Survey of Businesses’ Inflation Expectations

FEBRUARY 2015

RESEARCH SERVICES DEPARTMENT RESEARCH AND ECONOMIC PROGRAMMING DIVISION

Inflation Expectations Survey

Prepared by the Research Services Department Page 1 February 2015 Survey

The Statistical Institute of Jamaica (STATIN) undertakes surveys of businesses on behalf of the

Bank of Jamaica to ascertain the expectations of these economic agents about variables which are

likely to have an impact on inflation in the near-term. In this regard, the survey captures the

perception of Chief Executive Officers, Managing Directors and Financial Controllers about the

future movement of prices, current and future business conditions and the expected rate of increase

in wages/salaries. These responses assist the Central Bank in charting future policy decisions. The most recent

survey was conducted in February 2015 and had 302 respondents. Below are highlights from that survey.

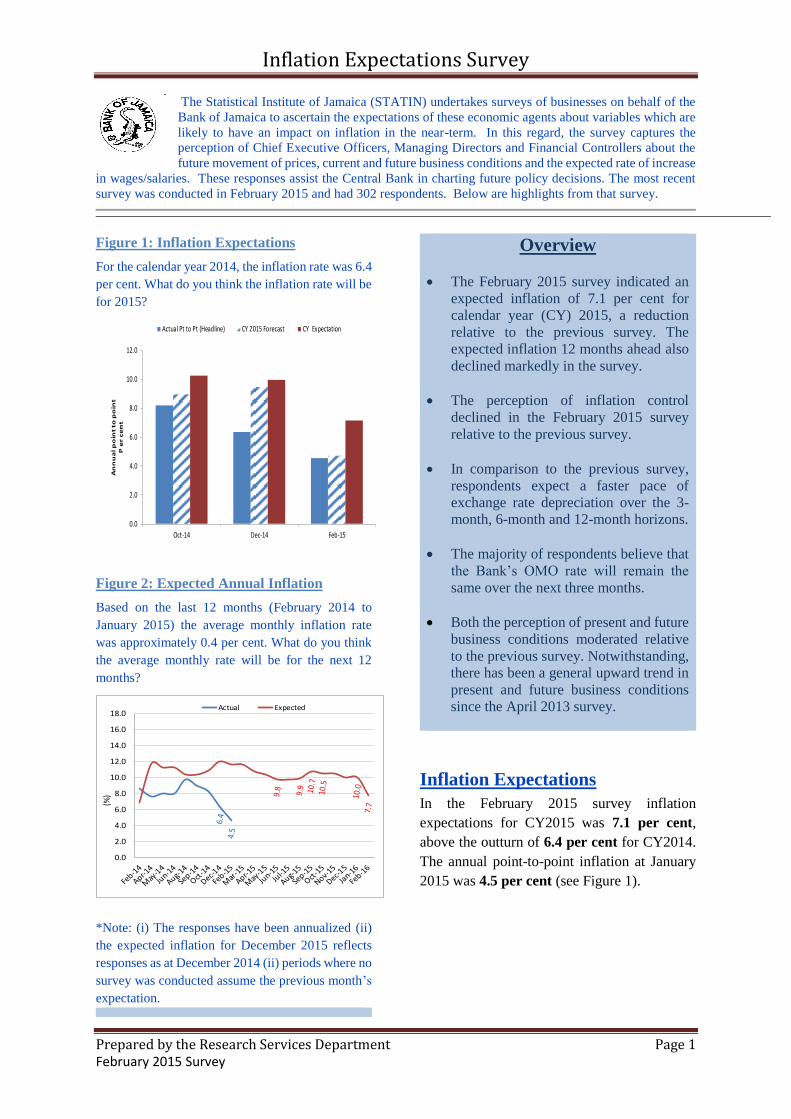

Figure 1: Inflation Expectations

For the calendar year 2014, the inflation rate was 6.4

per cent. What do you think the inflation rate will be

for 2015?

0.0

2.0

4.0

6.0

8.0

10.0

12.0

Oct-14 Dec-14 Feb-15

An

nu

al p

oin

t to

po

int

P e

r ce

nt

Actual Pt to Pt (Headline) CY 2015 Forecast CY Expectation

Figure 2: Expected Annual Inflation

Based on the last 12 months (February 2014 to

January 2015) the average monthly inflation rate

was approximately 0.4 per cent. What do you think

the average monthly rate will be for the next 12

months?

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

(%)

Actual Expected

*Note: (i) The responses have been annualized (ii)

the expected inflation for December 2015 reflects

responses as at December 2014 (ii) periods where no

survey was conducted assume the previous month’s

expectation.

Overview

The February 2015 survey indicated an

expected inflation of 7.1 per cent for

calendar year (CY) 2015, a reduction

relative to the previous survey. The

expected inflation 12 months ahead also

declined markedly in the survey.

The perception of inflation control

declined in the February 2015 survey

relative to the previous survey.

In comparison to the previous survey,

respondents expect a faster pace of

exchange rate depreciation over the 3-

month, 6-month and 12-month horizons.

The majority of respondents believe that

the Bank’s OMO rate will remain the

same over the next three months.

Both the perception of present and future

business conditions moderated relative

to the previous survey. Notwithstanding,

there has been a general upward trend in

present and future business conditions

since the April 2013 survey.

Inflation Expectations

In the February 2015 survey inflation

expectations for CY2015 was 7.1 per cent,

above the outturn of 6.4 per cent for CY2014.

The annual point-to-point inflation at January

2015 was 4.5 per cent (see Figure 1).

Inflation Expectations Survey

Prepared by the Research Services Department Page 2 February 2015 Survey

Figure 3: Perception of Inflation Control

How satisfied are you with the way inflation is being

controlled by the Government?1 10

.0

8.4

24.8

5.5 9.3

10.0

7.3 15

.0

4.3 14

.5

8.0 10

.7

9.8 15

.4 18.2

17.4 21

.8 25.3

20.9

34.2

28.2

35.9

20.6 24

.7 28.2

29.8 27

.2

22.3

28.4

23.6 20

.9

26.4 26

.5

23.3 32

.2 28.9 30

.6

26.1

36.5

38.3

27.6

36.1

37.3 33

.0

38.1

35.0

38.3

31.4

40.0 44

.0

39.0

36.4

37.0

37.4

32.9 30

.2

29.4

18.4

23.8

10.0

36.8 28

.3

27.8 23

.8

22.8

34.3 25

.7

27.6 23

.5

24.8 21

.3

21.2 12

.6

15.1

12.5

20.3

0

50

100

150

200

250

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

% R

espo

nse

Very Satisfied Satisfied Neither Dissatisfied Very Dissatisfied

.

*December 2005 = 100

Table 1: Exchange Rate Expectations

In January 2015 the exchange rate was

J$115.81=US$1.00. What do you think the rate will

be for the following time periods ahead, 3 months, 6

months and 12 months?

OVERALL SURVEY

Periods Ahead

Expected Depreciation

Sep-14 Oct-14 Dec-14 Feb-15

3 Months 1.3 1.0 1.4 1.7

6 Months 2.2 1.4 2.1 3.0

12 Months 3.2 2.3 3.0 3.8

Figure 4: 180-day T-bill

In January 2015 the 180-day T-bill rate was 7.0 per

cent. What do you think the rate will be for the next

3 months?

7.77.1 7.2

8.4

7.4 7.3

8.3

7.3 7.3

0

1

2

3

4

5

6

7

8

9

10

Oct 2014 Dec 2014 Feb 2015

% R

espo

nse

( A

ctu

al

& E

xp I

ntr

ate

)

Actual Intrate (6mth T-bill) Exp(All) Exp Intrate(Fin)

1 Index of inflation control calculated as the number of satisfied

respondents minus the number of dissatisfied respondents plus 100

Respondents’ expectation of inflation 12

months ahead also declined to 7.7 per cent in

the February 2015 survey from 10.0 per cent in

the December 2014 survey (see Figure 2).

Businesses’ perception of inflation control by

the authorities declined in the February 2015

survey when compared to the previous survey.

Specifically, the index of inflation control fell

to 193.5 from 218.2 in the December 2014

survey (see Figure 3). This outturn mainly

reflected an increase in the number of

respondents who were ‘very dissatisfied’ with

the authorities’ control of inflation.

Additionally, there was a decline in the number

of respondents who were ‘satisfied’.

Exchange Rate Expectations

Relative to the survey in December 2014,

respondents expected a faster pace of

depreciation in the domestic currency for the 3-

month, 6-month and 12-month period beyond

the survey date. Specifically, in the February

2015 survey, the exchange rate was expected to

depreciate by 1.7 per cent, 3.0 per cent and 3.8

per cent for the 3-month, 6-month and 12-

month horizons, respectively (see Table 1). The

survey in December 2014 had indicated

expected depreciation of 1.4 per cent, 2.1 per

cent and 3.0 per cent over the respective

horizons.

Interest Rate Expectations: 180-

day T-bill

The expected 180-day Treasury bill rate, three

months hence, declined to 7.3 per cent from 7.4

per cent in the previous survey. This expected

rate was marginally above the actual outturn of

7.2 per cent for February 2015 (see Figure 4).

Inflation Expectations Survey

Prepared by the Research Services Department Page 3 February 2015 Survey

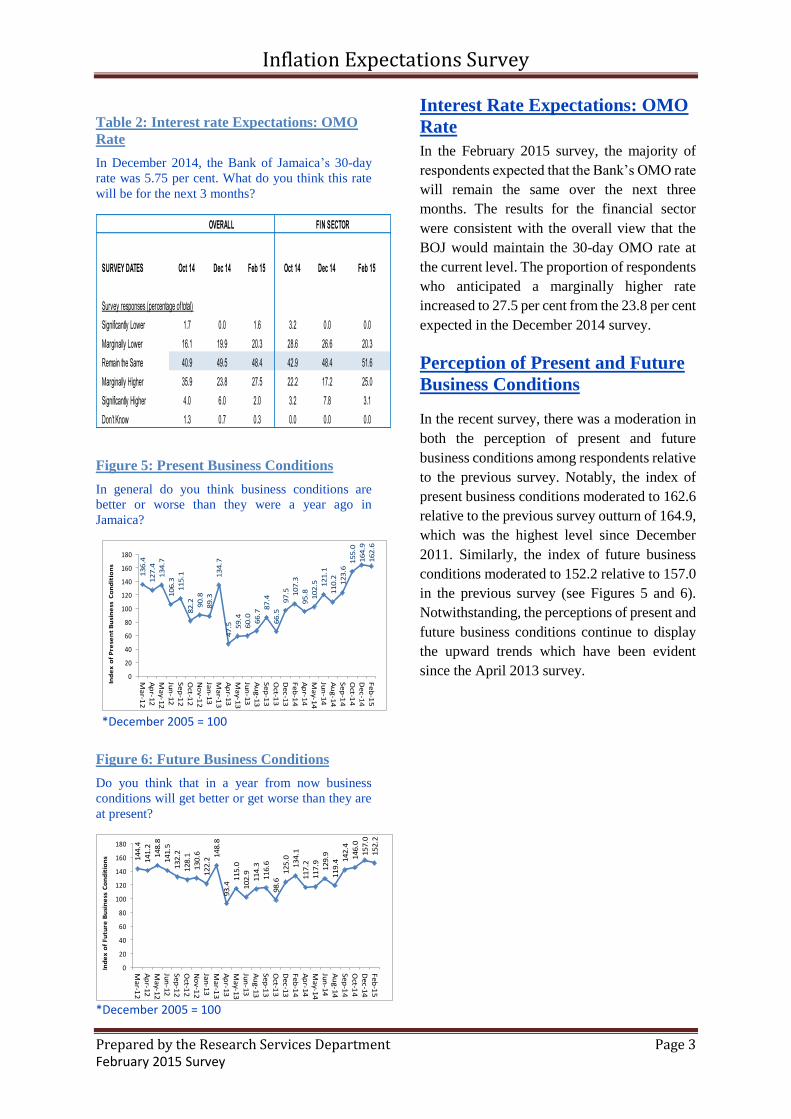

Table 2: Interest rate Expectations: OMO

Rate

In December 2014, the Bank of Jamaica’s 30-day

rate was 5.75 per cent. What do you think this rate

will be for the next 3 months?

SURVEY DATES Oct 14 Dec 14 Feb 15 Oct 14 Dec 14 Feb 15

Survey responses (percentage of total)

Significantly Lower 1.7 0.0 1.6 3.2 0.0 0.0

Marginally Lower 16.1 19.9 20.3 28.6 26.6 20.3

Remain the Same 40.9 49.5 48.4 42.9 48.4 51.6

Marginally Higher 35.9 23.8 27.5 22.2 17.2 25.0

Significantly Higher 4.0 6.0 2.0 3.2 7.8 3.1

Don’t Know 1.3 0.7 0.3 0.0 0.0 0.0

OVERALL FIN SECTOR

Figure 5: Present Business Conditions

In general do you think business conditions are

better or worse than they were a year ago in

Jamaica?

13

6.4

12

7.4

13

4.7

10

6.3

11

5.1

82

.2 90

.8

89

.3

13

4.7

47

.5 59

.4

60

.0 66

.7

87

.4

66

.5

97

.5 10

7.3

95

.8 10

2.5 1

21

.1

11

0.2 12

3.6

15

5.0

16

4.9

16

2.6

0

20

40

60

80

100

120

140

160

180

Ma

r-12

Ap

r-12

Ma

y-12

Jun

-12

Se

p-1

2

Oct-1

2

No

v-1

2

Jan

-13

Ma

r-13

Ap

r-13

Ma

y-13

Jun

-13

Au

g-1

3

Se

p-1

3

Oct-1

3

De

c-1

3

Fe

b-1

4

Ap

r-14

Ma

y-14

Jun

-14

Au

g-1

4

Se

p-1

4

Oct-1

4

De

c-1

4

Fe

b-1

5

Ind

ex

of

Pre

sen

t B

usi

ne

ss C

on

dit

ion

s

*December 2005 = 100

Figure 6: Future Business Conditions

Do you think that in a year from now business

conditions will get better or get worse than they are

at present?

14

4.4

14

1.2

14

8.8

14

1.5

13

2.2

12

8.1

13

0.6

12

2.2

14

8.8

93

.4

11

5.0

10

2.9

11

4.3

11

6.6

98

.6

12

5.0

13

4.1

11

7.2

11

7.9 12

9.9

11

9.4 1

42

.4

14

6.0

15

7.0

15

2.2

0

20

40

60

80

100

120

140

160

180

Ma

r-12

Ap

r-12

Ma

y-12

Jun

-12

Se

p-1

2

Oct-1

2

No

v-1

2

Jan

-13

Ma

r-13

Ap

r-13

Ma

y-13

Jun

-13

Au

g-1

3

Se

p-1

3

Oct-1

3

De

c-1

3

Fe

b-1

4

Ap

r-14

Ma

y-14

Jun

-14

Au

g-1

4

Se

p-1

4O

ct-14

De

c-1

4

Fe

b-1

5

Ind

ex

of

Fu

ture

Bu

sin

ess

Co

nd

itio

ns

*December 2005 = 100

Interest Rate Expectations: OMO

Rate

In the February 2015 survey, the majority of

respondents expected that the Bank’s OMO rate

will remain the same over the next three

months. The results for the financial sector

were consistent with the overall view that the

BOJ would maintain the 30-day OMO rate at

the current level. The proportion of respondents

who anticipated a marginally higher rate

increased to 27.5 per cent from the 23.8 per cent

expected in the December 2014 survey.

Perception of Present and Future

Business Conditions

In the recent survey, there was a moderation in

both the perception of present and future

business conditions among respondents relative

to the previous survey. Notably, the index of

present business conditions moderated to 162.6

relative to the previous survey outturn of 164.9,

which was the highest level since December

2011. Similarly, the index of future business

conditions moderated to 152.2 relative to 157.0

in the previous survey (see Figures 5 and 6).

Notwithstanding, the perceptions of present and

future business conditions continue to display

the upward trends which have been evident

since the April 2013 survey.

Inflation Expectations Survey

Prepared by the Research Services Department Page 4 February 2015 Survey

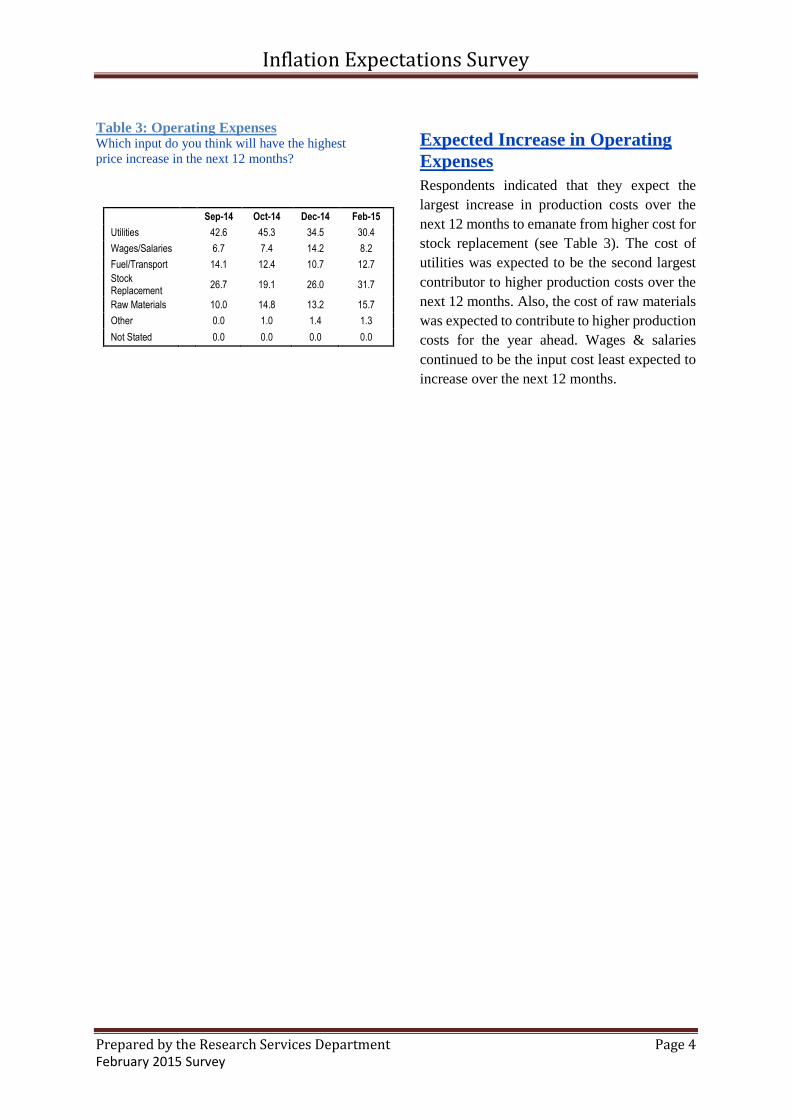

Table 3: Operating Expenses Which input do you think will have the highest

price increase in the next 12 months?

Sep-14 Oct-14 Dec-14 Feb-15

Utilities 42.6 45.3 34.5 30.4

Wages/Salaries 6.7 7.4 14.2 8.2

Fuel/Transport 14.1 12.4 10.7 12.7

Stock Replacement

26.7 19.1 26.0 31.7

Raw Materials 10.0 14.8 13.2 15.7

Other 0.0 1.0 1.4 1.3

Not Stated 0.0 0.0 0.0 0.0

Expected Increase in Operating

Expenses

Respondents indicated that they expect the

largest increase in production costs over the

next 12 months to emanate from higher cost for

stock replacement (see Table 3). The cost of

utilities was expected to be the second largest

contributor to higher production costs over the

next 12 months. Also, the cost of raw materials

was expected to contribute to higher production

costs for the year ahead. Wages & salaries

continued to be the input cost least expected to

increase over the next 12 months.