SHREE Ganeshaya Namah

Question Bank

Standard On Auditing

C.A. FINAL

EDITION - 5

CA SURENDRA AGRAWAL

PH-9313336776

Visit At-www.casurendra.wordpress.com

https://www.facebook.com/casurendra.agrawal

Dedicated to

My family & Friends

Thanks to

AAshish Gupta

Quality Education

beyond your imagination...!

Price: 200/-

COMPLITE YOUR CA FINAL AUDIT IN 18 DAYS

BY CA SURENDRA AGRAWAL(M.COM,LLB,ACA)PH-9313336776

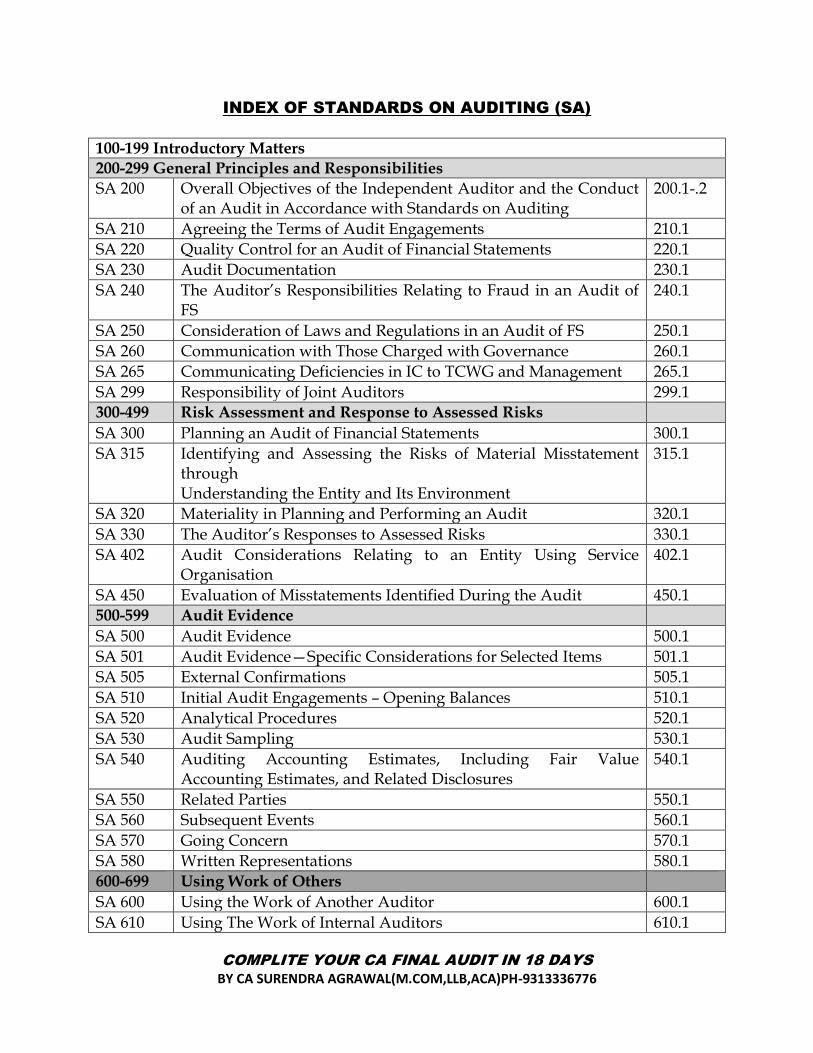

INDEX OF STANDARDS ON AUDITING (SA)

100-199 Introductory Matters 200-299 General Principles and Responsibilities

SA 200 Overall Objectives of the Independent Auditor and the Conduct of an Audit in Accordance with Standards on Auditing

200.1-.2

SA 210 Agreeing the Terms of Audit Engagements 210.1

SA 220 Quality Control for an Audit of Financial Statements 220.1

SA 230 Audit Documentation 230.1

SA 240 The Auditor’s Responsibilities Relating to Fraud in an Audit of FS

240.1

SA 250 Consideration of Laws and Regulations in an Audit of FS 250.1

SA 260 Communication with Those Charged with Governance 260.1

SA 265 Communicating Deficiencies in IC to TCWG and Management 265.1

SA 299 Responsibility of Joint Auditors 299.1 300-499 Risk Assessment and Response to Assessed Risks

SA 300 Planning an Audit of Financial Statements 300.1

SA 315 Identifying and Assessing the Risks of Material Misstatement through Understanding the Entity and Its Environment

315.1

SA 320 Materiality in Planning and Performing an Audit 320.1

SA 330 The Auditor’s Responses to Assessed Risks 330.1

SA 402 Audit Considerations Relating to an Entity Using Service Organisation

402.1

SA 450 Evaluation of Misstatements Identified During the Audit 450.1 500-599 Audit Evidence

SA 500 Audit Evidence 500.1

SA 501 Audit Evidence—Specific Considerations for Selected Items 501.1

SA 505 External Confirmations 505.1

SA 510 Initial Audit Engagements – Opening Balances 510.1

SA 520 Analytical Procedures 520.1

SA 530 Audit Sampling 530.1

SA 540 Auditing Accounting Estimates, Including Fair Value Accounting Estimates, and Related Disclosures

540.1

SA 550 Related Parties 550.1

SA 560 Subsequent Events 560.1

SA 570 Going Concern 570.1

SA 580 Written Representations 580.1

600-699 Using Work of Others

SA 600 Using the Work of Another Auditor 600.1

SA 610 Using The Work of Internal Auditors 610.1

COMPLITE YOUR CA FINAL AUDIT IN 18 DAYS

BY CA SURENDRA AGRAWAL(M.COM,LLB,ACA)PH-9313336776

SA 620 Using the Work of an Auditor’s Expert 620.1

700-799 Audit Conclusions and Reporting

SA 700 Forming an Opinion and Reporting on Financial Statements 700.1

SA 705 Modifications to the Opinion in the Independent Auditor’s Report

705.1

SA 706 Emphasis of Matter Paragraphs and Other Matter Paragraphs in the Independent Auditor’s Report

706.1

SA 710 Comparative Information - Corresponding Figures and Comparative Financial Statements

710.1

SA 720 The Auditor’s Responsibility in Relation to Other Information in Documents Containing Audited Financial Statements

720.1

800-899 Specialized Areas

SA 800 Audits of Financial Statements Prepared in Accordance with Special Purpose Frameworks

800.1

SA 805 Special Considerations - Audits of Single Financial Statements and Specific Elements, Accounts or Items of a Financial Statement

805.1

SA 810 Engagements to Report on Summary Financial Statements 810.1

2000-2699 Standards on Review Engagements (SREs)

SRE 2400 Engagements to Review Financial Statements 2400.1

SRE 2410 Review of Interim Financial Information Performed by the Independent Auditor of the Entity

2410.1

Engagements Other Than Audits or Reviews of Historical Financial Information

SAE 3400 The Examination of Prospective Financial Information 3400.1

SAE 3402 Assurance Reports on Controls At a Service Organisation 3402.1

SAE 3420 Engagements to Report on the Compilation of Pro Forma Financial Information

2420.1

4000-4699 Standards on Related Services (SRSs)

SRS 4400 Engagements to Perform Agreed-upon Procedures Regarding Financial Information

4400.1

SRS 4410 Engagements to Compile Financial Information 4410.1

Standards on Quality Control (SQCs)

SQC 1 QC for Firms that Perform Audit and Reviews of Historical Financial Information, & other Assurance & Related Services Engagements

SQC.1

200.1

SA – 200 (Revised)

“Overall Objectives of the Independent Auditor and Conduct of Audit in accordance with SAs

Question-1 Enumerate (in brief) the basic principles governing an audit.

Answer-

The basic principles which govern the auditor’s professional responsibilities and which should

be complied with wherever an audit is carried are described below:

(i) Integrity, Objectivity and

Independence:

The auditor should be straightforward, honest and

sincere in his approach to his professional work.

(ii) Confidentiality: The auditor should respect the confidentiality of

information acquired in the course of his work and

should not disclose any such information to a third party

without specific authority or unless there is a legal or

professional duty to disclose.

(iii) Skills and Competence: The audit should be performed and the report prepared

with due professional care by persons who have

adequate training, experience and competence in

auditing.

(iv) Work performed by others: When the auditor delegates work to assistants or uses

work performed by other auditor and experts, he will

continue to be responsible for forming and expressing his

opinion on the financial information. However, he will be

entitled to rely on work performed by others, provided

he exercises adequate skill and care and is not aware of

any reason to believe that he should not have so relied.

(v) Documentation: The auditor should document matters which are

important in providing evidence that the audit was

carried out in accordance with the basic principles.

(vi) Planning: The auditor should plan his work to enable him to

conduct an effective audit in an efficient and timely

manner. Plans should be based on knowledge of the

client’s business.

(vii) Audit evidence: The auditor should obtain sufficient appropriate audit

evidence through the performance of compliance and

substantive procedures to enable him to draw reasonable

conclusions therefrom on which to base his opinion on

the financial information.

(viii) Accounting System and

Internal Control:

The auditor should gain an understanding of the

accounting system and related controls and should study

and evaluate the operation of those internal controls

upon which he wishes to rely in determining the nature,

timing and extent of other audit procedures.

(ix) Audit conclusions and

reporting:

The auditor should review and assess the conclusions

drawn from the audit evidence obtain and from his

knowledge of business of the entity as the basis for the

expression of his opinion on the financial information.

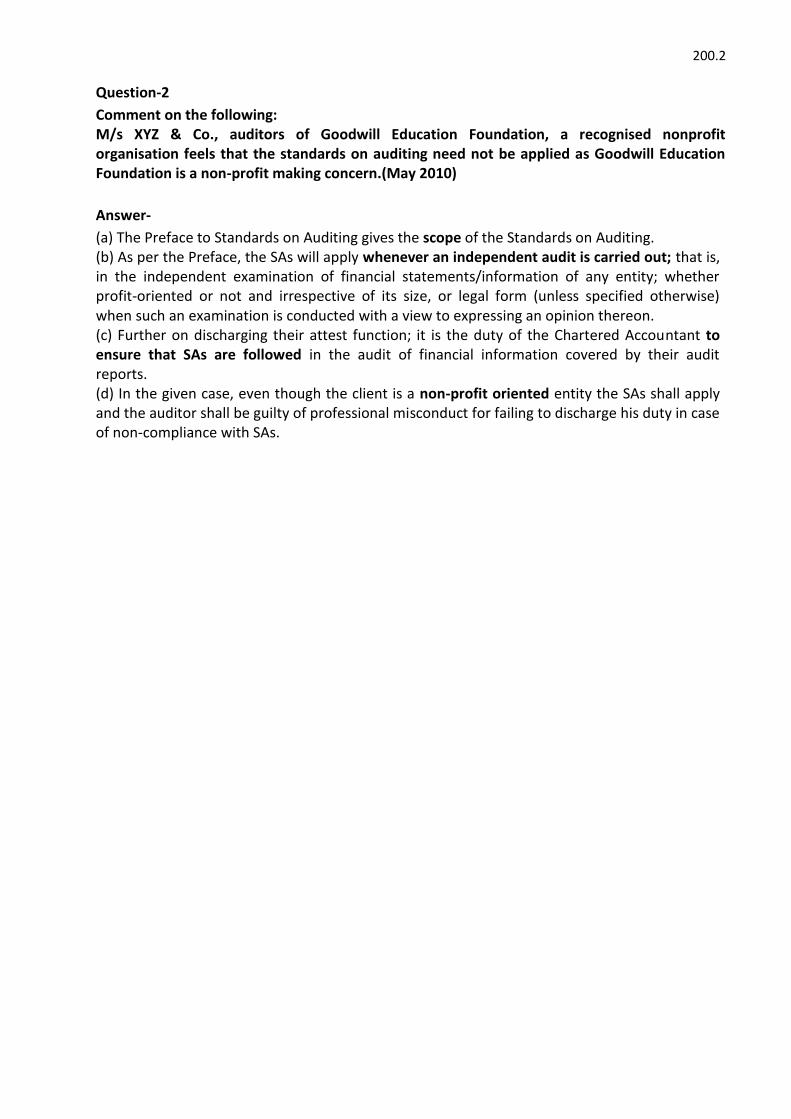

200.2

Question-2

Comment on the following:

M/s XYZ & Co., auditors of Goodwill Education Foundation, a recognised nonprofit

organisation feels that the standards on auditing need not be applied as Goodwill Education

Foundation is a non-profit making concern.(May 2010)

Answer-

(a) The Preface to Standards on Auditing gives the scope of the Standards on Auditing.

(b) As per the Preface, the SAs will apply whenever an independent audit is carried out; that is,

in the independent examination of financial statements/information of any entity; whether

profit-oriented or not and irrespective of its size, or legal form (unless specified otherwise)

when such an examination is conducted with a view to expressing an opinion thereon.

(c) Further on discharging their attest function; it is the duty of the Chartered Accountant to

ensure that SAs are followed in the audit of financial information covered by their audit

reports.

(d) In the given case, even though the client is a non-profit oriented entity the SAs shall apply

and the auditor shall be guilty of professional misconduct for failing to discharge his duty in case

of non-compliance with SAs.

210.1

SA 210 (REVISED)

AGREEING THE TERMS OF AUDIT ENGAGEMENTS

Question1

R&Co., a firm of Chartered Accountants have not revised the terms of engagements and

obtained confirmation from the clients, for last 5years despite changes in business and

professional environment. Please elucidate the circumstances that may warrant the

revision in terms of engagement.

Answer-

As per SA210 on Agreeing the Terms of Audit Engagements , the auditor may decide not to

send a new audit engagement letter or other written agreement each period. However, the

following factors may make it appropriate to revise the terms of the audit engagement or to

remind the entity of existing terms:

(i) Any indication that the entity misunderstands the objective and scope of the audit.

(ii) Any revised or special terms of the audit engagement.

(iii) A recent change of senior management.

(iv) A significant change in ownership.

(v) A significant change in nature or size of the entity s business.

(vi) A change in legal or regulatory requirements.

(vii) A change in the financial reporting framework adopted in the Preparation of the financial

statements.

(viii) A change in other reporting requirements.

Question2

M/s. PQR & Company, Chartered Accountants have been appointed Statutory Auditors of

a listed Company for the year ended 31st March, 2008. Draft an appropriate engagement

letter to be sent to the Board of Directors for the same.

To, the Board of Directors of .................. (name of the Entity)

(Address)

Dear Sirs, I

/ We refer to the letter dated _________ informing me / us about my / our (re) appointment/ratification

as the auditors of the Company. You have requested that I / we audit the financial statements of the

Company as defined in Section 2(40) of the Companies Act, 2013 ( 2013 Act ), for the financial year(s)

beginning April 1, 20XX and ending March 31, 20YY2 . The financial statements of the Company include,

where applicable, consolidated financial statements of the Company and of all its subsidiaries, associate

companies and joint ventures.

I am / We are pleased to confirm my / our acceptance and my / our understanding of this audit

engagement by means of this letter.

My / Our audit will be conducted with the objective of me / our expressing an opinion if the aforesaid

financial statements give the information required by the 2013 Act in the manner so required, and give a

true and fair view in conformity with the applicable accounting principles generally accepted in India, of

the state of affairs of the Company as at 31st March, 20YY, and its profit/loss and its cash flows for the

210.2

year ended on that date which, inter alia, includes reporting in conjunction whether the Company has an

adequate internal financial controls system over financial reporting in place and the operating

effectiveness of such controls. In forming my / our opinion on the financial statements, I / we will rely on

the work of branch auditors appointed by the Company and my / our report would expressly state the

fact of such reliance.

I / We will conduct my / our audit in accordance with the Standards on Auditing (SAs), issued by the

Institute of Chartered Accountants of India (ICAI) and deemed to be prescribed by the Central

Government in accordance with Section 143(10) of the 2013 Act. Those Standards require that I / we

comply with ethical requirements and plan and perform the audit to obtain reasonable assurance about

whether the financial statements are free from material misstatements. An audit involves performing

procedures to obtain audit evidence about the amounts and the disclosures in the financial statements.

The procedures selected depend on the auditor s judgment, including the assessment of the risks of

material misstatement of the financial statements, whether due to fraud or error. In making those risk

assessments, the auditor considers internal financial control relevant to the Company s preparation of the

financial statements that give a true and fair view in order to design audit procedures that are

appropriate in the circumstances. The terms of reference for my / our audit of internal financial controls

over financial reporting carried out in conjunction with our audit of the Company s financial statements

will be as stated in the separate engagement letter for conducting such audit and should be read in

conjunction with this letter. An audit also includes evaluating the appropriateness of the accounting

policies used and the reasonableness of accounting estimates made by the Management, as well as

evaluating the overall presentation of the financial statements. Because of the inherent limitations of an

audit, including the possibility of collusion or improper management override of controls, there is an

unavoidable risk that material misstatements due to fraud or error may occur and not be detected, even

though the audit is properly planned and performed in accordance with the SAs. Also, projections of any

evaluation of the internal financial controls over financial reporting to future periods are subject to the

risk that the internal financial control over financial reporting may become inadequate because of

changes in conditions, or that the degree of compliance with the policies or procedures may deteriorate.

My / Our audit will be conducted on the basis that the Management and those charged with governance

(Audit Committee / Board) acknowledge and understand that they have the responsibility: (a) For the

preparation of financial statements that give a true and fair view in accordance with the applicable

Financial Reporting Standards and other generally accepted accounting principles in India. This includes:

Compliance with the applicable provisions of the 2013 Act; Proper maintenance of accounts and other

matters connected therewith; The responsibility for the preparation of the financial statements on a

going concern basis; The preparation of the annual accounts in accordance with, the applicable

accounting standards and providing proper explanation relating to any material departures from those

accounting standards; Selection of accounting policies and applying them consistently and making

judgments and estimates that are reasonable and prudent so as to give a true and fair view of the state

of affairs of the Company at the end of the financial year and of the profit and loss of the Company for

that period; Taking proper and sufficient care for the maintenance of adequate accounting records in

accordance with the provisions of the 2013 Act for safeguarding the assets of the Company and for

preventing and detecting fraud and other irregularities; Laying down internal financial controls to be

followed by the Company and that such internal financial controls are adequate and were operating

effectively; and Devising proper systems to ensure compliance with the provisions of all applicable laws

and that such systems were adequate and operating effectively. (b) Identifying and informing me / us of

financial transactions or matters that may have any adverse effect on the functioning of the Company. (c)

Identifying and informing me / us of : All the pending litigations and confirming that the impact of the

210.3

pending litigations on the Company s financial position has been disclosed in its financial statements; All

material foreseeable losses, if any, on long term contracts including derivative contracts and the accrual

for such losses as required under any law or accounting standards; and Any delay in transferring

amounts, required to be transferred, to the Investor Education and Protection Fund by the Company. (d)

Informing me / us of facts that may affect the financial statements, of which Management may become

aware during the period from the date of my / our report to the date the financial statements are issued.

(e) Identifying and informing me / us as to whether any director is disqualified as on March 31, 20YY from

being appointed as a director in terms of Section 164 (2) of the 2013 Act. This should be supported by

written representations received from the directors as on March 31, 20YY and taken on record by the

Board of Directors. (f) To provide me / us, inter alia, with: (i) Access, at all times, to all information,

including the books, accounts, vouchers and other records and documentation of the Company, whether

kept at the Head Office or elsewhere, of which the Management is aware that are relevant to the

preparation of the financial statements such as records, documentation and other matters. This will

include books of account maintained in electronic mode; (ii) Access, at all times, to the records of all the

subsidiaries (including associate companies and joint ventures as per Explanation to Section 129(3) of the

2013 Act) of the Company in so far as it relates to the consolidation of its financial statements, as

envisaged in the 2013 Act; (iii) Access to reports, if any, relating to internal reporting on frauds (e.g., vigil

mechanism reports etc.), including those submitted by cost accountant or company secretary in practice

to the extent it relates to their reporting on frauds in accordance with the requirements of Section

143(12) of the 2013 Act; (iv) Additional information that I / we may request from the Management for the

purposes of my / our audit; (v) Unrestricted access to persons within the Company from whom I / we

deem it necessary to obtain audit evidence. This includes my / our entitlement to require from the

officers of the Company such information and explanations as I / we may think necessary for the

performance of my / our duties as the auditors of the Company; and (vi) All the required support to

discharge my / our duties as the statutory auditors as stipulated under the Companies Act, 2013/ ICAI

standards on auditing and applicable guidance. As part of my / our audit process, I / we will request from

the Management written confirmation concerning representations made to me / us in connection with

my / our audit. My / Our report prepared in accordance with relevant provisions of the 2013 Act would be

addressed to the shareholders of the Company for adoption of the accounts at the Annual General

Meeting. In respect of other services, my / our report would be addressed to the Board of Directors. The

form and content of my / our report may need to be amended in the light of my / our audit findings. In

accordance with the requirements of Section 143(12) of the 2013 Act, if in the course of performance of

my / our duties as auditor, I / we have reason to believe that an offence involving fraud is being or has

been committed against the Company by officers or employees of the Company, I / we will be required to

report to the Central Government, in accordance with the rules prescribed in this regard which, inter alia,

requires me / us to forward my / our report to the Board or Audit Committee, as the case may be, seeking

their reply or observations, to enable me / us to forward the same to the Central Government. As stated

above, given that I am / we are required as per Section 143(12) of the Act to report on frauds, such

reporting will be made in good faith and, therefore, cannot be considered as breach of maintenance of

client confidentiality requirements or be subject to any suit, prosecution or other legal proceeding since it

is done in pursuance of the 2013 Act or of any rules or orders made there under. I / We also wish to invite

your attention to the fact that our audit process is subject to 'peer review' / quality review under the

Chartered Accountants Act, 1949. The reviewer(s) may inspect, examine or take abstract of my / our

working papers during the course of the peer review/quality review. I / We may involve specialists and

staff from our affiliated network firms to perform certain specific audit procedures during the course of

my / our audit. In terms of Standard on Auditing 720 – The Auditor s Responsibility in Relation to Other

Information in Documents Containing Audited Financial Statements issued by the ICAI and deemed to be

prescribed by the Central Government in accordance with Section 143(10) of the 2013 Act , I / we request

210.4

you to provide to me / us a Draft of the Annual Report containing the audited financial statements so as

to enable me / us to read the same and communicate material inconsistencies, if any, with the audited

financial statements, before issuing the auditor s report on the financial statements {Insert Other

information, such as fee arrangements, billings and other specific terms, as appropriate.} This letter

should be read in conjunction with my / our letter dated ___ for the Audit of Internal Financial Controls

Over Financial Reporting under the 2013 Act, in respect of which separate fees have been fixed/will be

mutually agreed.

I / We look forward to full cooperation from your staff during my / our audit. Please sign and return the

attached copy of this letter to indicate your acknowledgement of, and agreement with, the arrangements

for my / our audit of the financial statements including our respective responsibilities.

Yours faithfully,

(signature)

(Name of the Member)

(Designation)

(Name of the Firm)

Date:

Place:

Copy to: Chairman, Audit Committee

Acknowledged on behalf of <>

Name and Designation: _________________ Date: ______________

220.1

SA 220 - QUALITY CONTROL FOR AN AUDIT OF FS

Question-1

You are an audit senior working for the firm Kala & Company. You are currently carrying out

the audit of W Ltd., a manufacturer of waste paper bins. You are unhappy with W Ltd.'s

inventory valuation policy and have raised the issue several times with the audit manager. He

has dealt with the client for a number of years and does not see what you are making a fuss

about. He has refused to meet you on site to discuss these issues.

The former engagement partner to W Ltd. retired two months ago. As the audit manager had

dealt with W Ltd. for so many years, the other partners have decided to leave the audit of W

Ltd. in his capable hands. Comment on the situation outlines above. (RTP)

Answer:

Several quality control issues are raised in the scenario:

(1) Engagement Partner: An engagement partner is usually appointed to each audit

engagement undertaken by the firm, to take responsibility for the engagement on

behalf of the firm.

Assigning the audit to an experienced audit manager is not sufficient.

(2) The lack of an audit engagement partner also means that several of the requirements of

SA 220 directing, supervising and reviewing the audit are not in place.

(3) Conflicting Views: In this scenario the audit manager and senior have conflicting views

about the valuation of inventory. This does not appear to have been handled well, with

the manager refusing to discuss the issue with the senior.

(4) Resolving of Disputes: SA 220, requires that the audit engagement partner takes

responsibility for setting disputes in accordance with the firm's policy in respect of

resolution of difference of opinion required by SQC 1" Quality Control for Firms that

Perform Audits and Reviews of Historical Financial Information, and Other Assurance and

Related Services Engagements".

(5) Reasons for Failure to Resolve the Disputes: In this case, the lack of engagement partner

may have contributed to this failure to resolve the disputes. In any event, at best, the

failure to resolve the difference of opinion is a breach of the firm's policy under SQC 1. At

worst, it indicates that the firm does not have a suitable policy concerning such

disputes required by SQC.l "Quality Control for Firms that Perform Audits and Reviews of

Historical Financial Information, and Other Assurance and Related Services

Engagements".

Question-2

"The work performed by each assistant needs to be reviewed by personnel of at least equal

competence."(May 2011)

Answer:

Reviewing the work performed by Assistant: As per SA 220 "Quality Control for an Audit of

Financial Statements" the firm's review responsibility policies and procedures are determined on

the basis that work of less experienced team members is reviewed by more experienced team

members.

220.2

EP is responsible for the engagement and its performance, and for the report that is issued on

behalf of the firm, and who, where required, has the appropriate authority from a

professional, legal or regulatory body.

Engagement partner's satisfaction on or before the date of the auditor's report:

The engagement partner shall ensure that reviews being performed are in accordance with

the firm's review policies and procedures. A review consists of consideration whether, for

example:

(1) The work has been performed in accordance with professional standards and regulatory and

legal requirements;

(2) Significant matters have been raised for further consideration;

(3) Appropriate consultations have taken place and the resulting conclusions have been

documented and implemented;

(4) There is a need to revise the nature, timing and extent of work performed;

(5) The work performed supports the conclusions reached and is appropriately documented;

(6) The evidence obtained is sufficient and appropriate to support the auditor's report; and

(7) The objectives of the engagement procedures have been achieved.

Question-3

Importance of KYC Requirements for a Chartered Accountant's Practice. (Nov 2014)

Answer

As per SA-220 (Revised) The practicing chartered accountant should obtain information

regarding the client, whether or not to undertake the assignment with the client. This may be

due to:

a) Client doing an illegal activity.

b) Client putting unnecessary pressure for completing the audit.

The firm should establish policies and procedures for the acceptance and continuance of

client relationships and specific engagements, designed to provide it with reasonable

assurance that it will undertake or continue relationships and engagements only where it:

a) Has considered the integrity of the client and does not have information that would lead it to

conclude that the client lacks integrity;

b) Is competent to perform the engagement and has the capabilities, time and resources to do

so; and

c) Can comply with the ethical requirements.

d) The firm should obtain such information as it considers necessary in the circumstances before

accepting an engagement with a new client, when deciding whether to continue an existing

engagement, and when considering acceptance of a new engagement with an existing client.

With regard to the integrity of a client matters that the firm considers include, for example:

(1) The identity and business reputation of the client's principal owners, key management, related

parties and those charged with its governance.

(2) The nature of the client's operations, including its business practices.

(3) Information concerning the attitude of the client's principal owners, key management and

those charged with its governance towards such matters as aggressive interpretation of

accounting standards and the internal control environment.

(4) Whether the client is aggressively concerned with maintaining the firm's fees as low as

possible.

(5) Indications of an inappropriate limitation in the scope of work.

(6) Indications that the client might be involved in money laundering or other criminal activities.

220.3

Question-4

M/s Sureshchandra & Co. has been appointed as an auditor of SC Ltd. for the financial year

2014-15. CA. Suresh, one of the partners of M/s Sureshchandra & Co., completed entire

routine audit work by 29th May, 2015. Unfortunately, on the very next morning, while roving

towards office of SC Ltd. to sign final audit report,he met with a road accident and died. CA.

Chandra, another partner of M/s Sureshchandra & Co., therefore, signed the accounts of SC

Ltd., without reviewing the work performed by CA. Suresh. State with reasons whether CA.

Chandra is right in expressing an opinion on financial statements the audit of which is

performed by another auditor.

Answer-

Relying on Work Performed by Another Auditor: As per SA 220 Quality Control for an Audit of

Financial Statements , an engagement partner taking over an audit during the engagement may

apply the review procedures such as the work has been performed in accordance with

professional standards and regulatory and legal requirements

The engagement partner shall take responsibility For reviews being performed in accordance

with the firm’s review policies and procedures On or before the date of the auditor’s report, The

engagement partner shall, be satisfied that sufficient appropriate audit evidence has been

obtained to support the conclusions and the auditor’s report.

Further, one of the basic principles, which govern the auditor’s professional responsibilities and

which should be complied with wherever an audit is carried, is that when the auditor delegates

work to assistants or uses work performed by other auditor and experts, he will continue to be

responsible for forming and expressing his opinion on the financial information. However, he will

be entitled to rely on work performed by others, provided he exercises adequate skill and care is

not aware of any reason to believe that he should not have so relied. This is the fundamental

principle which is ethically required as per Code of Ethics.

In the given case, all the auditing procedures before the moment of signing of final report have

been performed by CA. Suresh. However, the report could not be signed by him due to his

unfortunate death. Later on, CA. Chandra signed the report relying on the work performed by

CA. Suresh. Here, CA. Chandra is allowed to sign the audit report, though, will be responsible for

expressing the opinion. He may rely on the work performed by CA. Suresh provided he further

exercises adequate skill and due care and review the work performed by him.

230.1

SA 230 - AUDIT DOCUMENTATION

Question-1

As an auditor how would you deal with the following: The statutory auditor of the holding

company demands for the working paper of the auditors of the subsidiary company, of which

you are the auditor?

Answer:

As per SA 230, Audit Documentation working papers are the property of the auditor. The

auditor may, at his discretion, make portion of or extracts of his working papers available to his

client.

SA 600 Using the Work of Another Auditors also states that an auditor should respect the

confidentiality of information acquired during the course of his audit work and should not

disclose such information unless there is a legal or professional duty to disclose.

As per ICAI Guidelines, statutory auditor of an enterprise do not have right of access to the audit

working papers of the branch auditor. An auditor can rely on the work of another auditor,

without having any right of access to the audit working papers of other auditor.

Conclusion: Statutory auditor of Holding company cannot have access to audit working papers of

the subsidiary company’s auditor. He can however, asks the auditor to answer certain questions

about the manner in which the audit is conducted and certain other clarifications regarding audit

Question-2

What are Audit working papers and why should they be carefully preserved by auditor?

Answer

Record of:

Audit procedures performed

Relevant audit evidence obtained, &

Conclusions reached

Purpose

includes the following:

(1) Assist in Planning and performance of Audit.

(2) Direction, supervision & Review of work.

(3) To fix accountability.

(4) Record for future reference.

(5) Quality control review and inspections

(6) Conduct of external inspections.

Question-3

Discuss various contents of permanent audit file and current file. (Nov 2005, May 2007)?

Answer-

(I) Permanent Audit file: It includes -

230.2

(1) Information concerning the legal and organisational structure of the entity. Example: MOA,

AOA etc.

(2) Extracts or copies of important legal documents, agreements and minutes relevant to the

audit.

(3) A record of the study and evaluation of the internal controls related to the accounting system.

(4) Copies of audited financial statements for previous years.

(5) Analysis of significant ratios and trends.

(6) Copies of management letters issued by the auditor, if any.

(7) Record of communication with the retiring auditor, if any, before acceptance of the

appointment as auditor.

(8) Notes regarding significant accounting policies.

(9) Significant audit observations of earlier years.

(II) Current Audit file:The current file normally includes:

(1) Correspondence relating to acceptance of annual reappointment.

(2) Extracts of important matters in the minutes of Board Meetings and General

(3) Meetings, as are relevant to the audit.

(4) Evidence of the planning process of the audit and audit programme.

(5) Analysis of transactions and balances.

(6) A record of the nature, timing and extent of auditing procedures performed and the results of

such procedures.

(7) Evidence that the work performed by assistants was supervised and reviewed.

(8) Copies of communications with other auditors, experts and other third parties.

(9) Copies of letters or notes concerning audit matters communicated to or discussed with the

client, including the terms of the engagement and material weaknesses in relevant internal

controls.

(10) Letters of representation or confirmation received from the client.

(11) Conclusions reached by the auditor concerning significant aspects of the audit.

(12) Copies of the financial information being reported on and the related audit reports.

Question-3

Mr. A, a practising Chartered Accountant, has been appointed as an auditor of True Pvt. Ltd.

What factors would influence the amount of working papers required to be maintained for the

purpose of his audit?(Nov-15)

Answer

(a) Factors Influencing the Amount of Working Papers: As per SA 230 Audit Documentation ,

which refers to the record of audit procedures performed, relevant audit evidence obtained and

conclusions the auditor reached, the amount of audit working papers depend on factors such as-

(i) The size and complexity of the entity.

(ii) The nature of the audit procedures to be performed.

(iii) The identified risks of material misstatement.

(iv) Thesignificance of the audit evidence obtained.

(v) The nature and extent of exceptions identified.

230.3

(vi) The need to document a conclusion or the basis for a conclusion not readily determinable

from the documentation of the work performed or audit evidence obtained.

(vii) The audit methodology and tools used.

(viii) Timely preparation of Audit Documentation.

Question-4 Discuss the Auditor’s responsibility to provide access to his audit working papers to

Regulators and third parties.

Answer-Audit Working Paper:

1. The auditor should not provide access to working papers to any third party without

specific authority or unless there is a legal or professional duty to disclose.

2. Clause (1) of Part I of Second Schedule to the Chartered Accountants Act, 1949 states

that a Chartered Accountant in practice shall be deemed to be guilty of professional

misconduct if he discloses information acquired in the course of his professional

engagement to any person other than his client, without the consent of his client or

otherwise than as required by law for the time being in force.

3. SA 200 on “Overall Objectives of the Independent Auditor and the conduct of an audit in

accordance with Standards on Auditing also reiterates that, the auditor should respect

the confidentiality of the information obtained and should not disclose any such

information to any third party without specific authority or unless there is a legal or

professional duty to disclose .If there is a request to provide access by the regulator

based on the legal requirement,the same has to be complied with after informing the

client about the same.

4. Further, Standard on Quality Control (SQC) 1, Quality Control for Firms that Perform

Audits and Reviews of Historical Financial Information, and Other Assurance and Related

Services Engagements , provides that, unless otherwise specified by law or regulation,

audit documentation is the property of the auditor. He may at his discretion, make

portions of, or extracts from, audit documentation available to clients, provided such

disclosure does not undermine the validity of the work performed, or, in the case of

assurance engagements, the independence of the auditor or of his personnel.

5. As per SA 230, Audit documentation serves a number of additional purposes, including

the enabling the conduct of external inspections in accordance with applicable legal,

regulatory or other requirements.

Therefore, it is auditor’s responsibility to provide access to his audit working papers to

Regulators whereas it’s at auditor’s discretion, to make portions of, or extract from his

working paper to third parties.

240.1

SA 240 - THE AUDITOR’S RESPONSIBILITIES RELATING TO FRAUD IN AN AUDITOF FINANCIAL

STATEMENTS

Question-1

The Managing Director of the Company has committed a Teeming and Lading Fraud. The

amount involved has been however subsequently after the year end deposited in the company.

As a Statutory Auditor, how would you deal?

Answer

Fraud Committed by Managing Director: The Managing Director of the company has committed a

Teeming and Lading fraud. The fact that the amount involved has been subsequently deposited

after the year end is not important because the auditor is required to perform his responsibilities

as laid down in SA 240, The Auditor’s responsibilities relating to Fraud in an Audit of Financial

Statements . First of all, as per SA 240, the auditor needs to perform procedures whether the

financial statements are materially misstated. Because an instance of fraud cannot be considered

as an isolated occurrence and it becomes important for the auditor to perform audit procedures

and revise the audit risk assessment. Secondly, the auditor needs to consider the impact of fraud

on financial statements and its disclosure in the audit report. Thirdly, the auditor should

communicate the matter to the Chairman and Board of Directors. Finally, in view of the fact that

the fraud has been committed at the highest level of management, it affects the reliability of audit

evidence previously obtained since there is a genuine doubt about representations of

management.

Further, as per section 143(12) of the Companies Act, 2013, if an auditor of a company, in the

course of the performance of his duties as auditor, has reason to believe that an offence

involving fraud is being or has been committed against the company by officers or employees of

the company, he shall immediately report the matter to the Central Government within 60 days

of his knowledge and after following the prescribed procedure.

Question-2

As a Statutory Auditor, how would you deal with the following?

While auditing accounts of a public limited company for the year ended 31st March 2014, an

auditor found out an error in the valuation of inventory, which affects the financial statement

materially – Comment as per standards on auditing.

Answer

Errors in Valuation of Inventories and Auditor’s Responsibilities: SA 240, The Auditor’s

Responsibilities Relating Fraud in an Audit of Financial Statements , requires that if circumstances

240.2

indicate the possible existence of fraud or error, the auditor should consider the potential effect

of the suspected fraud or error on the financial information.

If the auditor believes the suspected fraud or error could have a material effect on the financial

information, he should perform such modified or additional procedures as he determines to be

appropriate.

SA 240 also requires that when the auditor identifies a misstatement, the auditor shall evaluate

whether such a misstatement is indicative of fraud.

If there is such an indication, the auditor shall evaluate the implications of the misstatement in

relation to other aspects of the audit, particularly the reliability of management representations,

recognizing that an instance of fraud is unlikely to be an isolated occurrence.

The auditor should consider requesting the management to adjust the financial information

or consider extending his audit procedures. If the management refuses to adjust the financial

information and the results of extended audit procedures do not enable the auditor to conclude

that the aggregate of uncorrected misstatements is not material, the auditor should express a

qualified or adverse opinion, as appropriate. In the instant case, the auditor has detected the

material errors affecting the financial statements; the auditor should communicate his findings to

the management on a timely basis, consider the implications on true and fair view and also ensure

that appropriate disclosures have been made.

Question-3

M/s Honest Limited has entered into a transaction on 5th March, 2014, near year-end, whereby

it has agreed to pay ` 5 lakhs per month to Mr. Y as annual retainer-ship fee for "engineering

consultation". No amount was actually paid, but ` 60 lakhs is provided in books of account as on

March 31, 2014.

Your inquiry elicits a response that need-based consultation was obtained round the year, but

there is no documentary or other evidence of receipt of the service. As the auditor of M/s

Honest Limited, what would be your approach?

Answer

As per SA 240 on The Auditor’s Responsibilities Relating to Fraud in an Audit of Financial

Statements , fraud can be committed by management overriding controls using such

techniques as Recording fictitious journal entries, particularly close to the end of an accounting

period, to manipulate operating results or achieve other objectives.

Keeping in view the above, it is clear that Company has passed fictitious journal entries near year

end to manipulate the operating results. Also Auditor’s enquiry elicited a response that

need-based consultation was obtained round the year, but there is no documentary or other

evidence of receipt of the service, is not acceptable.

Accordingly, the auditor would adopt the following approach-

240.3

Consider whether such a misstatement is an indication of Fraud. If Fraud identified-

Further, as per section 143(12) of the Companies Act, 2013, if an auditor of acompany, in

the course of the performance of his duties as auditor, has reason to believe that an offence

involving fraud is being or has been committed against the company by officers or employees of

the company, he shall immediately report the matter to the Central Government within 60

days of his knowledge and after following the prescribed procedure.

Question-4

In the course of audit of K Ltd., its auditor Mr. 'N' observed that there was a special audit

conducted at the instance of the management on a possible suspicion of a fraud and requested

for a copy of the report to enable him to report on the fraud aspects. Despite many reminders it

was not provided.In absence of the special audit report, Mr. 'N' insisted that he be provided

with at least a written representation in respect of fraud on/by the company. For this request

also, the management remained silent. Please guide Mr. 'N'.

Answer

Auditors Responsibilities Relating to Fraud: As per SA 240, The Auditor’s Responsibilities relating

to Fraud in an Audit of Financial Statements , the primary responsibility for the prevention and

detection of fraud rests with both those charged with governance of the entity and management.

In addition an auditor conducting anaudit in accordance with SAs is responsible for obtaining

reasonable assurance that the financial statements taken as a whole are free from material

misstatement, whether caused by fraud or error.

The risk of not detecting a material misstatement resulting from fraud is higher than the risk of

not detecting one resulting from error. This is because fraud may involve sophisticated and

carefully organized schemes designed to conceal it, such as forgery, deliberate failure to record

transactions, or intentional misrepresentations being made to the auditor.

As per SA 580, Written Representations , if management modifies or does not provide the

requested written representations, it may alert the auditor to the possibility that one or more

significant issues may exist. Further, If management does not provide one or more of the

requested written representations, the auditor shall discuss the matter with management; re-

evaluate the integrity of management and evaluate the effect that this may have on the reliability

of representations (oral or written) and audit evidence in general; and take appropriate actions,

including determining the possible effect on the opinion in the auditor’s report.

Communicate to Mngt. &TCWG(and to Regulatory

and Enforcement authorities, if required by Law)

Auditor unable to complete

Consider the Possibility of

If withdraw: Discuss with

240.4

In the instant case, in the course of audit of K Ltd., its auditor Mr. N observed that there was a

special audit conducted at the instance of the management on a possible suspicion of

fraud. Therefore, the auditor requested for special audit report, which was not provided by the

management despite of many reminders. Mr. N also insisted for written representation in respect

of fraud on/by the company. For this request also management remained silent.

Hence, the fact is required to be reported and the auditor should also disclaim an opinion on the

financial statements.

Question-5

In the course of audit of A Ltd you suspect the management has indulged in fraudulent

financial reporting? State the possible source of such fraudulent financial reporting.

Answer

As per SA 240, , Fraudulent financial reporting involves intentional misstatements or

omissions of amounts or disclosures in financial statements to deceive financial statement

users. It may be accomplished by manipulation, falsification, or alteration of accounting records or

supporting documents from which the financial statements are prepared or Misrepresentation in,

or intentional omission from, the financial statements of events, etc.

It often involves management override of controls, misappropriation of assets etc that

otherwise may appear to be operating effectively. Fraud can be committed by management

overriding controls using such techniques as:

(1) Recording fictitious journal entries, particularly close to the end of an accounting period, to

manipulate operating results or achieve other objectives.

(2) Inappropriately adjusting assumptions and changing judgments used to estimate account

balances.

(3) Omitting, advancing or delaying recognition in the financial statements of events and

transactions that have occurred during the reporting period.

(4) Concealing, or not disclosing, facts that could affect the amounts recorded in the

financial statements.

(5) Engaging in complex transactions that are structured to misrepresent the financial

position or financial performance of the entity.

(6) Altering records and terms related to significant and unusual transactions.

(7) Embezzling receipts (for example, misappropriating collections on accounts receivable or

diverting receipts in respect of written-off accounts to personal bank accounts).

(8) Stealing physical assets or intellectual property (for example, stealing inventory for

personal use or for sale, stealing scrap for resale, colluding with a competitor by

disclosing technological data in return for payment).

(9) Causing an entity to pay for goods and services not received (for example, payments to

fictitious vendors, kickbacks paid by vendors to the entity’s purchasing agents in return for

inflating prices, payments to fictitious employees).

Question-6

240.5

Explain briefly duties and responsibilities of an auditor in case of material misstatement

resulting from Management Fraud.

Answer

As per SA 240 The Auditor’s Responsibilities Relating to Fraud in an Audit of Financial

Statements , the primary responsibility for the prevention and detection of fraud rests with both

those charged with governance of the entity and management.

The auditor, conducting an audit, is responsible for obtaining reasonable assurance that the

financial statements taken as a whole are free from material misstatement, whether caused by

fraud or error.

Owing to the inherent limitations of an audit, there is an unavoidable risk that some material

misstatements of the financial statements may not be detected, even though the audit is properly

planned and performed in accordance with the SAs.

The risk of not detecting a material misstatement resulting from fraud is higher than the risk of

not detecting one resulting from error. This is because fraud may involve sophisticated and

carefully organized schemes designed to conceal it, such as forgery, deliberate failure to record

transactions, or intentional misrepresentations being made to the auditor. Such attempts at

concealment may be even more difficult to detect when accompanied by collusion. Collusion may

cause the auditor to believe that audit evidence is persuasive when it is, in fact, false.

Furthermore, the risk of the auditor not detecting a material misstatement resulting from

management fraud is greater than for employee fraud, because management is frequently in a

position to directly or indirectly manipulate accounting records, present fraudulent financial

information or override control procedures designed to prevent similar frauds by other

employees.

When obtaining reasonable assurance, the auditor is responsible for maintaining professional

skepticism throughout the audit, considering the potential for management override of

controlsand recognizing the fact that audit procedures that are effective for detecting error may

not be effective in detecting fraud.

Question-7

Comment on the following: While conducting statutory Audit of ABC Ltd., you come across IOUs

amounting to Rs. 2 crores as against a cash balance shown in books of Rs. 2.10 crores. You also

observe that despite similar high balances throughout the year, small amounts of Rs. 50,000 are

withdrawn from the bank to meet day-to-day expenses. [May 09 - New (5 marks)]

Answer

According to SA 240 "Auditors responsibilities relating to Fraud in an audit of financial

statements", when the auditor comes across such circumstances indicating the possible

misstatements resulting from entity's procedure, the auditor shall evaluate whether such a

misstatement is indicative of fraud.

240.6

In this case, the circumstances indicate the possibility of fraud and accordingly, the] auditor must

investigate further to consider effect on financial statements.

The Guidance Note on Audit of Cash and Bank balances also mentions that if the entity is

maintaining an unduly large balance of cash, he should carry out surprise verification of cash more

frequently to ascertain whether it agrees. If cash in hand is not in agreement with the book

balance, he should seek explanations and if the same are not satisfactory, he should state this fact

appropriately in his Audit Report.

Question-8

You notice a misstatement resulting from fraud or suspected fraud during the audit and

conclude that it is not possible to continue the performance of audit. As a Statutory Auditor,

how would you deal?

Answer

Impossibility to continue the performance of audit:According to SA 240 The Auditor’s

Responsibilities Relating to Fraud in an Audit of Financial Statements , if, as a result of a

misstatement resulting from fraud or suspected fraud, the auditor encounters exceptional

circumstances that bring into question the auditor’s ability to continue performing the audit, the

auditor shall: 1. Determine the professional and legal responsibilities applicable in the circumstances, including

whether there is a requirement for the auditor to report to the person or persons who made

the audit appointment or, in some cases, to regulatory authorities;

2. Consider whether it is appropriate to withdraw from the engagement, where withdrawal from

the engagement is legally permitted; and 3. If the auditor withdraws: a. Discuss with the appropriate level of management and those charged with governance,

the auditor’s withdrawal from the engagement and the reasons for the withdrawal; and

b. Determine whether there is a professional or legal requirement to report to the person

or persons who made the audit appointment or, in some cases, to regulatory authorities, the

auditor’s withdrawal from the engagement and the reasons for the withdrawal. Question-9

As a Statutory Auditor, How would you deal with the following?

"While auditing accounts of a public limited company for the year ended 31st march 2012, an

auditor found out an error in the valuation of inventory, which affects the financial Statement

materially - comment as per standards on auditing." (RTP Nov 2013)

Answer

(1) SA 240 requires that if circumstances indicate the possible existence of fraud or error, the

auditor should consider the potential effect of the suspected fraud or error on the financial

information.

240.7

(2) If the auditor believes the suspected fraud or error could have a material effect on the financial

information, he should perform such modified or additional procedures as he determines to be

appropriate.

(3) SA 240 also requires that whence auditor identifies a misstatement, the auditor shall evaluate

whether such a misstatement is indicative of fraud.

(4) If there is such an indication, the auditor shall evaluate the implications of the misstatement in

relation to other aspects of the audit, particularly the reliability of management

representations, recognising that an instance of fraud is unlikely to be an isolated occurrence.

(5) Further, SA 320 Materiality in Planning and Performing an Audit, also requires that in such

circumstances, the auditor should consider requesting the management to adjust the financial

information or consider extending his audit procedures.

(6) If the management refuses to adjust the financial information and the results of extended audit

procedures do not enable the auditor to conclude that the aggregate of uncorrected

misstatements is not material, the auditor should express a qualified or adverse opinion, as

appropriate.

(7) In the instant case, the auditor has detected the material errors affecting the financial

statements; the auditor should communicate his findings to the management on a timely basis,

consider the implications on true and fair view and also ensure that appropriate disclosures

have been made.

Question-10

As a Statutory Auditor, how would you deal with a misstatement resulting from fraud or

suspected fraud during the audit and conclude that it is not possible to continue the

performance of audit. (RTP)

Question-11

Is it appropriate for the auditor to make inquires of management regarding management’s own

assessment of the risk of fraud and the controls in place to prevent and detect it? Discuss.

Answer

Auditor to make Inquiries regarding Management’s own Assessment of Risk of Fraud and

Controls: As per SA 240 The Auditor’s Responsibilities Relating to Fraud in an Audit of Financial

Statements , management accepts responsibility for the entity’s internal control and for the

preparation of the entity’s financial statements. Accordingly, it is appropriate for the auditor to

make inquiries of management regarding management’s own assessment of the risk of fraud and

the controls in place to prevent and detect it. The nature, extent and frequency of management’s

assessment of such risk and controls may vary from entity to entity.

240.8

In some entities, management may make detailed assessments on an annual basis or as part of

continuous monitoring. In other entities, management’s assessment may be less structured and

less frequent. The nature, extent and frequency of management’s assessment are relevant to the

auditor’s understanding of the entity’s control environment. For example, the fact that

management has not made an assessment of the risk of fraud may in some circumstances be

indicative of the lack of importance that management places on internal control.

The auditor’s inquiries of management may provide useful information concerning the risks of

material misstatements in the financial statements resulting from employee fraud. However, such

inquiries are unlikely to provide useful information regarding the risks of material misstatement in

the financial statements resulting from management fraud.

Management is often in the best position to perpetrate fraud. Accordingly, when evaluating

management’s responses to inquiries with an attitude of professional skepticism, the auditor may

judge it necessary to corroborate responses to inquiries with other information.

Question 12

The Managing Director of the Company has committed a Teeming and Lading Fraud. The

amount involved has been however subsequently after the year end deposited in the company.

As a Statutory Auditor, how would you deal?

Answer-Fraud Committed by Managing Director: The Managing Director of the company has

committed a Teeming and Lading fraud. The fact that the amount involved has been

subsequently deposited after the year end is not important because the auditor is required to

perform his responsibilities as laid down in SA 240, The Auditor’s responsibilities relating to Fraud

in an Audit of Financial Statements . First of all, as per SA 240, the auditor needs to perform

procedures whether the financial statements are materially misstated. Because an

instance of fraud cannot be considered as an isolated occurrence and it becomes important for

the auditor to perform audit procedures and revise the audit risk assessment. Secondly, the

auditor needs to consider the impact of fraud on financial statements and its disclosure in

the audit report. Thirdly, the auditor should communicate the matter to the Chairman and

Board of Directors. Finally, in view of the fact that the fraud has been committed at the highest

level of management, it affects the reliability of audit evidence previously obtained since thereis a

genuine doubt about representations of management. Further, as per section 143(12) of the

Companies Act, 2013, if an auditor of a company, in the course of the performance of his duties as

auditor, has reason to believe that an offence involving fraud is being or has been committed

against the company by officers or employees of the company, he shall immediately report the

matter to the Central Government (in case amount of fraud is 1 crore or above)or Audit

Committee or Board in other cases (in case the amount of fraud involved in less than 1 crore)

within such time and in such manner as may be prescribed.

The auditor is also required to report as per Clause (x) of Paragraph 3 of CARO, 2016,

Whether any fraud by the company or any fraud on the company by its officers or employees

has been noticed or reported during the year; If yes, the nature and the amount involved is to

be indicated.

Question 13

240.9

In the course of audit of A Ltd. you suspect the management has indulged in fraudulent

financial reporting. State the possible source of such fraudulent financial reporting.

Answer

Possible Sources of Fraudulent Financial Reporting: As per SA 240, The Auditor’s responsibilities

relating to Fraud in an Audit of Financial Statements , fraudulent financial reporting involves

intentional misstatements or omissions of amounts or disclosures in financial statements to

deceive financial statement users. It may be accomplished by manipulation, falsification, or

alteration of accounting records or supporting documents from which the financial statements are

prepared or Misrepresentation in, or intentional omission from, the financial statements of

events, transactions or other significant information or intentional misstatements involve

intentional misapplication of accounting principles relating to measurement, recognition,

classification, presentation, or disclosure etc.It often involves management override of controls,

misappropriation of assets etc that otherwise may appear to be operating effectively. Fraud can

be committed by management overriding controls using such techniques as:

(i) Recording fictitious journal entries, particularly close to the end of an accounting period,

to manipulate operating results or achieve other objectives.

(ii) Inappropriately adjusting assumptions and changing judgments used to estimate account

balances.

(iii) Omitting, advancing or delaying recognition in the financial statements of events and

transactions that have occurred during the reporting period.

(iv) Concealing, or not disclosing, facts that could affect the amounts recorded in the financial

statements.

(v) Engaging in complex transactions that are structured to misrepresent the financial position or

financial performance of the entity.

(vi) Altering records and terms related to significant and unusual transactions.

(vii) Embezzling receipts (for example, misappropriating collections on accounts receivable or

diverting receipts in respect of written-off accounts to personal bank accounts).

(viii) Stealing physical assets or intellectual property (for example, stealing inventory for personal

use or for sale, stealing scrap for resale, colluding with a competitor by disclosing technological

data in return for payment).

(ix) Causing an entity to pay for goods and services not received (for example, payments to

fictitious vendors, kickbacks paid by vendors to the entity’s purchasing agents in return

for inflating prices, payments to fictitious employees).

(x) Using an entity’s assets for personal use (for example, using the entity’s assets as collateral for

a personal loan or a loan to a related party).

Question-14

You are appointed as an auditor of Global Ltd. Explain the risk factors relating to misstatements

arising from misappropriation of assets.

Answer

(a) Risk Factors Relating to Misstatements Arising from Misappropriation of Assets:

As per SA 240, The Auditor’s Responsibilities Relating to Fraud in audit of Financial Statements ,

misappropriation of assets involves the theft of an entity’s assets and is often perpetrated by

240.10

employees in relatively small and immaterial amounts. However, it can also involve management

who are usually more able to disguise or conceal misappropriations in ways that are difficult to

detect. Risk factors that relate to misstatements arising from misappropriation of assets are

classified according to the three conditions generally present when fraud exists:

incentives/pressures, opportunities, and attitudes/rationalization. The following are examples of

risk factors related to misstatements arising from misappropriation of assets:

Incentives/Pressures: Personal financial obligations may create pressure on management or

employees with access to cash or other assets susceptible to theft to misappropriate those assets.

Adverse relationships between the entity and employees with access to cash or other assets

susceptible to theft may motivate those employees to misappropriate those assets. For example,

adverse relationships may be created by the following:

1. Known or anticipated future employee layoffs.

2. Recent or anticipated changes to employee compensation or benefit plans.

3. Promotions, compensation or other rewards inconsistent with expectations. Opportunities:

Certain characteristics or circumstances may increase the susceptibility of assets to

misappropriation. For example, opportunities to misappropriate assets increase when there are

the following:

Inventory items that are small in size, of high value, or in high demand.

Fixed assets which are small in size, marketable, or lacking observable identification of

ownership.

Inadequate internal control over assets may increase the susceptibility of misappropriation

of those assets.

Inadequate segregation of duties or independent checks.

Attitudes/Rationalizations

Disregard for the need for monitoring or reducing risks related to misappropriations of

assets.

Disregard for internal control over misappropriation of assets by overriding existing

controls or by failing to take appropriate remedial action on known deficiencies in internal

control.

Behavior indicating displeasure or dissatisfaction with the entity or its treatment of the

employee.

Changes in behavior or lifestyle that may indicate assets have been misappropriated.

250.1

SA 250 - CONSIDERATIONS OF LAW AND REGULATIONS IN AN AUDIT OFFINANCIAL

STATEMENTS

Question-1

As a statutory auditor of a company, comment on the following:

While verifying the employee records in a company, it was found that a major portion of the

Labour employed was child labour. On questioning the management, the auditor was told that

it was outside his scope of the financial audit to look into the compliance with other laws.

Question-2

State the reporting responsibility of an auditor in the context of non-compliance of Law and

Regulation in an audit of Financial Statement.

Answer

Reporting responsibility of an auditor in the context of non-compliance of Law and

Regulation: According to SA 250 Consideration of Laws and Regulations in an Audit of

Financial Statements , the reporting responsibilities of an Auditor may be divided into the

following categories-

Reporting Non-Compliance to Those Charged with Governance: Unless all of those

charged with governance are involved in management of the entity, and therefore are aware of

matters involving identified or suspected non-compliance already communicated by the

auditor, the auditor shall communicate with those charged with governance matters involving

non-compliance with laws and regulations that come to the auditor’s attention during

the course of the audit, other than when the matters are clearly inconsequential.

If, in the auditor’s judgment, the non-compliance referred above is believed to be intentional

and material, the auditor shall communicate the matter to those charged with governance as

soon as practicable.

If the auditor suspects that management or those charged with governance are involved in

non-compliance, the auditor shall communicate the matter to the next higher level of authority

at the entity, if it exists, such as an audit committee or supervisory board. Where no higher

authority exists, or if the auditor believes that the communication may not be acted upon or is

unsure as to the person to whom to report, the auditor shall consider the need to obtain legal

advice.

Reporting Non-Compliance in the Auditor’s Report on the Financial Statements: If the auditor

concludes that the non-compliance has a material effect on the financial statements, and has

not been adequately reflected in the financial statements, the auditor shall, in accordance with

SA 705 express a qualified or adverse opinion on the financial statements.

250.2

If the auditor is precluded by management or those charged with governance from obtaining

sufficient appropriate audit evidence to evaluate whether non-compliance that may be material

to the financial statements has, or is likely to have, occurred, the auditor shall express a

qualified opinion or disclaim an opinion on the financial statements on the basis of a limitation

on the scope of the audit in accordance with SA 705.

If the auditor is unable to determine whether non-compliance has occurred because of

limitations imposed by the circumstances rather than by management or those charged with

governance, the auditor shall evaluate the effect on the auditor’s opinion in accordance with SA

705.

Reporting Non-Compliance to Regulatory and Enforcement Authorities: If the auditor has

identified or suspects non-compliance with laws and regulations, the auditor shall determine

whether the auditor has a responsibility to report the identified or suspected non-compliance

to parties outside the entity.

Question-3

R & M Co. wants to be alert on the possibility of non-compliance with 5 Laws and Regulations during

the course of audit of SRS Ltd, R &. M Co. seeks your guidance for identifying the indications of non

compliance with Laws and Regulations.(May-16)

Answer

As per SA 250, Consideration of Laws and Regulations, the auditor shall perform the audit

procedures to help identify instances of non-compliance with other laws and regulations that

may have a material effect on the financial statements by inquiring of management and, where

appropriate, those charged with governance, as to whether the entity is in compliance with

such laws and regulations; and Inspecting correspondence, if any, with the relevant licensing or

regulatory authorities.

However, when the auditor becomes aware of the existence of, or information about, the

following matters, it may also be an indication of non-compliance with laws and regulations:

(i) Investigations by regulatory organisations and government departments or payment of

fines or penalties.

(ii) Payments for unspecified services or loans to consultants, related parties, employees or

government employees.

(iii) Sales commissions or agent’s fees that appear excessive in relation to those ordinarily

paid by the entity or in its industry or to the services actually received.

(iv) Purchasing at prices significantly above or below market price.

(v) Unusual payments in cash, purchases in the form of cashiers’ cheques payable to bearer

or transfers to numbered bank accounts.

(vi) Unusual payments towards legal and retainership fees.

(vii) Unusual transactions with companies registered in tax havens.

(viii) Payments for goods or services made other than to the country from which the goods or

services originated.

(ix) Payments without proper exchange control documentation.

(x) Existence of an information system which fails, whether by design or by accident, to

provide an adequate audit trail or sufficient evidence.

250.3

(xi) Unauthorised transactions or improperly recorded transactions.

(xii)Adverse media comment.

260.1

Standard on Auditing (SA) 260 (Revised)

Communication with Those Charged with Governance

Question-1

The auditors should communicate audit matters of governance interest arising from the audit

of financial statements with those charged with the governance of an entity . Briefly state the

matters to be included in such Communication.

Answer

Communications of audit matters with those charged with governance: As per SA 260

Communication with those Charged with Governance , the auditor shall communicate with

those charged with governance, the responsibilities of the auditor in relation to the financial

statement audit, including that:

(i) The auditor is responsible for forming and expressing an opinion on the financial

statements that have been prepared by management with the oversight of those charged

with governance; and

(ii) The audit of the financial statements does not relieve management or those charged with

governance of their responsibilities.

The auditor shall communicate with those charged with governance the following:

a) The auditor’s views about significant qualitative aspects of the entity’s accounting

practices, including accounting policies, accounting estimates and financial statement

disclosures. When applicable, the auditor shall explain to those charged with governance why

the auditor considers a significant accounting practice, that is acceptable under the applicable

financial reporting framework, not to be most appropriate to the particular circumstances

of the entity;

b) Significant difficulties, if any, encountered during the audit;

c) Unless all of those charged with governance are involved in managing the entity:

(i) Significant matters, if any, arising from the audit that were discussed, or subject to

correspondence with management; and

(ii) Written representations the auditor is requesting; and

d) Other matters, if any, arising from the audits that, in the auditor’s professional judgment, are

significant to the oversight of the financial reporting process.

Question-2

Write short notes on the following: (Nov 2010)

Factors governing modes of communication of auditor with those charged with governance.

Applicable Standard: SA 260, "Communication with Those Charge with Governance"

Answer:

260.2

As per SA 260, the auditor may decide whether to communicate orally or in writing, the extent of

detail or summarization in the communication, and whether to communicate in a structured or

unstructured manner) may be affected by such factors as:

Size, operating structure, control environment, & legal structure of entity.

In the case of an audit of special purpose F.S., whether the auditor also audits the entity’s

general purpose F. S.

Requirements of respective law specifying written communication with TCWG in a prescribed

form.

Expectations of TCWG, including arrangements made for periodic meetings or

communications with the auditor.

The amount of ongoing contract and dialogue the auditor has with TCWG.

Significant changes in the membership of a governing body.

265.1

SA 265

COMMUNICATING DEFICIENCIES IN INTERNAL CONTROL TO THOSE CHARGED WITH

GOVERNANCE (TCWG) & MANAGEMENT

Question -1