Systems Design:Process Costing

2/23/04

Chapter 4

© The McGraw-Hill Companies, Inc., 2003McGraw-Hill/Irwin

Job-orderCosting

ProcessCosting

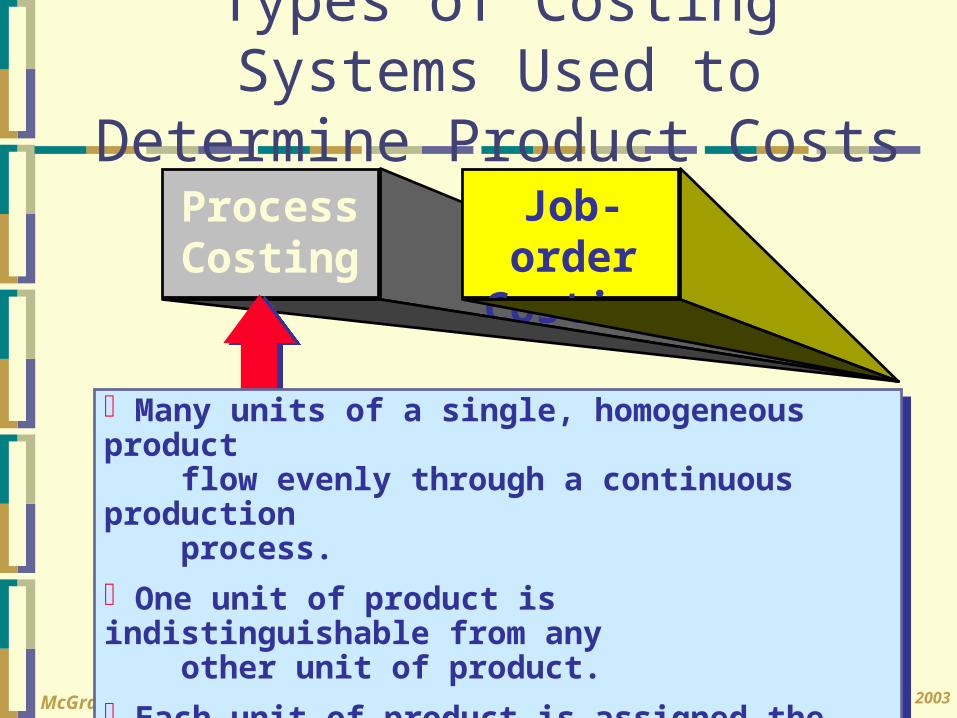

Many units of a single, homogeneous product flow evenly through a continuous production process.

One unit of product is indistinguishable from any other unit of product.

Each unit of product is assigned the same average cost.

Many units of a single, homogeneous product flow evenly through a continuous production process.

One unit of product is indistinguishable from any other unit of product.

Each unit of product is assigned the same average cost.

Types of Costing Systems Used to Determine Product Costs

© The McGraw-Hill Companies, Inc., 2003McGraw-Hill/Irwin

Types of Costing Systems Used to Determine Product Costs

Job-orderCosting

ProcessCosting

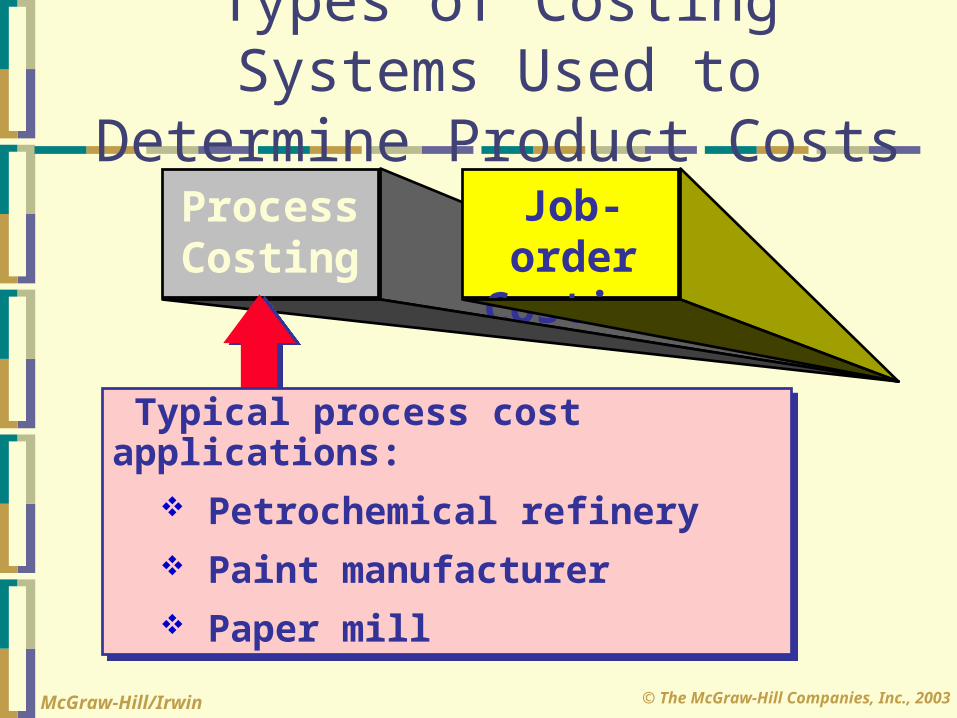

Typical process cost applications: Petrochemical refinery Paint manufacturer Paper mill

Typical process cost applications: Petrochemical refinery Paint manufacturer Paper mill

© The McGraw-Hill Companies, Inc., 2003McGraw-Hill/Irwin

Job order costing Many products are

produced during the period.

Costs are accumulated by individual jobs.

Job cost sheet is the key document.

Unit cost computed by job.

Job order costing Many products are

produced during the period.

Costs are accumulated by individual jobs.

Job cost sheet is the key document.

Unit cost computed by job.

Process costing A single product is

produced for a long period of time.

Costs are accumulated by departments.

Department production report is key document.

Unit costs are computed by department.

Process costing A single product is

produced for a long period of time.

Costs are accumulated by departments.

Department production report is key document.

Unit costs are computed by department.

Differences Between Job-Order and Process Costing

© The McGraw-Hill Companies, Inc., 2003McGraw-Hill/Irwin

Process Costing

Type of Product Cost

Do

llar

Am

ou

nt Conversion

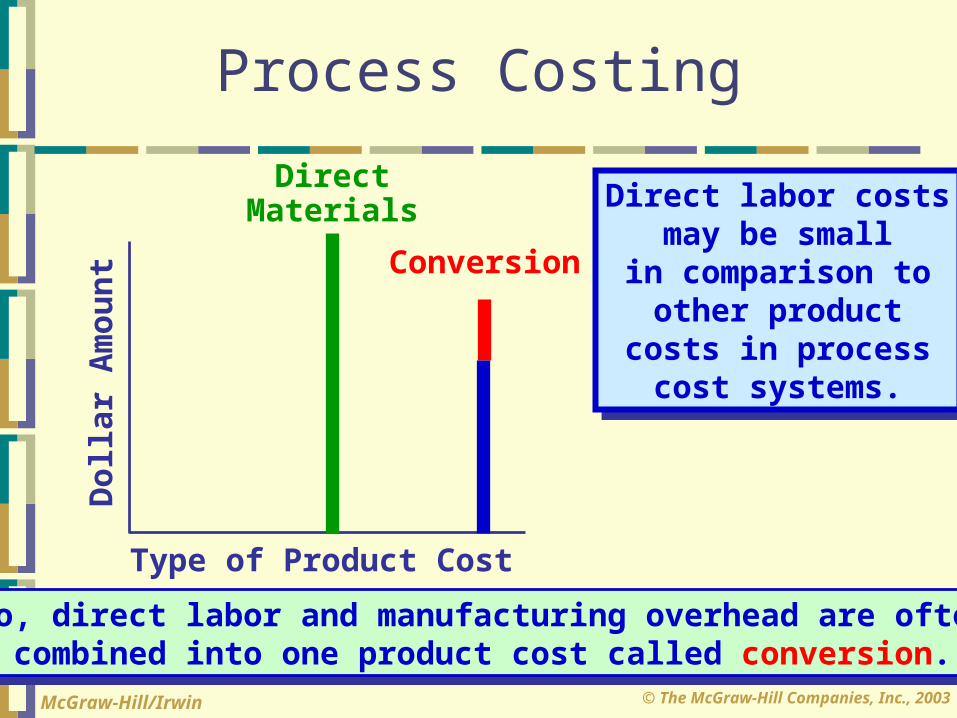

So, direct labor and manufacturing overhead are oftencombined into one product cost called conversion.

So, direct labor and manufacturing overhead are oftencombined into one product cost called conversion.

Direct labor costsmay be small

in comparison toother product

costs in processcost systems.

Direct labor costsmay be small

in comparison toother product

costs in processcost systems.

DirectMaterials

© The McGraw-Hill Companies, Inc., 2003McGraw-Hill/Irwin

Comparing Job-Orderand Process Costing

FinishedGoods

FinishedGoods

Cost of GoodsSold

Cost of GoodsSold

Direct LaborDirect Labor

ManufacturingOverhead

ManufacturingOverhead

JobsJobs

Costs are traced andapplied to individualjobs in a job-order

cost system.

Costs are traced andapplied to individualjobs in a job-order

cost system.Direct

Materials

Direct Materials

© The McGraw-Hill Companies, Inc., 2003McGraw-Hill/Irwin

Comparing Job-Orderand Process Costing

FinishedGoods

FinishedGoods

Cost of GoodsSold

Cost of GoodsSold

Direct LaborDirect Labor

ManufacturingOverhead

ManufacturingOverhead

ProcessingDepartmentsProcessing

Departments

Costs are traced and applied to departments

in a process cost system.

Costs are traced and applied to departments

in a process cost system.

Direct Materials

Direct Materials

© The McGraw-Hill Companies, Inc., 2003McGraw-Hill/Irwin

Process Cost Systems

Exh. 4-2 Sequential Processing, p.152

Exh. 4-3 Parallel Processing, p. 153

Exh. 4-4 T-Account Model, p. 154

Exh. 4-5 Double Diamond, p. 156

© The McGraw-Hill Companies, Inc., 2003McGraw-Hill/Irwin

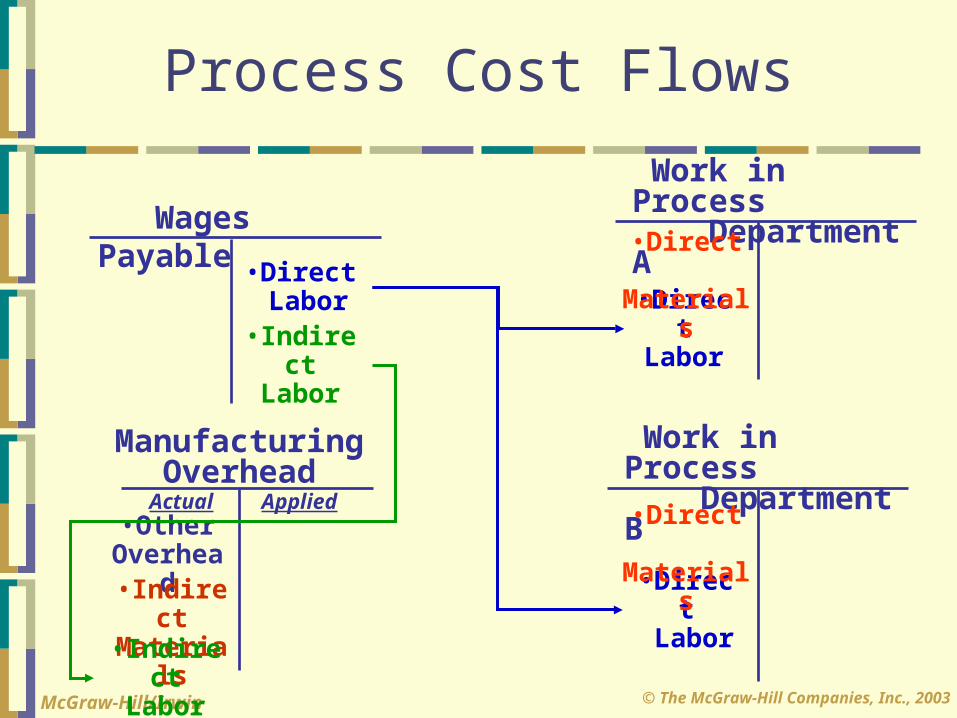

Process Cost Flows

Let’s look at cost flows in a process cost system with

Departments A and B.We will use

T-accounts andstart with materials.

© The McGraw-Hill Companies, Inc., 2003McGraw-Hill/Irwin

Raw Materials•Purchases •Direct

Materials

Process Cost Flows

•Indirect Materials

•Direct Materials

Work in Process Department B

Work in Process Department A

•OtherOverhead

Manufacturing Overhead

Actual Applied

•IndirectMaterials

•Direct Materials

© The McGraw-Hill Companies, Inc., 2003McGraw-Hill/Irwin

Process Cost Flows

Work in Process Department B

•Direct Labor

Work in Process Department A

•OtherOverhead

Manufacturing Overhead

Actual Applied

•IndirectMaterials•Indirect

Labor

Wages Payable

•Direct Labor

•IndirectLabor

•Direct Materials

•Direct Labor

•Direct Materials

© The McGraw-Hill Companies, Inc., 2003McGraw-Hill/Irwin

Process Cost Flows(MOH is applied using Departmental rates)

Work in Process Department B

Work in Process Department A

•OverheadApplied to

Work inProcess

•POHR

•AppliedOverhead

•AppliedOverhead

•OtherOverhead

Manufacturing Overhead

Actual Applied

•IndirectMaterials•Indirect

Labor

•Direct Labor

•Direct Materials

•Direct Labor

•Direct Materials

© The McGraw-Hill Companies, Inc., 2003McGraw-Hill/Irwin

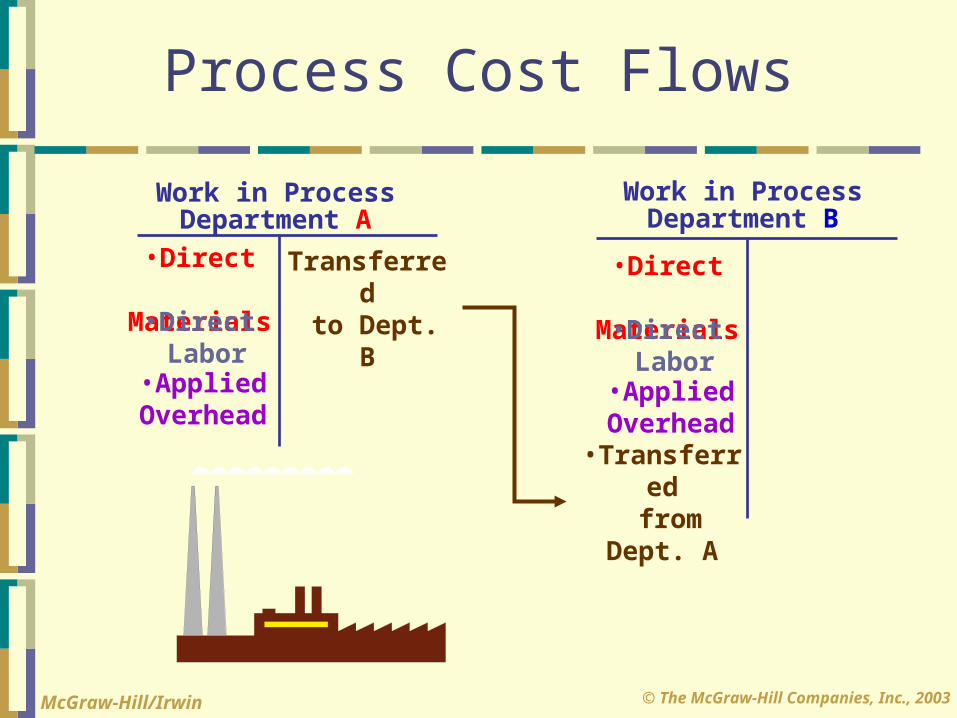

Process Cost Flows

Next, transfer workfrom Department Ato Department B.

© The McGraw-Hill Companies, Inc., 2003McGraw-Hill/Irwin

Process Cost Flows

Work in Process Department B

Work in ProcessDepartment A

•Direct Materials

•Direct Labor

•AppliedOverhead

•Direct Materials

•Direct Labor

•AppliedOverhead

Transferred to Dept. B

•Transferred from Dept. A

© The McGraw-Hill Companies, Inc., 2003McGraw-Hill/Irwin

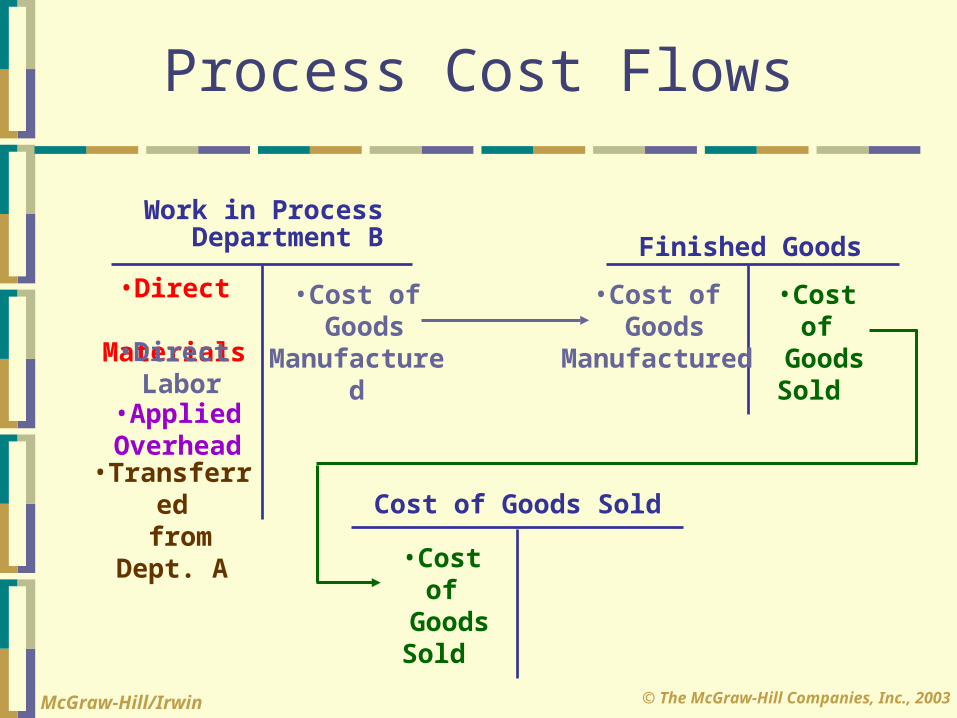

Process Cost Flows

Now let’s completethe goods in

Department Band sell them.

© The McGraw-Hill Companies, Inc., 2003McGraw-Hill/Irwin

Finished Goods

Cost of Goods Sold

Process Cost Flows

Work in Process Department B

•Cost of Goods

Manufactured

•Direct Materials

•Direct Labor

•AppliedOverhead

•Transferred from Dept. A

•Cost of GoodsSold

•Cost of GoodsSold

•Cost of Goods

Manufactured

© The McGraw-Hill Companies, Inc., 2003McGraw-Hill/Irwin

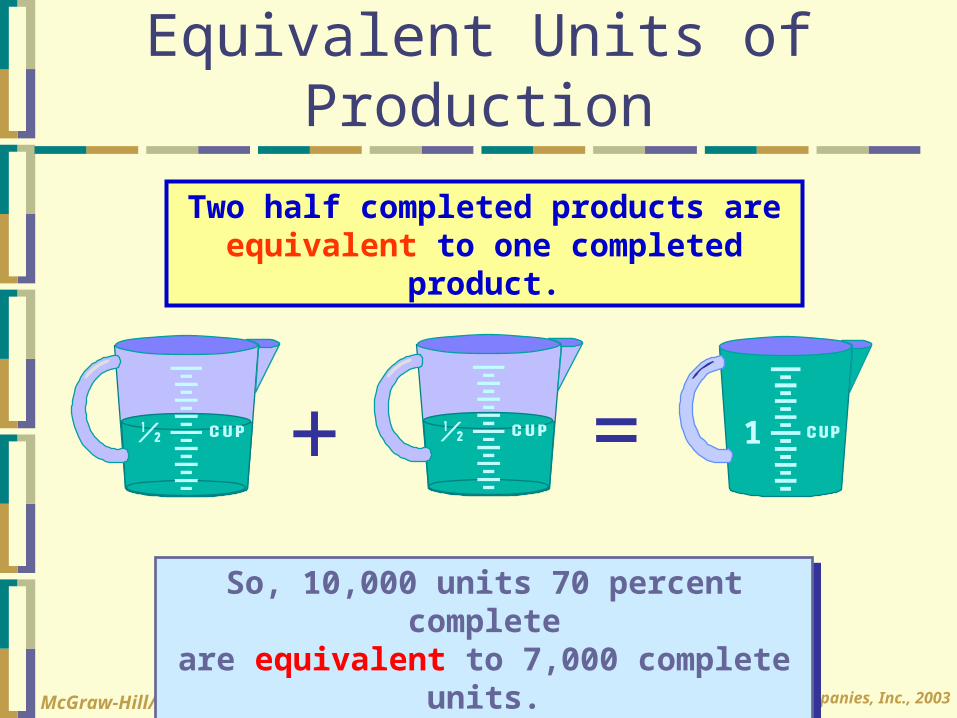

Equivalent Units of Production(Accounting for partially completed units in WIP)

Equivalent units are partially complete and are part of work in process inventory. Partially completed

products are expressed in terms of a smaller number of fully completed

units.

© The McGraw-Hill Companies, Inc., 2003McGraw-Hill/Irwin

Equivalent Units of Production

Two half completed products are equivalent to one completed product.

So, 10,000 units 70 percent completeare equivalent to 7,000 complete units.

So, 10,000 units 70 percent completeare equivalent to 7,000 complete units.

+ = 1

© The McGraw-Hill Companies, Inc., 2003McGraw-Hill/Irwin

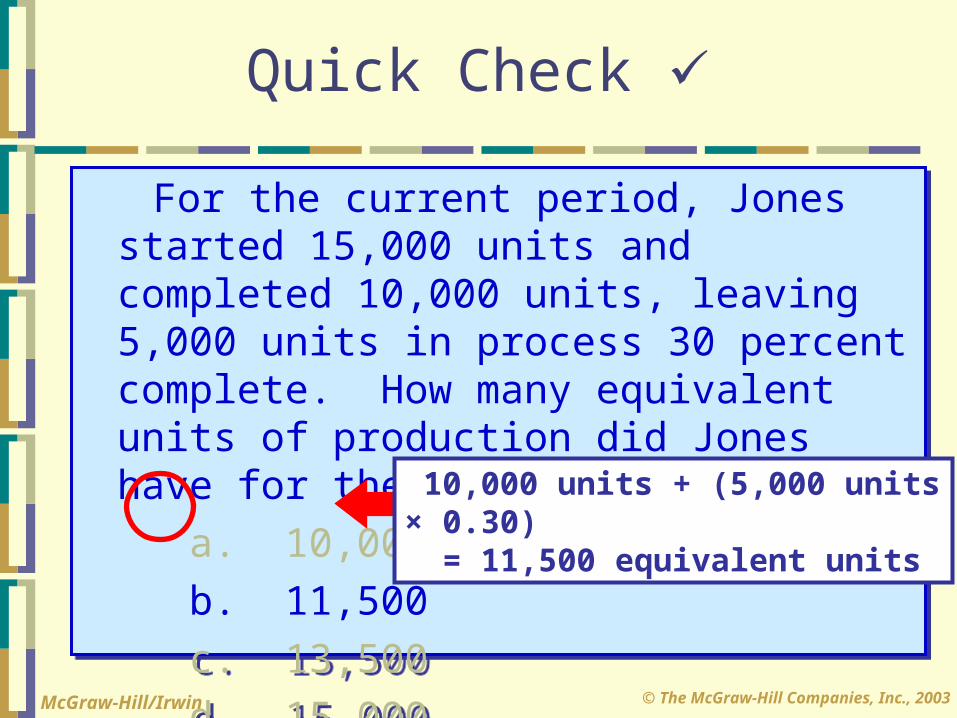

For the current period, Jones started 15,000 units and completed 10,000 units, leaving 5,000 units in process 30 percent complete. How many equivalent units of production did Jones have for the period?

a. 10,000

b. 11,500

c. 13,500

d. 15,000

For the current period, Jones started 15,000 units and completed 10,000 units, leaving 5,000 units in process 30 percent complete. How many equivalent units of production did Jones have for the period?

a. 10,000

b. 11,500

c. 13,500

d. 15,000

Quick Check

© The McGraw-Hill Companies, Inc., 2003McGraw-Hill/Irwin

For the current period, Jones started 15,000 units and completed 10,000 units, leaving 5,000 units in process 30 percent complete. How many equivalent units of production did Jones have for the period?

a. 10,000

b. 11,500

c. 13,500

d. 15,000

For the current period, Jones started 15,000 units and completed 10,000 units, leaving 5,000 units in process 30 percent complete. How many equivalent units of production did Jones have for the period?

a. 10,000

b. 11,500

c. 13,500

d. 15,000

10,000 units + (5,000 units × 0.30) = 11,500 equivalent units

Quick Check

© The McGraw-Hill Companies, Inc., 2003McGraw-Hill/Irwin

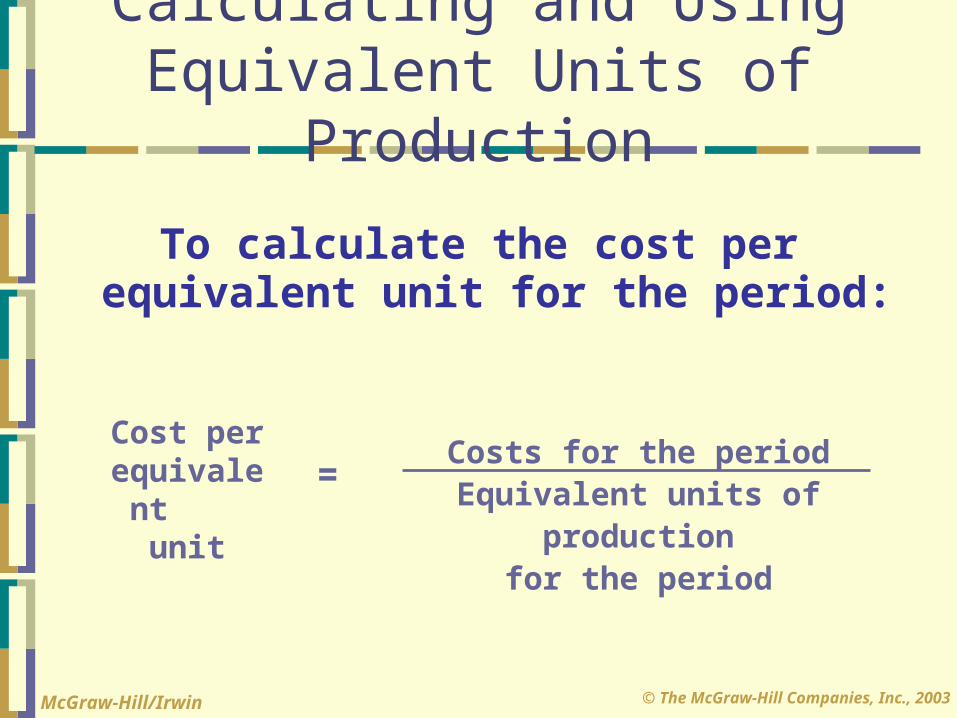

Calculating and Using Equivalent Units of Production

To calculate the cost perequivalent unit for the period:

Cost perequivalent

unit

=Costs for the period

Equivalent units of productionfor the period

© The McGraw-Hill Companies, Inc., 2003McGraw-Hill/Irwin

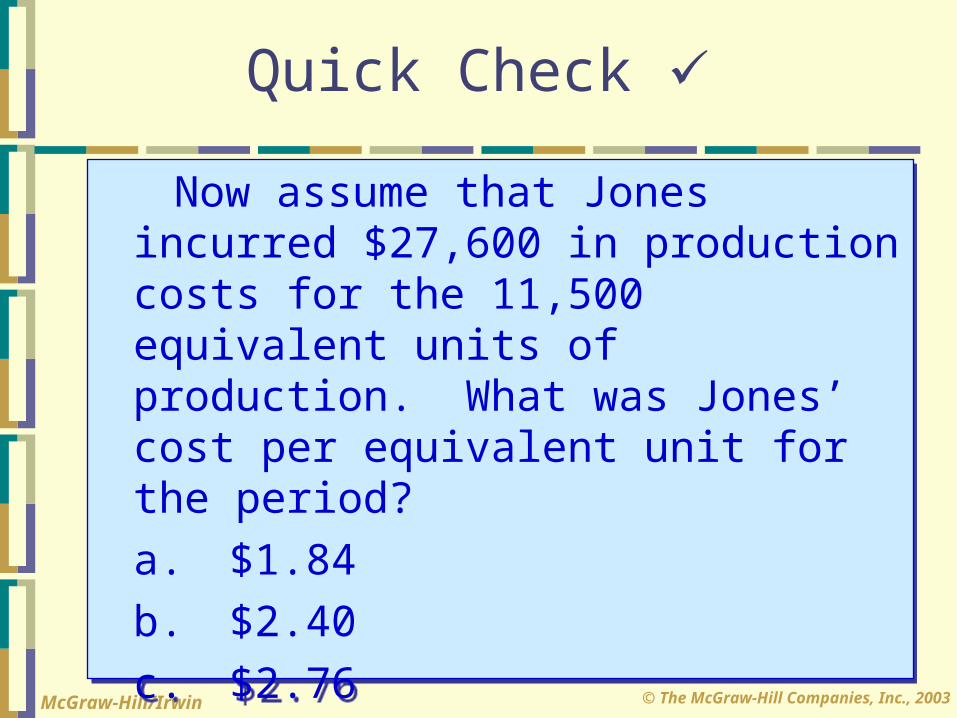

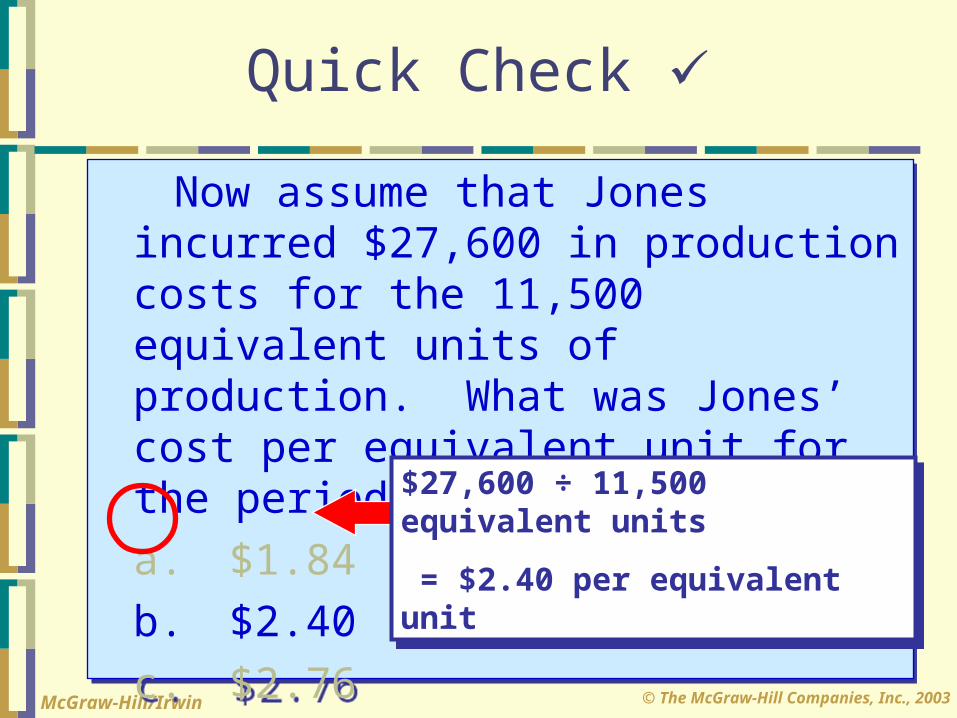

Now assume that Jones incurred $27,600 in production costs for the 11,500 equivalent units of production. What was Jones’ cost per equivalent unit for the period?

a. $1.84

b. $2.40

c. $2.76

d. $2.90

Now assume that Jones incurred $27,600 in production costs for the 11,500 equivalent units of production. What was Jones’ cost per equivalent unit for the period?

a. $1.84

b. $2.40

c. $2.76

d. $2.90

Quick Check

© The McGraw-Hill Companies, Inc., 2003McGraw-Hill/Irwin

Now assume that Jones incurred $27,600 in production costs for the 11,500 equivalent units of production. What was Jones’ cost per equivalent unit for the period?

a. $1.84

b. $2.40

c. $2.76

d. $2.90

Now assume that Jones incurred $27,600 in production costs for the 11,500 equivalent units of production. What was Jones’ cost per equivalent unit for the period?

a. $1.84

b. $2.40

c. $2.76

d. $2.90

$27,600 ÷ 11,500 equivalent units

= $2.40 per equivalent unit

$27,600 ÷ 11,500 equivalent units

= $2.40 per equivalent unit

Quick Check

© The McGraw-Hill Companies, Inc., 2003McGraw-Hill/Irwin

Equivalent Units of Production –Weighted Average Method

The weighted average method . . .Makes no distinction between work done in prior

and current period.Blends together units and costs from prior

period and current period.

Let’s see how this works!

Weighted Average Method

Equivalent units of production = Units completed and transferred

to the next department + equivalent units in ending WIP

© The McGraw-Hill Companies, Inc., 2003McGraw-Hill/Irwin

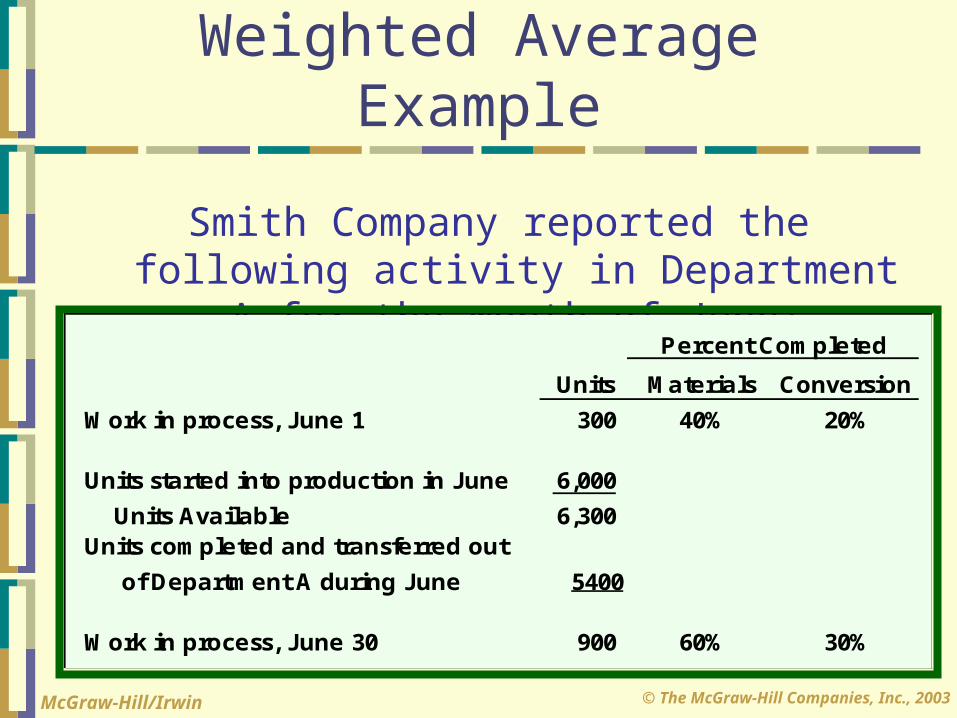

Weighted Average Example

Smith Company reported the following activity in Department A for the month of June:

Percent Completed

Units Materials Conversion

Work in process, June 1 300 40% 20%

Units started into production in June 6,000

Units Available 6,300 Units completed and transferred out

of Department A during June 5400

Work in process, June 30 900 60% 30%

© The McGraw-Hill Companies, Inc., 2003McGraw-Hill/Irwin

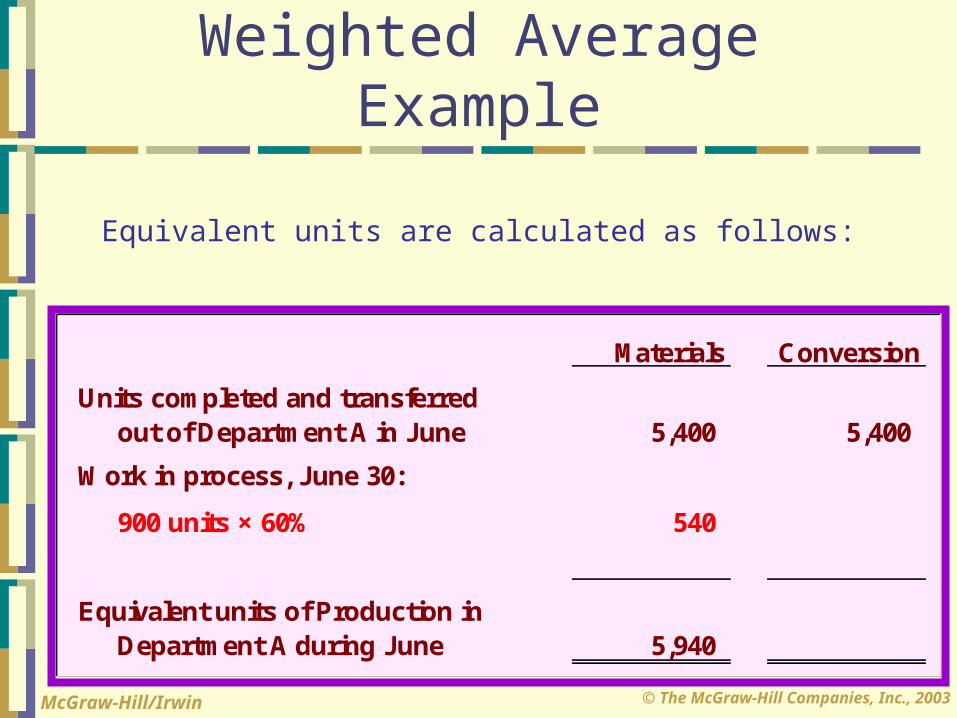

Equivalent units are calculated as follows:

Weighted Average Example

Materials Conversion

Units completed and transferred out of Department A in June 5,400 5,400

© The McGraw-Hill Companies, Inc., 2003McGraw-Hill/Irwin

Equivalent units are calculated as follows:

Weighted Average Example

Materials Conversion

Units completed and transferred out of Department A in June 5,400 5,400

Work in process, June 30:

900 units × 60% 540

Equivalent units of Production in Department A during June 5,940

© The McGraw-Hill Companies, Inc., 2003McGraw-Hill/Irwin

Equivalent units are calculated as follows:

Weighted Average Example

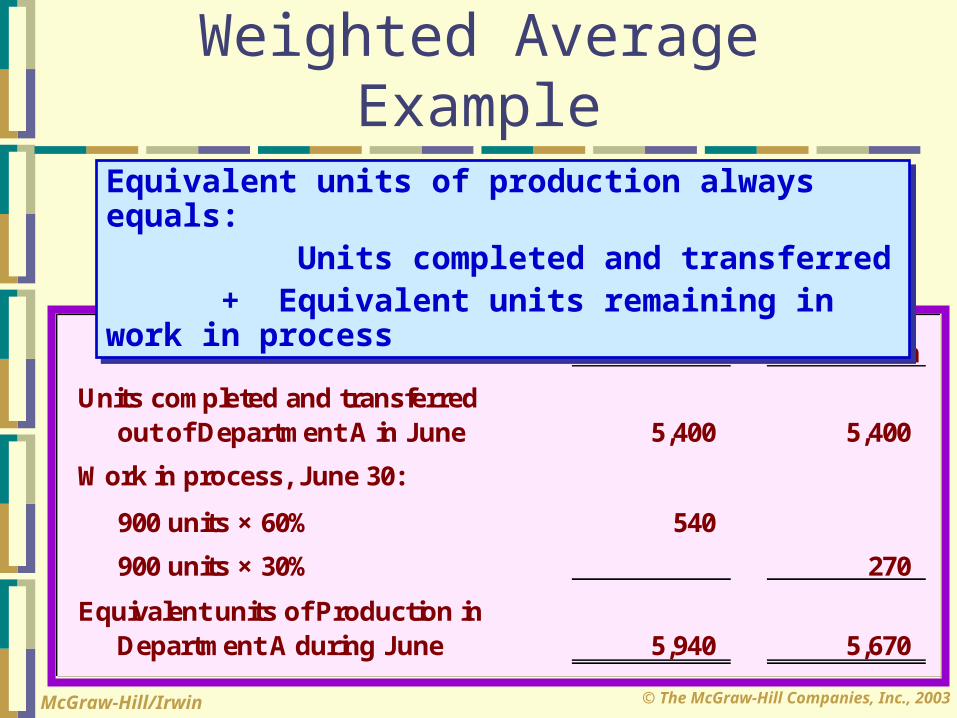

Materials Conversion

Units completed and transferred out of Department A in June 5,400 5,400

Work in process, June 30:

900 units × 60% 540

900 units × 30% 270

Equivalent units of Production in Department A during June 5,940 5,670

© The McGraw-Hill Companies, Inc., 2003McGraw-Hill/Irwin

Materials Conversion

Units completed and transferred out of Department A in June 5,400 5,400

Work in process, June 30:

900 units × 60% 540

900 units × 30% 270

Equivalent units of Production in Department A during June 5,940 5,670

Equivalent units of production always equals: Units completed and transferred + Equivalent units remaining in work in process

Equivalent units of production always equals: Units completed and transferred + Equivalent units remaining in work in process

Weighted Average Example

© The McGraw-Hill Companies, Inc., 2003McGraw-Hill/Irwin

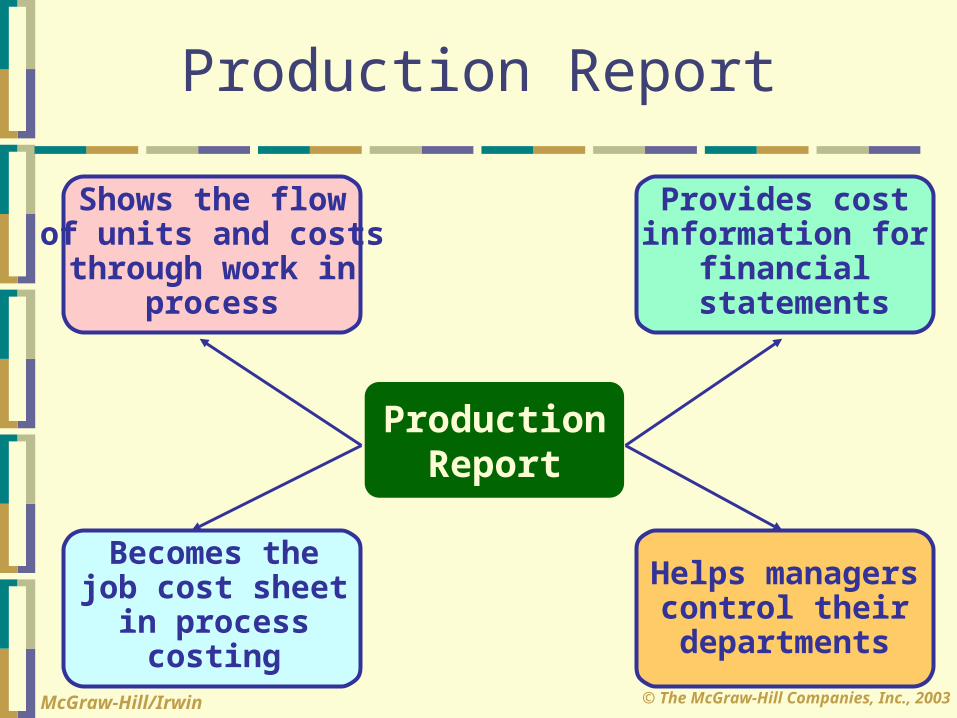

Production Report

ProductionReport

Helps managerscontrol theirdepartments

Provides costinformation for

financial statements

Shows the flowof units and coststhrough work in

process

Becomes thejob cost sheet

in processcosting

© The McGraw-Hill Companies, Inc., 2003McGraw-Hill/Irwin

Production Report

A computation ofcost per equivalent unit.

A computation ofcost per equivalent unit.

Section 1

Section 2

Section 3

Production Report A quantity schedule showing the flow of units and the computation of

equivalent units.

A quantity schedule showing the flow of units and the computation of

equivalent units.

© The McGraw-Hill Companies, Inc., 2003McGraw-Hill/Irwin

Production Report

A reconciliation of cost flows for the period, including:

Total cost for units completed and transferred from the processing department.

Total cost for partially completed units remaining in work in process.

A reconciliation of cost flows for the period, including:

Total cost for units completed and transferred from the processing department.

Total cost for partially completed units remaining in work in process.

Section 1

Section 2

Section 3

Production Report

© The McGraw-Hill Companies, Inc., 2003McGraw-Hill/Irwin

Double Diamond Skis uses process costing to determine unit costs in its Shaping and Milling Department.

Double Diamond uses the weighted average cost procedure.

Using the following information for the month of May, let’s prepare a production report for Shaping and Milling.

Double Diamond Skis uses process costing to determine unit costs in its Shaping and Milling Department.

Double Diamond uses the weighted average cost procedure.

Using the following information for the month of May, let’s prepare a production report for Shaping and Milling.

Production Report ExamplePage 160

© The McGraw-Hill Companies, Inc., 2003McGraw-Hill/Irwin

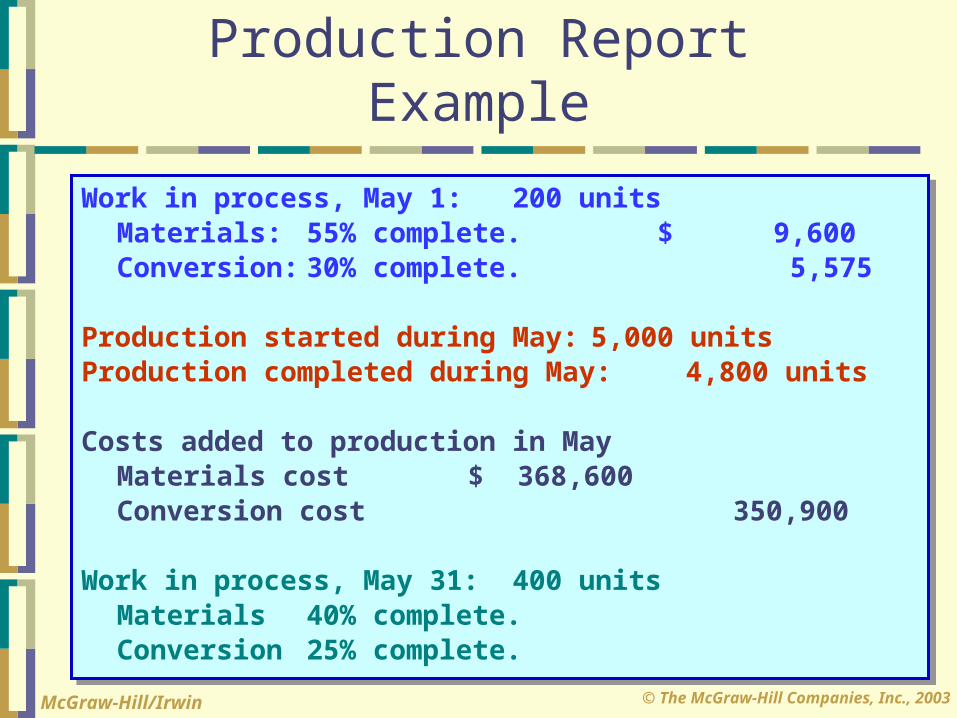

Work in process, May 1: 200 units Materials: 55% complete. $ 9,600Conversion: 30% complete. 5,575

Production started during May: 5,000 unitsProduction completed during May: 4,800 units

Costs added to production in MayMaterials cost $ 368,600Conversion cost 350,900

Work in process, May 31: 400 unitsMaterials 40% complete.Conversion 25% complete.

Work in process, May 1: 200 units Materials: 55% complete. $ 9,600Conversion: 30% complete. 5,575

Production started during May: 5,000 unitsProduction completed during May: 4,800 units

Costs added to production in MayMaterials cost $ 368,600Conversion cost 350,900

Work in process, May 31: 400 unitsMaterials 40% complete.Conversion 25% complete.

Production Report Example

© The McGraw-Hill Companies, Inc., 2003McGraw-Hill/Irwin

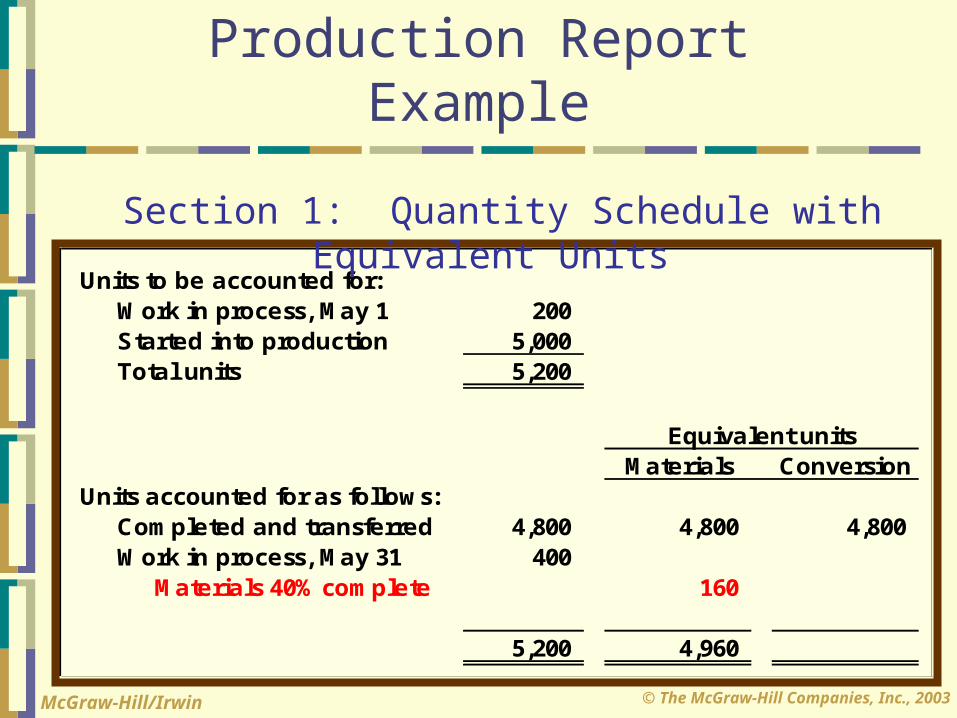

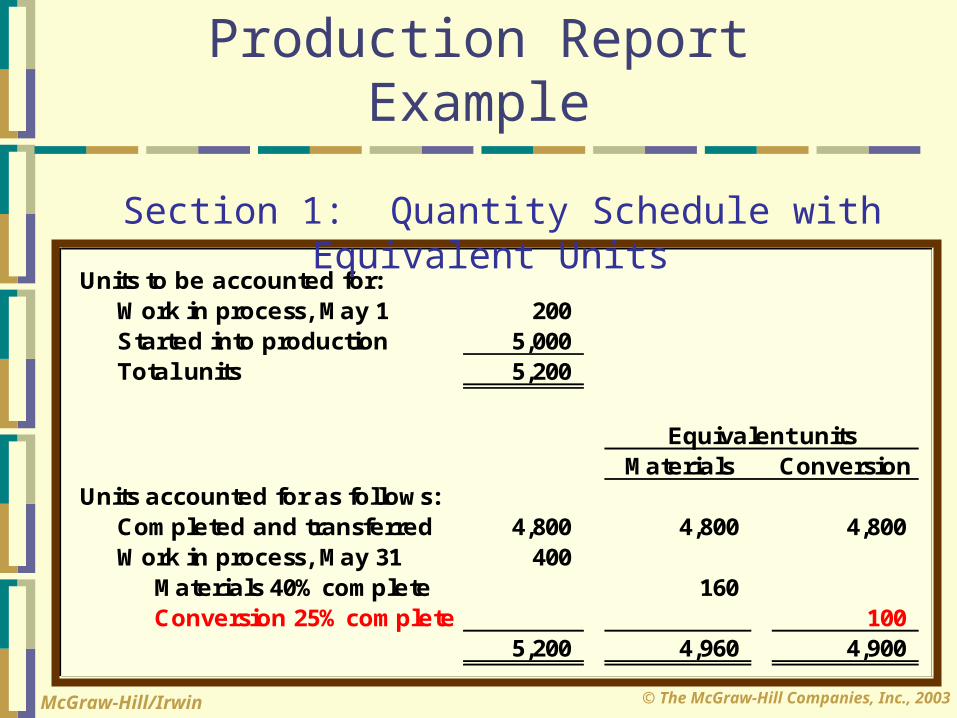

Section 1: Quantity Schedule with Equivalent Units

Production Report Example

Units to be accounted for: Work in process, May 1 200 Started into production 5,000 Total units 5,200

Equivalent unitsMaterials Conversion

Units accounted for as follows: Completed and transferred 4,800 4,800 4,800 Work in process, May 31 400

© The McGraw-Hill Companies, Inc., 2003McGraw-Hill/Irwin

Production Report Example

Units to be accounted for: Work in process, May 1 200 Started into production 5,000 Total units 5,200

Equivalent unitsMaterials Conversion

Units accounted for as follows: Completed and transferred 4,800 4,800 4,800 Work in process, May 31 400 Materials 40% complete 160

5,200 4,960

Section 1: Quantity Schedule with Equivalent Units

© The McGraw-Hill Companies, Inc., 2003McGraw-Hill/Irwin

Production Report Example

Units to be accounted for: Work in process, May 1 200 Started into production 5,000 Total units 5,200

Equivalent unitsMaterials Conversion

Units accounted for as follows: Completed and transferred 4,800 4,800 4,800 Work in process, May 31 400 Materials 40% complete 160 Conversion 25% complete 100

5,200 4,960 4,900

Section 1: Quantity Schedule with Equivalent Units

© The McGraw-Hill Companies, Inc., 2003McGraw-Hill/Irwin

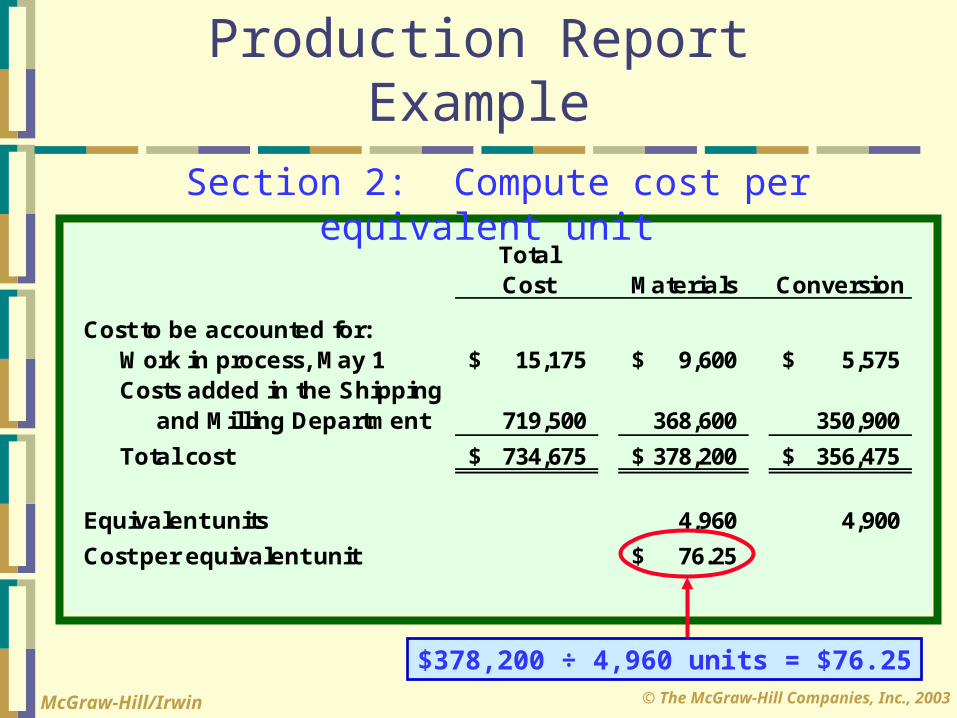

Section 2: Compute cost per equivalent unit

Production Report Example

TotalCost Materials Conversion

Cost to be accounted for: Work in process, May 1 15,175$ 9,600$ 5,575$ Costs added in the Shipping and Milling Department 719,500 368,600 350,900

Total cost 734,675$ 378,200$ 356,475$

Equivalent units 4,960 4,900

Cost per equivalent unit

© The McGraw-Hill Companies, Inc., 2003McGraw-Hill/Irwin

TotalCost Materials Conversion

Cost to be accounted for: Work in process, May 1 15,175$ 9,600$ 5,575$ Costs added in the Shipping and Milling Department 719,500 368,600 350,900

Total cost 734,675$ 378,200$ 356,475$

Equivalent units 4,960 4,900

Cost per equivalent unit 76.25$

Production Report Example

Section 2: Compute cost per equivalent unit

$378,200 ÷ 4,960 units = $76.25

© The McGraw-Hill Companies, Inc., 2003McGraw-Hill/Irwin

TotalCost Materials Conversion

Cost to be accounted for: Work in process, May 1 15,175$ 9,600$ 5,575$ Costs added in the Shipping and Milling Department 719,500 368,600 350,900

Total cost 734,675$ 378,200$ 356,475$

Equivalent units 4,960 4,900

Cost per equivalent unit 76.25$ 72.75$ Total cost per equivalent unit = $76.25 + $72.75 = $149.00

Production Report Example

$356,475 ÷ 4,900 units = $72.75

Section 2: Compute cost per equivalent unit

© The McGraw-Hill Companies, Inc., 2003McGraw-Hill/Irwin

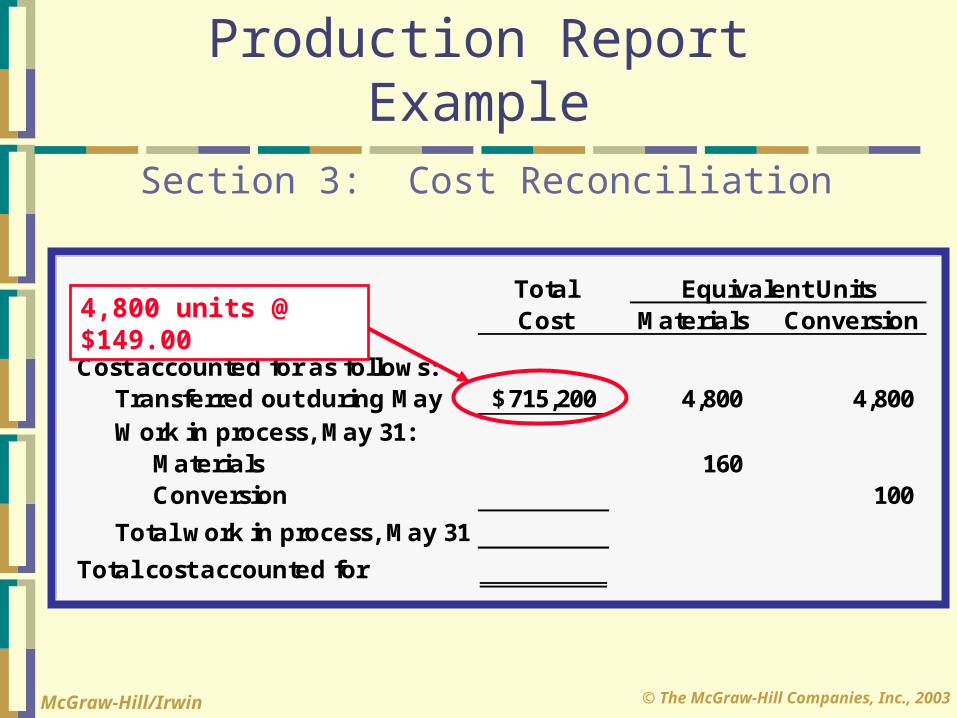

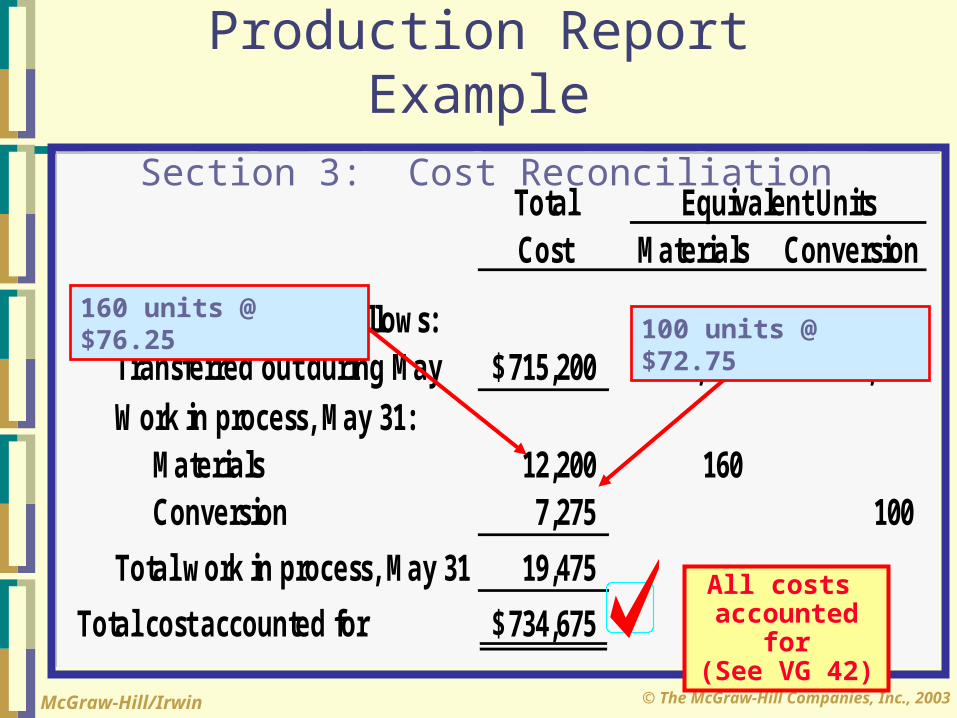

Section 3: Cost Reconciliation

Production Report Example

Total Equivalent UnitsCost Materials Conversion

Cost accounted for as follows: Transferred out during May 4,800 4,800 Work in process, May 31: Materials 160 Conversion 100

Total work in process, May 31

Total cost accounted for

© The McGraw-Hill Companies, Inc., 2003McGraw-Hill/Irwin

Total Equivalent UnitsCost Materials Conversion

Cost accounted for as follows: Transferred out during May 715,200$ 4,800 4,800 Work in process, May 31: Materials 160 Conversion 100

Total work in process, May 31

Total cost accounted for

4,800 units @ $149.00

Production Report Example

Section 3: Cost Reconciliation

© The McGraw-Hill Companies, Inc., 2003McGraw-Hill/Irwin

Total Equivalent UnitsCost Materials Conversion

Cost accounted for as follows: Transferred out during May 715,200$ 4,800 4,800 Work in process, May 31: Materials 12,200 160 Conversion 7,275 100

Total work in process, May 31 19,475

Total cost accounted for 734,675$

160 units @ $76.25

Production Report Example

Section 3: Cost Reconciliation

All costs accounted for(See VG 42)

100 units @ $72.75

© The McGraw-Hill Companies, Inc., 2003McGraw-Hill/Irwin

I’m going to end this chapter and process some leisure time, unless

you want to see some journal entries. Noooo!

Do You Want to SeeJournal Entries?

© The McGraw-Hill Companies, Inc., 2003McGraw-Hill/Irwin

End of Chapter 4