Download - Sunny Optical Technology Group Co., Limited

DISCLOSURE APPENDIX CONTAINS ANALYST CERTIFICATIONS AND THE STATUS OF NON US ANALYSTS. US Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

CREDIT SUISSE SECURITIES RESEARCH & ANALYTICS BEYOND INFORMATION®

Client-Driven Solutions, Insights, and Access

06 March 2013

Asia Pacific/China

Equity Research

Electronic Components & Connectors

Sunny Optical Technology Group Co., Limited (2382.HK / 2382 HK)

INITIATION

Lights, camera, action!

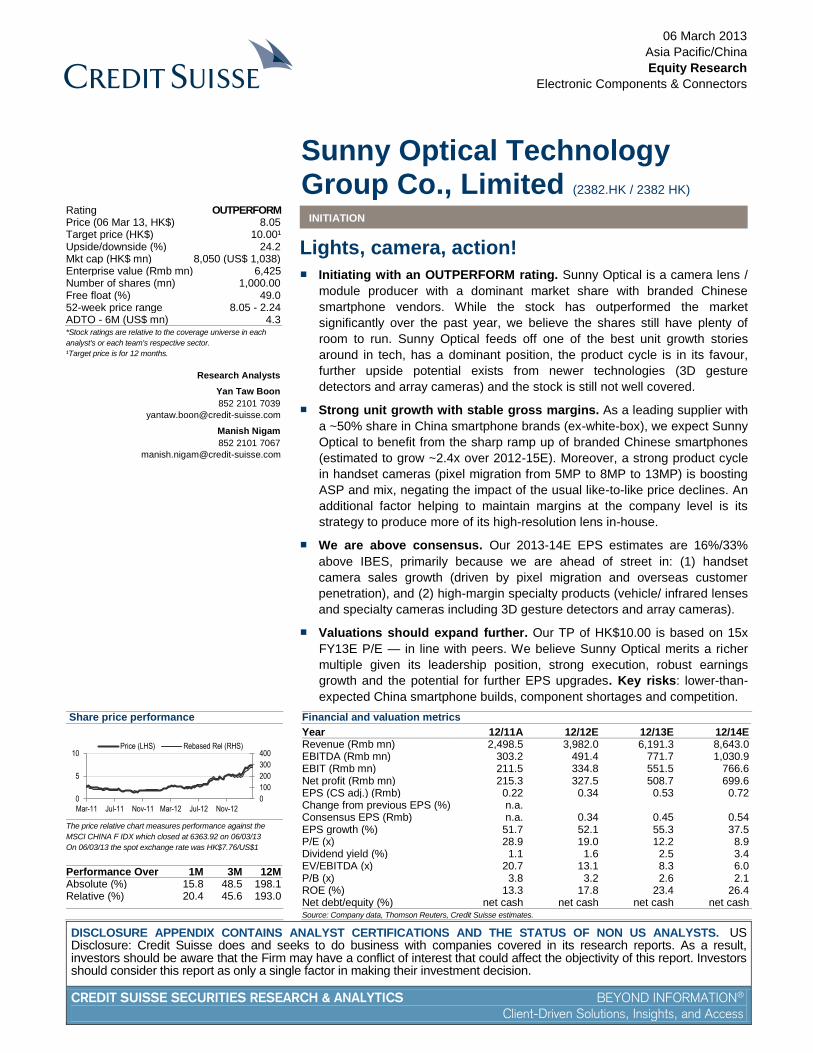

■ Initiating with an OUTPERFORM rating. Sunny Optical is a camera lens /

module producer with a dominant market share with branded Chinese

smartphone vendors. While the stock has outperformed the market

significantly over the past year, we believe the shares still have plenty of

room to run. Sunny Optical feeds off one of the best unit growth stories

around in tech, has a dominant position, the product cycle is in its favour,

further upside potential exists from newer technologies (3D gesture

detectors and array cameras) and the stock is still not well covered.

■ Strong unit growth with stable gross margins. As a leading supplier with

a ~50% share in China smartphone brands (ex-white-box), we expect Sunny

Optical to benefit from the sharp ramp up of branded Chinese smartphones

(estimated to grow ~2.4x over 2012-15E). Moreover, a strong product cycle

in handset cameras (pixel migration from 5MP to 8MP to 13MP) is boosting

ASP and mix, negating the impact of the usual like-to-like price declines. An

additional factor helping to maintain margins at the company level is its

strategy to produce more of its high-resolution lens in-house.

■ We are above consensus. Our 2013-14E EPS estimates are 16%/33%

above IBES, primarily because we are ahead of street in: (1) handset

camera sales growth (driven by pixel migration and overseas customer

penetration), and (2) high-margin specialty products (vehicle/ infrared lenses

and specialty cameras including 3D gesture detectors and array cameras).

■ Valuations should expand further. Our TP of HK$10.00 is based on 15x

FY13E P/E — in line with peers. We believe Sunny Optical merits a richer

multiple given its leadership position, strong execution, robust earnings

growth and the potential for further EPS upgrades. Key risks: lower-than-

expected China smartphone builds, component shortages and competition.

Share price performance

The price relative chart measures performance against the

MSCI CHINA F IDX which closed at 6363.92 on 06/03/13

On 06/03/13 the spot exchange rate was HK$7.76/US$1

Performance Over 1M 3M 12M Absolute (%) 15.8 48.5 198.1 Relative (%) 20.4 45.6 193.0

Financial and valuation metrics

Year 12/11A 12/12E 12/13E 12/14E Revenue (Rmb mn) 2,498.5 3,982.0 6,191.3 8,643.0 EBITDA (Rmb mn) 303.2 491.4 771.7 1,030.9 EBIT (Rmb mn) 211.5 334.8 551.5 766.6 Net profit (Rmb mn) 215.3 327.5 508.7 699.6 EPS (CS adj.) (Rmb) 0.22 0.34 0.53 0.72 Change from previous EPS (%) n.a. Consensus EPS (Rmb) n.a. 0.34 0.45 0.54 EPS growth (%) 51.7 52.1 55.3 37.5 P/E (x) 28.9 19.0 12.2 8.9 Dividend yield (%) 1.1 1.6 2.5 3.4 EV/EBITDA (x) 20.7 13.1 8.3 6.0 P/B (x) 3.8 3.2 2.6 2.1 ROE (%) 13.3 17.8 23.4 26.4 Net debt/equity (%) net cash net cash net cash net cash

Source: Company data, Thomson Reuters, Credit Suisse estimates.

0

100

200

300

400

0

5

10

Mar-11 Jul-11 Nov-11 Mar-12 Jul-12 Nov-12

Price (LHS) Rebased Rel (RHS)

Rating OUTPERFORM Price (06 Mar 13, HK$) 8.05 Target price (HK$) 10.00¹ Upside/downside (%) 24.2 Mkt cap (HK$ mn) 8,050 (US$ 1,038) Enterprise value (Rmb mn) 6,425 Number of shares (mn) 1,000.00 Free float (%) 49.0 52-week price range 8.05 - 2.24 ADTO - 6M (US$ mn) 4.3

*Stock ratings are relative to the coverage universe in each

analyst's or each team's respective sector.

¹Target price is for 12 months.

Research Analysts

Yan Taw Boon

852 2101 7039

Manish Nigam

852 2101 7067

06 March 2013

Sunny Optical Technology Group Co., Limited (2382.HK / 2382 HK) 2

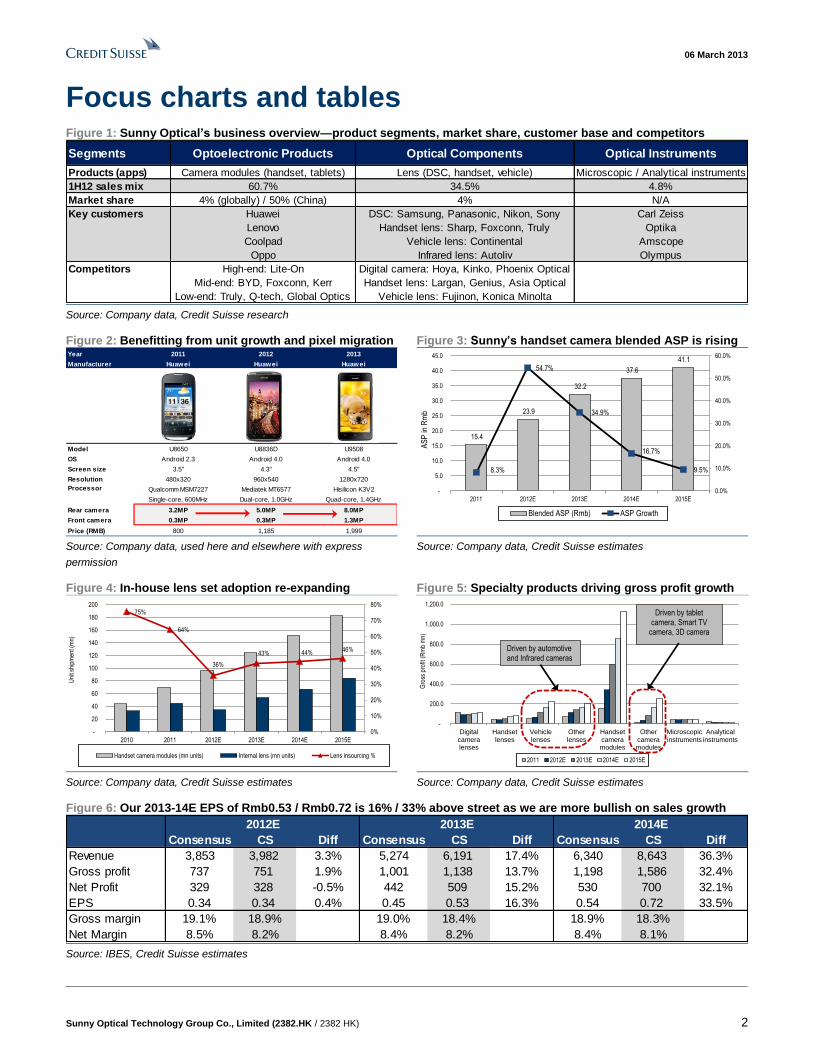

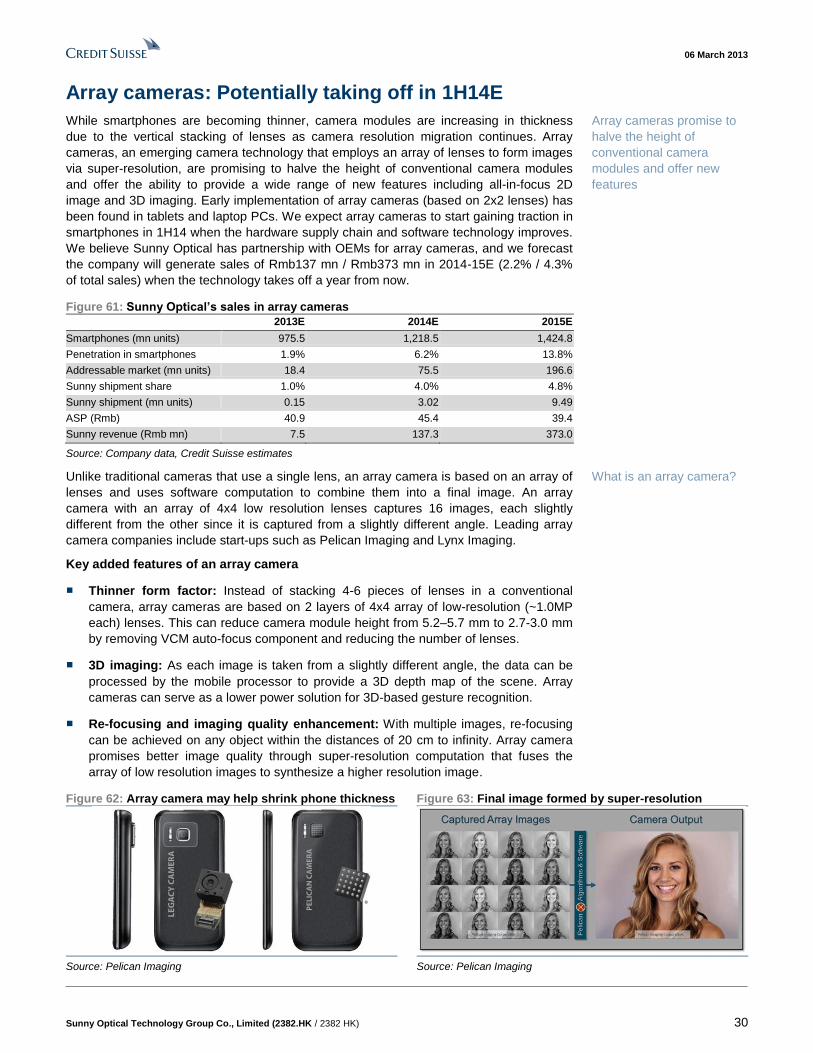

Focus charts and tables Figure 1: Sunny Optical’s business overview—product segments, market share, customer base and competitors

Source: Company data, Credit Suisse research

Figure 2: Benefitting from unit growth and pixel migration Figure 3: Sunny’s handset camera blended ASP is rising

Source: Company data, used here and elsewhere with express

permission

Source: Company data, Credit Suisse estimates

Figure 4: In-house lens set adoption re-expanding Figure 5: Specialty products driving gross profit growth

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

Figure 6: Our 2013-14E EPS of Rmb0.53 / Rmb0.72 is 16% / 33% above street as we are more bullish on sales growth

Source: IBES, Credit Suisse estimates

Segments Optoelectronic Products Optical Components Optical Instruments

Products (apps) Camera modules (handset, tablets) Lens (DSC, handset, vehicle) Microscopic / Analytical instruments

1H12 sales mix 60.7% 34.5% 4.8%

Market share 4% (globally) / 50% (China) 4% N/A

Key customers Huawei DSC: Samsung, Panasonic, Nikon, Sony Carl Zeiss

Lenovo Handset lens: Sharp, Foxconn, Truly Optika

Coolpad Vehicle lens: Continental Amscope

Oppo Infrared lens: Autoliv Olympus

Competitors High-end: Lite-On Digital camera: Hoya, Kinko, Phoenix Optical

Mid-end: BYD, Foxconn, Kerr Handset lens: Largan, Genius, Asia Optical

Low-end: Truly, Q-tech, Global Optics Vehicle lens: Fujinon, Konica Minolta

Year 2011 2012 2013

Manufacturer Huawei Huawei Huawei

Model U8650 U8836D U9508

OS Android 2.3 Android 4.0 Android 4.0

Screen size 3.5" 4.3" 4.5"

Resolution 480x320 960x540 1280x720

Qualcomm MSM7227 Mediatek MT6577 Hisilicon K3V2

Single-core, 600MHz Dual-core, 1.0GHz Quad-core, 1.4GHz

Rear camera 3.2MP 5.0MP 8.0MP

Front camera 0.3MP 0.3MP 1.3MP

Price (RMB) 800 1,185 1,999

Processor

15.4

23.9

32.2

37.6

41.1

8.3%

54.7%

34.9%

16.7%

9.5%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

-

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

2011 2012E 2013E 2014E 2015E

AS

P in

Rm

b

Blended ASP (Rmb) ASP Growth

75%

64%

36%

43% 44% 46%

0%

10%

20%

30%

40%

50%

60%

70%

80%

-

20

40

60

80

100

120

140

160

180

200

2010 2011 2012E 2013E 2014E 2015E

Uni

t shi

pmen

t (m

n)

Handset camera modules (mn units) Internal lens (mn units) Lens insourcing %

-

200.0

400.0

600.0

800.0

1,000.0

1,200.0

Digitalcameralenses

Handsetlenses

Vehiclelenses

Otherlenses

Handsetcameramodules

Othercameramodules

Microscopicinstruments

Analyticalinstruments

Gro

ss p

rofit

(R

mb

mn)

2011 2012E 2013E 2014E 2015E

Driven by automotive and Infrared cameras

Driven by tablet camera, Smart TV

camera, 3D camera

Consensus CS Diff Consensus CS Diff Consensus CS Diff

Revenue 3,853 3,982 3.3% 5,274 6,191 17.4% 6,340 8,643 36.3%

Gross profit 737 751 1.9% 1,001 1,138 13.7% 1,198 1,586 32.4%

Net Profit 329 328 -0.5% 442 509 15.2% 530 700 32.1%

EPS 0.34 0.34 0.4% 0.45 0.53 16.3% 0.54 0.72 33.5%

Gross margin 19.1% 18.9% 19.0% 18.4% 18.9% 18.3%

Net Margin 8.5% 8.2% 8.4% 8.2% 8.4% 8.1%

2012E 2013E 2014E

06 March 2013

Sunny Optical Technology Group Co., Limited (2382.HK / 2382 HK) 3

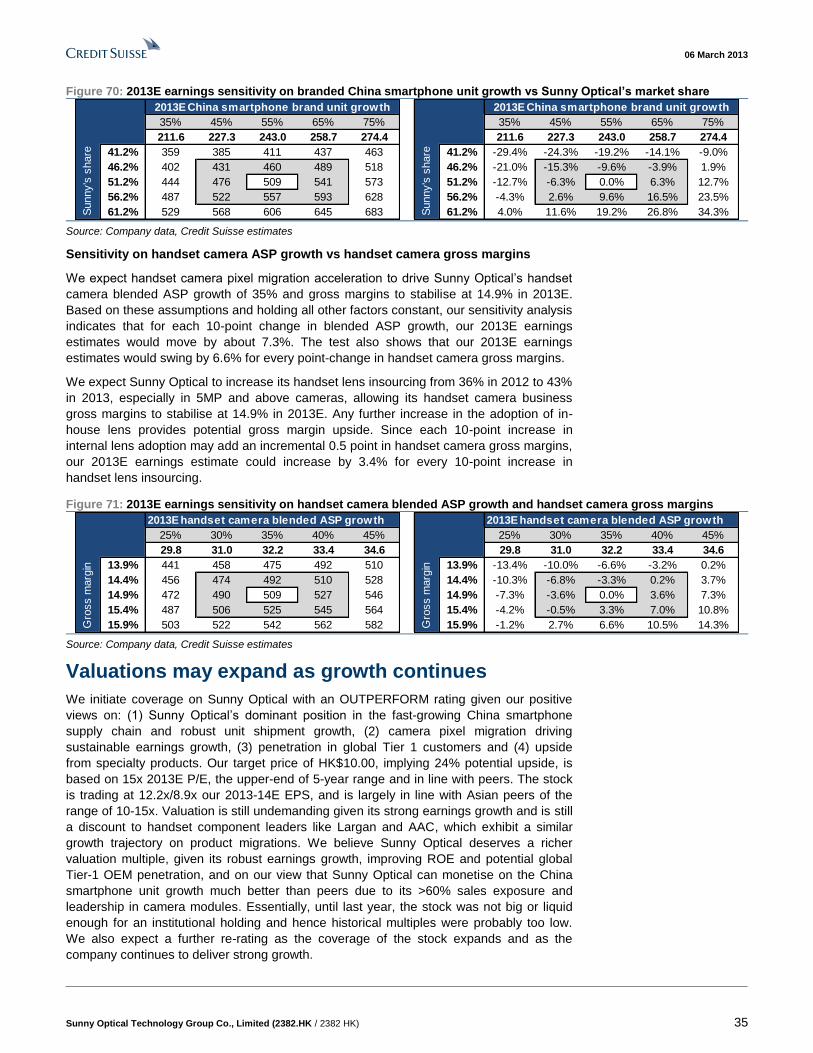

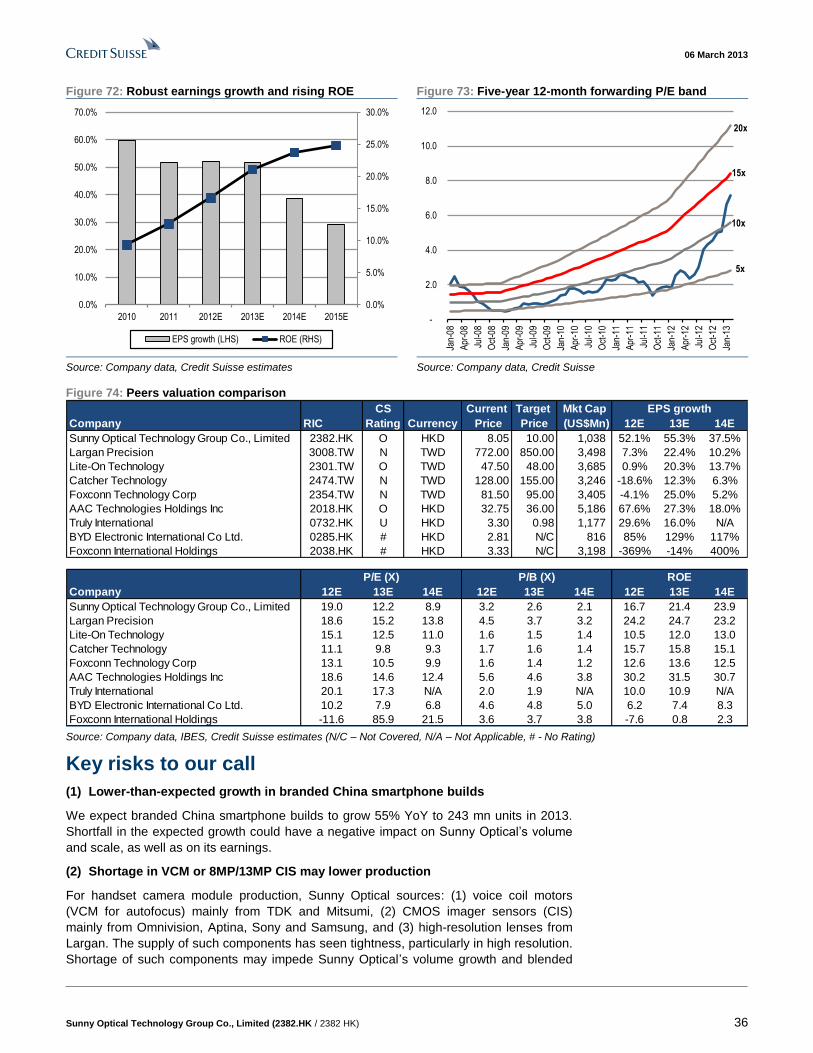

Lights, camera, action! We initiate coverage on Sunny Optical with an OUTPERFORM rating and a TP of HK$10.0.

Our positive stance is based on Sunny Optical’s: (1) dominant position in China smartphone

supply chain and robust unit shipment growth, (2) view of sustainable earnings growth driven

by pixel migration, (3) potential penetration at global tier one customers, and (4) upside

potential from specialty products (vehicle/IR lenses, tablets, gesture control, array cameras).

Riding on China smartphone growth

Sunny Optical is a leading handset camera lens/module maker in China (over 60% of

revenue from handset cameras) with top-tier Chinese smartphone OEMs (Huawei,

Lenovo, Coolpad, Oppo) as its customers. We estimate that branded Chinese smartphone

builds will see a 172% CAGR over 2011-15E, from 43 mn units to 382 mn units, driven by

share gains in the domestic market and export channel expansion. With its dominant

share (~50%) in branded Chines smartphones, we view Sunny Optical as one of the best

proxies of China smartphone growth. While competition is intense, Sunny Optical is

solidifying its position with its edge in vertical integration, strong optical imaging know-how

and long-standing customer relationship. China smartphone camera pixel migration is

raising the entry barrier further, widening the gap against domestic low-end competitors.

Mix improvement + lens insourcing = stable margins

Rapid smartphone market growth is leading to aggressive camera pixel migration as

OEMs compete to provide better imaging experience to consumers. Chinese smartphone

brands are still one generation behind at 3MP/5MP versus global brands which are ahead

at 5MP/8MP. As Chinese smartphones play catch up in pixel migration, we expect Sunny

Optical’s sales mix of 8MP and above camera modules to rise from 18.5% in 2012E to

50.3%/77.6%/88.6% over 2013-15E. Despite a like-to-like price erosion of 10-30%, rising

sales of high-resolution camera modules should drive blended ASP higher. Further, as the

company improves its high-resolution handset lens production capability, we look for a

rebound in its lens insourcing starting 2Q13E. We expect improving product mix and

increase insourcing of lenses to lead to sustainable gross margins (c.15%) in 2013-15E.

Specialty products providing upside

Beyond handset cameras, multiple new products are emerging as key earnings drivers,

such as vehicle / infrared lens, tablet cameras, Smart TV cameras and other specialty

cameras (gesture control and array cameras). While Sunny Optical is likely to gain more

lens outsourcing orders from Japanese digital still camera (DSC) makers, we do not

expect its DSC product sales to grow over the next few year given the cannibalisation from

smartphones. The rapid expansion of new high-margin specialty products should more

than offset the weaknesses in digital camera-related products, in our view. Future positive

revenue surprise could come if gesture control or if array cameras find wider acceptance.

Street’s earnings estimates look too light

Our 2013/2014 EPS estimates are 16%/33% above consensus as we are more bullish on

blended ASP growth and high-margin specialty products. We expect Sunny to deliver

52%/55%/38%/30% earnings growth in 2012-15E. Our target price of HK$10.0 is based on

15x FY13E P/E, the upper-end of its five-year range and in line with peers. We believe

Sunny deserves a richer valuation given its strong earnings growth, expanding ROE and

potential global tier one customer penetration. Essentially, until last year the stock, was not

big or liquid enough for an institutional holding; hence historical multiples were probably

too low. Key risks include: (1) lower-than-expected growth in China smartphone builds,

(2) component shortage (VCM and 8MP/13MP CIS), (3) intensified pricing pressure in

camera modules, and (4) slower-than-expected ramp-up of specialty cameras/lenses.

Sunny Optical is a key

beneficiary of unit growth in

China smartphone brands

Ramp-up of 8MP/13MP

handset cameras increasing

blended ASPs

Specialty lens and cameras

are emerging as earnings

drivers, offsetting DSC

weaknesses

Sunny, in our view,

deserves a richer valuation

given its earnings

momentum and expanding

ROE

06 March 2013

Sunny Optical Technology Group Co., Limited (2382.HK / 2382 HK) 4

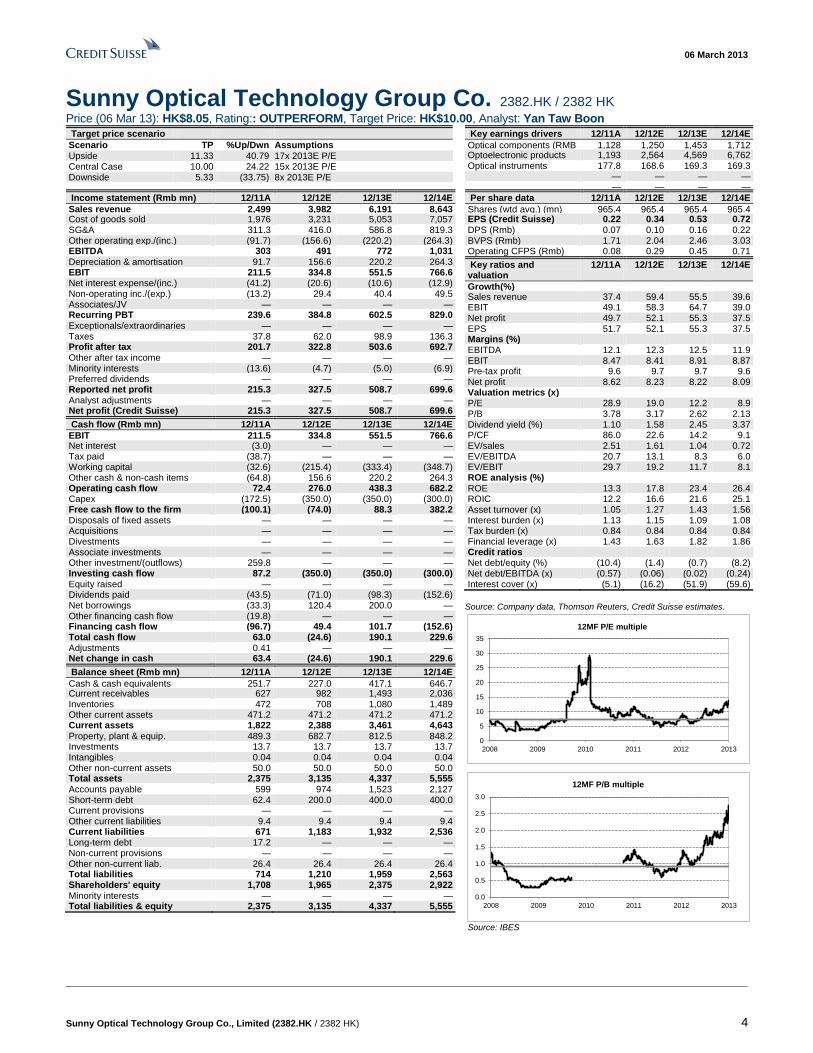

Sunny Optical Technology Group Co. 2382.HK / 2382 HK Price (06 Mar 13): HK$8.05, Rating:: OUTPERFORM, Target Price: HK$10.00, Analyst: Yan Taw Boon

Target price scenario

Scenario TP %Up/Dwn Assumptions Upside 11.33 40.79 17x 2013E P/E Central Case 10.00 24.22 15x 2013E P/E Downside 5.33 (33.75) 8x 2013E P/E

Key earnings drivers 12/11A 12/12E 12/13E 12/14E

Optical components (RMB mn)

1,128 1,250 1,453 1,712 Optoelectronic products 1,193 2,564 4,569 6,762 Optical instruments 177.8 168.6 169.3 169.3 — — — — — — — —

Income statement (Rmb mn) 12/11A 12/12E 12/13E 12/14E

Sales revenue 2,499 3,982 6,191 8,643 Cost of goods sold 1,976 3,231 5,053 7,057 SG&A 311.3 416.0 586.8 819.3 Other operating exp./(inc.) (91.7) (156.6) (220.2) (264.3) EBITDA 303 491 772 1,031 Depreciation & amortisation 91.7 156.6 220.2 264.3 EBIT 211.5 334.8 551.5 766.6 Net interest expense/(inc.) (41.2) (20.6) (10.6) (12.9) Non-operating inc./(exp.) (13.2) 29.4 40.4 49.5 Associates/JV — — — — Recurring PBT 239.6 384.8 602.5 829.0 Exceptionals/extraordinaries — — — — Taxes 37.8 62.0 98.9 136.3 Profit after tax 201.7 322.8 503.6 692.7 Other after tax income — — — — Minority interests (13.6) (4.7) (5.0) (6.9) Preferred dividends — — — — Reported net profit 215.3 327.5 508.7 699.6 Analyst adjustments — — — — Net profit (Credit Suisse) 215.3 327.5 508.7 699.6

Cash flow (Rmb mn) 12/11A 12/12E 12/13E 12/14E

EBIT 211.5 334.8 551.5 766.6 Net interest (3.0) — — — Tax paid (38.7) — — — Working capital (32.6) (215.4) (333.4) (348.7) Other cash & non-cash items (64.8) 156.6 220.2 264.3 Operating cash flow 72.4 276.0 438.3 682.2 Capex (172.5) (350.0) (350.0) (300.0) Free cash flow to the firm (100.1) (74.0) 88.3 382.2 Disposals of fixed assets — — — — Acquisitions — — — — Divestments — — — — Associate investments — — — — Other investment/(outflows) 259.8 — — — Investing cash flow 87.2 (350.0) (350.0) (300.0) Equity raised — — — — Dividends paid (43.5) (71.0) (98.3) (152.6) Net borrowings (33.3) 120.4 200.0 — Other financing cash flow (19.8) — — — Financing cash flow (96.7) 49.4 101.7 (152.6) Total cash flow 63.0 (24.6) 190.1 229.6 Adjustments 0.41 — — — Net change in cash 63.4 (24.6) 190.1 229.6

Balance sheet (Rmb mn) 12/11A 12/12E 12/13E 12/14E

Cash & cash equivalents 251.7 227.0 417.1 646.7 Current receivables 627 982 1,493 2,036 Inventories 472 708 1,080 1,489 Other current assets 471.2 471.2 471.2 471.2 Current assets 1,822 2,388 3,461 4,643 Property, plant & equip. 489.3 682.7 812.5 848.2 Investments 13.7 13.7 13.7 13.7 Intangibles 0.04 0.04 0.04 0.04 Other non-current assets 50.0 50.0 50.0 50.0 Total assets 2,375 3,135 4,337 5,555 Accounts payable 599 974 1,523 2,127 Short-term debt 62.4 200.0 400.0 400.0 Current provisions — — — — Other current liabilities 9.4 9.4 9.4 9.4 Current liabilities 671 1,183 1,932 2,536 Long-term debt 17.2 — — — Non-current provisions — — — — Other non-current liab. 26.4 26.4 26.4 26.4 Total liabilities 714 1,210 1,959 2,563 Shareholders' equity 1,708 1,965 2,375 2,922 Minority interests — — — — Total liabilities & equity 2,375 3,135 4,337 5,555

Per share data 12/11A 12/12E 12/13E 12/14E

Shares (wtd avg.) (mn) 965.4 965.4 965.4 965.4 EPS (Credit Suisse) (Rmb)

0.22 0.34 0.53 0.72 DPS (Rmb) 0.07 0.10 0.16 0.22 BVPS (Rmb) 1.71 2.04 2.46 3.03 Operating CFPS (Rmb) 0.08 0.29 0.45 0.71

Key ratios and valuation

12/11A 12/12E 12/13E 12/14E

Growth(%) Sales revenue 37.4 59.4 55.5 39.6 EBIT 49.1 58.3 64.7 39.0 Net profit 49.7 52.1 55.3 37.5 EPS 51.7 52.1 55.3 37.5 Margins (%) EBITDA 12.1 12.3 12.5 11.9 EBIT 8.47 8.41 8.91 8.87 Pre-tax profit 9.6 9.7 9.7 9.6 Net profit 8.62 8.23 8.22 8.09 Valuation metrics (x) P/E 28.9 19.0 12.2 8.9 P/B 3.78 3.17 2.62 2.13 Dividend yield (%) 1.10 1.58 2.45 3.37 P/CF 86.0 22.6 14.2 9.1 EV/sales 2.51 1.61 1.04 0.72 EV/EBITDA 20.7 13.1 8.3 6.0 EV/EBIT 29.7 19.2 11.7 8.1 ROE analysis (%) ROE 13.3 17.8 23.4 26.4 ROIC 12.2 16.6 21.6 25.1 Asset turnover (x) 1.05 1.27 1.43 1.56 Interest burden (x) 1.13 1.15 1.09 1.08 Tax burden (x) 0.84 0.84 0.84 0.84 Financial leverage (x) 1.43 1.63 1.82 1.86 Credit ratios Net debt/equity (%) (10.4) (1.4) (0.7) (8.2) Net debt/EBITDA (x) (0.57) (0.06) (0.02) (0.24) Interest cover (x) (5.1) (16.2) (51.9) (59.6)

Source: Company data, Thomson Reuters, Credit Suisse estimates.

Source: IBES

0

5

10

15

20

25

30

35

2008 2009 2010 2011 2012 2013

12MF P/E multiple

0.0

0.5

1.0

1.5

2.0

2.5

3.0

2008 2009 2010 2011 2012 2013

12MF P/B multiple

06 March 2013

Sunny Optical Technology Group Co., Limited (2382.HK / 2382 HK) 5

Table of contents Focus charts and tables 2 Lights, camera, action ! 3

Riding on China smartphone growth 3 Mix improvement + lens insourcing = stable margins 3 Specialty products providing upside 3 Street’s earnings estimates are too light 3

Sunny Optical Technology Group Co. 2382.HK / 2382 HK 4 Riding on China smartphone growth 6

A leading China smartphone camera module supplier 6 Global smartphone shipments going higher 7 Chinese smartphone share gains accelerating 7 A small player in a large global market ….. 10 …. and a fragmented supply chain ….. 10 …But dominates the China smartphone supply chain 11 Competitive edges strengthening market position 12

Mix improvement + lens insourcing = stable margins 14 Handset camera pixel migration trend continues 14 Image sensor innovations supporting pixel migration 16 Chinese smartphones migrating to 8/13MP in 2013 17 Pixel migration driving volume growth and better mix 18 Improving mix supporting rising blended ASP 19 Largan saw similar growth due to pixel migration 20 Revamp of in-house lens stabilizing gross margins 20

Specialty products providing upside 22 (1) Vehicle lens: Automotive cameras expanding fast 22 (2) Infrared lens: a long-tail growth opportunity 23 (3) Smart TV video module market growth continues 25 (4) Tablet cameras and emerging specialty cameras 26 Gesture recognition broadening addressable market 27 Array cameras – potentially taking off in 1H14E 30 New products offset digital still camera weakness 31

Street’s earnings estimates too light 32 Earnings outlook 32 Balance sheet analysis 33 CS estimates versus consensus 34 Sensitivity analysis 34 Valuations may expand as growth continues 35 Key risks to our call 36

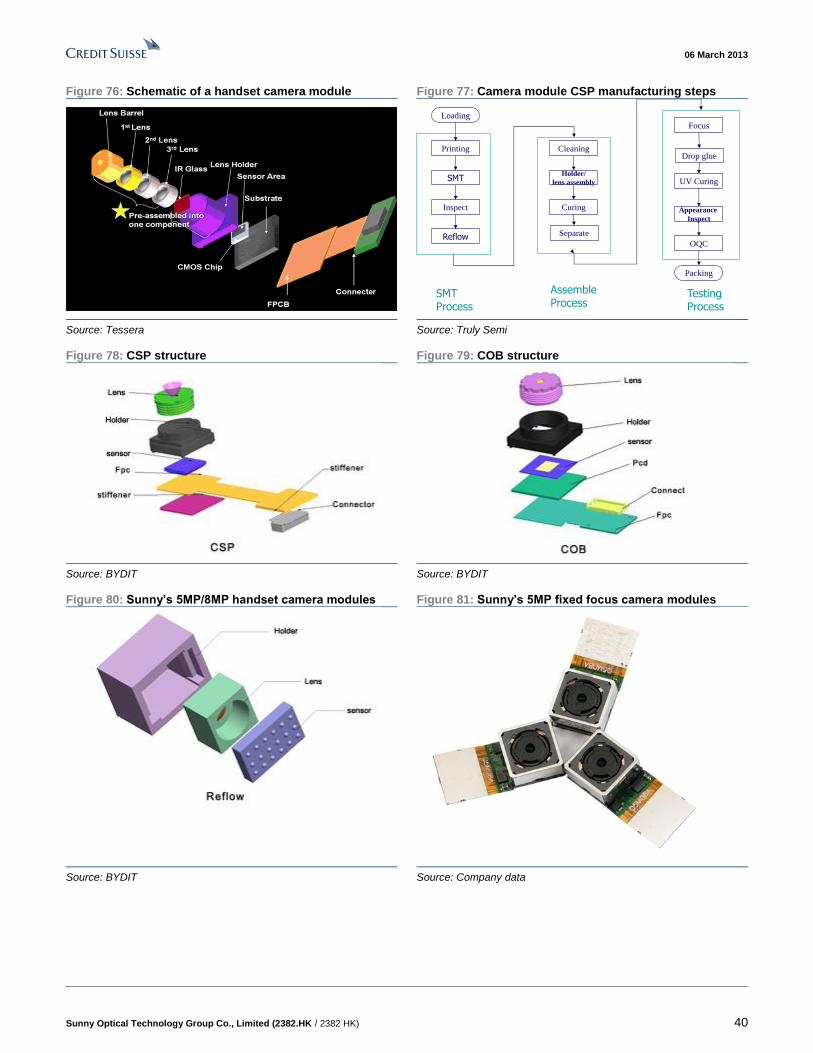

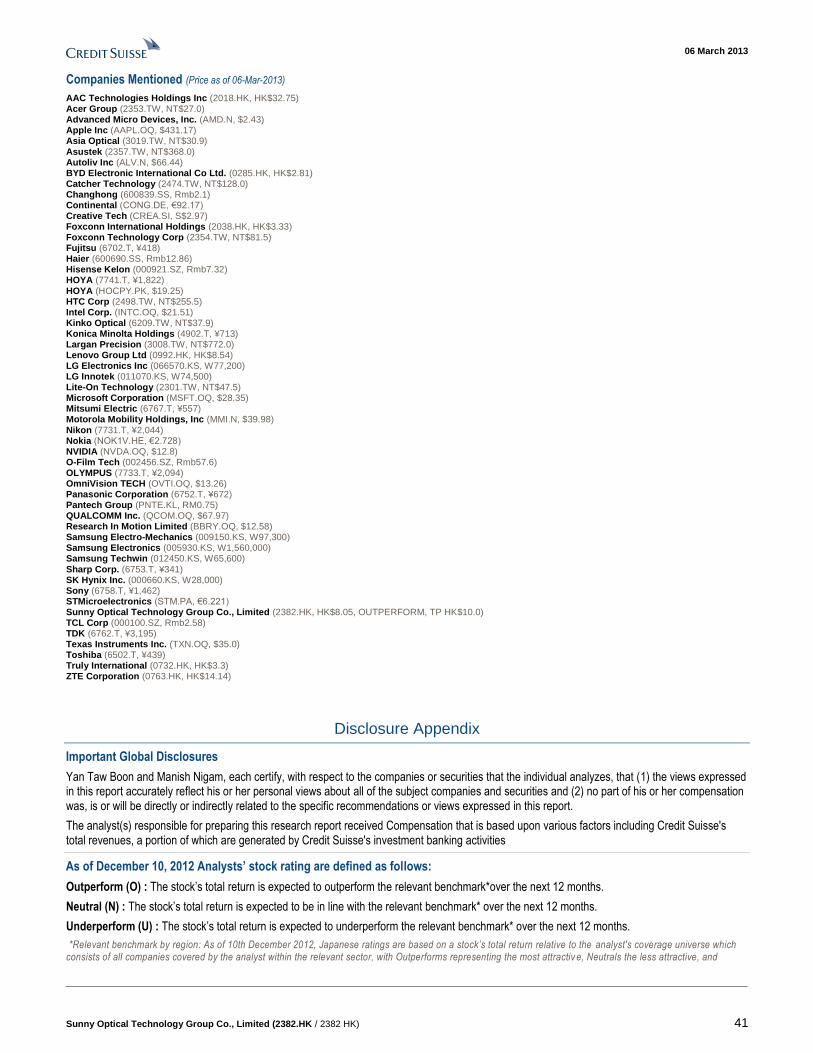

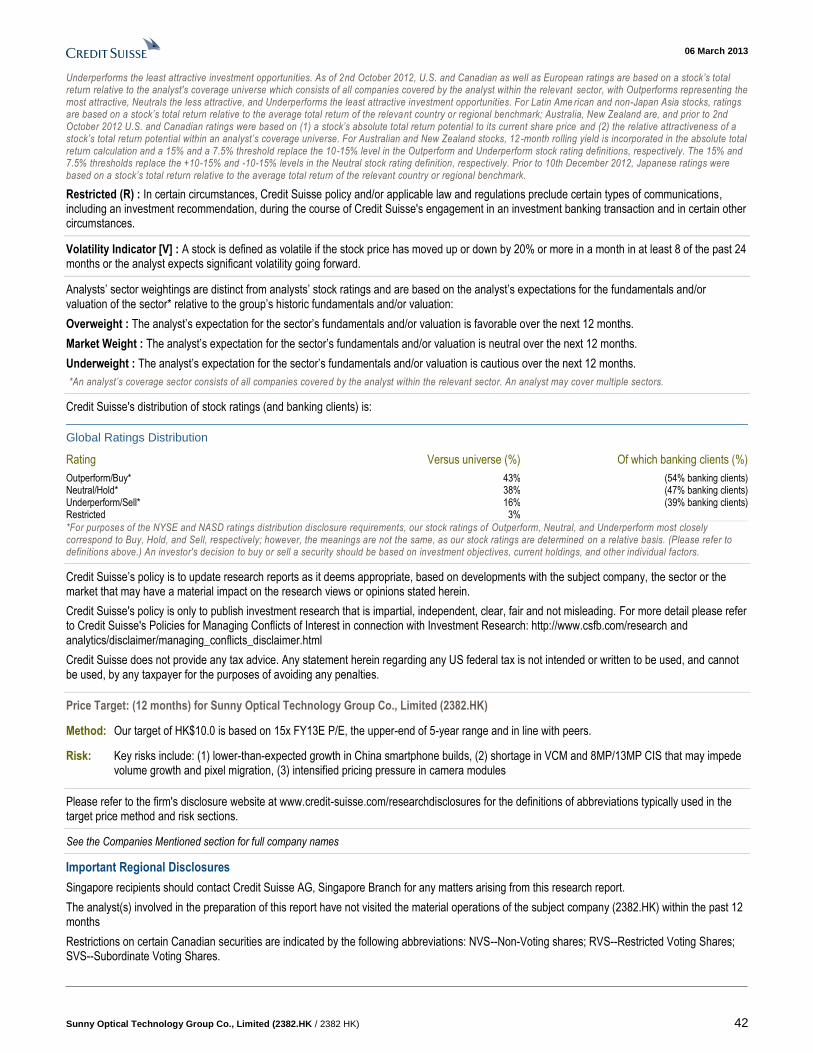

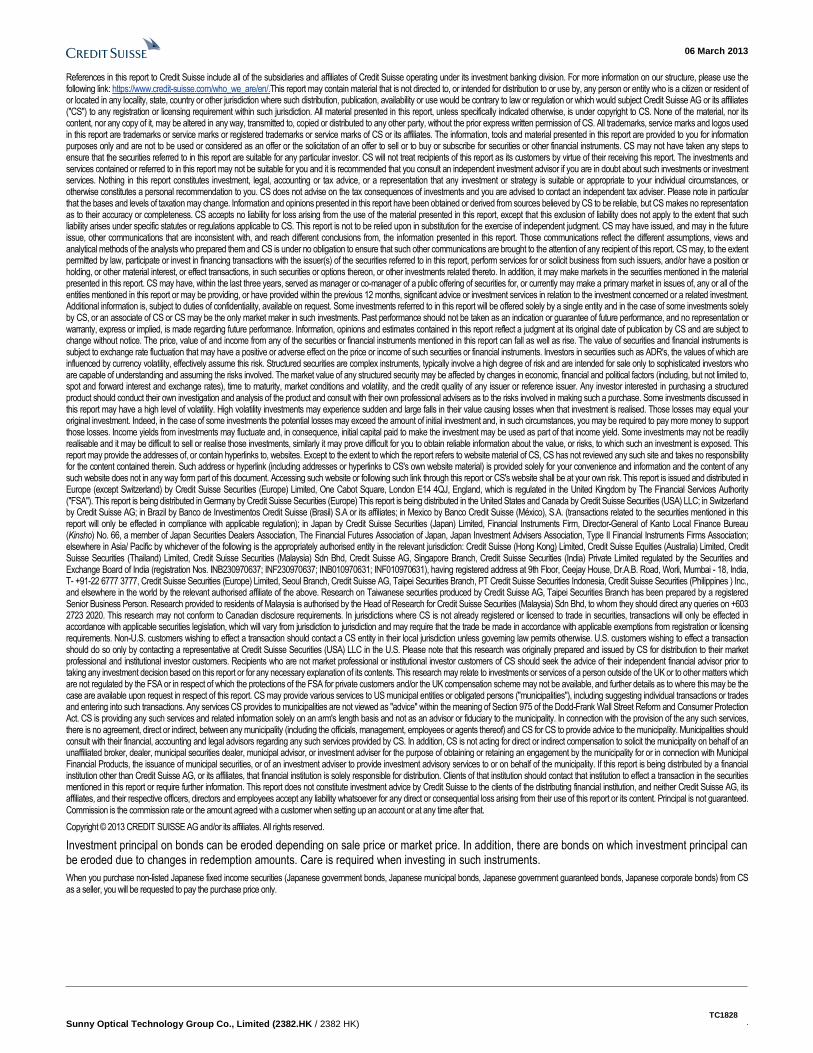

Appendices 38 Company background 38 Employees and production bases 38 Sunny Optical management team profiles 38 Handset camera lens and modules 39

06 March 2013

Sunny Optical Technology Group Co., Limited (2382.HK / 2382 HK) 6

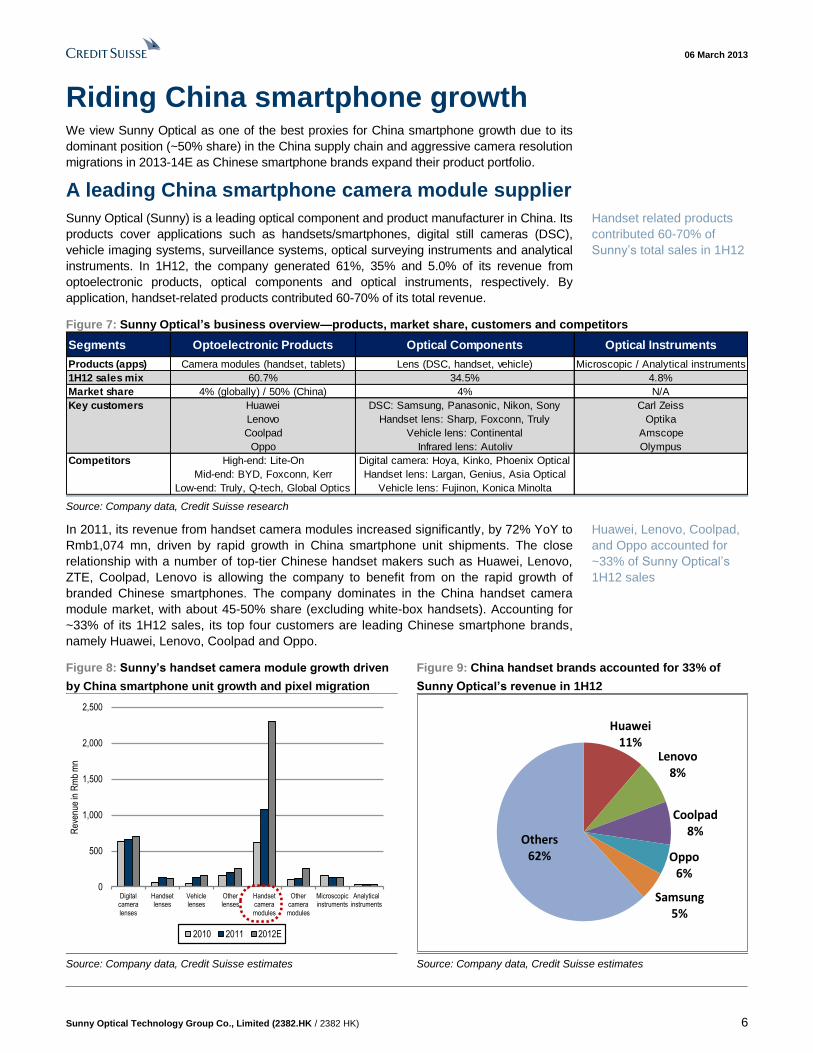

Riding China smartphone growth We view Sunny Optical as one of the best proxies for China smartphone growth due to its

dominant position (~50% share) in the China supply chain and aggressive camera resolution

migrations in 2013-14E as Chinese smartphone brands expand their product portfolio.

A leading China smartphone camera module supplier

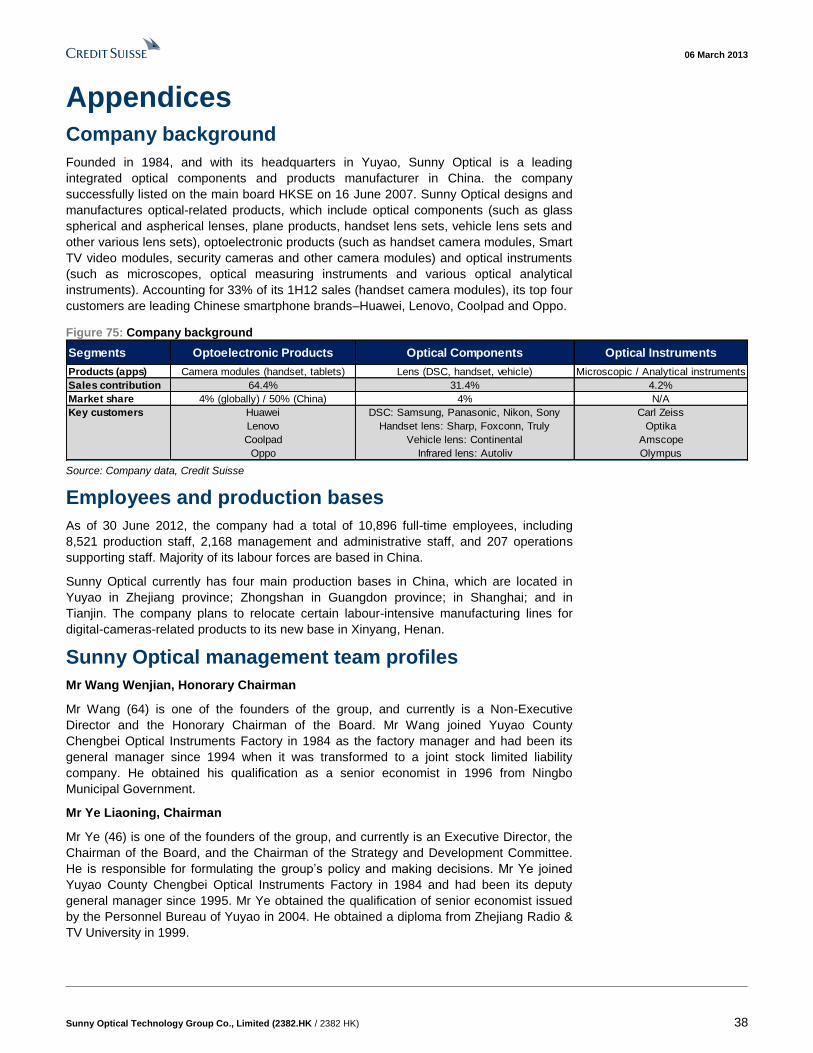

Sunny Optical (Sunny) is a leading optical component and product manufacturer in China. Its

products cover applications such as handsets/smartphones, digital still cameras (DSC),

vehicle imaging systems, surveillance systems, optical surveying instruments and analytical

instruments. In 1H12, the company generated 61%, 35% and 5.0% of its revenue from

optoelectronic products, optical components and optical instruments, respectively. By

application, handset-related products contributed 60-70% of its total revenue.

Figure 7: Sunny Optical’s business overview—products, market share, customers and competitors

Source: Company data, Credit Suisse research

In 2011, its revenue from handset camera modules increased significantly, by 72% YoY to

Rmb1,074 mn, driven by rapid growth in China smartphone unit shipments. The close

relationship with a number of top-tier Chinese handset makers such as Huawei, Lenovo,

ZTE, Coolpad, Lenovo is allowing the company to benefit from on the rapid growth of

branded Chinese smartphones. The company dominates in the China handset camera

module market, with about 45-50% share (excluding white-box handsets). Accounting for

~33% of its 1H12 sales, its top four customers are leading Chinese smartphone brands,

namely Huawei, Lenovo, Coolpad and Oppo.

Figure 8: Sunny’s handset camera module growth driven

by China smartphone unit growth and pixel migration

Figure 9: China handset brands accounted for 33% of

Sunny Optical’s revenue in 1H12

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

Segments Optoelectronic Products Optical Components Optical Instruments

Products (apps) Camera modules (handset, tablets) Lens (DSC, handset, vehicle) Microscopic / Analytical instruments

1H12 sales mix 60.7% 34.5% 4.8%

Market share 4% (globally) / 50% (China) 4% N/A

Key customers Huawei DSC: Samsung, Panasonic, Nikon, Sony Carl Zeiss

Lenovo Handset lens: Sharp, Foxconn, Truly Optika

Coolpad Vehicle lens: Continental Amscope

Oppo Infrared lens: Autoliv Olympus

Competitors High-end: Lite-On Digital camera: Hoya, Kinko, Phoenix Optical

Mid-end: BYD, Foxconn, Kerr Handset lens: Largan, Genius, Asia Optical

Low-end: Truly, Q-tech, Global Optics Vehicle lens: Fujinon, Konica Minolta

0

500

1,000

1,500

2,000

2,500

Digitalcameralenses

Handsetlenses

Vehiclelenses

Otherlenses

Handsetcameramodules

Othercameramodules

Microscopicinstruments

Analyticalinstruments

Rev

enue

in R

mb

mn

2010 2011 2012E

Huawei11%

Lenovo 8%

Coolpad 8%

Oppo 6%

Samsung5%

Others62%

Handset related products

contributed 60-70% of

Sunny’s total sales in 1H12

Huawei, Lenovo, Coolpad,

and Oppo accounted for

~33% of Sunny Optical’s

1H12 sales

06 March 2013

Sunny Optical Technology Group Co., Limited (2382.HK / 2382 HK) 7

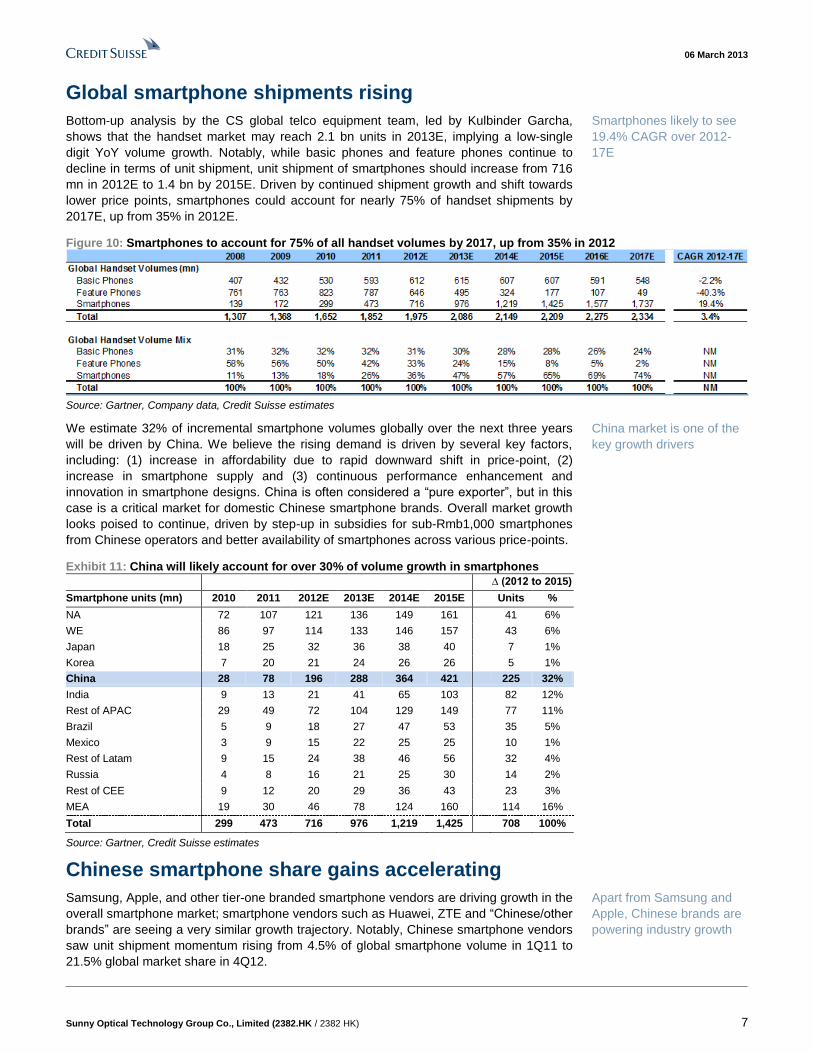

Global smartphone shipments rising

Bottom-up analysis by the CS global telco equipment team, led by Kulbinder Garcha,

shows that the handset market may reach 2.1 bn units in 2013E, implying a low-single

digit YoY volume growth. Notably, while basic phones and feature phones continue to

decline in terms of unit shipment, unit shipment of smartphones should increase from 716

mn in 2012E to 1.4 bn by 2015E. Driven by continued shipment growth and shift towards

lower price points, smartphones could account for nearly 75% of handset shipments by

2017E, up from 35% in 2012E.

Figure 10: Smartphones to account for 75% of all handset volumes by 2017, up from 35% in 2012

Source: Gartner, Company data, Credit Suisse estimates

We estimate 32% of incremental smartphone volumes globally over the next three years

will be driven by China. We believe the rising demand is driven by several key factors,

including: (1) increase in affordability due to rapid downward shift in price-point, (2)

increase in smartphone supply and (3) continuous performance enhancement and

innovation in smartphone designs. China is often considered a “pure exporter”, but in this

case is a critical market for domestic Chinese smartphone brands. Overall market growth

looks poised to continue, driven by step-up in subsidies for sub-Rmb1,000 smartphones

from Chinese operators and better availability of smartphones across various price-points.

Exhibit 11: China will likely account for over 30% of volume growth in smartphones

∆ (2012 to 2015)

Smartphone units (mn) 2010 2011 2012E 2013E 2014E 2015E Units %

NA 72 107 121 136 149 161 41 6%

WE 86 97 114 133 146 157 43 6%

Japan 18 25 32 36 38 40 7 1%

Korea 7 20 21 24 26 26 5 1%

China 28 78 196 288 364 421 225 32%

India 9 13 21 41 65 103 82 12%

Rest of APAC 29 49 72 104 129 149 77 11%

Brazil 5 9 18 27 47 53 35 5%

Mexico 3 9 15 22 25 25 10 1%

Rest of Latam 9 15 24 38 46 56 32 4%

Russia 4 8 16 21 25 30 14 2%

Rest of CEE 9 12 20 29 36 43 23 3%

MEA 19 30 46 78 124 160 114 16%

Total 299 473 716 976 1,219 1,425 708 100%

Source: Gartner, Credit Suisse estimates

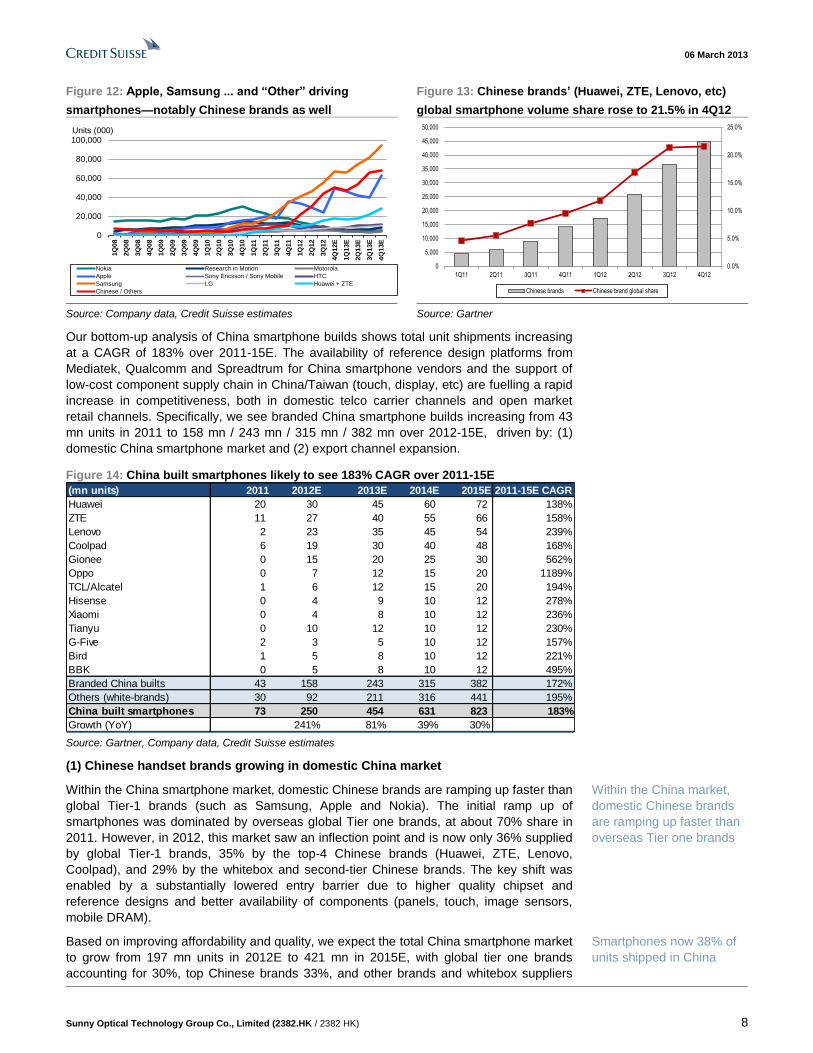

Chinese smartphone share gains accelerating

Samsung, Apple, and other tier-one branded smartphone vendors are driving growth in the

overall smartphone market; smartphone vendors such as Huawei, ZTE and “Chinese/other

brands” are seeing a very similar growth trajectory. Notably, Chinese smartphone vendors

saw unit shipment momentum rising from 4.5% of global smartphone volume in 1Q11 to

21.5% global market share in 4Q12.

Smartphones likely to see

19.4% CAGR over 2012-

17E

China market is one of the

key growth drivers

Apart from Samsung and

Apple, Chinese brands are

powering industry growth

06 March 2013

Sunny Optical Technology Group Co., Limited (2382.HK / 2382 HK) 8

Figure 12: Apple, Samsung ... and “Other” driving

smartphones—notably Chinese brands as well

Figure 13: Chinese brands’ (Huawei, ZTE, Lenovo, etc)

global smartphone volume share rose to 21.5% in 4Q12

Source: Company data, Credit Suisse estimates Source: Gartner

Our bottom-up analysis of China smartphone builds shows total unit shipments increasing

at a CAGR of 183% over 2011-15E. The availability of reference design platforms from

Mediatek, Qualcomm and Spreadtrum for China smartphone vendors and the support of

low-cost component supply chain in China/Taiwan (touch, display, etc) are fuelling a rapid

increase in competitiveness, both in domestic telco carrier channels and open market

retail channels. Specifically, we see branded China smartphone builds increasing from 43

mn units in 2011 to 158 mn / 243 mn / 315 mn / 382 mn over 2012-15E, driven by: (1)

domestic China smartphone market and (2) export channel expansion.

Figure 14: China built smartphones likely to see 183% CAGR over 2011-15E

Source: Gartner, Company data, Credit Suisse estimates

(1) Chinese handset brands growing in domestic China market

Within the China smartphone market, domestic Chinese brands are ramping up faster than

global Tier-1 brands (such as Samsung, Apple and Nokia). The initial ramp up of

smartphones was dominated by overseas global Tier one brands, at about 70% share in

2011. However, in 2012, this market saw an inflection point and is now only 36% supplied

by global Tier-1 brands, 35% by the top-4 Chinese brands (Huawei, ZTE, Lenovo,

Coolpad), and 29% by the whitebox and second-tier Chinese brands. The key shift was

enabled by a substantially lowered entry barrier due to higher quality chipset and

reference designs and better availability of components (panels, touch, image sensors,

mobile DRAM).

Based on improving affordability and quality, we expect the total China smartphone market

to grow from 197 mn units in 2012E to 421 mn in 2015E, with global tier one brands

accounting for 30%, top Chinese brands 33%, and other brands and whitebox suppliers

0

20,000

40,000

60,000

80,000

100,000

1Q

08

2Q

08

3Q

08

4Q

08

1Q

09

2Q

09

3Q

09

4Q

09

1Q

10

2Q

10

3Q

10

4Q

10

1Q

11

2Q

11

3Q

11

4Q

11

1Q

12

2Q

12

3Q

12

4Q

12E

1Q

13E

2Q

13E

3Q

13E

4Q

13E

Units (000)

Nokia Research in Motion Motorola

Apple Sony Ericsson / Sony Mobile HTC

Samsung LG Huawei + ZTE

Chinese / Others

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12 4Q12

Chinese brands Chinese brand global share

(mn units) 2011 2012E 2013E 2014E 2015E 2011-15E CAGR

Huawei 20 30 45 60 72 138%

ZTE 11 27 40 55 66 158%

Lenovo 2 23 35 45 54 239%

Coolpad 6 19 30 40 48 168%

Gionee 0 15 20 25 30 562%

Oppo 0 7 12 15 20 1189%

TCL/Alcatel 1 6 12 15 20 194%

Hisense 0 4 9 10 12 278%

Xiaomi 0 4 8 10 12 236%

Tianyu 0 10 12 10 12 230%

G-Five 2 3 5 10 12 157%

Bird 1 5 8 10 12 221%

BBK 0 5 8 10 12 495%

Branded China builts 43 158 243 315 382 172%

Others (white-brands) 30 92 211 316 441 195%

China built smartphones 73 250 454 631 823 183%

Growth (YoY) 241% 81% 39% 30%

Within the China market,

domestic Chinese brands

are ramping up faster than

overseas Tier one brands

Smartphones now 38% of

units shipped in China

06 March 2013

Sunny Optical Technology Group Co., Limited (2382.HK / 2382 HK) 9

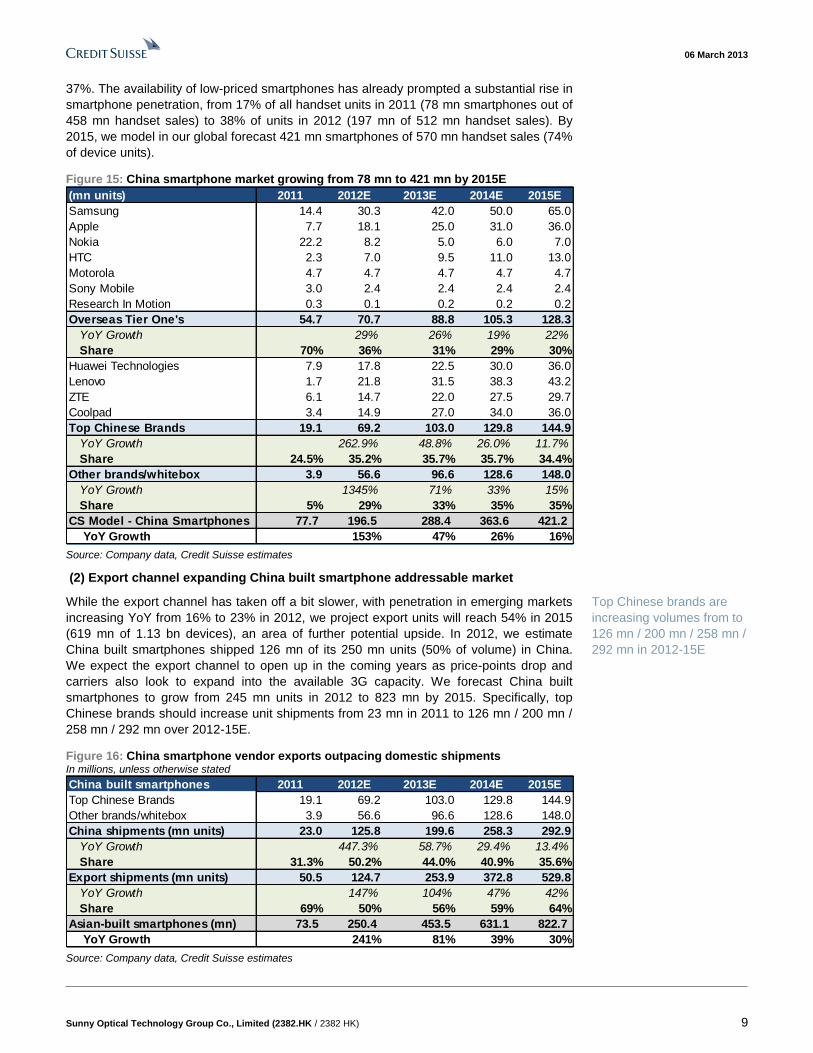

37%. The availability of low-priced smartphones has already prompted a substantial rise in

smartphone penetration, from 17% of all handset units in 2011 (78 mn smartphones out of

458 mn handset sales) to 38% of units in 2012 (197 mn of 512 mn handset sales). By

2015, we model in our global forecast 421 mn smartphones of 570 mn handset sales (74%

of device units).

Figure 15: China smartphone market growing from 78 mn to 421 mn by 2015E

Source: Company data, Credit Suisse estimates

(2) Export channel expanding China built smartphone addressable market

While the export channel has taken off a bit slower, with penetration in emerging markets

increasing YoY from 16% to 23% in 2012, we project export units will reach 54% in 2015

(619 mn of 1.13 bn devices), an area of further potential upside. In 2012, we estimate

China built smartphones shipped 126 mn of its 250 mn units (50% of volume) in China.

We expect the export channel to open up in the coming years as price-points drop and

carriers also look to expand into the available 3G capacity. We forecast China built

smartphones to grow from 245 mn units in 2012 to 823 mn by 2015. Specifically, top

Chinese brands should increase unit shipments from 23 mn in 2011 to 126 mn / 200 mn /

258 mn / 292 mn over 2012-15E.

Figure 16: China smartphone vendor exports outpacing domestic shipments In millions, unless otherwise stated

Source: Company data, Credit Suisse estimates

(mn units) 2011 2012E 2013E 2014E 2015E

Samsung 14.4 30.3 42.0 50.0 65.0

Apple 7.7 18.1 25.0 31.0 36.0

Nokia 22.2 8.2 5.0 6.0 7.0

HTC 2.3 7.0 9.5 11.0 13.0

Motorola 4.7 4.7 4.7 4.7 4.7

Sony Mobile 3.0 2.4 2.4 2.4 2.4

Research In Motion 0.3 0.1 0.2 0.2 0.2

Overseas Tier One's 54.7 70.7 88.8 105.3 128.3

YoY Growth 29% 26% 19% 22%

Share 70% 36% 31% 29% 30%

Huawei Technologies 7.9 17.8 22.5 30.0 36.0

Lenovo 1.7 21.8 31.5 38.3 43.2

ZTE 6.1 14.7 22.0 27.5 29.7

Coolpad 3.4 14.9 27.0 34.0 36.0

Top Chinese Brands 19.1 69.2 103.0 129.8 144.9

YoY Growth 262.9% 48.8% 26.0% 11.7%

Share 24.5% 35.2% 35.7% 35.7% 34.4%

Other brands/whitebox 3.9 56.6 96.6 128.6 148.0

YoY Growth 1345% 71% 33% 15%

Share 5% 29% 33% 35% 35%

CS Model - China Smartphones 77.7 196.5 288.4 363.6 421.2

YoY Growth 153% 47% 26% 16%

China built smartphones 2011 2012E 2013E 2014E 2015E

Top Chinese Brands 19.1 69.2 103.0 129.8 144.9

Other brands/whitebox 3.9 56.6 96.6 128.6 148.0

China shipments (mn units) 23.0 125.8 199.6 258.3 292.9

YoY Growth 447.3% 58.7% 29.4% 13.4%

Share 31.3% 50.2% 44.0% 40.9% 35.6%

Export shipments (mn units) 50.5 124.7 253.9 372.8 529.8

YoY Growth 147% 104% 47% 42%

Share 69% 50% 56% 59% 64%

Asian-built smartphones (mn) 73.5 250.4 453.5 631.1 822.7

YoY Growth 241% 81% 39% 30%

Top Chinese brands are

increasing volumes from to

126 mn / 200 mn / 258 mn /

292 mn in 2012-15E

06 March 2013

Sunny Optical Technology Group Co., Limited (2382.HK / 2382 HK) 10

A small player in a large global market …..

Globally, Sunny Optical plays in the camera module supply chain with unit shipments of

about 2.16 bn in 2012, according to industry estimates. Based on Sunny Optical’s camera

module unit shipment of 97 mn in 2012 and our estimated 2012E camera modules

revenue of Rmb2.3 bn, Sunny Optical has ~4% global market share. According to Yole

Development, the US$9.3 bn camera module market in 2012 comprises the ~US$6.6 bn

CMOS image sensor (CIS) market and the camera module assembly and test value chain

of about US$2.7 bn. Given the higher value add and greater technology innovation, CMOS

image sensor industry is about 70% of the entire supply chain. The CMOS image sensor

market is made up of: (1) design value chain of ~US$2.0 bn (including overhead and

SG&A), (2) the front-end manufacturing supply chain of about US$3.0 bn, (3) optical layer

market of US$400 mn and (4) back-end packaging value chain of about US$1.2 bn. The

~US$2.7 bn camera module assembly and testing supply chain consists of: (1) ~US$1.4

bn optical component market of lenses and IF filters, (2) auto-focus component industry of

the size of US$460 mn, and (3) module assembly and test market of ~US$900 mn.

Migration to higher-resolution cameras is driving market growth. While most of the gain on

higher content value pertains to CIS vendors from design innovations, camera module

assembly and testing companies also benefit as: (1) CIS costs are generally passed

through to the customers and (2) higher resolution camera modules require more complex

and precise assembly and testing.

Figure 17: CIS and camera module value chain—US$6.6 bn + US$2.7 bn = US$9.3 bn market

Source: Yole, Credit Suisse

…. and a fragmented supply chain …..

Taking a closer look, the $9.3 bn camera module value chain with over 2 bn unit

shipments is fragmented and has no dominant player. The market is fragmented as no

single player has a broad share of technologies, competencies and IP. The supply chain is

complex with numerous business models and vertical integration is limited. The top four

players in the US$6.6 bn CIS market, namely Omnivision, Samsung, Sony, and Aptina,

accounted for 78% of 2012 volume. The camera module assembly market is even more

fragmented—no vendor shipped more than 11% of the total volumes in 2012.

US$9.3 bn camera

module market

US$6.6 bn CMOS

image sensor market

US$2.7 bn camera

assembly market

Sunny Optical is a small

player with 4% share in a

US$9.3 bn market with unit

shipments of 2.16 bn

Camera resolution upgrades

benefit assembly companies

as well

Sunny Optical is a smaller

player in a fragmented

supply chain with limited

vertical integration

06 March 2013

Sunny Optical Technology Group Co., Limited (2382.HK / 2382 HK) 11

Figure 18: CMOS image sensor volume share—top-4

vendors dominating nearly 80% of 2012 volume of 2.16 bn

Figure 19: The fragmented camera module market of 2.16

bn units, with no vendors having >11% share in 2012

Source: TSR, Company data, Credit Suisse estimates Source: TSR, Tessera, Credit Suisse estimates

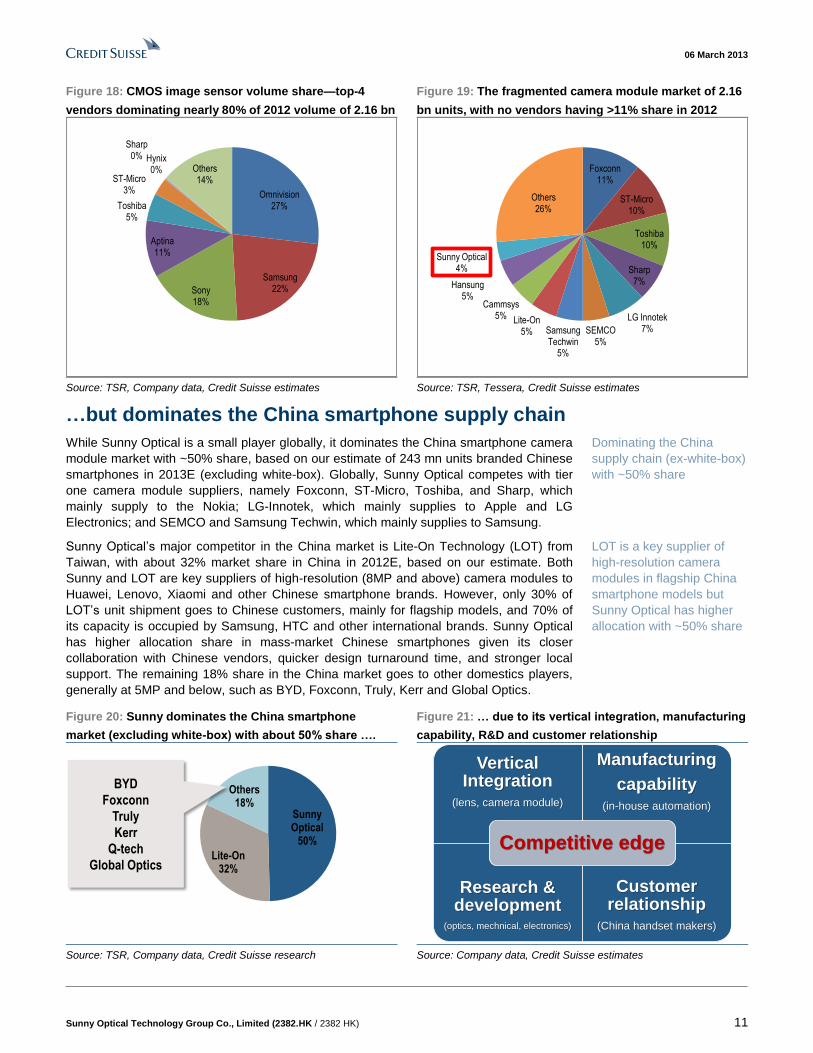

…but dominates the China smartphone supply chain

While Sunny Optical is a small player globally, it dominates the China smartphone camera

module market with ~50% share, based on our estimate of 243 mn units branded Chinese

smartphones in 2013E (excluding white-box). Globally, Sunny Optical competes with tier

one camera module suppliers, namely Foxconn, ST-Micro, Toshiba, and Sharp, which

mainly supply to the Nokia; LG-Innotek, which mainly supplies to Apple and LG

Electronics; and SEMCO and Samsung Techwin, which mainly supplies to Samsung.

Sunny Optical’s major competitor in the China market is Lite-On Technology (LOT) from

Taiwan, with about 32% market share in China in 2012E, based on our estimate. Both

Sunny and LOT are key suppliers of high-resolution (8MP and above) camera modules to

Huawei, Lenovo, Xiaomi and other Chinese smartphone brands. However, only 30% of

LOT’s unit shipment goes to Chinese customers, mainly for flagship models, and 70% of

its capacity is occupied by Samsung, HTC and other international brands. Sunny Optical

has higher allocation share in mass-market Chinese smartphones given its closer

collaboration with Chinese vendors, quicker design turnaround time, and stronger local

support. The remaining 18% share in the China market goes to other domestics players,

generally at 5MP and below, such as BYD, Foxconn, Truly, Kerr and Global Optics.

Figure 20: Sunny dominates the China smartphone

market (excluding white-box) with about 50% share ….

Figure 21: … due to its vertical integration, manufacturing

capability, R&D and customer relationship

Source: TSR, Company data, Credit Suisse research Source: Company data, Credit Suisse estimates

Omnivision27%

Samsung22%Sony

18%

Aptina11%

Toshiba5%

ST-Micro3%

Sharp0% Hynix

0% Others14%

Foxconn11%

ST-Micro10%

Toshiba10%

Sharp7%

LG Innotek7%SEMCO

5%Samsung Techwin

5%

Lite-On5%

Cammsys5%

Hansung5%

Sunny Optical4%

Others26%

Sunny Optical

50%

Lite-On32%

Others18%

BYD

Foxconn

Truly

Kerr

Q-tech

Global Optics

Vertical Integration

(lens, camera module)

Manufacturing

capability(in-house automation)

Research & development

(optics, mechnical, electronics)

Customer relationship

(China handset makers)

Competitive edge

Dominating the China

supply chain (ex-white-box)

with ~50% share

LOT is a key supplier of

high-resolution camera

modules in flagship China

smartphone models but

Sunny Optical has higher

allocation with ~50% share

06 March 2013

Sunny Optical Technology Group Co., Limited (2382.HK / 2382 HK) 12

Competitive edges strengthening market position

Competition in the camera module space in the China handset supply chain is increasing

with several new entrants, such as Kerr, O-Film and Truly, starting to ship 5MP cameras in

2013. Nevertheless, Sunny Optical has multiple competitive advantages that allow it to

stay above competition. Strong links with key CIS/VCM/lens suppliers, advanced

autofocus lens design and manufacturing capabilities, better scale and vertical integration

(in-house lens and camera module production capability) and strong relationship with top-

tier Chinese handset makers are key factors allowing Sunny Optical to remain a dominant

camera module supplier in the China smartphone supply chain, in our view.

(1) Vertical integration: Better scale, margins and efficiencies

Sunny Optical has better economies of scale in handset cameras versus its domestic

rivals, due to its capacity and vertical integration. It is one of the few companies in the

industry that possesses vertically integrated capability and deep know-how in optics (29

years in optics), electro-mechanical engineering and image processing. With in-house

module assembly and auto-focus lens set production capability, the company is able to

provide a total one-stop solution to its handset customers at a competitive price.

Sunny Optical’s handset camera gross margin is slightly higher than its peers who have to

source lenses externally. While most of its 3MP and below camera modules are equipped

with in-house lenses, Sunny Optical sources most of its high-resolution (>5MP) lenses

from Largan and Kantatsu in 2012. Per our checks, the company adopts voice coil motors

(VCM, for auto-focus) mainly from TDK and Mitsumi. To improve its cost structure, the

company plans to increase lens insourcing for high-resolution (5MP and above) camera

modules in 2013 and adopt VCM from domestic suppliers for its lower end products.

(2) Design manufacturing: Fast responsiveness and in-house automation stand out

Sunny Optical offers products with fast design response, optimised performance and

better cost balance to its cost sensitive and demanding Chinese handset customers. Most

importantly, it has in-house automation production capability, including automatic testers

and automatic painting machines. Its key production technologies include automation for

production and inspection for lens sets, plastic injection moulding technology with narrow

runway for handset lenses, mass production for glass aspherical lenses with several

cavities per mould. Its advanced COB technologies allow production of high-resolution

(>5MP) camera modules in a miniaturised form factor.

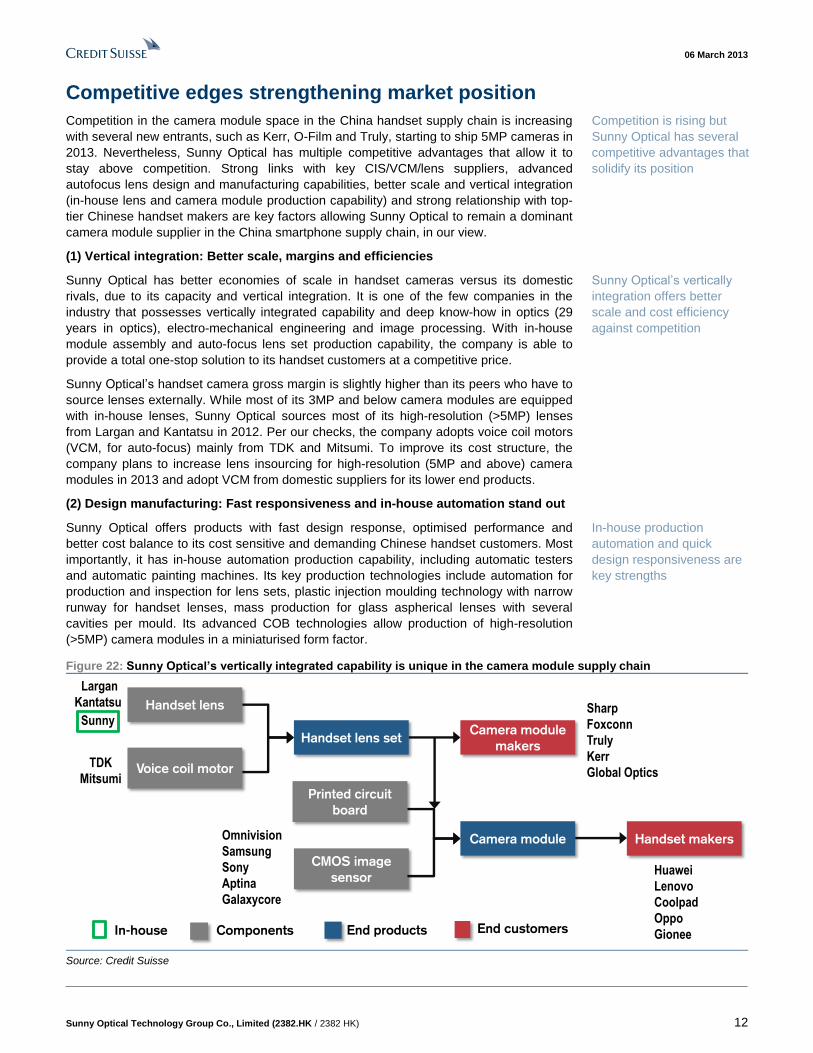

Figure 22: Sunny Optical’s vertically integrated capability is unique in the camera module supply chain

Source: Credit Suisse

Handset lens

Voice coil motor

Largan

Kantatsu

TDK

Mitsumi

Handset lens setCamera module

makers

CMOS image

sensor

Omnivision

Samsung

Sony

Aptina

Galaxycore

Printed circuit

board

Camera module Handset makers

Huawei

Lenovo

Coolpad

Oppo

Gionee

Sharp

Foxconn

Truly

Kerr

Global Optics

End productsComponents End customers

Sunny

In-house

Competition is rising but

Sunny Optical has several

competitive advantages that

solidify its position

Sunny Optical’s vertically

integration offers better

scale and cost efficiency

against competition

In-house production

automation and quick

design responsiveness are

key strengths

06 March 2013

Sunny Optical Technology Group Co., Limited (2382.HK / 2382 HK) 13

(3) Research and development: Nudging the entry barrier up

The ongoing camera resolution migration in smartphones and Sunny’s R&D focus on high-

resolution camera lens / modules and specialty cameras set it apart from rivals. R&D in

the areas of optics, electronics and software image processing allowed the company to

ramp up 8MP/13MP handset cameras ahead of its domestic rivals who are still at

5MP/8MP. This was a result of its extensive R&D partnership with Pantech that made the

company a qualified supplier of 8MP/13MP handset cameras in 2011/12.

The company has developed and obtained patents for ultra-wide-angle high resolution

vehicle lenses. Sunny Optical also has extensive R&D in various infrared lens sets for

vehicle and security surveillance applications. The company successfully started the mass

production of smart TV video camera modules for Samsung in 2012. It also completed

R&D for a number of microscopic systems, analytical instruments oriented for

spectrophotometers, gas chromatographs and mass spectrometers and high-end

measuring machines. The company is developing new technologies, including array

cameras (see page 31 for details on this technology) and 3D gesture recognition cameras.

(4) Solid customer relationship: Stickier business relationships

Sunny Optical has a clear advantage given its close proximity with Chinese customers and

long-term partnerships with key domestic handset makers. By entering into the supply

chain of TCL handset business segment in 2009-10, Sunny Optical established a close

relationship with a number of fast-growing branded Chinese customers such as Huawei,

Lenovo, Coolpad. As these customers grow their market shares, Sunny Optical further

strengthened its business relationship by offering cost-sensitive, high-performance

handset camera modules that differentiate from their global competitors. On top of its

success in China, Sunny Optical is expanding its presence to top-tier international

customers with meaningful production ramp-up potentially starting in 2H13.

Figure 23: Sunny Optical—Porter's five forces analysis shows mild competitive threats

Factors Forces Analysis

Bargaining power with

suppliers

Medium Scale advantage, diversified supplier base, ability to pass through cost

Top five suppliers account for about 33% of total purchase (11.1% by the largest supplier). Raw

materials form ~75% of COGS; CIS and VCM are the main components which account for 60-70%

within that. Nevertheless, CIS and VCM are pass-through costs. The company has scale advantage

given its sheer volumes and in-house automation.

Bargaining power with

customers

Medium Low customer concentration and high cost efficiency offsetting pricing pressure

While handset vendors are likely to assert pricing pressure on component suppliers, Sunny's ability to

offer cost-effective high-end products is a key differentiation. Customer concentration is low: the top

five customers accounted for only 38% of sales, the largest customer contributed 11.5% in 1H12.

Threat of new entrants Mid-to-Low New entrants emerging in 5MP but maintains leadership in 8MP/13MP

Domestic new entrants such as Kerr, O-Film, Truly and Q-Tech are ramping up on 5MP camera

modules for mass market smartphones. Nevertheless, Sunny Optical retains its leading position in

higher resolution as China smartphone vendors migrate mid-to-high end models towards 8MP/13MP

cameras. This forms a high entry barrier as Sunny Optical has better yields and technology leadership.

Threat of substitute

products

Mid-to-Low Immature technology limiting substitution threat

While substitutes are emerging, such as wafer level optics (WLO) and liquid lens, new technologies

are still running at low yields and are limited to low-resolution front-facing cameras.

Competitive rivalry

within the industry

Medium Competitive rivalry is mild given the fragmented value chain

Sunny is dominant supplier in the China camera module supply chain with strong relationship with

Tier-1 smartphone vendors: Huawei, Coolpad, Lenovo and ZTE. The company is also reaching

international customers in markets such as vehicle lens and tablets.

Source: Company data, Credit Suisse research

Strong R&D and pixel

migration allowing the

company to stay ahead of

competition

Diversifying into others

specialty optical products

Clear advantage given close

partnerships with key

domestic handset makers…

…and also overseas

customer penetration in

2013

06 March 2013

Sunny Optical Technology Group Co., Limited (2382.HK / 2382 HK) 14

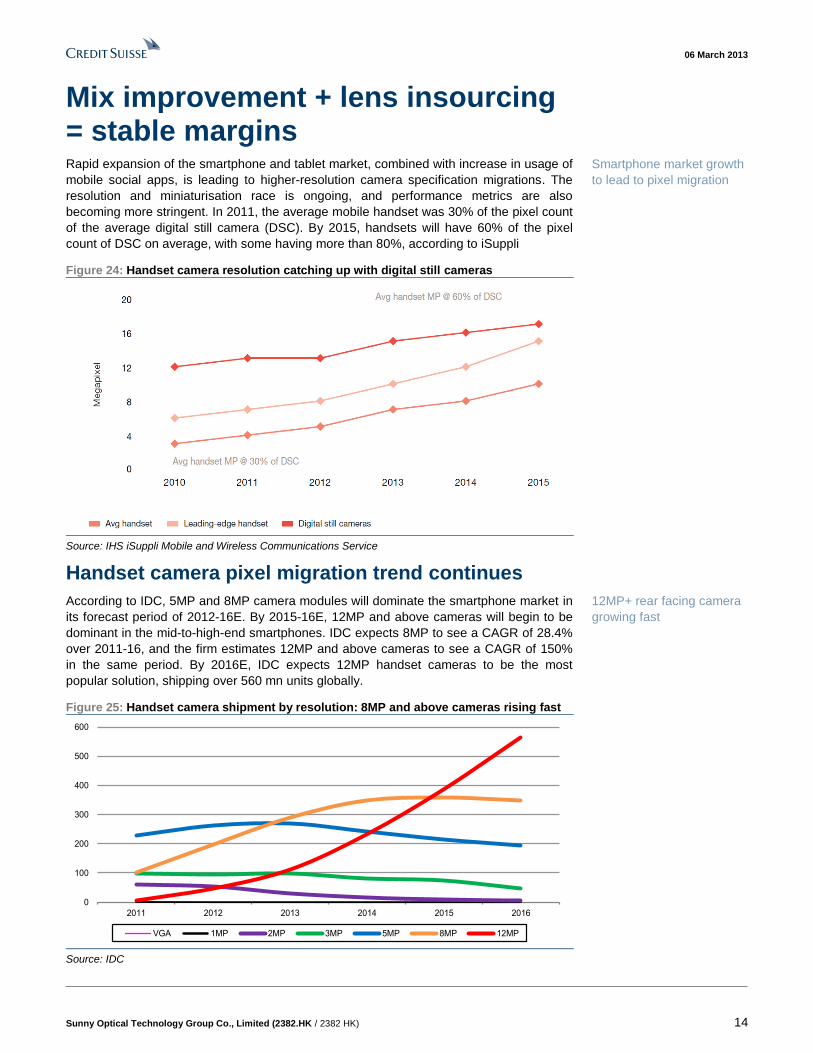

Mix improvement + lens insourcing = stable margins Rapid expansion of the smartphone and tablet market, combined with increase in usage of

mobile social apps, is leading to higher-resolution camera specification migrations. The

resolution and miniaturisation race is ongoing, and performance metrics are also

becoming more stringent. In 2011, the average mobile handset was 30% of the pixel count

of the average digital still camera (DSC). By 2015, handsets will have 60% of the pixel

count of DSC on average, with some having more than 80%, according to iSuppli

Figure 24: Handset camera resolution catching up with digital still cameras

Source: IHS iSuppli Mobile and Wireless Communications Service

Handset camera pixel migration trend continues

According to IDC, 5MP and 8MP camera modules will dominate the smartphone market in

its forecast period of 2012-16E. By 2015-16E, 12MP and above cameras will begin to be

dominant in the mid-to-high-end smartphones. IDC expects 8MP to see a CAGR of 28.4%

over 2011-16, and the firm estimates 12MP and above cameras to see a CAGR of 150%

in the same period. By 2016E, IDC expects 12MP handset cameras to be the most

popular solution, shipping over 560 mn units globally.

Figure 25: Handset camera shipment by resolution: 8MP and above cameras rising fast

Source: IDC

0

100

200

300

400

500

600

2011 2012 2013 2014 2015 2016

VGA 1MP 2MP 3MP 5MP 8MP 12MP

Smartphone market growth

to lead to pixel migration

12MP+ rear facing camera

growing fast

06 March 2013

Sunny Optical Technology Group Co., Limited (2382.HK / 2382 HK) 15

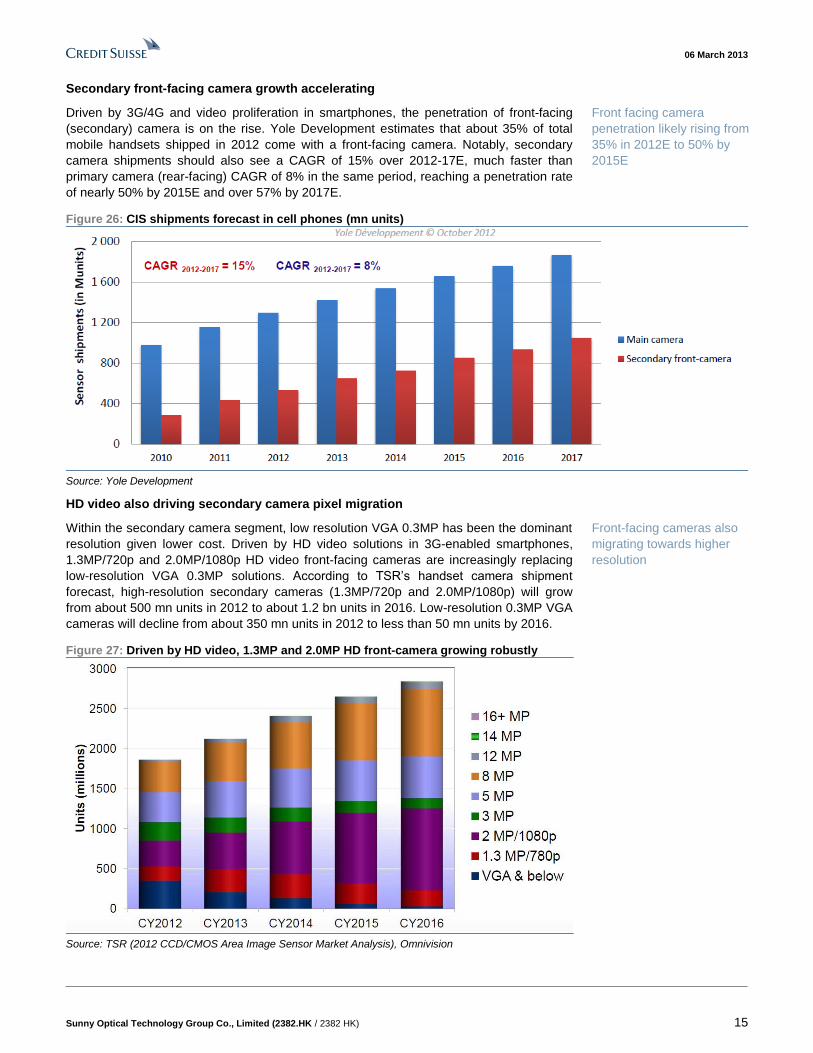

Secondary front-facing camera growth accelerating

Driven by 3G/4G and video proliferation in smartphones, the penetration of front-facing

(secondary) camera is on the rise. Yole Development estimates that about 35% of total

mobile handsets shipped in 2012 come with a front-facing camera. Notably, secondary

camera shipments should also see a CAGR of 15% over 2012-17E, much faster than

primary camera (rear-facing) CAGR of 8% in the same period, reaching a penetration rate

of nearly 50% by 2015E and over 57% by 2017E.

Figure 26: CIS shipments forecast in cell phones (mn units)

Source: Yole Development

HD video also driving secondary camera pixel migration

Within the secondary camera segment, low resolution VGA 0.3MP has been the dominant

resolution given lower cost. Driven by HD video solutions in 3G-enabled smartphones,

1.3MP/720p and 2.0MP/1080p HD video front-facing cameras are increasingly replacing

low-resolution VGA 0.3MP solutions. According to TSR’s handset camera shipment

forecast, high-resolution secondary cameras (1.3MP/720p and 2.0MP/1080p) will grow

from about 500 mn units in 2012 to about 1.2 bn units in 2016. Low-resolution 0.3MP VGA

cameras will decline from about 350 mn units in 2012 to less than 50 mn units by 2016.

Figure 27: Driven by HD video, 1.3MP and 2.0MP HD front-camera growing robustly

Source: TSR (2012 CCD/CMOS Area Image Sensor Market Analysis), Omnivision

Front facing camera

penetration likely rising from

35% in 2012E to 50% by

2015E

Front-facing cameras also

migrating towards higher

resolution

06 March 2013

Sunny Optical Technology Group Co., Limited (2382.HK / 2382 HK) 16

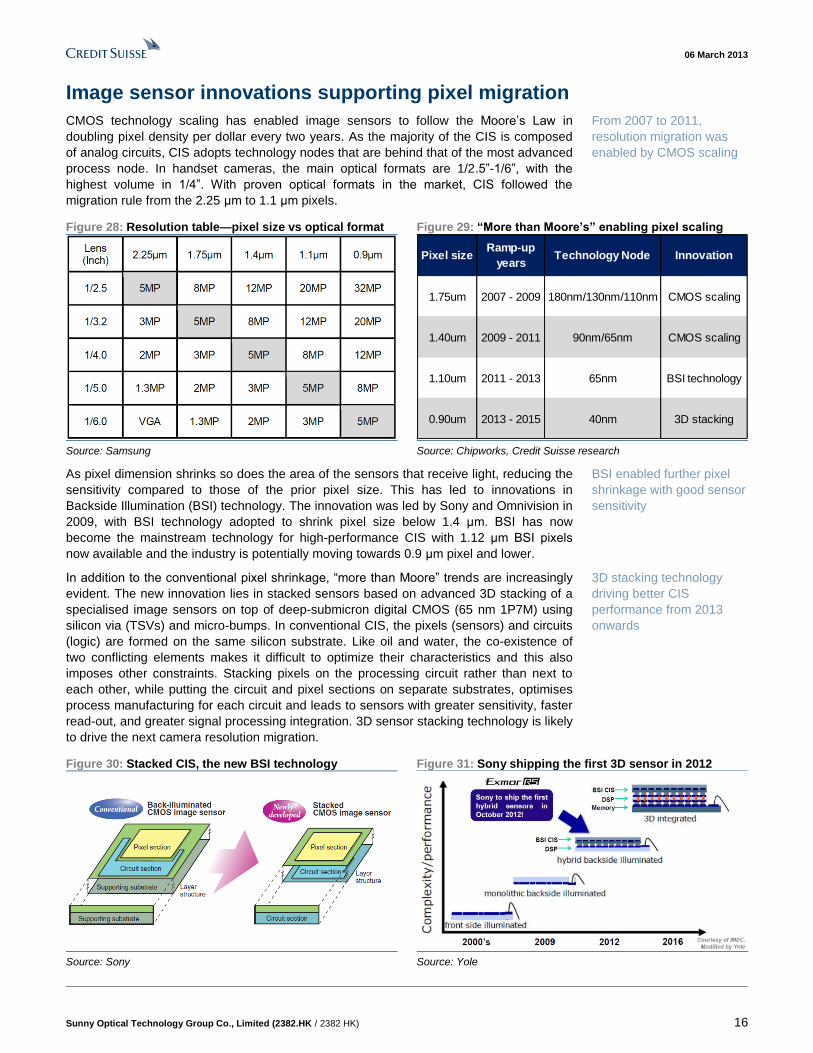

Image sensor innovations supporting pixel migration

CMOS technology scaling has enabled image sensors to follow the Moore’s Law in

doubling pixel density per dollar every two years. As the majority of the CIS is composed

of analog circuits, CIS adopts technology nodes that are behind that of the most advanced

process node. In handset cameras, the main optical formats are 1/2.5”-1/6”, with the

highest volume in 1/4”. With proven optical formats in the market, CIS followed the

migration rule from the 2.25 μm to 1.1 μm pixels.

Figure 28: Resolution table—pixel size vs optical format Figure 29: “More than Moore’s” enabling pixel scaling

Source: Samsung Source: Chipworks, Credit Suisse research

As pixel dimension shrinks so does the area of the sensors that receive light, reducing the

sensitivity compared to those of the prior pixel size. This has led to innovations in

Backside Illumination (BSI) technology. The innovation was led by Sony and Omnivision in

2009, with BSI technology adopted to shrink pixel size below 1.4 μm. BSI has now

become the mainstream technology for high-performance CIS with 1.12 μm BSI pixels

now available and the industry is potentially moving towards 0.9 μm pixel and lower.

In addition to the conventional pixel shrinkage, “more than Moore” trends are increasingly

evident. The new innovation lies in stacked sensors based on advanced 3D stacking of a

specialised image sensors on top of deep-submicron digital CMOS (65 nm 1P7M) using

silicon via (TSVs) and micro-bumps. In conventional CIS, the pixels (sensors) and circuits

(logic) are formed on the same silicon substrate. Like oil and water, the co-existence of

two conflicting elements makes it difficult to optimize their characteristics and this also

imposes other constraints. Stacking pixels on the processing circuit rather than next to

each other, while putting the circuit and pixel sections on separate substrates, optimises

process manufacturing for each circuit and leads to sensors with greater sensitivity, faster

read-out, and greater signal processing integration. 3D sensor stacking technology is likely

to drive the next camera resolution migration.

Figure 30: Stacked CIS, the new BSI technology Figure 31: Sony shipping the first 3D sensor in 2012

Source: Sony Source: Yole

Pixel sizeRamp-up

yearsTechnology Node Innovation

1.75um 2007 - 2009 180nm/130nm/110nm CMOS scaling

1.40um 2009 - 2011 90nm/65nm CMOS scaling

1.10um 2011 - 2013 65nm BSI technology

0.90um 2013 - 2015 40nm 3D stacking

From 2007 to 2011,

resolution migration was

enabled by CMOS scaling

BSI enabled further pixel

shrinkage with good sensor

sensitivity

3D stacking technology

driving better CIS

performance from 2013

onwards

06 March 2013

Sunny Optical Technology Group Co., Limited (2382.HK / 2382 HK) 17

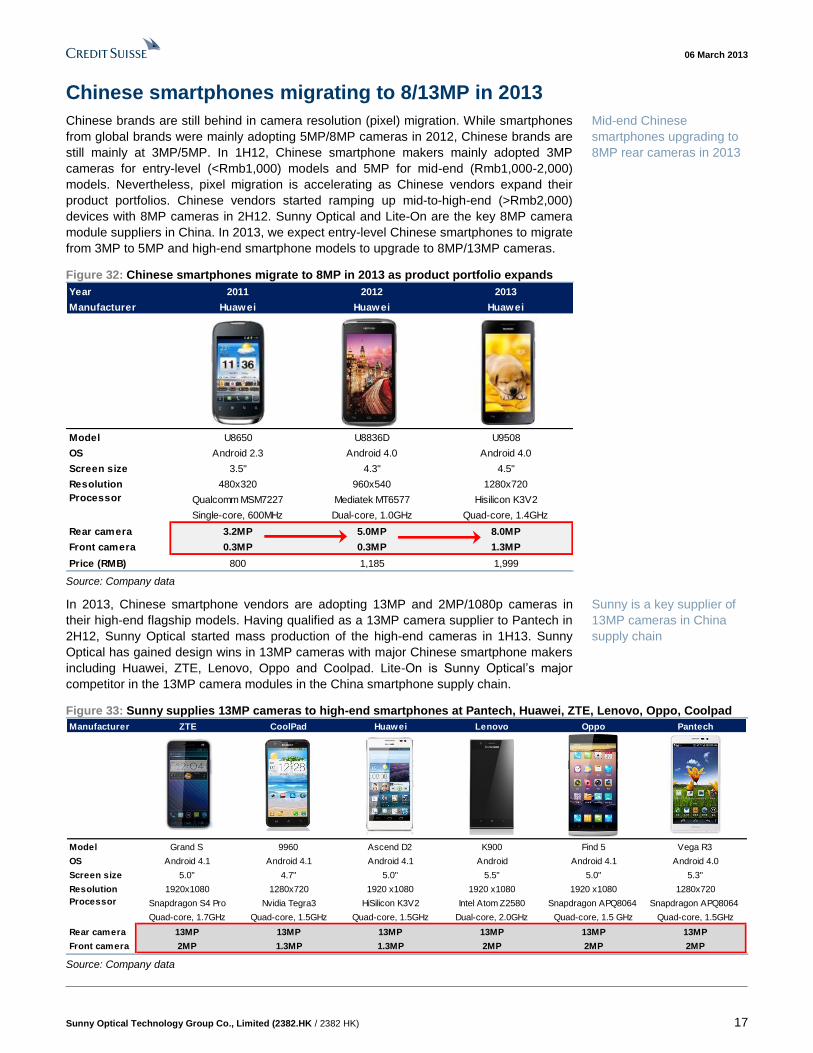

Chinese smartphones migrating to 8/13MP in 2013

Chinese brands are still behind in camera resolution (pixel) migration. While smartphones

from global brands were mainly adopting 5MP/8MP cameras in 2012, Chinese brands are

still mainly at 3MP/5MP. In 1H12, Chinese smartphone makers mainly adopted 3MP

cameras for entry-level (<Rmb1,000) models and 5MP for mid-end (Rmb1,000-2,000)

models. Nevertheless, pixel migration is accelerating as Chinese vendors expand their

product portfolios. Chinese vendors started ramping up mid-to-high-end (>Rmb2,000)

devices with 8MP cameras in 2H12. Sunny Optical and Lite-On are the key 8MP camera

module suppliers in China. In 2013, we expect entry-level Chinese smartphones to migrate

from 3MP to 5MP and high-end smartphone models to upgrade to 8MP/13MP cameras.

Figure 32: Chinese smartphones migrate to 8MP in 2013 as product portfolio expands

Source: Company data

In 2013, Chinese smartphone vendors are adopting 13MP and 2MP/1080p cameras in

their high-end flagship models. Having qualified as a 13MP camera supplier to Pantech in

2H12, Sunny Optical started mass production of the high-end cameras in 1H13. Sunny

Optical has gained design wins in 13MP cameras with major Chinese smartphone makers

including Huawei, ZTE, Lenovo, Oppo and Coolpad. Lite-On is Sunny Optical’s major

competitor in the 13MP camera modules in the China smartphone supply chain.

Figure 33: Sunny supplies 13MP cameras to high-end smartphones at Pantech, Huawei, ZTE, Lenovo, Oppo, Coolpad

Source: Company data

Year 2011 2012 2013

Manufacturer Huawei Huawei Huawei

Model U8650 U8836D U9508

OS Android 2.3 Android 4.0 Android 4.0

Screen size 3.5" 4.3" 4.5"

Resolution 480x320 960x540 1280x720

Qualcomm MSM7227 Mediatek MT6577 Hisilicon K3V2

Single-core, 600MHz Dual-core, 1.0GHz Quad-core, 1.4GHz

Rear camera 3.2MP 5.0MP 8.0MP

Front camera 0.3MP 0.3MP 1.3MP

Price (RMB) 800 1,185 1,999

Processor

Manufacturer ZTE CoolPad Huawei Lenovo Oppo Pantech

Model Grand S 9960 Ascend D2 K900 Find 5 Vega R3

OS Android 4.1 Android 4.1 Android 4.1 Android Android 4.1 Android 4.0

Screen size 5.0" 4.7" 5.0" 5.5" 5.0" 5.3"

Resolution 1920x1080 1280x720 1920 x1080 1920 x1080 1920 x1080 1280x720

Snapdragon S4 Pro Nvidia Tegra3 HiSilicon K3V2 Intel Atom Z2580 Snapdragon APQ8064 Snapdragon APQ8064

Quad-core, 1.7GHz Quad-core, 1.5GHz Quad-core, 1.5GHz Dual-core, 2.0GHz Quad-core, 1.5 GHz Quad-core, 1.5GHz

Rear camera 13MP 13MP 13MP 13MP 13MP 13MP

Front camera 2MP 1.3MP 1.3MP 2MP 2MP 2MP

Processor

Mid-end Chinese

smartphones upgrading to

8MP rear cameras in 2013

Sunny is a key supplier of

13MP cameras in China

supply chain

06 March 2013

Sunny Optical Technology Group Co., Limited (2382.HK / 2382 HK) 18

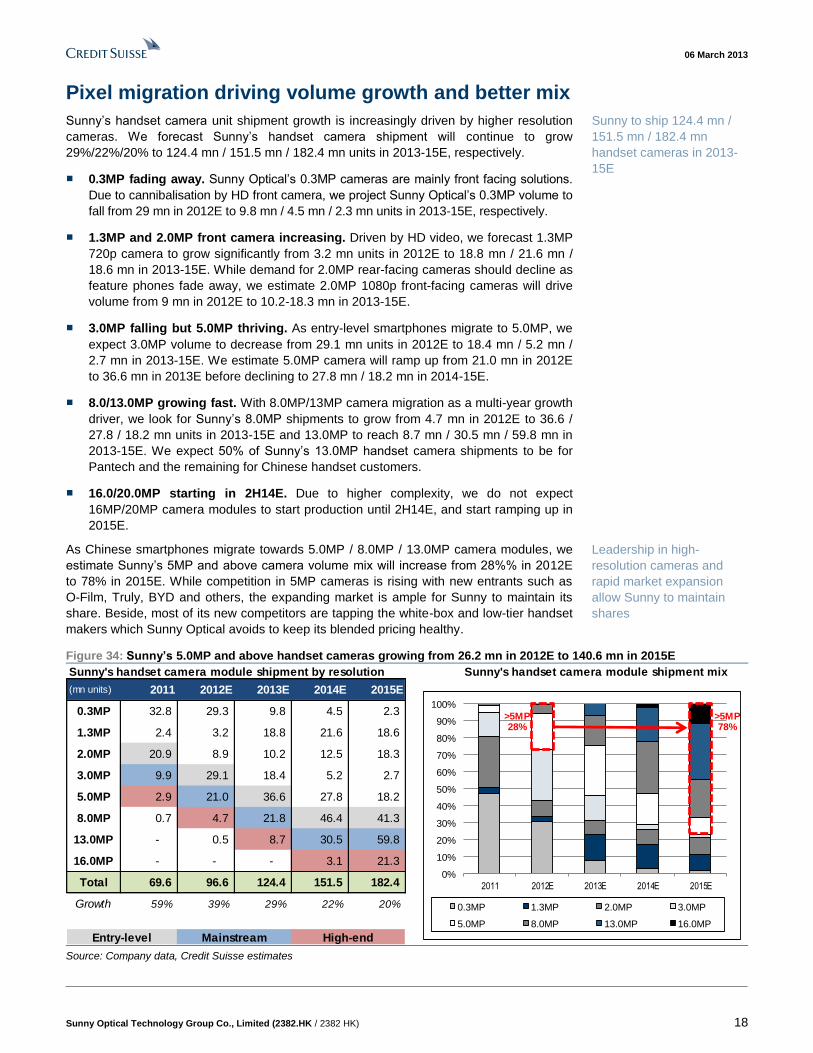

Pixel migration driving volume growth and better mix

Sunny’s handset camera unit shipment growth is increasingly driven by higher resolution

cameras. We forecast Sunny’s handset camera shipment will continue to grow

29%/22%/20% to 124.4 mn / 151.5 mn / 182.4 mn units in 2013-15E, respectively.

■ 0.3MP fading away. Sunny Optical’s 0.3MP cameras are mainly front facing solutions.

Due to cannibalisation by HD front camera, we project Sunny Optical’s 0.3MP volume to

fall from 29 mn in 2012E to 9.8 mn / 4.5 mn / 2.3 mn units in 2013-15E, respectively.

■ 1.3MP and 2.0MP front camera increasing. Driven by HD video, we forecast 1.3MP

720p camera to grow significantly from 3.2 mn units in 2012E to 18.8 mn / 21.6 mn /

18.6 mn in 2013-15E. While demand for 2.0MP rear-facing cameras should decline as

feature phones fade away, we estimate 2.0MP 1080p front-facing cameras will drive

volume from 9 mn in 2012E to 10.2-18.3 mn in 2013-15E.

■ 3.0MP falling but 5.0MP thriving. As entry-level smartphones migrate to 5.0MP, we

expect 3.0MP volume to decrease from 29.1 mn units in 2012E to 18.4 mn / 5.2 mn /

2.7 mn in 2013-15E. We estimate 5.0MP camera will ramp up from 21.0 mn in 2012E

to 36.6 mn in 2013E before declining to 27.8 mn / 18.2 mn in 2014-15E.

■ 8.0/13.0MP growing fast. With 8.0MP/13MP camera migration as a multi-year growth

driver, we look for Sunny’s 8.0MP shipments to grow from 4.7 mn in 2012E to 36.6 /

27.8 / 18.2 mn units in 2013-15E and 13.0MP to reach 8.7 mn / 30.5 mn / 59.8 mn in

2013-15E. We expect 50% of Sunny’s 13.0MP handset camera shipments to be for

Pantech and the remaining for Chinese handset customers.

■ 16.0/20.0MP starting in 2H14E. Due to higher complexity, we do not expect

16MP/20MP camera modules to start production until 2H14E, and start ramping up in

2015E.

As Chinese smartphones migrate towards 5.0MP / 8.0MP / 13.0MP camera modules, we

estimate Sunny’s 5MP and above camera volume mix will increase from 28%% in 2012E

to 78% in 2015E. While competition in 5MP cameras is rising with new entrants such as

O-Film, Truly, BYD and others, the expanding market is ample for Sunny to maintain its

share. Beside, most of its new competitors are tapping the white-box and low-tier handset

makers which Sunny Optical avoids to keep its blended pricing healthy.

Figure 34: Sunny’s 5.0MP and above handset cameras growing from 26.2 mn in 2012E to 140.6 mn in 2015E

Source: Company data, Credit Suisse estimates

Sunny's handset camera module shipment by resolution Sunny's handset camera module shipment mix

(mn units) 2011 2012E 2013E 2014E 2015E

0.3MP 32.8 29.3 9.8 4.5 2.3

1.3MP 2.4 3.2 18.8 21.6 18.6

2.0MP 20.9 8.9 10.2 12.5 18.3

3.0MP 9.9 29.1 18.4 5.2 2.7

5.0MP 2.9 21.0 36.6 27.8 18.2

8.0MP 0.7 4.7 21.8 46.4 41.3

13.0MP - 0.5 8.7 30.5 59.8

16.0MP - - - 3.1 21.3

Total 69.6 96.6 124.4 151.5 182.4

Growth 59% 39% 29% 22% 20%

Entry-level Mainstream High-end

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2011 2012E 2013E 2014E 2015E

0.3MP 1.3MP 2.0MP 3.0MP

5.0MP 8.0MP 13.0MP 16.0MP

>5MP28%

>5MP78%

Sunny to ship 124.4 mn /

151.5 mn / 182.4 mn

handset cameras in 2013-

15E

Leadership in high-

resolution cameras and

rapid market expansion

allow Sunny to maintain

shares

06 March 2013

Sunny Optical Technology Group Co., Limited (2382.HK / 2382 HK) 19

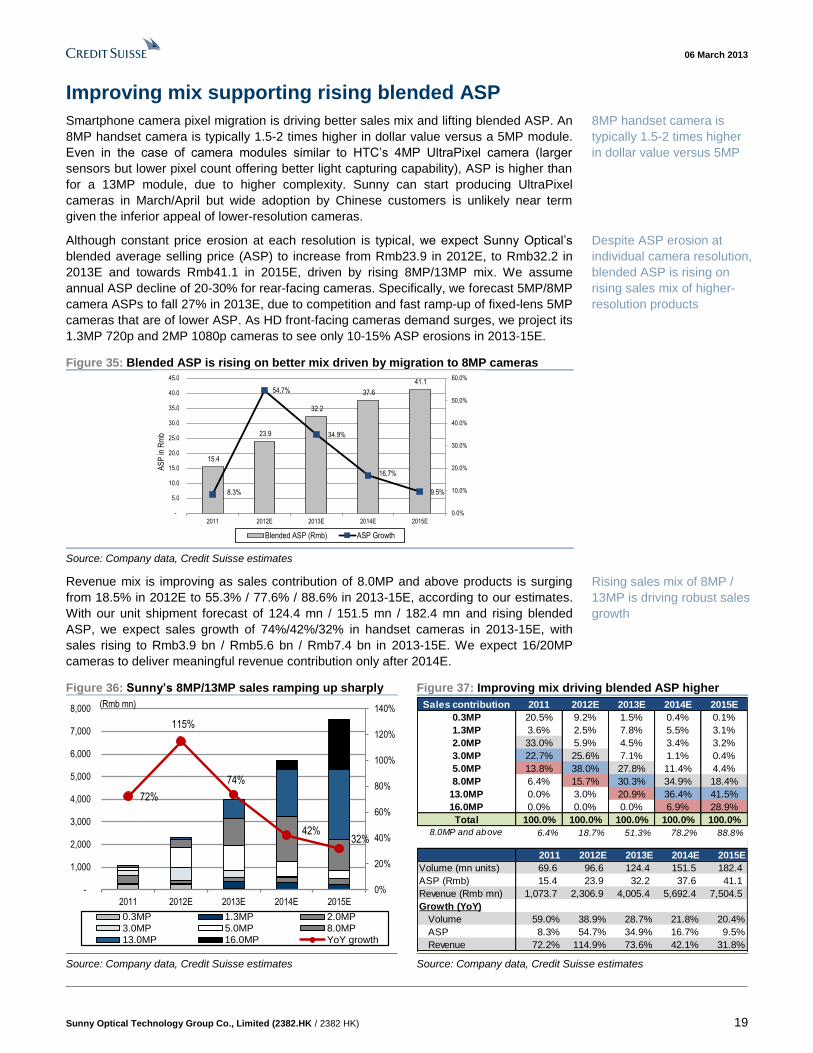

Improving mix supporting rising blended ASP

Smartphone camera pixel migration is driving better sales mix and lifting blended ASP. An

8MP handset camera is typically 1.5-2 times higher in dollar value versus a 5MP module.

Even in the case of camera modules similar to HTC’s 4MP UltraPixel camera (larger

sensors but lower pixel count offering better light capturing capability), ASP is higher than

for a 13MP module, due to higher complexity. Sunny can start producing UltraPixel

cameras in March/April but wide adoption by Chinese customers is unlikely near term

given the inferior appeal of lower-resolution cameras.

Although constant price erosion at each resolution is typical, we expect Sunny Optical’s

blended average selling price (ASP) to increase from Rmb23.9 in 2012E, to Rmb32.2 in

2013E and towards Rmb41.1 in 2015E, driven by rising 8MP/13MP mix. We assume

annual ASP decline of 20-30% for rear-facing cameras. Specifically, we forecast 5MP/8MP

camera ASPs to fall 27% in 2013E, due to competition and fast ramp-up of fixed-lens 5MP

cameras that are of lower ASP. As HD front-facing cameras demand surges, we project its

1.3MP 720p and 2MP 1080p cameras to see only 10-15% ASP erosions in 2013-15E.

Figure 35: Blended ASP is rising on better mix driven by migration to 8MP cameras

Source: Company data, Credit Suisse estimates

Revenue mix is improving as sales contribution of 8.0MP and above products is surging

from 18.5% in 2012E to 55.3% / 77.6% / 88.6% in 2013-15E, according to our estimates.

With our unit shipment forecast of 124.4 mn / 151.5 mn / 182.4 mn and rising blended

ASP, we expect sales growth of 74%/42%/32% in handset cameras in 2013-15E, with

sales rising to Rmb3.9 bn / Rmb5.6 bn / Rmb7.4 bn in 2013-15E. We expect 16/20MP

cameras to deliver meaningful revenue contribution only after 2014E.

Figure 36: Sunny’s 8MP/13MP sales ramping up sharply Figure 37: Improving mix driving blended ASP higher

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

15.4

23.9

32.2

37.6

41.1

8.3%

54.7%

34.9%

16.7%

9.5%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

-

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

2011 2012E 2013E 2014E 2015E

AS

P in

Rm

b

Blended ASP (Rmb) ASP Growth

72%

115%

74%

42%32%

0%

20%

40%

60%

80%

100%

120%

140%

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

2011 2012E 2013E 2014E 2015E

(Rmb mn)

0.3MP 1.3MP 2.0MP3.0MP 5.0MP 8.0MP13.0MP 16.0MP YoY growth

Sales contribution 2011 2012E 2013E 2014E 2015E

0.3MP 20.5% 9.2% 1.5% 0.4% 0.1%

1.3MP 3.6% 2.5% 7.8% 5.5% 3.1%

2.0MP 33.0% 5.9% 4.5% 3.4% 3.2%

3.0MP 22.7% 25.6% 7.1% 1.1% 0.4%

5.0MP 13.8% 38.0% 27.8% 11.4% 4.4%

8.0MP 6.4% 15.7% 30.3% 34.9% 18.4%

13.0MP 0.0% 3.0% 20.9% 36.4% 41.5%

16.0MP 0.0% 0.0% 0.0% 6.9% 28.9%

Total 100.0% 100.0% 100.0% 100.0% 100.0%

8.0MP and above 6.4% 18.7% 51.3% 78.2% 88.8%

2011 2012E 2013E 2014E 2015E

Volume (mn units) 69.6 96.6 124.4 151.5 182.4

ASP (Rmb) 15.4 23.9 32.2 37.6 41.1

Revenue (Rmb mn) 1,073.7 2,306.9 4,005.4 5,692.4 7,504.5

Growth (YoY)

Volume 59.0% 38.9% 28.7% 21.8% 20.4%

ASP 8.3% 54.7% 34.9% 16.7% 9.5%

Revenue 72.2% 114.9% 73.6% 42.1% 31.8%

8MP handset camera is

typically 1.5-2 times higher

in dollar value versus 5MP

Despite ASP erosion at

individual camera resolution,

blended ASP is rising on

rising sales mix of higher-

resolution products

Rising sales mix of 8MP /

13MP is driving robust sales

growth

06 March 2013

Sunny Optical Technology Group Co., Limited (2382.HK / 2382 HK) 20

Largan saw similar growth due to pixel migration

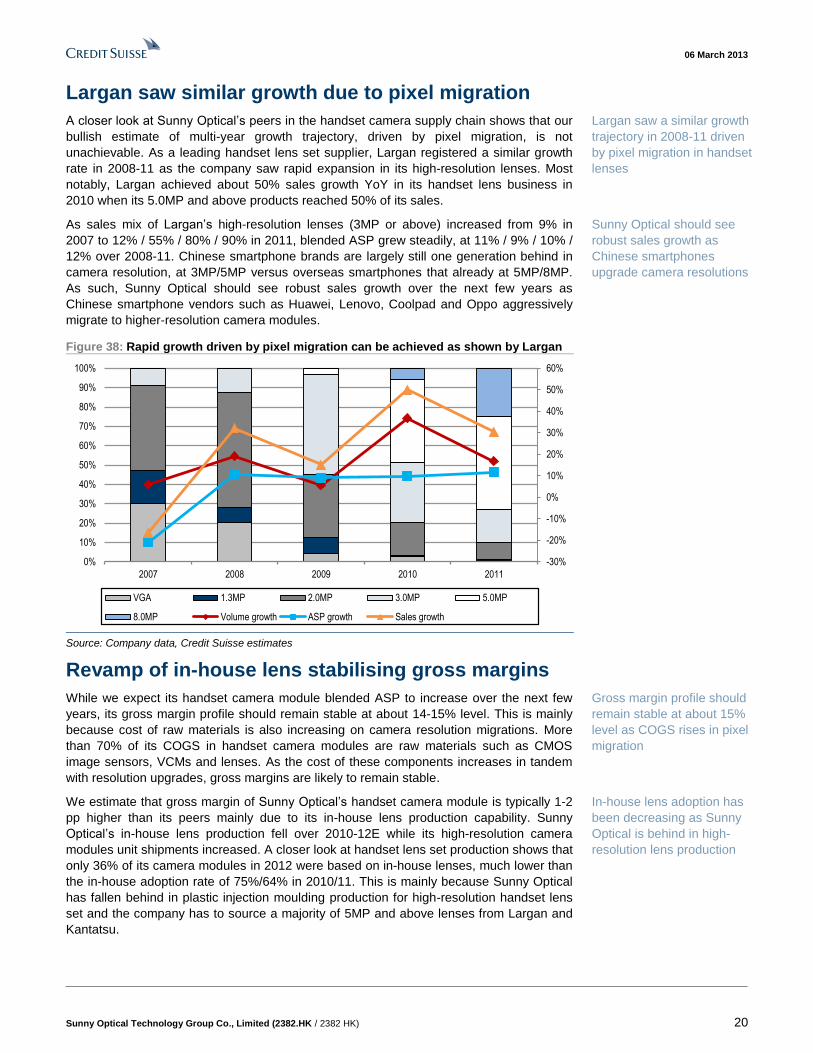

A closer look at Sunny Optical’s peers in the handset camera supply chain shows that our

bullish estimate of multi-year growth trajectory, driven by pixel migration, is not

unachievable. As a leading handset lens set supplier, Largan registered a similar growth

rate in 2008-11 as the company saw rapid expansion in its high-resolution lenses. Most

notably, Largan achieved about 50% sales growth YoY in its handset lens business in

2010 when its 5.0MP and above products reached 50% of its sales.

As sales mix of Largan’s high-resolution lenses (3MP or above) increased from 9% in

2007 to 12% / 55% / 80% / 90% in 2011, blended ASP grew steadily, at 11% / 9% / 10% /

12% over 2008-11. Chinese smartphone brands are largely still one generation behind in

camera resolution, at 3MP/5MP versus overseas smartphones that already at 5MP/8MP.

As such, Sunny Optical should see robust sales growth over the next few years as

Chinese smartphone vendors such as Huawei, Lenovo, Coolpad and Oppo aggressively

migrate to higher-resolution camera modules.

Figure 38: Rapid growth driven by pixel migration can be achieved as shown by Largan

Source: Company data, Credit Suisse estimates

Revamp of in-house lens stabilising gross margins

While we expect its handset camera module blended ASP to increase over the next few

years, its gross margin profile should remain stable at about 14-15% level. This is mainly

because cost of raw materials is also increasing on camera resolution migrations. More

than 70% of its COGS in handset camera modules are raw materials such as CMOS

image sensors, VCMs and lenses. As the cost of these components increases in tandem

with resolution upgrades, gross margins are likely to remain stable.

We estimate that gross margin of Sunny Optical’s handset camera module is typically 1-2

pp higher than its peers mainly due to its in-house lens production capability. Sunny

Optical’s in-house lens production fell over 2010-12E while its high-resolution camera

modules unit shipments increased. A closer look at handset lens set production shows that

only 36% of its camera modules in 2012 were based on in-house lenses, much lower than

the in-house adoption rate of 75%/64% in 2010/11. This is mainly because Sunny Optical

has fallen behind in plastic injection moulding production for high-resolution handset lens

set and the company has to source a majority of 5MP and above lenses from Largan and

Kantatsu.

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2007 2008 2009 2010 2011

VGA 1.3MP 2.0MP 3.0MP 5.0MP

8.0MP Volume growth ASP growth Sales growth

Largan saw a similar growth

trajectory in 2008-11 driven

by pixel migration in handset

lenses

Sunny Optical should see

robust sales growth as

Chinese smartphones

upgrade camera resolutions

Gross margin profile should

remain stable at about 15%

level as COGS rises in pixel

migration

In-house lens adoption has

been decreasing as Sunny

Optical is behind in high-

resolution lens production

06 March 2013

Sunny Optical Technology Group Co., Limited (2382.HK / 2382 HK) 21

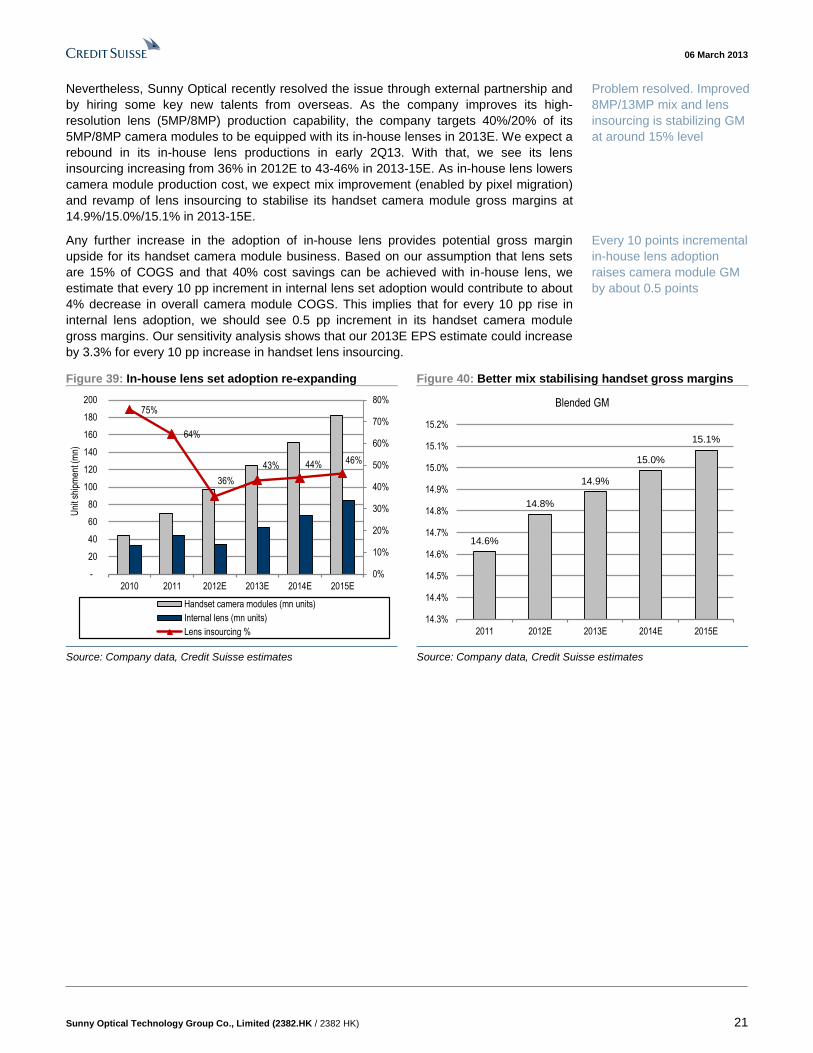

Nevertheless, Sunny Optical recently resolved the issue through external partnership and

by hiring some key new talents from overseas. As the company improves its high-

resolution lens (5MP/8MP) production capability, the company targets 40%/20% of its

5MP/8MP camera modules to be equipped with its in-house lenses in 2013E. We expect a

rebound in its in-house lens productions in early 2Q13. With that, we see its lens

insourcing increasing from 36% in 2012E to 43-46% in 2013-15E. As in-house lens lowers

camera module production cost, we expect mix improvement (enabled by pixel migration)

and revamp of lens insourcing to stabilise its handset camera module gross margins at

14.9%/15.0%/15.1% in 2013-15E.

Any further increase in the adoption of in-house lens provides potential gross margin

upside for its handset camera module business. Based on our assumption that lens sets

are 15% of COGS and that 40% cost savings can be achieved with in-house lens, we

estimate that every 10 pp increment in internal lens set adoption would contribute to about

4% decrease in overall camera module COGS. This implies that for every 10 pp rise in

internal lens adoption, we should see 0.5 pp increment in its handset camera module

gross margins. Our sensitivity analysis shows that our 2013E EPS estimate could increase

by 3.3% for every 10 pp increase in handset lens insourcing.

Figure 39: In-house lens set adoption re-expanding Figure 40: Better mix stabilising handset gross margins

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

75%

64%

36%

43% 44% 46%

0%

10%

20%

30%

40%

50%

60%

70%

80%

-

20

40

60

80

100

120

140

160

180

200

2010 2011 2012E 2013E 2014E 2015E

Uni

t shi

pmen

t (m

n)

Handset camera modules (mn units)

Internal lens (mn units)

Lens insourcing %

14.6%

14.8%

14.9%

15.0%

15.1%

14.3%

14.4%

14.5%

14.6%

14.7%

14.8%

14.9%

15.0%

15.1%

15.2%

2011 2012E 2013E 2014E 2015E

Blended GM

Problem resolved. Improved

8MP/13MP mix and lens

insourcing is stabilizing GM

at around 15% level

Every 10 points incremental

in-house lens adoption

raises camera module GM

by about 0.5 points

06 March 2013

Sunny Optical Technology Group Co., Limited (2382.HK / 2382 HK) 22

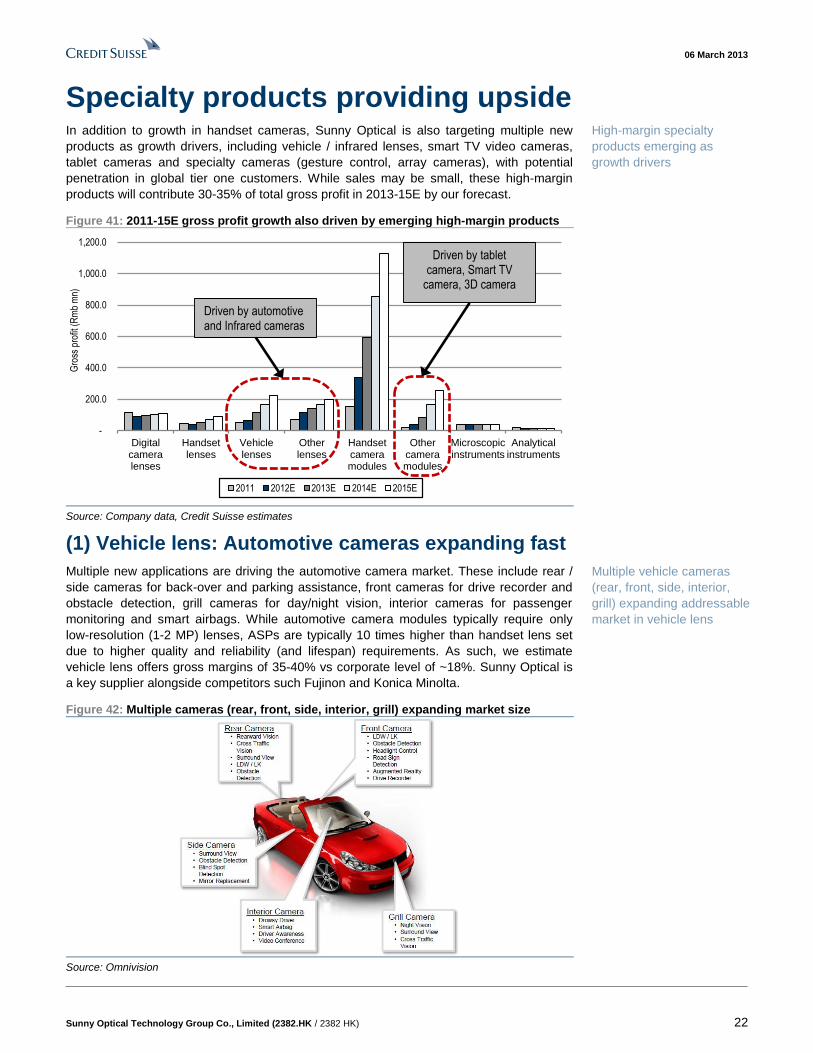

Specialty products providing upside In addition to growth in handset cameras, Sunny Optical is also targeting multiple new

products as growth drivers, including vehicle / infrared lenses, smart TV video cameras,

tablet cameras and specialty cameras (gesture control, array cameras), with potential

penetration in global tier one customers. While sales may be small, these high-margin

products will contribute 30-35% of total gross profit in 2013-15E by our forecast.

Figure 41: 2011-15E gross profit growth also driven by emerging high-margin products

Source: Company data, Credit Suisse estimates

(1) Vehicle lens: Automotive cameras expanding fast

Multiple new applications are driving the automotive camera market. These include rear /

side cameras for back-over and parking assistance, front cameras for drive recorder and

obstacle detection, grill cameras for day/night vision, interior cameras for passenger

monitoring and smart airbags. While automotive camera modules typically require only

low-resolution (1-2 MP) lenses, ASPs are typically 10 times higher than handset lens set

due to higher quality and reliability (and lifespan) requirements. As such, we estimate

vehicle lens offers gross margins of 35-40% vs corporate level of ~18%. Sunny Optical is

a key supplier alongside competitors such Fujinon and Konica Minolta.

Figure 42: Multiple cameras (rear, front, side, interior, grill) expanding market size

Source: Omnivision

-

200.0

400.0

600.0

800.0

1,000.0

1,200.0

Digitalcameralenses

Handsetlenses

Vehiclelenses

Otherlenses

Handsetcameramodules

Othercameramodules

Microscopicinstruments

Analyticalinstruments

Gro

ss p

rofit

(R

mb

mn)

2011 2012E 2013E 2014E 2015E

Driven by automotive and Infrared cameras

Driven by tablet camera, Smart TV

camera, 3D camera

High-margin specialty

products emerging as

growth drivers

Multiple vehicle cameras

(rear, front, side, interior,

grill) expanding addressable

market in vehicle lens

06 March 2013

Sunny Optical Technology Group Co., Limited (2382.HK / 2382 HK) 23

As the global market of automotive cameras expands from 17 mn units in 2012E to 48 mn

in 2015E, we expect Sunny Optical’s vehicle lens set volume to increase from about 4.4

mn units in 2012E to 7.7 mn / 11.9 mn / 16.6 mn units in 2013-15E. Orders from European

automotive camera makers, such as Continental, and Japanese automobile makers are

likely key volume growth drivers. This implies Sunny Optical’s market share could ramp up

rapidly from 26% in 2012E to about 30%/33%/35% in 2013-15E. We estimate a CAGR of

48% in Sunny Optical’s vehicle lens revenue over 2012-15E.

Figure 43: Sunny’s vehicle lens unit shipment increasing

to 16.6 mn as its unit market share rises to 35% by 2015E

Figure 44: Sales likely to see 48% CAGR and gross profit

contribution rising from 9% in 2012E to 12% in 2015E

Source: Omnivision, TSR 2011, Credit Suisse estimates Source: Company data, Credit Suisse estimates

(2) Infrared lens: A long-tail growth opportunity

An infrared camera is a thermal system that converts IR radiation into a visible image. The

main components of an IR camera include camera core, IR lenses and detectors—UFPA

(Uncooled Focal Plane Arrays) IR sensors. Due to high reliability requirements, we

estimate that Sunny Optical’s IR lens business offers gross margin of about 50%, the

highest among all product segments.

Figure 45: Main parts of an IR camera include camera core and detectors

Source: Yole Development

Infrared spectrum ranges from NIR to LWIR wavelengths. Each IR spectrum provides

different information and targets different market segments. LWIR (Long Wave IR) or FIR

(Far IR) is adopted for thermography and passive vision enhancement (as it does not

require light sources). NIR (Near IR) enables active vision enhancement (such as for

gesture control or night vision). SWIR (Short Wave IR) and MWIR (Medium Wave IR)

target active vision enhancement and material analysis. Initially developed by US defence

companies for the military market, LWIR uncooled camera is now the largest and fasting

growing market in the overall IR camera business and are increasingly emerging in

commercial applications, especially in automotive and video surveillance.

12.9%

18.3%

25.8%

29.7%

33.4%34.6%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

-

10.0

20.0

30.0

40.0

50.0

60.0

2010 2011 2012E 2013E 2014E 2015E

Uni

t shi

pmen

ts (

mn)

Global automotive camera unit shipment (mn)

Sunny unit shipment (mn)

Sunny market share

5%

10%

9%

10%11%

11%

0%

2%

4%

6%

8%

10%

12%

-

100.0

200.0

300.0

400.0

500.0

600.0

2010 2011 2012E 2013E 2014E 2015E

Sal

es (

Rm

b m

n)

Sunny vehicle lens sales (Rmb mn)

as % of total gross profit

Sunny’s high-margin vehicle

lens business could see a

48% CAGR over the next

three years

LWIR uncooled camera is

the hottest market segment

06 March 2013

Sunny Optical Technology Group Co., Limited (2382.HK / 2382 HK) 24

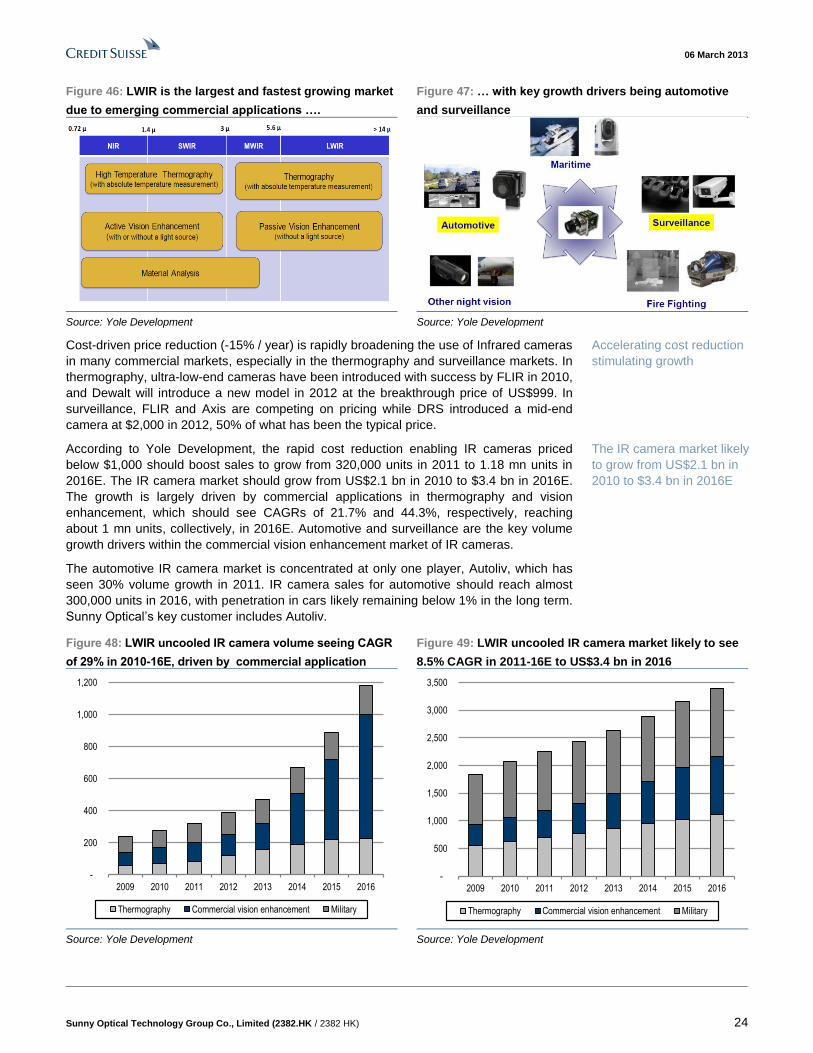

Figure 46: LWIR is the largest and fastest growing market

due to emerging commercial applications ….

Figure 47: … with key growth drivers being automotive

and surveillance

Source: Yole Development Source: Yole Development

Cost-driven price reduction (-15% / year) is rapidly broadening the use of Infrared cameras

in many commercial markets, especially in the thermography and surveillance markets. In

thermography, ultra-low-end cameras have been introduced with success by FLIR in 2010,

and Dewalt will introduce a new model in 2012 at the breakthrough price of US$999. In

surveillance, FLIR and Axis are competing on pricing while DRS introduced a mid-end

camera at $2,000 in 2012, 50% of what has been the typical price.