Tax Audit Report

Presented by CA Kusai Goawala

23rd August 2015

For WICASA jointly with Pune Branch of ICAI

Regulatory

CBDT notification no. 33/2014 dated 25.07.2014.

Amendments in Form 3CA, 3CB and 3CD

Made effective for Tax Audit for assessment year 2014-15

3CA where audit conducted under any other law

3CB where audit not conducted under any law

3CD form of particulars applicable to both - certificate

CA KUSAI GOAWALA

Basic Principles underlying the amendments

Bridge between the Direct and Indirect Tax Comprehensive Information Higher level of commitments from :

Management Auditor

Updated with the recent amendments in the IT Act

CA KUSAI GOAWALA

Part A : Clause 4 : Applicability and Registration under Indirect Tax laws

To ascertain which of the Indirect Taxes are applicable

– Service tax, VAT, Excise, Customs etc

If applicable whether registered. Registration number

or any identification number allotted to be given

Auditor has to first ascertain which Indirect Tax Laws

are applicable to assessee. Exchange of Vehicle by a

service company – VAT is applicable if exceeds the

limit.

CA KUSAI GOAWALA

44AB (a) Based on Turnover – Rs.1 crore for business

Whether purchase is considered as turnover for this purpose.

and (b) Rs.25 lacs for profession. 44AB (c)& (d) Turnover lower than

above, but profit lower than presumptive profit – 44AE, 44AD, 44BB, 44BBB

Part A : Clause 8 : Sub-section of 44AB under which Audit is conducted

CA KUSAI GOAWALA

Part B : Clause 11 (b) and (c) ; Location of books to be maintained and other documents

Auditor to indicate the location where the books of accounts are maintained.

Companies Act 2013 permits maintaining books in electronic mode – increase mobility.

Cloud Environment – Where is the location of the server

Location of books at what point of time. If the books of accounts are not kept at one

location, please furnish the addresses of locations along with the details of books of accounts maintained at each location.

List of other documents examined – what is meaning of other documents.

CA KUSAI GOAWALA

Part B : Clause 17 : Property transferred at less than Stamp Duty Value – 43CA and 50C

Information to be provided :

Details of PropertyConsideration as per

AgreementValue as per Stamp Duty

Ready Reckoner

CA KUSAI GOAWALA

Contd…

50C applies to Capital Asset whereas 43CA applies to Stock in Trade.

Verify agreements and documents.

Agreement Registered but sale not recognised.

Sale recognised on percentage completion method.Agreement executed but

Registration after considerable lapse of time.

CA KUSAI GOAWALA

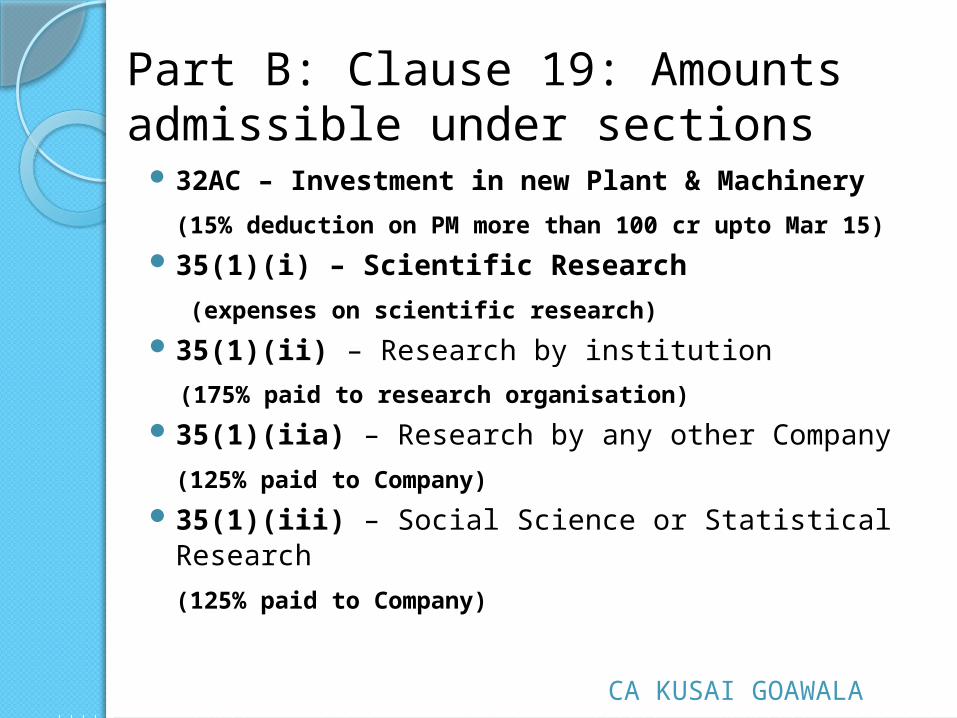

Part B: Clause 19: Amounts admissible under sections

32AC – Investment in new Plant & Machinery

(15% deduction on PM more than 100 cr upto Mar

15)

35(1)(i) – Scientific Research

(expenses on scientific research)

35(1)(ii) – Research by institution

(175% paid to research organisation)

35(1)(iia) – Research by any other Company

(125% paid to Company)

35(1)(iii) – Social Science or Statistical Research

(125% paid to Company)

CA KUSAI GOAWALA

Part B: Clause 19: Amounts admissible under sections

35(1)(iv) – Capital Expenditure on Scientific Research

35AD : Investments in Specified Business

◦ Capital Expenditure

◦ Specified Business

Cold chain facility

Hotel 2 star

Hospital 100 beds

SRA project

35CCC – Expenditure on agricultural extension

35CCD – Expenditure on skill development

◦ (150% of expenditure)

CA KUSAI GOAWALA

Part B Clause 21 Following expenditure to be reported even not debited to P&L

Disallowance for TDS 40a

Cash Payments – 40A(3) and (3A)

Provision for Gratuity 40A(7)

Provision for employees 40A(9)

Particulars of Contingent Liability

Amount inadmissible u/s 14A

Amount inadmissible u/s 36(1)(iii)

Details of Capital Expenditure, Personal

Expenses and Advertisement to be given.CA KUSAI GOAWALA

Part B : Clause 21(b): Amounts inadmissible u/s 40(a)

Non Resident - 40a(i)Section 195DTAASection 206AA

What if tax is not deductible as per DTAA ?

What about Imports of goods

Composite contract – Import of goods with

installation

Separate contract for installation

Not a defaulter u/s 201 – proviso –

considered as payment for 40a.

CA KUSAI GOAWALA

21(d) Disallowance/deemed income under section 40A(3)

Assertion regarding obtaining certificate not required.

However, to be obtained as audit MRL40A(3) Expenditure incurred and paid during

the same year 40A(3A) Expenditure incurred earlier year

but payment made in year under report.

PAN of the payee to be given if available

CA KUSAI GOAWALA

Clause 21(h) Section 14A

Disallowance of expenditure incurred for earning tax

free income

Whether existence of tax free income required during

the year

An investment capable of earning taxable and tax free

income – Shares of private companies – dividend

and/or capital gains CIT vs Delite Industries (Bom)

Procedure for applying 14A by AO - Rule 8D.

If investment exists during the year but no investments

at the beginning or at end of the year.

Can disallowance as per Rule 8D exceed expenditure

incurred.

CA KUSAI GOAWALA

Clause 23 Payments to parties referred u/s 40A2(b)

Ascertain parties referred u/s 40A 2(b)

Payments made = Expenditure Incurred

Also important and relevant for DTP

Very far reaching relationships

Extensive audit work and time for determination

CA KUSAI GOAWALA

Part B : Clause 28: Deem Gift – 56(2)(viia)

Transfer of shares of Closely held CompanyTo firm or closely held company (AOP not

covered)For consideration which is less than as

computed under Rule 11UA.Then the difference will be deemed as taxable

income (gift) in the hands of the transferee company

What about proprietorship concerns of Individuals or HUF (56 -2(vii) not covered)

CA KUSAI GOAWALA

Part B : Clause 29: Deem Income – 56(2)(viib)

Allotment of Shares by a Closely held companiesTo person other than Non Resident If at par the provision is not applicable If at a premium then if the share value is higher

than value as per DCF method or other method as may be prescribed.

Suppose Co A allots Shares to B at Rs.100 (FV Rs.10)

Value as per 11UA = 150Value as per DCF = 80Company will be taxed at Rs.20 (100-80)A will be taxed at Rs.50 (150-100)

CA KUSAI GOAWALA

Part B : Clause 32 (c)

Speculation Loss – 73.Loss in respect of Specified Business u/s 73A

Specified Businesses :Cold Chain FacilityWarehousing for agriculturalLaying and operating cross country natural gasBuilding and operating 2 star hotelBuilding and operating atleast 100 bed hospitalProject under SRA

CA KUSAI GOAWALA

Contd…

Project for affordable housing Production of fertiliser Set up and operating Inland container

depot Beekeeping Warehouse for sugar

CA KUSAI GOAWALA

Deem Speculative Business u/s 73

Explanation to Section 73 Company whose business income is

more than 50%. Income from sale of shares and

securitiesDeemed to be speculative income.To report :Whether company is deemed to be

carrying on speculative businessDetails of speculation lossSuppose the conditions change in

subsequent year – no set off of speculative loss CA KUSAI GOAWALA

Part B: Clause 33: Section-wise details of deductions under Chapter VIA and III

Chapter III Section 10A : Special provision in

respect of newly established undertakings in Free Trade Zone

Section 10AA: Special provision in respect of newly established units in Special Economic Zone

Whether conditions for claiming above deductions is satisfied as per Act, Rules, Guidelines, Circulars etc.

Form 10CCB ?CA KUSAI GOAWALA

Part B : Clause 34 Stringent Reporting requirement

TCS also covered

Total payment – nature of payment wise

Amount on which tax deductible out of above

Tax deducted at specified rates

Tax deducted at less than specified rates

Tax deducted but not paid

If return is not filed within time limit – then report

details of delay.

Further only if delay, statement to be given whether

all items of deduction have been considered in return.

Interest payable on delayed payment of tds and date

of payment CA KUSAI GOAWALA

CA KUSAI GOAWALA

Any Questions ?