Download - Taxation 1

TAXATION LAW I

TAXATION

- Sovereign power/process

Sovereign Power

One of the inherent powers of the State

No need for a law, even the Constitution

The source of power is the mere existence of the State

Process

Means by which government will collect contribution

Levy – enactment of a law (Legislative)

Assessment – computation of tax dues (Administrative)

Collection – demand to pay tax dues (Administrative)

- Supreme, plenary, unlimited, and comprehensive

- Restrictions/Limitations:

o Inherent

Public purpose

International comity

Essentially legislative

Territorial

Exemption of the Government

o Constitutional

Equal protection

Due process

- Importance:

o Continuance of delivery of service to the people

o Life Blood Doctrine – taxes are the life-blood of the government and

without taxes, the government cannot exist

- Justifications:

o Benefit-Receipt Theory–the State has the right to collect taxes because of

the protection received by a citizen

o Necessity – existence of a government is a necessity and without taxes, the

government cannot exist

o Symbiotic Theory – citizens will contribute so the State will protect and

render services to its citizens

Benefit-Receipt Theory v. Symbiotic Theory

BRT = past tense

ST = future tense

- Justice Marshall: power to tax is also power to destroy

Holmes: power to tax is not power to destroy whole the court sits

Cruz: power to destroy = police power

- Objectives:

o Revenue: for government to exist

o Non-Revenue:

Implement of Police Power

Reduction of Social Inequity (progressive system of taxation: higher

income = higher tax)

Protectionism (protect local industry)

Implement of Eminent Domain

General Welfare (public purpose)

- Sound Taxation System

o Fiscal Adequacy/Monetary Sufficiency

o Administrative Feasibility – laws must be reasonable and just in order to

collect

o Theoretical Justice – higher income = higher tax

Ability to Pay Principle

Progressive System of Taxation

TYPES OF TAXES

1. As to Subject Matter

a. Property – properties

b. Excise – interest, right, privilege

c. Poll – person; mandatory, but non-payment will NOT cause imprisonment

2. As to Burden

a. Direct – taxpayer will have the burden of paying his own tax

b. Indirect – the burden to pay can be shifted to another individual

NOTE: Burden is shifted, NOT the Obligation to pay the tax

TAX v. DEBT: not compulsory; has no limit; non-payment will not result in

imprisonment

TOLL: user fee

SPECIAL ASSESSMENT: for specific purpose; cannot exceed the

improvement/service it is financing

CONCEPT and CHARACTERISTICS:

1. Enforced – obligation mandated by law

2. Proportionate Contribution – pegged on certain amount; Ability to Pay Principle

3. Levied by Law-Making Body – Congress through enactment of law

4. Having Territorial Jurisdiction – tax situs (taxing authority)

5. Personal in Nature – only the burden and not the obligation can be shifted to

another person

6. Purpose –raising money and other public needs

LIMITATIONS:

1. Inherent

a. Public Purpose– for general welfare

b. Essentially Legislative

Inherent

Power is delegated to LGUs (Sanggunian)

Coverage – what to tax

Object – purpose of tax

Nature – kind/type of tax

Extent – tax rate

Situs – taxing authority

Cannot be questioned by Judiciary -> Judicial Non-Interference (not

applicable to LGUs’ taxing power)

GR: Power to tax cannot be delegated

Expn: LGU

(1) Separation of Power is not applicable to LGUs

(2) Delegation is by an immemorial practice

1987 Constitution directly confers the power to tax to LGUs (ergo,

no longer delegated to LGUs)

Double Taxation

Not prohibited, only frowned upon

Direct Double Taxation

Taxing the same:

Object at the same

Taxing authority for the same

Purpose by the same

Taxing authority

Tantamount to confiscation = violates due process =

unconstitutional

Indirect Double Taxation

Different taxing authorities

LGUs cannot impose tax akin to those imposed by the National

Government (i.e. import tax)

Flexible Tariff Clause

Sec. 28 (2), Art. VI, 1987 Constitution

Delegation to President

Administrative discretion subject to valid standards

(1) Congress authorizing President

(2) Fix tariff rates, import and export quotas, tonnage and wharfage

dues, other duties and imposts

(3) subject to limitations/restrictions imposed by Congress

c. Territoriality

Situs = taxing authority

Excise: WHERE income has been earned (based either on residence or

citizenship)

Property:

Tangible

- personal property: passage of title test

- real property: location

Intangible(personal property)

GR: Mobilia sequuntur personam (movables follow the person)

Expns:

(1) Business Situs (operating in the Philippines)

(2) 85% operation is in the Philippines

(3) Exercise of Business in the Philippines

Poll: RESIDENCE of the taxpayer

d. International Comity

Courteous and friendly interaction between States

Respect laws of other country

Employer tax withholding agent

Tax withholding = deduction of withholding tax from salaries of

employees -> remitted to the government

Embassies/International Organizations cannot be obliged by the

government to be tax withholding agent of the government for its Filipino

employees

e. Exemption of Government

Agencies and instrumentalities

GOCCs

GR: taxable

Expn: charter provides for exemption

2. Constitutional

a. Due Process

Substantial DP – existence of a valid tax law before tax may be levied

Procedural DP – there should first be the twin due process requirement

of notice and hearing before there can be foreclosure

NET INCOME(NI) = Gross Income (GI) minus Expense (E)

GI = Gross Sales/Receipts (GS or GR) minus Cost of Sales/Receipts (CoS or CoR)

CoS/CoR = Capital =direct cost = indispensable cost

E = allowable deductions (AD) = prerogative of Congress whether to remove

(broaden tax base) or not

The Government cannot tax the Capital

Gross Income is not the same as Capital

Congress has wide prerogative to choose the tax base

Deductions are mere legislative grace

Creditable

Withholding

Tax (CWT)

Final

Withholding

Tax (FWT)

Advance Final payment

payment

Not

extinguishes

tax liability

Extinguishes

tax liability

Included in ITRNot included in

ITR

CWT

30k/mo.

(CWT = 5k)

l11 mo.l

Jan. Dec.

CWT = 5k x 11 mo.

= 55k

Declared Taxable Income in ITR (TI)

TI = 30k x 12 mo.

= 360k

Taxable Due per Year = 100k

Final Tax Due = 100k – 55k

= 45k

CWT Certificate

Issued by the BIR for amount of tax paid in excess

Personal property = transferrable

FWT

1M = winning

-200k = FWT

800k will no longer be included in ITR

Legislative

Rules

Administrativ

e. Rules

Provide details

for the law

Provide for

mere

interpretation

of the law

Should be

published

Need not be

published

b. Free Exercise v. Non-Establishment

Free Exercise

Non-

Establishmen

t

Freedom to

exercise

religious belief

Government

should not

give undue

favor to a

religion/sect

License Tax – imposed before sale = prior restraint violates Free

Exercise = unconstitutional

VAT – imposed after sale = no prior restraint

– regressive (allowed but frowned upon), not progressive (not

mandated but encouraged)

c. Non-Imprisonment for Non-Payment of Poll Tax – no tax evasion

d. Non-Impairment Clause

Only refers to contract between government (proprietary function) and

taxpayer

ONLY Contractual Tax Exemption – agreed to by taxing authority through

contracts

Presuppositions:

Taxpayer was granted a tax exemption

Tax exemption revoked is contractual

Tax Holiday

Taxpayer will not pay tax for a definite period only

Can be revoked anytime

Government-Issued Bonds

Coupon bond, treasury bond

Loan agreements with the Government as the debtor

CANNOT be impaired

e. Exemption of Traditionally Exempted Tax Payers

Sec. 28(3), Art. VI, Const.

All L, B, I – real property property tax

A, D, E used – usage, not ownership

– directly and incidentally OLD interpretation

– (!!!) Lung Center of the Philippines Case: usage = solely,

excluding incidentally

R, E, C purpose

Sec. 4(3), Art. XIV, Const. (Omnibus Tax Exemption)

All Revenues and Assets – income and real prop. excise and property

taxes

NSNPEI

A, D, E used

Educational Purpose

Sec. 4(4), Art. XIV, Const.

All Grants, Endowments, Donations, Contributions – privilege

excise

A, D, E used

Educational Purpose

f. Uniformity

Tax operates with the same force and effect at any place for all members

of the same class

Equality

Fair, just, and reasonable

Progressive

Theoretical Justice = Ability to Pay

Valid Classification:

Substantial

Germane to the purpose of the law

Not limited to existing conditions

Applies equally to all members of the same class

Owner: X Corporation

Lessee: Systems Plus – Proprietary educational purpose

Lease

Pecuniary benefit:

Not Exempt: Primary usage = industrial proprietary sec. 30, NIRC

Taxable

X Exempt: Primary usage = educational

!!! AUF v. CITY OF ANGELES

AUF is not exempt from Building Permit – not tax

FINANCE DEPARTMENT ORDER NO. 137-87

Tax Exemptions of NSNP Corporations (sec. 30. NIRC) and Educational Institution

(Constitution)

Corporation – not exempt if income is derived from property/activity for profit

Educational Institution

Cafeteria/Canteen and Bookstores

1. Owned by the school

2. Operated by educational institution as ancillary activities

3. Located in school premises

Private Educational Institution

Exempt from VAT if accredited by CHED/DECS

Interest Income from Currency Bank Deposits

1. Certification from Depositary Banks

2. Certification of actual utilization of income – should be A, D, E in

pursuance of educational institution’s purposes

3. Board Resolution by School Administration on the proposed project to be

funded out of such money deposited

!!! CIR v. YMCA

YMCA – welfare, educational, charitable non-profit institution

X Sec. 28(3), A. VI: educational institution = hierarchically, chronologically

high graded

!!! MACEDA CASE

NPC

exempted from tax :government agencies and instrumentalities

may refuse to shoulder indirect tax

Oil Company

Taxpayer

Cannot shift burden to NPC

!!! GOTAMCO CASE

WHO – international organization = exempt from tax

Requested for Gotamco’s exemption

!! Refund – can be requested only by the statutory taxpayer who should hold the

refund in trust for the customers if request is granted

!! Tax Shield/Shelter – may be tax avoidance/evasion depending on the

circumstances

!! Tax Exemption – granted by Congress by a majority vote of all members

S.28(4), A.VI, Const.

FORMS OF ESCAPE FROM TAXATION

1. Resulting in Losses in the Government’s Revenue

a. Tax Evasion – tax-dodging scheme outside lawful means

Civil and/or criminal liability

b. Tax Avoidance – tax minimization

Devise within means sanctioned by law

Should be (1) in good faith and (2) at arm’s length

c. Tax Exemption – immunity from tax which should be expressed in law or

contract

Mere privilege = strictissimijuris

X Tax Credit – debt of government (not a privilege; considered as

property)

2. Not Resulting in Losses in the Government’s Revenue

a. Shifting – tax burden (i.e. VAT)

b. Capitalization – reduction in prices to cope with tax

c. Transformation – improvement in production = more efficient

Producers absorb the payment of tax to reduce prices and maintain

market share

RULES OF TAX LAWS’ CONSTRUCTION

1. Provision imposing tax – strict interpretation

Tax = burden

Strictly against the government

Power to tax – liberally in favor of the Government: inherent power of the

State

2. Grant of tax exemption – strictissimi juris

Mere exception to the rule of taxation

3. Both imposition and exemption

a. Strict interpretation (ascertain the applicability of the tax law first)

b. Strictissimi juris

! There must be an ambiguity first

!!! GULF AIR v. CIR

Rules and regulations issued by the Secretary of Finance is binding upon courts

as per Sec. 244, NIRC, which empowers the Secretary of Finance to promulgate

the same

CONCEPTS OF TAX LAWS

1. GR: Tax laws are not penal in nature (not ex post facto law)

2. Sources

a. Constitution – limitation, regulation of power

b. Statutes – Congress, National Tax

c. Issuances of Secretary of Finance – Revenue Regulations, Rules and

Regulations

d. Administrative Issuances by the BIR – rulings, Revenue Memorandum

Circulars

e. Tax Ordinances – Sangguniang Bayan, local taxes

f. Tax Treaties

(1) actual existence of the treaty

(2) the taxpayer must invoke it

!!! CIR v. SC JHONSON

The “Most Favored Nation Clause” eliminates double taxation

3. Principles

a. Prospectivity

GR: Applies to future circulars

Sec. 246, NIRC – no retroactive effect if prejudicial to the taxpayer

Expns:

The facts subsequently gathered by BIR are materially different from the

facts from which rulings has been based

Taxpayer deliberately omits material facts from returns or any document

required by BIR

Taxpayer deliberately misstates material facts from returns or any

document required by BIR

Taxpayer is in bad faith

Legislative Approval by Re-Enactment – tacit approval of the Congress

by adopting the rules into law

Sec. 246, NIRC

There are two acts by BIR

Second act is a reversal/revocation/modification of the first act

The second act is prejudicial to taxpayer

b. No Estoppel against the Government

The Government cannot be estopped by acts of its agents

An administrative issuance contrary to law is null and void and cannot be

a source of right

Rulings cannot override/supplant law

2 Methods to Avoid Double Taxation (SC Johnson Case)

1. Exemption – State of source (source of income) shall impose the tax but

resident State (taxpayer’s State) will not

2. Credit – State of source and resident State will impose tax but State of

residence will allow tax reduction

!!! SC JOHNSON CASE

To eliminate international double taxation, (1) determine the rights of the State

first then (2) choose between EXEMPTION and CREDIT for relief

Most Favored Nation Clause

Lower rate in the Philippines

Not involve privies

3rd State is not involved in agreement

Treaties should have similar reliefs

RP-US Treaty = 10% and 15%

RP-West Germany = 10% concessional tax rate

SC Johnson is based in US and RP-WG was used instead of RP-US

RP-WG cannot be used by SC Johnsons and Sons (Phils.): RP-US and RP-WG do

not have similar reliefs

c. Imprescriptibility

GR: Action of the Government does not prescribe

Expn: If covered by a tax return filed by the corporation/individual taxpayer

(prescriptive period may be 3 or 10 years)

Improperly Accumulated Tax

If the retained earnings (corporate income, subject to 30% tax, retained by

the corporation instead of being distributed to stockholders in the form of

dividends, subject to 5% FWT) is already equivalent to 100% or more of the

paid up capital (fully paid shares of stocks)

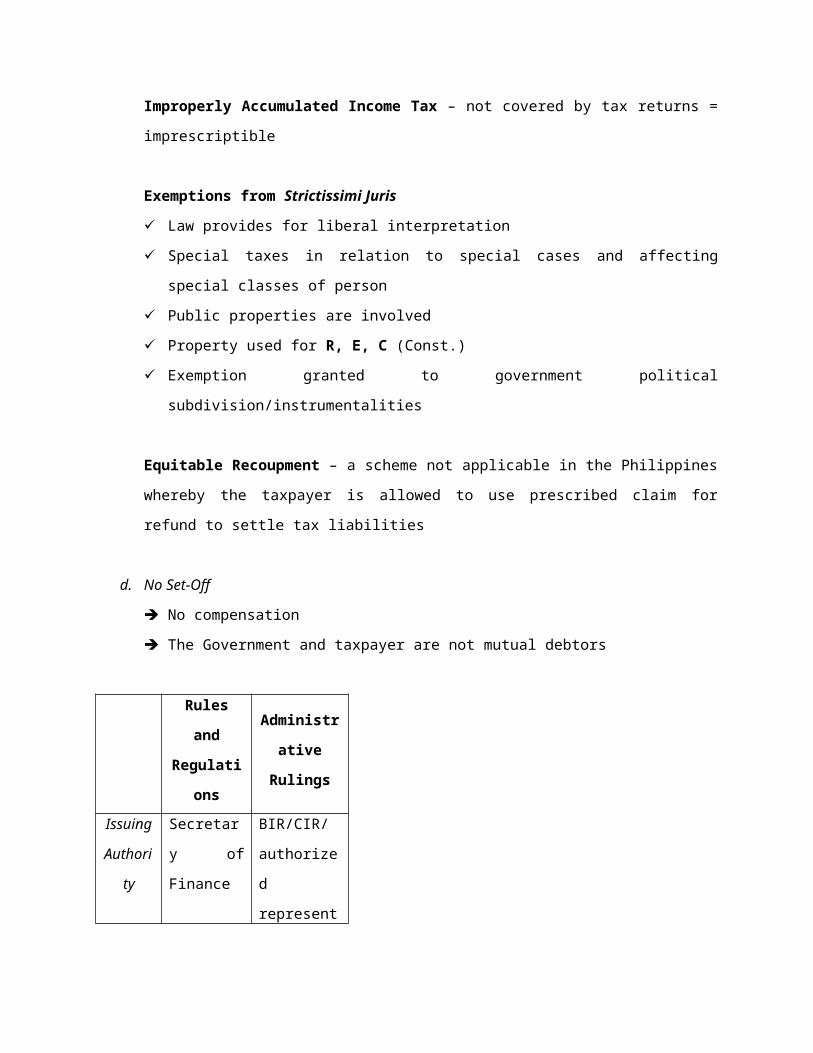

Improperly Accumulated Income Tax – not covered by tax returns =

imprescriptible

Exemptions from Strictissimi Juris

Law provides for liberal interpretation

Special taxes in relation to special cases and affecting special classes of

person

Public properties are involved

Property used for R, E, C (Const.)

Exemption granted to government political subdivision/instrumentalities

Equitable Recoupment – a scheme not applicable in the Philippines

whereby the taxpayer is allowed to use prescribed claim for refund to settle

tax liabilities

d. No Set-Off

No compensation

The Government and taxpayer are not mutual debtors

Rules

and

Regulati

ons

Administr

ative

Rulings

Issuing

Author

ity

Secretary

of

Finance

BIR/CIR/

authorized

representa

tive

Nature Implemen

ting rules

of tax

(CIR)

Rulings of

First

laws

(binding

upon

courts

and

applicable

to all

taxpayers

)

Impression

(not

binding

upon

courts, but

only

considered

with great

weight,

because

those are

only “best

guess” on

novel

issues

and

applicable

only to

those who

requested

the

rulings)

INCOME TAXATION

INCOME

All wealth other than mere return of capital

Profit of service, products, etc. coming to a certain person/company for a specific

period of time (amount of money)

Flow of wealth

Fruit of one’s labor

CAPITAL

Fund existing at the instance of time which can be used for purchase of goods

Not subject to tax

Fund/property

FOREIGN EXCHANGE

Conversion of one currency to another

Taxable event only if it is a buying and selling business

TEST IN DETERMINING EXISTENCE OF INCOME

1. Severance/Realization Test

Separation of something of exchangeable in value

2. Tax Benefit Rule

Benefit obtained in the payment of taxes

Economic Benefit

Increase in net worth of taxpayer whatever may have been the mode by

which it is effected

3. Claim of Right Doctrine

Taxable gain is conditioned upon presence of a claim of right to the alleged

gain/absence of a definite unconditional obligation to return

4. Income from Whatever Source

Flow of wealth regardless of source of income even if the source is illegal

REQUISITES FOR TAXABILITY OF INCOME

1. Existence of gain

2. Realization of gain

a. Actual – taxpayer has full control over income and physical possession

thereof

b. Constructive – taxpayer has no physical possession but with control over the

income (sec. 26 and 73(D), NIRC, bank account)

c. Presumptive – provided under the law (sec. 24(d), NIRC)

Sec. 24(d), NIRC

Sale of real property

Capital asset = not related to business(ordinary asset = related to

business)

Capital Gains Tax – 6% of the gross selling price/market value,

whichever is higher

Market Value – may be fair market value (determined by Assessor) or

zonal value (determined by BIR)

e.g. GSP = 3M 6% CGT

FMV = 2M

ZV = 1M

3. Gain must not be excluded by law

General

Professional

Partnership

Business

Partnership/

General Co-

Partnership

Constructive

receipt of

income

Actual receipt

of income

Not treated as

corporate

taxpayer

Treated as

corporate

taxpayer

among other

kinds of

partnership

except GPP

Not considered

as income

taxpayer

30% income

tax

Partners as

individual

taxpayer

Partnership

Income = 30%

Dividend = 5%

FWT

TAX BENEFIT RULE = seemingly non-taxable event but considered taxable

because of the tax benefit given to the taxpayer

e.g. BAD DEBT

Debt which cannot be collected

Debt is stricken off/written off the Books

Reduces NI = TI

Diligent effort to collect = allowable deductions (not all expenses can be

deducted)

Uncollectibility is certain

Allowance Method – method practiced by accountants whereby they

reserve a particular amount as bad debt, which CANNOT be treated as BAD

DEBT EXPENSE (BDE) for purposes of taxation

If collected subsequently, it will be taxed = seemingly non-taxable event

e.g.Yea

r 1

Year

2

Yea

r 3

GI 2M 5M 3M

AD 2M 2M2.5

M

NI – taxable

(default)0 3M

0.5

M

BD

E(subseque

ntly

recovered)

-1M -1M -1M

Net

Income/Lo

ss

-1M 2M

-

0.5

M

No

ben

efit

=

not

taxa

ble

w/

bene

fit

(exc

used

from

taxat

ion)

= 1M

taxa

ble

w/

ben

efit

=

0.5

M

taxa

ble

SURCHARGE

1. Ordinary – 25%

2. Fraud – 50%

PHILIPPINE INCOME TAX SYSTEM (Mixed)

1. Global System = fixed rate + schedular rate

Aggregation of all income regardless of source

2. Schedular System – based on the nature of income

SOURCE PRINCIPLE

Kinds of Taxpayers

1. Individual – calendar year (Jan. to Dec.)

2. Corporate – fiscal year (any 12-month period ending in any month other than

Dec.)

3. Estates – only if under judicial settlement; otherwise, the heirs are the taxpayers

(individual)

4. Trusts – only if irrevocable

3 Parties

TRUSTOR – taxpayer if trust is revocable

TRUSTEE – in possession of property when Trust is taxed

BENEFICIARY

Individual Taxpayer

1. Resident Citizen (RC) – income from within AND outside Philippines

2. Non-Resident Citizen (NRC) – income from within Philippines

Sec.22, NIRC

Establishes to the satisfaction of the CIR of his physical presence abroad

Leaving the Philippines with intent to permanently reside abroad as an

immigrant worker

Employment requires physical presence abroad for more than 183 days

(“most of the time”), which needs not be continuous

3. Resident Alien (RA) – income from within Philippines

An alien who comes to the Philippines for a definite purpose but has extended

his stay in the Philippines (temporary home)

Stayed for at least 1 calendar year

4. Non-Resident Alien – income from within Philippines

a. Engaged in Trade/Business (NRA-ETB)

Stayed in the Philippines for more than 180 days

b. Not Engaged in Trade/Business (NRA-NETB)

Corporate Taxpayer

1. Domestic (DC) – income from within AND outside Philippines

2. Resident Foreign (RFC) – income from outside Philippines

3. Non-Resident Foreign (NRFC) – income from outside Philippines

Elements in Taxing NRCs

1. Previously classified as NRC

2. Intent to reside in the Philippines permanently during the taxable period he

arrived (the period of arrival is the beginning of the taxable year)

Jan. May Dec.

lll

abroaddate of arrival

500k 700k

Not taxable taxable

OVERSEAS CONTRACT WORKERS – NRC

SEAFARER – NRC if with concurrence of:

1. Receiving compensation for services rendered abroad as a member of the

complement of a vessel

2. The vessel is engaged in international trade

RFC and NRFC – the determining factors are the continuity of transaction in the

Philippines and its conduct of business

SOURCE (SITUS) OF INCOME

1. Service – where the act that produced the income is performed

e.g.: X: employee of A

A: Domestic Corp

HK:HK-based subsidiary Corp of A

X: was sent to HK for a project

: 190 days abroad

: received salary and allowance from A

APPLICABLE TAXES:

HK: NRFC – income earned from within the Philippines

X: NRC (190>183) – income earned from within the Philippines

Salary: for service rendered – performed in HK = not taxable

Allowance: for project – performed in HK = not taxable

2. Interest Income – obligation of a resident

e.g.: X: RC

HK: NRFC

X: sent machines to HK for repairs

:total cost = 1M

: down payment = 500k

: 500k 5 equal installments with interest at 10% per annum

X: a RC who has the obligation to pay interest = taxable

3. Dividends – GI of the corporation declaring the dividends

Share of stockholders from the profit of the corporation

(a) cash – taxable

(b) property – taxable

(c) stock – GR: not taxable

(d) liquidating – GR: not taxable

Domestic – GI from within Philippines

Foreign – GI from within and outside Philippines

(1) date of declaration of the distribution of dividends

(2) compare GI

Count 3 years ending taxable year prior to declaration

Compare GI from within Philippines and worldwide income (WW)

WW = income from within + income from outside

If WW = 50% or more = considered income from within

If WW = less than 50% = pro-rated

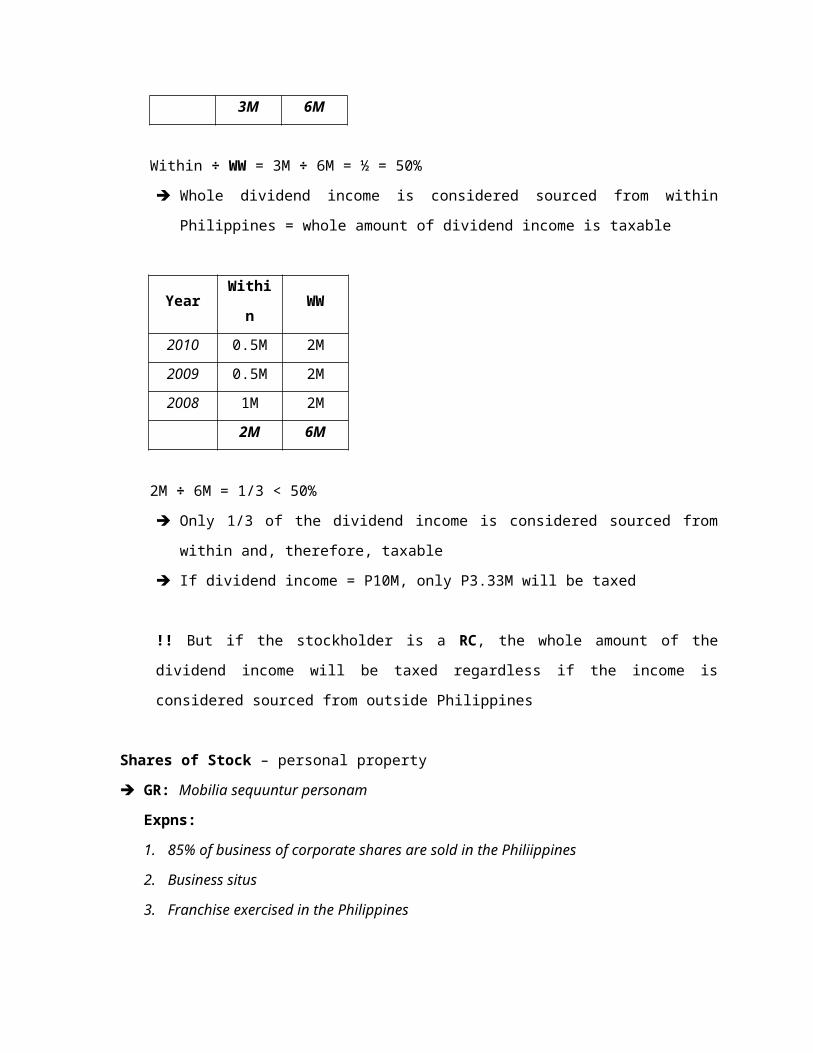

e.g.:2011 – declaration

2010 – ending taxable period prior to declaration

2009 to 2010 – 3 years prior to declaration

Year GI WW

Withi

n

2010 1M 2M

2009 1M 2M

2008 1M 2M

3M 6M

Within ÷ WW = 3M ÷ 6M = ½ = 50%

Whole dividend income is considered sourced from within Philippines =

whole amount of dividend income is taxable

YearWithi

nWW

2010 0.5M 2M

2009 0.5M 2M

2008 1M 2M

2M 6M

2M ÷ 6M = 1/3 < 50%

Only 1/3 of the dividend income is considered sourced from within and,

therefore, taxable

If dividend income = P10M, only P3.33M will be taxed

!! But if the stockholder is a RC, the whole amount of the dividend income

will be taxed regardless if the income is considered sourced from outside

Philippines

Shares of Stock – personal property

GR: Mobilia sequuntur personam

Expns:

1. 85% of business of corporate shares are sold in the Philiippines

2. Business situs

3. Franchise exercised in the Philippines

4. Sale of Property – depends on whether personal or real

(a) Real – location

(b) Personal – passage of title test

Passage of Title Tests

1. Free on Board (FOB) Shipping Point–ownership is transferred at shipping point

e.g. US US Port Philippines

Ownership is transferred at the US Port

Tax situs is US

2. FOB Destination–ownership is transferred at the point of destination

e.g. US US Port Philippines

Ownership is transferred at the Philippines

Tax situs is Philippines

Manufactured in the Philippines sold outside Philippines

Partly within and partly outside

!!! CIR v. BAIER-NICKEL

Case of BOAC its airplanes have no landing rights in the Philippines but it

maintains a liaison office, which sells tickets in the Philippines

The activity/product/service that produced the income is the selling of tickets in

the Philippines

The tax situs is the Philippines = taxable

5. Rents – where exercised

e.g. Real property – located in Japan owned by a Filipino residing in Japan who

rented it out

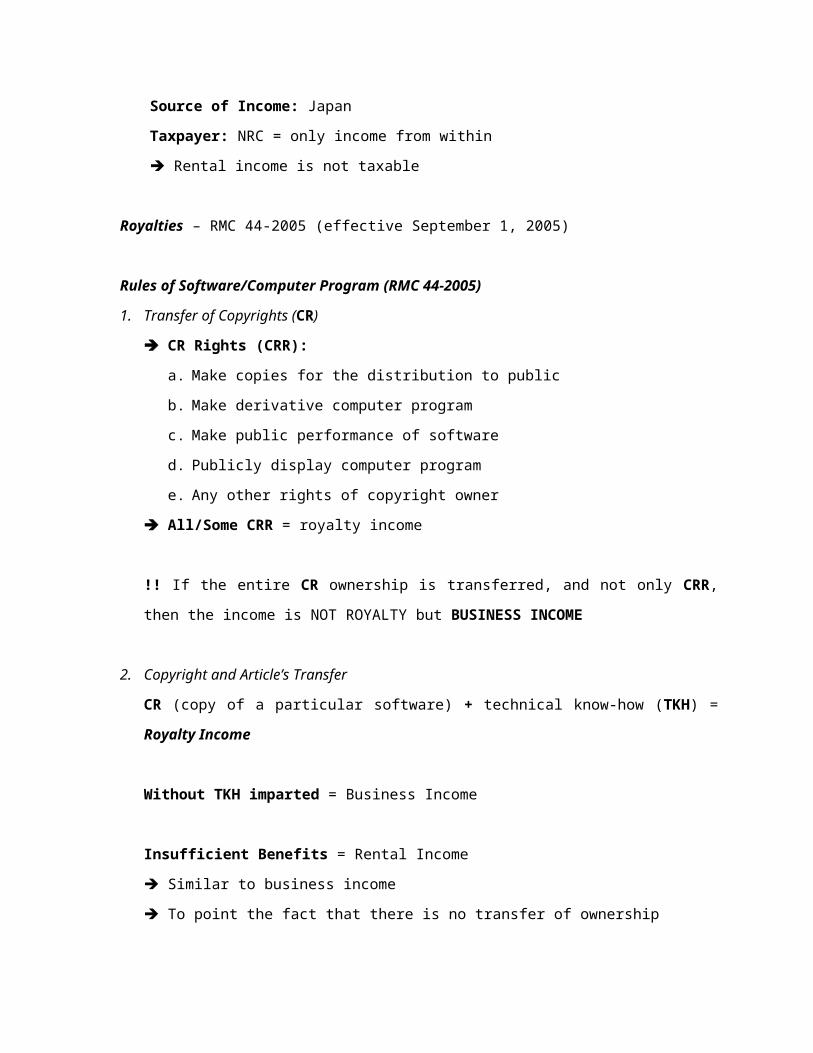

Source of Income: Japan

Taxpayer: NRC = only income from within

Rental income is not taxable

Royalties – RMC 44-2005 (effective September 1, 2005)

Rules of Software/Computer Program (RMC 44-2005)

1. Transfer of Copyrights (CR)

CR Rights (CRR):

a. Make copies for the distribution to public

b. Make derivative computer program

c. Make public performance of software

d. Publicly display computer program

e. Any other rights of copyright owner

All/Some CRR = royalty income

!! If the entire CR ownership is transferred, and not only CRR, then the

income is NOT ROYALTY but BUSINESS INCOME

2. Copyright and Article’s Transfer

CR (copy of a particular software) + technical know-how (TKH) = Royalty

Income

Without TKH imparted = Business Income

Insufficient Benefits = Rental Income

Similar to business income

To point the fact that there is no transfer of ownership

3. After-Sale Services

Depends on the Purpose

a. Use of software = royalty income

b. Provision of service = service income

Identify which is the principal and which is the ancillary purpose (ancillary

follows the tax treatment of the principal)

If both are principal, apportion the income

4. Site License/Network License Agreement

Transferee rights to make multiple copies of program for operation only

within its own business

Business income

5. Supply of Information

The computer programmer supplies information, formulae, principle which

cannot be separately copyrighted

Royalty income

6. Transfer of ownership on CR

Business Income or Capital Gains (for persons not engaged in business)

Royalty Business

20% (gross

amount of

royalties) FWT

Normal tax

No expense

deducted

With allowable

deductions

BIR DA-ITAD

e.g. Texas Instruments (Singapore) provided program and training in TI (Phils.)

a. provision of program = transfer ownership of ownership of program =

business income Principal

b. Training = technical know-how = royalty Ancillary

Whole service = Business income (ancillary follows the treatment of the

principal)

RMC 77-2003 – repealed by RMC 44-2005

All computer programs = royalty

6. Prizes – with exertion of effort (active)

P10k or less = not taxable

More than P10k = 20%FWT

Winnings – without exertion of effort (passive)

20% FWT

7. Pensions Compensation Income

GROSS INCOME

Sec. 27(a), NIRC

GI = GS or GR minus Sales Discount, Cost of Sales, Sale Returns

Sec. 32(a)

All pertinent items enumerated under sec. 32(a) and covers income from

whatever source

Compensation Income (CI)

Gross CI minus (Exclusions + Personal Exemption) = TI = tax base

Exclusions – SSS, GSIS, Pag-IBIG

Personal Exemption – assistance corresponding to support from the government

which is not applicable to NRA

Taxable Income (TI) from Business, Trade, and Profession

GS/GR

- COS/CoR

GI

- AD .

NI = TI

RECAP: Taxability of Income:

1. Existence of gains

2. Realization of gains

3. Not excluded by law

EXCLUDED BY LAW

1. Life Insurance

e.g.X Corp: Insurer

A: Insured

B and C: Beneficiaries

A died

P1M B and C

Income in nature but not treated as income for taxation purposes

Treated as indemnity = not taxable

2. Return of Premium

Mere return of capital not taxable

e.g. X: insured

A: insurer

Premium = P250k

Insurance Contract: if X survives in 10 years, he will receive P1M

X: survived in 10 years

: received P1M

P1M

- 250k premium = return of capital

750kincome = taxable

3. Gifts – donor’s tax

Bequests – personal estate tax

Devises – real property tax

Already subject to another type of tax: not included in GI anymore

4. Compensation from Injuries (Personal Injury)/Sickness

Hospital and Medical Expense = indemnity not taxable

Cost of Repair = return of capital not taxable

Moral Damages = personal injury not taxable

Attorney’s Fee = expense not taxable

Earned Salary = personal injury not taxable

Loss of Profit = opportunity loss taxable

5. Exempt under Treaty

Should be invoked by the taxpayer (SC Johnson Case)

6. Retirement Benefits

GR: Subject to tax

Expns:

a. Granted under Reasonable Private Benefit Plan (RPBP)

At least 50 years old

At least 10 years in service

Availed of the benefit of being excluded from tax for the first time

b. Without RPBP

60 to 65 years old

At least 5 years in service

c. Silent presume with RPBP

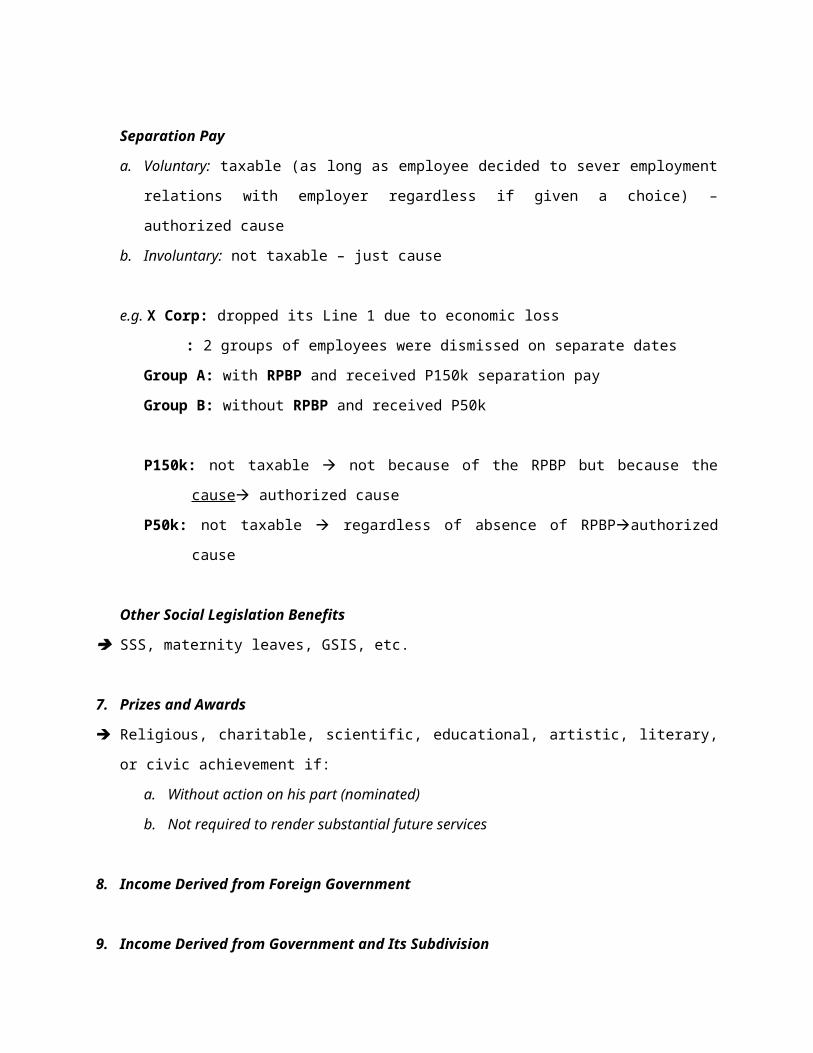

Separation Pay

a. Voluntary: taxable (as long as employee decided to sever employment

relations with employer regardless if given a choice) – authorized cause

b. Involuntary: not taxable – just cause

e.g. X Corp: dropped its Line 1 due to economic loss

: 2 groups of employees were dismissed on separate dates

Group A: with RPBP and received P150k separation pay

Group B: without RPBP and received P50k

P150k: not taxable not because of the RPBP but because the cause

authorized cause

P50k: not taxable regardless of absence of RPBPauthorized cause

Other Social Legislation Benefits

SSS, maternity leaves, GSIS, etc.

7. Prizes and Awards

Religious, charitable, scientific, educational, artistic, literary, or civic

achievement if:

a. Without action on his part (nominated)

b. Not required to render substantial future services

8. Income Derived from Foreign Government

9. Income Derived from Government and Its Subdivision

10. Prizes and Awards in Sports Competition

a. Local and international sports competition and tournaments

b. Sanctioned by national sports association

11. Gains from Sale of Bonds, Debentures, and Other Certificates of

Indebtedness

a. Sale of bonds, debentures, certificates of indebtedness

b. Maturity of more than 5 years

12. De Minimis Benefit

Benefits in small value – not taxable

Uniform allowance (UA) = up to P5k

Christmas bonus ( CB) = up to P5k

Rice allowance (RA) = up to P1,500 per month

e.g.

13th month 10K 10k

14th month 10K 10k

Productivit

y bonus5K 5k

CB 7KDM =

5k2k

UA 8KDM

=5k3k

RA 10KDM =

18k/yr0

30k

not

taxable

!!Benefits up to P30k is not taxable (#13)

13th month 15 k 15k

14th month 15k 15k

Productivit

y bonus1k 1k

CB 5k 0

UA 8k 3k

RA 10k 0

34k

30k = not

taxable

4k =

taxable

13. 13th Month and Other Benefits

Up to P30k

e.g. GS minus (SSS + Pag-IBIG + PhilHealth + Union Dues) = TI

RMC 27-2011

Whole amount (SSS, PhiliHealth, etc.) = not taxable

REPEALED by RMC 53-2011

July 2, 2011

Sec. 32(b): mandatory contributions only

SSS, PhilHealth, etc. = not taxable only up to the amount mandated

by law (EXCESS = not included in social legislation investment =

taxable)

RA 9994

Seniors are exempt from individual income tax if he is a minimum wage earner

(private government)

RA 9504, RR 10-2008

MINIMUM WAGE EARNER (MWE)

Exempt from income tax and withholding tax

Daily rate = Wage Order

+ Night Shift Differentials, Overtime Pay, Holiday Pay, Hazard Pay = still

minimum wage earner not taxable

+ Commissions, Honoraria, Fringe Benefits, Taxable Allowance (up to 30k = not

taxable; more than 30k = entire amount is taxable with both income and

creditable withholding) = entire earnings is taxable with both income and

creditable withholding tax

!! MWE + Income from Business, Trade, or Profession = whole amount subject to

income tax but not CWT

Public School Teachers not MWE

Subject to monthly CWT and annual FWT

DE MINIMIS

Not subject to Fringe Benefit Tax (FBT)

Exclusive enumeration RR 5-2011

1. Leave Credits

a. Private – only UNUSED VACATION LEAVE

Government – unused vacation AND sick leave

b. No. of Days to be Monetized – not taxable

Private: up to 10 days UVL

Government: up to 10 days UVL and 10 days USL

!! VL and SL not mandatory

Service Incentive MANDATORY

combination of SL and VL

Private: identify VL

Government: no limit

: both VL and SL

: no need to identify

!! If used compensation income

taxable = normal tax

CWT

2. Medical Allowance

a. Employee – P10,000.00

b. Dependents of Employees – P750.00 per semester = P1,500.00 per year

3. RA– P1,500.00 per month = P18,000.00 per year

4. UA – P5,000.00 (RR 8-2012)

5. Laundry Allowance – P300.00 per month = P3,600.00 per year

6. Employment Achievement Awards

Tangible personal property (actual monetary value = P10,000.00 not taxable)

other than cash and gift certificates (taxable)

7. Daily Meal Allowance

25% of minimum wage

ONLY if in favor of employee who works on overtime and night/graveyard shift

8. Gift of Flowers, etc. – taxable (RR 5-2011)

9. Representation And Transportation Allowance (RATA) and PERA

a. Government – not taxable

b. Private – GR: taxable

Expn: concurrence of:

Advance/reimbursements which are pre-computed on daily basis

Expense is necessary for business or trade of employer

Expense is liquidated

!! If not spent but KEPT taxable

10. Employer’s Convenience Rule

DA-233-07

BIR mobile allowances and communication allowances granted to employee =

NOT TAXABLE IF necessary business

e.g. Marketing supervisor communication allowance call different clients =

not taxable

FRINGE BENEFIT

subject to Fringe Benefit Tax(FBT) FWT paid by employer

granted to managerial/supervisory employees only for their benefit

e.g.

P10,000.00 granted by employer for personal use to:

a. MANAGER = taxable income FBT = FWT

b. CLERK not managerial rank and file = taxable income CI = CWT

GR: tax = 32% gross up monetary value

Expns:

a. 25% NRA-NETB

b. 15% special individual taxpayer

!! Special Individual Taxpayers taxpayers employed in:

a. Regional Area Headquarter

b. Regional Operating Headquarter

c. Offshore Banking Unit

d. Foreign Service Contractor/Sub-Contractor in Petrol Business

Gross Up Monetary Value (GUMV) = Monetary Value + FBT

GUMV value of FB inclusive of tax

Monetary Value (MV) = GUMV – FBT

MV FB Net of Tax = assumed value received

32%

68%

FB

FBT

MV = Net of Tax

GUMV = MV ÷ 68%

e.g.MV = P10,000.00

GUMV = P10,000.00 + 32% GUMV

X = 10,000 + 0.32 X

X – 0.32 X = 10,000

0.68X = 10,000

0.68 0.68

1. Housing

a. Transfer of use and possession

b. Transfer of ownership

Expn (Not Taxable):

a. AFP near military camp

b. Adjacent to business premises (within 50 km)

c. Temporary (3 months/less) use of employee

2. Expenses

Personal use of employee

If necessary for business = NOT FBT

3. Vehicle

a. Employer gives cash

b. Car delivered to employee

c. Transfer of ownership

d. Employer allowed employee to use company car for personal use

!! Official Use = employers benefit NOT FB

4. Household Expenses – household maid/helper, driver, etc.

5. Interest Foregone

Actual Interest Rate v. Market Rate

12% as per CB Circular

e.g. A manager of Metrobank

15% interest

30% interest normally given by Metrobank

ActualMarket

15% > 12% NT

10% < 12% 2% FBT

6. Membership Dues

Social/athletic clubs/akin thereto

Borne by employer

7. Foreign Travel

Personal use of employee

Should be documented substantiated by receipts

If not substantiated, entire amount = FBT

Expn (not taxable):

a. Attend meetings, etc. (employer’s benefit)

b. Inland travel

c. Hotel accommodation up to $300 per day

d. Airfare economy/business class ticket

first class ticket up to 70%

8. Holiday and Vacation Expense

9. Educational Assistance

Employee/dependent

Expn (not taxable)

a. Education should be necessary for business/trade of employer

Written Contract condition of future rendition of service of employee

b. Competitive scheme under a scholarship program by the employer

10. Life Insurance

Premiums paid by employer in excess of what the law allows

Beneficiary:

a. Employee/his family CI NT (sec. 32 (B), NIRC)

b. Employer NT (sec. 32 (B), NIRC)

Indemnity exempted under sec. 32 (B), NIRC

!!Rank and File(R&F) life insurance paid by employer beneficiary =

R&F/family benefit = TI CWT premium payment not indemnity

R&F not managerial not FB XFWT

TAX OPTION

a. Shares listed presumptive gain ½ of 1% of gross sales

b. Not listed actual gain

STAGES OF CONTRACT

1. Negotiation

2. Perfection approval of income

3. Consummation

TAXPAYER’S SUIT

1. Extraction of taxes

2. Such extraction is illegal

Dividends who declares

1. Domestic within

2. Foreign outside

Should be operating in the Philippines for 3 years as per BIR Ruling

EXPANDED FOREIGN CURRENCY

Income is not taxable if income earner is non-resident even if sourced from

within

NRF Corp automatically not engaged in business

PASSIVE FWT except lease income

RR nature of subordinate legislation binding upon courts

Pensions from foreign companies exempt from taxes

PURCHASE NT no flow of wealth on the part of the buyer

!!! CIR v. GEN. FOODS

Advertising Expense allowable deductions reasonable amount only

MCIT not tax on capital valid

tax basis = GI not capital

EMPLOYER’S CONVENIENCE RULE

Benefit of employer not FB

Expense for employer NT

!!All benefits derived from employer-employee relationship = CI

ALLOWABLE DEDUCTIONS (AD)

Recognizable against:

X CI

Income from Business, Trade, or Profession (BTP) must be related to BTP

e.g. Rental Income= business income all income derived from lease

Maintenance ExpenseAD

2 individuals: A owner of building

B Lessee of building

A: statutory taxpayer rental income

B: rental expense

!! Stipulation that B will shoulder tax – VALID income on the part of

A Rental Income

CASH BASIS ACCRUAL BASIS

Income

recognized

once collected

Income recognized

once accrued

whether

whether

earned or

unearned

collected/uncollecte

d

May be used

by service

enterprise

Must be used by

manufacturing/retail

enterprise

e.g.A: business of buying and selling pre-owned Louis Vuitton bags

Buy & Sell: Retail accrual basis

MONTHCOLLECTIO

N

January P10,000.00 incom

e

Februar

yP30,000.00

incom

e

March P50,000.00 incom

e

P90,000.00

!! When is income considered accrued?

When the right to collect arises perfection of contract

A: Lessor

Lease: Service cash basis

MONTHCOLLECTIO

N

Paymen

t for

January P30,000.00Nov,

Dec, Jan

Februar

yP20,000.00 Feb, Mar

March P10,000.00 April

NO INCOME for the months of November and December

Income for January: P30,000.00

February: P20,000.00

March: P10,000.00

!! Rental Expense ALWAYS accrual basis

Rental Income cash basis

J: lessee should pay every month but did not pay in March

March: Rental Expense should BE reported

Rental Income should NOT be reported

!! Prepaid Rental – advance payment for the next taxable year

!! Security Deposit

Indemnity to lessor if there are damages in leased premises

e.g. P10,000.00 security deposit

P 3,000.00 damages = indemnity not taxable

P 7,000.00 return to lessee

if kept = rental income

With Forfeiture Clause breach/violation of lease agreement = forfeit deposit

income in the year of breach

PASSIVE INCOME

GR: FWT

!!! Normal Tax – CWT

1. Royalties

a. Literary, Book, Musical Composition 10%

b. Others 20%

2. Prizes

a. P10,000.00 or less Normal tax [sec. 24 (A)]

b. More Than P10,000.00 20% of entire amount

Winnings 20% FWT

3. Interest Income

a. Bank Deposits and Deposit Substitute 20% FWT

b. Loan normal tax

Expns:

Long-term deposit/investment

holding period = not less than 5 years

v. Bonds, debentures, etc.

More than 5 years = exempt from tax

Gains from sale

Not cover exactly 5 years

e.g. Depositor 1M investment PNB

* P100,000.00 interest

* more than 5 years holding period tax exempt

* 1 month holding period 20% FWT

* 5 years holding period pre-terminated depends on the lapse

of period

Pre-

Terminate

d 5-Year

Holding

Period

Expired

Period

FWT

Rate

4 years

to less

than 5

years

5 %

3 years

to less

than 4

years

12 %

Less

than 3

years

20%

Interest income received by a member of a duly registered

cooperative CTA-registered

Expanded foreign currency deposit system

7.5% FWT if income earner is a resident

exempt if income earner is non-resident

4. Dividends

Date of declaration = right arises

Shares of stockholder in a particular corporation

May give rise to:

a. Dividend income

b. Fluctuation

Forms:

a. Cash – face value of cash

b. Property – fair market value

c. Script – provisional dividend

warrant/certificate already issued

issued in promissory note

Issue warrant/certificate

fair market value

permanent

Presumption of income

d. Liquidating – issued upon dissolution

e. Stock–GR: not subject to tax

merely represents a transfer of surplus to capital account

not represents any flow of wealth same percentage of ownership

e.g. At least 5 incorporators

In

co

rp

or

at

or

s

Co

nt

ri

bu

ti

on

s

%

of

Ow

ner

shi

p

10

%

Sto

ck

Dec

lara

tion

s

Tot

al

Sh

are

A 1k 1/8 1001,10

01/8

B 2k 2/8 2002,20

02/8

C 2k 2/8 2002,20

02/8

D 1k 1/8 1001,10

01/8

E 2k 2/8 2002,20

02/8

8k8,80

0

GR: Not taxable

Expn: When there is flow of wealth

!!! CIR v. ANSCOR

Transferring surplus

Unrealized gain

Cash dividend

STOCK DIVIDEND

GR: Not taxable

Expn:

1. Company granted options in favor of stockholder (cash/property/stock)

2. At least some exercise option to avail cash dividend

e.g.

In

co

rp

or

at

or

s

Co

nt

ri

bu

ti

on

s

%

of

Ow

ner

shi

p

10

%

Sto

ck

Dec

lara

tion

s

Sto

ck

Divi

den

d

Cho

ice

Sh

are

A 1k 1/8 100Cas

h1k

B 2k 2/8 200Stoc

k

2.2

k

C 2k 2/8 200Cas

h2k

D 1k 1/8 100Stoc

k

1.1

k

E 2k 2/8 200Stoc

k

2.2

k

8k8.5

k

Flow of wealth = taxable

Different percentage of shares

Sec. 73(B)

Dividend Equivalents redeem/cancels shares of stocks previously issued to

stockholder

Corporation reacquires shares

“Time and Manner”

question of fact

existence of dividend equivalents

should be as declaration of dividend distribution

Redemption capital transaction

!!! ANSCOR Case

criteria for dividend equivalent (not an automatic indication)

Anscor redeemed shares of Don Andres

P108,000 shares redeemed

25k original subscription

purchased by stockholder

return of capital = not taxable

83k earned by reason of stock dividend

acquired from income of corporation

stock equivalent = taxable

Requirements (sec. 73):

a. Redemption/Cancellation

b. Stock Declaration

c. Time and Manner = dividend declaration

Factual Circumstances

1. Lapse of time between of issuance to redemption not sufficient indicator to

determine taxability

2. Business Purpose should be legitimate (not taxable) at the time of

distribution

SALE OF REAL PROPERTY

Presumptive Gain 6% [sec. 24(D)]

Applicable to:

1. Sale

2. Exchange

3. Other disposition of real property (capital asset)

Pacto de retro salesale with right to repurchase execution = transfer of

ownership = CGT

Conditional sale no transfer of ownership unless condition happens = CGT

Contract to sell no transfer of ownership only upon execution of a Deed of

Absolute Sale = CGT

Forced sale properties sold due to tax lien, unpaid mortgage, etc. = CGT

Barter = exchange if resulted in income/loss = CGT

NRA-NETB 25% FWT [sec. 25(D)] except stock

Alternative/Optional Treatment in Taxation

Sale of real property (capital asset) to:

a. Government

b. Political subdivision

c. Agencies

d. GOCCs

Option of taxpayer to use 24(D) (FMV or GS) or 24(A) (normal tax with net

income as basis)

CAPITAL GAINS TAX

Within 30 days from execution of Deed of Sale violation = 20% interest per

year + 25% surcharge + compromise penalty

Avoided/Exemptions:

1. Sale of Principal Residence (Requirements):

a. New principal residence must be acquired and constructed within 18

months from sale

b. Notice to avail exemption within 30 days from execution of Deed of Sale

c. Once in 10 years availability

d. Revised Regulation

escrow account of the taxpayer will be included in CGT return

proceeds of sale should be wholly/fully utilized for acquisition of new

residence

!! If partially used: (utilized amount ÷ total proceeds) x Market Value

or GSP

2. Sale in Favor of Government

3. Comprehensive Agrarian Reform Law

4. Sec. 24(C) real property is transferred to a corporation to obtain corporate

control

Ensured by Government issuance of Certificate Authorizing Registration (RMO

15-2003)

SALES OF SHARES OF STOCKS

Sold by dealer = ordinary asset normal tax

Sold by non-dealer

Listed presumptive gain = ½ of 1% GSP

Not Listed actual gain = 5% of first 100k + 10% of excess of 100k

OTHER SOURCES:

1. Cancellation of Indebtedness

Condonation

Depends on circumstances of cancellation

e.g. A loaned 100k to B

If A cancelled B’s indebtedness by:

a. Gratuity: donor’s tax

b. Remuneration: income tax

c. Declaration of Dividends: FWT

If 3rd person renders service to cancel B’s debt: 3rd person income and

donor’s taxes

2. Leasehold

Lessor’s share in the income of lessee rental income

Improvement by lessee to be owned by lessor after lease period is Rental

Income recognized:

a. Outright FMV of improvement during the date of completion of

improvement

b. Spreadout value of improvement at the end of the lease term during the

entire period of lease

e.g. 25 M amount of construction cost of improvement

2013 finished

25 years estimated useful life

15 years lease term

Outright 25 M

Spreadout:

2013 to 2028 lease period

10 M depreciated value

Depreciation Expense (DE)

DE = Value of asset ÷ Estimated useful life

= 25M/25y

= 1M/yspread out over 15 years of lease term

3. Installment Transaction

Personal Property

a. Regular Basis automatically installment basis

b. Casual Basis initial payment (cash/property received, other than a

certificate of indebtedness, in the year of sale) should not exceed 25%

GSP

Real Property

a. Regular Basis automatically installment basis

b. Casual Basis:

Selling price is at least P1,000.00

Initial payment should not exceed 25% GSP

!! If more than 25%: Deferred sale

4. Mortgages (REM)

Public auction highest bidder Certificate of Sale

1 year redemption period:

a. If exercisedX CGT

b. If not exercised consolidation of title after 1 year (expiration of

redemption period) CGT (RR 4-99)

INSTALLMENT SALE

Real Property 25% rule + at least P1k selling price

Personal Property 25% rule

Initial Payment sec. 49, NIRC

a. Cash/Property/Shares of Stock

b. Except evidence of indebtedness

c. Received during the year the sale was made

!! Deferred Sale more than 25% down payment entire amount recognized

in the year of sale

e.g.1M (2013) selling price

600K (2013) purchase price

DP = Down Payment

1. DP = 350k (2013) Deferred = whole amount is recognized in 2013

2. DP = 200k cash + 100 shares of stock = 300k > 25% GSP deferred

sale

3. DP = 200k cash + 400k on promissory note

PN = evidence of indebtedness not initial payment

200k cash installment sale portion recognized = 200k/1M

4. DP = 200k cash + 400k on PN

PN with 10% interest and discounted to P350k

DP = 200k + 350k = 550k sufficient cashdeferred sale

METHODS OF RECOGNIZING INCOME FROM CONSTRUCTION PROJECT

1.Lump Sumnever used under long-term construction project should be

accomplished for more than one year

2. Percentage of Completion mandatory for long-term construction project

e.g.10M Cost of Project

9M Expense

1M 2013: 40%

2014: 40%

2015:20%