The World Bank-IMF Debt Sustainability Framework (DSF)

for LICsOverview and recent changes

1

Presentation bySudarshan Gooptu

Acting Director, Economic Policy and Debt DepartmentWorld Bank

Meeting of the OEWG of the General Assembly, UN, New York, April 12, 2010

Debt Management: the big picture

• Since 1996, there has been substantial progress in both the HIPC initiative and the MDRI: debt relief has opened space for contracting new debt– 40 eligible HIPCs willing to avail themselves of

relief under the HIPC Initiative– 5 countries reached CP recently: Burundi (Jan.

2009), CAR and Haiti (Jun. 2009), Rep. of Congo and Afghanistan (Jan. 2010)

– 2 countries have reached DP since late 2008: Togo (Nov. 2008) & Cote d’Ivoire (Mar. 2009)

Why assessing debt sustainability in LICs?

28 Post CP Countries

Afghanistan Benin Bolivia Burkina Faso Burundi Cameroon

Central African Republic Congo, Rep. of Ethiopia Ghana Guyana Gambia, The

Haiti Honduras Honduras Madagascar Malawi Mali

Mauritania Mozambique Nicaragua Niger Rwanda São Tomé and Príncipe

Senegal Sierra Leone Tanzania Uganda Zambia

7 Interim Countries

Chad Congo, Dem. Rep. of the Côte d’Ivoire Guinea Guinea-Bissau Liberia

Togo

5 Pre-DP Countries

ComorosComoros EritreaEritrea SomaliaSomalia Sudan Sudan Kyrgyz RepublicKyrgyz Republic

Why assessing debt sustainability in LICs?Heavily Indebted Poor Countries (as of January 2010)

Debt burdens have been reduced by 80% compared to DP levels(in billions of U.S. dollars, in end-2008 NPV terms)

89.275.6

36.8 31.57.0

48.5

38.8

20.2 20.2

16.9

0

20

40

60

80

100

120

140

160

Before traditional debt relief

After traditional debt relief

After HIPC Initiative debt relief

After additional bilateral debt relief

After MDRI

9 Interim Countries 26 Completion-Point Countries

Why assessing debt sustainability in LICs?

• In addition to the new landscape (i.e., new lenders) and the more volatile and uncertain financial environment …

• Potential mounting of fiscal deficits (due to fiscal stimulus packages)A proper institutional framework is necessary to manage public debt prudently and avoid a recurrence of debt distress (default) episodes, while adequately financing future growth.

Why assessing debt sustainability in LICs?

Empirical Foundation of the DSF

• Debt distress - quality of countries’ policies and institutions nexusEmpirical foundations: Kraay and Nehru – 2004

What factors explain episodes of external debt distress?

Debt distress measured as:• accumulation of arrears

• resort to Paris Club relief

• resort to IMF non-concessional support

Three sets of predictors:• vulnerability to (volatility of) macro shocks

• traditional debt burden indicators

• quality of policies and institutions7

Empirical Foundations (contd.)

• Debt distress - macro shocksEconometric results

8

9

Empirical Foundations (contd.)

• Debt distress - indebtednessEconometric results

10

Empirical Foundations (contd.)

• Debt distress - quality of countries’policies and institutions nexusEconometric results

The Country Policy and Institutional Assessment (CPIA)

• Index calculated by the World Bank that evaluates the quality of a country’s present policy and institutional framework (late 1990s)

• Calculated annually for all countries• Used by the Bank in the context of the allocation

process and the DSF• It comprises 16 criteria grouped in 4 clusters:

– Macroeconomic management– Structural policies– Policies for social inclusion and equity– Public sector management and institutions

11

The Country Policy and Institutional Assessment (CPIA)

• Countries are rated under each criterion (1 to 6)• The overall rating is the simple average of the

rates for all the criteria• Since 2001 several improvements have been

introduced to strengthen comparability across countries:– Detailed guidelines– 2-phase approach (benchmarking and rest of the

countries)

• Since 2005 CPIA overall rates for IDA-only countries are publicly available

12

• Debt distress - quality of countries’ policies and institutions nexus

1. The likelihood of debt distress is mainly explained by three factors:

• susceptibility to shocks,

• debt burden, and

• quality of policies and institutions

2. The quality of policies and institutions is as important as the debt burden in predicting debt distress episodes

→ For a constant probability of debt distress, country-specific debt thresholds are needed rather than a uniform threshold.

13

Interpretation of the results

The DSF

• Based on the: – Importance of debt sustainability for development– Need to take into account LIC’s specificities:– Empirical foundations on the link between the quality of

countries’ policies and institutions and the probability of debt distress

• A framework—called the LIC DSF—was developed jointly by the World Bank and the IMF (adopted in 2005) to:

– Bring a greater consistency, discipline, and transparency to sustainability analyses

– Allowing for better informed policy advice

14

Main features of the DSF

• A tool for borrowers and lenders

– Helps LICs define a borrowing strategy that matches their development objectives with their present/future capacity to pay

– Helps lenders & donors modulate (tailor) the terms of their financing according to debt sustainability risks

• Conducted annually

– Allows for corrections/adjustments

– Allows evaluation of earlier projections

• Two parallel exercises: for external debt and for total public debt (inc. domestic)

15

1.A standardized forward-looking analysis of debt and debt-service dynamics to asses a country’s debt sustainability (for total debt: external plus domestic).

2.An assessment of external debt sustainability in relation to indicative country-specific debt burden thresholds that, in turn, depend on the quality of countries’ policies and institutions.

3.A risk of external debt distress classification that takes into consideration this threshold assessment, as well as other country specific factors

16

The Three Pillars of the DSF

• Example:– Average CPIA for the last 3 years: 3.56

Quality of policies and institutionsQuality of policies and institutionsWeakWeak

CPIA<3.25CPIA<3.25MediumMedium

3.253.25≤≤CPIACPIA≤≤3.753.75StrongStrong

CPIA>3.75CPIA>3.75

NPV of debtNPV of debt--toto--GDPGDP 3030 4040 5050NPV of debtNPV of debt--toto--exportsexports 100100 150150 200200NPV of debtNPV of debt--toto--revenue revenue 200200 250250 300300

Debt serviceDebt service--toto--exportsexports 1515 2020 2525

Debt serviceDebt service--toto--revenuerevenue 2525 3030 3535

17

How does the DSF Work

• Example

18

How does the DSF Work

IDA’s use of the Debt Sustainability Framework

• DSF –a tool to assess a country’s risk of debt distress– is used to determine IDA’s grant eligibility among it’s borrowers.

• Grant allocation is based on external debt distress risk ratings determined under the DSF. Risk ratings are translated into a traffic light system for each country:

– Green Low Risk of Debt Distress

– Yellow Medium Risk of Debt Distress

– Red High Risk/on Debt Distress

IDA’s use of the Debt Sustainability Framework

– Green Low Risk of Debt Distress• 100% standard IDA credit highly

concessional terms (0.75%; 40 & 10 yrs)– Yellow Medium Risk of Debt Distress

• Mix of grants and loans 50%-50%– Red High Risk/on Debt Distress

• 100% grants• For medium and high risk of DD countries: grants

are subject to a 20% discount from grant allocation.

IDA: The Non-Concessional Borrowing Policy

• In place since July 2006; applies to countries that are grant-recipients or benefited from MDRI.

• Objective is to reduce the risk that non-concessional financing could lead to a re-accumulation of debt.

• Relies on a two-pronged strategy aimed at both creditors and borrowers:– Enhance creditor coordination using DSF (collective

action);– Discourage non-concessional borrowing (moral hazard

issue).• It consists of a case by case application of waivers of the

min. concessionality requirement (of 35% or more) or, if not complied with, more stringent lending conditions.

IDA: The Non-Concessional Borrowing Policy

• NOT a ban on non-concessional borrowing: specific criteria for a case-by-case assessment of potential exceptions to the policy:

• Country-specific criteria:– Overall borrowing plan– Impact of borrowing on macro framework– Impact on risk of Debt Default– Strength of policies and institutions

• Loan-specific criteria:– Development content– Estimated returns– Other potential additional costs associated

• Reporting requirement: enhance dialogue with borrowing countries regarding projects before borrowing occurs.

Use of the DSF by the IMFFund surveillance: The LIC DSA is important for the Fund’s overall assessment of macro-stability, the long-term sustainability of fiscal policy, and debt sustainability.The DSF integrates debt issues into and enriches Fund analyses and policy advice through its annual frequency, greater comparability of analyses across countries and inclusion of DSAs in country staff reports.Fund programs:

DSA is important to determine the grant element required for a countryFund-supported programs for low income countries incorporate limits on non-concessional external borrowing

Use of the DSF by other creditors

• An increasing number of creditors are incorporating elements of the DSF into their financing terms.Multilateral creditors: As of now, the AfDB, the IaDB, the AsDB, and IFAD incorporate elements of the DSF into their own financing terms.Bilateral creditors:

Most OECD donors explicitly use the DSF to guide their lending termsOECD export credit agencies adopted, in January 2008, a set of lending guidelines that adhere to IDA and IMF concessionality requirements for LICs.

Why reviewing the DSF?

• The DSF has been criticized on two grounds:– It restricts financing needed to meet

countries’ development goals (MDG)– It is too pro-cyclical

• The G20 and the IMFC called on the Bank and the Fund to review the DSF with a view to increasing its flexibility.

Staff’s approach to responding to the request

• The DSF is an analytical tool used to assess a country’s debt burden (thermometer).

• Increased flexibility should respect its integrity and reliability.

• Reforms to how the Bank and the Fund better meet members’ financing needs should be directed to its concessional lending and their policies on non-concessional borrowing (treatments).

Flexibility already inherent in the DSF

• Multi-year framework addresses criticism of pro-cyclicality;

• Staffs are required to exercise judgment in applying risk ratings (not a mechanistic approach) by looking at other aspects;– Short term debt; total debt; private debt;

foreign assets; reserves; etc.

Adding flexibility to the DSF

Four areas were considered:• Investment-growth nexus• Treatment of remittances• (Threshold effects)• Treatment of state-owned enterprise

debtIn addition, some changes to

operational aspects have been made.

The investment-growth nexus

IDA/IMF Boards agreed that the country specificapproach proposed in 2006, based on studying a number of indicators (structural/macro constraints, historical rates of return, etc.), remains largely valid.If a scaling-up of public investment is ongoing or imminent, or if high policy capacity increases the likelihood of such scaling-up, more formal model-based approaches should be considered (ex., a country specific GE model; growth diagnostics; etc.)“Full” DSAs should document staffs’ analysis of the investment-growth nexus

Remittances: Growing importance

An important source of FX for LICs

Figure 1: Workers' remittances and other inflows in low-income countries (% of GDP)

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

1980 1983 1986 1989 1992 1995 1998 2001 2004 2007

Gross official development assistanceForeign direct investment (net)Workers' remittances

Source: World Bank, World Development Indicators (2009)

Figure 2: Workers' remittances as a percentage of exports and GDP (average 2002-2007) for PRGF-eligible and IDA-only countries 1/

as a percentage of exports

0% 25% 50% 75% 100% 125% 150% 175% 200%

Côte d'IvoireBurundi

Congo, Republic ofVanuatuMalawi

TanzaniaMadagascar

DjiboutiMozambique

LesothoZambia

CameroonGhana

MyanmarSolomon Islands

CambodiaRwandaGuinea

NigerKenya

EthiopiaNigeria

São Tomé & PríncipeMali

MongoliaBenin

SierraLeoneTogo

GuyanaKyrgyz Republic

Sri LankaMoldova

SenegalHonduras

Guinea-BissauNicaragua

Gambia, TheSudan

Cape VerdeUganda

TajikistanBangladesh

NepalTongaHaiti

Source: World Bank, World Development Indicators (2009)1/ Average over 2002-2007 of available data.

as a percentage of GDP

0% 5% 10% 15% 20% 25% 30%

Côte d'Ivoire Burundi Malawi

TanzaniaVanuatu

MadagascarCongo, Republic ofPapua New Guinea

MozambiqueDjibouti

CameroonRwandaZambiaGhana

Lesotho Armenia

Niger Solomon Islands

EthiopiaGuinea

São Tomé & PríncipeKenya

Georgia Benin

CambodiaSierra Leone

MaliSt. Lucia

Bolivia Nigeria

St. Vincent & Grens.Sudan

UgandaDominicaGrenada Senegal

BangladeshTogo

MongoliaSri Lanka

Guinea-Bissau Kyrgyz Republic

Nicaragua Moldova

Cape VerdeGambia, The

AlbaniaNepal

HondurasGuyana

TajikistanHaiti

Tonga

Remittances: Growing importance

Remittances: Treatment in DSF

Boards agreed that insufficient data prevented remittances from being formally included in the empirical model underlying the DSFRemittances are important for DSAs—size, counter-cyclicalityGreater flexibility in taking account of remittances is justified on a case-by-case basis and more in-depth analysis is granted

• New debt burden indicators: – NPV of debt / (Exports + remittances)– NPV of debt / (GDP + remittances)(same for debt service indicators)

• Conditions to pursue modified or in-depth analysis:– Workers’ remittances should represent a

reliable (“large” and stable) source of foreign exchange

33

Remittances: Treatment in DSF

• Conditions to pursue “modified” or in depth analysis– Breaches of thresholds under the baseline or stress

tests before taking account of remittances are not very protracted

– Modified debt burden indicators are significantly lower than the applicable new DSF thresholds

Rule of thumb: apply a 10 percent margin to the “old” thresholds

34

Remittances: Treatment in DSF

Threshold effects: What is the problem?

• For countries close to the cut off points of CPIA ranges (≈ 3.25 and 3.75), small changes in a country’s CPIA may imply “large” changes in applicable debt thresholds (i.e., a CPIA drop from 3.26 to 3.24 threshold falls by 10% of GDP)

• This could result in changes to debt distress ratings• Such changes are hard to relate to a country’s

underlying capacity to service its foreign debt

Threshold effects: How do we address the problem?

Boards recommended:

• Add inertia to the CPIA score applicable for determining countries’ debt thresholds

• At present a 3-year moving average CPIA score is used to determine the policy performance category

• In the future, when the CPIA crosses its boundary– The new threshold will apply at once if the new 3 yr

average CPIA lies outside a range of ±0.05 from the boundary

– Otherwise, the CPIA will have to remain above/below the new boundary for 2 consecutive years

State-owned enterprise debt

• The current rule is that generally all SOEs external debt is included in the DSA.

• The Boards agreed that when SOEs can borrow without government guarantee and their operations pose a limited fiscal risk to public balance sheets, they could be excluded from consideration in DSAs.

SOE’s debt: indicators for exclusion

The following indicators are intended to help guide the decision to exclude a particular SOE:

•Managerial independence, including pricing and employment policies: cost-covering price setting; average prices vis-à-vis international benchmarks; independent employment and wage policies; etc.

•Relations with the government: existence of direct or indirect subsidies; on-lending and loan guarantees; quasi-fiscal or other activities not directly related to the SOE’s business objective; non-regular tax regimes; profit transfers from the SOE to the central budget, etc.

SOE’s debt: indicators for exclusion

• Periodic audits: are periodic audits carried out and published by a reputable private accounting firm applying international standards?

• Publication of comprehensive annual reports and protection of shareholders’ rights

• Financial conditions and sustainability: are costs of debt and borrowing rates comparable to private firms; are debt-to-asset ratios comparable to the industry average; is profitability positive and higher than average cost of debt? Is the average rate of return on investment equivalent to that required by cost-benefit analyses to approve new projects?

In addition: Discount rate

• The current rule required the discount rate (used to calculate PV of Debt) to be lowered by 100 basis points to 4 percent (in September ‘09).

• Simulations showed that a change in the discount rate to 4 percent generally resulted in relatively small increases in PV of debt.

• And a small number of countries were to experience small and temporary breaches of their respective thresholds (for some others, the size of existing breaches were to increase).

• These effects needed to be weighed against the cost of having a more sticky rule which would increase the lag of interest rateadjustments vis-à-vis market movements.

• The suggestion was not to change the existing rule.

Operational Procedures

– Full DSAs are expected to be prepared every three years and updated annually (risk ratings need to be provided annually), unless circumstances change significantly• Will take place only after we return to “normal” or “tranquil”

times

– Full DSAs should reflect the authorities’ views.• DSAs should be thoroughly discussed with the authorities

and the final DSA templates provided to them. A presentation of the authorities’ views in a separate short section would be desirable for DSAs to achieve their objectives.

41

• Framework for IDA’s response to non-concessional borrowing risks in grant-eligible and post-MDRI countries is adequate.

• While not a blanket restriction on non-concessional borrowing, it addresses the risk that such borrowing could lead to a rapid re-accumulation of debt and undermine debt sustainability

• Anticipates cases where non-concessional borrowing may be part of a financing strategy that helps promote economic growth, but also discourages non-concessional borrowing through financial disincentives

• IDA’s concessionality requirements are consistent with those of the IMF, but apply whether or not the country has a current IMF-supported arrangement.

IDA’s Policy towards LIC Non-concessional Borrowing

• IDA’s NCBP will require revision though changes on how the policy is implemented:

Countries would be evaluated every year based on the two criteria, and an annual waiver for some countries would be provided as opposed to the current practice of waivers for specific loans.

Countries that violate the aggregate concessionality or present value ceilings would be subject to the existing NCBP disincentives.

IDA’s response

IMF’s Previous policy : single design

• Purpose– Sustainable debt (size and rate of growth)

– Adequate external financing (concessional not covered)

• Institutional coverage and definition– Broad coverage: official PPG external debt– Definition: based on residency criterion

• Implementation– No restriction on concessional borrowing (minimum

concessionality requirement)

– No nonconcessional external borrowing with some exceptions (large-scale projects)

– Sectoral coverage varied: mainly central government.

44

IMF’s New Policy: more flexibility

• Purpose– Same but need to reflect diversity of

LICs

• Debt limit coverage– Clarification of institutional coverage

(SOEs)

– Residency and currency criterion– External and domestic debt

• More flexible approach (formal framework)

– Link to DSAs (stronger analytical underpinnings)

45

IMF’s Menu of Options

• Two dimensions (capture diversity)

1. Extent of debt vulnerabilities• Risk assessments and vulnerabilities

2. Macro and PFM capacity

• 2*2 ‘concessionality’ matrix

46

Concessionality Requirements-New IMF Matrix

47

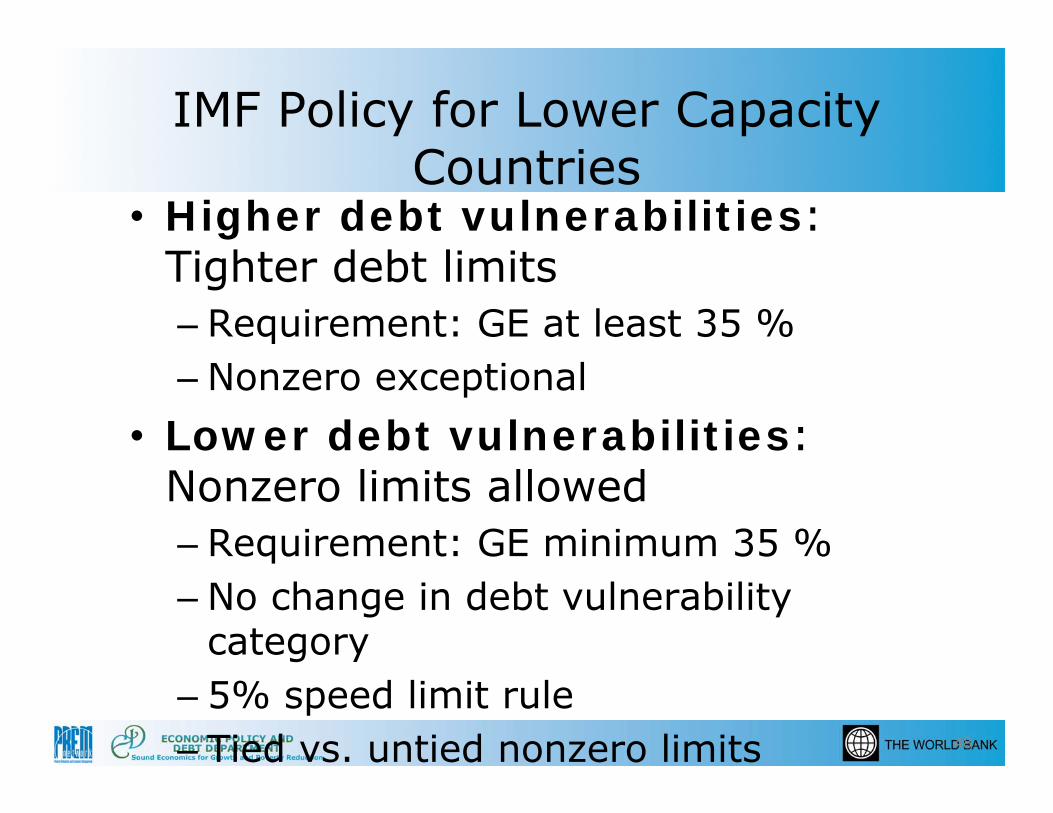

IMF Policy for Lower Capacity Countries

• Higher debt vulnerabilities: Tighter debt limits– Requirement: GE at least 35 %– Nonzero exceptional

• Lower debt vulnerabilities: Nonzero limits allowed– Requirement: GE minimum 35 %– No change in debt vulnerability

category– 5% speed limit rule– Tied vs. untied nonzero limits 48

IMF Policy for Higher Capacity Countries

• Higher debt vulnerabilities: PV target– Limit overall debt accumulation but;– Margin to maneuver on structure of

borrowing

• Lower debt vulnerabilities: Average concessionality target– Do no limit total borrowing– More flexible than PV target

49

For Further Information

• Information on the DSF and country DSAs can be found:

http://www.imf.org/dsa

http://www.worldbank.org/debt

• Write direct questions on DSAs and concessionality issues:

THANK YOU

02

46

8Pe

rcen

t

-.2 -.15 -.1 -.05 0 .05 .1 .15 .2 .25 .3allyrallc

years 2004-08

% of reversals 35%

Mean 0.011

Std. Dev. 0.075

N 229

% plus/minus 0.05 62%

Distribution of changes in the 3 yr average CPIA

How does the DSF Work

Note that the use of thresholds imply different probabilities of debt distress for countries with different CPIAs.

10%

15%

20%

25%

30%

35%

2.50 2.75 3.00 3.25 3.50 3.75 4.00 4.25 4.50

Probability of Debt Distress

CPIA