- 1 -

Cable Television: The Industry Today and Its Outlook for the Future

1. Markets for streaming content and triple play service

An important feature of today’s cable television industry is the rapid advancement of

broadcasting services using communications technology. Smart televisions combining video

and internet services and linking television and mobile terminals are growing increasingly

popular in areas where mobile broadband and mobile terminals are in wide use. Firms are

competing to provide the most user-friendly experience in terms of the freedom to choose

viewing time, place, and package, in addition to the upper-layer content which has long been a

major part of cable television’s appeal (Figure 1).

Figure 1 Diversification of Content Audience

Summary

The cable television industry is facing enormous changes in the telecommunications and

broadcasting markets and in the technological landscape as well. Multichannel broadcasters

are experiencing sluggish growth, and even internet operators, which had proved strong until

now, are being forced by fierce competition into exploring new business strategies. Struggling

to cope with the advent of broadband, smart television, and other new services, growing

numbers of cable television firms are turning to alliances to boost their competitiveness. How

these strategic alliances will be implemented, both by firms and communities, is a matter of

keen interest throughout the industry.

This paper is a summary of the report Present State of the Cable Television Industry, FY 2012

Edition (“the FY 2012 Report”).

Source: Development Bank of Japan Inc.

MobileBroadband

(LTE・WiMAX・WiFi)

Television PC

Platform

Transmission

Terminal

STB

Content(Apps)

TabletPC

OSWeb

User

BS,CS

D

T

T

Unidirectional

=Information access, entertainment, etc.

Bidirectional

=Communication

CATV FTTH・DSL

Stick

Wi-Fi

Smartphone

- 2 -

① The multichannel market

IP multicast broadcasting has driven growth in the multichannel market for the past

several years. If IP multicast were omitted, FY 2012 results would be level with those of

the previous year (Figure 2). The number of cable subscribers showed a decline of 0.1%

year-on-year, greatly reducing its contribution to the growth of the multichannel market.

The precipitous fall in cable subscriptions is a trend that bears watching.

Figure 2 Changes in the Multichannel Market (Subscriber Households)

② The broadband market

Fiber-to-the-home (FTTH) drove growth in the broadband market until about 2010. Since

2011, however, a huge increase in subscriptions to 3.9 generation mobile telephone

terminal packets (long-term evolution, or LTE) has brought new growth to the broadband

market (Figure 3). Mobile broadband (such as WiMAX), including broadband wireless

access (BWA), is rapidly becoming the chief driver of growth in this market.

Figure 3 Changes in the Broadband Market (Subscriber Households)

Source: Ministry of Internal Affairs and Communications; Hoso Journal - sha Inc.; Corporate investor relations materials

Source: Ministry of Internal Affairs and Communications

5.5%

-10%

0%

10%

20%

30%

40%

50%

60%

0

10

20

30

40

50

60

70

04 05 06 07 08 09 10 11 12

Million households

3.9-generation mobile telephone packet communication (LTE)BWA (WiMAX, etc.)FTTHDSLCATVFWA (fixed wireless access)Growth rate (right scale)

FY

-2%

0%

2%

4%

6%

8%

10%

12%

14%

16%

0

5

10

15

20

01 02 03 04 05 06 07 08 09 10 11 12

Million households

IP multicastCATVSKY PerfecTVWOWOWMultichannel total (excluding IP multicast)CATV

※Growth rates are comparisons with same month of previous year.

FY

- 3 -

③ The telephone market

The number of landline subscriptions peaked in 1998 and has since been on a gradual

decline (Figure 4). While OABJ-IP subscriptions have increased, the falling number of NTT

subscriptions has kept the number of landline subscribers as a whole on the decline.

Mobile telephone subscriptions, on the other hand, are showing strong and steady

growth, the number reaching 131 million as of the end of fiscal year 2012. Growing

numbers of users are replacing their landlines with mobiles, and signs point to a greater

presence for LTE as a mobile broadband circuit. The spread of smartphones in the past

few years has brought a proliferation of free applications; it will be interesting to see what

kind of impact these will have on the telephone industry.

Figure 4 Changes in Numbers of Landline Subscribers

2. Trends in cable television businesses

① Broadcasting

The FY 2012 Report is based on responses from some 150 cable television operators

across Japan. In FY 2012, the multichannel subscription rate was 20.4% per company,

continuing a year-on-year decline in the number of subscribing households (Figure 5).

The number of households acquiring or cancelling multichannel subscriptions maintained

sluggish growth (for MSOs1) or went into a slight decline (for non-MSOs) (Figure 6). 1

Multiple system operator: A company owning multiple cable systems.

Notes 1. Source: Ministry of Internal Affairs and Communications 2. IP telephone services provided by CATV operators are counted under IP telephones.

56.8

131.7

24.1

0

3

6

9

12

15

0

20

40

60

80

100

120

140

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Landline telephone

Mobile telephone

Of which, NTT subscribers

Of which, 0ABJ-IP telephone

Of which, dedicated line (right scale)

Of which, CATV telephone (right scale)

Million Million

FY

- 4 -

Figure 5 Changes in Numbers of Multichannel Subscriber Households

and Subscription Rates, Per Firm (n = 96)

Figure 6 Changes in Multichannel Acquisitions/Cancellations, Per Firm

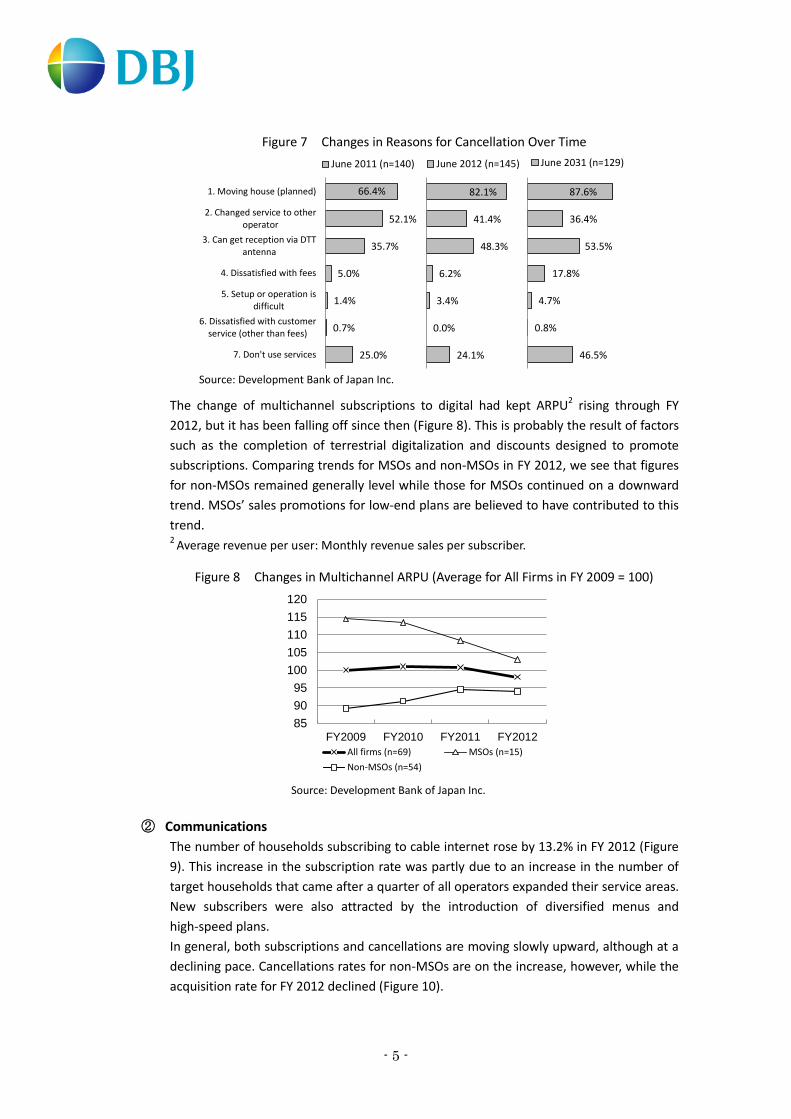

When questioned as to the reasons for the cancellation of services, the greatest number

of respondents replied that it was due to the subscribers’ “moving house.” The

percentage of respondents giving this answer was particularly high among MSOs, which

operate primarily in urban areas (Figure 7). The reason “Don’t use these services” showed

sharp growth in the current fiscal year, probably due at least in part to the diversification

of tastes that has come with the spread of smartphones and similar devices.

Source: Development Bank of Japan Inc.

Source: Development Bank of Japan Inc.

112 118 121 122

24.3 24.6 24.8 24.9

21.6%20.8% 20.5% 20.4%

15%

20%

25%

30%

0

50

100

150

FY2009 FY2010 FY2011 FY2012

Thousand households

Target households Subscriber households Subscription rate (right scale)

18,778 18,934 19,037 19,024

6.3% 7.1% 6.4% 6.9% 4.7% 4.7%

1,185 1,341 +156 1,211 1,314 +103 900 887 -13

10

20

30

FY2009 Cancellations Acquisitions FY2010 Cancellations Acquisitions FY2011 Cancellations Acquisitions FY2012

Thousand households

46,418 47,447 48,256 48,747

12.0% 14.2% 10.8% 12.5% 9.7% 10.7%

5,573 6,602 +1,029 5,134 5,943 +809 4,657 5,148 +491

10

20

30

40

FY2009 Cancellations Acquisitions FY2010 Cancellations Acquisitions FY2011 Cancellations Acquisitions FY2012

Thousand households

Net growth rate+2.2%

Net growth rate+1.7%

Net growth rate+1.0%

Net growth rate+0.8%

Net growth rate+0.5%

Net growth rate-0.0%

MSO (n=19)

Non-MSO (n=77)

- 5 -

Figure 7 Changes in Reasons for Cancellation Over Time

The change of multichannel subscriptions to digital had kept ARPU2 rising through FY

2012, but it has been falling off since then (Figure 8). This is probably the result of factors

such as the completion of terrestrial digitalization and discounts designed to promote

subscriptions. Comparing trends for MSOs and non-MSOs in FY 2012, we see that figures

for non-MSOs remained generally level while those for MSOs continued on a downward

trend. MSOs’ sales promotions for low-end plans are believed to have contributed to this

trend. 2

Average revenue per user: Monthly revenue sales per subscriber.

Figure 8 Changes in Multichannel ARPU (Average for All Firms in FY 2009 = 100)

② Communications

The number of households subscribing to cable internet rose by 13.2% in FY 2012 (Figure

9). This increase in the subscription rate was partly due to an increase in the number of

target households that came after a quarter of all operators expanded their service areas.

New subscribers were also attracted by the introduction of diversified menus and

high-speed plans.

In general, both subscriptions and cancellations are moving slowly upward, although at a

declining pace. Cancellations rates for non-MSOs are on the increase, however, while the

acquisition rate for FY 2012 declined (Figure 10).

85

90

95

100

105

110

115

120

FY2009 FY2010 FY2011 FY2012

All firms (n=69) MSOs (n=15)

Non-MSOs (n=54)

Source: Development Bank of Japan Inc.

Source: Development Bank of Japan Inc.

82.1%

41.4%

48.3%

6.2%

3.4%

0.0%

24.1%

June 2012 (n=145)

66.4%

52.1%

35.7%

5.0%

1.4%

0.7%

25.0%

1. Moving house (planned)

2. Changed service to otheroperator

3. Can get reception via DTTantenna

4. Dissatisfied with fees

5. Setup or operation isdifficult

6. Dissatisfied with customerservice (other than fees)

7. Don't use services

June 2011 (n=140)

87.6%

36.4%

53.5%

17.8%

4.7%

0.8%

46.5%

June 2031 (n=129)

- 6 -

Figure 9 Changes in Numbers of Cable Internet Subscriber Households

and Subscription Rates, Per Firm (n = 102)

Figure 10 Changes in Cable Internet Acquisitions/Cancellations, Per Firm

From FY 2009 through FY 2012, the average ARPU for all firms displayed a downward

trend. The decline was especially large in FY 2012 (Figure 11). Notably, MSO operators

saw their year-on-year ARPU drop steeply that year. The reason is thought to be sales

strategies stressing customer retention, along with intense competition from telecom

operators.

Looking at plans with the greatest number of subscribers over the last five years, we see a

drop in the percentage of operators offering 2Mbps, the slowest speed, combined with a

sustained rise in the percentage of those offering 20Mbps, the fastest speed – both signs

of a general transition from slow- to high-speed plans (Figure 12).

115 117 120 121

13.8 14.6 15.3 15.9

12.0%12.5%

12.8%13.2%

10%

11%

12%

13%

14%

15%

0

50

100

150

FY2009 FY2010 FY2011 FY2012

Thousand households

Target households Subscriber households

Source: Development Bank of Japan Inc.

Source: Development Bank of Japan Inc.

26,875 28,858 30,273 32,254

12.7% 20.1%12.6% 17.5% 12.5% 19.1%

3,422 5,405 +1,983 3,623

5,038 +1,415 3,790 5,771 +1,981

10

20

30

FY2009 Cancellations Acquisitions FY2010 Cancellations Acquisitions FY2011 Cancellations Acquisitions FY2012

Thousand households

10,603 11,157 11,688 11,9238.1% 13.3% 8.9% 13.6% 9.4% 11.4%

857 1,411 +554 990 1,521 +531 1,100 1,335 +235

5

10

15

FY2009 Cancellations Acquisitions FY2010 Cancellations Acquisitions FY2011 Cancellations Acquisitions FY2012

Thousand households

Net growth rate+7.4%

Net growth rate+4.9%

Net growth rate+6.6%

Net growth rate+5.2%

Net growth rate

+4.7%

Net growth rate+2.0%

MSOs (n=20)

Non-MSOs (n=82)

- 7 -

Figure 11 Changes in Cable Internet ARPU

Figure 12 Speed of Most Popular Service of Subscribers with Each Operator

③ Landline services

As landline services have been launched relatively recently, there are many operators with

much room for growth. Subscriber households and subscription rates are increasing

steadily (Figure 13).

Figure 13 Changes in Numbers of Landline Subscriber Households

and Subscription Rates, Per Firm (n = 42)

Source: Development Bank of Japan Inc.

Source: Development Bank of Japan Inc.

85

90

95

100

105

110

115

FY2009 FY2010 FY2011 FY2012

All firms (n=87) MSOs (n=16) Non-MSOs (n=71)

12.9% 10.5% 8.9% 7.3% 4.8%

39.5% 44.4%37.1% 39.5% 38.7%

26.6% 24.2%29.8% 25.8%

24.2%

21.0% 21.0% 24.2% 27.4%32.3%

0%

20%

40%

60%

80%

100%

FY2008 FY2009 FY2010 FY2011 FY2012

2.0Mbps 2.0 10.0Mbps 10.0 20.0Mbps 20.0Mbps

158 161 162 164

12.4 15.7 18.6 21.2

7.8%

9.7%

11.5% 12.9%

0%

5%

10%

15%

20%

0

50

100

150

200

FY2009 FY2010 FY2011 FY2012

Thousand households

Target households Subscriber households Subscription rate (right scale)

Source: Development Bank of Japan Inc.

- 8 -

With MSOs giving precedence to landline services, as of FY 2008 a substantial gap existed

between the ratios of MSOs and non-MSOs. Over the last five years, however, even

non-MSOs have been introducing landline services at a growing rate; over 60% now

handle landline.

Among non-MSOs, subscription rates for landline services are lower than those for

multichannel services. Therefore, non-MSOs hope to sustain their growth trend by

expanding sales to existing subscribers. MSOs cannot expect much more than sluggish

growth in this category, as their subscription rates for landline services already approach

those for multichannel (Figure 14).

Figure 14 Changes in Landline Acquisitions/Cancellations, Per Firm

3. Business conditions

According to the FY 2012 Report, revenue earned by cable television firms in FY 2012 failed to

grow from the previous year’s level. The sluggishness of the year-on-year growth rate was

conspicuous.

An analysis of business earnings shows little change: revenue from broadcasting and other

businesses was essentially flat, even while that from communications business was on the rise

(Figure 15).

24,95729,064

32,28235,646

8.4% 24.8%

7.9% 19.0%

7.5% 17.9%2,092

6,199 +4,107 2,299

5,517 +3,218 2,429

5,793 +3,364

10

20

30

40

FY2009 Cancellations Acquisitions FY2010 Cancellations Acquisitions FY2011 Cancellations Acquisitions FY2012

Thousand households

MSOs (n=16)

Net increase rate+16.4%

Net increase rate+11.1%

4,6097,475

10,23112,274

5.5% 67.7%

6.4% 43.3%

6.6% 26.5%

255

3,121 +2,866 481

3,237 +2,756672

2,715 +2,043

5

10

15

FY2009 Cancellations Acquisitions FY2010 Cancellations Acquisitions FY2011 Cancellations Acquisitions FY2012

Thousand households

Non-MSOs (n=26)

Net increase rate+62.2%

Net increase rate

+36.9%

Net increase rate+19.9%

Net increase rate+10.4%

Source: Development Bank of Japan Inc.

- 9 -

Figure 15 Changes in Earnings for Each Type of Business (Average for DBJ Clients)

The average of total assets for all companies showed a contracting tendency, with a

progressive shrinking of interest-bearing debt over three fiscal years (Figure 16). With

sustained current-term surpluses producing accumulated income, net assets took up a growing

proportion on the creditor side (right-hand side of the figure).

Figure 16 Average Operator’s Balance Sheet

4. Recent activity in communications and broadcasting

① Development of smart televisions by carriers

As smart television enters the realm of commercial viability within the cable television

industry, mobile communications carriers have simultaneously rolled out smart television

services using their own stick terminals. The aim is to expand to home televisions content

that communications carriers have gathered and constructed for smartphones.

3,670

1,471

2,200

FY2010

3,666

1,632

2,034

FY2011

3,577

1,738

1,839

FY2012

Liabilities Liabilities Liabilities

(Interest-bearing liabilities:

1,746)

(Interest-bearing liabilities:

1,604)

(Interest-bearing liabilities:

1,381)

(Capital:1,123)

(Cumulative profit & loss:348)

(Capital:1,123)

(Cumulative profit & loss:509)

(Capital:1,085)

(Cumulative profit & loss:653)

Net assetsNet assets

Net assets

Total assets Total assets Total assets

Source: Development Bank of Japan Inc.

Source: Development Bank of Japan Inc.

1,2301,249(+2%)

1,256(+1%)

1,261(+0%)

681752

(+10%)

805(+7%)

834(+4%)

5189 42 13

2,440

478

2,655(+9%)

565(+18%)

2,684(+1%)

581(+3%)

2,693(+0%)

585(+1%)

0

1,000

2,000

3,000

FY2009 FY2010 FY2011 FY2012

Million yen

Broadcasting revenue Communications revenueRetransmission revenue Other revenue

- 10 -

② Moves toward platform development

With the industry facing difficult circumstances both outside and within, some firms are

moving to establish a “cable platform” aimed at improving the competitiveness of the

industry as a whole. An exploratory committee within the Japan Cable and

Telecommunications Association has focused on developing regional potential. At the

Ministry of Internal Affairs and Communications (MIC), the Study Group for Acceleration

of Broadcasting Services has formed a Cable Platform Working Group to look at ways of

creating a proprietary platform for the cable television industry. In a report issued in May

2013, the MIC set down five capabilities required of such a platform (Figure 17).

Figure 17 Five Functions Required of a Platform, According to MIC

Operators have also been moving ahead with a number of initiatives.

Japan Digital Serve Corporation (JDS), for example, is building a platform involving a tie-up

with IP-based video on demand provided by Jupiter Telecommunications Co., Ltd.

(J:COM).

In another new development, J.COTT Inc., a collaboration among several independent

cable operators, is working with firms including Actvila Corporation to create a platform

that would enable firms throughout Japan to provide VOD and other services.

5. Moves to advance alliances

① The situation in the United States

Like their counterparts in Japan, local independent operators in the U.S. face stiff

competition from rivals in the communications sector. Their difficulties are compounded

by listless regional economies, competition from satellite broadcasters, and repercussions

of government policy. Some independent firms are fighting back by forming alliances

among themselves.

The National Cable Television Cooperative (NCTC) is a partnership of independent

operators. In addition to making joint purchases and handling rights, the NCTC recently

launched the TV Everywhere platform aimed at small and medium-sized firms. The

American Cable Association (ATA) handles office work relating to retransmission

legislation while coordinating with the FCC. The two organizations cooperate in providing

support to independent operators (Figure 18).

Source: Ministry of Internal Affairs and Communications

① IP video transmission capabilities

② Platform for alliances among existing ID operators

③ Monitoring platform

④ AJC-CMS capabilities

⑤Customer management system (SMS) platform

capabiltiies

- 11 -

Figure 18 The Alliance Situation in the United States

A number of consulting services have sprung up to assist independent operators in

introducing Internet Protocol television (IPTV) and over-the-top content (OTT) services by

handling the rights to technology and programs (Figure 19).

The U.S. Midwest is home to the Mid-American Cable Show, an annual gathering of

independent operators from across the region. In 2013 the show was held from

September 4-6 in Springfield, Missouri. Sessions included presentations by the NCTC and

TV Everywhere, an alliance of independent operators, during which they described their

activities and outlined technological road maps (Figure 20). At the exhibition booths

visitors could watch local high school teams compete in football and basketball games in

broadcasts presented on tablets and other devices, showcasing independent operators at

their best (Figure 21).

Individual firms are paying attention to the tie-up trend. Responding to our questionnaire,

one local independent operator said that since TV Everywhere was likely to extend into

outlying regions, independents should facilitate its spread through alliances with ①

MSOs and ② cooperatives of small to medium-sized operators such as the NCTC. Some

firms said they were seeking to expand their business through alliances with nearby

power companies. Some, however, were concerned that tie-ups could cost independents

their individuality, at least to some extent.

Leading MSOs

Independent terrestrial CATV providers

ACANCTC

Satellitecompanies

Telecomcarriers

The cable television industry

TV Everywhere

Alliances among independent operators

Price negotiation &coordination

Rights handlingContent company holding

Price negotiation &coordination

Rights handling

Development &supply of

TV Everywhereplatform

Development ofTV Everywhereplatform (trial)

Triple play

Competition

Cooperative sourcing of content・Economies of scale = power when negotiating with content providers

・Applications to FCC・Legal paperwork

Development ofTV Everywhere platform・Technological development + handling of content rights

Content providers,DTT networks, etc.

Users

Triple play services

IndependentCATV

Source: Development Bank of Japan Inc.

- 12 -

Figure 19 OTT/IPTV Services for Regional Telephone Companies and CATV Operators

(Photo is of Skitter TV)

Figure 20 Figure 21

② Japanese views on alliances

In a climate of intensifying competition and constant technological innovation,

momentum appears to be growing for alliances within the cable television industry. For

the FY 2012 Report, we asked Japanese cable operators about their intentions in regard

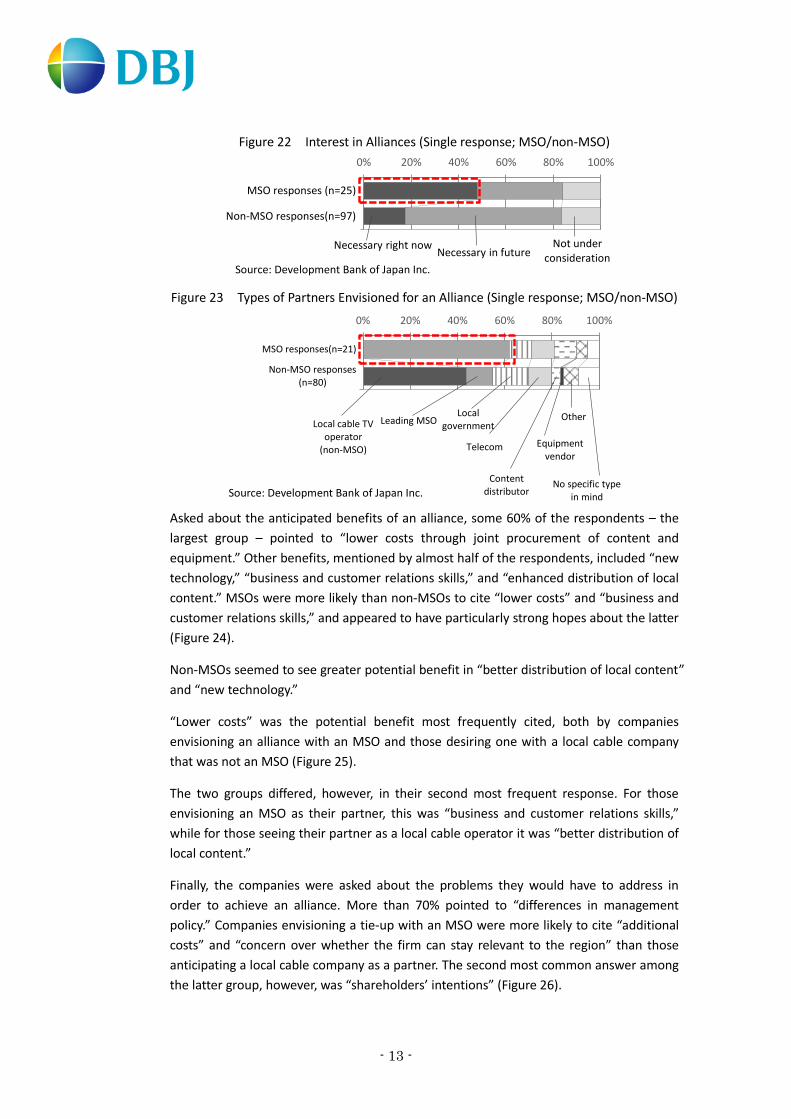

to alliances. More than 80% of the responding firms said that alliances were “necessary.”

MSOs and non-MSOs held differing views on just how necessary, however: While more

than 40% of MSOs said that they were needed “immediately,” less than 20% of non-MSOs

agreed (Figure 22).

Companies that believed alliances were necessary were asked about the kinds of partners

they envisioned having. “Operators other than MSOs” was the most frequent response,

followed by “MSOs.” The composition of the responses differed widely, however,

depending on whether the respondent was an MSO or non-MSO. Among non-MSOs,

“operators other than MSOs” drew the most responses, with “local government” drawing

a fairly large number as well. Among MSOs, however, “operators other than MSOs” did

not draw a single response (Figure 23).

Source: Skitter, Inc.

Source: Development Bank of Japan Inc. Source: Development Bank of Japan Inc.

- 13 -

Figure 22 Interest in Alliances (Single response; MSO/non-MSO)

Figure 23 Types of Partners Envisioned for an Alliance (Single response; MSO/non-MSO)

Asked about the anticipated benefits of an alliance, some 60% of the respondents – the

largest group – pointed to “lower costs through joint procurement of content and

equipment.” Other benefits, mentioned by almost half of the respondents, included “new

technology,” “business and customer relations skills,” and “enhanced distribution of local

content.” MSOs were more likely than non-MSOs to cite “lower costs” and “business and

customer relations skills,” and appeared to have particularly strong hopes about the latter

(Figure 24).

Non-MSOs seemed to see greater potential benefit in “better distribution of local content”

and “new technology.”

“Lower costs” was the potential benefit most frequently cited, both by companies

envisioning an alliance with an MSO and those desiring one with a local cable company

that was not an MSO (Figure 25).

The two groups differed, however, in their second most frequent response. For those

envisioning an MSO as their partner, this was “business and customer relations skills,”

while for those seeing their partner as a local cable operator it was “better distribution of

local content.”

Finally, the companies were asked about the problems they would have to address in

order to achieve an alliance. More than 70% pointed to “differences in management

policy.” Companies envisioning a tie-up with an MSO were more likely to cite “additional

costs” and “concern over whether the firm can stay relevant to the region” than those

anticipating a local cable company as a partner. The second most common answer among

the latter group, however, was “shareholders’ intentions” (Figure 26).

Local cable TV operator

(non-MSO)

Leading MSOLocal

government

Telecom

Content distributor

Equipment vendor

Other

No specific type in mind

0% 20% 40% 60% 80% 100%

MSO responses(n=21)

Non-MSO responses(n=80)

Source: Development Bank of Japan Inc.

Necessary right nowNecessary in future

Not under consideration

0% 20% 40% 60% 80% 100%

MSO responses (n=25)

Non-MSO responses(n=97)

Source: Development Bank of Japan Inc.

- 14 -

Source for Figs.24 through 26:

Development Bank of Japan Inc.

65%

50%

75%

45%

0%

10%

5%

57%

54%

41%

51%

1%

14%

4%

0% 20% 40% 60%

Lower costs through jointprocurement of programs and

equipment

Compatibility with newtechnologies (linkups with

smartphones & tablets; internetvideo transmission, etc.)

Sharing of skills: business,customers relations, etc.

Better distribution of localcontent

Compatibility with landlinetelephone services

Compatibility with wirelessservices (WiMAX, WiFi, etc.)

Other

MSO responses (n=20)

Non-MSO responses (n=74)

82%

55%

73%

32%

0%

5%

0%

74%

43%

49%

66%

0%

6%

3%

0% 20% 40% 60% 80%

Lower costs through jointprocurement of content and

equipment

Compatibility with newtechnology (linkups with

smartphones & tablets; videotransmission on smart TV &

internet; etc.)

Sharing of business skills,customer relations skills, etc.

Better distribution of localcontent

Compatibility with landlinetelephone service

Compatiblity with wirelessservice (WiMAX, Wi-Fi, etc.)

Other

Alliance with MSO(n=22)

Alliance with non-MSO(n=35)

Figure 24 Desired Effects of an Alliance

(Multiple res ponses; MSO/non-MSO)

Figure 25 Desired Effects of an Alliance

(Multiple responses; partner is MSO/non-MSO)

86%

41%

5%

59%

50%

0%

5%

74%

54%

14%

34%

29%

29%

3%

0% 20% 40% 60% 80%

Differences in managementpolicy

Shareholders' intentions

Differences with contentdistributors

Additional costs

Concern over whether firm canstay relevant to the region

Lack of a person or group tolead and coordinate the alliance

Other

Firms responding "MSO" (n=22)

Firms responding "Local cable operator (non-MSO)" (n=35)

Figure 26 Obstacles in the Way of Alliances

(Multiple responses)

- 15 -

③ Alliance strategies

In expectation of further competition with telecoms and a shrinking market, cable

television operators are weighing their options. The survey suggested that they were

leaning towards two broad strategies: “greater ability to compete on cost,” and

“differentiation through services tailored to the locality” (Figure 27). Alliances play a key

role in each. On the vertical axis of the scale, we see that specific steps such as the joint

use of facilities, joint purchasing of terminals and content, and integration of functions

are already producing results for a number of companies.

On the horizontal axis, “differentiation through services tailored to the locality,” through

tie-ups with a variety of local organizations, is shown to resolve local issues and enrich the

lives of local residents.

Figure 27 Effects of Alliances on Competition Strategy

Differentiation from telecoms

Enh

ance

me

nt o

f cost

com

petitive

ne

ss

Lower investmentthrough

shared facilities

Cost reductionthrough

joint purchasing

Better productivitythrough

functional integration

Differentiation throughlocalized services

Cost leadership strategies promoted by MSOs and other leading companiesKey to success: Partnering with other firms in the industry.

Operators seeking strategies to deal with problems such as the ageing and shrinking of Japan's populationKey to success: Partnering with other industries.

Shared headend

Shared telephone center equipment

Joint purchasing of subscriber terminals

Joint purchasing of internet upper network

Joint purchasing of CS programs

Shared program guides

Shared advertising and business functions

Integrated call center

Integration & sharing of production capabilties

Shared service center for clerical work

Collaborative staff training & R&D

Partnership

Retailers, carriers, etc.

Medical & welfare facilities

Schools

Ward offices, town halls

Partnerships withDifferentiation throughlocalized services

Source: Development Bank of Japan Inc.

- 16 -

The FY 2012 Report revealed signs of change in the business environment. Cable

operators must take changing trends into account as they perform the urgent task of

formulate their mid-to-long-term outlooks. As the questions on attitudes toward alliances

made clear, momentum for alliances may be increasing, but companies’ views on such

tie-ups – and what they expect to gain from them – tend to differ. Japan’s cable television

operators must focus on creating alliance strategies that spell out which forms of

cooperation will best suit their corporate needs.

Figure 28 Putting Alliance Strategies into Effect

Hiroyuki Sawada,

Corporate Finance Department, Division 2

Makoto Shimizu,

Economic & Industrial Research Department

Development Bank of Japan Inc.

Source: Development Bank of Japan Inc.

Partners:MSOs, independent operators, telecoms, local

governments …

Scope of alliance:Sharing of facilities, joint purchasing of programs,

compatibility with new technologies …

Expected results and advantages:

Specific economic benefits

Reduction in investment, services benefiting the

general public …

Reduction in costs (approx. --- yen)

Obstacles and disadvantages:

Capital problems, possible loss of independence …

The right alliance for your firm?

Area, scale …

- 17 -

All inquiries should be directed to the Economic & Industrial Research Department,

Development Bank of Japan Inc.

the Economic & Industrial Research Department,

Development Bank of Japan Inc.

Phone: 03-3244-1840 E-mail: [email protected]