Successful Technology LicensingChapter III: Key Terms Cluster 3: Financial Terms

Cluster 4: Technology Growth and Development

• Value: Total value of the licensed IP in context of the other key terms; and

• Form of payment: How the payments will be made.

• Value: Total value of the licensed IP in context of the other key terms; and

• Form of payment: How the payments will be made.

Cluster 3: Financial Terms in License Agreements

• What is IP Valuation?

• Benefit

• Risk

Valuation: The process of identifying and measuring financial benefit and risk from an asset.

When is IP Valuation Used?

• Merger and acquisition

• IP audit

• Financial reporting

• Financing

• Investment transactions

• Licensing

How does IP Valuation Work?

The Three Classic Methods

• Income– value over time discounted for

• risk• time value of money

• Market comparables– Competing technology

• Cost of alternatives– Invent around– Law suit

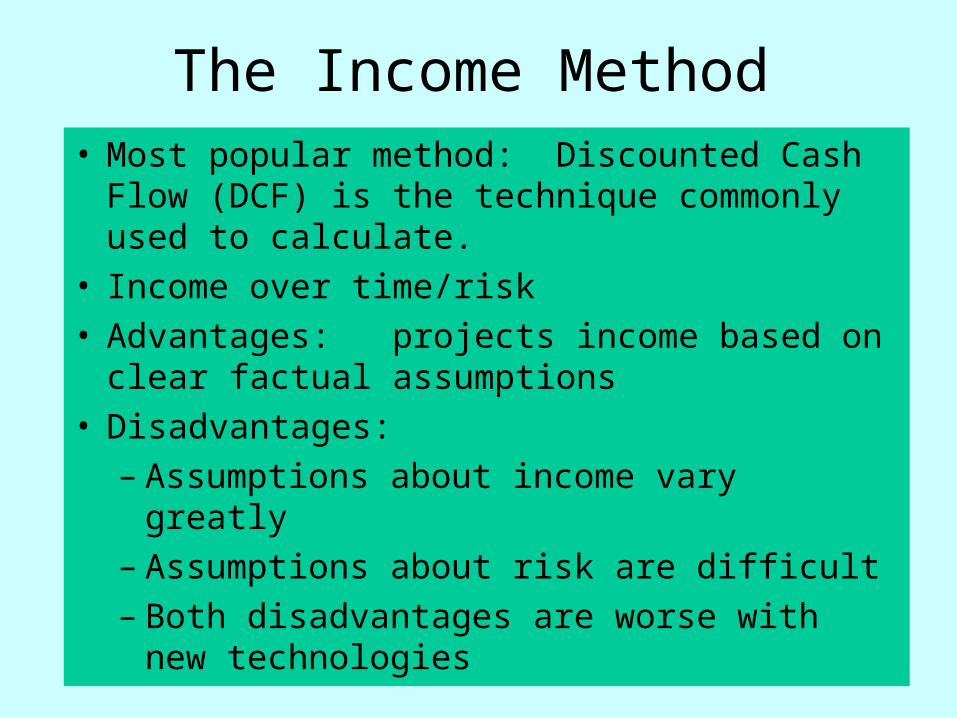

The Income Method• Most popular method: Discounted Cash Flow

(DCF) is the technique commonly used to calculate.

• Income over time/risk• Advantages: projects income based on clear

factual assumptions • Disadvantages:

– Assumptions about income vary greatly– Assumptions about risk are difficult– Both disadvantages are worse with new

technologies

DCF Basic Approach

• Determine projected cash flow over time

• Determine time value of money

• Determine risk that projected cash flow will not be achieved

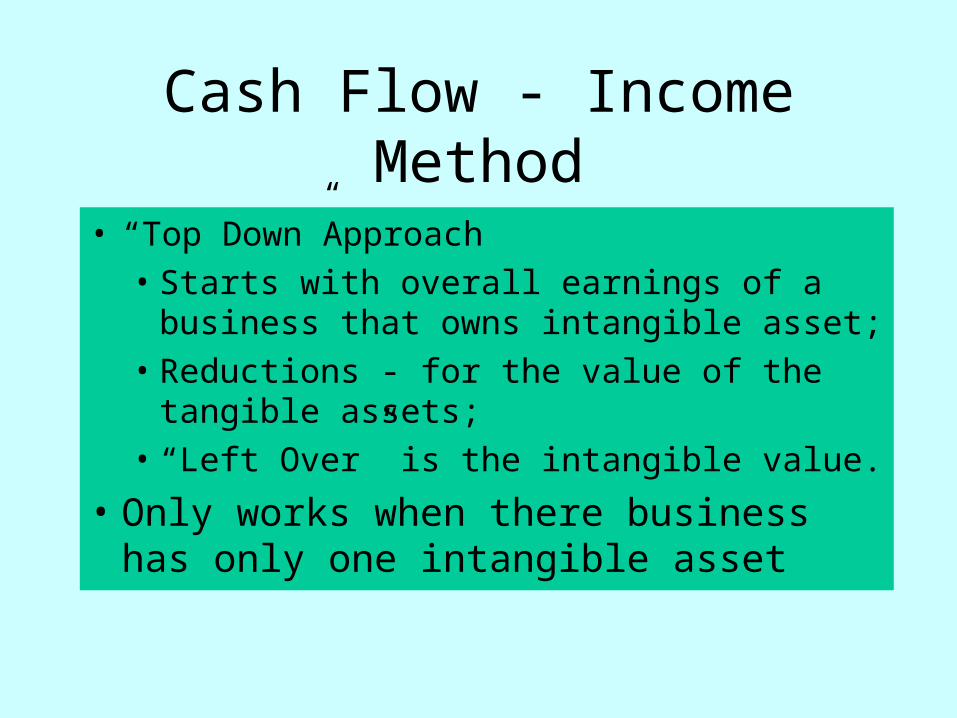

Cash Flow - Income Method

• “Top Down”Approach• Starts with overall earnings of a business that

owns intangible asset;• Reductions - for the value of the tangible assets;• “Left Over” is the intangible value.

• Only works when there business has only one intangible asset

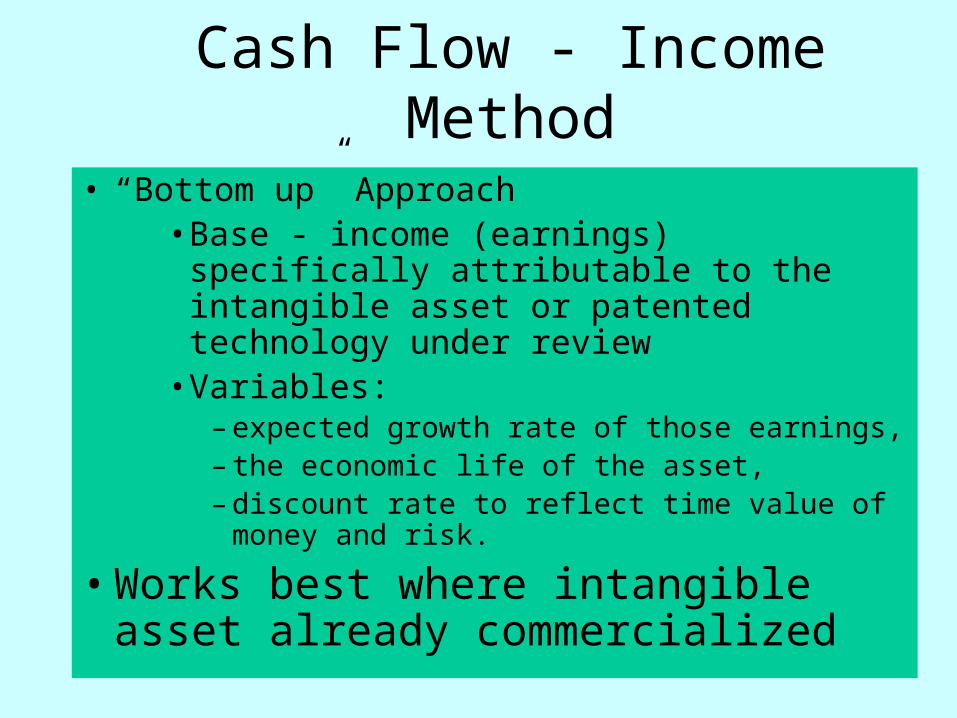

Cash Flow - Income Method

• “Bottom up” Approach• Base - income (earnings) specifically

attributable to the intangible asset or patented technology under review

• Variables:– expected growth rate of those earnings, – the economic life of the asset, – discount rate to reflect time value of money and

risk.

• Works best where intangible asset already commercialized

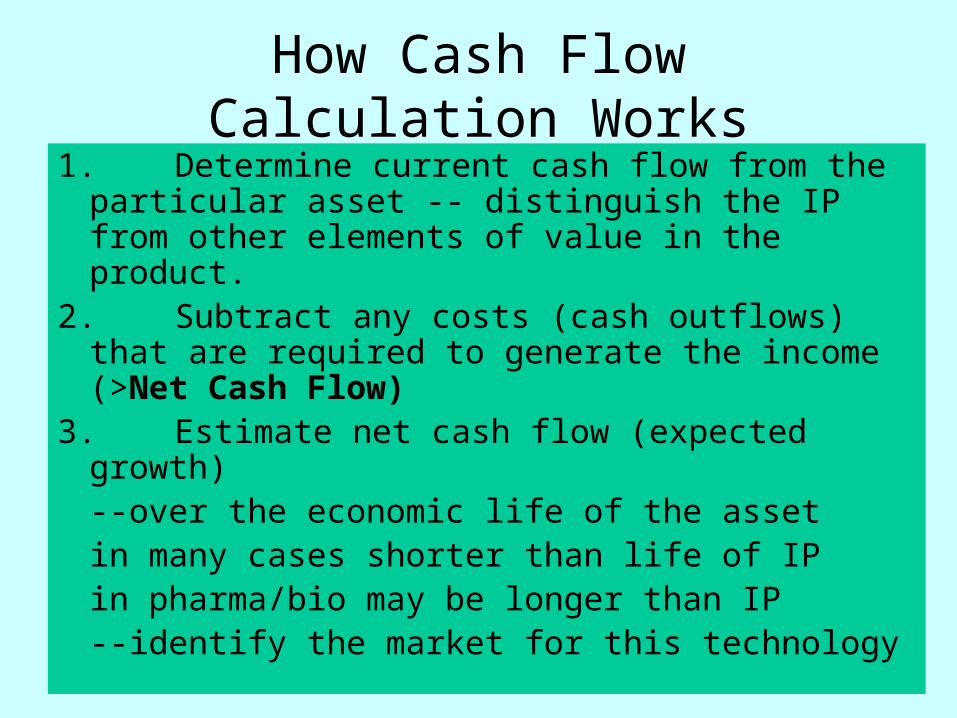

How Cash Flow Calculation Works

1. Determine current cash flow from the particular asset -- distinguish the IP from other elements of value in the product.

2. Subtract any costs (cash outflows) that are required to generate the income (>Net Cash Flow)

3. Estimate net cash flow (expected growth) --over the economic life of the asset

in many cases shorter than life of IPin pharma/bio may be longer than IP

--identify the market for this technology

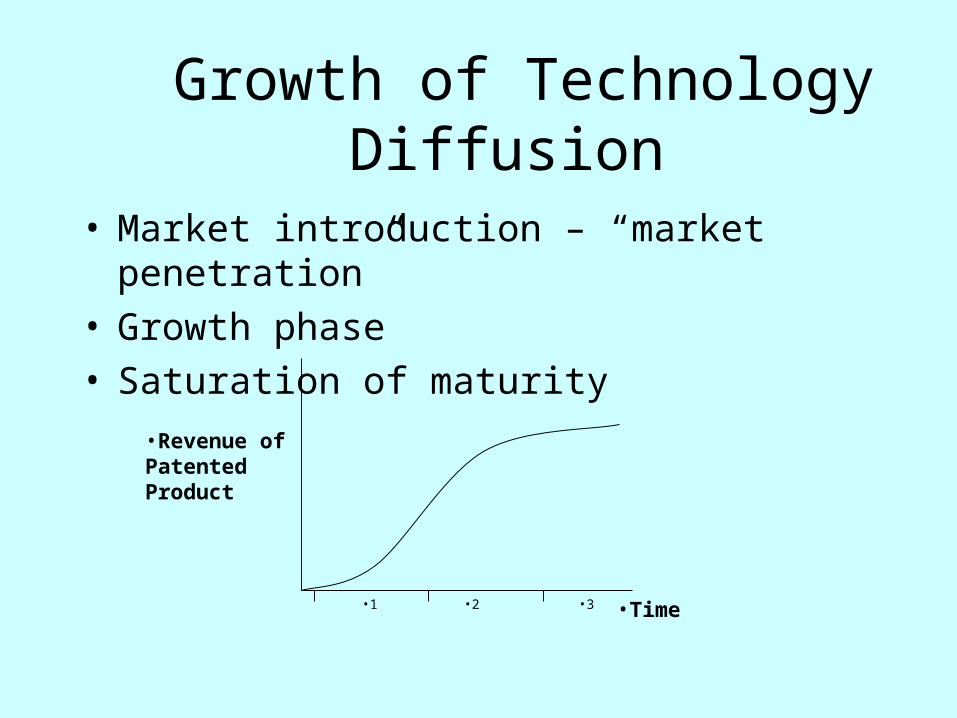

Growth of Technology Diffusion

• Market introduction – “market penetration”• Growth phase• Saturation of maturity

•1 •2 •3

•Revenue of Patented Product

•Time

How DCF Calculation Works

4. Discount projected future net cash flow to a lump sum that is the present value.

5. To do this, you make a judgment to determine a “discount rate” based on:

• Real interest rate – cost of capital• Expected inflation rate• Risk premium – probability of success• Apply discount rate on the projected net

cash flow over the economic life of the asset = PRESENT VALUE AMOUNT

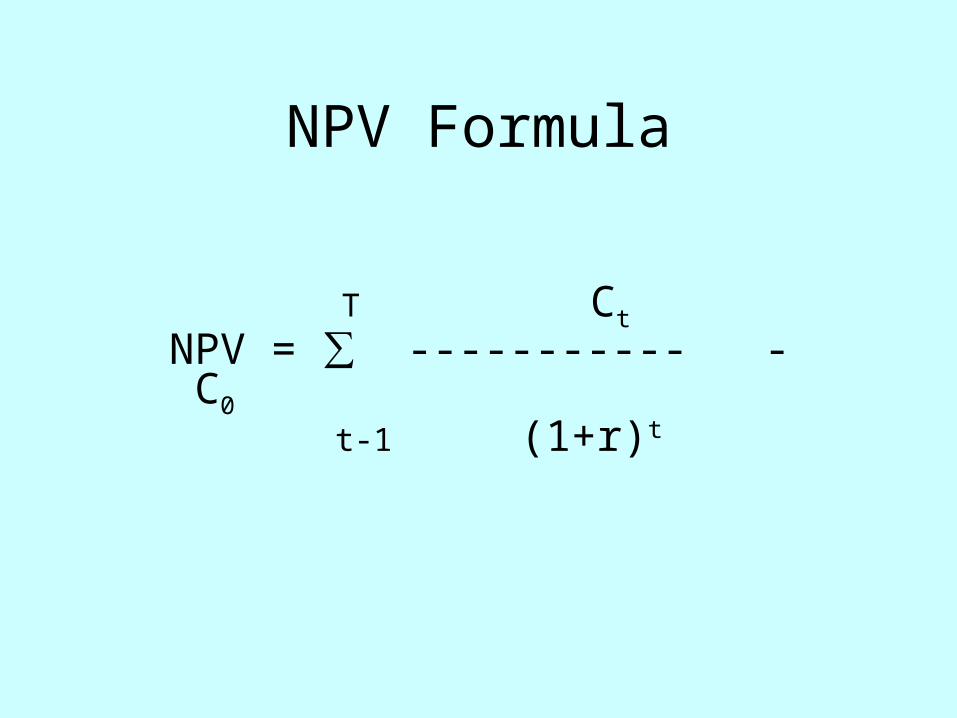

NPV Formula

T Ct

NPV = ∑ ----------- - C0

t-1 (1+r)t

Example

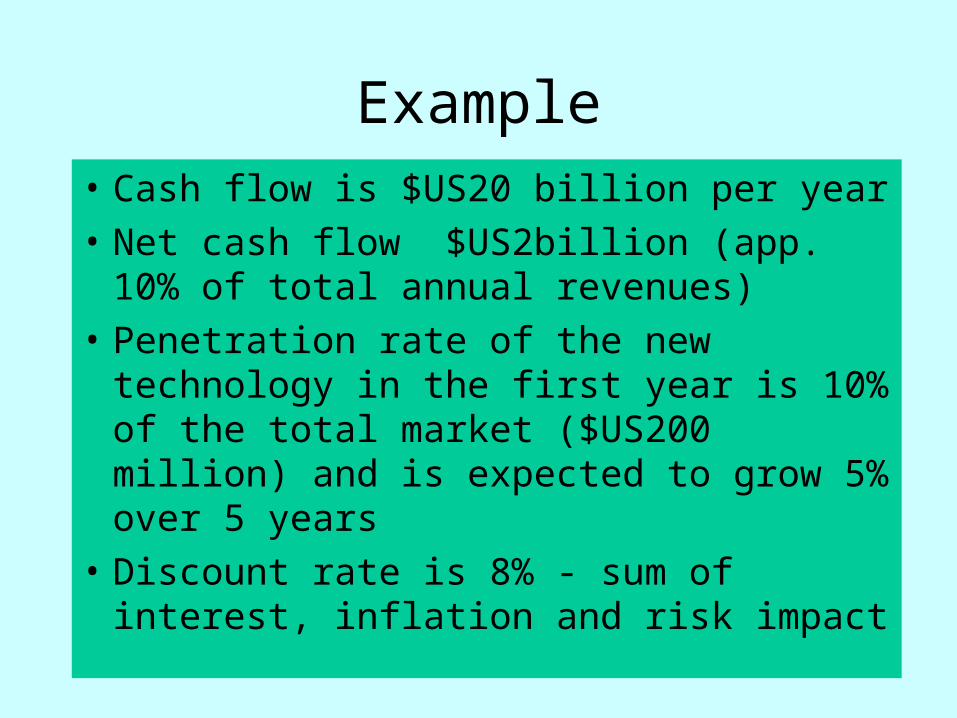

• Cash flow is $US20 billion per year

• Net cash flow $US2billion (app. 10% of total annual revenues)

• Penetration rate of the new technology in the first year is 10% of the total market ($US200 million) and is expected to grow 5% over 5 years

• Discount rate is 8% - sum of interest, inflation and risk impact

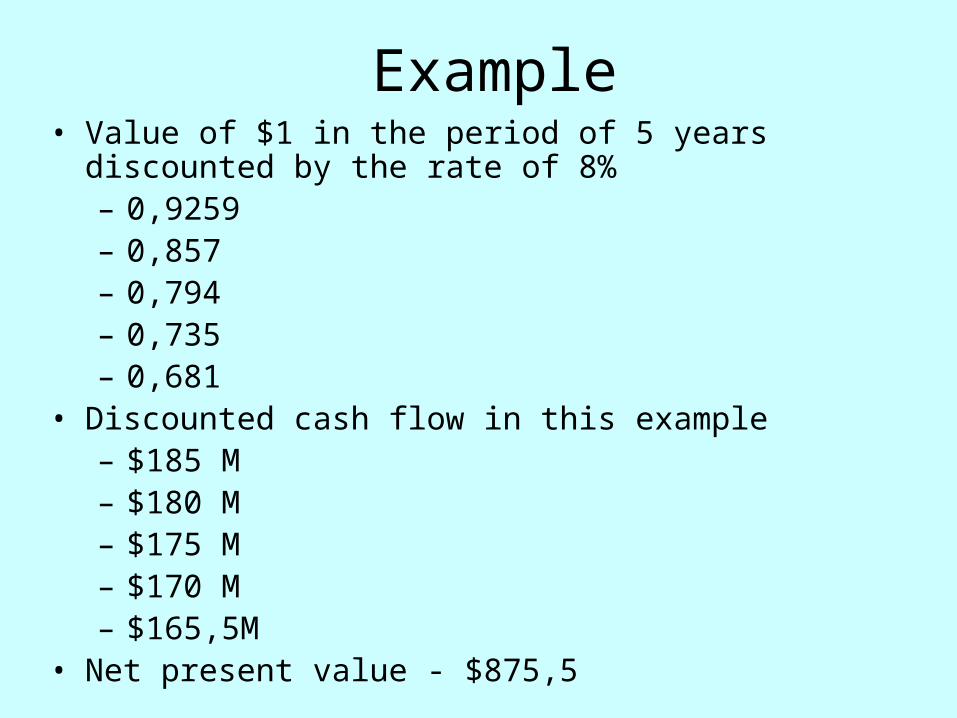

Example• Value of $1 in the period of 5 years discounted by the rate of

8%– 0,9259– 0,857– 0,794– 0,735– 0,681

• Discounted cash flow in this example– $185 M– $180 M– $175 M– $170 M– $165,5M

• Net present value - $875,5

Year 1 2 3 4 5 6 $244 $232 $220 $210 $200

(1) Expected economic benefit

(2) Discount factor

(NPV Formula)

1 1 (1.08)

1 _ (1.08)2

1 _ (1.08)3

1 _ (1.08)4

1 (1.08)5

0

(3) Discount factor

.925 .857 .794 .735 .681

(4) Discount benefit stream a

= $185 $180 $175 $170 $165,5

(5) Present Value

$875,5 = 185 + 180 + 175 + 170 + 165,5

*a Note: (4)=(2) X (1)

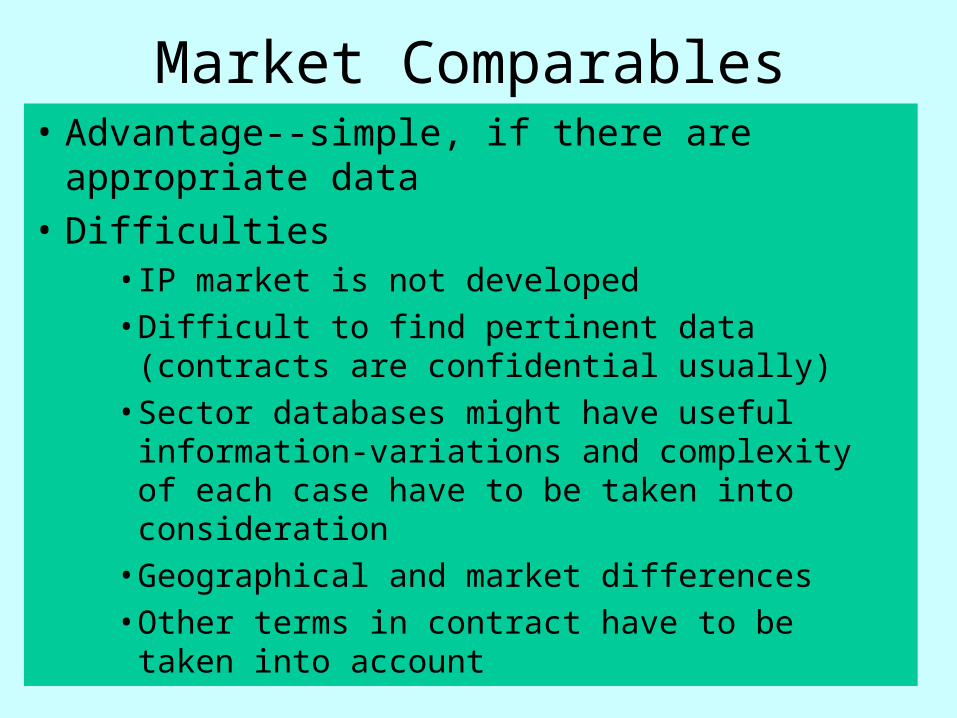

Market Comparables• Advantage--simple, if there are appropriate data

• Difficulties • IP market is not developed• Difficult to find pertinent data (contracts are

confidential usually)• Sector databases might have useful information-

variations and complexity of each case have to be taken into consideration

• Geographical and market differences• Other terms in contract have to be taken into

account

Alternative Costs• Replacement (creation) cost--cost of R&D +

cost of IP protection + probability of success; • Advantages: useful to estimate a

competitor’s invent-around costs and understand licensor’s perspective;

• Disadvantages– lost time

– difficult to determine

– cost of creation is not always representative of the value of the protected technology.

Alternative Costs

• Infringement suit– Costs

• Impact on existing business

• Legal fees

– Probability of success

• 25% Rule of Thumb

- Licensor gets 25% of profit

• Real options

• Monte Carlo simulation - a form of income analysis

• Qualitative valuation - subjective valuation used taking into account the strength or quality of the IP

• Many other variations

Other Valuation Methods

• Licensee perspective: how much can it afford to add to its cost of goods sold?

• Licensor perspective: – What rate of return on R&D investment does it

expect? • Misleading if R&D investment sunk cost• Misleading if technology is spin off

– What is cost of granting license• Competition• Warranites, guarantees. liabilities• Administration, enforcement

Practical approach

Forms of Payment in IP Licensing

• Royalties

• Lump sum• Installment payments

Forms of Payment

Royalties

• Royalty rate times royalty base

• Base is critical– Related to use of licensed IP– Kept in ordinary course of licensee’s business– Not subject to “creative accounting”– Not subject to unexpected fluctuations

Royalty Base

• Anything related to use of IP– Number of patented products made– Cycles of patented machine– Sale price of patented product– Sale price of product made using patented

method

• Price inflation sensitive, otherwise consider escalation provision

• The basis for royalty calculation:– Net Sales (must be defined -- gross sales net of

freight, shipping, rebates, insurance). – May be better to fix a % of gross sales in order

to avoid disputes or fix % of deductions.– What is the product on which the royalty is

measured--the whole device, only a part? Affects rate, not base

– Royalties on product that does not contain the licensed IP—possible problem

Form of Payment

• Increasing royalty rate as volume decreases– Keeps income to licensor constant

• Increasing royalty rate as volume increases– Restrain production– Reflect higher profits in pharmaceutical licenses

• Decrease royalty rate as volume increases– where value of technology is declining– incentive to produce more

Royalty Variations

• Based on business plan

• Important in exclusive licenses as security for licensor, incentive

• Absolute payment obligations? Risky for the licensee--can run it into insolvency, restrictions on sales– Licensee should have right to terminate

• Trigger for termination/ modification

Minimum Royalties

• Capped royalties

– Cap royalties over term of agreement to a fixed amount/avoids windfall

– Licensor doesn‘t like as it limits upside

• Vary royalty rate based on profit margin– 4 cylinder vs 8 cylinder auto

• Advances against royalties (where licensor needs up front cash to fund operations)

Royalty Variations

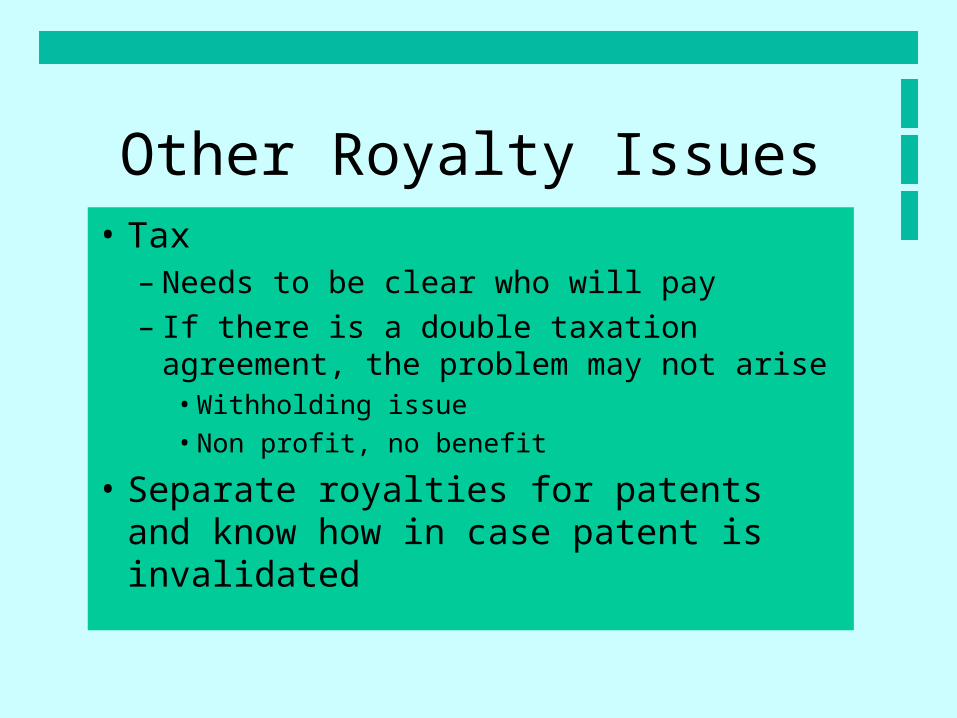

• Tax– Needs to be clear who will pay– If there is a double taxation agreement, the

problem may not arise• Withholding issue

• Non profit, no benefit

• Separate royalties for patents and know how in case patent is invalidated

Other Royalty Issues

• Product warranty– Product defects– Failure to perform to specification

• Indemnification – Third party claims of infringement– Product liability, malfunction, personal injury

• Indemnity should be capped at a fixed sum

• Indemnity by small party not worth much

Other Financial Terms: Warranties and Indemnities

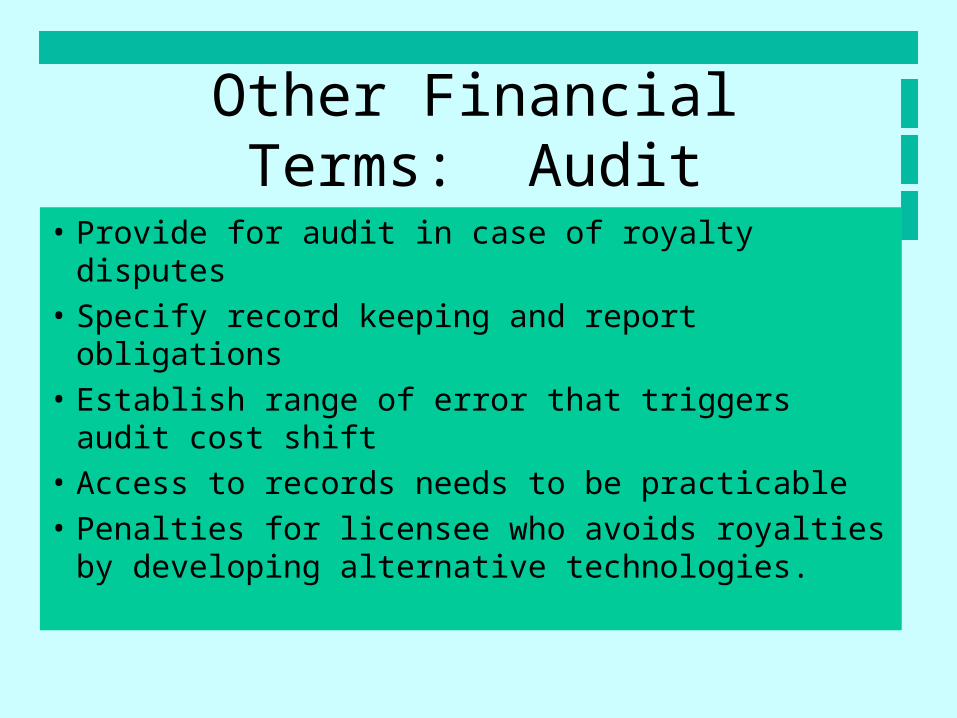

• Provide for audit in case of royalty disputes

• Specify record keeping and report obligations

• Establish range of error that triggers audit cost shift

• Access to records needs to be practicable

• Penalties for licensee who avoids royalties by developing alternative technologies.

Other Financial Terms: Audit

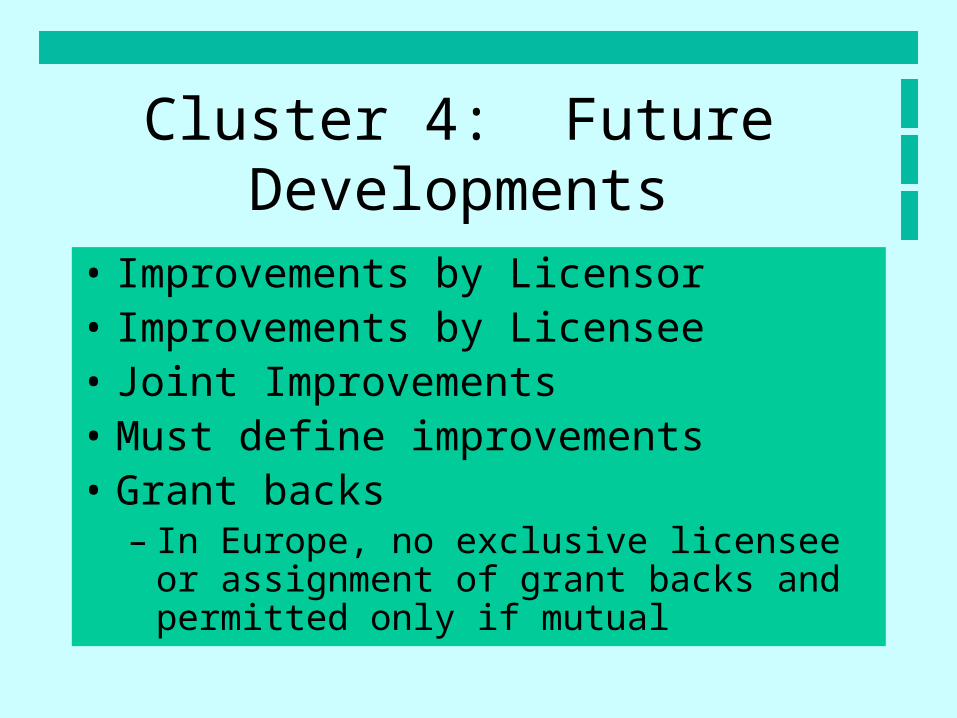

• Improvements by Licensor• Improvements by Licensee• Joint Improvements• Must define improvements• Grant backs

– In Europe, no exclusive licensee or assignment of grant backs and permitted only if mutual

Cluster 4: Future Developments

• Teaching and Training– Technical assistance limitations

• Consulting• New Versions• New Products• Maintenance, telephone support• Spare parts

Service and Support

• Avoid any commitments that limit options to develop new products

• Options to acquire new IP--but on what terms

• Rights of first refusal can be illusory and hold up deals

• Licensee will generally want access to the latest, but freedom to stay with the old

Future developments

• Financial Terms are always related to Clusters 1, 2 and 4.

• Look at total value

• Use flexibility in deciding how to pay

• Give both sides financial incentives to continue to work together.

Clusters 3 and 4: Conclusion