Specialty pharmacy: The topic that won’t

stop growing.

Grant Knowles, PharmD, CSP Ardon Health – Specialty pharmacy Vice President of Operations June 4th, 2015

Employee Benefits Planning Association

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

Overview

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

Healthcare spending (past and future)

$2,298 $2,501

$2,701 $2,915

$3,273 $3,660

$4,142

$4,702

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

• CMS. National Health Expenditure Projections 2006-2022. http://www.cms.gov/Research-Statistics-Data-and-Systems/Statistics-

Trends-and-Reports/NationalHealthExpendData/downloads/proj2012.pdf

↑53%

Bill

ion

s

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

Prescription spending (past and future)

• CMS. National Health Expenditure Projections 2010-2020. https://www.cms.gov/nationalhealthexpenddata/downloads/proj2010.pdf • CMS. National Health Expenditures Aggregate, Per Capita Amounts, Percent Distribution, and Average Annual Percent Growth: Selected

Calendar Years 1960-2009. https://www.cms.gov/nationalhealthexpenddata/downloads/tables.pdf

236 255 263 262

295 331

373

426

0

50

100

150

200

250

300

350

400

450

500↑54%

Bill

ion

s

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

$90 billion dollars in reduced spend over the last 5 years

Patent cliff – generic relief

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

Patent cliff – generic relief

• *First-time generics are subject to significant change as a result of multiple patent protections, patent litigation, pediatric or other exclusivities, at-risk launches, and delays between patent expiration and launch of first-time generics.

• IMS retail claims data [database online]. Fairfield, CT: IMS Health; 2014. http://www.imshealth.com.

Brand name (generic name) Uses Retail sales ($Mil)

Lipitor® (atorvastatin) High cholesterol 5,803

Plavix® (clopidigrel) Prevention of arterial thrombotic events 5,020

Singulair® (montelukast) Asthma, allergic rhinitis 3,823

Seroquel® (quetiapine) Schizophrenia, bipolar disorder 3,549

Actos® (pioglitazone) Type 2 diabetes 2,913

Cymbalta® (duloxetine) Depression, fibromyalgia, chronic pain, diabetic peripheral neuropathy

2,891

Lexapro® (escitalopram) Depression 2,590

Zyprexa® (olanzapine) Schizophrenia, bipolar disorder 2,114

Concerta® (methylphenidate extended-release)

ADHD 1,560

Levaquin® (levofloxacin) Bacterial infections 1,542

Diovan® (valsartan) Hypertension, CHF 1,430

Diovan HCT (valsartan/HCTZ) Hypertension 1,430

TriCor® (fenofibrate) Hypotriglyceridemia 1,123

Lidoderm® (topical patch) Post-herpetic neuralgia 1,066

Geodon® (ziprasidone) Schizophrenia 1,058

Provigil® (modafinil) Narcolepsy, idiopathic hypersomnolence 1,014

Aciphex® (rabeprazole) GERD, stomach ulcers 1,006

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

Specialty prescriptions

An undeniable and growing proportion of healthcare spend.

Defining

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

What is specialty medication?

“Certain pharmaceuticals, biotech, or biological drugs, which

may be offered by PBM*, that are used in the management of

chronic or genetic disease, including but not limited to injectable,

infused, or oral medications, or products that otherwise require special handling.”

•*PBM - Prescription Benefit Manager

•Chan, L (2009). Control Specialty Drug Cost By Making Your PBM Helpful. Managed Care.

http://www.managedcaremag.com/archives/0908/0908.specialtydrugcost.html

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

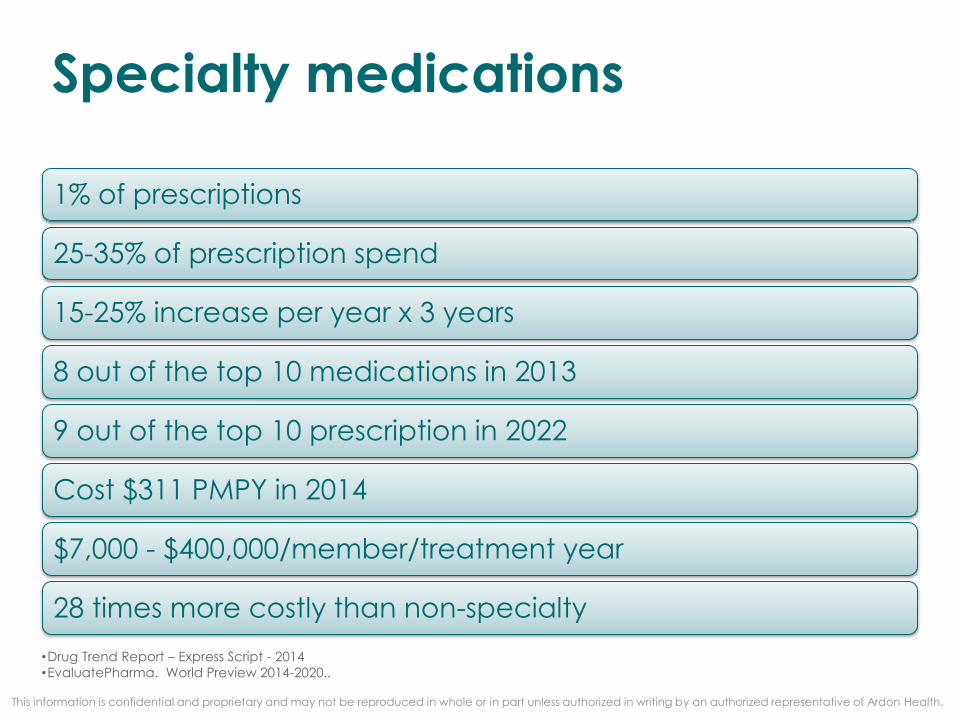

Specialty medications

•Drug Trend Report – Express Script - 2014

•EvaluatePharma. World Preview 2014-2020..

1% of prescriptions

25-35% of prescription spend

15-25% increase per year x 3 years

8 out of the top 10 medications in 2013

9 out of the top 10 prescription in 2022

Cost $311 PMPY in 2014

$7,000 - $400,000/member/treatment year

28 times more costly than non-specialty

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

Specialty Parameters

High Cost

$1,000-$40,000 per

Rx

Complex admin

Injection, infusion

Unique monitoring

REMS*, efficacy criteria

Specific climate needs

Specific storage or shipment protocol

Require additional

patient education

“high-touch” disease states,

adherence

Require 24/7

clinical support

High side-effects,

adherence assistance

Drugs not available in retail settings

LDD±

*REMS – Risk Evaluation and Mitigation Strategies ± LDD – Limit Distribution Drugs

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

How payers define specialty

43%

66%

67%

73%

71%

81%

85%

0% 20% 40% 60% 80% 100%

Requires patient admin training

Indicated for disease already

classified as specialty

Limited distribution

Requires specialty handling

Treats orphan disease

Requiring special monitoring

High Cost

• From 91 payers with over 124 million lives • EMD Serono Injectable Digest (10th Edition).

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

How payers define high cost

14%

40%

29%

17%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

<$600 $600-$800 $1000-1200 >$1,200• From 91 payers with over 124 million lives • EMD Serono Injectable Digest (10th Edition).

Past & Future

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

Spending on traditional therapies will grow at slower rates.

Specialty spend will experience hand-over-fist growth in the foreseeable future.

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

Specialty spend

$55

$124

$0

$20

$40

$60

$80

$100

$120

$140

2005 2014

$ in Billions

Specialty Spend

$1.7 trillion spend

by 2030,

estimates PCMA

•IMS - Medicines Use and Spending Shifts – April, 2015 •PCMA - Pharmaceutical Care Management Association

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

Towering trends

•Drug Trend Report 2014 – Express Script

-0.5%

3.9% 4.3%

22.6% 22.3% 21.3%

9.0% 10.3% 10.9%

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

2015 2016 2017

Traditional Specialty Overall

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

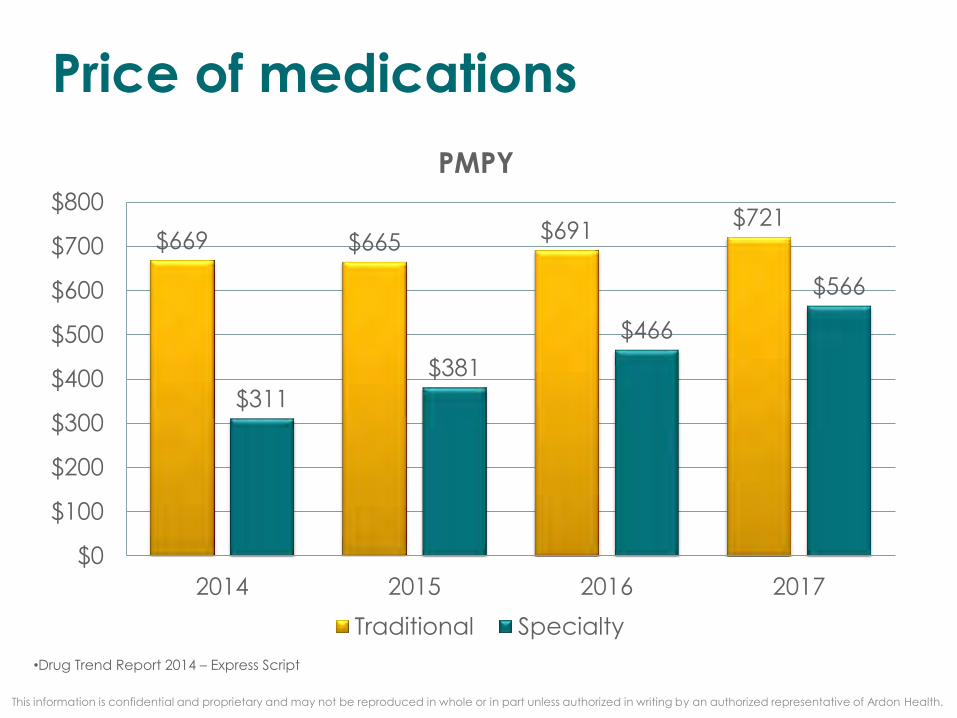

Price of medications

•Drug Trend Report 2014 – Express Script

$669 $665 $691

$721

$311

$381

$466

$566

$0

$100

$200

$300

$400

$500

$600

$700

$800

2014 2015 2016 2017

PMPY

Traditional Specialty

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

Top 10 medications in 2010

•BOLD – Indicate Specialty Medications •*Now generic products •EvaluatePharma. World Preview 2016. May 2010. Available at: http://www.windhover.com/download/blog/EP0510worldpreview2016.pdf. Accessed August 30, 2011.

Medication 2009 Sales in

Billions 2010 Sales in

Billions

1 *Plavix $5.5 $6.1

2 *Lipitor $5.6 $5.3

3 Advair $4.0 $4.0

4 *Seroquel $3.4 $3.7

5 Epogen/Procrit $3.8 $3.5

6 *Actos $3.2 $3.5

7 Abilify $3.2 $3.3

8 Enbrel $3.2 $3.3

9 *Singulair $3.0 $3.2

10 Remicade $3.0 $3.0

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

Top 10 medications in 2013

•BOLD – Indicate Specialty Medications •EvaluatePharma. World Preview 2020.

Product Generic Name Company Pharmacologic

al Class 2013 2020

1 Humira adalimumab AbbVie Anti-tumour necrosis factor alpha (TNFa) MAb

5,236 6,566

2 Lantus insulin glargine recombinant

Sanofi Insulin 4,978 6,299

3 Enbrel etanercept Amgen Tumour necrosis factor alpha (TNFa)

inhibitor

4,256 4,918

4 Remicade infliximab Johnson & Johnson Anti-tumour necrosis factor alpha (TNFa) MAb

3,891 4,594

5 Rituxan rituximab Roche Anti-CD20 MAb 3,594 2,251

6 Neulasta pegfilgrastim Amgen Granulocyte colony-stimulating factor (G-CSF)

3,499 2,640

7 Januvia/

Janumet sitagliptin phosphate

Merck & Co Dipeptidyl peptidase IV inhibitor

2,946 3,255

8 Avastin bevacizumab Roche Anti-VEGF MAb 2,780 2,130

9 Epogen/

Procrit epoetin alfa Amgen + JNJ Erythropoietin 2,748 1,502

10 Revlimid lenalidomide Celgene Immunomodulator 2,489 2,603

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

Top 10 medications in 2020

•BOLD – Indicate Specialty Medications •EvaluatePharma. World Preview 2020.

Product Generic Name

Company Pharmacological

Class 2013 2020

1 Humira adalimumab AbbVie

Anti-tumour necrosis factor alpha (TNFa) MAb

5,236 6,566

2 Lantus insulin glargine recombinant

Sanofi Insulin 4,978 6,299

3 Enbrel etanercept Amgen Tumour necrosis factor

alpha (TNFa) inhibitor 4,256 4,918

4 Remicade infliximab Johnson & Johnson

Anti-tumour necrosis factor alpha (TNFa) MAb

3,891 4,594

5 Sovaldi sofosbuvir Gilead Sciences

Hepatitis C nucleoside NS5B polymerase inhibitor

136 4,567

6 Tecfidera dimethyl fumarate

Biogen Idec

Nuclear factor

erythroid 2-related factor (Nrf2) pathway activator

864 4,175

7 Nivolumab nivolumab Bristol-Myers Squibb Anti-programmed death-1 (PD-1) MAb

- 3,618

8 Eylea aflibercept Regeneron Pharmaceuticals

VEGFr kinase inhibitor 1,409 3,583

9 Imbruvica ibrutinib Pharmacyclics Bruton's tyrosine kinase

(BTK) inhibitor 14 3,564

10 Xtandi enzalutamide Astellas Pharma Androgen receptor antagonist

442 3,337

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

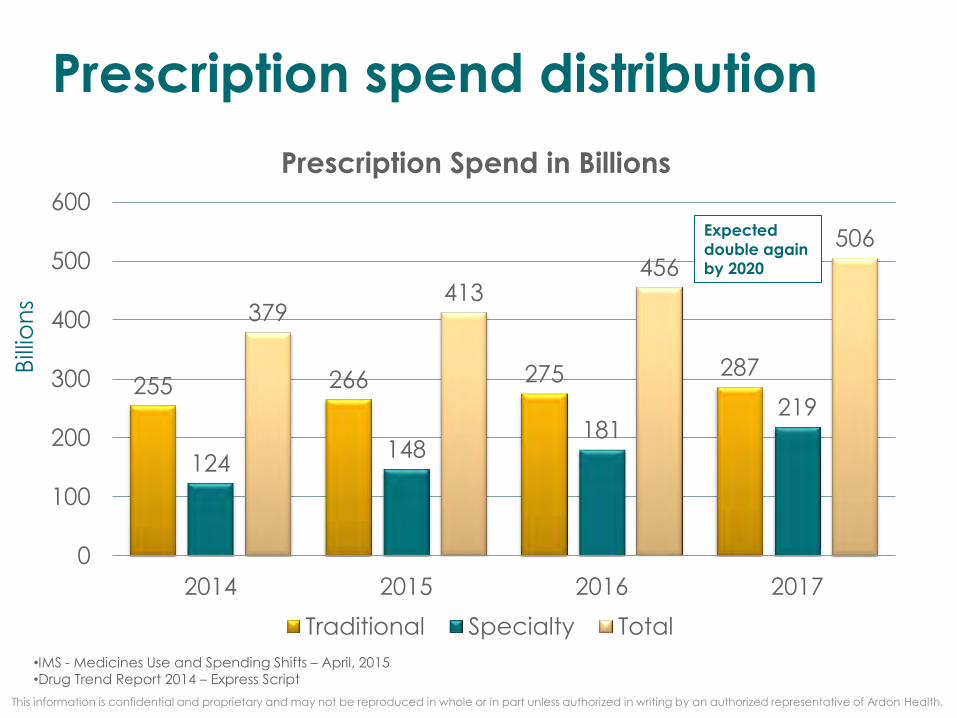

Prescription spend distribution

255 266 275 287

124 148

181 219

379 413

456

506

0

100

200

300

400

500

600

2014 2015 2016 2017

Prescription Spend in Billions

Traditional Specialty Total

•IMS - Medicines Use and Spending Shifts – April, 2015 •Drug Trend Report 2014 – Express Script

Bill

ion

s

Expected

double again

by 2020

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

Prescription spend distribution

•IMS - Medicines Use and Spending Shifts – April, 2015 •Drug Trend Report 2014 – Express Script

67%

33%

2014

Traditional Specialty

64%

36%

2015

Traditional Specialty

60%

40%

2016

Traditional Specialty

57%

43%

2017

Traditional Specialty

Why so special?

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

Why so special?

• Treatment & cures for conditions that may have had none

• Serious benefits and serious potential for side effects

• Shifting therapies to patient administered

› More home, less hospital

› Oncology

• Biologics typically do not face generic competition after their original patent

protection has expired, thus extending high prices indefinitely

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

Fueling the growth

Trend Novel mechanisms

Improved efficacy

Large patient

populations

New indications for existing

drugs

Large pipeline of new drugs

Price increases

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

Specialty pipeline

• Pharmaceutical Research and Manufacturers of America. .

• EMD Serono Specialty Digest, 10th Edition

70% FDA approvals were specialty, 2012-2013

50% of approvals in 2014

>900 biologics, for more than 100 diseases

>70% for cancer, infectious diseases, autoimmune diseases, and cardiovascular disease

37% monoclonal antibodies or therapeutic proteins (e.g. Humira, Enbrel)

Focus on small (orphan) populations (e.g. Sensipar, Soliris)

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

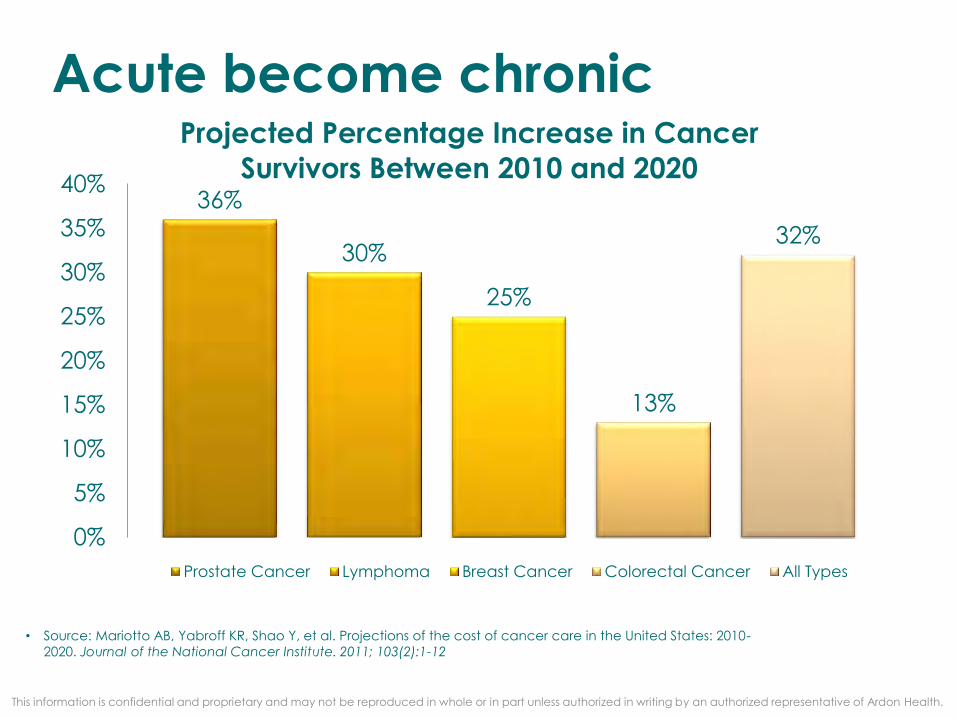

Acute become chronic

36%

30%

25%

13%

32%

0%

5%

10%

15%

20%

25%

30%

35%

40%

Projected Percentage Increase in Cancer

Survivors Between 2010 and 2020

Prostate Cancer Lymphoma Breast Cancer Colorectal Cancer All Types

• Source: Mariotto AB, Yabroff KR, Shao Y, et al. Projections of the cost of cancer care in the United States: 2010-

2020. Journal of the National Cancer Institute. 2011; 103(2):1-12

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

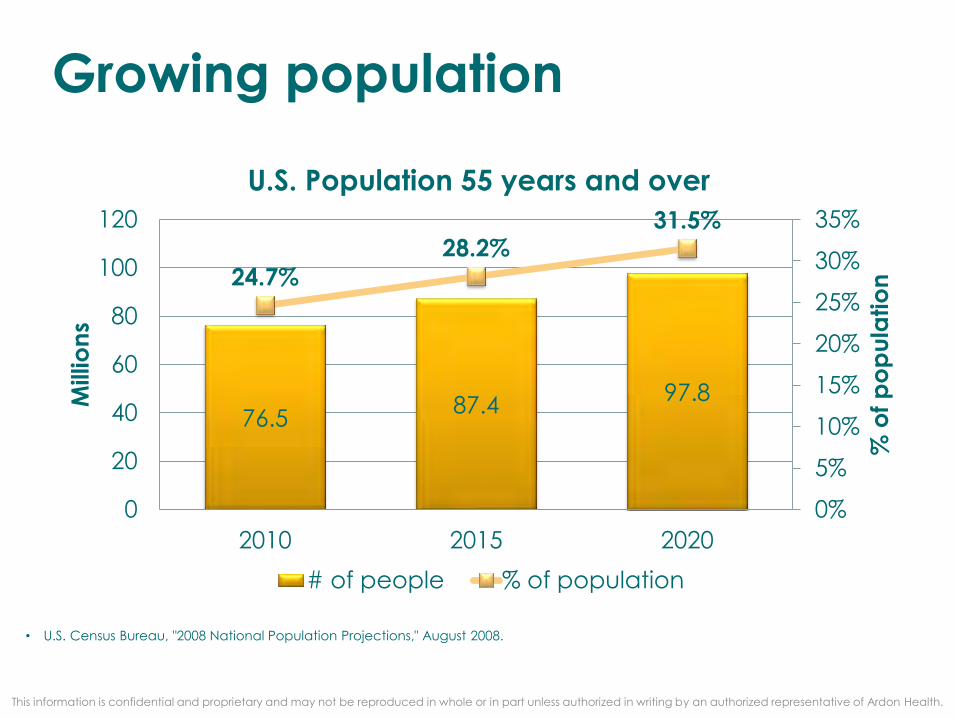

Growing population

76.5 87.4

97.8

24.7%

28.2% 31.5%

0%

5%

10%

15%

20%

25%

30%

35%

0

20

40

60

80

100

120

2010 2015 2020

% o

f p

op

ula

tio

n

Millio

ns

U.S. Population 55 years and over

# of people % of population

• U.S. Census Bureau, "2008 National Population Projections," August 2008.

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

Price increases

17.6%

9.8% 9.8% 10.5%

17.5%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%

20.0%

Copaxone Enbrel Humira Forteo Rebif

Average Annual Increase Since 2007/2008

Where’s the

generics? Trick question, there aren’t any…

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

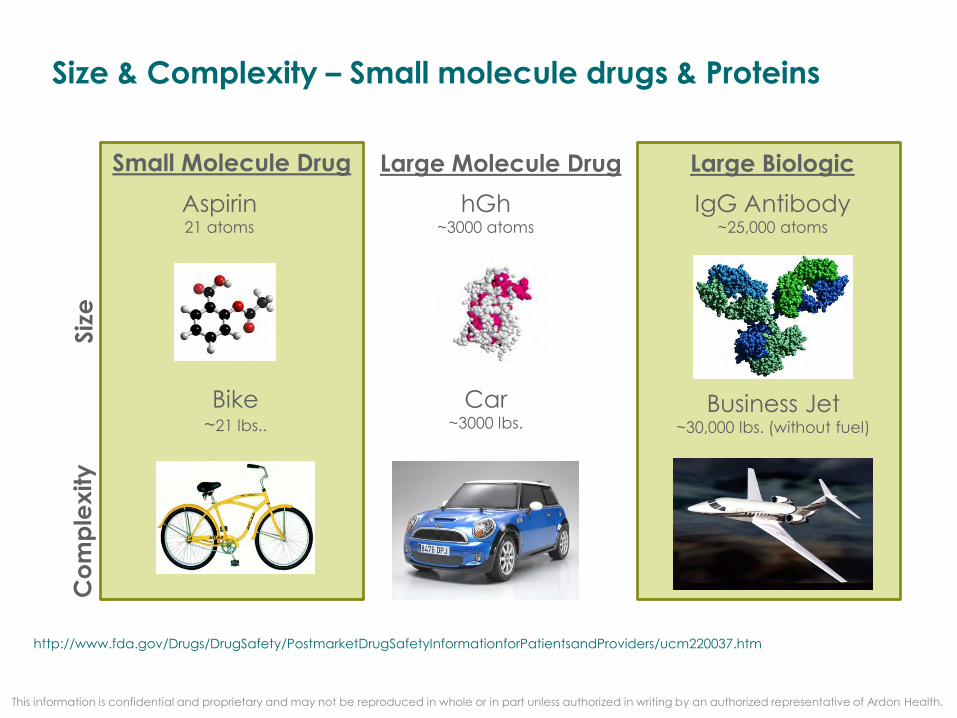

Size & Complexity – Small molecule drugs & Proteins

http://www.fda.gov/Drugs/DrugSafety/PostmarketDrugSafetyInformationforPatientsandProviders/ucm220037.htm

Siz

e

Co

mp

lex

ity

Aspirin 21 atoms

Small Molecule Drug Large Molecule Drug

Bike ~21 lbs..

hGh ~3000 atoms

Car ~3000 lbs.

Large Biologic

IgG Antibody ~25,000 atoms

Business Jet ~30,000 lbs. (without fuel)

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

Slow biosimilars slow to market

• Made available by the Patient Protection and Affordable Care

Act

• No abbreviated approval process like small molecule drugs

• Must demonstrate safety, purity, and potency to reference

product with: › Analytical Testing

› Bioassays

› Animal studies

› Human clinical studies

• FDA Purple book › No clinically meaningful differences between biologic and reference

product in terms of safety, purity, and potency

› Interchangeable biosimilars may be substituted for the reference product

by a pharmacist without intervention from the prescribing physician

• http://www.fda.gov/Drugs/DevelopmentApprovalProcess/HowDrugsareDevelopedandApproved/ApprovalApplications/TherapeuticBiologicApplications/Biosimilars/ucm411418.htm

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

Market impact - biosimilars

• Potential $44.2 billion reduction in spending from 2015 to 2024

• New competition

› Reference product (brand) will not go away

• New delivery mechanisms

› Syringe vs. Pen

› Something cooler than what is out there

• First biosimilar was approved this year

› Zarxio to compete with Neupogen

• The Cost Savings Potential of Biosimilar Drugs in the United States

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

Specialty categories

• Drug Trend Report – Express Script – 2014

• Blockbuster Drugs Fill 2015 Pipeline – March 2015

• Bold – generics or soon to be generic

Rank Therapy Class Avg. Cost/Rx Medications Rx Per 1000

1 Inflammatory

Conditions $2,913.33 Humira® , Enbrel® Stelara®, 27

2 Multiple Sclerosis $4,510.06 Copaxone®, Tecfidera®, Avonex® 12

3 Oncology $6,191.29 Gleevec®, Revlimid®,

Capecitabine, Temozolomide 7

4 Hepatitis C $16,373.40 Sovaldi®, Harvoni® 2

5 HIV $1,138.48 Atripla®, Truvada® 24

6 Misc. $4,539.50 Botox® , Xyrem® 2

7 Growth Deficiency $3,852.58 Norditropin® FlexPro®, Genotropin® 3

8 Hemophilia $7,519.16 Advate 1

9 Pulmonary Arterial

Hypertension $4,023.23 Sildenafil, Adcirca®, Tracleer® 1

10 Transplant $208.00 Azathioprine, Mycophenolate,

Tacrolimus, Prograf® 25

PCSK9 – estimates up to$100 billion annually spend

2014 specialty spend was $124 billion

Focus

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

Cancer

Anticoagulants

Hepatitis C

Specialty

Afinitor®

Zavesca®

Sutent®

Xyrem®

Xiaflex®

Tykerb®

Stelara®

Simponi®

Sprycel®

Rituxan® Revatio®

Revlimid®

Promacta®

Ilaris®

Procrit®

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

Focused industry

•Drug Trend Report 2014 – Express Script

Top 10

89%

Others

11%

% spend of

top 10

specialty

classes

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

Focus

•Drug Trend Report 2014 – Express Script

2%

2%

2%

3%

4%

9%

12%

13%

17%

26%

0% 5% 10% 15% 20% 25% 30%

Transplant

Pulmonary Arterial Hypertension

Hemophilia

Growth Deficiency

Misc. Specialty Conditions

HIV

Hepatitis C

Oncology

Multiple Sclerosis

Inflammatory Conditions

% Makeup

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

Manufacturer attention

• Blockbusters require smaller populations

› $10.3B – Sovaldi (Hepatitis C)

• Development cost of orphan drugs can be lower with a higher

anticipated return

› Avg. orphan drug cost per patient per year $137,782

› Avg. non-orphan drug cost per patient per year $20,875

• New report shows orphan drug market to reach $176 billion by 2020. EvaluatePharma. New release. October 29, 2014

• Succeeding in the rapidly changing U.S. Specialty market.

https://www.imshealth.com/deployedfiles/imshealth/Global/North%20America/United%20States/Managed%20Markets/5-29-

14%20Specialty_Drug_Trend_Whitepaper_Hi-Res.pdf

Managing

specialty

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

Determining value

Gleevec Tarceva

Displaced prior therapy and drastically improved 5-year survival

to 89% in CML

•Fojo T, Grady C. How much is life worth: cetuximab, non–small cell lung cancer, and the $440 billion question.

Journal of the National Cancer Institute. 2009;101(15):1044-1048.

•CML = chronic myeloid leukemia

Improves survival by 10 days when giving with the standard of care for pancreatic cancer.

Prior

Therapy

for CML

$43,100 per

life-year

saved

$410,000 per

life-year saved

30%, 5-year survival

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

Financial Assistance

Does cost mattes? Evidence: • 3.8% reduction in adherence for every $10 in patient cost

• Patients with a cost <$100 initiate therapy:

› 37% more than those with >$200 › 14% more than with $101-$200

• Patients using financial assistance:

› 30% more likely of achieving an medication possession rate (MPR) >80%

Non-adherence:

A $300B problem

• Non-adherence/persistence? › Not starting therapy

› Not continually staying on therapy

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

Financial Assistance

• Ardon Health financial assistance for 2015:

› Avg. medication cost: $4,652

› Avg. copay/coinsurnace: $292

› Avg. assistance: $278 › Avg. patient out-of-pocket cost: $14

Copaxone Avonex Rebif Gilenya Betaseron

Pt Cost $0 $0 $0 $0 $0

Monthly

Max $2,500 - - - -

Annual

Max $12,000 - $12,000 $12,000 $9,500

• Types of funding

› Manufacturer assistance* › Need based-assistance

› Charitable assistance

*Government programs (Medicare &

Medicaid) are not eligible for most

manufacturer assistance

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

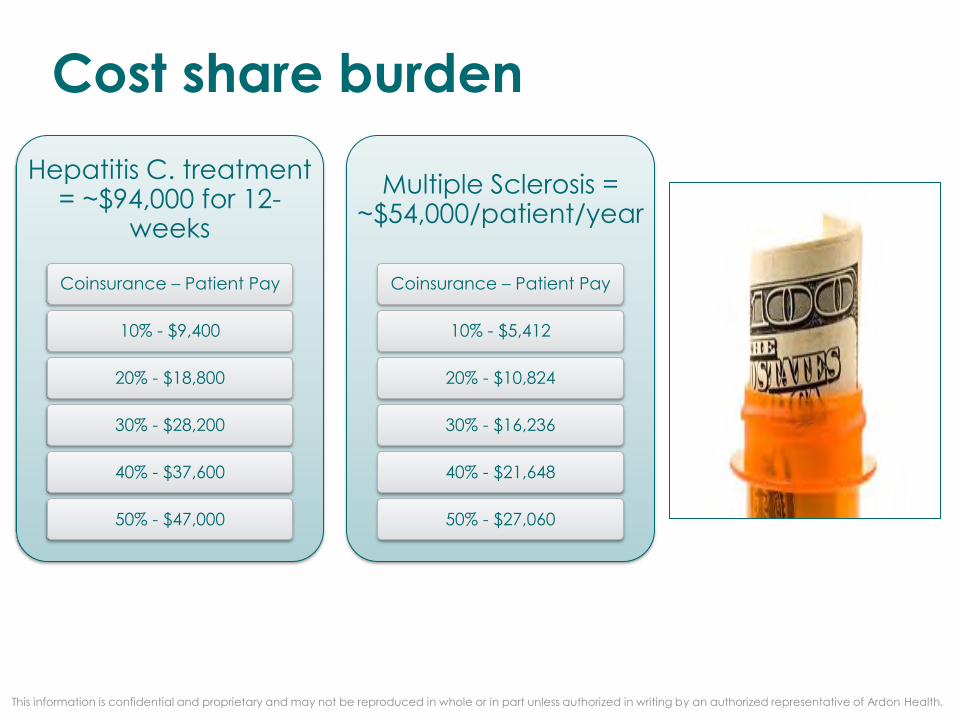

Cost share burden

Hepatitis C. treatment = ~$94,000 for 12-

weeks

Coinsurance – Patient Pay

10% - $9,400

20% - $18,800

30% - $28,200

40% - $37,600

50% - $47,000

Multiple Sclerosis = ~$54,000/patient/year

Coinsurance – Patient Pay

10% - $5,412

20% - $10,824

30% - $16,236

40% - $21,648

50% - $27,060

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

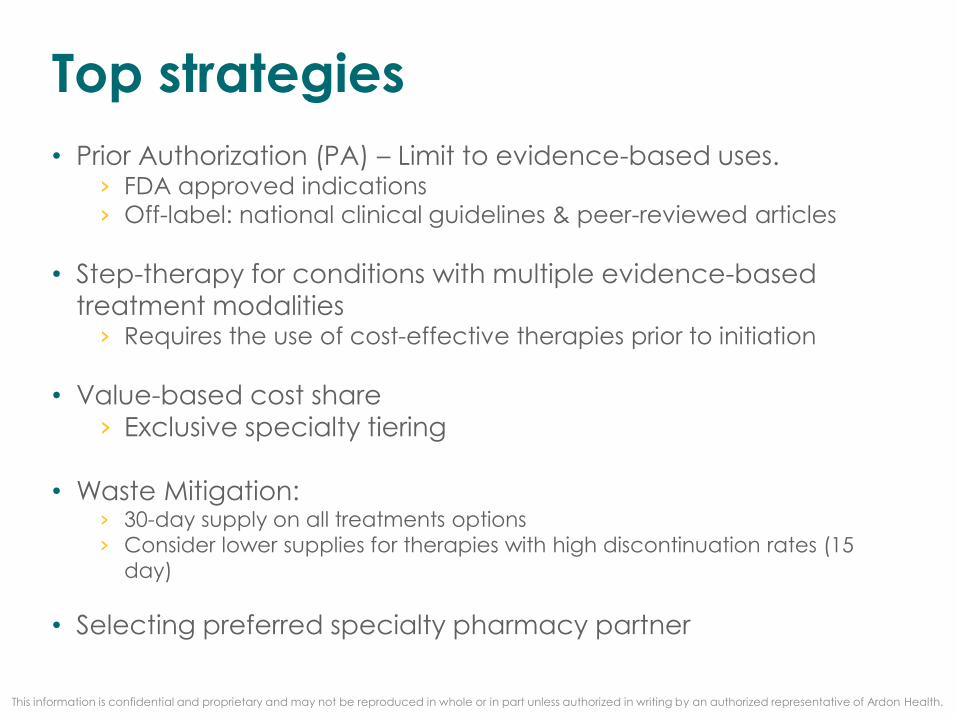

Top strategies

• Prior Authorization (PA) – Limit to evidence-based uses. › FDA approved indications

› Off-label: national clinical guidelines & peer-reviewed articles

• Step-therapy for conditions with multiple evidence-based

treatment modalities › Requires the use of cost-effective therapies prior to initiation

• Value-based cost share › Exclusive specialty tiering

• Waste Mitigation: › 30-day supply on all treatments options

› Consider lower supplies for therapies with high discontinuation rates (15

day)

• Selecting preferred specialty pharmacy partner

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

Benefit design strategies

12%

23%

30%

44%

55%

58%

94%

0% 20% 40% 60% 80% 100%

Lower cost share to improve adherence

Allow 90-day supply for stable patients

Implement value-based benefit design

Create specialty drug benefit for all drugs

Create cost share tier for specialty

Equalize cost share between RX and

medical benefits

Limit specialty products to 30-day supply

Strategies implemented or will be in 12 months

• From 91 payers with over 124 million lives • EMD Serono Injectable Digest (10th Edition).

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

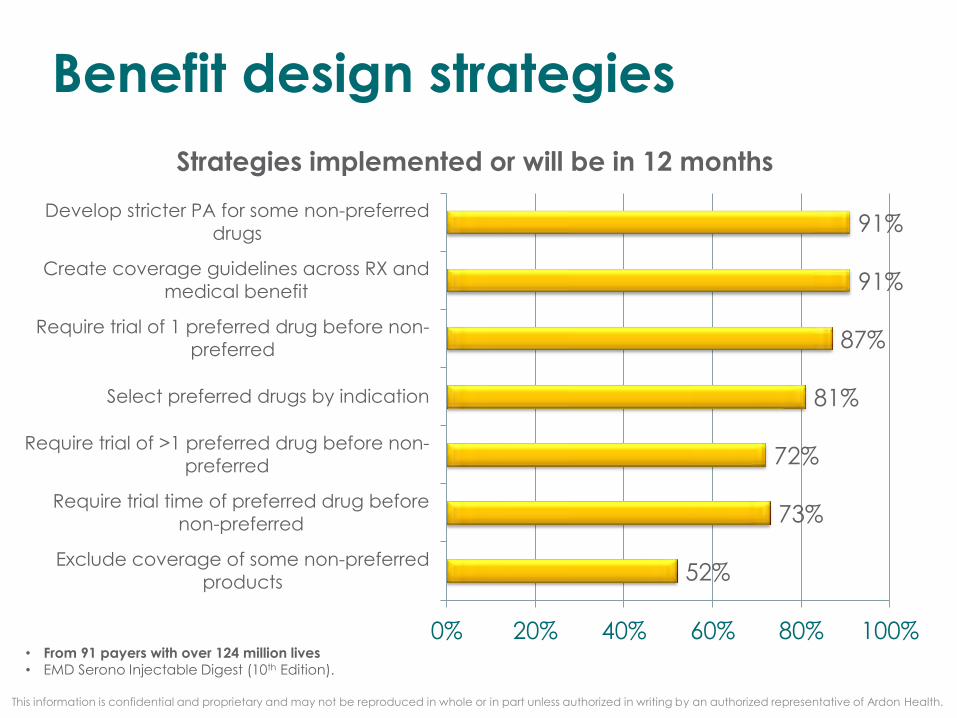

Benefit design strategies

• From 91 payers with over 124 million lives • EMD Serono Injectable Digest (10th Edition).

52%

73%

72%

81%

87%

91%

91%

0% 20% 40% 60% 80% 100%

Exclude coverage of some non-preferred

products

Require trial time of preferred drug before

non-preferred

Require trial of >1 preferred drug before non-

preferred

Select preferred drugs by indication

Require trial of 1 preferred drug before non-

preferred

Create coverage guidelines across RX and

medical benefit

Develop stricter PA for some non-preferred

drugs

Strategies implemented or will be in 12 months

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

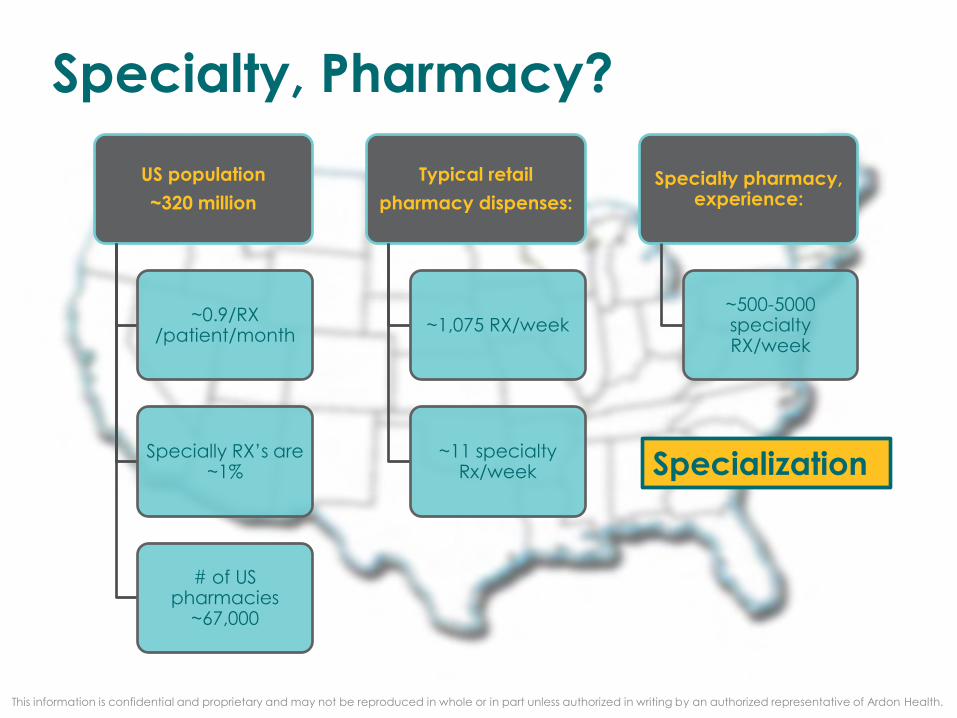

Specialty, Pharmacy?

US population

~320 million

~0.9/RX /patient/month

Specially RX’s are ~1%

# of US pharmacies

~67,000

Typical retail

pharmacy dispenses:

~1,075 RX/week

~11 specialty Rx/week

Specialty pharmacy, experience:

~500-5000 specialty RX/week

Specialization

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

Making it Right

• Specialty medication can make up 80% or more of a patient’s health care spend

• Is it appropriate to start?

• Is it appropriate to continue?

Right medication

• Is it the initiation of therapy?

• Is it continuation of therapy?

Right dose

• Is it being taken it?

• Is it at the correct frequency?

Right time

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

Sp

ec

ialty

Se

rvic

es

Proactive adherence management

Provide disease specific patient education & management

Reimbursement and eligibility coordination

Provide 24/7 access to RN or pharmacist

Preventative measures for drug waste, abuse and misuse

Ensure appropriate dose of medication

Flexible shipping distribution direct to patient’s home, business, or MD

First-level claims denial and appeals processing

Patient-assistance programs

In-office, in-home training capability

Audit capabilities

Benefit design, formulary support

Expertise in benefit investigations, prior authorization, appeals

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

Connectivity

• Connecting patient’s with support programs › Patient receiving injection training

◦ 40% more likely to have a MPR >80%

› 24/7 pharmacist support

› Advocacy groups › Medication disposal services › Case management integration

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

Continued Assessment/Counseling

• Every fill:

› Proactive refill call (at least 7 days)

› Adherence assessment

› Side effect assessment

› Appropriateness assessment

• Improved adherence

› Better outcomes

› Reduced waste

• Decreased side effects and increased knowledge

› Reduced premature discontinuation

› Reduced additional health cost

• Appropriateness check

› Proper patient outcomes

› Reduce waste

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

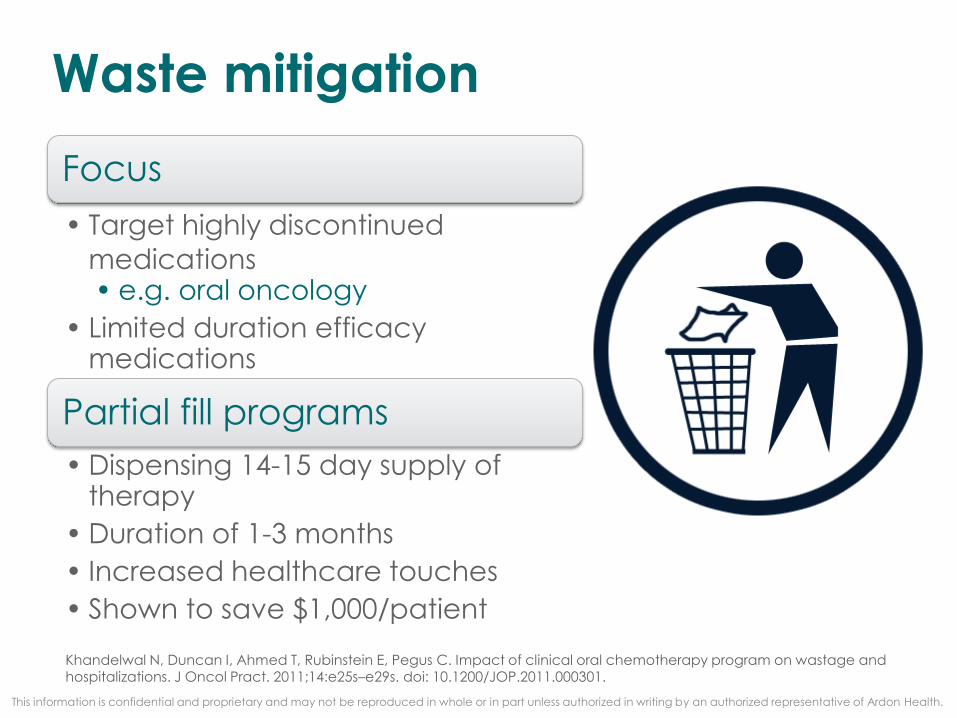

Waste mitigation

Focus

• Target highly discontinued

medications • e.g. oral oncology

• Limited duration efficacy medications

Partial fill programs

• Dispensing 14-15 day supply of therapy

• Duration of 1-3 months

• Increased healthcare touches

• Shown to save $1,000/patient

Khandelwal N, Duncan I, Ahmed T, Rubinstein E, Pegus C. Impact of clinical oral chemotherapy program on wastage and hospitalizations. J Oncol Pract. 2011;14:e25s–e29s. doi: 10.1200/JOP.2011.000301.

This information is confidential and proprietary and may not be reproduced in whole or in part unless authorized in writing by an authorized representative of Ardon Health.

Compounds

• What is a compound?

› combining, mixing, or altering ingredients of a drug to create

a medication tailored to the needs of an individual patient • What’s in the limelight?

› Topical pain compounds

• Why?

› High cost - $500-$10,000

› AWP prices have risen substantially

› No MAC pricing

› 128% increase in trend in 2014

› Intense marketing

• Can topical pain compounds be helpful?

› Limited evidence that the active ingredients, in combination, have been

evaluated by the FDA for safety and/or efficacy

› Many include 10-15 different active ingredients

◦ combining products from the same drug class.

◦ 10-20 time the commercially manufactured medication.

• What’s being done

› Restrictions on use and/or cost.

• Drug Trend Report – Express Script – 2014