Download - THE DETERMINANTS OF EXCHANGE RATE IN NIGERIA

THE DETERMINANTS OF EXCHANGE RATE IN NIGERIA BY UDOYE, RITA A. PG/M.Sc/ 07/43765

BEING A RESEARCH PROJECT SUBMITTED TO THE DEPARTMENT OF

ECONOMICS, UNIVERSITY OF NIGERIA, NSUKKA IN PARTIAL

FULFILLMENT OF THE REQUIREMENTS FOR THE AWARD OF M.Sc IN

ECONOMICS

NOVEMBER, 2009.

i

TITLE PAGE THE DETERMINANTS OF EXCHANGE RATE IN NIGERIA.

ii

APPROVAL PAGE THE DETERMINANTS OF EXCHANGE RATE IN NIGERIA BY UDOYE, RITA A. PG/ M.Sc/ 07/ 43765 THIS PROJECT IS APPROVED BY THE DEPARTMENT OF ECONOMICS, UNIVERISTY OF NIGERIA, NSUKKA. __________________ _____________________ Prof. C.C Agu Prof. C.C Agu Supervisor Head of Department ____________________ External Examiner

iii

DEDICATION. This work is dedicated to God Almighty for His infinite mercies upon me. I also

dedicate this work to my husband, Mr L.O Udoye and to my children – Onyii,

Nelo, Chukwudi, Chibuzo, Nnemeka and Ogoo. May the blessings of the Lord

continue to abide with you all.

iv

ACKNOWLEDGEMENT I am very grateful to God for successful completion of this program.

I also acknowledge the help of my supervisor, Prof.C.C.Agu, whose advice,

guidance and understanding contributed immensely to the success of this work.

I am also greatly indebted to my brothers and sisters - Mary, Cordy, Vitus, Emeka

and my nephew - Tochukwu and many others. May God bless you all in Jesus

name, Amen.

Udoye, R.A. U.N.N.

v

ABSTRACT

The study examines the determinants of real exchange rate in the recent years in

Nigeria over the period of 1970 to 2006 using the Nigerian time series data.

Following literature, we identified the potential determinants of real exchange rate

as lag of real exchange rate, real interest rate, inflation rate, trade openness and

real gross domestic product. After examined the time series characteristics of the

data with Augmented Dickey-Fuller (ADF) unit roots test of stationarity and

Engle-Granger procedure for co-integration test, we applied Auto-regressive

Distributed Lag Model (ARDL-ECM). The result suggests that one year past value

of real exchange rate and immediate past value of trade openness are the major

determinants of real exchange rate in Nigeria. The result further indicates that

there is evidence of long run relationship between real exchange rate and two

explanatory variables (gross domestic product growth rate and trade openness).

vi

TABLE OF CONTENT TITLE PAGE ii APPROVAL PAGE iii DEDICATION iv ACKNOWLEDGEMENT v ABSTRACT vi TABLE OF CONTENT vii LIST OF TABLES ix CHAPTER ONE: INTRODUCTION 1 1.1 BACKGROUND INFORMATION 1 1.2 STATEMENT OF THE PROBLEM 3 1.3 OBJECTIVES OF THE STUDY 5 1.4 STATEMENT OF HYPHOTHESIS 5 1.5 JUSTIFICATION OF THE STUDY 6 1.6 SCOPE AND LIMITATION OF THE STUDY 6 CHAPTER TWO: LITERATURE REVIEW 7 2.0 THEORETICAL BACKGROUND 7 2.1 MODELS OF EXCHANGE RATE DETERMINATION 7 2.1.1 TRADITIONAL FLOW MODEL 7 2.1.2 THE PORTFOLIO BALANCE MODEL 8 2.1.3 THE MONETARY APPROACH 8 2.1.4 PURCHASING POWER PARITY (PPP) 9 2.1.5 BALANCE OF PAYMENTS APPROACH 9 2.1.6 EXCHANGE RATE REGIMES 10 2.1.7 CRAWLING PEG 10 2.1.8 ADJUSTABLE PEG EXCHANGE RATE 11 2.1.9 TARGET ZONE 12 2.1.10 CURRENCY PEG 12 2.2 BRIEF THEORETICAL REVIEW 13 2.3 AN OVERVIEW OF NAIRA EXCHANGE RATE MANAGEMENT 16 2.4 EMPIRICAL REVIEW 21 2.5 LIMITATION OF PREVIOUS STUDIES 28 2.6 EXCHANGE RATE MOVEMENTS IN NIGERIA 1975-2006 29

vii

CHAPTER THREE: METHODOLOGY 31 3.1 THE MODEL 31 3.2 MODEL SPECIFICATION 31 3.3 ESTIMATION PROCEDURE 32 3.4 UNIT ROOT TEST 33 3.5 CO-INTEGRATION TEST 34 3.6 TECHNIQUES OF RESULTS EVALUATION 35 3.7 MODEL JUSTIFICATION 35 3.8 DATA SOURCES 36 3.9 ECONOMETRIC SOFTWARE 36 CHAPTER FOUR: PRESENTATION AND INTERPRETATION OF RESULT 37 4.1 OVERVIEW 37 4.2 CO-INTEGRATION TEST 38 4.3 PRESENTATION OF DYNAMIC ECM MODELING OF REXCH RESULT 38 4.4 INTERPRETATION OF RESULT 39 4.5 COEFFICIENT OF DETERINATION R2 41 4.6 TEST OF AUTOCORRELATION 41 4.7 F-TEST 41 4.8 TESTOF MULTICOLLINEARITY 42 CHAPTER FIVE: SUMMARY, CONCLUSION AND POLICY RECOMMENDATION 43 5.1 SUMMARY AND CONCLUSION 43 5.2 POLICY RECOMMENDATION 44 5.3 CONCLUSION 46 REFERENCES 48 APPENDIX

viii

LIST OF TABLES 4.1 UNIT ROOT TEST 37 4.2 CO-INTEGRATION RESULT 38 4.3 RESULT SUMMARY 38 4.4 CORRELATION MATRIX 42

1

CHAPTER ONE

INTRODUCTION

1.1 Background Information

The exchange rate is the rate at which one currency is exchanged for another. It is

the price of one currency in terms of another currency ( Jhingan, 2005). Exchange

rate is the price of one unit of the foreign currency in terms of the domestic

currency. The debate over what determines the choice of exchange rate regimes

has continued unabated over some decades now. Friedman (1953) argued that in

the presence of sticky prices, floating rates would provide better insulation from

foreign shocks by allowing relative prices to adjust faster. His popular support for

floating exchange rate stipulates that in the long run the exchange rate system does

not have significant real consequences. His reasoning is that the exchange rate

system is ultimately a choice of monetary regimes. In the end, monetary policy

does not matter for real quantities, but in the short run it does. While Mundell’s

(1963) posits that in a world of capital mobility, optimal choice of exchange rate

regime should depend on the type of shocks hitting an economy: real shocks would

call for a floating exchange rate, whereas monetary shocks would call for a fixed

exchange rate.

�

Traditionally, it has been argued that a country’s optimal real exchange rate is

determined by some key macroeconomic variables and that the long-run value of

the optimal real exchange rate is determined by suitable (permanent) values of

these macroeconomic variables (Williamson, 1994). Incidentally, since the fall of

Bretton-Woods system in 1970s and the subsequent introduction of floating

2

exchange rates, the exchange rates have in some cases become extremely volatile

without any corresponding link to changes in the macroeconomic fundamentals.

This however has led to higher interest in exchange rate modeling as the question

of exchange rate determination reveals to be one of the most important problems

on theoretical field of monetary macroeconomics.

�

There are different types of exchange rate regimes practiced all over the world;

from the extreme case of fixed exchange rate system to a freely floating regime.

Practically, countries tend to adopt a combination of different regimes such as

adjustable peg, crawling peg, target zone/crawling bands, and managed float,

whichever that suits their peculiar economic conditions. For instance, exchange

rate managements in Nigeria has witness different significant changes over the past

four decades. Nigeria maintained fixed exchange rates from 1960 till the

breakdown of the Bretton Woods Monetary System in the early 1970s. Between

1970 and mid 1980 Nigeria exchange rate policy shifted from fixed exchange rate

to a pegged arrangement and finally, to the various types of the floating regime

since 1986 following the adoption of the Structural Adjustment Programme (SAP)

(see Sanusi, 2004).

A regime of managed float, without any strong commitment to defend any

particular parity, has been the predominant characteristic of the floating regime in

Nigeria since 1986. The changes from the different regimes are not peculiar to the

Naira as the US dollar was fixed in gold terms until 1971 when it was de-linked

and has since been floated. The fixed exchange rate regime induced an

overvaluation of the naira and was supported by exchange control regulations that

engendered significant distortions in the economy. That gave vent to massive

importation of finished goods with the adverse consequences for domestic

3

production, balance of payments position and the nation’s external reserves level.

Moreover, the period was bedeviled by sharp practices perpetrated by dealers and

end-users of foreign exchange. These and many other problems informed the

adoption of a more flexible exchange rate regime in the context of the SAP,

adopted in 1986 (Sanusi, 1988).

1.2 Statement of the Problem

Foreign exchange is said to be an important element in the economic growth and

development of a developing nation. Foreign exchange policies influence the

economic activities and to a large extent, dictate the direction of the macro-

economic variables in the country. The mechanism of exchange rate determination

are different systems of managing the exchange rate of a nation’s currency in

terms of other currencies and this should be properly done in a way that will bring

about efficient allocation of scarce resources so as to achieve growth and

development. Jhingan (2005) posited that to maintain both internal and external

balance, a country must control its exchange rate.

Optimal exchange rate policy is designed to obtain real exchange rate (RER) that

maintains both internal and external balance (Agu, 2002). The concept of real

exchange rate comes from a realization that the observable nominal exchange rate

movements, result from both price changes and inflation rate changes in trading

economies. When the real exchange rate is optimal, domestic producers of tradable

goods can compete internationally; imports are not artificially cheaper than

comparable domestic alternatives. Exporters also are not disadvantaged by the

exchange rate, when the real exchange rate is right (Maciejewski, 1983). What

determines the exchange rate regime for an open economy is one of the oldest

issues in international economics. The single most influential idea in this context

4

has been the Mundellian prescription that if shocks facing the country are mostly

monetary then fixed exchange rates are optimal whereas flexible rates are optimal

if the shocks are mostly real (Amartya et al.2004). The key friction underlying

Mundell’s results was the assumption of sticky prices in the goods market. Since

the fall of Bretton-Woods system in 1970s and the subsequent introduction of

floating exchange rates, the exchange rates have in some cases become extremely

volatile without any corresponding link to changes in other macroeconomic

variables. Nigeria’s exchange rate changes have been a subject of debate among

policy makers, concerned monetary authorities and academics because of the

recognition of the vital role exchange rate regime plays in the achievement of

sustainable growth. Government and monetary authorities in Nigeria, over the

years have done a lot of work in the area of finding the appropriate exchange rate

management, given the peculiarities of the economy. Since the adoption of the

Structural Adjustment Programme in 1986, Nigeria has adopted different types of

exchange rate regimes, ranging from floating exchange rate regimes to

fixed/pegged regimes.

However, maintaining a realistic exchange rate for the naira in Nigeria is very

crucial, given the structure of the economy. Sanusi (2004) opined the importance

of maintaining a realistic exchange rate for naira, and also the need to minimize

distortions in production and consumption, increase the inflow of non-oil export

receipts and attract foreign direct investment. This is expected to ensure that the

naira is not overvalued in real terms, and that the external sector remains

competitive. Nigeria in 1960 and in the early 1970s, maintained fixed exchange

rates. Between 1970 and mid 1980 Nigeria exchange rate shifted from fixed

exchange rate to a pegged arrangement and since the introduction of Structural

Adjustment Programme in 1986 till date Nigeria has adopted various types of

5

floating exchange regime (Sanusi 2004). The quest for a realistic naira exchange

rate made the Central Bank of Nigeria (CBN) in the time past to employ the

Purchasing Power Parity (PPP) model as a guide to gauge movements in the

nominal exchange rate and to determine deviations from the equilibrium exchange

rate. Although the PPP as a relative price does not provide clear criteria for

choosing a base period, and is generally criticized for its insensitivity to short-term

policy actions, it nonetheless, provides a reasonable framework for a comparative

analysis of trading partners’ performances. Nigeria, having adopted various types

of exchange rate mechanism over the years with Dutch Auction System (DAS)

being the latest and still the exchange rate did not maintain both internal and

external balance. Thus, the ultimate questions which this research seeks to answer

are: what determines exchange rate in Nigeria? Again, is there any long run

relationship between the exchange rate and its identified determinants in Nigeria?

1.3 Objectives of the Study

The general objective of this study is to investigate which of the macroeconomic variables best determine the real exchange rate in Nigeria. Specifically, the study will find out: 1. The determinants of exchange rate in Nigeria.

2. If there is any long run relationship between the exchange rate and its

identified�determinants in Nigeria.

1.4 Statement of Hypothesis

1. The determinants exchange rate in Nigeria is unknown?

2. There is no long run relationship between the exchange rate and its identified

determinants in Nigeria?

6

1.5 Justification of the Study

The policy thrust of the NEED document is to use the retail Dutch Auction System

to determine the nominal exchange rate regime, and adopt a wholesale Dutch

auction in the medium to long term (NEED 2004). This is in view of the fact that

the overall goal of monetary policy remains price and exchange rate stability.

Thus, economic relevance of studying the determinants of real exchange rate need

not be overemphasized. This study is imperative given the recent efforts by

monetary authorities in Nigeria to revive the economy through the financial sector

reform which among other things sought to maintain stability in exchange rate.

Consequently, this study will assist the nation’s economic planners in their

economic development planning. Specifically, the outcome of this study would

provide a basic understanding of the dynamics of exchange rate and the key

macroeconomic variables in Nigeria and it also contribute to knowledge.

1.6 Scope and Limitation of Study

This study shall cover the period of 1970-2006; a sample size of 36 years is long

enough for time series analysis. The choice of this period is largely informed by

data availability, and also due to the fact that Nigerian economy has practiced

different types of exchange rate regimes within the given period.

7

CHAPTER TWO

LITERATURE REVIEW

2.0 Theoretical Background

Exchange rate is the rate at which one country’s currency is exchanged for the

currency of another country (Dornbusch, 2004). It can also be defined as the price

of one country’s currency relative to other countries’ currency. While, Mankiw,

(1997) define it as the price at which exchange between two countries take place.

How to determine the exchange rate is issue that has taken the centre stage of

monetary and international economics. Monetary policy authority in Nigeria is

faced with the problems of having a stable and realistic exchange rate which is in

consonance with other macroeconomic fundamentals. This is because exchange

rate instability can have serious adverse consequences on prices, investments and

international trade decisions. A realistic exchange rate is one that reflects the

strength of foreign exchange inflow and outflow, the stock of reserves as well as

ensuring equilibrium in the balance of payments that is consistent with the cost and

price levels of trading partners (Ojo, 1998).

2.1 Models of Exchange Rate Determination

In general, three models theoretical foundations of exchange rate determination

exist; they include the traditional flow, the portfolio balance and the monetary

models of exchange rate

2.1.1 Traditional Flow Model

This model posits that exchange rate is simply determined by the market flow of

demand and supply of foreign exchange. Thus, there is equilibrium when the

supply equals the demand for foreign exchange. The model assumes that two basic

8

variables interact to determine the exchange rate. The variables are: relative

income and interest rate differential. This is justified since foreign demand for

domestic goods is a function of foreign income and vice versa, and also asset

demand depends on the difference between domestic and foreign interest rates.

2.1.2 The Portfolio Balance Model

This approach to exchange rate determination conceptualizes exchange rate as the

result of the substitution between money and financial assets in the domestic

economy and the substitution between domestic and foreign financial assets (CBN,

1998). Macdonald and Taylor (1992) posited that an exchange rate is determined

at least in the short-run by the supply and demand in the markets for wide range of

financial assets would not be automatic. This is an asset pricing view of the

exchange rate. The idea is that agents have a portfolio choice decision between

domestic and foreign assets. Those instruments (either money or bonds) have an

expected return that could be arbitraged. This arbitrage opportunity is what

determines the process of the exchange rate (Dornbusch, 1988).

2.1.3 The Monetary Approach

The shortfalls of the portfolio balance theory led to the development of the

monetary approach. This approach is based on the importance of money as a unit

of exchange, thus, it visualizes exchange rate as a function of relative shift in

money stock, inflation rate and domestic output, between a country and a trading

partner economy. Frankel (1978) posits that this model of exchange rate

determination attains equilibrium when existing stocks of money in the two

countries are willingly held. The monetary approach, under the flexible exchange

rate can be presented in two forms the monetary approach or the asset market

approach, and it emphasized on the role of money and other assets in determining

9

the exchange. Obioma (2000) holds the view that asset market or monetary

approach attributes variation in exchange rate essentially to income and expected

rates of return as well as to other factors that influence the supplies of and demands

for the various national monies. Thus, based on the fact that supply and demand for

monies is determined by the level of income, the monetary model postulates three

basic determinants of exchange rate as follows: relative money supplies, relative

income and interest rate differentials.

2.1.4 Purchasing Power Parity (PPP)

The purchasing power parity approach to the exchange rate determination was, and

continues to be, a very influential way of thinking about the exchange rate. The

PPP posits that the exchange rate between two currencies would be equal to the

relative national level prices. The PPP derives from the assumption that in the

world there exists the "law of one price". This law states that identical goods

should be sold at identical prices. (Note this assumption not law). The law of one

price implies that exchange rates should adjust to compensate for price differentials

across countries (Hoontrakul 1999). In other words, if we are in a bread-world

(only bread exists), and a bread is sold in US at 1 Dollar, and the same bread is

sold in Nigeria at 150 naira, then the exchange rate has to be 150 naira per Dollar.

2.1.5 Balance of Payments Approach

This approach of exchange rate determination is that there exists internal and

external equilibrium. The internal equilibrium assumes that there is full

employment: in it there is natural rate of unemployment. Or in other words, the

unemployment is such that there are no pressures to change real wages. The

external equilibrium refers to equilibrium in the balance of payments. This

approach explains permanent deviations of PPP. The main problem with this

10

approach is that in general it is extremely difficult to determine what is the exact

natural rate of unemployment, or the exchange rate that is consistent with

equilibrium of the external accounts. However, the model will determine where the

exchange rate has to converge to; however, it provides very little guidance to the

short term fluctuations (Hoontrakul 1999).

2.1.6 Exchange Rate Regimes

The options available to countries for adopting a particular exchange rate regimes

range from floating arrangements at one extreme to firmly fixed arrangements at

the other extreme, with the remaining regimes falling on a continuum in between.

These include pegs, target zones, and fixed but adjustable rates. As exchange rate

management have a defining goal of exchange rate stability, the fixed exchange

rate regime and its variants are more relevant. A fixed exchange rate system is one

in which exchange rates are maintained at fixed levels. Each country has its

currency fixed against another currency, and it is seldom changed. For example,

Nigeria maintained fixed exchange rates from the time of attainment of political

independence in 1960 till the breakdown of the Bretton Woods Monetary System

in the early 1970s. There are two major reasons why fixed exchange rates are

appealing. They are to promote orderliness in foreign exchange markets and

certainty in international transactions. Some of the variants of fixed exchange rates

are as follows:

2.1.7 Crawling Peg

This exchange rate arrangement is a middle course between fixed and flexible

exchange rates. It is appropriate for countries that have significant inflation

compared with their trading partners, as has often been the case in Latin America.

11

Under the crawling peg, the government fixes the exchange rate on any day but

over time adjusts the rate in a pre-announced fashion, taking into consideration the

inflation differentials between it and its major trading partners. Essentially, the peg

can be either passive, meaning that the exchange rate is altered in light of past

inflation, or active, whereby the country announces in advance the exchange rate

adjustments it intends to make. The advantage of this peg is that it combines the

flexibility needed to accommodate different trends in inflation rates between

countries while maintaining relative certainty about future exchange rates relevant

to exporters and importers. The disadvantage is that the crawling peg leaves the

currency open to speculative attack because the government is committed on any

one day or over a period to a particular value of the exchange rate.

2.1.8 Adjustable Peg Exchange Rate This refers to the system in which a national currency is pegged to a key currency,

for example, the U.S dollar, but the level of the peg could be changed occasionally,

albeit within a narrow band. This exchange rate regime features a strong exchange

rate commitment, and its adherents before the currency crises of the mid- and late

1990s, included Brazil, Mexico and Thailand. In these emerging market

economies, where capital mobility increased steadily during the 1970s and 1980s

and up to a high point in the 1990s, the authorities had difficulties in maintaining

the peg (Corden, 2001). However, it is still workable for countries that have low

capital mobility either because they are not integrated with the capital markets (like

some very poor countries) or because they have effective capital controls (e.g.

China).

12

2.1.9 Target Zone This is a compromise between floating rates and fixed but adjustable rates and is a

popular regime. Under it, a central rate that can be fixed, crawling or flexible is

surrounded by a band within which the central rate is permitted to float. It allows

for flexibility among a country’s policy objectives. It is also said to prevent

extreme movements in the exchange rate.

2.1.10 Currency Peg In a currency peg a local currency is pegged to an external currency, e.g., that of a

dominant trading partner or to a basket of currencies, with weights reflecting the

shares of the countries in foreign trade. Pegging to a single currency may yield a

number of advantages, one of which is the reduction in the exchange rate

fluctuations between the focus country and the country to which it is pegged. This

facilitates trade and capital flows between the two countries. One major weakness

of the single currency peg, however, is that where the currency is pegged to a

floating currency, e.g., the dollar, the local currency will float along with the dollar

vis-à-vis other currencies. Another disadvantage is that movements in the exchange

rate in relation to the currencies of other countries may interfere with domestic

macroeconomic policy objectives.

In an attempt to stabilize its effective exchange rate the developing country may

peg its currency to a basket of currencies. Often this entails the weighted average

of several currency values, the resulting exchange rate being total trade-weighted,

export weighted or import-weighted. One major advantage of pegging to a basket

is that a country may be able to avoid large fluctuations in its exchange rate with

respect to several trading partners’ currencies. Consequently, it is able to stabilize

13

its nominal effective exchange rate. Another advantage is that the system results in

the reduction of price instability which arises from exchange rate changes.

However, one major disadvantage of the basket peg is the determination of the

exchange rate without reference to the domestic policies of the pegging authorities.

Another is that a basket-weighted exchange rate, which, by definition, moves

against all major currencies, might reduce confidence on the part of foreign

investors and reduce capital inflows.

2.2 Brief Theoretical Review Given the potential impact of exchange rate on inflation prices, investment,

balance of payment, and interest rate, the issue of the determination of optimal

exchange rate becomes imperative for the successful implementation of

development programmes in the country. Chuka, (1990) argues that the objectives

of exchange rate policy are to increase output and its optimal distribution. A

necessary condition for the achievement of the above objectives is that the

exchange rate should be stable as possible. According to him, stability permits

viability of the rate in response to changes in relative prices, international terms of

trade and growth factors.

Exchange rate policy involves choosing an exchange rate system and determining

the particular rate at which foreign transaction will take place. Exchange rate

policy affects growth by determining capital flow, foreign investment and external

balance for most developing countries. The inadequacy of foreign exchange

constitutes a bottle neck in the process of development. In the course of

development, the rate of growth of national output and the demand for imports

tend to exceed export based capacity. Therefore, there is a conflict between

accelerating internal development and maintaining external balance. This conflict

14

is resolved by a realistic exchange rate policy. Exchange rate policy by devaluation

or over-valuation has an implication for an economy. Devaluation help to improve

the external competitiveness either through contraction in imports or expansion in

exports and this influences both consumption and investment decision. Over-

valuation of foreign exchange exacerbate external borrowing, balance of payment

disequilibrium and the distortion of the economy, while under valuation results in

income distortion detrimental to labour, trade, current account surpluses, standard

of living and the growth of the economy (Sodersten, 1997).

The basic element of efficient exchange rate system is the assumption that

exchange rate reflects the relative productivity of an economy (Obadan, 2003). In

the long-term, the devalued Naira protects domestic industries, encourages

domestic production, reduction in the cost of imported raw materials and makes

domestically produced goods competitive.

Several factors influencing the choice of a particular exchange rate regime in a

country, a major consideration is the internal economic conditions or

fundamentals, the external economic environment and the effect of various random

shocks on the domestic economy. Thus, countries like Nigeria which are

vulnerable to unstable internal financial conditions and external shocks, (including

terms of trade shocks, and excessive debt burden), which require real exchange

rate depreciation, tend to adopt a regime which ensures greater flexibility. Overall,

there is a general consensus that a fixed exchange rate regime is preferred if the

source of macroeconomic instability is predominantly endogenous. Conversely, a

flexible regime is preferred if disturbances are predominantly exogenous in nature.

It is, nevertheless, becoming increasingly recognized that whatever exchange rate

regime a country may adopt, the long-term success depends on its commitment to

15

the maintenance of strong economic fundamentals and a sound banking system

(see Sanusi, 2004).

Meese, and Rogoff (1990) maintains that the floating exchange rate was adopted in

developing countries from 1973 and the question of whether exchange rate

changes/uncertainties have independent adverse effect on transaction of a country

have attracted a lot of literature. According to them, the introduction of adjustment

programmes by many of these countries and the attendant liberalization of

exchange rates have brought the discussion of this work further into global focus.

Economists are divided over whether government’s arguments for managing

exchange rate rest on three points firstly, the government can determine the

fundamental equilibrium exchange rate. Secondly, floating exchange rate has been

too volatile. Thirdly under floating exchange rate currencies can become

significantly over-valued or undervalued. The first and third points are related.

Williamson, (1994) proclaim that the supporters of floating exchange rates points

out that exchange rate volatility may or may not have adverse effect on favorable

terms of trade depending on it’s effect on import. Therefore exchange rate

volatility or fluctuation can be positive or negative.

Taylor, (1995) in his work stated quite categorically what became known as

purchasing power parity theory that the value of a foreign currency in terms of

another depends mainly on the relative purchasing power of the two currencies in

their respective countries. In other words, the exchange rates settles at the level

which make purchasing power of a given unit of currency the same in what ever

country it is spent. He argues further that the theory fails in some areas like a

16

change in the exchange rate may originate in factor independent of price level.

Therefore the purchasing power parity is not a complete explanation of what

determines exchange rate but this does not mean that the theory has no value.

Krueger, (1983) maintains that in a completely free exchange market, exchange

rate would fluctuate freely in response to varying demand for the different

currencies; with fluctuating demand for currencies. Large savings in foreign

exchange rate could be expected especially since capital movement affect

exchange rate as directly as do merchandise export and imports. On the other hand,

as long as supply and demand for various currencies remains responsibly in

balance, stable exchange rate would prevail under free exchange markets. In

addition, Krueger, (1983) argues that how the exchange is determined depends on

whether the rate is a fixed exchange rate or floating exchange rate. A fixed

exchange rate is an exchange rate that is set by government decree or intervention

within a small range of variation. A floating exchange rate is freely determined by

the interaction of supply or demand.

2.3 An Overview of Naira Exchange Rate Management

Before the introduction of Structural Adjustment Programme (SAP) in 1986, the

naira exchange rate remained fixed. That is, the rate was fixed vis-à-vis the US and

UK’s dollar and pound sterling respectively. Although this was in line with the

global practice on exchange rate determination then, the system was found to be

fraught with high distortions leading to inefficiencies and misallocation of

resources. It observed that exchange rate in Nigeria did not become a policy

instrument until late 1988 like other developing countries. The Naira exchange rate

was pegged initial to the British pound sterling and subsequently to the United

States dollar as part of global exchange rate management under the Bretton woods

17

system. Here in, the naira exchange rate could be changed only in response to a

prolonged disequilibrium.

The Nigeria pound has its parity defined in June 1962 in terms of gold at one

Nigerian pound to 2.48828 grams for fine gold. From that time to August 14, 1971,

the exchange rate of the Nigerian pound of the use dollar was determined by its

gold parity. The Naira replaced the pound as Nigerian currency in 1973, and its par

value was set at half that of the pound. Hence the exchange rate against the dollar

became US $ 1.52 to the Naira. Within a month of this the US dollar was

devalued by 10 percent and Nigeria suit with a 10 percent matching devaluation,

thereby maintaining the existing Naira-dollar rate. During most of 1973, the

anchor currencies, the dollar and sterling weakened considerably, sustained

weakness brought into sharp focus the dilemma, inherent in the method of

determining the exchange rate of the Nigerian currency.

However, in September, 1986, the Second Tier Foreign Exchange market (SFEM)

began as a dual exchange rate system which produced the official first tier rate and

the SFEM or free market rate. The former was administratively determined and

gradually depreciated. It applied to a few official international organizations the

free market rate which applied to other transactions. The free market rate which

applied to other transactions was determined by the market forces of demand

supply within the framework of a foreign exchange auction system. The essence

of the dual exchange rate system was to avoid a deliberate uniform and sizeable

devaluation of the Naira but to allow it to depreciate in the SFEM while at the

same time the monetary authorities continued a downward adjustment of the first

tier rate until the two rates converge to produce a realistic exchange rate.

18

This convergence which Ojamenaye (1991) has described was achieved on July 2,

1987 at an exchange rate of N3.74: $1.00. With this development, the first tier

market was abolished and unified foreign exchange market (FEM) with a single

rate that came into being. The FEM also embraced the autonomous market, which

was allowed to develop. The autonomous segment of the FEM was expected to be

competitive with the parallel foreign exchange market and thus be attractive to

exporters to repatriate their proceeds.

The introduction of the autonomous market led to the existence of three exchange

rates - FEM, rate autonomous and the parallel market rate which failed to show any

tendency toward convergence. And as Akinmoladun (1990) has argued the merger

of the first tier rate and the SFEM rate was more technical than real as shortly after

the gap between the auction rate and those of the autonomous market rates began

to grow at one point, there was more than 50 percent differential between the two

rates and this became a source of concern for the monetary authorities. The price

differential had the effect of making the auction funds sort of subsidized.

The operations of the autonomous market later became destabilizing arising from

the tendency towards high arbitrage premium and accusations of authorized dealers

of diverting official funds making substantial gains effortlessly (Ojo, 1991). Other

malpractices also developed as the market officials or authorized dealers were

accused of corruption and allocation of foreign exchange to favored customers.

In the light of these, the autonomous market was merged with the official segment

in January 1989 and the Inter-Bank Foreign Exchange Market (IFEM) was

introduced. The IFEM entailed a daily bidding system under which the central

Bank injected official funds into the market by way of direct sales to the banks as

and when funds were available. Various but specific methods were used (single or

19

combined) to determine rates. The daily bidding system was characterized by

spurious demands for foreign exchange and it came to an end on the 13th

December, 1990. The following day, the CBN reintroduce the Dutch Auction

System (DAS) on a weekly basis.

The system continued throughout 1991. It may be recalled that the Dutch auction

system was first introduced in 1988, but was later replaced by IFEM. The DAS

was originally introduced to enhance professionalism in the FEM and prevent

outrageous rate which invariably led to the continued depreciation of the naira.

The system did not achieve this goal. For example, the naira showed heavier

deprivation in 1991 compared to the relative stability of the exchange rate in 1990

(Obadan, 1992). The exchange rate management system appeared to have been

predicated on various methods that are yet to achieve the desired goal. Not only

has there been a metamorphosis of the institutional framework from SFEM to FEM

to IFEM, there have been frequent changes in the operational guidelines. Besides

the Dutch Auction System, the market has experimented among which various

techniques and operational procedures among which are the average and marginal

exchange rate determination or fixed methods, the weekly, fortnight and daily

bidding system.

In January 1999, Nigeria’s dual exchange rate regime was abandoned as the

official N22 to a dollar exchange rate was scrapped. Prior to then, the official rate

co-existed with the rates on the Autonomous Foreign Exchange Market (AFEM)

and was used for selected government transactions including external debt service.

From then, the prevailing rate on the AFEM applied to all foreign exchange

transactions. The elimination of the dual exchange rate system introduced

uniformity of price in foreign exchange transactions and eliminated the arbitrage

20

opportunities created by having an overvalued official rate side-by-side with a

market determined rate. It also introduced more transparency into government

financial transactions as only the President previously had the right to determine

which transactions were to be conducted at the official rate. In October 1999, a

daily Inter-Bank Foreign Exchange Market (IFEM) replaced the AFEM. Under the

IFEM, the CBN monopoly on the supply of foreign exchange was removed as oil

exploration and producing companies were allowed to sell foreign exchange

directly to banks rather than through the CBN. The CBN however remains the

principal supplier of foreign exchange in the market and exerts considerable

influence on the determination of the exchange rate. In July, 2002, Nigeria

reintroduced a bi-weekly Dutch auction system (DAS) as an operational system for

its foreign exchange market to replace the inter bank foreign exchange market

(IFEM).

The DAS is a method of exchange rate determination through auction where

bidders pay according to their bid rates where the ruling rate is an arrived at with

the last bid rate that clears the market. In short, contrary to the old IFEM system,

where supply of currency was elastic at some given rate, take or leave some

allowance for depreciation when demand was perceived to be too large, under the

DAS the exchange rate is mainly determined by bids made by commercial banks

on behalf of their clients. So the move back to a DAS indicates that Nigeria seems

to be wishing for more, rather than less, flexibility in the exchange rate and leads

one to think that Nigeria appears to be opting for the last monetary regime

solution: stable prices and a freely floating exchange rate.

21

2.4 Empirical review

Jimoh, (2006) examines the Nigerian data from 1960 to 2000 to see what support it

provides for traditional theory of real exchange rate. He used the well-known

Johanson’s (1992) methods for estimating models whose variables are non-

stationary but co integrated, the study found that the decisive trade liberalization

programme of 1986 – 87 led to about 13 per cent depreciation in the Nigerian real

exchange rate and made the real rate more responsive to changes in its terms of

trade. He also found out that less decisive changes in trade regime produced no

significant changes in the real exchange rate.

Shehu and Aliyu (2006) estimate the long run behavioral equilibrium exchange

rate in Nigeria. They used quarterly data from 1984Q1 to 2004Q4 and derive a

Behavioral Equilibrium Exchange Rate (BEER) and a Permanent Equilibrium

Exchange Rate (PEER). Regression results show that most of the long-run

behavior of the real exchange rate could be explained by real net foreign assets,

terms of trade, index of crude oil volatility, index of monetary policy performance

and government fiscal stance. On the basis of these fundamentals, four episodes

each of overvaluation and undervaluation were identified and the antecedents

characterizing the episodes were equally traced to the archive of exchange rate

management in the country within the review period. Among others for instance,

large inflow of oil revenues into the country and stable macroeconomic

performance were discovered to account for undervaluation of the real exchange

rate between 2001Q1 and 2004Q4 in Nigeria. The results further suggest that

deviations from the equilibrium path are eliminated within one to two years.

Agnès and Coeuré (2001), in their paper “The Survival of Intermediate Exchange

Rate Regimes show how the traditional trade off between stabilization and

22

disinflation can produce soft pegs as optimal exchange rate regimes even when

financial fragility and the cost of regime switches in terms of credibility are taken

into account. The optimal degree of exchange rate flexibility depends on the

structural characteristics of the country and on the preferences of monetary

authorities. The finding is confirmed by cross-section logit estimation for 92

countries before and after the 1997-1998 emerging markets crises, relating

exchange rate regime choice with the countries structural patterns. The model

correctly predicts up to 86% of observed regimes and some of the recent moves

towards hard pegs.

Devereux and Engel (1988) directly examine how price setting affects the optimal

choice of exchange rate regime. They find that when prices are set in consumers’

currency, floating exchange rates always dominate fixed exchange rates. When

prices are set in producers’ currency, there is a trade-off between floating and fixed

exchange rates. Exchange rate adjustment under floating rates allows for a lower

variance of consumption, but exchange rate volatility itself leads to a lower

average level of consumption. The implication from the simple analysis of their

study indicates that, if the exchange rates is volatile, fixing exchange rates to both

US dollar and Japanese Yen is better than floating, because both US and Japanese

exporters set the price in producers’ currency.

Again, Devereux and Engel (2000) investigate the choice of exchange-rate regime

– fixed or floating in a dynamic, intertemporal general equilibrium framework.

They used an extended Devereux and Engel (1998) framework to investigating the

implications of internationalized production. They examine the role of price setting

– whether prices are set in the currency of producers or the currency of consumers

– in determining the optimality of exchange-rate regimes in an environment of

23

uncertainty created by monetary shocks. They find that when prices are set in

producers’ currencies, floating exchange rates are preferred when the country is

large enough, or not too risk averse. On the other hand, floating exchange rates are

always preferred when prices are set in consumers’ currencies because floating

exchange rates allow domestic consumption to be insulated from foreign monetary

shocks. The gains from floating exchange rates are greater when there is

internationalized production in this case.

Engel (2000) examines optimal exchange-rate policy in two-country, he used

sticky-price general equilibrium models in which households and firms optimize

over an infinite horizon in an environment of uncertainty. The models are in the

vein of the “new open-economy macroeconomics” as exemplified by Obstfeld and

Rogoff (1995). The conditions under which fixed or floating exchange rates yield

higher welfare, or the optimal foreign exchange intervention rule, depend on the

exact nature of price stickiness and on the degree of risk-sharing opportunities. The

study provides some preliminary empirical evidence on the behavior of consumer

prices in Mexico that suggests failures of the law of one price are important. The

evidence on price setting and risk-sharing opportunities is not refined enough to

make definitive conclusions about the optimal exchange-rate regime for that

country.

Amartya et al (2004) revisits the issue of the optimal exchange rate regime in a

flexible price environment. The key innovation is that he analyze the question in

the context of environments where only a fraction of agents participate in asset

market transactions (i.e., asset markets are segmented). He shows that flexible

exchange rates are optimal under monetary shocks and fixed exchange rates are

optimal under real shocks. These findings are the exact opposite of the standard

24

Mundellian prescription derived under the sticky price paradigm wherein fixed

exchange rates are optimal if monetary shocks dominate while flexible rates are

optimal if shocks are mostly real. This result thus suggests that the optimal

exchange rate regime should depend not only on the type of shock (monetary

versus real) but also on the type of friction (goods market friction versus financial

market friction).

Chuka, (1990) show in its study of optimal exchange rate determination that there

is no such thing as ''the'' optimal or best exchange rate policy. It all depends on the

underlying fundamentals, which may be both domestic and external, as well as

perceptions of policy credibility. How countries react to them will not be the same

at all. Floating the currency would, of course, be deemed to be better than the other

approaches but questions need to be answered as to, among others, whether the

country has sufficient reserves to intervene in the market at all times when it is

necessary. In the case of Malawi, this has proved to be very difficult since the

availability of foreign exchange is highly seasonal. He concludes that Malawi also

faces another problem in that public confidence in the floating regime is taking

rather long to stabilize with the consequence that the kwacha is constantly under

speculative attacks.

Kildegaard (2005) examines the role of structural factors in Mexican real exchange

rate experience since 1970, particularly in the crisis of December, 1994. He finds

that fundamental determinants of the real exchange-omitted from previous research

are co integrated with nominal exchange rates and relative prices, while tests of

PPP alone fail. The co integrating equation indicates a severe undervaluation

during the 1980s and only modest overvaluation in the period immediately

preceding the devaluation in December, 1994. The author concludes that nothing in

25

the fundamentals can account for magnitude of the blow Mexico suffered at that

time.

El-Mefleh (2004) investigates the proper exchange rate system that serves main

macroeconomic goals within increasing integrated global financial markets. The

major findings of the study are that (1) It is unrealistic to assume that one exchange

rate regime is the best for all circumstances and for all countries; (2) The choice of

pegging the currency to another currency or a basket of currencies depends on the

degree of trade concentration with another country (country B) and the currency in

which the country’s (country A) foreign debt is mostly denominated; and (3) The

managed float or free float system is more realistic for a country highly integrated

into global financial markets.

Barnett and Kwag (2005) incorporate aggregation and index number theory into

monetary models of exchange rate determination in a manner that is internally

consistent with money market equilibrium. Divisia monetary aggregates and user-

cost are concepts used for money supply and opportunity-cost variables in the

monetary models. They estimate a flexible price monetary model, a sticky price

monetary model, and the Hooper and Morton (1982) model for the US dollar/UK

pound exchange rate. They compare forecast results using mean square error,

direction of change, and Diebold-Mariano statistics. They find that models with

Divisia indexes are better than the random walk assumption in explaining the

exchange rate fluctuations.

Leo (2006) explores the welfare implications of a small country’s exchange rate

regime, for the small country itself, as well as for a large country, the currency of

which the small country potentially pegs to. A two-country dynamic stochastic

26

general equilibrium model is developed for the analysis. Floating exchange rate

regimes was modeled as Taylor type interest rate rules, with different feedback

coefficients on inflation and output. He shows that compared to a fixed exchange

rate regime, both countries will be worse off if the small country adopts an interest

rate rule with a large feedback coefficient on output and a small feedback

coefficient on inflation. He also shows that it is important for the small country not

to respond to output fluctuations in its interest rate rule, as it will generate costly

fluctuations of inflation.

Batini and Levine (2006), in their study of Optimal Exchange Rate Stabilization in

a Dollarized Economy with Inflation Targets shows that First, dollarization

complicates the conduct of monetary policy; however monetary policy can still be

carried out successfully and with low costs in terms of real activity under

dollarization if the central bank commits to an inflation target. Thus, introducing

an inflation target in partially dollarized economies can reduce the cost of price

stabilization. Second, even if the degree of dollarization depends endogenously on

the response of monetary policy from the exchange rate, it is still desirable to

‘smooth’ the exchange rate, in addition to correcting deviations of expected

inflation from target. In this sense, an optimal simple rule for a partially dollarized

is different from that of a non-dollarized economy, in that in the former economy

there are substantial gains from including an exchange rate term in the rule,

contrary to common findings on similar rules for non dollarized economies.

Abstracting from the many other adverse consequences of dollarization, the

findings show that countries with no credibility may benefit from partial

dollarization in that it constrains monetary policy to be conservative. Third,

exchange rate smoothing reduces the chances of multiple equilibria under

dollarization.

27

Faia, (2005) study the optimal choice of exchange rate regimes in a two country

model with sticky prices and matching frictions in the labour market. Currency

fluctuations by affecting the price of tradable goods tend to exacerbate movements

in and out of the labour market and the volatility of vacancy creation which in turn

tend to increase overall macroeconomic volatility. For this reason and despite the

well-known insulating properties of currency fluctuations the monetary authority

(Faia, 2005) can accomplish domestic stabilization and increase welfare by having

exchange rate as an independent target in the monetary policy rule. The study also

shows that the model presented is compatible with well-known stylized facts of

both the international transmission of shocks (such as positive co-movements of

output and employment) and of the labour market (such as the Beveridge curve,

the procyclicality of labour market tightness and the high volatility of labour

market variables).

Benigno and Benigno (2004) propose a theory of exchange rate determination

under interest rate rules. They show that simple interest-rate feedback rules can

determine a unique and stable equilibrium without any explicit reaction to the

nominal exchange rate in their two-country optimizing model with sticky prices.

They characterize how the behavior of the exchange rate and the terms of trade

depend crucially on the monetary regime chosen, though not necessarily on

monetary shocks. They give a simple account of exchange rate volatility in terms

of monetary policy rules; they provide an explanation of the relation between

nominal exchange rate volatility and macroeconomic variability in terms of the

monetary regime adopted by monetary authorities.

Bruno and Pugh (2006) studied the trade effects of exchange rate variability on

international economies for the past 30 years. The study applies meta-regression

28

analysis (MRA). They find that, on average, exchange rate variability exerts a

negative effect on international trade. In addition, MRA helps to explain the wide

variation of results in this literature ranging from significantly positive to

significantly negative effects and suggests new lines of enquiry. In particular, their

results suggest a regime effect, whereby the trade effect of exchange rate

variability is conditioned by the institutional environment.

Kandil (2004) examines the effects of exchange rate fluctuations on real output

growth and price inflation in a sample of twenty-two developing countries. The

analysis introduces a theoretical rational expectation model that decomposes

movements in the exchange rate into anticipated and unanticipated components.

The model demonstrates the effects of demand and supply channels on the output

and price responses to changes in the exchange rate. In general, exchange rate

depreciation, both anticipated and unanticipated, decreases real output growth and

increases price inflation. The evidence confirms concerns about the negative

effects of currency depreciation on economic performance in developing countries.

2.5 Limitation of Previous Studies

From the avalanches of literature reviewed, we observed the following;

First, most studies on exchange rates either focused on the impact of exchange rate

volatility on trade or on growth.

Second, majority of the studies were done outside the shore of this country. This

led us to venture into the research.

29

Third, majority of the studies on the determinant of exchange rate did not consider

the possibility of long run relationship between exchange rate and their

macroeconomic variables (determinants), although, Shehu and Aliyu (2006)

estimate the long run behavioral equilibrium exchange rate in Nigeria using

quarterly data from 1984Q1 to 2004Q4. Suffice it to say that this period is too

short to access the long run behaviour of exchange rate and its macroeconomic

variables since most time series econometricians suggest the minimum of 25 years

observation for time series data.

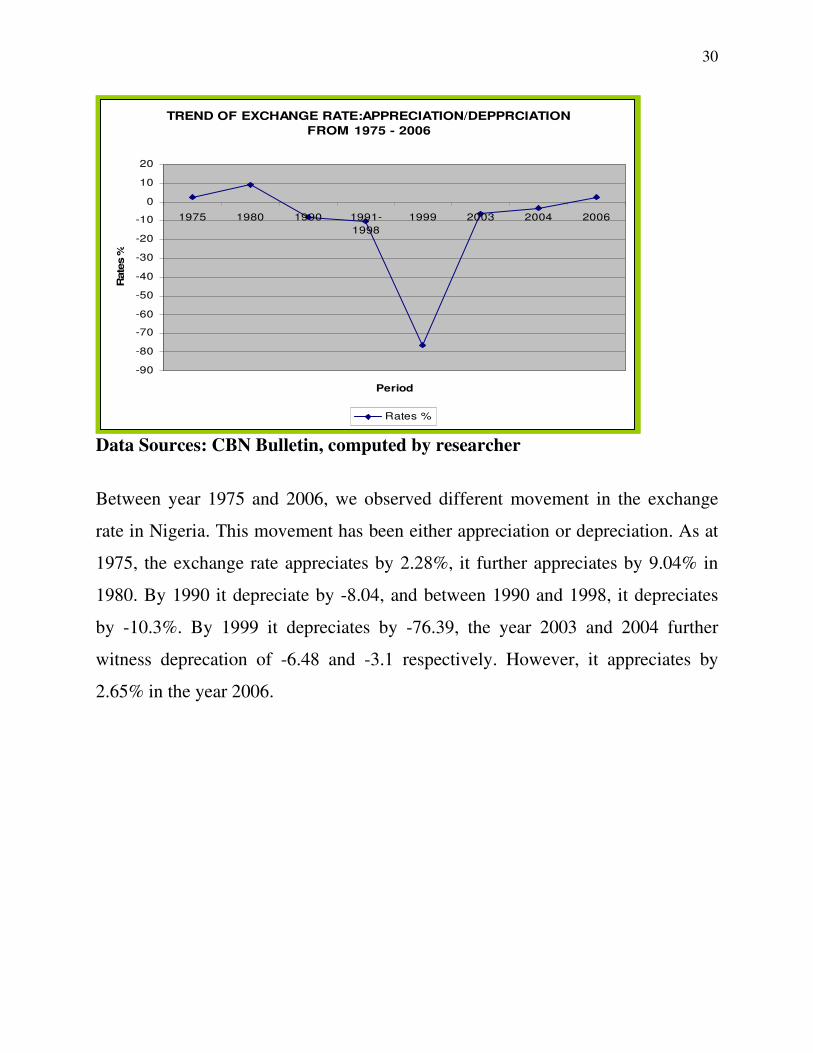

2.6 Exchange rate Movements in Nigeria 1975-2006

Exchange Rate: Appreciation/Depreciation

Year 1975 1980 1990 1991-1998 1999 2003 2004 2006 Rates of change in % 2.28 9.04 -8.04 -10.3 -76.39 -6.48 -3.1 2.65 Computed from CBN Bulletin 2006

-80 -70 -60 -50 -40 -30 -20 -10

0 10

Rates %

1975 1980 1990 1991- 1998

1999 2003 2004 2006

Period

EXCHANGE RATE: APPRECIATION/DEPPRECIATION FROM 1975 - 2006

Rates %

30

TREND OF EXCHANGE RATE:APPRECIATION/DEPPRCIATION FROM 1975 - 2006

-90

-80

-70

-60

-50

-40

-30

-20

-10

0

10

20

1975 1980 1990 1991-1998

1999 2003 2004 2006

Period

Rat

es %

Rates %

Data Sources: CBN Bulletin, computed by researcher

Between year 1975 and 2006, we observed different movement in the exchange

rate in Nigeria. This movement has been either appreciation or depreciation. As at

1975, the exchange rate appreciates by 2.28%, it further appreciates by 9.04% in

1980. By 1990 it depreciate by -8.04, and between 1990 and 1998, it depreciates

by -10.3%. By 1999 it depreciates by -76.39, the year 2003 and 2004 further

witness deprecation of -6.48 and -3.1 respectively. However, it appreciates by

2.65% in the year 2006.

31

CHAPTER THREE

METHODOLOGY

3.1 The model

The study will follow a simple linear specification of the multivariate time series

function using the partial adjustment approach to estimating given parameters of a

model. In so doing, Autoregressive Distributed Lag Model (ADLM) shall be used.

This is because past value of exchange is likely to determine the present value and

also the relationship between exchange rate and macroeconomic fundamentals that

determine it are likely to be dynamic in nature. That is, these determinants may

transmit beyond the present period. Consequently, The ADLM model will allow

the joint estimation of relationships between exchange rate and the

macroeconomics variables. Furthermore, there may be the need for us to transform

the model into an Autoregressive Distributed Lag Error Correction (ADL-ECM)

Model if at any point in time; there is evidence of co-integration among the

variables. The ECM will help to capture both the long run and the short run

dynamics of exchange rate and macroeconomics variables (See Engle and Granger,

1987).

3.2 Model Specification

Following the argument of Williamson, (1994) that a country’s optimal real

exchange rate is determined by its macroeconomic fundamentals (i.e. some key

macroeconomic variables) and that the long-run value of the real exchange rate is

determined by suitable (permanent) values of these fundamentals, we formulate the

determinant of real exchange rate in Nigeria as follows;

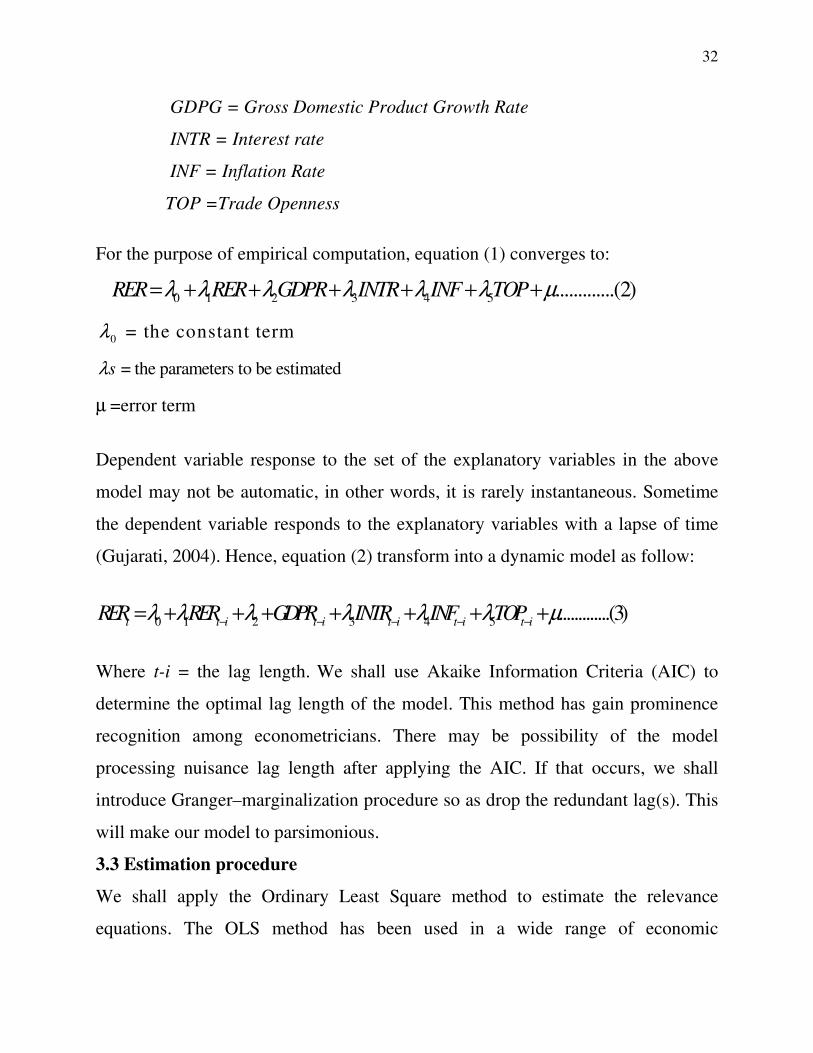

( ), , , ...................(1)RER F GDPR INTR INF TOP=

where

RER = Real Exchange Rate

32

GDPG = Gross Domestic Product Growth Rate

INTR = Interest rate

INF = Inflation Rate

TOP =Trade Openness

For the purpose of empirical computation, equation (1) converges to:

0 1 2 3 4 5 .............(2)RER RER GDPR INTR INF TOPλ λ λ λ λ λ µ= + + + + + +

0 = the constant termλ = the parameters to be estimatedsλ

µ =error term

Dependent variable response to the set of the explanatory variables in the above

model may not be automatic, in other words, it is rarely instantaneous. Sometime

the dependent variable responds to the explanatory variables with a lapse of time

(Gujarati, 2004). Hence, equation (2) transform into a dynamic model as follow:

0 1 2 3 4 5 .............(3)t t i t i t i t i t iRER RER GDPR INTR INF TOPλ λ λ λ λ λ µ− − − − −= + + + + + + +

Where t-i = the lag length. We shall use Akaike Information Criteria (AIC) to

determine the optimal lag length of the model. This method has gain prominence

recognition among econometricians. There may be possibility of the model

processing nuisance lag length after applying the AIC. If that occurs, we shall

introduce Granger–marginalization procedure so as drop the redundant lag(s). This

will make our model to parsimonious.

3.3 Estimation procedure

We shall apply the Ordinary Least Square method to estimate the relevance

equations. The OLS method has been used in a wide range of economic

33

relationship with satisfactory result. The method employs a sound statistical

technique appropriate for empirical problems; and it has become so standard that

its estimates are presented as a point of reference even when result from other

estimation technique are used. More so, the reliability of this method lies on its

desirability properties which are efficiency, consistency and unbiased. This implies

that its error term has a minimum and equal variance. The conditional mean value

is zero and normally distributed (Gujarat, 2004).

3.4 Unit Root Test

Conventionally, the universal assumption in building and testing economic models

that underlies variables are stationary, but is unfortunately not generally true.

Before estimating our model in equation (3), we shall check for the time series

properties of the data. This is necessary because time series econometricians such

as Granger and Newbold, (1974); Eagle and Granger, (1987), Dickey and Fuller,

(1981); Enders, (1995); Pindyck and Rubinfeld, (1998),among others, observed

that results emanating from most macroeconomic variables are likely to be

“Spurious” if the time series properties of such series are not examined. Hence, the

time series properties of the data would be examined using Augmented Dickey

Fuller (ADF) test and the Engle-Granger co-integration procedure.

The testing procedure for the ADF is as follows:

0 1 1 1 ... .........(4)t t t p t p tRER t RER RER RER Uλ β γ δ δ− − −∆ = + + ∆ + ∆ + + ∆ +

where

�0 is a constant, �t is the coefficient on a time trend and p is lag order of the

autoregressive process and � is difference operator. The unit root test is then

carried out under the null hypothesis � = 0 against the alternative hypothesis of � <

0. If the test statistic is greater (in absolute value) than the critical value let say at

34

5% or 1% level of significance, then the null hypothesis of � = 0 is rejected and no

unit root is present.

From the above discussion, our model in equation (3) becomes;

0 1 2 3 4 5 .............(5)t t i t i t i t i t iRER RER GDPR INTR INF TOPλ λ λ λ λ λ µ− − − − −∆ = + ∆ + ∆ + ∆ + ∆ + ∆ + Where, � is the difference operator. 3.5 Co-integration Test

If RER and the explanatory variables are linked by some long-run relationship,

from which they can deviate in the short run but must return to in the long run, the

residuals obtain from their linear combination will be stationary. If the variables

diverge without bound (i.e. non-stationary residuals) we must assume no

equilibrium relationship exists. In other words, if RER and any of the explanatory

variable(s) are both integrated of order d (i.e. I(d)), then, in general, any linear

combination of the RER and any of the explanatory variables will also be I(d); that

is, the residuals obtained from regressing RER on the explanatory variable(s) are

I(d). Should the residual is stationary it implies there is evidence of long run

relationship among the variables. Hence our model in equation (5) becomes;

0 1 2 50 0 0

... ........(6)n n n

t t t t t t i Iti i i

REX REX GDPG TOPλ λ λ λ β µ µ−= = =

∆ = + ∆ + ∆ + + ∆ + +∑ ∑ ∑

Where;

11 −t

uβ = Error Correction Representation

1

β = Coefficient measuring the degree of error corrected

Hence, the model in equation (6) is the Autoregressive Distributed Lag Error

Correction Model (ADLECM) we hope to estimate if there is evidence co-

integration among the variables. On the contrary, if there is no co integration

35

among the variables we shall estimate the Autoregressive Distributed Lag Model

specified in equation (5). 3.6 Techniques of Results Evaluation

We shall use three basic criteria to evaluate the results obtain from the model;

economic (a priori expectations), statistical and econometric criteria. The economic

criteria will inform us if the signs of the variables coefficient conform to economic

theory. While the Statistical criteria shall focus on testing the significance of the

variables using T-test, and F-statistic will be used to assess the joint significance of

the overall regression in order to see whether the model is well specified. In the

same, the econometric criterion would involve such tests as autocorrelation and

multicollinear. The autocorrelation will help to check for the existence of serial

correlation among the variables, while the multicollinear test would help to check

if the variables are collinear.

3.7 Model Justification

There are varieties of model available to econometricians/researchers when

modeling. However the choice of a particular model is base on reliability,

effectiveness and adequacy of the model. Thus among the numerous rival models,

we opted for Autoregressive Distributed Lag Error Correction model (ADLM-

ECM). The choice of this model is informed by the fact that, apart from the

efficiency of the ADLM, it will also help to draw inferences about dynamic

behavior of the variables since it has been established that it take lapse of time for

the dependent variables to response to the explanatory variables when modeling.

Also, the ECM will be most appropriate and efficient model that can capture the

long run behavioral pattern of variables under co-integration situation (See Enders,

36

1995). Lastly, the model will take care of the problem of the so-called “spurious”

regression associated with non-stationary data.

3.8 Data Sources

The data for this study are secondary in nature. They shall be obtained from the

Central Bank Nigeria Statistical Bulletin 2006 publication

3.9 Econometric software

We shall use PC-GIVE software, for the analysis after the data must have been

loaded into Microsoft Excel worksheet and then imported into the PC-GIVE.

37

CHAPTER FOUR

PRESENTATION AND INTERPRETATION OF RESULT

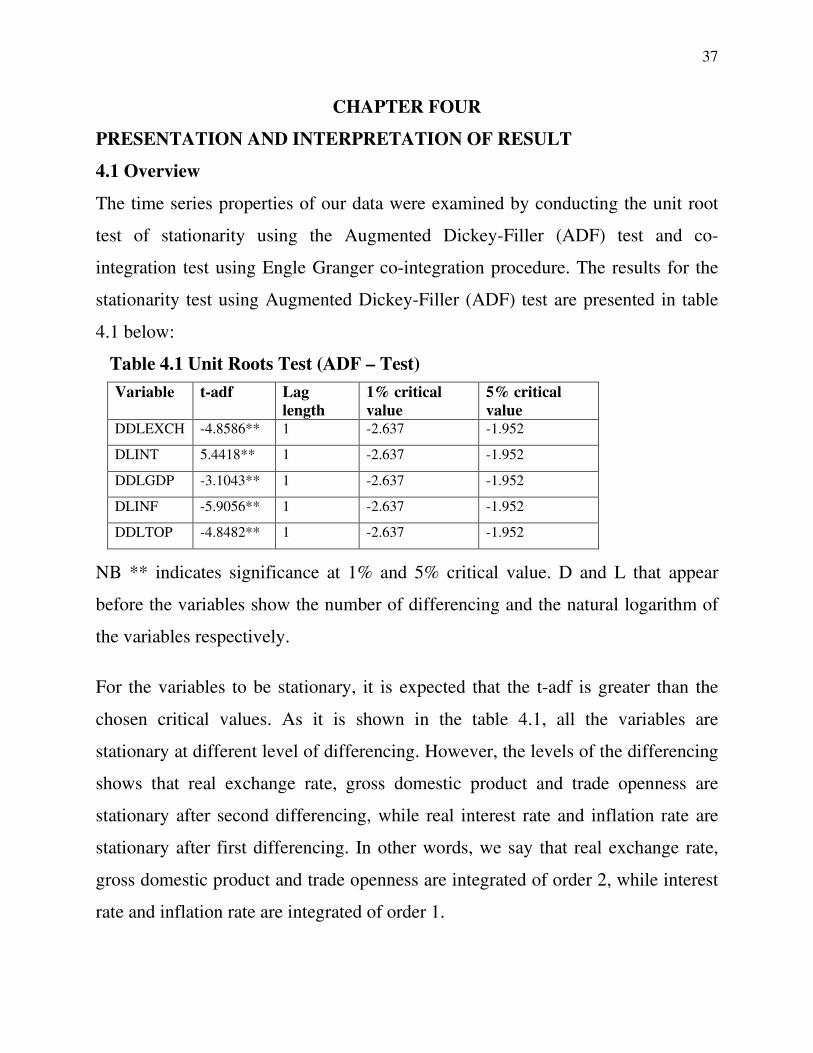

4.1 Overview

The time series properties of our data were examined by conducting the unit root

test of stationarity using the Augmented Dickey-Filler (ADF) test and co-

integration test using Engle Granger co-integration procedure. The results for the

stationarity test using Augmented Dickey-Filler (ADF) test are presented in table

4.1 below:

Table 4.1 Unit Roots Test (ADF – Test) Variable t-adf Lag

length 1% critical value

5% critical value

DDLEXCH -4.8586** 1 -2.637 -1.952

DLINT 5.4418** 1 -2.637 -1.952

DDLGDP -3.1043** 1 -2.637 -1.952

DLINF -5.9056** 1 -2.637 -1.952

DDLTOP -4.8482** 1 -2.637 -1.952

NB ** indicates significance at 1% and 5% critical value. D and L that appear

before the variables show the number of differencing and the natural logarithm of

the variables respectively.

For the variables to be stationary, it is expected that the t-adf is greater than the

chosen critical values. As it is shown in the table 4.1, all the variables are

stationary at different level of differencing. However, the levels of the differencing

shows that real exchange rate, gross domestic product and trade openness are

stationary after second differencing, while real interest rate and inflation rate are

stationary after first differencing. In other words, we say that real exchange rate,

gross domestic product and trade openness are integrated of order 2, while interest

rate and inflation rate are integrated of order 1.

38

4.2 Co integration test

From the unit root test in table 4.1, we noticed that real exchange rate which is the

dependent variable in the specified equations have the same order of integration

with gross domestic product and trade openness which are independent variables,

we then estimated their linear combination without the constant term and obtain

their residual which was tested for unit root test of stationary using Augmented

Dickey Fuller. The outcome of the test is given below: Table 4.2 co integration result

t-adf lag 5% critical value

1% critical value

Residual -3.0838** 2 -1.951 -2.632

Residual -2.8096** 1 -1.951 -2.632

Residual -3.1688** 0 -1.951 -2.632

The result shows the existence of co-integration among the variables because the

residual obtained from the linear combination of none stationary series is stationary

at both 5% and 1% critical values. Hence there is necessity to estimate an Error

Correction Model (ECM) that is the model in equation number (6).

4.3 Presentation of Dynamic ECM modeling of REXCH result

Table 4.3 Result Summary

Variables Coefficient Std.Error T-value T-prob Part YR ˆ

CONSTANT 0.049238 0.054465 0.904 0.3754 0.0343

DDLEXCH_1 -0.42343 0.16501 -2.566 0.0173 0.2226

DLINT 0.35261 0.27102 1.301 0.2061 0.0686

DLINT_1 0.22703 0.26289 0.864 0.3967 0.0314

DDLGDP 0.079066 0.2148 1.276 0.2148 0.0661

DDLGDP_1 0.38623 0.27671 1.396 0.1761 0.0781

DLINF -0.10849 0.070760 -1.533 0.1389 0.0927

39

DLINF_1 -0.15561 0.078079 -1.993 0.0583 0.1473

DDLTOP -0.0072796 0.13445 -0.054 0.9573 0.0001

DDLTOP_1 -0.37950 0.17008 -2.231 0.0357 0.1779

ECM_1 -0.012684 0.0041802 -3.034 0.0059 0.2859

R2 =0.660298, DW = 1.86, F-Stat (10, 23) = 4.4706

4.4 Interpretation of Result

From the result, the constant term is positive, even though it does not have any

economic meaning, it meet our a priori expectation. That is if other variable that

contribute to real exchange rate is zero, there are other variables that can contribute

in a positive or negative way to real exchange rate

The lag value of real exchange rate has a negative and significant relationship with

real exchange rate. The result shows that a 10% increase in the past value of real

exchange rate leads to 42% decrease in real exchange rate. The t-value of -2.566

which is greater than absolute 2 using a 2-t Rule of Thumb is statistically

significant suggest that the past one year value of real exchange rate is a major

determinant of real exchange rate in Nigeria.

The current and immediate past year value of real interest has a direct relationship

with real exchange rate. A 10% increase in real interest in the current and previous

one year leads to 35% and 0.22% increase in real exchange rate respectively. The

positive sign display by real interest rate meet economic apriori expectation since

interest rate differentials will affect the equilibrium exchange rate. A rise in

Nigeria interest rates relative to other countries rates all things being equal, will

cause investors to switch from their currency to Naira-denominated securities to

take advantage of the higher Naira rates. The net result will be depreciation of the

Naira in the absence of government intervention. However, the result indicates that

40

real interest is not a major determinant of real exchange rate in Nigeria as shown

by its t-values of 1.301 and 0.864 which are statistically insignificant.

Similarly, gross domestic product growth rate has a direct and insignificant

relationship with real exchange rate both in the current and previous year. From the

regression result, a 10% increase in gross domestic product growth rate causes real

exchange rate to increase by 7.9% and 38% in the current year and immediate past

year respectively. The positive signs display by real gross domestic product growth

rate meet economic a priori expectation. This is because a nation with strong

economic growth will attract investment capital seeking to acquire domestic assets.

The demand for domestic assets in turn will results in an increased demand for the

domestic currency and a stronger currency, other things being equal. Empirical

evidence supports the hypothesis that economic growth should lead to a stronger

currency. Conversely, nations with poor growth prospects will see an exodus of

capital and weaker currencies. However, the result shows that gross domestic

product growth rate is not statistically significant in the analysis showing that it is

not a major determinant of real exchange rate in Nigeria.

Inflation rate displays a negative insignificant relationship with real exchange rate

both in the current year and past one year. From the regression result, a 10%

increase in inflation rate causes 10% and 15% decrease in real exchange rate in the

current and immediate past year respectively. Notwithstanding, inflation rate is not

a significant factor that determine country real exchange rate.

Surprisingly, while trade openness both at the current and past one year value has a

negative relationship with real exchange rate, the current year value is insignificant

in determine real exchange rate, while the past one year value appeared to be one

of the major determinant of real exchange in Nigeria. According to the regression

41

result, a 10% increase in trade openness in the current and previous year leads to

0.72% and 37% decrease in real exchange rate respectively. The fact that trade

openness is statistically significant in determine real exchange rate suggests the

important of external factors in the determination of real exchange rate in Nigeria

and the fact that trade openness is expected to transmits its impact through

unexpected changes in the exchange rate.

4.5 coefficient of determination R2

In the error correction model, we expect a lower R2, given that the dependent

variable is differenced. Given the parsimonious specification, the size of the R2 is

impressive. The R2 is 0.660298 shows that the explanatory variables (lag of real

exchange rate, real interest rate, inflation rate, and gross domestic product growth

rate) explained 66% of the total variation in real exchange rate.

4.6 Test of Autocorrelation

The underlying assumption of autocorrelation is that the successive values of the

random Mi are temporally independent. The convectional Durbin Watson d

statistics is employed. Since DW which is 1.86 is close 2 rather than zero, we

conclude that there is autocorrelation.

4.7 F- test

We also conducted the f-test to check for model adequacy.

Hypothesis formulation

H0: the model is well specify

H1: there is misspecification of model

Decision Rule: If F-tabulated > F-calculated, we accept H0,

F (11, 21) =4.4706 and F- Table =2.65

42

Since the F-calculated of 4.4706 is greater than the F-tabulated of 2.65 at 5% level

of significance, we accept H0 and reject H1. Thus we concluded that the model is

good and well specified.

4.8 Test of Multicollinearity

We used the correlation matrix table in test for multicollinearity among the

variables. Gujarati, (2004) states that two explanatory variables is said to be

multicollinear if the pair –wise or zero – order correlation coefficient of the

variables is in excess of 0.8.

Table 4.4 Correlation Matrix

VARIABLE DDLEXCH DLINT DDLGDP DLINF DDLTOP DDLMS

DDLEXCH 1.000

DLINT 0.2705 1.000