be followed by TBL Auditing. How far do you agree? * Category Cross tabulation

Figure 4 shows that considerable % of respondents in each category is neutral on the fact that

reporting and auditing are the two sides of the same coin. Respondents may be willing to

report or audit TBL yet the lack of guidance and regulators regarding this issue give rise to

reluctances.

Proceedings of the Fifth Asia-Pacific Conference on Global Business, Economics, Finance

and Social Sciences (AP16Mauritius Conference) ISBN - 978-1-943579-38-9

Ebene-Mauritius, 21-23 January, 2016. Paper ID: M627

13 www.globalbizresearch.org

4.5 Ranking of TBL Reporting Drivers Assessment

Table 5 : Percentage of respondents Ranking TBL Reporting

Drivers

Table 5 illustrates the ranking of reporting drivers of TBL by each category of

respondents. It is to be noted that Sustainability and Transparency are the two determinant

drivers which were closely rank first and second by each category respectively. Most

academics ranked transparency driver first compared to most professionals who ranked the

same driver second and third. Similarly, most academics ranked Sustainability driver second

while professionals ranked it first. Interviews with professionals pointed out that reporting

TBL demonstrates a drive towards increased transparency thus promoting sustainability.

Furthermore, it is observed that stakeholders’ activism was mostly ranked third by both

academics and professionals. This may be explained by stakeholders placing increasing

emphasis on understanding the approach of managing the three bottom lines. Storer and

Frost (2002) declared that TBL reporting responses to the increasing demands of the business

community and groups for reporting on environmental and social aspects along with

economic aspect of a firm.

In addition, it is noticed that the ranking of corporate governance is a more important driver

for academics than professionals. Statistics above show that most academics ranked this

driver first to fourth mainly. This may be illustrated by the fact that academics being well

versed with the corporate governance code as it forms part of their teaching and learning

outcomes. Besides, professionals showed relatively less importance since most ranked this

driver fifth. Henceforth, discussions with professionals have revealed that they are likely to

abide by the code for fear of litigation and good image.

Hereafter, statistics show that the driver of good image is indeed a significant driver for

TBL reporting for professionals as most of them ranked it second. This is in contrast with

academics, who ranked the same driver sixth. From such observation, it may be concluded

that TBL reporting somehow acts as advertising in disguise from a professional perspective.

Proceedings of the Fifth Asia-Pacific Conference on Global Business, Economics, Finance

and Social Sciences (AP16Mauritius Conference) ISBN - 978-1-943579-38-9

Ebene-Mauritius, 21-23 January, 2016. Paper ID: M627

14 www.globalbizresearch.org

In contrast, discussions with academics point out that they consider this driver to be more a

benefit than a driver itself. Similarly, this applies to competitive advantage driver as well,

where considerable number academics ranked that driver last.

For globalization trend driver no significant discrepancy arose between academics and

professional ranking globalization trend driver. Ranking revolve around fifth, sixth and

seventh mainly. As such, it may be concluded that this driver is less important compared to

other drivers yet respondents do uphold it as a driver for TBL reporting.

4.6 Ranking of TBL Auditing Drivers assessment

Table 4: Percentage of Respondents Ranking aach TBL Audit Drivers

Statistics illustrates that a complementary relationship is shared between ranking of

Transparency driver and Truth and Fairness driver. It is worth mentioning that a considerable

number of professionals and academics ranked the above drivers first and second mainly.

Interviews with professionals pointed out that by conducting TBL audit, auditors are able to

give reasonable assurance about truth and fairness of figures and this simultaneously

enhances transparency of firm. Similar reaction was observed upon discussions with

academics.

Furthermore, ranking of sustainability and disclosure of material matters are substantial

drivers which were equally important to professionals and academics in determining drivers

to TBL audit. Professionals and academics explain that sustainability driver helps in

determining going concern of firm which is one of main concern of stakeholders. Moreover,

investigations with auditors reveal that disclosure of material matters driver assist them in

scrutinizing any fraudulent activity in disguise under environmental or social aspect. On the

other hand, academics opine that this driver of TBL audit is likely to promote reliability and

credibility of audit reports.

Proceedings of the Fifth Asia-Pacific Conference on Global Business, Economics, Finance

and Social Sciences (AP16Mauritius Conference) ISBN - 978-1-943579-38-9

Ebene-Mauritius, 21-23 January, 2016. Paper ID: M627

15 www.globalbizresearch.org

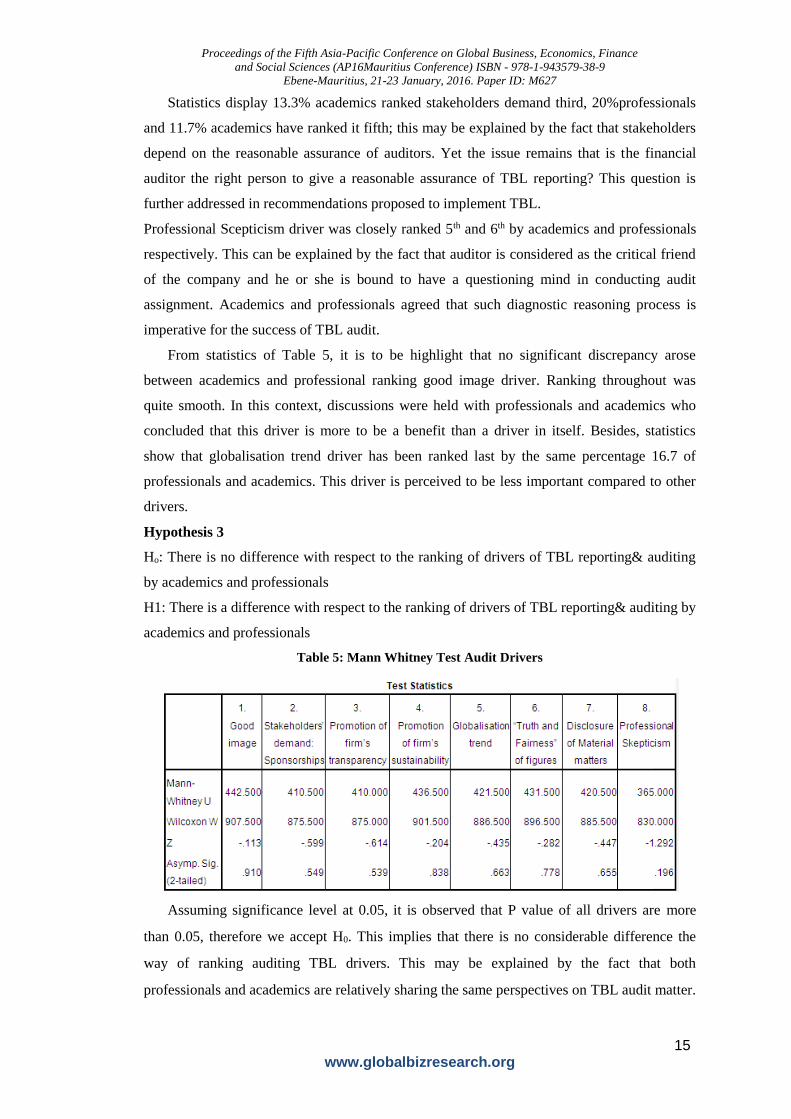

Statistics display 13.3% academics ranked stakeholders demand third, 20%professionals

and 11.7% academics have ranked it fifth; this may be explained by the fact that stakeholders

depend on the reasonable assurance of auditors. Yet the issue remains that is the financial

auditor the right person to give a reasonable assurance of TBL reporting? This question is

further addressed in recommendations proposed to implement TBL.

Professional Scepticism driver was closely ranked 5th and 6th by academics and professionals

respectively. This can be explained by the fact that auditor is considered as the critical friend

of the company and he or she is bound to have a questioning mind in conducting audit

assignment. Academics and professionals agreed that such diagnostic reasoning process is

imperative for the success of TBL audit.

From statistics of Table 5, it is to be highlight that no significant discrepancy arose

between academics and professional ranking good image driver. Ranking throughout was

quite smooth. In this context, discussions were held with professionals and academics who

concluded that this driver is more to be a benefit than a driver in itself. Besides, statistics

show that globalisation trend driver has been ranked last by the same percentage 16.7 of

professionals and academics. This driver is perceived to be less important compared to other

drivers.

Hypothesis 3

Ho: There is no difference with respect to the ranking of drivers of TBL reporting& auditing

by academics and professionals

H1: There is a difference with respect to the ranking of drivers of TBL reporting& auditing by

academics and professionals

Table 5: Mann Whitney Test Audit Drivers

Assuming significance level at 0.05, it is observed that P value of all drivers are more

than 0.05, therefore we accept H0. This implies that there is no considerable difference the

way of ranking auditing TBL drivers. This may be explained by the fact that both

professionals and academics are relatively sharing the same perspectives on TBL audit matter.

Proceedings of the Fifth Asia-Pacific Conference on Global Business, Economics, Finance

and Social Sciences (AP16Mauritius Conference) ISBN - 978-1-943579-38-9

Ebene-Mauritius, 21-23 January, 2016. Paper ID: M627

16 www.globalbizresearch.org

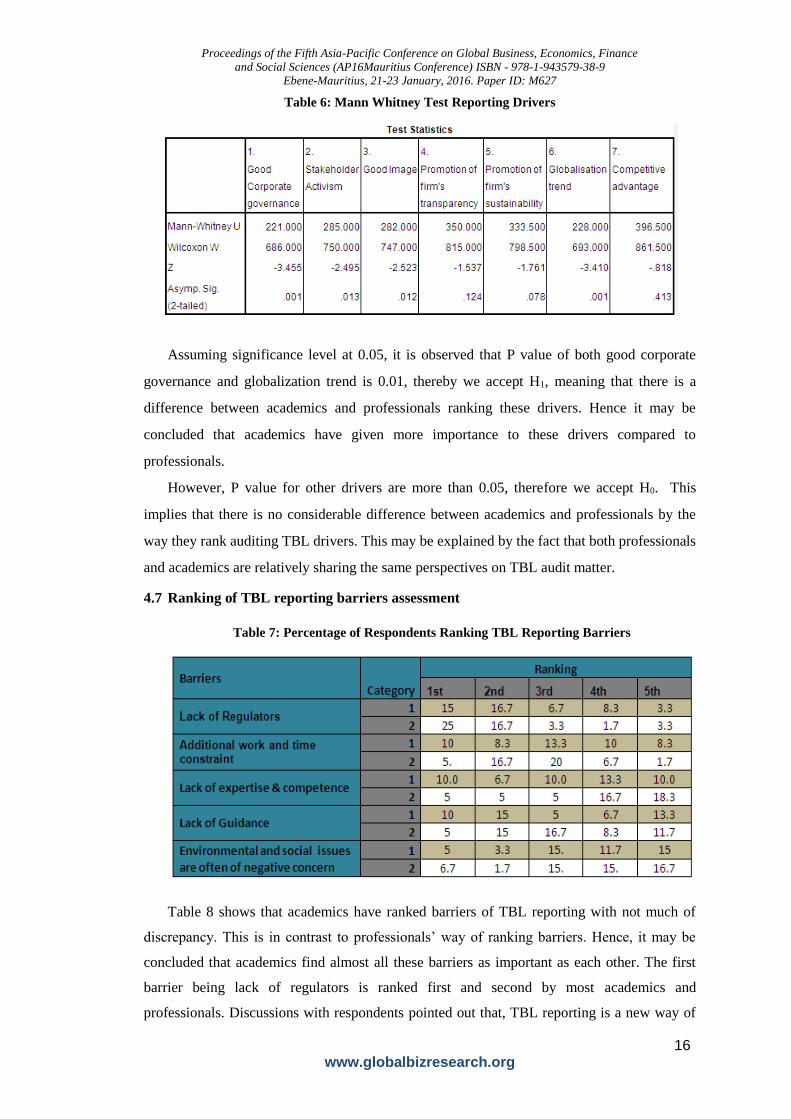

Table 6: Mann Whitney Test Reporting Drivers

Assuming significance level at 0.05, it is observed that P value of both good corporate

governance and globalization trend is 0.01, thereby we accept H1, meaning that there is a

difference between academics and professionals ranking these drivers. Hence it may be

concluded that academics have given more importance to these drivers compared to

professionals.

However, P value for other drivers are more than 0.05, therefore we accept H0. This

implies that there is no considerable difference between academics and professionals by the

way they rank auditing TBL drivers. This may be explained by the fact that both professionals

and academics are relatively sharing the same perspectives on TBL audit matter.

4.7 Ranking of TBL reporting barriers assessment

Table 7: Percentage of Respondents Ranking TBL Reporting Barriers

Table 8 shows that academics have ranked barriers of TBL reporting with not much of

discrepancy. This is in contrast to professionals’ way of ranking barriers. Hence, it may be

concluded that academics find almost all these barriers as important as each other. The first

barrier being lack of regulators is ranked first and second by most academics and

professionals. Discussions with respondents pointed out that, TBL reporting is a new way of

Proceedings of the Fifth Asia-Pacific Conference on Global Business, Economics, Finance

and Social Sciences (AP16Mauritius Conference) ISBN - 978-1-943579-38-9

Ebene-Mauritius, 21-23 January, 2016. Paper ID: M627

17 www.globalbizresearch.org

reporting in Mauritius and therefore, specific regulators have not yet been assigned to monitor

and regulate it.

Moreover, for barrier additional cost, work and time, academics have almost evenly

ranked it, hence it may be concluded that this barrier is of average importance to academics.

On the other hand, a significant proportion of professionals ranked the same driver second

and third. This may be explained by the fact that accountants will have more responsibilities

yet time to prepare accounts will remain same.

Similarly, academics give moderate importance to the barrier of lack of expertise &

competence as they are moderately versed with reporting of TBL. In contrary, most

professionals ranked the same barrier fourth and fifth. Looking at the ranking as such may be

misleading. Investigations with professionals revealed that accountants do have the expertise

to assess the financial aspect of environmental and social matters mainly. The literature

review mentions standards in place to assist accountants in this matter.

4.8 Ranking of TBL Auditing Barriers Assessment

Table 8: Percentage Respondents Ranking TBL Audit Barriers

According to statistics in Figure 7, it is noticed that significant number of professionals

have ranked barriers reliance on work of expert/ management, lack of expertise, competence

and knowledge and lack of regulators first, second and third respectively. Upon discussion

with professionals, financial auditors have declared that they have to rely on the work of an

expert/ management if they are to conduct TBL audit, as they lack expertise, competence and

knowledge and guidance on environmental and social matters.

Similarly, a considerable number of academics ranked lack of expertise, competence and

knowledge and lack of guidance first and second respectively. Most academics state being a

completely new issue, research has to been carried out to gather information on this matter.

Hereafter, guidance, knowledge and expertise may be acquired on the procedures and scope

of TBL audits.

Proceedings of the Fifth Asia-Pacific Conference on Global Business, Economics, Finance

and Social Sciences (AP16Mauritius Conference) ISBN - 978-1-943579-38-9

Ebene-Mauritius, 21-23 January, 2016. Paper ID: M627

18 www.globalbizresearch.org

Moreover, it is to be note that most academics and professionals ranked the barrier of

additional cost, work, and time last. Respondents it was pointed out that additional cost would

be in terms of paying for trainings, examinations, courses and seminars to acquire the

knowledge of TBL audit. Indeed, such practice will increase work load and audit assignment

may take longer to be completed.

Hypothesis 4

Ho: There is no difference with respect to the ranking of barriers of TBL reporting& auditing

by academics and professionals.

H1: There is a difference with respect to the ranking of barriers of TBL reporting& auditing

by academics and professionals.

Table 9: Mann Whitney Tests for barriers

Assuming significance level at 0.05, it is observed that P value for all barriers are more

than 0.05 for both auditing and reporting ,thereby we accept H0, meaning that there is no

difference between academics and professionals ranking these barriers. This may be

explained by the fact that both professionals and academics are relatively ranking the barriers

by sharing the same perspectives on TBL reporting and auditing matter.

Proceedings of the Fifth Asia-Pacific Conference on Global Business, Economics, Finance

and Social Sciences (AP16Mauritius Conference) ISBN - 978-1-943579-38-9

Ebene-Mauritius, 21-23 January, 2016. Paper ID: M627

19 www.globalbizresearch.org

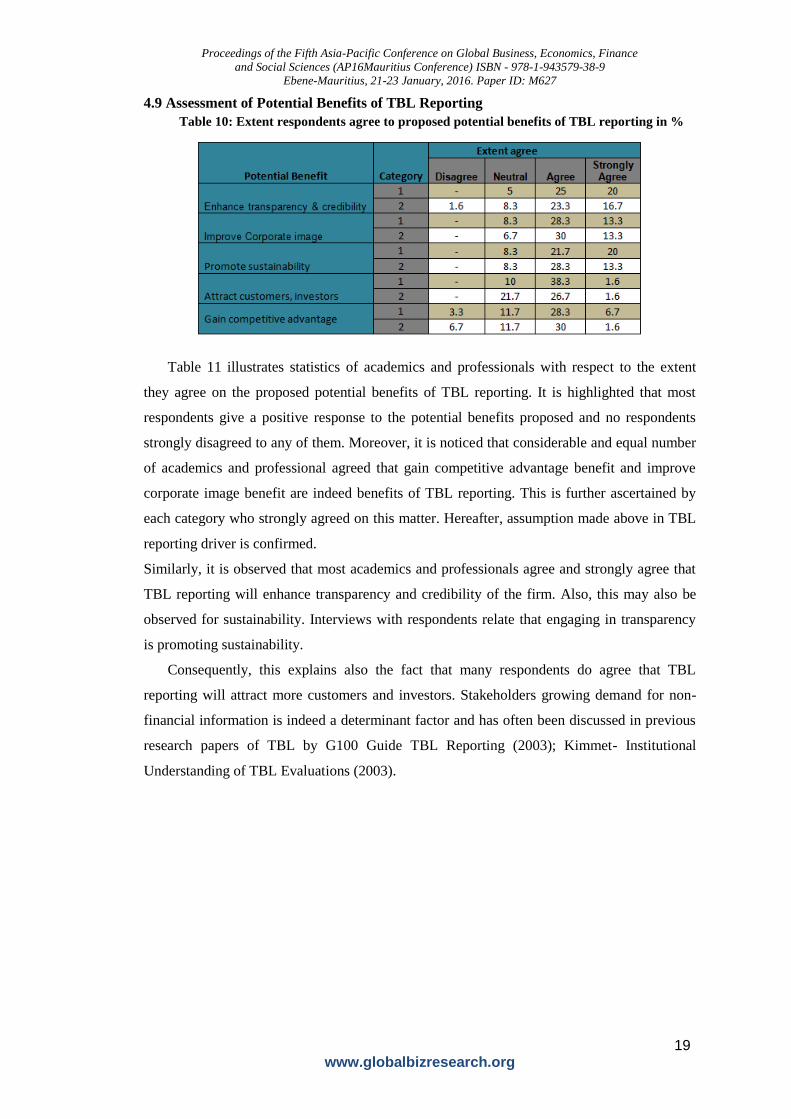

4.9 Assessment of Potential Benefits of TBL Reporting

Table 10: Extent respondents agree to proposed potential benefits of TBL reporting in %

Table 11 illustrates statistics of academics and professionals with respect to the extent

they agree on the proposed potential benefits of TBL reporting. It is highlighted that most

respondents give a positive response to the potential benefits proposed and no respondents

strongly disagreed to any of them. Moreover, it is noticed that considerable and equal number

of academics and professional agreed that gain competitive advantage benefit and improve

corporate image benefit are indeed benefits of TBL reporting. This is further ascertained by

each category who strongly agreed on this matter. Hereafter, assumption made above in TBL

reporting driver is confirmed.

Similarly, it is observed that most academics and professionals agree and strongly agree that

TBL reporting will enhance transparency and credibility of the firm. Also, this may also be

observed for sustainability. Interviews with respondents relate that engaging in transparency

is promoting sustainability.

Consequently, this explains also the fact that many respondents do agree that TBL

reporting will attract more customers and investors. Stakeholders growing demand for non-

financial information is indeed a determinant factor and has often been discussed in previous

research papers of TBL by G100 Guide TBL Reporting (2003); Kimmet- Institutional

Understanding of TBL Evaluations (2003).

Proceedings of the Fifth Asia-Pacific Conference on Global Business, Economics, Finance

and Social Sciences (AP16Mauritius Conference) ISBN - 978-1-943579-38-9

Ebene-Mauritius, 21-23 January, 2016. Paper ID: M627

20 www.globalbizresearch.org

4.10 Assessment of potential benefits of TBL Auditing

Table 11: Extent respondents agree to proposed potential benefits of TBL audit in %

As per results in Table 12, it is observed that most respondents agreed on the proposed

potential benefits of TBL auditing and no respondents strongly disagreed to any of them. It is

worth mentioning that highest proportion of respondents strongly agree and agree that TBL

reporting enhances transparency and credibility of firms. Interviews with respondents pointed

out that reasonable assurance of firms’ transparency contribute to enhance stakeholders’

commitment vis-à-vis firms thereby promoting sustainability in future.

Consequently, this analysis further asserts that more customers and investors are willing

to consider dealings with such firms. Discussions with academics and professionals show that

Mauritius is a developing country and most firms have already reached maturity level of their

life cycle, hence securing their license to operate by having a good customer cushion is

important for their survival. Thus, it may be concluded this is one of the reasons why firms’

respond to stakeholders concerns.

Moreover, competitive advantage benefit is likely to be agreed by respondents, whereby

professionals stated that this may enhance corporate image and ultimately attract more

customers. On the other hand, academics pointed out that this benefit may be considered as a

competitive positioning tool for firms creating a synergy to respond to competition,

sustainability and stakeholders concern.

Hypothesis 5

Ho: There is no difference between academics and professionals finding that all potential

benefits proposed may be achieved by TBL reporting and auditing

H1: There is no difference between academics and professionals finding that all potential may

be achieved by TBL reporting and auditing

Proceedings of the Fifth Asia-Pacific Conference on Global Business, Economics, Finance

and Social Sciences (AP16Mauritius Conference) ISBN - 978-1-943579-38-9

Ebene-Mauritius, 21-23 January, 2016. Paper ID: M627

21 www.globalbizresearch.org

Table 12: Mann Witney test for proposed potential benefits

Assuming significance level at 0.05, it is observed that P value for all benefits are more

than 0.05 for both auditing and reporting, thereby we accept H0, meaning that there is no

difference between academics and professionals finding that all potential benefits proposed

may be achieved by TBL reporting and auditing. This may be because respondents are

sharing same reasons on each benefit.

4.11 Assessment of Auditing and reporting frameworks

Table 13: Extent respondents agree on TBL framework adequacy and appropriateness in %

From table it is observed that academics and professionals of reporting and auditing TBL

share the same views. This observation is further analysed with a Chi square test.

Hypothesis 6

Ho: Academics and professionals do not find reporting framework appropriate and adequate

and implement TBL auditing compared to academics.

H1: More professionals find reporting framework appropriate and adequate and implement

TBL auditing compared to academics.

Proceedings of the Fifth Asia-Pacific Conference on Global Business, Economics, Finance

and Social Sciences (AP16Mauritius Conference) ISBN - 978-1-943579-38-9

Ebene-Mauritius, 21-23 January, 2016. Paper ID: M627

22 www.globalbizresearch.org

Table 14: Chi square Test for framework adequacy and appropriateness

Assuming significance level at 0.05, it is observed that P value for both Chi Square tests

are more than 0.05 for both auditing and reporting, thereby we accept H0, meaning that

academics and professionals do not find reporting framework appropriate and adequate and

implement TBL auditing compared to academics. This may be explained by the fact that TBL

Reporting and Auditing is a new concept and there is a need to develop frameworks to assist

such activity. This also explains why respondents found that lack of regulators is a

determining barrier.

4.12 Assessment of which regulators would be appropriate to regulate TBL reporting

and auditing

Table 15: Percentage of respondents who find existing regulators appropriate to regulate TBL

Observations from tables above show that respondents do find Financial Reporting

Council (FRC) and Financial Services Commission (FSC) are two regulators that would be

appropriate to regulate TBL reporting and auditing. However, discussions with respondents

argue that necessary amendments need to make each institution before they are fully able to

regulate TBL.

Moreover, it is noted that responses regarding Registrar varied. Most academics mainly

students found that Registrar is not an appropriate regulator. Discussions with them pointed

out that they lack knowledge on the role of Registrar and thus preferred to give a negative

response.

Proceedings of the Fifth Asia-Pacific Conference on Global Business, Economics, Finance

and Social Sciences (AP16Mauritius Conference) ISBN - 978-1-943579-38-9

Ebene-Mauritius, 21-23 January, 2016. Paper ID: M627

23 www.globalbizresearch.org

On the other hand, it is noticed that responses to Bank of Mauritius (BOM) as a regulator was

quite smooth by academics and professionals. It is to be noted that BOM regulated banks of

which Mauritius Commercial Bank and State Bank of Mauritius have been engaging in TBL

activities such as CSR and Go Green engagement.

4.13 Assessment of the extent of importance of recommendations given by academics

and professionals for TBL reporting.

Table 16: Extent respondents agree on proposed recommendations for TBL reporting

implementation in %

Table 17 shows that considerable proportion of respondents give high importance to make

TBL reporting mandatory. Upon discussions, respondents stated that in doing so, uniformity

and transparency will prevail in reported accounts. As such, this will enable stakeholders to

perform proper comparisons within firms. Similarly, promulgation and enforcement of

appropriate reporting standards was also given high importance by most respondents.

Respondents declared that these standards will assist in measuring, characterising and

classifying environmental and social matters.

Moreover, it is noted that most professionals have given moderate importance to

mandatory good corporate governance compared to most academics who find it more

important. Most academics especially lecturers pointed out that in doing so, this may reduce

risk of financial crisis and increase access to external finance. However it is worth mentioning

that lately, amendments to economic and financial measures in Financial Reporting Act in

2012 have made good corporate governance a mandatory statue.

Statistics illustrate that most respondents find it important to improve display of responsibility

and competence from Top to Bottom in a company. If orders come from top then it is also

true that example come from top. It is one of the fundamental duties of those in management

level to display the right attitude, behaviour and be the leader by example. Therefore, it is the

responsibility of management to take decision on whether to report TBL or not. Interviews

Proceedings of the Fifth Asia-Pacific Conference on Global Business, Economics, Finance

and Social Sciences (AP16Mauritius Conference) ISBN - 978-1-943579-38-9

Ebene-Mauritius, 21-23 January, 2016. Paper ID: M627

24 www.globalbizresearch.org

with respondents pointed out that top Management may include TBL reporting as part of

company’s culture or policy.

Furthermore, it is to be highlighted that academics and professionals assigned high

importance to awareness and guidance campaigns by providing for certified training,

seminars and workshops to encourage TBL reporting. Such recommendation will remove the

barrier of lack of guidance faced by professionals and academics. In addition discussions

pointed that respondents promoting awareness of benefits that may be achieved by reporting

TBL. Respondents discussed on provision of sufficient incentives to disclose environmental

and social matters will also encourage respondents to engage on TBL reporting.

In addition, academics and professionals lay emphasis on the recommendation that

Mauritius needs to improve the quality of financial reporting before it can even consider TBL

reporting. Upon discussions it is noted that respondents have criticized current reporting

frameworks due to scandals such as Air Mauritius black-box, Med point, Mauritius

Commercial Bank (MCB)- National Pension Fund (NPF), White Dot and Sunkai. Upon

investigation, respondents pointed out that those scandals involve renowned companies which

by default were supposed to set examples but the case indeed is different.

5. Conclusion

As popularity of TBL reporting and auditing grows in the world trade village, Mauritius

cannot remain indifferent to this matter. Hence, it is imperative to set guidance, frameworks

and measures to assist in TBL matters. By adopting TBL, businesses in Mauritius understand

that they are held to specific principles that are developed by internal and external forces.

Analysis highlighted long-term sustainability and promotion of transparency were the

main drivers chosen by respondents. On the other hand, main barriers were lack of regulators

and lack of expertise and competence which indicates that awareness programs and trainings

are a MUST for successful TBL implementation. In addition, to be the leading company, the

latter has to undertake innovative business strategies. One way of achieving this may be by

aligning TBL reporting and auditing as a strategy.

Taking into consideration drivers, barriers, potential benefits and recommendations, it

may be concluded that the adoption of TBL reporting and auditing is worthwhile in our dot

island. The Moto of TBL may be captured from Andrew W. Savitz and Karl Weber, who

beautifully praised TBL as “Your Company’s sweet spot is where its financial interests

coincide with social and environmental interest.”

References

Adeyeye, A., 2011. Universal standards in CSR: are we prepared? Corporate Governance, 11(1),

pp.107–119. Available at: http://www.emeraldinsight.com/10.1108/14720701111108880 [Accessed

February 28, 2013].

Proceedings of the Fifth Asia-Pacific Conference on Global Business, Economics, Finance

and Social Sciences (AP16Mauritius Conference) ISBN - 978-1-943579-38-9

Ebene-Mauritius, 21-23 January, 2016. Paper ID: M627

25 www.globalbizresearch.org

AlNaimi, H.A., 2012. Corporate social responsibility reporting in Qatar: a descriptive analysis. Social

Responsibility Journal, 8(4), pp.511–526. Available at:

http://www.emeraldinsight.com/10.1108/17471111211272093 [Accessed April 9, 2013].

Assurance, O. & Services, R., 2004. INTERNATIONAL AUDITING PRACTICE STATEMENT 1010

THE CONSIDERATION OF ENVIRONMENTAL MATTERS IN., (December), pp.150–175.

Barker, R., 2003. The revolution ahead in financial reporting: reporting financial performance. Balance

Sheet, 11(4), pp.19–23. Available at: http://www.emeraldinsight.com/10.1108/09657960310502502

[Accessed April 9, 2013].

Batra, G.S., 2010. Emerald Article: a study of the Indian corporate sector Dynamics of social auditing

in corporate enterprisespp

Burritt, R.L., 2012. Environmental performance accountability: planet, people, profits. Accounting,

Auditing & Accountability Journal, 25(2), pp.370–405. Available at:

http://www.emeraldinsight.com/10.1108/09513571211198791 [Accessed April 6, 2013].

Dutta, S. & Reporting, S., 2011. “Triple Bottom Line Reporting: an innovative accounting

initiative”International Journal for Business, Strategy & Management. , pp.1–13.

Deegan, C. and Rankin, M. (1997), “The materiality of environmental information to users of annual

reports”,Accounting, Auditing and Accountability Journal, Vol 10 No.4, pp.65-69.

Eugénio, T., Lourenço, I.C. & Morais, A.I., 2010. Recent developments in social and environmental

accounting research. Social Responsibility Journal, 6(2), pp.286–305. Available at:

http://www.emeraldinsight.com/10.1108/17471111011051775 [Accessed December 6, 2012].

Faux, J., 2012. Environmental event materiality and decision making. Managerial Auditing Journal,

27(3), pp.284–298. Available at: http://www.emeraldinsight.com/10.1108/02686901211207500

[Accessed December 6, 2013].

Frost, G. (2007), “The introduction of mandatory environmental reporting guidelines”, Abacus, Vol 43

No. 2, pp190-216.

Ifrs, I.A.S. & Barbu, E.M., 2011. CAHIER DE RECHERCHE n ° 2011-09 E2 LilianaFeleagă.

Khomba, J.K. &Vermaak, F.N.S., 2012. Relevance of financial reporting systems: Single-bottom line

or triple-bottom line. African Journal of Business Management, 6(9), pp.3519–3527. Available at:

http://www.academicjournals.org/ajbm/abstracts/abstracts/abstracts2012/7Mar/Khomba and Vermaak

3.htm [Accessed December 9, 2012].

Lander, G.H. & Auger, K. A, 2008. The need for transparency in financial reporting: Implications of

off-balance-sheet financing and inferences for the future. Journal of Accounting & Organizational

Change, 4(1), pp.27–46. Available at: http://www.emeraldinsight.com/10.1108/18325910810855770

[Accessed December 6, 2012].

Low, W. et al., Parellel lines- the development of social auditing and triple bottom line reporting in

New Zealand Will Low. , pp.138–148.

Michael Watson, Joyce MacKay, (2003),"Auditing for the environment", Managerial Auditing Journal,

Vol. 18 Iss: 8 pp. 625 – 630

Morimoto, R, Ash, J & Hope, C, 2004, in Management Studies corporate social responsibility audit:

from theory to practice audit

Morimoto, Risako, Ash, John & Hope, Chris, 2012a. Corporate Social Responsibility to Practice Audit:

62(4), pp.315–325.

Negash, M., 2012. IFRS and environmental accounting. Management Research Review, 35(7), pp.577–

601. Available at: http://www.emeraldinsight.com/10.1108/01409171211238811 [Accessed December

9, 2012].

Norman, W. & MacDonald, C., 2004. Getting to the Bottom of “Triple Bottom Line. Business Ethics

Quarterly, 14(2), pp.1–19. Available at: http://www.jstor.org/stable/3857909.

Raar, J., 2002. Environmental initiatives: towards triple-bottom line reporting. Corporate

Communications, An International Journal, 7(3), pp.169–183. Available at:

http://www.emeraldinsight.com/10.1108/13563280210436781 [Accessed December 9, 2012].

Proceedings of the Fifth Asia-Pacific Conference on Global Business, Economics, Finance

and Social Sciences (AP16Mauritius Conference) ISBN - 978-1-943579-38-9

Ebene-Mauritius, 21-23 January, 2016. Paper ID: M627

26 www.globalbizresearch.org

Ramdhony, D. & Oogarah-hanuman, V., Improving CSR Reporting in Mauritius – Accountants’

perspectives. , pp.1–13.

Websites

Accountancy body chief executive gives thoughts on IIRC | ACCA | ACCA Global. 2013. . [ONLINE]

Available at: [Accessed 2 January, 013].

Barriers to Environmental Reporting - Essays - Nuzha11. 2013. [ONLINE] Available

at:http://www.studymode.com/essays/Barriers-To-Environmental-Reporting-599333.html. [Accessed

10 January 2013].

CSR Strategy in Developing Countries | Triple Bottom Line Magazine. 2013. CSR Strategy in

Developing Countries. [ONLINE] Available at: http://www.tbl.com.pk/csr-strategy-in-developing-countries/. [Accessed 8 December, 2012].

Debunking the Notion of a Triple Bottom Line | GreenBiz.com. 2013. [ONLINE] Available

at: http://www.greenbiz.com/blog/2009/08/31/debunking-notion-triple-bottom-line. [Accessed 8

December 2012].

Financial Reporting Council Mauritius. 2013. [ONLINE] Available at:

http://www.gov.mu/portal/sites/frc/org_charter.html. [Accessed 2 January, 2012].

Financial Reporting Vol. 1. 2013. Financial Reporting Vol. 1. [ONLINE] Available

at: http://www.scribd.com/doc/17369569/Financial-Reporting-Vol-1. [1 January, 2013].

Financial Statements - benefits, cost, financial reporting, Major financial statements. 2013. [ONLINE]

Available at: http://www.referenceforbusiness.com/small/Eq-Inc/Financial-Statements.html. [Accessed 31 December 2012].

Home | SBM. 2013. Home | SBM. [ONLINE] Available at: http://www.sbmgroup.mu/ csr_internal_programs.php?suf1=csr&lang=en. [Accessed 6 December, 2012].

IAPS 1010 2013. . [ONLINE] Available at: http://www.ifac.org/sites/default/files/ downloads/b007-2010-iaasb-handbook-iaps-1010.pdf. [Accessed 4 December, 2012].

ISA-500. 2013. [ONLINE] Available at: http://www.scribd.com/doc/13994533/ISA500. [Accessed 10

December 2012].

It’s Time for Triple Bottom Line Reporting. 2013. [ONLINE] Available at: http://www.nysscpa.org/ cpajournal/2003/1203/nv/nv3a.htm. [Accessed 5 January 2013].

MID - Maurice Ile Durable. 2013. [ONLINE] Available at: [Accessed 2 January 2013].

Objectives of Financial Reporting. 2013. [ONLINE] Available at: http://highered.mcgraw-hill.com/sites/0072994029/student_view0/ebook/chapter1/chbody1/objectives_of_financial_reporting.html. [Accessed 12 December 2012].

Observatoire de L'Industrie Mauritius. 2013. Observatoire de L'Industrie Mauritius. [ONLINE]

Available at:http://www.industryobservatory.org/carbon_credit.php. [Accessed 2 February 2013].

Polémique autour de l’attribution de la licence EIA à CT Power: le travailleur social Jeff Lingaya

démarre une grève de la faim | Defimedia.info. 2013. Defimedia.info. [ONLINE] Available

at: http://www.defimedia.info/live-news/item/25661-pol%C3%A9mique-autour-de-l%E2%80%99attribution-de-la-licence-eia-%C3%A0-ct-power-le-travailleur-social-jeff-lingaya-d%C3%A9marre-une-gr%C3%A8ve-de-la-faim.html. [Accessed 2 February, 2013].

Proceedings of the Fifth Asia-Pacific Conference on Global Business, Economics, Finance

and Social Sciences (AP16Mauritius Conference) ISBN - 978-1-943579-38-9

Ebene-Mauritius, 21-23 January, 2016. Paper ID: M627

27 www.globalbizresearch.org

Purpose of Financial Statements and Users of Financial Statements. 2013. [ONLINE] Available

at: http://accounting-simplified.com/purpose-of-financial-statements.html. [Accessed 10

December, 2012].

SASA - South Africa's Leading Accountancy Journal. 2013. [ONLINE] Available at:

http://www.accountancysa.org.za/resources/ShowItemArticle.asp?ArticleId=1828&Issue=1088.

[Accessed 15 December, 2012].

Social Auditing - A Method of Determining Impact. 2013. Social Auditing - A Method of Determining

Impact. [ONLINE] Available at: http://www.caledonia.org.uk/socialland/social.htm. [Accessed 11

December 2012].

Social Auditing. 2013. [ONLINE] Available at: http://www.partas.ie/Consultancy/ SocialAuditing.aspx. [Accessed 11 December 2012].

Social Audits. 2013. [ONLINE] Available at:http://www.pgexchange.org/ index.php?option=com_content&view=article&id=142&Itemid=136. [Accessed 11 December 2012].

The Nutty C.I.O » Blog Archive » Competitive advantage and the triple bottom line. 2013. [ONLINE]

Available at: http://www.thenuttycio.com/blog/?p=36. [Accessed 11 January 2013].

The Triple Bottom Line. 2013. [ONLINE] Available at:http://toolkit.smallbiz.nsw.gov.au/ part/17/84/363. [Accessed 11 January 2013].

The Triple Bottom Line: What Is It and How Does It Work? 2013 [ONLINE] Available

at:http://www.ibrc.indiana.edu/ibr/2011/spring/article2.html. [Accessed 22 December, 2012].

Triple Bottom Line Reporting | Suite101. 2013. Suite101. [ONLINE] Available

at: http://suite101.com/article/triple-bottom-line-reporting-a136110. [Accessed 22 December,

2012].

Types of Audit Opinions. 2013 [ONLINE] Available at: http://www.urlaubaccounting.com/ typeaudit.html. [7 January, 2013].

Books

Savitz Andrew W. & Weber Karl, 2006 “The triple bottom line: how today’s best-run companies are

achieving economic, social and environmental success- and how you can too”. First edition. United

States of America. Published by Jossey Bass.

AndrianHenriques& Julie Richardson editors, 2004 “The triple bottom line: does it add up all?

Assessing the sustainability of business and CSR”.First edition.United Kingdom and United States of

America.Published by Earthscan.