Thinking outside the boxTroy Smith

• Maximising Centrelink benefits

• Considering annuities

• Changes to the pension

• Getting affairs into order

Agenda

Solar panels• Expenditure on the main residence is exempt– Reduction in assessable assets

• Solar feed in tariffs paid as an electricity account credit are not assessable as income• Solar feed in tariffs paid as cash (or direct deposit) are assessed as income

Solar hot water• Expenditure on the main residence is exempt– Reduction in assessable assets

• Receipt of rebates is not assessable as income

Water tanks• Expenditure on the main residence is exempt– Reduction in assessable assets

Maximising Centrelink benefits

Funeral bonds• Invest up to the exempt funeral investment threshold– $12,250 as at 1 July 2015

• Earnings are exempt • Each member of a couple may invest in up to the exempt threshold

Arthur and Martha • Each invest $12,250 in a funeral bond. • $24,500 is exempt from assessment

Maximising Centrelink benefits

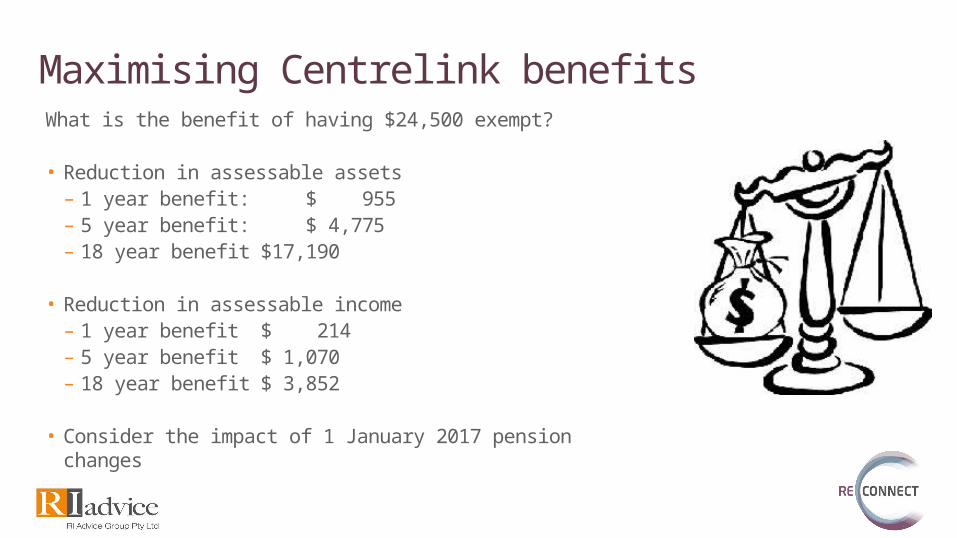

What is the benefit of having $24,500 exempt?

• Reduction in assessable assets– 1 year benefit: $ 955– 5 year benefit: $ 4,775– 18 year benefit $17,190

• Reduction in assessable income– 1 year benefit $ 214– 5 year benefit $ 1,070– 18 year benefit $ 3,852

• Consider the impact of 1 January 2017 pension changes

Maximising Centrelink benefits

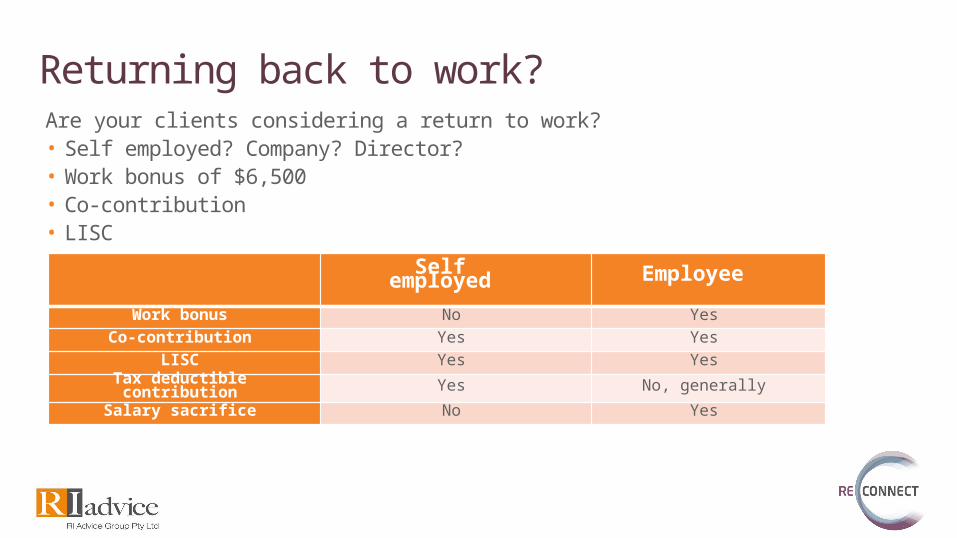

Are your clients considering a return to work?• Self employed? Company? Director?• Work bonus of $6,500• Co-contribution• LISC

Returning back to work?

Self employed Employee

Work bonus No Yes

Co-contribution Yes Yes

LISC Yes Yes

Tax deductible contribution Yes No, generally

Salary sacrifice No Yes

Term certain annuities

Income test assessment– RCV 0%, RCV 100% or something in between?– Pension amount – [(Purchase price – Commutations – RCV) / Term]

Bill invests $200,000 into a 10 year annuity with a RCV 0%– Receives an annual income of $24,230– Centrelink non-assessable component of $20,000– Assessable component of $4,230

Are annuities an option?

Term certain annuities

Assets test assessment– RCV 0%, RCV 100% or something in between?

Purchase price – {[(Purchase price – RCV) / Term] x TE}

– Bill invests $200,000 into a 10 year annuity with a RCV 0%

– First 6 months: $200,000 $200,000 – {[($200,000 - $0) / 10] x 0}

– Next 6 months $190,000 $200,000 – {[($200,000 - $0) / 10] x 0.5}

– Following 6 months $180,000 $200,000 – {[($200,000 - $0) / 10] x 1.0}

Are annuities an option?

• Comparing a term certain annuity and an account based pension

Are annuities an option?

Assets test assessment

Income test assessment

ABP ($200,000) $200,000 $5,771

Annuity (6 months) $200,000 $4,230

Annuity (12 months) $190,000 $4,230

Annuity (18 months) $180,000 $4,230

Changes to asset thresholdsFrom 1 January 2017, the assets test free area will increase. Once assets exceed these thresholds, Parenting payment, allowances (e.g. Widow, Youth, Newstart, Sickness, Partner), Austudy and Special benefit) are not payable and pensions are reduced.

Changes to the pension

Status Current threshold Increased lower

threshold (1 Jan 2017)

Single homeowner $202,000 $250,000

Single non-homeowner $348,500 $450,000

Couple homeowner $286,500 $375,000

Couple non-homeowner $433,000 $575,000

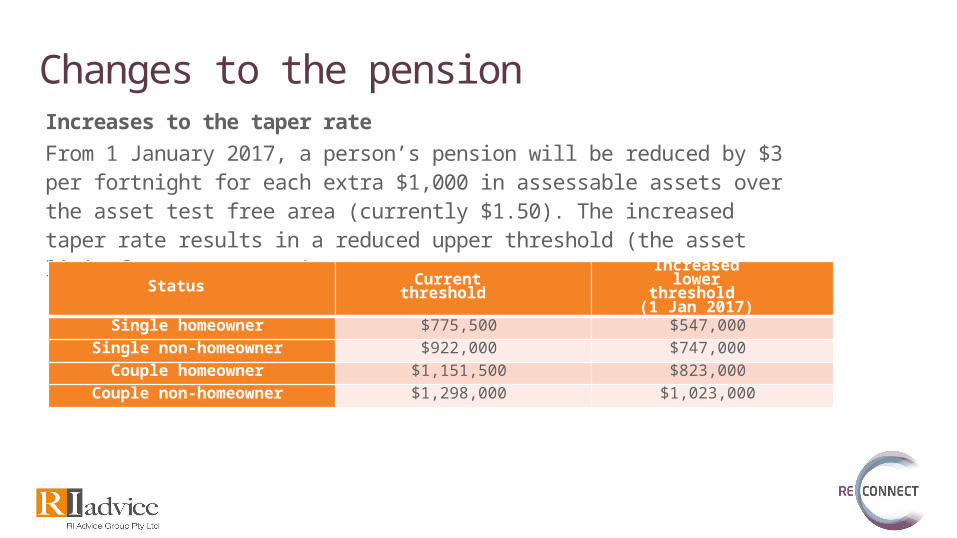

Increases to the taper rateFrom 1 January 2017, a person’s pension will be reduced by $3 per fortnight for each extra $1,000 in assessable assets over the asset test free area (currently $1.50). The increased taper rate results in a reduced upper threshold (the asset limit for a part pension).

Changes to the pension

Status Current threshold Increased lower

threshold (1 Jan 2017)

Single homeowner $775,500 $547,000

Single non-homeowner $922,000 $747,000

Couple homeowner $1,151,500 $823,000

Couple non-homeowner $1,298,000 $1,023,000

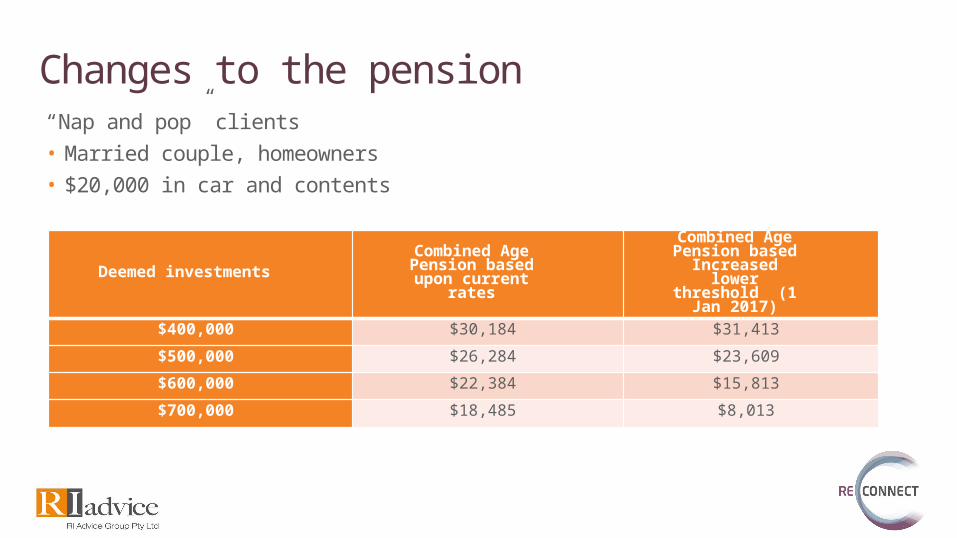

“Nap and pop” clients• Married couple, homeowners• $20,000 in car and contents

Changes to the pension

Deemed investmentsCombined Age Pension based

upon current rates

Combined Age Pension based Increased lower threshold (1 Jan

2017)

$400,000 $30,184 $31,413

$500,000 $26,284 $23,609

$600,000 $22,384 $15,813

$700,000 $18,485 $8,013

Age Pension calculator

Based upon previous ‘nan and pop’ example with $700,000 of deemed (note that calculations are based on a per person basis

Age Pension calculator

The principle place of residence: Downsizing

Moving to another house– If a person or their partner sells their principal home and intends to use the proceeds

within 12 months to purchase another home, the portion of the proceeds that will be used to acquire another home are exempt from the assets test for up to 12 months from the date of sale.

– No exemption applies for income testing purposes

Moving to something smaller– Arthur and Martha sell their house for $1,000,000. They intend to downsize and plan to

spend $650,000 on a new house. – Assets test exemption applies to $650,000– No exemption applies for income testing purposes

Downsizing

Having two homes– If a person, or their partner, has more than one home, their principal home is the one

in which they spend the greatest amount of time. If they spend the same amount of time in each of them, the most expensive home is defined as the principal home.

Temporary vacation– If a person temporarily vacates their principal home with the intention to return, the

home remains an exempt asset for up to 12 months. – After a 12 month temporary absence the home is no longer the person's principal

home and becomes an assessable asset.

Downsizing

A campervan, caravan, transportable home or boat in which a person lives, falls within the definition of a permanent home (or principal residence) for social security assets test purposes. – the person is classed as a homeowner and the lower homeowner’s assets limit applies; – the value of the campervan, caravan, transportable home, or boat is an exempt asset.– Rent Assistance can be received for fees payable on a regular basis as a condition of occupying

their home, e.g. fees for the use of a caravan site.

Becoming a grey nomad

Organise appropriate documents• Power of Attorney• Enduring Power of Attorney• Guardianship order

• Professional drafted versus DIY will kit• Testamentary trust?– Protective– Bloodline– Other?

Getting affairs into order

Getting around ‘gifting’• Bequeathing of assets are not subject to gifting

• Remember Arthur and Martha?– Upon death of either partner, the surviving partner will be assessed as a single

person. Consider if their assets exceed the thresholds– Consider the impact of 1 January 2017 changes

Getting affairs into order

• Centrelink back to basics

• Comparing annuities to account based pensions

• Downsizing the principle place of residence

• Getting their affairs into order

Wrap-up