Tax Legislation 2017:

On the Road to Nowhere?

John Gimigliano

July2017

2 © 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Notices The following information is not intended to be “written advice concerning one or more

Federal tax matters” subject to the requirements of section 10.37(a)(2) of Treasury

Department Circular 230.

The information contained herein is of a general nature and based on authorities that are

subject to change. Applicability of the information to specific situations should be

determined through consultation with your tax adviser.

3 © 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

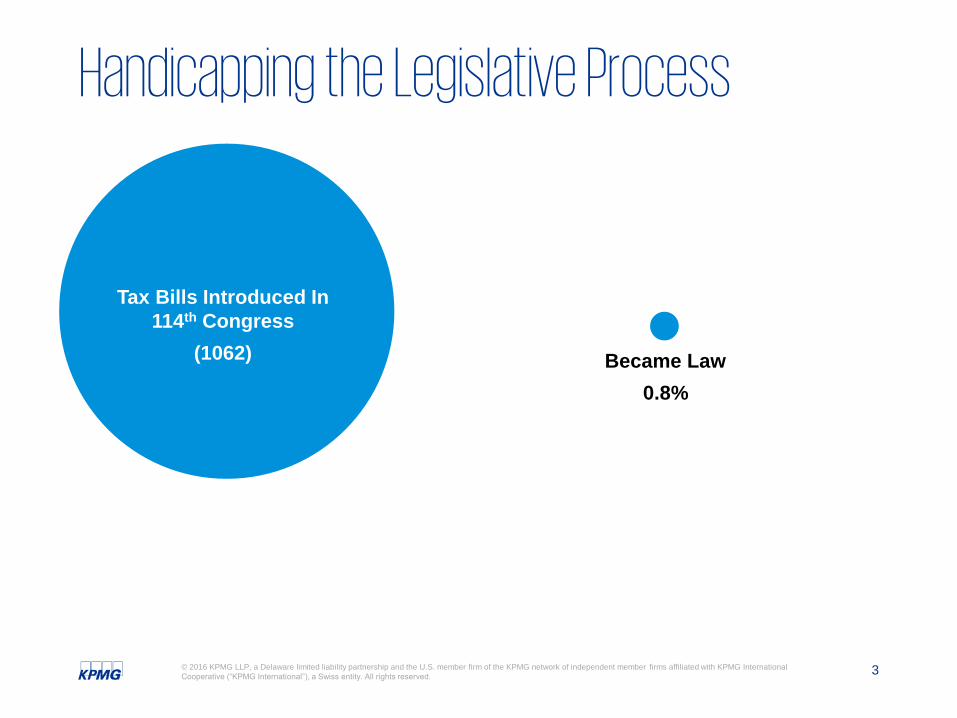

Handicapping the Legislative Process

Tax Bills Introduced In

114th Congress

(1062) Became Law

0.8%

4 © 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

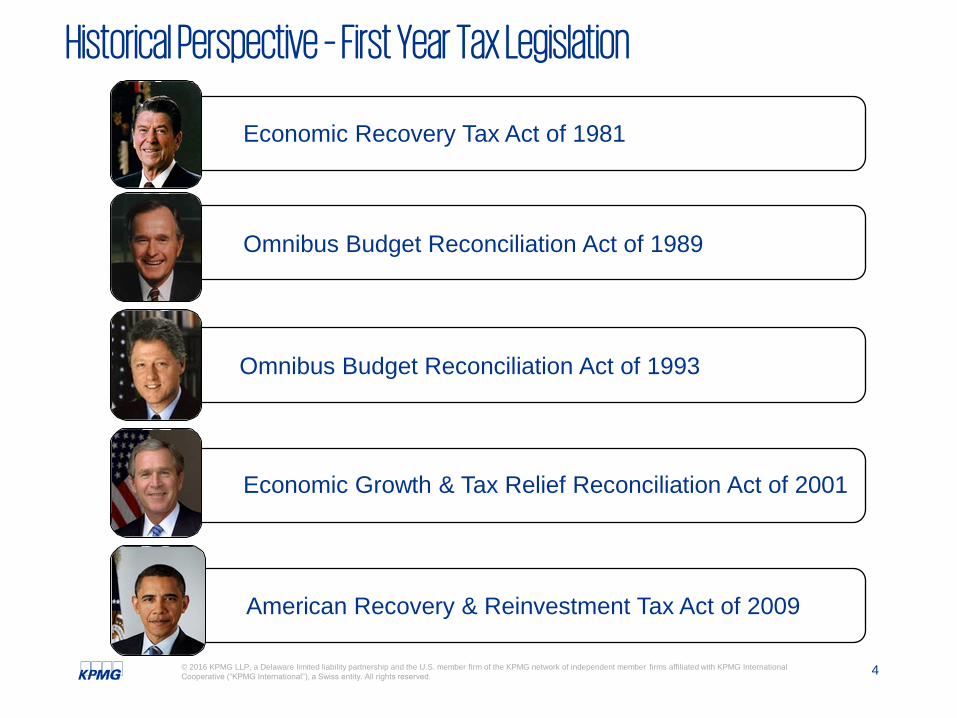

Economic Recovery Tax Act of 1981

Omnibus Budget Reconciliation Act of 1989

Omnibus Budget Reconciliation Act of 1993

American Recovery & Reinvestment Tax Act of 2009

Economic Growth & Tax Relief Reconciliation Act of 2001

Historical Perspective – First Year Tax Legislation

5 © 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Making tax law

Policy

Politics

Personalities

The Political Setting:

6

7 © 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

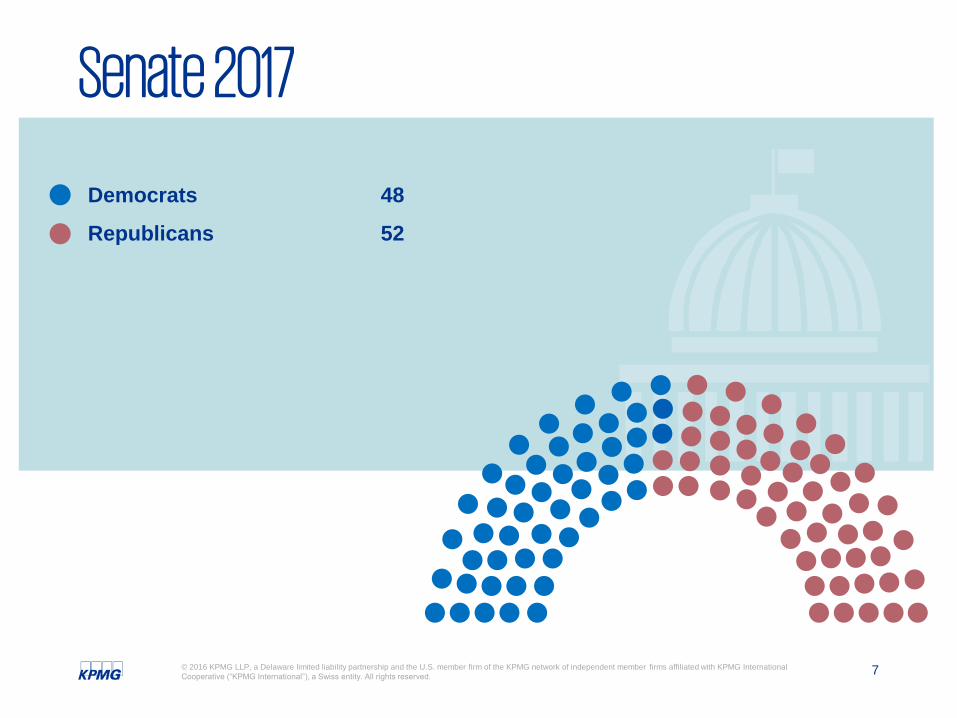

Senate 2017

Democrats 48

Republicans 52

8 © 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

House 2017

Democrats 194

Republicans 241

9 © 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Elections: United States Senate election map, 2018

Democratic

incumbent*

Republican

incumbent

Independent

incumbent

*Includes 10 of 12 Democratic Finance Committee members

*

* *

*

* *

*

*

*

*

10 © 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

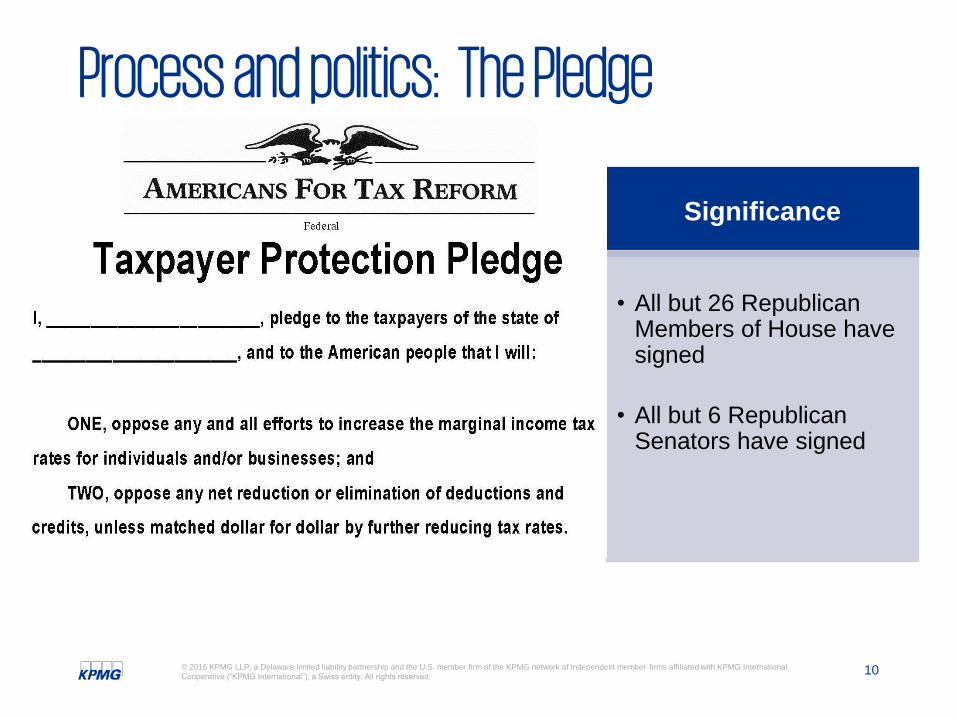

Process and politics: The Pledge

Significance

• All but 26 Republican Members of House have signed

• All but 6 Republican Senators have signed

The Personalities: Principal Tax Writers

12 © 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

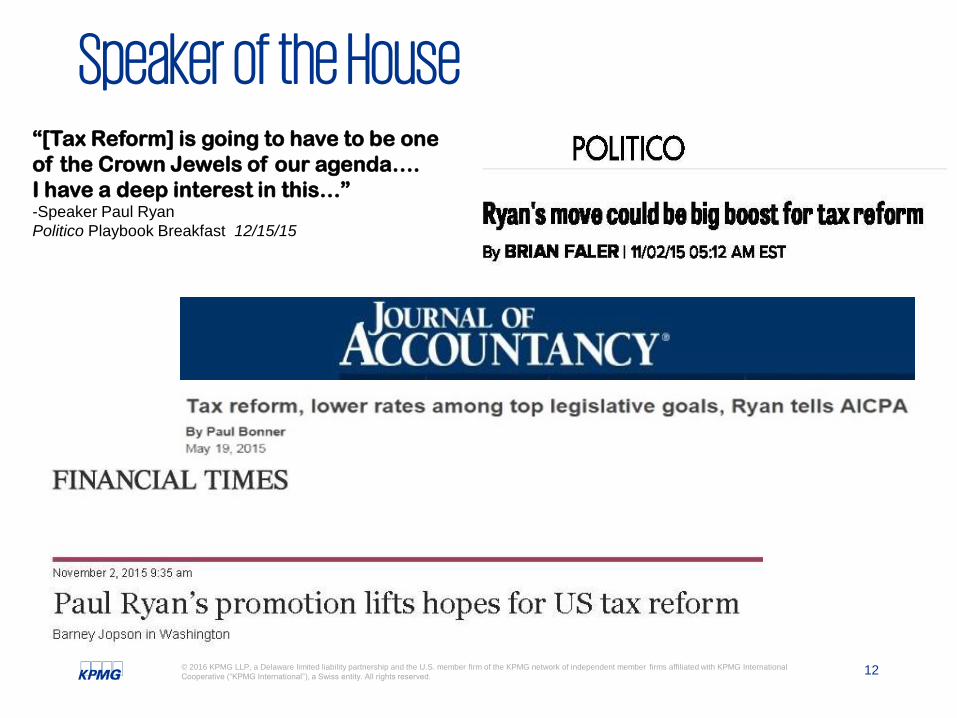

Speaker of the House “[Tax Reform] is going to have to be one

of the Crown Jewels of our agenda….

I have a deep interest in this…” -Speaker Paul Ryan

Politico Playbook Breakfast 12/15/15

13 © 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

The “Big Four”

Chair: Orrin Hatch (R-UT)

Senate Finance Committee:

Chair: Kevin Brady (R-TX)

Ranking Member:

Ron Wyden (D-OR)

Ranking Member:

Richard Neal (D-MA)

Ways & Means Committee:

14 © 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

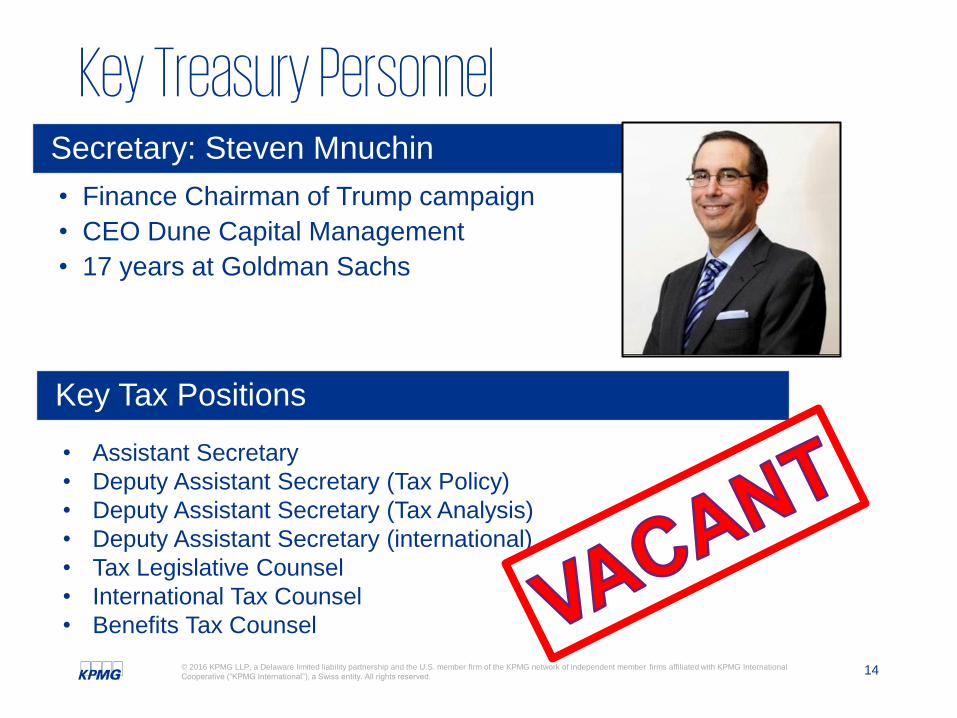

Secretary: Steven Mnuchin

• Finance Chairman of Trump campaign

• CEO Dune Capital Management

• 17 years at Goldman Sachs

Key Treasury Personnel

Key Tax Positions

• Assistant Secretary

• Deputy Assistant Secretary (Tax Policy)

• Deputy Assistant Secretary (Tax Analysis)

• Deputy Assistant Secretary (international)

• Tax Legislative Counsel

• International Tax Counsel

• Benefits Tax Counsel

Policy: Tax Reform

15

16 © 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Tax Reform: U.S. and other OECD statutory corporate tax rates

Source: Forbes - http://blogs-images.forbes.com/niallmccarthy/files/2016/07/20160713_Corporate_Tax.jpg

(Percent)

17 © 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Tax Reform: Statutory tax rates, United States and OECD

Source: Tax Foundation (http://taxfoundation.org/article/countdown-over-were-1)

18 © 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Competing Goals of Tax Reform

Distributional Neutrality

19 © 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

The House: Thinking Outside the Box

20 © 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Ways & Means strategy: towards consumption

Infrastructure

Spending

Inversions

Rate

Differentials

Income Tax VAT

Camp

Tax Reform Act

2014

Nunes

ABC Act

2015

Brady

House Blueprint

June 2016

Renacci

SATS

July 2016 Ryan/Brady

International Reform

2015

21 © 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Source: Ways and Means Committee

22 © 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Tax Reform: Why Consumption Tax?

Pro-Growth • Emphasis on Savings

• ROI on Capital Investments

Border Adjustable

• Territoriality

• Ability to attract Investment

• Manage Base Erosion

Base Broadening

• More Taxpayers

• Better Compliance

Consumption

Tax

23 © 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Outside the Box: Senate Approach Corporate Integration

• Corporate integration plan to mitigate double taxation on corporate income

• Dividend paid deduction to reduce corporate level tax to the extent of

distribution of income

• Potentially solves several problems including base erosion, debt-equity issue,

pass-through conversion, etc.

Other considerations:

• Revenue neutrality

• Shifting of tax burden

• Design complexity including tax exempts and interaction with treaty provisions

• Effect on partnerships, MLPs, etc.

• Fate of policy preferences (PTCs, ITCs, R&D, etc.)

• Hatch says “may” be released in April May June soon when advisable

24 © 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

The Senate: Back Inside the Box

Cartoon: New Yorker magazine, November 30, 1998

25 © 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Inside the Box: Senate Approach Camp Rides Again?

• “Quasi-territoriality”

• MinTax on foreign earnings

• Dividend exemption on foreign-sourced dividends

• Mandatory Repatriation

Camp and “let’s not do that again” possibilities

• MACRS remains

• Possibly permanence for bonus depreciation

• Interest deductibility and a thin-cap rule

• Innovation box regime

• Other pay fors

Question remains whether the math works and if the political calculus will

be different this time

26 © 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Arial Use for everything except titles and slide headers

(including charts, graphics, text)

KPMG Extra Light Use for title slide and main headers only

KPMG Extra Light Italics Use for emphasis in title slide and main headers only

KPMG Light When presenting in a large room, this may be used for title

slide and main headers only

KPMG Light Italics When presenting in a large room, this may be used for

emphasis in title slide and main headers only

KPMG Thin Do not use

KPMG Thin Italics Do not use

Key Proposals - Individual President Trump

(April 26, 2017)

House blueprint

Camp bill

Ordinary income rate 10%-25%-35% 12%-25%-33% 10%-25%-35%. (Special

calculation for qualified

domestic manufacturing

income) Standard deduction/personal

exemption

Double standard deduction Consolidate personal

exemption/standard deduction

into larger standard deduction

Increase standard deduction

with phase out; eliminate

personal exemptions Itemized deductions Eliminate itemized deductions

other than home mortgage

interest and charitable

deductions

Eliminate itemized deductions

other than home mortgage

interest and charitable

deductions (with possible

changes to home mortgage

interest deduction)

Eliminate many itemized

deductions, including

deduction for interest on home

equity debt. 2% floor on

charitable deductions

Individual AMT Repeal Repeal Repeal

Net investment income tax Repeal Not part of tax reform blueprint

(but contemplated as part of

healthcare)

Does not address

Investment income rate Same as current law (20%) 50% deduction for capital

gains, interest, and dividends

(6%, 12.5%, 16.5% rates)

Deduction of 40% of adjusted

net capital gain

Estate tax Repeal estate tax Repeal. Silent as to basis

consequences

Keep

27 © 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Arial Use for everything except titles and slide headers

(including charts, graphics, text)

KPMG Extra Light Use for title slide and main headers only

KPMG Extra Light Italics Use for emphasis in title slide and main headers only

KPMG Light When presenting in a large room, this may be used for title

slide and main headers only

KPMG Light Italics When presenting in a large room, this may be used for

emphasis in title slide and main headers only

KPMG Thin Do not use

KPMG Thin Italics Do not use

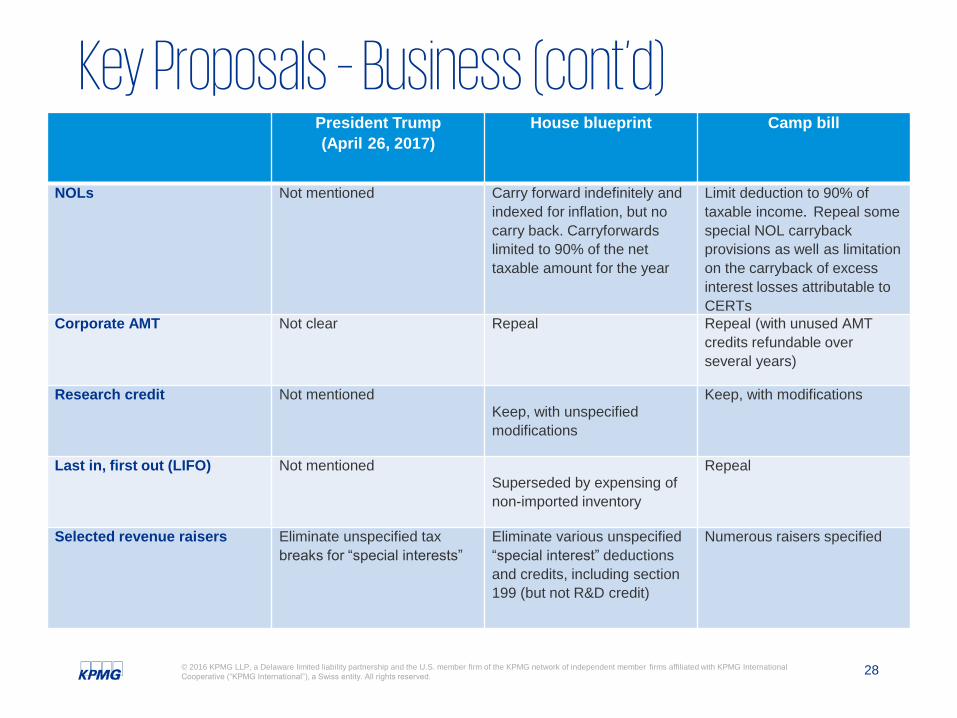

Key Proposals – Business President Trump

(April 26, 2017)

House blueprint

Camp bill

Corporate rate 15% 20% Reduce to 25% (over several

years)

Individual owners of

passthroughs and

proprietorships

15% rate, possibly limited to

“small” and “medium”

passthrough businesses (with

unspecified anti-abuse rules)

“Active business income” of

owners of passthrough entities

capped at 25% ordinary income

rate. Backstopped by

“reasonable compensation”

requirement for owner-

operators

Qualified domestic

manufacturing generally taxed

at no higher than 25%. Owners

who materially participate treat

70% of combined

compensation and distributive

share as subject to employment

taxes. Other changes to Sub K.

Carried interest Not mentioned Not clear Special rules

Cost recovery Not mentioned Full and immediate expensing

for investments in tangible

property and intangible assets,

but not land

Replace MACRS with system

that lengthens recovery lives

and indexes depreciable basis

for inflation. Extend

amortization period for acquired

Code section 197 intangibles.

Caps on expensing. Other.

Interest expense Not mentioned Net interest expense not

deductible but carried forward

indefinitely—with unspecified

special rules for financial

services companies

No broad rule, but limits

amount of deductible interest

expense that could apply to a

U.S. corporation shareholder

with one or more foreign

corporations in some cases

28 © 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Arial Use for everything except titles and slide headers

(including charts, graphics, text)

KPMG Extra Light Use for title slide and main headers only

KPMG Extra Light Italics Use for emphasis in title slide and main headers only

KPMG Light When presenting in a large room, this may be used for title

slide and main headers only

KPMG Light Italics When presenting in a large room, this may be used for

emphasis in title slide and main headers only

KPMG Thin Do not use

KPMG Thin Italics Do not use

Key Proposals – Business (cont’d) President Trump

(April 26, 2017)

House blueprint

Camp bill

NOLs Not mentioned Carry forward indefinitely and

indexed for inflation, but no

carry back. Carryforwards

limited to 90% of the net

taxable amount for the year

Limit deduction to 90% of

taxable income. Repeal some

special NOL carryback

provisions as well as limitation

on the carryback of excess

interest losses attributable to

CERTs Corporate AMT Not clear Repeal Repeal (with unused AMT

credits refundable over

several years)

Research credit Not mentioned Keep, with unspecified

modifications

Keep, with modifications

Last in, first out (LIFO) Not mentioned Superseded by expensing of

non-imported inventory

Repeal

Selected revenue raisers Eliminate unspecified tax

breaks for “special interests”

Eliminate various unspecified

“special interest” deductions

and credits, including section

199 (but not R&D credit)

Numerous raisers specified

29 © 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Arial Use for everything except titles and slide headers

(including charts, graphics, text)

KPMG Extra Light Use for title slide and main headers only

KPMG Extra Light Italics Use for emphasis in title slide and main headers only

KPMG Light When presenting in a large room, this may be used for title

slide and main headers only

KPMG Light Italics When presenting in a large room, this may be used for

emphasis in title slide and main headers only

KPMG Thin Do not use

KPMG Thin Italics Do not use

Key Proposals - International President Trump

(April 26, 2017)

House blueprint

Camp bill

Destination based cash

flow system, with border

adjustments

Not mentioned in one-page

summary document

Move towards a destination-

based tax system, with

border adjustments

Not included

Territorial system Move to territorial system.

No details.

Territorial tax system, with

100% exemption for

dividends received from

foreign subsidiaries. Repeal

most of current subpart F

regime, but retain foreign

personal holding company

rules for passive foreign

income.

U.S. corporate shareholder

gets 95% deduction for

foreign sourced portion of

dividends received from

certain foreign subsidiaries.

Complex provisions to

prevent offshore shifting of

profits. Minimum tax of 15%

on CFC’s foreign earnings.

Modify active financing

exception Repatriation of existing

earnings and profits (E&P)

Foreign earnings

accumulated under old

system taxed; rate

determined in consultation

with Congress

Foreign earnings

accumulated under old

system repatriated by paying

tax of 8.75% to the extent

held in cash or cash

equivalents or 3.5%

otherwise (payable in

installments over 8 years)

Foreign earnings

accumulated under old

system repatriated by paying

tax of 8.75% to the extent

held in cash or cash

equivalents or 3.5%

otherwise (payable in

installments over 8 years)

30 © 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

$1,325

$883

$160

$388

$185

$936

$1,172

$677

GOP House Blueprint – Doing the Math*

▼ Reduce rate to 20%

▼ Full expensing

▼ True territorial system

▼ 25% passthrough rate

▲ Repatriation at 8.75% / 3.5%

▲ Border adjustment

▲ Only “net interest” deductible

▲ Nearly all other credits/deductions eliminated

Corporate Highlights

* Tax Foundation dynamic scoring estimates from “Details and Analysis of the 2016 House Republican Tax

Reform Plan” https://taxfoundation.org/details-and-analysis-2016-house-republican-tax-reform-plan/ (July 5,

2016). Dollar amounts are in billions.

31 © 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Tax Reform and Cooperatives: Considering the Options Options 2: Camp Approach - make conforming and

consistent changes only.

Option 3: Repeal Subchapter T and 501(c)(12)

Option 1: Do nothing

Where to from here?

33 © 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

The Universe (?) of Options – What can be done?

Go Big (Major rate reduction, restructuring of tax system)

The Blueprint

Credit Invoice (i.e., traditional) VAT

Revenue Losing Tax Reform (i.e., tax cuts)

Corporate Integration (e.g., DPD)

Political Orphans – Camp 2014, Carbon Tax

Go Small

Modest rate cuts

Repatriation only (mandatory or voluntary)

Small business + individual?

Payroll tax holiday

34 © 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

The Universe (?) of Options – How to do it? Getting to 60

Can it be done part one

Can it be done part two

Budget Reconciliation -

About that budget . . .

Achieving permanence through revenue neutrality

“Flexibility” in defining neutrality

Revisit the budget window

One last option . . .

Thank you

36 © 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Contact us

John P. Gimigliano

202-533-4022

@johngimigliano