Autofacts ®

State of the Auto Industry Brandon Mason, PwC Autofacts

PwC

Agenda

Introduction to Autofacts ®

Global industry update

North America

Autofacts ® May 2012

Slide 2

PwC

Introduction to Autofacts ®

Autofacts ® May 2012

Slide 3

PwC

Autofacts – Our business model in context

Autofacts is a team of auto industry specialists within PwC’s Global Automotive practice dedicated to ongoing sector analysis. Autofacts data and analysis is used by the practice and by our clients to assess implications, make recommendations, and support auto industry decisions.

Autofacts ®

Global Automotive Practice

Analyst Briefings

(Quarterly)

Analyst Notes

(Monthly)

Analysis Services

Custom Deliverables

Global Light Vehicle &

Powertrain Forecast

Autofacts®

External Client Service

May 2012

Slide 4

PwC

Autofacts – Forecast methodology: A comprehensive and tested approach

Autofacts ®

Market Drivers Modeling Application Forecast

Macroeconomic Metrics Gross Domestic Product Interest Rate Trends Credit Availability Metrics Consumer Spending/Sentiment Employment Debt/Equity Accumulation Commodity Prices Inflationary Measures (CPI) Manufacturing/Housing Indices Demographics Government Stimulus Industry Indicators Imports/Exports/Inventory Plant Capacity/Utilisation Product Portfolio/Technology Incentives/Auto Financing Environmental/Safety Regulation Competitive Landscape

Analyst Input

Balancer Output

+

Proprietary

Data

Size Class /

Segment

Brand /

Nameplate

Region / Country

Alliance Group /

OEM

Platform / Product

Code

Forecast Level Quarterly Release

Autofacts®

Synchronous Forecasting

Integrated Data & Analysis

Online Client Access

Light Vehicle Assembly

Capacity / Utilisation

Powertrain

NA / EU Bodystyle

May 2012

Slide 5

PwC

Autofacts – Capabilities summary

Autofacts ®

Forecasts

Synchronous Global Update

Integrated Data & Analysis

Online Client Access

Analyst Briefings

Issues-based POV analysis

Regional market outlooks

Custom Analysis

Decision support Business

planning Thought leadership

Analyst Notes

Regional Industry Snapshots

Free Monthly Distribution

Engaging Viewpoints

Tested and trusted detailed

planning data and analysis on the

global light vehicle sector:

• Assembly / Capacity

• Powertrain

• Bodystyle (NA / EU)

Covering key issues facing

companies operating in the global

automotive sector:

• Deep regional insights

• Market trend analysis

• Powertrain outlook

Working in tandem with PwC’s

automotive practice, Autofacts can

assist with:

• M&A valuation support

• Industry studies

• Portfolio risk analysis

Providing easily digestible industry

updates on key market

developments:

• Unique auto viewpoints

• Key industry data sets

• autofacts.com/signup

Key Client

Benefits

• An independent, unbiased global perspective

• Differentiating & refined industry viewpoints

• Proactive & informed dialogue with executives

• Access to industry specialists with deep

expertise

For more information about

Autofacts products and

services, please contact:

May 2012

Slide 6

PwC

Global industry update

Autofacts ® May 2012

Slide 7

PwC

Global update – Assembly outlook Truly a global growth industry

Autofacts ®

106 million

The number of light

vehicles that will likely be

produced in 2018

5.2%

The CAGR for global light

vehicle assembly between

2011 - 2018

84%

Emerging markets’

contribution to growth

between 2011 - 2018

Source: Autofacts 2012 Q2 Data Release

May 2012

Slide 8

PwC

Global update – Forecast drivers Accentuate the positive, contain the negative

Assuming the European debt crisis is contained within the region’s borders, the auto industry has good reason to be optimistic for 2012. Monetary easing in key growth markets and recovery in Japan and Thailand should deliver a third sequential global record for light vehicle assembly in 2012.

Autofacts ®

74.6 74.6

76.8

78.2

79.5 79.7 79.7

2.2

1.4

1.2

0.6

-0.3

70

72

74

76

78

80

20

11

BR

IC

JP

NT

HA

NA

Oth

er

EU

20

12

Global: Light Vehicle Assembly Outlook 2011 – 2012 (millions)

European debt containment

BRICs regain momentum

Strong NA rebound

Japan + Thailand recovery

Non-resolution and/or

contagion scenario(s)

Divergent BRIC growth

trends

NA demand/ economic

flatline

Volatile ForEx + unknown

supply chain risk

Global: Light Vehicle Outlook Near-term positive and negative drivers

Source: Autofacts 2012 Q2 Data Release

May 2012

Slide 9

PwC

Global update – Assembly outlook After 2011 emerging market production dominates

For the first time in history, the number of vehicles produced in developing and emerging markets in 2011 was greater than the number of vehicles produced in mature markets. Sustainable demand for light vehicles in emerging markets will underpin organic growth for the foreseeable future.

Autofacts ®

Global: Light Vehicle Assembly by Market Type 2000 – 2018 (millions)

Global: Contribution to Growth by Region 2011 – 2018

0

10

20

30

40

50

60

70

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

Mature Emerging 0% 10% 20% 30% 40% 50% 60% 70%

MEA

EE

EU

SA

NA

AP China 39.4% India 12.9%

Brazil 6.9%

Russia 4.7%

May 2012

Slide 10

Source: Autofacts 2012 Q2 Data Release

PwC

Global update– Alliance group growth The gap at the top gets smaller

Autofacts ®

The contentious issue of who is number one remains, with Toyota expected to benefit from recovery from disruption caused by a number of natural disasters. Longer term we anticipate the three horse race will become a four horse one as Renault-Nissan enter the fray.

Global: Current Alliance Group Assembly Outlook* 2011, 2012, 2018 (millions)

0.0 1.0 2.0 3.0 4.0 5.0 6.0 7.0 8.0 9.0 10.0 11.0 12.0

Daimler

BMW

Suzuki

PSA

Honda

Fiat

Ford

Hyundai

RN

Toyota

VW

GM

2018 2012 2011

*RN = Renault-Nissan

May 2012

Slide 11

Source: Autofacts 2012 Q2 Data Release

PwC

Powertrain outlook – Global Engine, transmission, and technology forecast

Autofacts ®

Fuel Type and Delivery 2011 – 2018 (percent share)

Engine Intake Type 2011 – 2018 (percent share)

Weighted Engine Displacement 2011 – 2018 (litres)

Transmission Consumption 2011 vs. 2018 (percent share)

2011 2018

Engine Cons. by Configuration 2011 – 2018 (percent share)

Transmission Cons. by Gear Count 2011 vs. 2018 (percent share)

AMT DCT Auto CVT Electric Manual

Fuel / intake Transmission Engine

Gasoline Diesel Hybrid Electric DI

1.7

1.8

1.9

2.0

2.1

2.2

2011

2012

2013

2014

2015

2016

2017

2018

Th

ou

san

ds

0%

20%

40%

60%

80%

100%

2011

2012

2013

2014

2015

2016

2017

2018

0%

20%

40%

60%

80%

100%

2011

2012

2013

2014

2015

2016

2017

2018

R1/R2/I1/I2/I3 H4/I4/I5 H6/I6/V6

V8+ Electric

0% 20% 40% 60% 80% 100%

2018

2011

3 4 5 6 7 8 9 CVT Electric

0% 20% 40% 60% 80% 100%

20112012201320142015201620172018

Nat. Aspirated Turbo Twin Turbo Other

May 2012

Slide 12

Source: Autofacts 2012 Q2 Data Release

PwC

Powertrain outlook – Global Technology trending

Autofacts ®

Increasingly stringent global emission standards, combined with the ongoing consolidation of engine and transmission programs will result in a further shift towards alternative fuel technologies, with wider use of modularity to cater to individual market needs.

Global: Engine Fuel Type Consumption Outlook 2011 vs. 2018 (percent share)

Global: Top 5 Trending Powertrain Applications Market share gain (2018 vs. 2011)

75.46%

19.07% 3.17% 1.26% 1.04%

77.87%

20.21% 1.75% 0.05% 0.12%

2018

2011

Gasoline Diesel Hybrid PHEV PEV

1

2

3

4

5

Direct Injection +16.1%

DOHC

Turbocharging

CVTs

8-speed Trans.

+5.9%

+5.1%

+3.2%

+2.1%

May 2012

Slide 13

Source: Autofacts 2012 Q2 Data Release

PwC

North America

Autofacts ® May 2012

Slide 14

PwC

Market overview – Auto balancer key indicators in an atypical post-recession environment

May 2012

Slide 15

Autofacts ®

2%

4%

6%

8%

10%

2006

2007

2008

2009

2010

2011

2012

US: Long-Term Unemployment (27+ wks) 2000 – 2012 YTD (millions)

US: Non-Manufacturing Composite Index Jan 2008 – Mar 2012 (2008 = 100)

0

2

4

6

8

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Th

ou

san

ds

US: Auto Finance Average Prime Interest Rate 2006 – 2012 YTD

US: Total New Privately Owned Housing Starts* 2000 – 2012 YTD (millions) – *all units

US: Quarterly Real GDP Growth 2007 – 2011 Q4 final estimate (YoY Rate)

US: Total Asset Backed Security Issuance 2007 Q1 – 2012 Q1 (billions)

-10%

-6%

-2%

2%

6%

Q107

Q207

Q307

Q407

Q108

Q208

Q308

Q408

Q109

Q209

Q309

Q409

Q110

Q210

Q310

Q410

Q111

Q211

Q311

Q411

35

40

45

50

55

60

Jan

-08

Ap

r-08

Jul-0

8

Oct-

08

Jan

-09

Ap

r-09

Jul-0

9

Oct-

09

Jan

-10

Ap

r-10

Jul-1

0

Oct-

10

Jan

-11

Ap

r-11

Jul-1

1

Oct-

11

Jan

-12

0%

20%

40%

60%

80%

$0

$50

$100

$150

$200

Q1

07

Q4

07

Q3

08

Q2

09

Q1

10

Q4

10

Q3

11

A myriad of factors influence the sales and

assembly toplines

Structural Labour Market

Weakness 10 Quarters of Modest

Real GDP Growth

High Volume Vehicle

Launch Cadence

Interest Rates, Leasing, &

Incentive Upside Consumer Releveraging

Weak Service Spending

Housing Market Woes

& Household Debt

Auto Asset-Backed

Securitization Market

(+)

(-)

Supportive

Influences

Risk

Factors

Commodity Volatility

Inventory Recovery /

Replacement Demand

Euro Debt

Crisis

0.0

0.5

1.0

1.5

2.0

2.5

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Th

ou

san

ds

Source: US Federal Reserve, US Census, US BLS, EIA.gov, Edmunds, ISM

PwC

Sales outlook – North America Restrained 2011, breakneck start to 2012

Autofacts ®

The US light vehicle market continues to represent ~87% of all sales in North America, which confirms that the fate of the region is intrinsically tied to and driven by US performance. By historical standards, the environment remains subdued, yet the regional sales topline continues to cycle incrementally upward.

North America: Light Vehicle Sales Landscape 1990 – 2013(f) (millions)

North America: Light Vehicle Sales Jan 2007 – Mar 2012 (millions)

0

2

4

6

8

10

12

14

16

18

20

19

90

19

92

19

94

19

96

19

98

20

00

20

02

20

04

20

06

20

08

20

10

20

12

US Canada Mexico

0.0

0.3

0.5

0.8

1.0

1.3

1.5

1.8

Jan-0

7

Apr-

07

Jul-0

7

Oct-

07

Jan-0

8

Apr-

08

Jul-0

8

Oct-

08

Jan-0

9

Apr-

09

Jul-0

9

Oct-

09

Jan-1

0

Apr-

10

Jul-1

0

Oct-

10

Jan-1

1

Apr-

11

Jul-1

1

Oct-

11

Jan-1

2

US Canada Mexico

Source: Ward’s Automotive Reports, Autofacts Analysis

May 2012

Slide 16

PwC

Sales outlook – US The methodical recovery materialises

Autofacts ®

US light vehicle sales once remained fixed atop a 16–17.8 million unit plateau through the use of various industry stimulants. However, the theoretical end to the “push” model is delivering a methodical recovery more properly aligned with changes in metrics that drive real economic and industry health.

US: LV Sales Seasonally Adjusted Annual Rate Jan 2000 – Mar 2012 (millions)

US: SAAR + Annual LV Baseline Sales Forecast 2007 – 2013(f) (millions)

8

10

12

14

16

18

20

22

Jan-0

0

Jan-0

1

Jan-0

2

Jan-0

3

Jan-0

4

Jan-0

5

Jan-0

6

Jan-0

7

Jan-0

8

Jan-0

9

Jan-1

0

Jan-1

1

Jan-1

2

16.1

13.2

10.4 11.6

12.7 14.0

14.9

0

2

4

6

8

10

12

14

16

18

2007 2008 2009 2010 2011 2012(f) 2013(f)

Source: Ward’s Automotive Reports, Autofacts Analysis

May 2012

Slide 17

PwC

Sales overview – US New mix growth favors fuel economy

Autofacts ®

A series of new product launches in the small and mid car segments are helping buyers choose smaller, more economical vehicles better suited to blunt the impact of elevated fuel prices. The 2008 fuel price spike gave rise to a new era of pickup truck market share, which remains well below historical trend.

US: Light Vehicle Sales by Segment 2000 – Mar 2012

US: Light Vehicle Segmentation Market Share 2011 YTD vs. 2012 YTD

0%

20%

40%

60%

80%

100%

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

Small Car Mid Car Large Car Luxury Car

CUV SUV Van Pickup

0%

5%

10%

15%

20%

25%

30%

Sm

Ca

r

Mid

Car

Lg

Car

Lu

x C

ar

CU

V

SU

V

Van

Pic

ku

p

2012 2011Source: Ward’s Automotive Reports, Energy Information Agency

May 2012

Slide 18

PwC

Sales overview – US Sales momentum by automaker

Autofacts ®

While the Detroit 3 continue to perform with the market, share increases have been primarily bolstered by uncharacteristically low Japanese automaker sales that resulted from the post-crisis inventory shortages. D3 market share gains are encouraging, but will continue to feel near-term pressure.

US: Light Vehicle Sales by Automaker 2011 vs. 2012 YTD (thousands)

US: Light Vehicle Market Share by Automaker 2008 – 2012 YTD

-10%

0%

10%

20%

30%

40%

50%

0

200

400

600

GM

Ford

Toyota

Chry

sle

r

Nis

sa

n

Hond

a

Hyund

ai*

VW

2012 2011 YoY % Change (R-Axis)

0%

5%

10%

15%

20%

25%

GM

Ford

Toyota

Chry

sle

r

Ho

nd

a

Hyund

ai*

Nis

sa

n

VW

Oth

er

2012 2011 2010 2009 2008

*Includes KIA Source: Ward’s Automotive Reports

May 2012

Slide 19

PwC

Sales overview – US Inventory builds despite demand buoyancy

Autofacts ®

While demand strengthened substantially (14-15m SAAR) in Q1 2012, overall US inventory continues to register gradual increases, topping 2.75 million units in March – a figure last seen in 2009 when the economy was approaching historic lows and the industry was falling from unsustainable levels.

US: Light Vehicle Inventory Jan 2000 – Mar 2012 (millions)

US: Light Vehicle Inventory by Automaker Mar 2011 vs. Mar 2012 (thousands / days’ supply)

1

2

3

4

5

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

-20

-15

-10

-5

0

5

10

15

20

0

100

200

300

400

500

600

700

GM

Ford

Ch

rysle

r

Toyota

Ho

nda

Nis

san

Hyun

dai*

VW

2012 2011 Days' Supply Chg (R-Axis)

Source: Ward’s Automotive Reports, NBER, Autofacts Analysis

May 2012

Slide 20

PwC

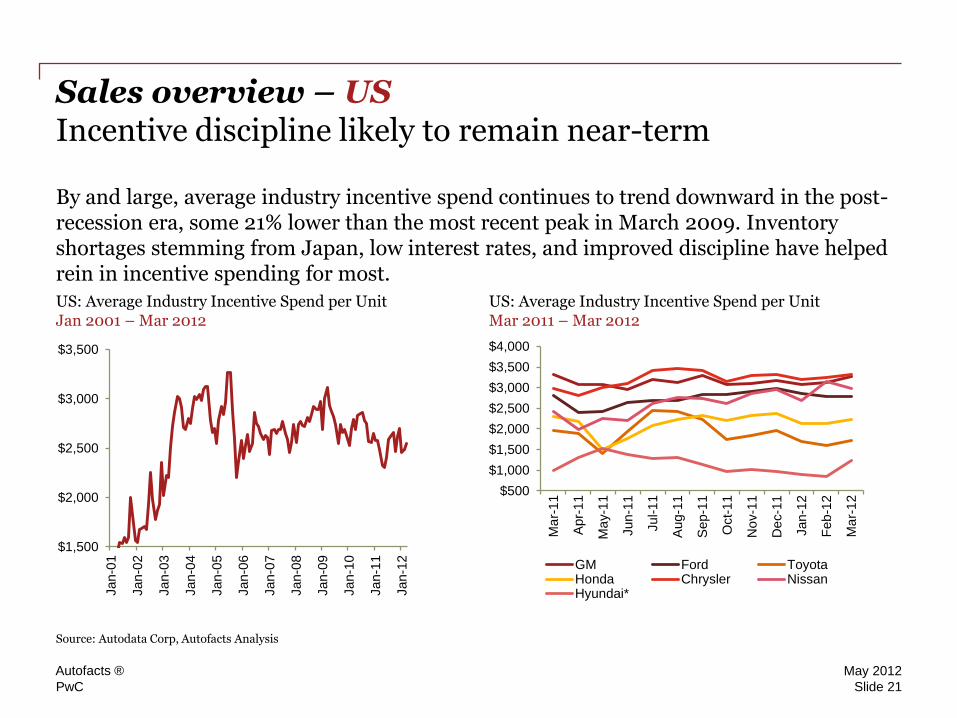

Sales overview – US Incentive discipline likely to remain near-term

Autofacts ®

By and large, average industry incentive spend continues to trend downward in the post-recession era, some 21% lower than the most recent peak in March 2009. Inventory shortages stemming from Japan, low interest rates, and improved discipline have helped rein in incentive spending for most.

US: Average Industry Incentive Spend per Unit Jan 2001 – Mar 2012

US: Average Industry Incentive Spend per Unit Mar 2011 – Mar 2012

$1,500

$2,000

$2,500

$3,000

$3,500

Jan-0

1

Jan-0

2

Jan-0

3

Jan-0

4

Jan-0

5

Jan-0

6

Jan-0

7

Jan-0

8

Jan-0

9

Jan-1

0

Jan-1

1

Jan-1

2

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

$4,000

Ma

r-1

1

Apr-

11

Ma

y-1

1

Jun-1

1

Jul-1

1

Aug-1

1

Sep-1

1

Oct-

11

No

v-1

1

De

c-1

1

Jan-1

2

Feb

-12

Ma

r-1

2

GM Ford ToyotaHonda Chrysler NissanHyundai*

Source: Autodata Corp, Autofacts Analysis

May 2012

Slide 21

PwC

Assembly outlook – North America New mix footprint returns assembly topline to prior peaks

Autofacts ®

Although GM and Ford will remain atop the output hierarchy, the North American landscape continues to be characterised by additional foreign brand assembly. Recent announcements stating global automakers’ intent to build new global product in North America bodes well for regional light vehicle production.

NA: Light Vehicle Assembly Outlook 1990 – 2018 (millions)

NA: Current Alliance Group Assembly Outlook* 2011 – 2013 (millions)

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

6789

1011121314151617181920

19

90

19

92

19

94

19

96

19

98

20

00

20

02

20

04

20

06

20

08

20

10

20

12

20

14

20

16

20

18

Assembly Volume Excess Capacity

Utilisation (R-Axis)

0.0 0.5 1.0 1.5 2.0 2.5 3.0 3.5

Other

VW

Hyundai

RN

Honda

Toyota

Fiat

Ford

GM

2013 2012 2011

Source: Autofacts 2012 Q2 Data Release *RN = Renault-Nissan. Chrysler Group LLC is classified under the Fiat Alliance Group outlook, including all potential volume from product sharing within the partnership.

May 2012

Slide 22

The information contained in this report represents the culmination of proprietary research

conducted by Autofacts, an analytical group within the PwC Research & Analysis Organisation.

All material contained in this report was developed independently of any PwC client

relationship and does not represent the firm’s view as an auditor to any legal business entity.

While every effort has been made to ensure the quality of information provided, no

representation or warranty of any kind (whether expressed or implied) is given by PwC as to

the accuracy, completeness or fitness for any purpose of this document. As such, this

document does not constitute the giving of investment advice, nor a part of any advice on

investment decisions. Accordingly, regardless of the form of action, whether in contract, tort or

otherwise, and to the extent permitted by applicable law, PwC accepts no liability of any kind

and disclaims all responsibility for the consequences of any person acting or refraining from

acting in reliance on this document.

© 2012 PricewaterhouseCoopers LLP. All rights reserved. PwC refers to the United States

member firm, and may sometimes refer to the PwC network. Each member firm is a separate

legal entity. Please see www.pwc. com/structure for further details.