TelecomSeptember 2006

www.imacs.in

TELECOMwww.imacs.in

• Market Overview

• Government regulations & policy

• Advantage India and business opportunities

Contents

TELECOMwww.imacs.in

Market Overview• Market Overview

• Government regulations & policy

• Advantage India and business opportunities

TELECOMwww.imacs.in

India’s telecom market has grown rapidly in the last few years…

• Revenues ~ USD 19.5 bn (FY 2006) • CAGR (FY 2002-06) - 21%• Have doubled in last 3 years

• Subscribers ~ 160 million (Aug 2006)• CAGR (FY 2002-06) - 38 %• Nearly quadrupled since FY 02• 5-6 million being added every month

• Tele-Density - 14.8 (Aug 2006)• Has doubled in 3 years• Target set for 2007 under NTP 1999

achieved during FY 2005

Revenue growth20

15

1110

9

0

5

10

15

20

2002 2003 2004 2005 2006

$ Billion

CAGR - 21%

Subscriber growth 164

98

7653

44

0

60

120

180

2002 2003 2004 2005 Aug-06

CAGR - 38 %

Source: www.voicendata.com, Telecom regulatory Authority of India (TRAI), Year indicates financial year ending March

Market Overview

TELECOMwww.imacs.in

…and is poised to be the second largest network globally by 2008*

Source: International Telecommunications Union (ITU)

Telecom Subscribers - Country wise December 2005China743

USA360

Ind125

Rus130

Germany134

Japan 153

0

200

400

600

800

mn. subscribers

India - Nov 2006

184 mn. subs

Expected to overtake US by 2008

* Based on excerpts from Worldwide Wireless Data Trends 2006 - a mid year update. Datacomm research

Market Overview

TELECOMwww.imacs.in

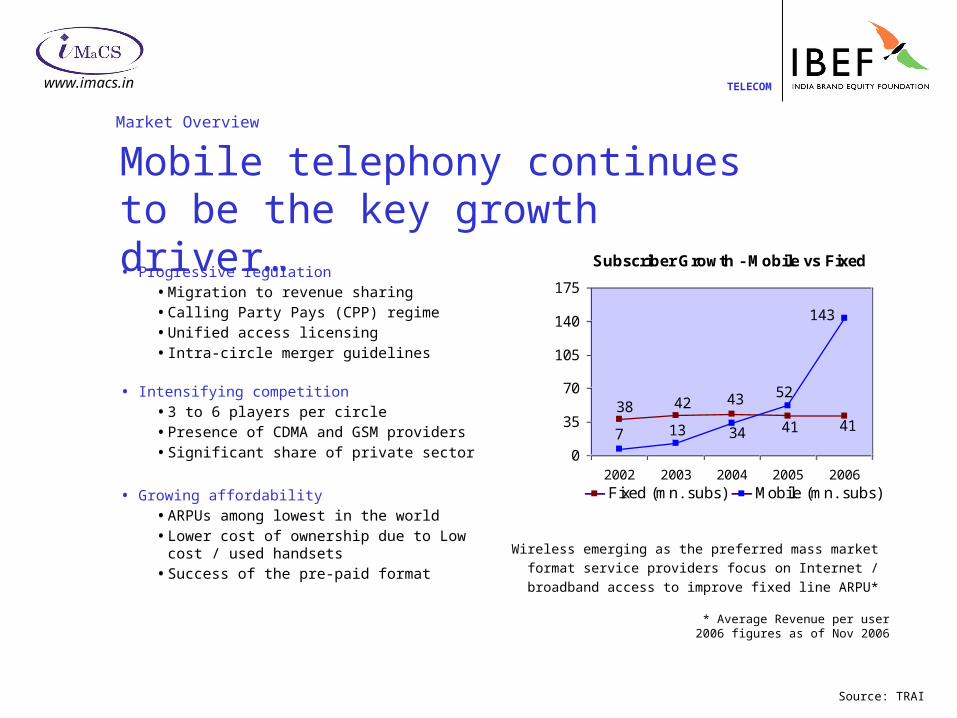

Mobile telephony continues to be the key growth driver…• Progressive regulation

• Migration to revenue sharing• Calling Party Pays (CPP) regime• Unified access licensing• Intra-circle merger guidelines

• Intensifying competition• 3 to 6 players per circle• Presence of CDMA and GSM providers• Significant share of private sector

Subscriber Growth - Mobile vs Fixed

4141

434238

143

52

7 13 34

0

35

70

105

140

175

2002 2003 2004 2005 2006

Mn. subscribers

Fixed (mn. subs) Mobile (mn. subs)

Wireless emerging as the preferred mass market format service providers focus on Internet / broadband access to

improve fixed line ARPU*

• Growing affordability• ARPUs among lowest in the world• Lower cost of ownership due to Low cost /

used handsets• Success of the pre-paid format

Source: TRAI

* Average Revenue per user2006 figures as of Nov 2006

Market Overview

TELECOMwww.imacs.in

Growing network coverage is triggering further market expansion

Support from Universal Service Obligation Fund envisaged for shared network infrastructure creation in uncovered rural areas

Segment Cellular reach (2003-04) Cellular reach (End 2006 - Est.)

Locations Population Locations Population

Urban ~ 1700 of 5200 towns

200 million ~ 4900 towns out of nearly 5200 towns

300 million

Rural Negligible Negligible ~ 350,000 out of 607,000

villages

450 million

Source: Recommendations on Rural Telephony 2005 - TRAI

Market Overview

TELECOMwww.imacs.in

Vibrant and competitive telecom market

Source: TRAI, IMaCS research

Consolidation leading to emergence of integrated pan-national service providers

Company Presence

Subscribers Jul 06 (mn)

Share (%)

Fixed Mobile Fixed Mobile

BSNLGovernment owned. Has ramped up GSM services. National presence (except Mumbai and Delhi)

37.4 17.7 74.7% 19.6%

MTNL Government owned. Operates in Delhi and Mumbai. 3.8 2.0 7.7% 2.3%

BhartiIntegrated operator, with presence in all sectors. Largest mobile services provider.

1.4 19.6 2.7% 21.7%

RelianceIntegrated operator. Plans expansion of GSM network apart from being the largest private CDMA operators.

3.0 17.3 6.0% 19.2%

Hutch Pure play GSM operator in 11 circles. 15.4 17.0%

IDEA Pure play GSM operator in 6 circles 7.4 8.2%

Tata Teleservices

Integrated operator (along with VSNL) with presence in all segments. Provides CDMA services in 20 circles

4.0 4.9 8.0% 5.4%

AircelOperates in 2 circles. Announced Plans to expand GSM footprint in North and North east

2.6 2.9%

Spice Pure play GSM player in 2 circles 1.9 2.1%

Others 0.4 1.4

Total 50 90

Market Overview

TELECOMwww.imacs.in

Several Indian firms gaining a foothold in the global market• Indian service providers acquiring scale in the International Long Distance market through

acquisitions…

• Acquisitions - FLAG by Reliance, Tyco and Teleglobe by Videsh Sanchar Nigam Limited

• VSNL is now the world's fifth largest carrier of voice globally

• Reliance’s FLAG network connects with 28 countries. FLAG’s FALCON cable system when completed would connect 12 countries with 25 international cable landing stations

• Investments in Infrastructure and

• Bharti-Singtel and VSNL investments in undersea cable

• Emerging as Integrated telco, positioning themselves as full service providers

• Tata teleservices-VSNL, Bharti, Reliance have end-to-end presence in ILD, NLD and Access; BSNL has announced plans to get into ILD

• Focus on corporate connectivity - IPLCs, Frame relay, VPNs

• Strong thrust on internet and broadband - both corporate and retail segments

Market Overview

TELECOMwww.imacs.in

Government regulations and policy • Market Overview

• Government regulations & policy

• Advantage India and business opportunities

TELECOMwww.imacs.in

Reform thrust on independent regulation, competition and investment facilitationPre-reform Partial Deregulation Further Deregulation

Pre-1994 1994-1999 1999 - 2002

• MTNL - Mumbai and Delhi; DTS elsewhere

• No mobile service

• NLD - DoT per/ BSNL ILD - VSNL

• 4 private fixed service providers with less than 1% market share

• 2 GSM mobile players in each circle

• 13 players start mobile service

• Licenses converted to revenue sharing

• Private sector share less than 5% in revenue terms

• Competition in NLD and ILD

• Licenses on Revenue share

• 4 mobile operators / circle

• NTP 1999

• BSNL formed 2001

• Internet Telephony 2002

• FDI - 49 %

• National Telecom Policy (NTP) 1994

• TRAI constituted 1997

• Calling Party Pays

• CDMA launch

• 3-6 operators in each circle

• Intra-circle merger guidelines

• Unified Licensing

Take-off

2002 onwards

• Broadband policy 2004

• FDI - 74% 2005

National Telecom Policy, 1994

New Telecom Policy, 1999

Unified Licensing Regime

Government Regulations and policy

TELECOMwww.imacs.in

Independent regulation has been a critical factor in growth

2002

• ILD opened to competition

• Internet Telephony allowed.

• Reduction in License fees

2003

Calling Party Pays Regime

Unified Access Licensing

Reference Interconnect Order

2004Intra-circle merger guidelinesInternet / broadband penetration

Mature regulatory regime and an enabling policy framework already in place

2005 Unified LicensingQuality of Service regulationRural Telephony

2006 Number portabilityConvergence

TRAI’s recommendations

Government Regulations and policy

TELECOMwww.imacs.in

Important policy initiatives

Creating a favourable investment climate to support growth

• Broadband policy unveiled in 2004 - Targets 20 million broadband subscribers by 2010

• Focus on making India a regional Telecom manufacturing hub

• FDI limit increased from 49% to 74%

• 100% FDI permitted under automatic route in the manufacturing sector

• Deregulation virtually complete and Unified Licensing regime

• Interconnection Usage Charge framework in place

• Exemption from customs duty for import of Mobile Switching Centres

• Comprehensive Spectrum policy and 3G policy on the anvil

Government Regulations and policy

TELECOMwww.imacs.in

Advantage India and business opportunities • Market Overview

• Government regulations & policy

• Advantage India and business opportunities

TELECOMwww.imacs.in

Recent developments are indicative of the paradigm shift in wireless growth

• Of the 160 million subscribers, more than 90 million subscribers added in the last two years

• More than 5 million subscribers added every month since Dec. 2005, translating into the highest growth rate in the world

• On a comparison of growth since introduction of mobile telephony, India surpasses China at the same stage of market evolution

India China comparison

0

250

500

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18

Year

Million Subscribers

China

India

In the 11th year India - 76 mn. China - 24 mn.

Source:TRAI

Advantage India and business opportunities

TELECOMwww.imacs.in

Mobile Value Added Services (VAS) set to register explosive growth*

• Indian Idol - a reality show on Sony Television got 55 million SMS messages in 5 months

• Radio Mirchi - a popular FM radio channel receives ~ 40000-45000 SMS messages every day

• R-World - the mobile portal of Reliance Communications had 5.3 million visitors out of its 18 million subscribers in 2005

• Data and VAS contributed to 7% of revenue in 2004

• Messaging and music (ringtones, downloads etc) to be key contributors

• VAS revenues expected to grow given

• Demand - Young population (60% < 30 years) and an affinity to music and movies

• Supply - aggressive pricing, vibrant ecosystem of content providers /

broadcasters, declining GPRS/mp3 handset prices

VAS expected to contribute 20% of revenue by 2008 and 30% by 2010

* Excerpts from Mobile Data in India. Lehmann brothers report. Oct 2005. IMaCS research

Advantage India and business opportunities

TELECOMwww.imacs.in

Broadband and Internet connectivity on the verge of a take-off

• Internet / Broadband market (FY 2006)• 6.94 mn.Internet customers

(25% growth YoY)• 1.35 mn. broadband customers

(6-fold growth YoY)• Incumbents (BSNL / MTNL)

dominate - 66% share• 7-fold growth in broadband

connections during FY 2006

• Broadband Policy 2004• Recognises the importance of

internet penetration• Envisages 40 million internet

connections by 2010• Visualises creation of

infrastructure through various access technologies

Broadband subscriber growth2.00

1.38

0.18

0

0.75

1.5

Mar-05 Mar-06 Nov-06

Mn. subscribers

6-fold growth

Growing PC sales, Internet adoption in

small towns and offerings including triple

play and video-on-demand / IPTV

expected to be major growth drivers

Source: TRAI

Advantage India and business opportunities

TELECOMwww.imacs.in

Growth-driving sustainable factors in the telecom sector

• Favorable Macro-Economic fundamentals and Demographics• Strong Economic Growth and rising

incomes• By 2020, working age population to

rise to 65%• Low tele-density relative to Asian peers

• Progressive policy and regulation• Independent regulation• Consistent policy framework• Favourable Investment Climate

• Rising Affordability• Declining ARPUs • Lowering cost of handsets • Growing popularity of pre-paid format

• India not just a cost-sensitive mass market

• 300 million plus middle class population

• Value added service revenue expected to

grow at 80% CAGR over next 5 years.

• IDC estimates phones with color screens/

cameras to account for 30%of handset

sales in 2005 and 62%by 2008

“People think about the Indian market as a lower tier. About 30%of the U.S. market is high end and maybe it's only 5%in India. But India has 1.1 billion people”

Ron Garriques. Executive vice president, Motorola's personal communications sector in On the Razor's Edge:Cell Phones Morph into Hip Consumer Electronics Devices Knowledge@Wharton

Advantage India and business opportunities

TELECOMwww.imacs.in

India poised to be a USD 40 bn - 45 bn telecom market by FY 2010…Telecom sector targets announced by Government of India

• 250 million subscribers by 2007

• 500 million subscribers by 2010

• 20 million broadband subscribers by 2010

• Mobile access to all villages with population more than 5,000 by 2006

• Mobile access to all villages with population of more than 1,000 by 2007

Translating into an investment requirement of USD 25 bn to USD 30 Translating into an investment requirement of USD 25 bn to USD 30

bn…bn…

Advantage India and business opportunities

TELECOMwww.imacs.in

• Nortel offers a suite of products and solutions across two broad categories Carrier Networks (incorporating Wireless Networks, Wireline Networks and Optical Networks) and Enterprise Networks.

• In India since 1991. Has an R&D centre in Bangalore

• Promotes and supports a range of telecommunications products and services in India in association with licensed operators.

• Has invested in Bharti Airtel and also Network i2i is a 50:50 Joint Venture between Bharti and SingTel, connecting Chennai to Singapore

• Largest pure-play GSM service provider in India

• Has over 15 million subscribers

• Has a 10% stake in Bharti telecom, an integrated service provider

• Represents the largest foreign investment in the telecom services

sector in India

A compelling destination for Telecom service providers and equipment majors

Advantage India and business opportunities

TELECOMwww.imacs.in

• BSNL - Incumbent service provider and World's 7th largest Telecommunications Company providing comprehensive range of telecom services in India

• Services include Wireline, CDMA mobile, GSM Mobile, Internet, Broadband, Carrier service, MPLS-VPN, VSAT, VoIP services, IN Services etc.

• MTNL - State owned operator covering the cities of Mumbai an Delhi

• Provides both fixed and mobile services

• Bharti Airtel - Integrated operator with presence in all segments

• Leads the mobile segment in the country

• Reliance Communications - Largest player in India in the CDMA segment

• Plans a GSM network

• Tata Teleservices - Integrated operator (with VSNL) with presence in all segments

• Provides CDMA services in 20 circles

Advantage India and business opportunities

Key Indian Companies

TELECOMwww.imacs.in

The India Brand Equity Foundation is a public-private

partnership between the Ministry of Commerce & Industry,

Government of India and the Confederation of Indian

Industry. The Foundation’s primary objective is to build

positive economic perceptions of India globally

India Brand Equity Foundation

c/o Confederation of Indian Industry

249-F Sector 18, Udyog Vihar Phase IV

Gurgaon 122015, Haryana, INDIA

Tel +91 124 401 4087, 4060 - 67

Fax +91 124 401 3873

Email [email protected]

Web www.ibef.org

TELECOMwww.imacs.in

DisclaimerThis publication has been prepared by ICRA Management Consulting Services (IMaCS) for the India Brand Equity Foundation (“IBEF”).

All rights reserved. All copyright in this publication and related works are jointly owned by IBEF and IMaCS.

The same may not be reproduced, wholly or in part in any material form (including photocopying or storing it in any medium by electronic means and whether or not transiently or incidentally to some other use of this publication), modified or in any manner communicated to any third party except with the written approval of IBEF.

This publication is for information purposes only. While due care has been taken during the compilation of this publication to ensure that the information is accurate to the best of knowledge and belief of IBEF and IMaCS, the content is not to be construed in any manner whatsoever as a substitute for professional advice.

IBEF and IMaCS neither recommend nor endorse any specific products or services that may have been mentioned in this publication and nor do they assume any liability or responsibility for the outcome of decisions taken as a result of any reliance placed on this publication.

IBEF or IMaCS shall in no way, be liable for any direct or indirect damages that may arise due to any act or omission on the part of the user due to any reliance placed or guidance taken from any portion of this publication.

ICRA Management Consulting Services Limited