The Future of Fashion Retail

Abheek Singhi, Senior Partner and Director

15 March 2016

India Fashion Forum 2016.pptx 1Draft—for discussion only

Copyr

ight

© 2

016 b

y T

he B

osto

n C

onsultin

g G

roup,

Inc.

All

rights

reserv

ed.

Predictions about the future are dangerous..especially in the short run

Global financial crisis Elections 2009/2014.. Weather

India Fashion Forum 2016.pptx 2Draft—for discussion only

Copyr

ight

© 2

016 b

y T

he B

osto

n C

onsultin

g G

roup,

Inc.

All

rights

reserv

ed.

India's consumption to increase 3x this decade

INR '000 Cr

2010 2020

2,181

392

1,237

326

1,117

472

858

6,590

5,952

1,496

5,001

1,217

4,416

1,968

3,791

23,8343.6x

4.4x

4.2x

3.9x

3.8x

4.0x

3.8x

2.7xFood1

Clothes and footwear

Housing and Consumer

durable2

Health

Transport and

Communication

Education and Leisure3

Others4

TOTAL

1.Includes spend on Alcoholic beverages and tobacco (excludes food sold by catering services such as restaurants, hotels, kiosks, etc) 2.Includes spend on Utilities, homecare products, servant salaries, consumer durables, home renovation, rent3.Includes spend on Internet, entertainment (picnic, eating out, etc), children education 4.Include: Personal care, baby care, EMI, loan payment, Holidays, social gatheringsSource: Euromonitor, NSSO, India Retail Report; BCG Indian Consumer Survey, N=6278, BCG analysis

India Fashion Forum 2016.pptx 3Draft—for discussion only

Copyr

ight

© 2

016 b

y T

he B

osto

n C

onsultin

g G

roup,

Inc.

All

rights

reserv

ed.

Three big questions

Formats

Categories

Capabilities

India Fashion Forum 2016.pptx 4Draft—for discussion only

Copyr

ight

© 2

016 b

y T

he B

osto

n C

onsultin

g G

roup,

Inc.

All

rights

reserv

ed.

The ABCDE of what consumers want

E

Experience

A B

AvailabilityBreadth of

assortment

C D

Deals &

discountsConvenience

India Fashion Forum 2016.pptx 5Draft—for discussion only

Copyr

ight

© 2

016 b

y T

he B

osto

n C

onsultin

g G

roup,

Inc.

All

rights

reserv

ed.

The new consumer wants to break the compromise

Spend AND save

Traditional AND modern

Blend in AND be distinctive

Comfort AND style

Convenience AND experential

Touch and feel AND digital

India Fashion Forum 2016.pptx 6Draft—for discussion only

Copyr

ight

© 2

016 b

y T

he B

osto

n C

onsultin

g G

roup,

Inc.

All

rights

reserv

ed.

The rise of new categories will happen at the intersection

India Fashion Forum 2016.pptx 7Draft—for discussion only

Copyr

ight

© 2

016 b

y T

he B

osto

n C

onsultin

g G

roup,

Inc.

All

rights

reserv

ed.

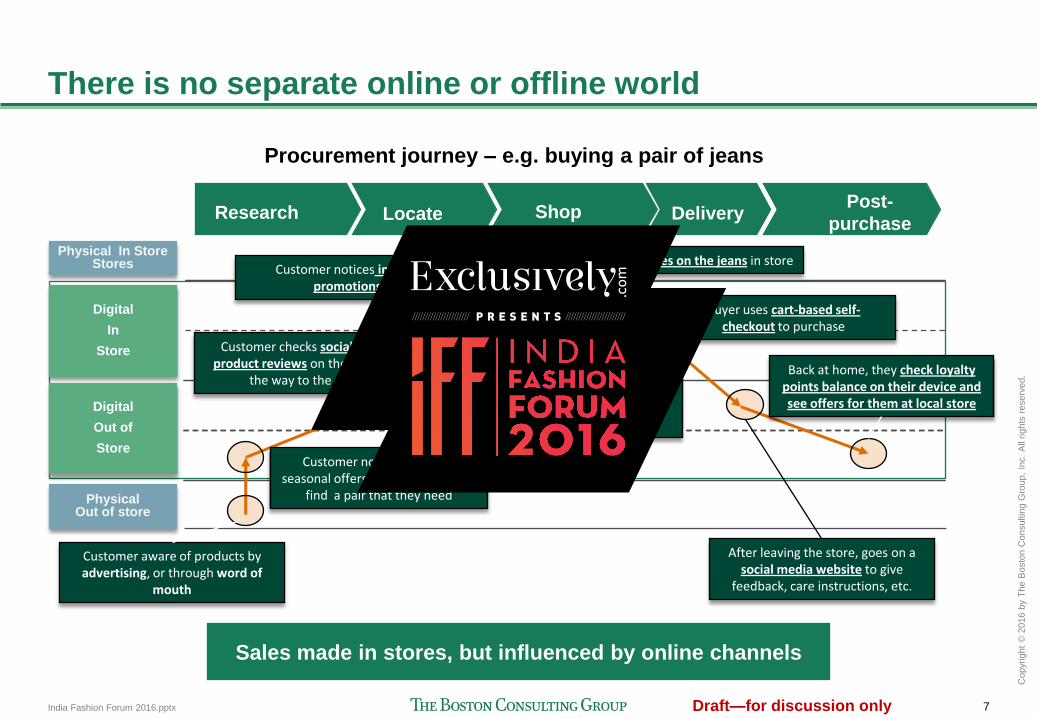

There is no separate online or offline world

Procurement journey – e.g. buying a pair of jeans

Physical In StoreStores

PhysicalOut of store

Digital

In

Store

Digital

Out of

Store

• Product information kiosks

After leaving the store, goes on a social media website to give

feedback, care instructions, etc.

Customer notices an ad for seasonal offers and goes online to

find a pair that they need

Customer aware of products by advertising, or through word of

mouth

Customer checks social media product reviews on their iPad on

the way to the storeCustomer uses an branded digital

App on mobile device to locate various jeans options in-store

Back at home, they check loyalty points balance on their device and see offers for them at local store

Buyer uses cart-based self-checkout to purchase

Customer notices in-aisle promotions

Sales made in stores, but influenced by online channels

Research Locate Shop Post-

purchaseDelivery

Customer tries on the jeans in store

India Fashion Forum 2016.pptx 9Draft—for discussion only

Copyr

ight

© 2

016 b

y T

he B

osto

n C

onsultin

g G

roup,

Inc.

All

rights

reserv

ed.

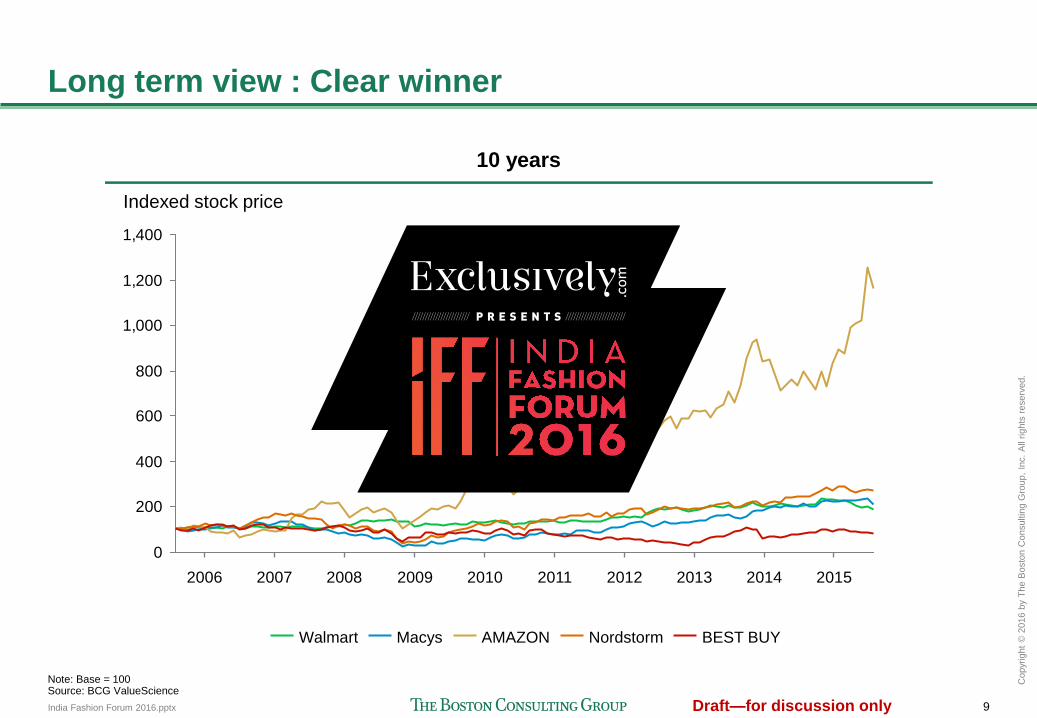

10 years

0

200

400

600

800

1,000

1,200

1,400

20102007 2009 201520142011 2012 201320082006

Indexed stock price

Walmart Macys NordstormAMAZON BEST BUY

Note: Base = 100Source: BCG ValueScience

Long term view : Clear winner

India Fashion Forum 2016.pptx 10Draft—for discussion only

Copyr

ight

© 2

016 b

y T

he B

osto

n C

onsultin

g G

roup,

Inc.

All

rights

reserv

ed.

0

50

100

150

200

250

300

350

400

450

20152014201320122011

Indexed stock price

AMAZON BEST BUYNordstormWalmart Macys

5 years

Medium term view : The answers change

Note: Base = 100Source: BCG ValueScience

India Fashion Forum 2016.pptx 11Draft—for discussion only

Copyr

ight

© 2

016 b

y T

he B

osto

n C

onsultin

g G

roup,

Inc.

All

rights

reserv

ed.

Retailers are going omni-channel

US : 8/10 of top e-comm players are

retailers

UK : 7/10 of top e-comm players are

retailers

1

2

3

4

5

6

7

8

9

10

1

2

3

4

5

6

7

8

9

10

India Fashion Forum 2016.pptx 12Draft—for discussion only

Copyr

ight

© 2

016 b

y T

he B

osto

n C

onsultin

g G

roup,

Inc.

All

rights

reserv

ed.

Winning in multi channel...

Zara's

new "green store"

• Store features the latest

advances in sustainability:

– Motion detectors to dim

lights when needed

– Thermostats to regulate

heating and cooling

– Air curtains at entrance

door to prevent hot or cold

air from entering

• Wood materials used inside

were sustainably harvested

New Balance's "experience

store"

• Store designed to reflect the

heritage and spirit of the

century-old brand

• Shoemakers assemble

sneakers in real time in the

upfront space of the store

• Each pair sold in special

“Assembled in NYC” bag

stamped with the edition

number and date made

Apartment 32's

"chic apartment store"

• Store resembles a chic city

apartment, featuring a couch

and kitchen counter

• Customers are referred to as

“house guests” and can relax

on a couch and sip espresso

while shopping

• Store has “no-talking on

smartphones rule"

Source: News searches, sprignwise.com

India Fashion Forum 2016.pptx 14Draft—for discussion only

Copyr

ight

© 2

016 b

y T

he B

osto

n C

onsultin

g G

roup,

Inc.

All

rights

reserv

ed.

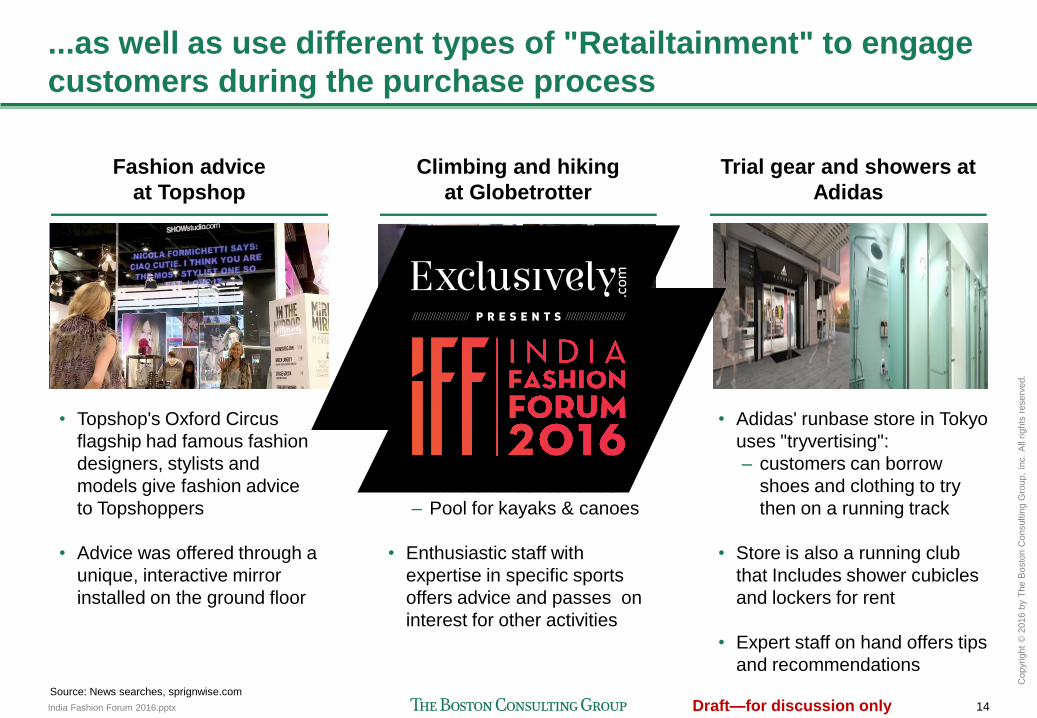

...as well as use different types of "Retailtainment" to engage

customers during the purchase process

Climbing and hiking

at Globetrotter

Fashion advice

at Topshop

Trial gear and showers at

Adidas

• Adidas' runbase store in Tokyo

uses "tryvertising":

– customers can borrow

shoes and clothing to try

then on a running track

• Store is also a running club

that Includes shower cubicles

and lockers for rent

• Expert staff on hand offers tips

and recommendations

Source: News searches, sprignwise.com

• Topshop's Oxford Circus

flagship had famous fashion

designers, stylists and

models give fashion advice

to Topshoppers

• Advice was offered through a

unique, interactive mirror

installed on the ground floor

• Globetrotter stores feature

experiential elements:

– Rock climbing wall

– Different floor surfaces

– Pool for kayaks & canoes

• Enthusiastic staff with

expertise in specific sports

offers advice and passes on

interest for other activities

India Fashion Forum 2016.pptx 16Draft—for discussion only

Copyr

ight

© 2

016 b

y T

he B

osto

n C

onsultin

g G

roup,

Inc.

All

rights

reserv

ed.

RTRWarby Parker Bonobos Birch Box

Move from the other side as well

India Fashion Forum 2016.pptx 18Draft—for discussion only

Copyr

ight

© 2

016 b

y T

he B

osto

n C

onsultin

g G

roup,

Inc.

All

rights

reserv

ed.

Lululemon

India Fashion Forum 2016.pptx 21Draft—for discussion only

Copyr

ight

© 2

016 b

y T

he B

osto

n C

onsultin

g G

roup,

Inc.

All

rights

reserv

ed.

The services and materials provided by The Boston Consulting Group (BCG) are subject to BCG's Standard Terms

(a copy of which is available upon request) or such other agreement as may have been previously executed by BCG. BCG does not

provide legal, accounting, or tax advice. The Client is responsible for obtaining independent advice concerning these matters. This

advice may affect the guidance given by BCG. Further, BCG has made no undertaking to update these materials after the date

hereof, notwithstanding that such information may become outdated or inaccurate.

The materials contained in this presentation are designed for the sole use by the board of directors or senior management of the

Client and solely for the limited purposes described in the presentation. The materials shall not be copied or given to any person or

entity other than the Client ("Third Party") without the prior written consent of BCG. These materials serve only as the focus for

discussion; they are incomplete without the accompanying oral commentary and may not be relied on as a stand-alone document.

Further, Third Parties may not, and it is unreasonable for any Third Party to, rely on these materials for any purpose whatsoever. To

the fullest extent permitted by law (and except to the extent otherwise agreed in a signed writing by BCG), BCG shall have no liability

whatsoever to any Third Party, and any Third Party hereby waives any rights and claims it may have at any time against BCG with

regard to the services, this presentation, or other materials, including the accuracy or completeness thereof. Receipt and review of

this document shall be deemed agreement with and consideration for the foregoing.

BCG does not provide fairness opinions or valuations of market transactions, and these materials should not be relied on or construed

as such. Further, the financial evaluations, projected market and financial information, and conclusions contained in these materials

are based upon standard valuation methodologies, are not definitive forecasts, and are not guaranteed by BCG. BCG has used public

and/or confidential data and assumptions provided to BCG by the Client. BCG has not independently verified the data and

assumptions used in these analyses. Changes in the underlying data or operating assumptions will clearly impact the analyses and

conclusions.

Disclaimer

Thank you

bcg.com | bcgperspectives.com