TECHNOLOGIES FOR

DIGITAL FINANCIAL SERVICES

About The Author

This study has been authored by Hasaan Anwar Raza. Hasaan is a Technical Project

Manager in the Digital Financial Services team of Karandaaz Pakistan. He has an extensive

experience of Technology Strategy, Planning and Implementation of financial products and

services.

The views expressed in this document are those of the author and do not necessarily reflect

the views and policies of Karandaaz Pakistan or the donors who have funded the study.

©2017 Karandaaz Pakistan

Table of Contents

Glossary ___________________________________________________________________________________________________ 1

The Company _____________________________________________________________________________________________ 2

Introduction ______________________________________________________________________________________________ 3

Objective __________________________________________________________________________________________________ 4

Core Banking System _____________________________________________________________________________________ 6

Financial Switch __________________________________________________________________________________________ 8

API Management _______________________________________________________________________________________ 10

Mobile Financial Services ______________________________________________________________________________ 12

Conclusion ______________________________________________________________________________________________ 14

Annex 01: Reference Architecture ____________________________________________________________________ 15

Table of Figures

Figure 1 .............................................................................................................................................................................................................5

Figure 2 .............................................................................................................................................................................................................8

Figure 3 .......................................................................................................................................................................................................... 10

Figure 4 .......................................................................................................................................................................................................... 11

Figure 5 .......................................................................................................................................................................................................... 12

Page | 1

©2017 Karandaaz Pakistan

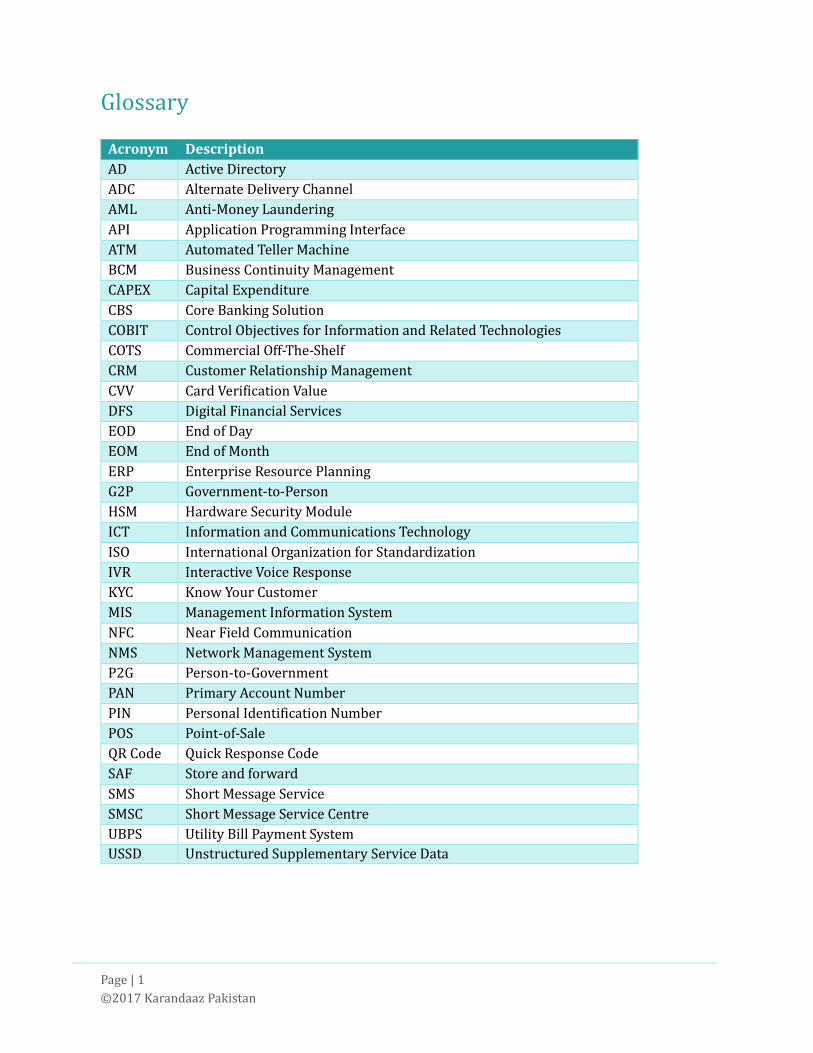

Glossary

Acronym Description

AD Active Directory

ADC Alternate Delivery Channel

AML Anti-Money Laundering

API Application Programming Interface

ATM Automated Teller Machine

BCM Business Continuity Management

CAPEX Capital Expenditure

CBS Core Banking Solution

COBIT Control Objectives for Information and Related Technologies

COTS Commercial Off-The-Shelf

CRM Customer Relationship Management

CVV Card Verification Value

DFS Digital Financial Services

EOD End of Day

EOM End of Month

ERP Enterprise Resource Planning

G2P Government-to-Person

HSM Hardware Security Module

ICT Information and Communications Technology

ISO International Organization for Standardization

IVR Interactive Voice Response

KYC Know Your Customer

MIS Management Information System

NFC Near Field Communication

NMS Network Management System

P2G Person-to-Government

PAN Primary Account Number

PIN Personal Identification Number

POS Point-of-Sale

QR Code Quick Response Code

SAF Store and forward

SMS Short Message Service

SMSC Short Message Service Centre

UBPS Utility Bill Payment System

USSD Unstructured Supplementary Service Data

Page | 2

©2017 Karandaaz Pakistan

The Company

Karandaaz Digital

Focuses on expanding access to digital financial services in Pakistan by working across the

ecosystem with all stakeholders including regulators, policymakers, government

departments, businesses, researchers and academics.

Karandaaz Capital

Invests growth capital in small and medium size enterprises (SMEs) with the twin objectives

of generating financial returns for Karandaaz Pakistan and supporting broad-based

employment generation in Pakistan.

Karandaaz Knowledge Management and Communication

Develops and disseminates evidence-based insights and solutions to inform the core themes

of the organization, including innovation, women entrepreneurship and youth, and to

influence the financial ecosystem to promote financial inclusion in Pakistan.

Karandaaz Pakistan is a not-for-profit development finance company

established in 2014 and registered with the Securities and Exchange

Commission of Pakistan (SECP). The organization promotes access to finance

for small businesses through commercially directed investments, and

financial inclusion for individuals by employing technology-enabled digital

solutions. It operates through three program verticals:

Karandaaz Pakistan has received funding from the United Kingdom

Department for International Development (DFID) and Bill and Melinda

Gates Foundation (BMGF).

Page | 3

©2017 Karandaaz Pakistan

Introduction

The Financial Services industry in Pakistan is

currently at varying degrees of digital maturity.

While on one side we have organizations which

are leading the digital transformation and

innovation in the industry; on the far side of the

spectrum we have organizations which are in

the preliminary stages of their digital journeys.

The telecoms are leading the digital front –

benefitting from their technology reliant core

business. The banks are following up with their

digital strategies and tactical plans to

transform the digital journey of their

customers. These are followed by government

institutions which have a far greater outreach

to the unbanked and under-served population

of the country.

At Karandaaz Pakistan, we are committed to

uplifting the overall knowledge and abilities of

the Digital Financial Services (DFS) industry.

There is a need to quickly capitalize on new

market opportunities. Players who want to

jump on the DFS bandwagon have a lot of

catching up to do. Karandaaz Pakistan sees this

as a significant opportunity to improve service

delivery by providing a means to digitize a

range of payment use cases. A considerable

impact can be delivered by digitizing

government payments alone. This is because

digitization helps reduce the cost of a

transaction. It also provides greater access to

formal financial services by simplifying the

procedural requirements of opening a digital

transaction account and performing digital

transactions. Such interventions hold the

potential for increasing digital financial

inclusion for the unbanked by collaboration

between the regulator, various government

institutions, commercial banks, and telecoms.

As part of its efforts to support the Digital

Financial Services industry, Karandaaz Pakistan

is providing an overview of the technology

domains that are essential for setting up a DFS

ecosystem. This study lists the product features

and capabilities of various platforms to deliver

solutions for clients. It is anticipated that these

efforts would build the knowledge and capacity

of our partners and stakeholders in the DFS

space.

Page | 4

©2017 Karandaaz Pakistan

Objective

The objective of this study is to act as a

guide for the industry; enabling the

practitioners of Digital Financial Services to

make well-informed decisions when it

comes to building, expanding, or upgrading

their technology enterprise stacks.

While writing this document, a conscious

effort has been made to ensure that it is

written in a manner that even professionals

without a technology background are able

to comprehend and benefit from this

information.

Technology Domains

In the scope of this study, we have discussed the following four domains – three of which are central to

most DFS implementations. One of these, API Management, is a relatively new phenomenon that is

rapidly becoming commonplace in digital implementations the world over. A brief description of these

domains has been provided below, with detailed sections to follow.

Core Banking System

o A software that enables the processing of financial transactions, manages the customer

account and maintenance of other financial records.

Financial Switch

o Enables the authorization and routing of financial transactions between a financial

institution’s internal platforms (such as Core Banking and Card Management systems)

and external networks (such as the Interbank Fund Transfer network). It can be used

to drive front-end devices such as ATMs and Point-of-Sale (POS) terminals.

API Management

o Enables an enterprise to create, publish, analyze and manage APIs to external

consumers in a secure and scalable environment.

Mobile Financial Services

o Similar to a Core Banking System, a Mobile Financial Services platform enables basic

financial transactions such as bill payments and top-ups, disbursements and

collections, cash deposits and withdrawals, fund transfers, and agent liquidity

management.

APIs, or Application Programming Interfaces, are a set a programming functions and procedures which

allow one software application to access the features or data of another application exposing the APIs.

An enterprise stack is a collection of

software applications and hardware,

designed specifically for large

organizations such as commercial

banks and telecom operators.

Page | 5

©2017 Karandaaz Pakistan

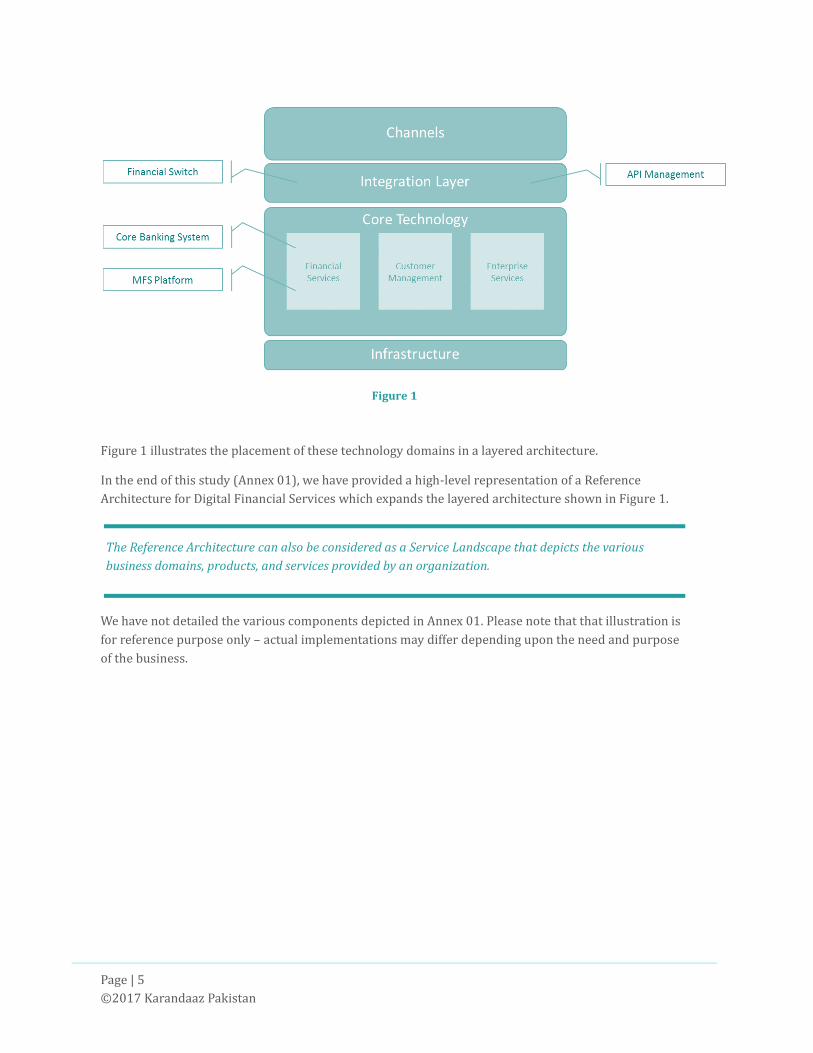

Figure 1

Figure 1 illustrates the placement of these technology domains in a layered architecture.

In the end of this study (Annex 01), we have provided a high-level representation of a Reference

Architecture for Digital Financial Services which expands the layered architecture shown in Figure 1.

We have not detailed the various components depicted in Annex 01. Please note that that illustration is

for reference purpose only – actual implementations may differ depending upon the need and purpose

of the business.

The Reference Architecture can also be considered as a Service Landscape that depicts the various

business domains, products, and services provided by an organization.

Page | 6

©2017 Karandaaz Pakistan

Core Banking System

A core banking system is at the heart of any banking institution’s

technology enterprise application stack. “Gartner defines a core

banking system as a back-end system that processes daily banking

transactions and posts updates to accounts and other financial

records. Core banking systems typically include deposit, loan and

credit processing capabilities, with interfaces to general ledger

systems and reporting tools.”1

A Core Banking System generally comprises of the following

features:

Customer Account and KYC Management:

This includes account opening, capturing KYC information and documents, manage the process

flow of registration, maintain account statuses, manage updates in customer’s KYC and account

information, Closure of Account, Customer Profile, Level of Account, etc.

Multiple Account Options:

The system should enable opening of multiple account types such as Current Account, Deposit

Account, Corporate Current Account, and Savings Account.

Loans, Leasing, Credit Management:

Ability to manage both Consumer as well as Corporate loans and leasing products.

Cards Management:

This includes linking of Debit, Credit, and ATM Cards to customer’s account; as well as

processing of Card Transactions, Card Billing and Payments.

Transaction Management:

The financial transaction processing engine manages all the debit and credit transactions.

General Ledger and Accounting Management:

Integration with the General Ledger system for reporting of accrual transactions and closing

entries, and consolidation of financial statements.

Core Operations:

This includes the back office functions such as managing authorizations based on Maker-

Checker concept; execution of End of Day (EOD) and End of Month (EOM) batch processes; cash

management; teller operations; configuration of interest, commission, fees and taxes;

configuring products and defining product rules; etc.

AML, Fraud and Risk Management:

This is catered either as a sub-module of Core Banking or via integration with a separate

dedicated AML, Fraud and Risks Management module for validation and verification of

accounts and transaction patterns.

1 Gartner, http://www.gartner.com/it-glossary/core-banking-systems/

A Core Banking

Application is

generally the most

capex-intensive

platform in a

financial enterprise

stack.

Page | 7

©2017 Karandaaz Pakistan

Reporting and MIS:

Regulatory reports, Analytical reports, Operational and Monitoring reports, Product-based

reports.

Access Control and User Management:

The system allows limited access to confidential information by authorized users only. These

users can be assigned to configurable roles with defined access levels.

According to a Gartner Industry Research Note2, following are some of the key evaluation criteria to

focus on during the selection process of a Core Banking System:

1. Functionality

2. Flexibility

3. Cost

4. Viability

5. Operational performance

6. Program management

7. Partner management

8. Customer references

2 Gartner, Core Banking System Selection: Criteria That Matter, 27 April 2011

Page | 8

©2017 Karandaaz Pakistan

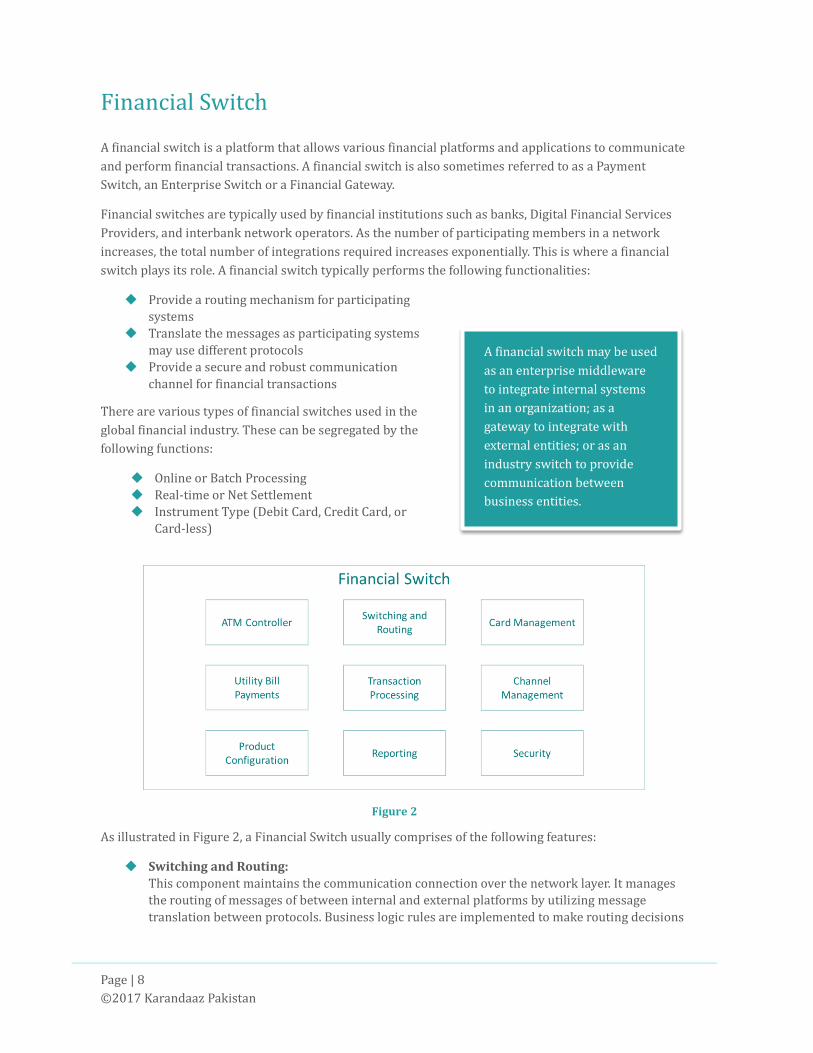

Financial Switch

A financial switch is a platform that allows various financial platforms and applications to communicate

and perform financial transactions. A financial switch is also sometimes referred to as a Payment

Switch, an Enterprise Switch or a Financial Gateway.

Financial switches are typically used by financial institutions such as banks, Digital Financial Services

Providers, and interbank network operators. As the number of participating members in a network

increases, the total number of integrations required increases exponentially. This is where a financial

switch plays its role. A financial switch typically performs the following functionalities:

Provide a routing mechanism for participating

systems

Translate the messages as participating systems

may use different protocols

Provide a secure and robust communication

channel for financial transactions

There are various types of financial switches used in the

global financial industry. These can be segregated by the

following functions:

Online or Batch Processing

Real-time or Net Settlement

Instrument Type (Debit Card, Credit Card, or

Card-less)

Figure 2

As illustrated in Figure 2, a Financial Switch usually comprises of the following features:

Switching and Routing:

This component maintains the communication connection over the network layer. It manages

the routing of messages of between internal and external platforms by utilizing message

translation between protocols. Business logic rules are implemented to make routing decisions

A financial switch may be used

as an enterprise middleware

to integrate internal systems

in an organization; as a

gateway to integrate with

external entities; or as an

industry switch to provide

communication between

business entities.

Page | 9

©2017 Karandaaz Pakistan

based on PIN translation. Store-and-forward (SAF) queue mechanism and timers are used to

manage the flow of messages between two systems.

Transaction Processing:

This comprises of the authorization of financial transactions, clearing and settlement.

Channel Management:

This is used to integrate, manage configurations and monitor the financial operations of

various channels. The integration protocols used by financial switches are ISO 8583, ISO 20022,

or Open APIs.

Card Management:

This is used to manage multiple card products. It includes card production, PAN provisioning,

generation of CVV/CVV2, Card linking to customer’s accounts, card status management, etc.

Utility Bill Payments:

A Financial Switch can be integrated with a UBPS module to allow online and offline

mechanisms of bill presentment and bill payment.

ATM Controller:

Allows to manage and monitor the operations of ATMs. ATM functionalities, statuses and

screen flows can be configured with the help of this feature.

Product Configuration and Reporting:

This allows to implement basic product customizations and reporting requirements.

Security:

The switch is responsible to authorize the PINs of all financial transactions via a hardware

security module (HSM).

Page | 10

©2017 Karandaaz Pakistan

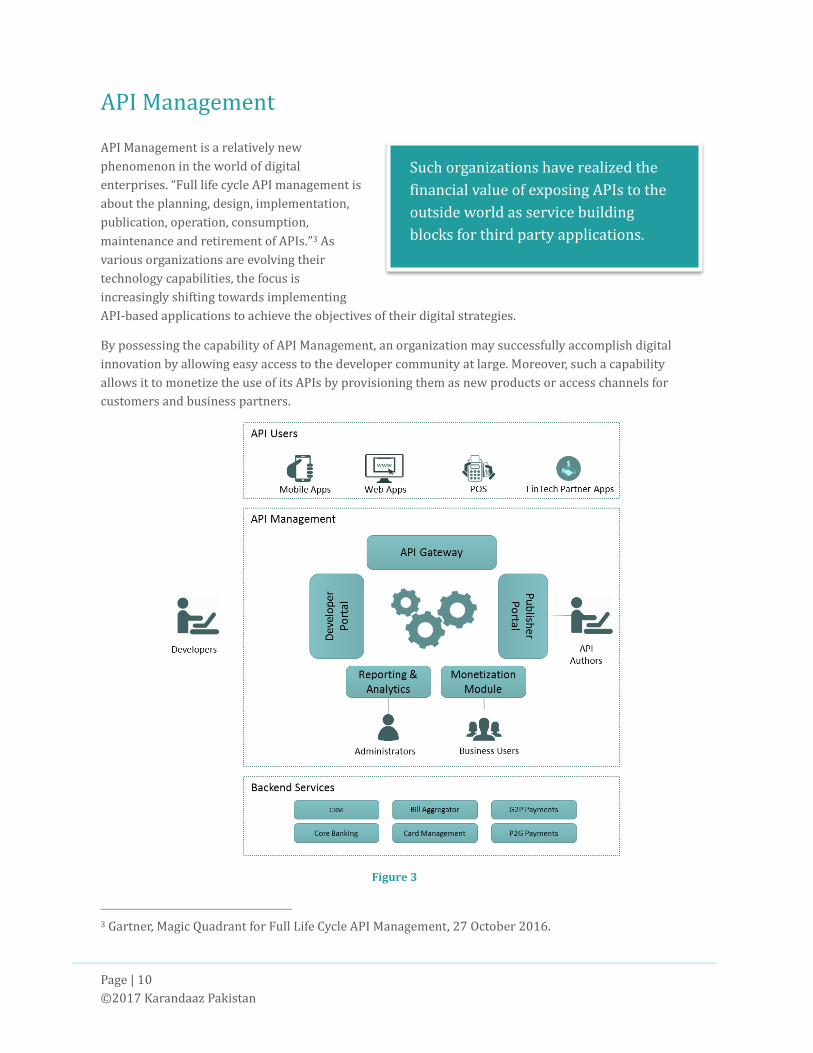

API Management

API Management is a relatively new

phenomenon in the world of digital

enterprises. “Full life cycle API management is

about the planning, design, implementation,

publication, operation, consumption,

maintenance and retirement of APIs.”3 As

various organizations are evolving their

technology capabilities, the focus is

increasingly shifting towards implementing

API-based applications to achieve the objectives of their digital strategies.

By possessing the capability of API Management, an organization may successfully accomplish digital

innovation by allowing easy access to the developer community at large. Moreover, such a capability

allows it to monetize the use of its APIs by provisioning them as new products or access channels for

customers and business partners.

Figure 3

3 Gartner, Magic Quadrant for Full Life Cycle API Management, 27 October 2016.

Such organizations have realized the

financial value of exposing APIs to the

outside world as service building

blocks for third party applications.

Page | 11

©2017 Karandaaz Pakistan

As depicted in Figure 3, an API Management platform typically consists of the following components:

API Gateway:

This component acts as the mediator between the internal and external domains. API requests

are received at the front-end from third-party integrators, modified and orchestrated, and

passed on to the back-end services. API Gateways also ensure the implementation of

performance throttling and security policies.

API Creation and Publishing Tools:

This component is used by API providers to expose the internal APIs by defining the

parameters, usage policies and access rules. This component primarily manages the API

Lifecycle.

Developer Portal:

This portal is available to the API subscribers for consumption of the exposed APIs.

Reporting and Analytics:

This component provides insights into the usage of the APIs along with their performance to

identify the business impacting trends.

Monetization Module: 45This is used to configure the pricing of commercial APIs for monetization purposes.

4 A Forrester Total Economic Impact™ Study, April 2015

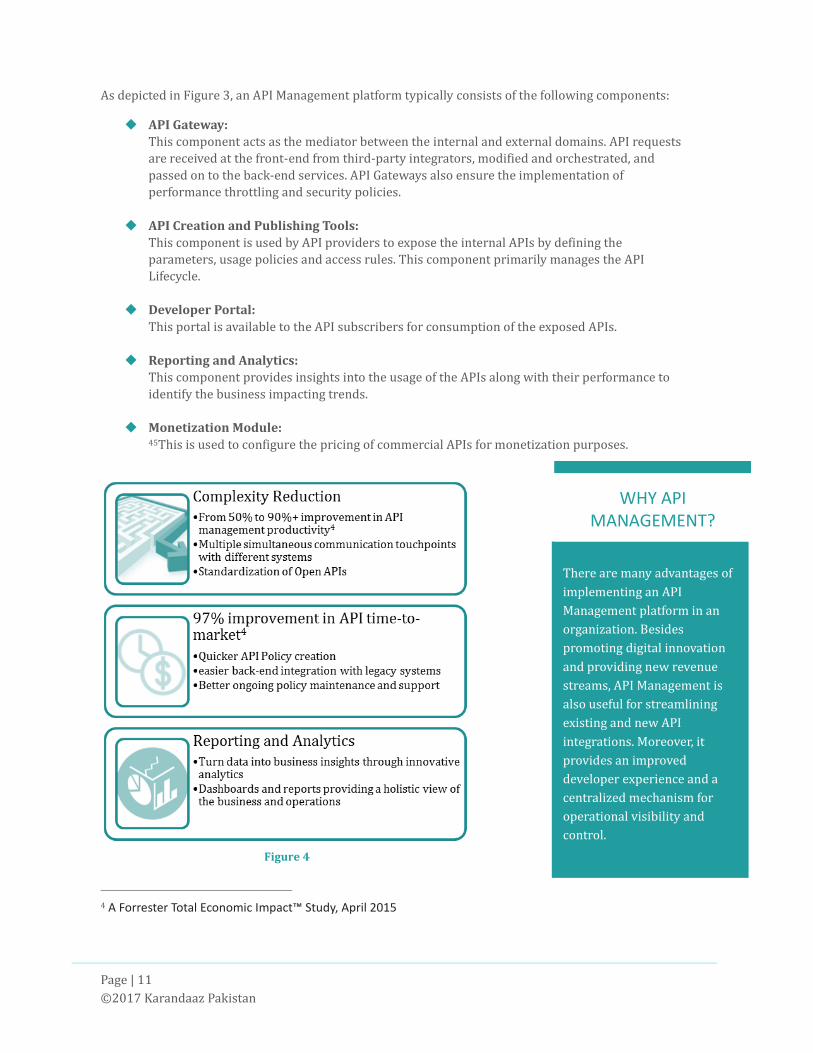

There are many advantages of

implementing an API

Management platform in an

organization. Besides

promoting digital innovation

and providing new revenue

streams, API Management is

also useful for streamlining

existing and new API

integrations. Moreover, it

provides an improved

developer experience and a

centralized mechanism for

operational visibility and

control.

WHY API MANAGEMENT?

Figure 4

Page | 12

©2017 Karandaaz Pakistan

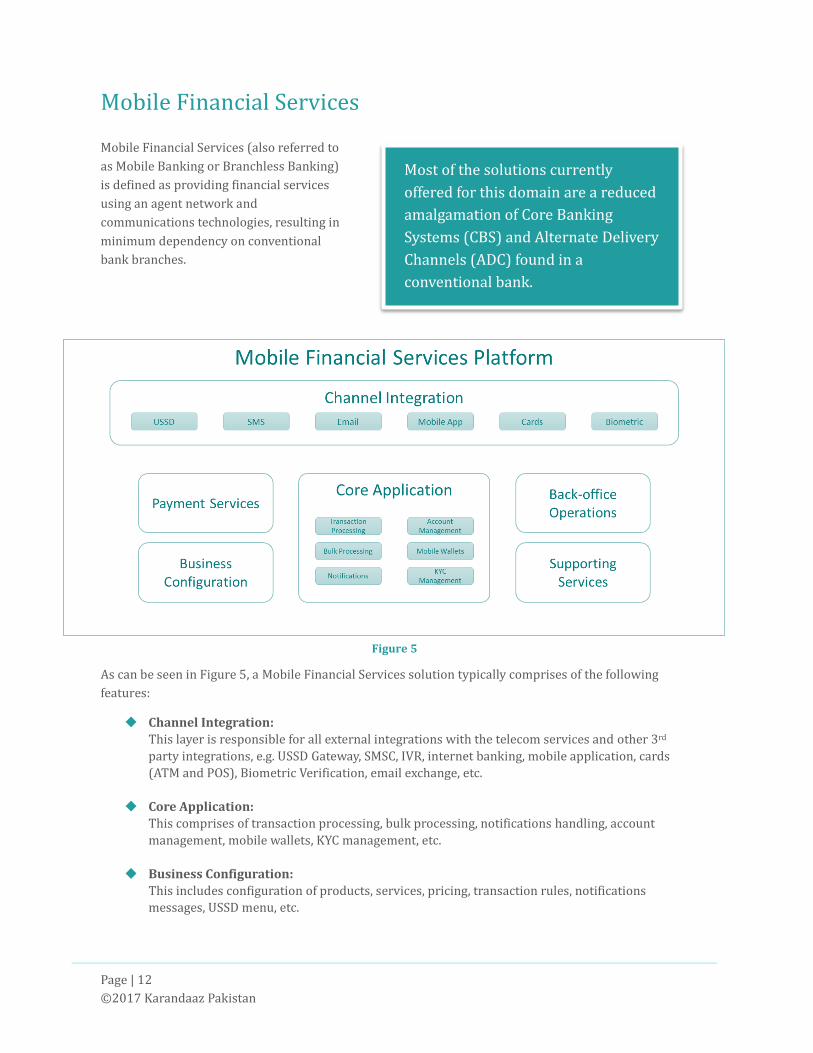

Mobile Financial Services

Mobile Financial Services (also referred to

as Mobile Banking or Branchless Banking)

is defined as providing financial services

using an agent network and

communications technologies, resulting in

minimum dependency on conventional

bank branches.

Figure 5

As can be seen in Figure 5, a Mobile Financial Services solution typically comprises of the following

features:

Channel Integration:

This layer is responsible for all external integrations with the telecom services and other 3rd

party integrations, e.g. USSD Gateway, SMSC, IVR, internet banking, mobile application, cards

(ATM and POS), Biometric Verification, email exchange, etc.

Core Application:

This comprises of transaction processing, bulk processing, notifications handling, account

management, mobile wallets, KYC management, etc.

Business Configuration:

This includes configuration of products, services, pricing, transaction rules, notifications

messages, USSD menu, etc.

Most of the solutions currently

offered for this domain are a reduced

amalgamation of Core Banking

Systems (CBS) and Alternate Delivery

Channels (ADC) found in a

conventional bank.

Page | 13

©2017 Karandaaz Pakistan

Payment Services:

This comprises of services such as bill payments, airtime top-ups, e-commerce payments,

domestic remittances (money transfers), card payments, international remittances, cash

deposits and cash withdrawals.

Back-office Operations:

This includes User Management, Role Management, maker-checker authorization, agent

hierarchy management, definition of transaction limits, cash management, etc.

Supporting Services:

This involves services which are utilized for service monitoring, alarm generation, reporting,

event logging, etc.

Page | 14

©2017 Karandaaz Pakistan

Conclusion

In this study, we have touched upon the

features and functions of only a select few

platforms that play a vital role in the Digital

Financial Services Technology Landscape. It

should be noted that this domain has evolved

considerably over the past two decades; and

that it will continue to evolve as technological

enhancements become more accessible.

The recent advancements in technology have

encouraged DFS players to experiment with

new payment mechanisms using NFC and QR

Codes. It is crucial for technology suppliers and

FinTech start-ups to continue exploring the

possibilities and expand the horizons of the

existing DFS space.

When setting up a DFS Enterprise ecosystem, it

is important for DFS Providers to maintain the

right balance between Commercial off-the-shelf

(COTS) platforms and in-house developed

products and services. A good strategy is to

acquire products for mature domains such as

Core Banking Applications and Financial

Switches from established technology

suppliers; but rely on local in-house

development for newer experimental products.

Another aspect that DFS players need to be

cautious of is whether to opt for a multi-vendor

(best-of-breed) ecosystem, or a single vendor

enterprise suite. This is important when setting

up or upgrading a technology stack as it has a

direct impact on your financial expenditure and

vendor management strategy.

As new services and technologies are being

introduced in the industry, it is of utmost

importance for regulators to play their due

role. New technologies always bring with them

a new set of vulnerabilities and challenges for

the customers. By providing guidance policies

and a robust framework on security and

controls, a regulator can ensure that the DFS

providers and technology suppliers can launch

products and services that would have a

minimum negative impact on the well-being of

customers. Though, care has to be taken to

avoid overregulation as it limits

experimentation and innovation.

Last but not least, DFS Providers should have a

firm focus on Enterprise Governance of IT. This

is an area often neglected even by

technologically advanced and established

organizations. There are quite a few

frameworks available for reference that can be

employed in this regard, e.g. COBIT (Control

Objectives for Information and Related

Technologies).

It is well established that Information and

Communications Technology (ICT) plays a vital

role in promoting Financial Inclusion. By

implementing a DFS technology ecosystem in

an effective manner, we can ensure additional

impact on the lives of the underprivileged.

Page | 15

©2017 Karandaaz Pakistan

Annex 01: Reference Architecture

Page | 16

©2017 Karandaaz Pakistan