SpareBank 1 Nord-Norge Preliminary accounts for 2009 – The Group

Very good result for the 4th quarter and for 2009 as a whole. The bank's financial strength is good.

Key figures (figures in parentheses refer to the same period 2008):

• Operating profit before tax after 4th quarter NOK 1,002 million (NOK 493 million).

• Return on equity after tax was 18.2 % (8.1 %).

• Earnings per equity certificate (parent bank): NOK 13.85 (NOK 4.09).

• Good underlying banking operations: result of core operations before loan losses amounted to NOK 708

million (NOK 760 million).

• Total contribution from the group's subsidiaries: NOK 8 million (- NOK 16 million).

• Net return on investment securities: NOK 479 million (- NOK 84 million).

• Profit contribution from SpareBank 1 Gruppen AS totals NOK 175 million (-NOK 151 million).

• Badwill taken to income in connection with acquisition of stake in BN Bank ASA: NOK 56 million.

Amortisation of net lesser value in connection with acquisition of BN Bank ASA: NOK 8 million.

Share of profit of BN Bank as at 4th quarter: NOK 28 million.

• Share of result of SpareBank 1 Boligkreditt: NOK 13 million.

• Net gain on bank's securities portfolio: NOK 118 million.

• Net gain on fixed interest portfolio (including related derivative trading): NOK 21 million.

• Income from other foreign exchange and financial derivatives and assets: NOK 36 million.

• Cost developments are in check, up NOK 1 million compared with 2008.

Cost ratio 45 % (59 %).

• Low losses on loans taking into account the macroeconomic situation: Net losses totalled NOK 185 million

(NOK 183 million).

• Total growth in lending last 12 months (incl. loans transferred to SpareBank 1 Boligkreditt): 4.0 % (8.0 %).

• Retail market: 8.4 % (incl. SpareBank 1 Boligkreditt).

• Corporate market: - 4.8 %.

• The accounts show a decline in lending over the last 12 months of 6.0% (+ 2.1 %).

• Growth in deposits the last 12 months: 0.9 % (7.9 %).

• Retail market: 5.7 %.

• Corporate market: - 15.1 %.

• Public sector marked: 20.2 %.

• Deposit-to-loan ratio: 72.4 % (67.4 %).

• The bank's capital strength is good and the core capital ratio (group) is 11.9% (9.1%). The total capital ratio is

14.3% (10.6%).

• Liquidity continues to be satisfactory.

• Proposed cash dividend to the equity certificate owners: NOK 6.75.

Introductory comments

The quarterly accounts are prepared in accordance with

International Financial Reporting Standards (IFRS),

including IAS 34 relating to interim account reporting.

IAS 1 – Presentation of Financial Statements – was

amended in 2009, and this results in several changes in the

presentation of the Income Statement and statement of

changes in equity. Items that are posted directly against

equity shall now also be presented in the income statement

as extended items. In the equity statement a distinction is

made between transactions between the owners and other

transactions.

IFRS calls for the use of different principles for

incorporation of subsidiaries and joint venture companies

between the parent company's accounts and the group

accounts. In the consolidated accounts, the equity method

is used, where the results of joint ventures are included in

the consolidated accounts based on the equity interest and

after taking into account the book values in the balance

sheets. The results of subsidiaries are consolidated. In

accordance with IFRS only the cost method shall be

applied in the parent company accounts. This results in the

book values of subsidiaries and joint ventures in the parent

bank's accounts being recorded at historic cost. In the

parent bank's accounts, only the annual dividends received

from these are shown.

Pursuant to the regulations issued by the Ministry of

Finance on 16 October 2008, permission was granted to

reclassify some securities in the trading portfolio from the

category "Fair value with value changes over the income

statement" to categories that are assessed at amortised cost.

The group resolved to make such reclassifications of much

of the interest-bearing portfolio held for trading as at 1

July 2008. Future assessments of these categories will be

at amortised costs with the help of the effective interest

method and taken to income as interest income over the

remaining life of the securities in question. The bank's

other holdings of certificates and bonds are classified as

"Fair value with value changes over the income

statement". To the extent that there is an active market for

the security in question, recorded market prices are used

when fixing fair values. For some parts of the portfolio

there are no recorded market values and the bank has

therefore used an alternative evaluation method pursuant

1/22

to IFRS 39 in order to ascertain a fair market value as at 31

December 2009 for the securities in question. This is

described in more detail in the principle note to the

accounts.

A consortium of SpareBank 1-banks acquired Glitnir Bank

ASA, now renamed BN Bank ASA in December 2008.

SpareBank 1 Nord-Norge then held 20 per cent of the

shares in BN Bank ASA. In this connection, SpareBank 1

Nord-Norge took to income badwill (negative goodwill)

amounting to NOK 415.4 million in its consolidated

accounts for 2008. An adjustment was made in the 4th

quarter of 2009 of original badwill, when a further NOK 9

million was taken to income.

In October 2009, SpareBank 1 Nord-Norge acquired a

further 3.5 per cent of the shares in BN Bank ASA and 3.5

per cent of the shares in SpareBank 1 Næringskreditt AS

from SpareBank 1 SMN. Subsequent to this the bank's

stake in these companies is 23.5 per cent. In connection

with the increase in the stake new badwill (negative

goodwill) was taken to income in the 4th

quarter of 2009 in

the amount of NOK 47 million.

In 2009 the difference between the bank's book value of

the share capital in BN Bank and the book value of the

equity in BN Bank's accounts is recorded (taken to

income). This is done by amortising the excess/shortfall of

purchase price over net assets value of balance sheet items

in accordance with agreed maturities for the individual

items. As at the 4th

quarter of 2009 a total of NOK 8

million has been taken to income as amortisation as a

result of last year's preliminary assessment now being

finally adopted, including the amortisation subsequent to

the bank increasing its stake in BN Bank.

Badwill is not recorded in the parent company's accounts.

Earnings development

As at the 4th

quarter of 2009, operating profit before tax

amounted to NOK 1,002 million. The corresponding profit

in 2008 was NOK 493 million. The group's core operations

(operations excluding net income from investment

securities) remain good, showing a profit before losses of

NOK 708 million, which is NOK 52 million lower than at

the end of the 4th

quarter of 2008.

The increase in the operating profit compared with the

preceding year is to a great extent due to the impact of

recording losses on securities last year as a consequence of

the global financial crisis.

In 2009, the group's return on equity after tax was 18.2 per

cent (8.1 per cent). For the parent bank, the return on

equity was 18.3 per cent (5.9 per cent) and earnings per

equity certificate in the parent bank were NOK 13.85

(NOK 4.09).

The tax charge is estimated at NOK 143 million.

The reasons for the NOK 509 million improvement in the

profit before tax, compared with 2008, are as follows:

• Reduction in net interest income -NOK 102 million

• Increase in net commission

income

NOK 44 million

• Increase in income from

investment securities NOK 563 million

• Increase in other operating

income

NOK 7 million

• Increase in costs - NOK 1 million

• Increase in net losses -NOK 2 million

For the 4th

quarter of 2009 seen in isolation, the operating

profit before tax was NOK 331 million compared with

NOK 118 million in the same period last year. As for the

result of the year as a whole, the improvement in the

quarter's result is primarily due to the higher contribution

from investment securities. Compared to the 3rd

quarter of

2009, there was also a significant improvement in income

from investment securities. Net interest income rose by

NOK 6 million from the 3rd

quarter of the year.

For the 4th

quarter seen in isolation, return on equity was

25.2 per cent.

Share of result of SpareBank 1 Gruppen

SpareBank 1 Gruppen's preliminary profit after tax at the

end of the 4th

quarter of 2009 amounts to NOK 881million.

SpareBank 1 Nord-Norge group's share of the profit, NOK

175 million, has been incorporated into the accounts. As

can be seen from the extended income statement, a

negative correction of the final result for 2009 was made in

the amount of NOK 10 million which has been recognised

directly against equity. Adjustments have also been made

to equity for the group's share of SpareBank 1 Gruppen's

estimate discrepancies regarding pension provisions for

2008. Reference is made to the statement of changes in

equity.

Subsidiaries

The group's subsidiaries made an aggregate contribution of

NOK 8 million as at the end of the 4th

quarter. Of this, the

result from SpareBank 1 Finans Nord-Norge amounted to

NOK 65 million kroner. The contribution from SpareBank

1 Invest was minus NOK 65 million kroner. This negative

result was mainly due to the write-down of a single

investment.

Reference is also made to the notes to the quarterly

accounts.

Proposed allocation of the profit The parent bank's profit after tax is divided between the

equity certificate owners and the bank's social capital in

accordance with the distribution of equity between these

groups of owners as at 1 January 2009.

In line with the bank's ownership policy (see separate

paragraph below) distribution is proposed paid in

cash/endowments to the groups of owners (equity

certificates and social capital) so that the owner groups'

shares of the bank's equity are maintained at the same level

as at 1 January 2009.

The main Board of Directors proposes that the Supervisory

Board declares a cash dividend of NOK 6.75 per equity

certificate, totalling NOK 121 million, and a provision to

the equalisation fund of NOK 127 million. Furthermore, it

proposes an allocation to the endowment fund of NOK 229

million.

2/22

The proposed allocation of the profit is therefore as

follows:

The parent bank's profit before tax NOK 718 million

Allocated to cash dividend NOK 121 million

Allocated to equalisation fund NOK 127 million

Total to equity certificate

owners (34.54 %) NOK 248 million

Allocated to payments for public benefits NOK160 million

Allocated to donations NOK 69 million

Allocated to savings banks fund NOK 241 million

Total to bank's social capital (65.46 %) NOK 470 million

Total allocations NOK 718 million

Dividend will be paid to those equity certificate owners

who are registered as owners as of 17 March 2010. The

bank's equity certificates will be quoted ex dividend on 18

March 2010.

Interest margins

At the end of the 4th

quarter of 2009, the group's net

interest income aggregated NOK 1,218 million, down

NOK 102 million compared with the end of 4th

quarter of

2008. In terms of average total assets, net interest income

at the end of the 4th

quarter was 1.87 per cent, which is

0.28 percentage points lower than in the same period last

year.

For the 4th quarter seen in isolation, net interest income

was NOK 6 million higher than in the 3rd quarter and

NOK 32 million lower than in the same period in 2008.

The reduction in the interest margin in 2009 is to a great

extent due to the effect of falling interest rate levels,

including:

• Reduced current interest earnings on the bank's

equity

• Reduced interest margin that is not fully

compensated for by increased margins on lending.

The improving interest margins in the 4th

quarter come

from measures introduced in the 3rd

quarter having full

effect in the 4th

quarter.

To ensure liquidity, the bank raised substantial long-term

funding from the capital markets during the financial crisis

in 2007 and 2008. These loans have large credit spreads

compared with the current level and have raised the bank's

average funding cost. Redemption and replacement of

older capital market funding raised before the financial

crisis (with low credit spreads) will continue to have an

increasing negative impact on the bank's interest margin.

The bank maintains its constant focus on the lending

margin. The low interest rates, coupled with the relatively

low activity levels in the economy, are expected to

continue to exert pressure on the bank's interest margin,

also in nominal terms.

Net income from banking services and other income

At the end of the 4th

quarter, net commission income

totalled NOK 438 million, compared with NOK 394

million at the same time last year.

With effect from 1 July 2008, SpareBank 1 Nord-Norge

waived the usage and monthly fees for card and electronic

transmission services for prioritised customers. The bank

will strive to compensate for the reduced income as a

result of this change by increasing other income and

reducing costs.

Seen in isolation, net commission income in the 4th

quarter

amounted to NOK 121 million, compared with NOK 122

million in the preceding quarter and NOK 100 million in

the 4th

quarter of 2008.

In the 1st quarter of 2009, NOK 20 million was recognised

as other income in the consolidated accounts following the

sale of the group's factoring business from SpareBank 1

Finans Nord-Norge AS to SpareBank 1 Gruppen Finans

Holding AS.

Income from investment securities

Net income from investment securities at the end of the 4th

quarter of 2009 amounted to NOK 479 million, divided as

follows:

Result from SpareBank 1 Gruppen NOK 175 million

Result from SpareBank 1

Boligkreditt

Result from BN Bank

Income - badwill BN Bank

Amortised net lesser value book as

income BN Bank

Dividends

Net gains on shares

NOK 13 million

NOK 28 million

NOK 56 million

NOK 8 million

NOK 23 million

NOK 118 million

Net gains on bonds NOK 22 million

Net gains on foreign exchange and

financial derivatives

NOK 36 million

Compared with the end of the 4th

quarter of 2008, the net

result from investment securities rose by NOK 563

million. This improvement is first and foremost a

consequence of last year's write-downs of securities being

replaced by book gains in 2009.

For the 4th

quarter seen in isolation, the net result of

investment securities was NOK 210 million, divided as

follows:

Result from SpareBank 1 Gruppen NOK 36 million

Result from SpareBank 1

Boligkreditt

Result from BN Bank

Income - badwill BN Bank

Amortised net lesser value book as

income BN Bank

Dividends

Net gains on shares

NOK 4 million

NOK 10 million

NOK 56 million

NOK 1 million

NOK 17 million

NOK 85 million

Net gains on bonds - NOK 2 million

Net gains on foreign exchange and

financial derivatives

NOK 3 million

On 1 July 2008, the bank completed a reclassification of

large parts of the fixed income trading portfolio from the

category "Fair value with value changes over the income

statement" to categories that are assessed at amortised cost.

This included NOK 3,807 million of the portfolio totalling

NOK 4.981 million at 30 June 2008. Had such a

reclassification not been made, further unrealised losses of

3/22

NOK 212 million on this portfolio would have been

charged to the income statement from 1 July 2008 to 31

December 2008 as a result of increased credit spreads.

This unrealised loss would have been reduced to NOK 18

million as at 31 December 2009, without such

reclassification. Previously written-down amounts on this

part of the portfolio as at 30 June 2008 amounted to NOK

112 million and are now included as income (amortised)

over the remaining life of each of the securities involved.

As at the end of the 4th

quarter of 2009, this inclusion of

income totalled NOK 26 million. As at 31 December 2009,

the average maturity of the reclassified part of the portfolio

has been assessed at two years. The reclassified portfolio

has been assessed with regard to permanent impairment in

value. As at 31 December 2008 such write-downs were

made on two of the bank's investments, involving NOK 46

million. Further write-downs of an individual security have

been made in 2009 in the amount of NOK 17 million.

Reference is made to the relevant note in the quarterly

accounts.

Operating expenses

Ordinary operating expenses at the end of the 4th quarter

of 2009 totalled NOK 972 million, up by NOK 1 million

or 0.1 per cent compared with 2008.

Personnel costs rose by NOK 45 million, while

administration costs, depreciation and other operating

expenses were cut by NOK 44 million. The increase in

personnel costs is first and foremost a result of allocations

in 2009 of NOK 35 million for the group's profit sharing

with the employees .No such allocation was made in

2008. In terms of average total assets expenses accounted

for 1.49 per cent, a reduction of 0.09 percentage points

compared with the same period last year.

The group's cost ratio was 45.0 per cent in 2009 compared

with 59.0 per cent in 2008.

For the 4th

quarter in isolation, ordinary operating expenses

totalled NOK 276 million compared with NOK 227

million in the preceding quarter and NOK 247 million in

the 4th

quarter of 2008

The rise in operating expenses in the 4th

quarter, compared

with the 3rd

quarter, came from the following:

Allocations to bonuses/profit sharing NOK 20 million

Increase in allocation for social

security contributions NOK 3 million

Increased personnel costs subsidiaries NOK 4 million

Increased IT costs NOK 11 million

Increased admin. expenses subsidiaries NOK 4 million

Increase in other expenses NOK 12 million

Total increase NOK 54 million

At the end of 2009, the group employed 778 man-years, of

which 690 in the parent bank. The corresponding figures in

2008 were 821 and 724 respectively.

Against the backdrop of continued expected weak growth,

cost-reducing measures have been introduced. This work

will be continued, including possible measures aimed at

further enhancing overall efficiency within the areas of

distribution and staff levels.

Net losses and commitments in default

As at 31 December 2009, the group's net losses on loans

totalled NOK 185 million, of which unspecified write-

downs and changes in the long-term monitoring portfolio

accounted for NOK 36 million. Net losses in the corporate

market aggregated NOK 163 million, while in the retail

market they totalled NOK 22 million.

Seen in isolation, net losses in the 4th

quarter totalled NOK

44 million.

Net non-performing loans and doubtful commitments

totalled NOK 571 million as at 31 December 2009,

representing 1.19 per cent of total loans, up by NOK 18

million at the same time in 2008.

Group specific loss write-downs in the 4th

quarter of 2009

totalled NOK 228 million, NOK 21 million more than in

the preceding quarter. The increase in the 4th

quarter, and

the total for 2009 as a whole compared with 2008, is

largely ascribable to losses on a small number of

individual commitments. Although, overall, there has been

an increase in the number of defaults, there are at present

few new bankruptcies and unexpected events involving

commitments. The bank is still to a smaller extent

observing a weaker performance in certain sectors or in the

portfolio generally

As a result of the weak economic situation, the group has

increased unspecified write-downs by NOK 5 million in

the 4th

quarter. Provisions for unspecified losses

represented 0.49 per cent of the group's total loans as at 31

December 2009.

The bank's scoring models for loans made to the corporate

market show a significant rise in the high risk share. This

change, however, is largely attributable to the model basis

having been changed in June 2009 to calculate the

probability of default as a long-term average throughout an

economic cycle, as against point-in-time as was previously

the case. The increased share of high risk is, however, also

due to impairment in the financial soundness and

economic status of the bank's corporate customers.

A comparison of the portfolio at 31 December 2009

compared with 31 December 2008, using the new scoring

models at both dates, shows little change in the risk.

In the opinion of the main Board of Directors, the quality

of the bank's lending portfolio remains good, and every

effort is being made to deal effectively with non-

performing loans and doubtful commitments throughout

the group. As a result of the weakened prospects nationally

and internationally, however, we still expect a higher loss

level compare with the very low level seen over the last

couple of year.

Taxes

The group's tax charge for 2009 is estimated at NOK 143

million. In the parent bank's accounts, the tax basis is

reduced by permanent differences and the effect of the

exemption model. According to IFRS, wealth tax is not a

tax charge and NOK 7 million has therefore been charged

to the income statement as part of other operating

expenses.

4/22

Total assets

The group's total assets amounted to NOK 64,239 million

as at 31 December 2009. This is NOK 1,268 million or 2

per cent lower than one year earlier.

Lending

The group's gross lending amounted to NOK 48,180

million at 31 December 2009. This is 6.0 per cent lower

than at 31 December 2008. As at 31 December 2009, loans

totalling NOK 10,881 million with collateral in the form of

mortgages on housing has been transferred to SpareBank 1

Boligkreditt AS. The growth in lending, including these

loans, was 4.0 per cent. Growth in the retail market was

8.4 per cent, whilst growth in the corporate market and the

public sector was down 4.8 per cent. Including loans

transferred to SpareBank 1 Boligkreditt, the percentage of

loans to the retail market was somewhat higher at the end

of the 4th

quarter and accounted for 69 per cent of total

lending at 31 December 2009.

The financial crisis, with the diminishing economic

growth, has brought about reduced lending growth. The

immediate future is expected to be characterised by a weak

macro-economy, with relatively low growth in lending,

especially in the corporate market. However, the main

Board of Directors still anticipates some lending growth

and increased market shares. As regards new loans,

particular emphasis is placed on customers' ability to

service their outstanding loans and on a satisfactory level

of collateral security to ensure that credit risk is

maintained at an acceptable level.

Savings and investments

As at 31 December 2009, the group had customer deposits

aggregating NOK 34,877 million. This is NOK 305

million or 0.9 per cent higher than one year earlier. 5.7 per

cent of the rise came from the retail market, 20.2 per cent

from the public sector market, while the volume of

deposits from the corporate market declined by 15.1 per

cent.

Portfolio of certificates and bonds

At 31 December 2009, the group's portfolio of certificates

and bonds aggregated NOK 8,893 million. The

corresponding figure at 30 September 2009 and 31

December 2008 was NOK 10,378 and NOK 6,756 million

respectively. The portfolio of interest-bearing papers is

still higher than in previous years as a result of:

• Increased liquidity reserves in the form of

certificates and Treasury bills

• The transfer of mortgage loans to SpareBank 1

Boligkreditt results in an increase in the portfolio

of covered bonds (and reduced lending)

• Use of the authorities swap arrangement for

covered bonds involves accounting-related

incorporation on a gross basis, which in turn

means a parallel increase in assets (including

certificates) and liabilities.

The increase in the certificates and bonds portfolio entails

only a small degree of increased risk.

Liquidity

Deposits from customers represent the bank's main

funding source. The deposit-to-loan ratio at 31 December

2009 was 72.4 per cent, up 5.0 percentage points on the

preceding year. Apart from equity and deposits from

customers, the bank's remaining funding represents first

and foremost long-term borrowings from the capital

markets. The bank's access to liquidity has been

satisfactory throughout the period of unrest in the

international markets. The bank's strategic goal is to

maintain the overall funding risk at a low level.

Basel II

With effect from 1 January 2007, new capital adequacy

rules and regulations (Basel II – EU’s new directive for

capital coverage) were implemented in Norway. The new

rules and regulations are based on a proposal for a new

standard for capital adequacy calculations from Bank for

International Settlements (BIS).

With effect from 1 January 2007, SpareBank 1 Nord-

Norge was given permission by the Financial Supervisory

Authority of Norway (FSAN) to apply internal measuring

methods (Internal Rating-Based Approach) to credit risk.

From 2007, therefore, the statutory minimum requirement

for capital adequacy for credit risk was based on the

Bank’s internal risk assessment. The new rules and

regulations make the statutory minimum capital adequacy

requirement more risk-sensitive, so that the capital

adequacy requirement will to a larger extent correspond to

the risk in the underlying portfolios. The use of internal

measuring methods involves comprehensive demands with

regard to the Bank’s organisation, competence, risk

models and risk management systems.

As a result of transition rules in the new regulations, IRB

banks will nevertheless only experience the full effect of

the reduced regulatory requirements in 2010.It has now

been resolved that this is to be postponed and the

transitional rules for 2009 will continue in 2010.

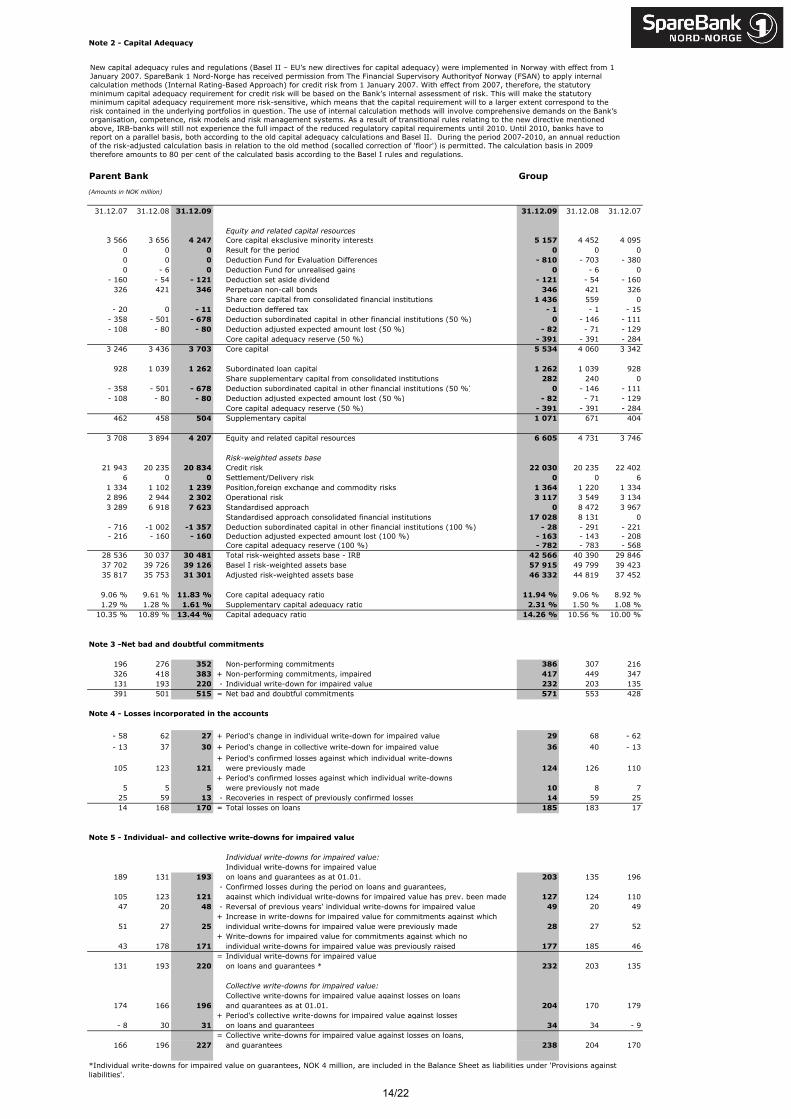

Equity capital and capital adequacy

At the 31 December 2009, the Group’s core capital

adequacy was 11.94 per cent (9.06 per cent) of the

calculation base. The total capital adequacy was 14.26

percent (10.56 per cent). The calculation in 2009 is made

in accordance with the transitional rules and regulations

provided by FSAN.

As at 31.12.09, the Parent Bank’s capital adequacy ratio

was 13.44 per cent (10.8 per cent), and the core capital

ratio 11.83 per cent (9.61 per cent).

The bank raised a subordinated loan of NOK 350 million

in July 2009. Further subordinated loan capital amounting

to NOK 100 million was raised in the 4th

quarter of 2009.

The new subordinated loan capital was raised to replace a

EURO 50 million subordinated loan with redemption right

(call/step up) at the beginning of 2010.

The group has been given permission from FSAN to use

proportional consolidation in the capital adequacy

reporting of stakes in SpareBank 1Boligkreditt and

SpareBank 1 Næringskreditt.

The bank's stated goal is a core capital ratio of 10% or

higher. The bank's capital strength is considered to be

satisfactory.

5/22

The Bank’s equity certificate holders

The Bank’s equity certificate capital was NOK 896 million

divided into 17,912,073 equity certificates. As at 01.01.09,

the equity certificate ratio was estimated at 34.54 per cent.

The number of equity certificate holders was 8,207 as at

31 December 2009, down 164 during the last 12 months.

The number of equity certificate holders domiciled in

North Norway was 2,199. A summary of the Bank’s 20

largest equity certificate owners is included in the notes to

the accounts.

Equity certificates and dividend policy

A new act and regulations relating to equity certificates,

formerly primary capital certificates) came into effect on 1

July 2009. The new regulations imply, inter alia, that

savings banks' equity certificates will to a greater extent be

treated in line with shares. The regulations imply a greater

degree of equality between the various owner groups in

saving banks and will to a great extent minimise earlier

challenges reacting to dilution of equity certificate holders

in the case of payment of cash dividends. The new

legislation is positive for equity certificates as a security.

On the basis of the new legislation, the main Board of

Directors has adopted a new dividend policy for the bank.

Taking into account the bank's financial strength, the bank

aims at up to 50 per cent of the profit being allocated to

dividends (cash dividend and gifts and endowments).

The bank's other adaptations to the new regulations will be

considered prior to the ordinary meeting of the bank's

Supervisory Board in the spring of 2010.

Concluding remarks –prospects

The result for 2009 is regarded as very good especially

taking into consideration the difficult macroeconomic

situation. The Bank’s core operations remain good.

The macro-economic situation is expected to remain

relatively weak in Norway and North Norway in the near

future. This will mean lower credit demand than is normal,

especially in the corporate market, and a relatively high

level of credit losses. A low level of interest rates is likely

to continue to result in downward pressure on the bank’s

net interest income.

The bank considers balanced growth both for deposits and

loans to be important. Emphasis will be placed on

increasing other income through the sale of different

products and services. Lending growth will continue to be

conditional upon good credit quality.

As a result of expected weak growth, the Bank will

continue to focus sharply on cost-reducing measures. This

includes possible measures aimed at enhancing overall

effectiveness within distribution and in staff levels.

Tromso, 10 February 2010

The Main Board of Directors of SpareBank 1 Nord-

Norge

6/22

Key figures group

Amounts in NOK million and in % of average assets 31.12.09 % 31.12.08 % 31.12.07 %From the profit and loss accountNet interest income 1 218 1.87 % 1 320 2.15 % 1 206 2.08 %

Net fee-, commision and other operating income 462 0.71 % 411 0.67 % 465 0.80 %

Net income from financial investments 479 0.74 % - 84 -0.14 % 201 0.35 %

Total income 2 159 3.31 % 1 647 2.69 % 1 872 3.23 %

Total costs 972 1.49 % 971 1.58 % 962 1.66 %

Result before losses 1 187 1.82 % 676 1.10 % 910 1.57 %

Losses 185 0.28 % 183 0.30 % 17 0.03 %

Result before tax 1 002 1.54 % 493 0.80 % 893 1.54 %

Tax 143 0.22 % 143 0.23 % 186 0.32 %

Minority interests 1 0.00 % 2 0.00 % 4 0.01 %

Result for the period 858 1.32 % 348 0.57 % 703 1.21 %

Profitability

Return on equity capital 1 18.2 % 8.1 % 18.1 %

Interest margin 2 1.87 % 2.15 % 2.08 %

Cost/income 3 45.0 % 59.0 % 51.4 %

Balance sheet figures

Loans and advances to customers 48 180 51 268 50 213

Loans and advances to customers including SpareBank 1 Boligkreditt AS 59 061 56 806 52 582

Deposits from customers 34 877 34 572 32 034

Deposits as a percentage of gross lending 4 72.4 % 67.4 % 63.8 %

Growth in loans and advances to customers past 12 months -6.0 % 2.1 % 8.6 %

Growth in loans and advances to customers including SpareBank 1 Boligkreditt AS 4.0 % 8.0 % 13.7 %

Growth in deposits from customers past 12 months 0.9 % 7.9 % 15.3 %

Average assets 5 65 169 61 267 58 023

Total assets 64 239 65 507 60 969

Losses on loans and commitments in default

Losses on loans to customers as a percentage of gross loans 0.38 % 0.36 % 0.03 %

Commitments in default as a percentage of gross loans 0.80 % 0.60 % 0.43 %

Commitments at risk of loss as a percentage of gross loans 0.87 % 0.88 % 0.69 %

Net commitments in default and at risk of loss as a percentage of gross loans 1.19 % 1.08 % 0.85 %

Solidity

Capital adequacy ratio 6 14.26 % 10.56 % 10.00 %

Core capital adequacy ratio 7 11.94 % 9.06 % 8.92 %

Core capital 5 534 4 060 3 342

Equity and related capital resources 6 605 4 731 3 746

Adjusted risk-weighted assets base 46 332 44 819 37 452

Branches and full-time employees

Branches 76 81 81

Manyear 778 821 813

Equity Certificates 31.12.09 31.12.08 31.12.07 31.12.06 31.12.05 31.12.04

Equity Certificate ratio overall 8 34.54 % 34.22 % 32.88 % 34.19 % 35.60 % 39.01 %

Quoted/market price NONG as at 110.00 44.00 127.00 149.50 157.00 276.00

Quotation value 9 1 970 788 2 135 2 367 2 486 1 821

Equity capital per Equity Certificate (NOK) 10 83.18 72.35 76.19 72.95 60.07 140.37

Result per Equity Certificate (Parent Bank) 11 13.85 4.09 10.00 14.03 11.64 24.04

Cash dividend per Equity Certificate to be paid 12 6.75 3.00 9.50 10.00 10.00 19.00

P/E (Price/Earnings) 13 7.9 10.8 12.7 10.7 13.5 11.5

P/V (Price/Book Value) 14 1.3 0.6 1.7 2.0 2.6 2.0

Before Equity Certificate split in 2005

13 Market price on Oslo Stock Exchange at end of period, divided by result for the period per EC 14 Market price on Oslo Stock Exchange at end of period, divided by book value of equity capital per EC

1 Profit for the period as a percentage of average total equity, calculated as average amount of quarterly equity and per 01.01. and 31.12. 2 Total interest margin as a percentage of average total assets 3 Total costs as a percentage of total net income4 Deposits from customers as a percentage of gross lending(ex. Sp1.Boligkreditt) 5 Average assets are calculated as average assets each quarter and at 01.01. and 31.12. 6 Net subordinated capital as a percentage of calculated risk-weighted balance 7 Core capital as a percentage of calculated risk-weighted balance 8 EC holders share of equity capital as at 01.01. 9 Quoted price on Oslo Stock Exchange multiplied by numbers of EC's outstanding 10 EC-capital + Premium Fund + Dividend Equalisation Fund, divided by number of EC's outstanding 11 Profit for the period (parent bank) multiplied by Equity Certificates holders' share of the equity capital as at 01.01., in relation to total number of EC's 12 Cash dividend per EC for the accounting year. Resolution made by Main Board of Directors

*)

*)

7/22

31.12.07 4Q08 4Q09 31.12.08 31.12.09 31.12.09 31.12.08 4Q09 4Q08 31.12.07

3 216 1 156 588 4 285 2 731 Interest income 2 808 4 334 603 1 171 3 250

2 048 828 293 3 021 1 591 Interest costs 1 590 3 014 286 822 2 044

1 168 328 295 1 264 1 140 Net interest income 1 218 1 320 317 349 1 206

427 106 124 424 449 Fee- and commission income 526 478 145 122 502

67 23 24 85 87 Fee- and commission costs 88 84 24 22 65

7 2 2 6 5 Other operating income 24 17 3 3 28

367 85 102 345 367 Net fee-, commision and other operating income 462 411 124 103 465

11 2 17 15 22 Dividend 23 16 17 2 11

60 0 - 38 114 144 Income from investments 281 277 109 220 231

- 66 - 163 104 - 349 233 Net gain from investments in securities 175 - 377 84 - 195 - 41

5 - 161 83 - 220 399 Net income from financial investments 479 - 84 210 27 201

1 540 252 480 1 389 1 906 Total income 2 159 1 647 651 479 1 872

410 87 131 398 441 Personnel costs 508 463 151 107 473

260 72 79 278 264 Administration costs 284 304 84 79 293

38 10 9 37 34 Ordinary depreciation 49 62 12 22 55

149 37 35 156 153 Other operating costs 131 142 29 39 141

857 206 254 869 892 Total costs 972 971 276 247 962

683 46 226 520 1 014 Result before losses 1 187 676 375 232 910

14 104 37 168 170 Losses 185 183 44 114 17

669 - 58 189 352 844 Result before tax 1 002 493 331 118 893

177 19 16 138 126 Tax 143 143 20 18 186

492 - 77 173 214 718 Result for the period 859 350 311 100 707

Majority interest 858 348 310 99 703

Minority interests 1 2 1 1 4

Result per Equity Certificate

10.00 -1.47 3.34 4.09 13.85 Result per Equity Certificate (Parent Bank) 16.39 6.65 5.92 1.89 14.30

10.00 -1.47 3.34 4.09 13.85 Diluted result per Equity Certificate 16.39 6.65 5.92 1.89 14.30

Allocation of result for the period:

Fund for Evaluation Differences 119 133 211

168 73 248 Dividend Equalisation Fund 248 73 168

83 40 69 Donations 69 40 83

241 101 401 Saving Bank's Fund 422 102 241

492 214 718 Total allocations 858 348 703

492 -77 173 214 718 Result for the period 859 350 311 100 7070 0 0 0 0 Effective part of change in fair market value in cash flow hedging -18 0 -18 0 00 0 0 0 0 Net change in fair market value of investment in joint ventures 0 -17 0 0 00 0 0 6 -6 Net change in fair market value of financial assets available for sale -6 6 0 0 00 0 0 2 -2 Tax on other comprehensive income -7 2 -5 0 00 0 0 4 -4 Other comprehensive income for the period -17 -13 -13 0 0

492 -77 173 218 714 Total comprehensive income for the period 842 337 298 100 707

Majority interest 841 335 297 99 703Minority interests 1 2 1 1 4

Totalresult per Equity Certificate

10.00 -1.47 3.34 4.17 13.76 Total result per Equity Certificate (Parent Bank) 16.08 6.44 5.69 1.91 14.30

10.00 -1.47 3.34 4.17 13.76 Diluted total result per Equity Certificate 16.08 6.44 5.69 1.91 14.30

Tax on other comprehensive income:0 0 0 0 0 Effective part of change in fair market value in cash flow hedging -5 0 -5 0 00 0 0 2 -2 Net change in fair market value of financial assets available for sale -2 2 0 0 00 0 0 2 -2 Tax on other comprehensive income -7 2 -5 0 0

Group

Comprehensive income

Statement of comprehensive incomeParent Bank

(Amounts in NOK million)

8/22

31.12.07 31.12.08 31.12.09 31.12.09 31.12.08 31.12.07

Assets2 484 3 290 2 159 Cash and balances with central banks 2 159 3 290 2 4841 726 1 964 2 671 Loans and advances to credit institutions 908 143 330

48 945 49 491 46 431 Loans and advances to customers 48 180 51 268 50 213 130 191 216 - Individual write-downs for impaired value 228 201 134 166 196 227 - Collective write-downs for impaired value 238 204 170

48 649 49 104 45 988 Net loans and advances to customers 47 714 50 863 49 909 423 346 410 Shares 560 472 547

4 856 6 749 8 891 Certificates and bonds 8 893 6 756 4 856 276 647 561 Financial derivatives 561 647 276 227 284 248 Investments in Group Companies 0 0 0 717 1 092 1 586 Investments in assosiated companies and joint ventures 2 396 1 796 1 248 125 126 110 Property, plant and equipment 469 489 567 20 0 11 Intangible assets 1 1 15

665 937 554 Other assets 578 1 050 737

60 168 64 539 63 189 Total assets 64 239 65 507 60 969

Liabilities2 415 3 720 6 869 Deposits from credit institutions 6 868 3 708 2 414

32 053 34 599 34 892 Deposits from customers 34 877 34 572 32 03419 665 19 746 14 162 Debt securities in issue 14 162 19 746 19 665

297 367 319 Financial derivatives 319 367 297 918 878 1 092 Other liabilities 1 242 1 083 1 051

0 112 0 Deferred tax liabilities 3 112 01 254 1 461 1 608 Subordinated loan capital 1 608 1 461 1 254

56 602 60 883 58 942 Total liabilities 59 079 61 049 56 715

Equity

841 896 896 Equity Certificate capital 896 896 841

76 123 123 Equity Certificate premium reserve 123 123 76

364 277 471 Dividend Equalisation Fund 471 277 364

2 121 2 221 2 624 The Savings Bank's Fund 2 724 2 314 2 270

164 133 133 Donations 133 133 164

0 6 0 Fund for unrealised gains 0 6 0

0 0 0 Other equity capital 810 703 530

Minority interests 3 6 93 566 3 656 4 247 Total equity 5 160 4 458 4 254

60 168 64 539 63 189 Total liabilities and equity 64 239 65 507 60 969

Statement of financial positionParent Bank

(Amounts in NOK million)

Group

9/22

(Amounts in NOK million) 4Q09 3Q09 2Q09 1Q09 4Q08 3Q08 2Q08 1Q08 4Q07

Interest income 603 635 702 868 1 171 1 126 1 049 988 953

Interest costs 286 324 415 565 822 777 736 679 629

Net interest income 317 311 287 303 349 349 313 309 324

Fee- and commission income 145 143 126 112 122 119 126 111 126

Fee- and commission costs 24 21 23 20 22 26 20 16 16

Other operating income 3 - 1 0 22 3 1 6 7 13

Net fee-, commision and other operating income 124 121 103 114 103 94 112 102 123

Dividend 17 1 5 0 2 1 5 8 0

Income from investments 109 97 68 7 220 8 30 19 60

Net gain from investments in securities 84 48 - 18 61 - 195 - 65 - 2 - 115 4

Net income from financial investments 210 146 55 68 27 - 56 33 - 88 64

Total income 651 578 445 485 479 387 458 323 511

Personnel costs 151 124 117 116 107 124 119 113 116

Administration costs 84 59 66 75 79 71 74 80 73

Ordinary depreciation 12 12 12 13 22 13 13 14 17

Other operating costs 29 32 31 39 39 25 31 47 40

Total costs 276 227 226 243 247 233 237 254 246

Result before losses 375 351 219 242 232 154 221 69 265

Losses 44 39 49 53 114 41 25 3 8

Result before tax 331 312 170 189 118 113 196 66 257

Tax 20 50 36 37 18 49 48 28 48

Minority interests 1 0 0 0 1 0 1 0 1

Result for the period 310 262 134 152 99 64 147 38 208

Profitability

Return on equity capital 25.23 % 22.71 % 11.56 % 13.13 % 9.27 % 5.98 % 13.67 % 3.62 % 21.40 %

Interest margin 1.97 % 1.88 % 1.75 % 1.88 % 2.21 % 2.31 % 2.10 % 2.06 % 2.15 %

Cost/income 42.40 % 39.27 % 50.79 % 50.10 % 51.57 % 60.21 % 51.75 % 78.64 % 48.14 %

Balance sheet figures

Loans and advances to customers 48 180 49 413 50 473 50 900 51 268 50 414 49 907 49 815 50 213

Deposits from customers 34 877 34 256 36 129 34 078 34 572 32 148 33 793 31 106 32 034

Deposits as a percentage of gross lending 72.4 % 69.3 % 71.6 % 67.0 % 67.4 % 63.8 % 67.7 % 62.4 % 63.8 %

Growth in loans and advances to customers including SpareBank 1 Boligkreditt AS 4.0 % 5.6 % 5.1 % 7.4 % 8.0 % 9.0 % 11.0 % 11.2 % 13.7 %

Growth in deposits from customers past 12 months 0.9 % 6.6 % 6.9 % 9.6 % 7.9 % 6.1 % 4.3 % 7.3 % 15.3 %

Average assets 65 169 65 402 65 678 64 537 61 267 60 207 59 983 59 900 58 023

Total assets 64 239 64 574 67 961 63 566 65 507 60 879 60 148 58 831 60 969

Losses on loans and commitments in default

Losses on loans to customers as a percentage of gross loans 0.37 % 0.32 % 0.39 % 0.42 % 0.89 % 0.33 % 0.20 % 0.02 % 0.06 %

Commitments in default as a percentage of gross loans 0.80 % 0.79 % 0.93 % 0.88 % 0.60 % 0.55 % 0.32 % 0.34 % 0.43 %

Commitments at risk of loss as a percentage of gross loans 0.87 % 0.83 % 0.76 % 0.74 % 0.88 % 0.93 % 0.95 % 0.75 % 0.69 %

Net commitments in default and at risk of loss as a percentage of gross loans 1.19 % 1.21 % 1.34 % 1.27 % 1.08 % 1.11 % 0.98 % 0.85 % 0.85 %

Solidity

Capital adequacy ratio 14.26 % 12.07 % 11.08 % 11.73 % 10.56 % 11.26 % 10.93 % 11.71 % 10.00 %

Core capital adequacy ratio 11.94 % 10.08 % 9.65 % 10.13 % 9.06 % 9.35 % 9.44 % 9.54 % 8.92 %

Core capital 5 534 4 683 3 914 4 059 4 060 3 448 3 415 3 403 3 342

Equity and related capital resources 6 605 5 609 4 494 4 699 4 731 4 151 3 955 4 175 3 746

Basel I risk-weighted assets base 46 332 46 476 40 559 40 069 44 819 36 862 36 191 35 665 37 452

Result from the Group's quarterly accounts

10/22

Parent Bank

31.12.08 31.12.09

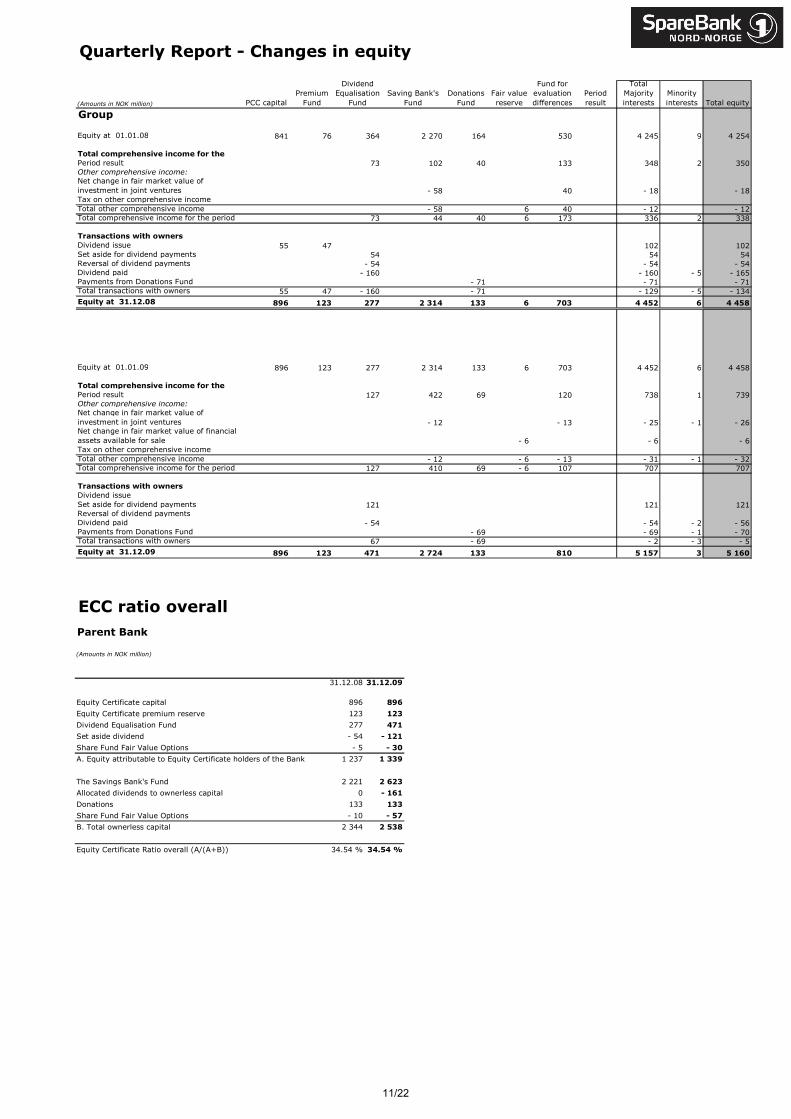

Equity Certificate capital 896 896

Equity Certificate premium reserve 123 123

Dividend Equalisation Fund 277 471

Set aside dividend - 54 - 121

Share Fund Fair Value Options - 5 - 30

A. Equity attributable to Equity Certificate holders of the Bank 1 237 1 339

The Savings Bank's Fund 2 221 2 623

Allocated dividends to ownerless capital 0 - 161

Donations 133 133

Share Fund Fair Value Options - 10 - 57

B. Total ownerless capital 2 344 2 538

Equity Certificate Ratio overall (A/(A+B)) 34.54 % 34.54 %

ECC ratio overall

(Amounts in NOK million)

(Amounts in NOK million) PCC capital

Premium

Fund

Dividend

Equalisation

Fund

Saving Bank's

Fund

Donations

Fund

Fair value

reserve

Fund for

evaluation

differences

Period

result

Total

Majority

interests

Minority

interests Total equity

Group

Equity at 01.01.08 841 76 364 2 270 164 530 4 245 9 4 254

Total comprehensive income for the

Period result 73 102 40 133 348 2 350Other comprehensive income:

Net change in fair market value of

investment in joint ventures - 58 40 - 18 - 18Tax on other comprehensive income Total other comprehensive income - 58 6 40 - 12 - 12Total comprehensive income for the period 73 44 40 6 173 336 2 338

Transactions with owners

Dividend issue 55 47 102 102Set aside for dividend payments 54 54 54Reversal of dividend payments - 54 - 54 - 54Dividend paid - 160 - 160 - 5 - 165Payments from Donations Fund - 71 - 71 - 71Total transactions with owners 55 47 - 160 - 71 - 129 - 5 - 134

Equity at 31.12.08 896 123 277 2 314 133 6 703 4 452 6 4 458

Equity at 01.01.09 896 123 277 2 314 133 6 703 4 452 6 4 458

Total comprehensive income for the

Period result 127 422 69 120 738 1 739Other comprehensive income:

Net change in fair market value of

investment in joint ventures - 12 - 13 - 25 - 1 - 26Net change in fair market value of financial

assets available for sale - 6 - 6 - 6Tax on other comprehensive income Total other comprehensive income - 12 - 6 - 13 - 31 - 1 - 32Total comprehensive income for the period 127 410 69 - 6 107 707 707

Transactions with owners

Dividend issue Set aside for dividend payments 121 121 121Reversal of dividend payments Dividend paid - 54 - 54 - 2 - 56Payments from Donations Fund - 69 - 69 - 1 - 70Total transactions with owners 67 - 69 - 2 - 3 - 5

Equity at 31.12.09 896 123 471 2 724 133 810 5 157 3 5 160

Quarterly Report - Changes in equity

11/22

31.12.07 31.12.08 31.12.09 31.12.09 31.12.08 31.12.07

669 352 844 Result before tax 1 002 493 893 38 36 34 + Ordinary depreciation 49 61 55 0 6 0 + Write-downs, gains/losses fixed assets 0 11 6

14 168 170 + Losses on loans and guarantees 185 183 17 177 138 126 - Tax 142 143 193

0 0 0 - Group contributions 0 0 0 158 160 54 - Dividend paid on Equity Certificates 54 160 158

386 264 868 Provided from the year's operations 1 040 445 620

- 316 76 - 22 Change in sundry liabilities: + increase/ - decrease - 89 125 - 323 150 - 623 485 Change in various claims: - increase/ + decrease 545 - 671 91

-3 641 - 623 2 946 Change in gross lending to and claims on customers: - increase/ + decrease 2 964 -1 137 -4 070 15 -1 816 -2 232 Change in short term-securities: - increase/ + decrease -2 225 -1 825 - 50

4 179 2 546 293 Change in deposits from and debt owed to customers: + increase/ - decrease 305 2 538 4 250 432 1 305 3 149 Change in debt owed to credit institutions: + increase/ - decrease 3 160 1 294 449

1 205 1 129 5 487 A. Net liquidity change from operations 5 700 769 967

- 68 - 45 - 17 - Investment in fixed assets - 33 - 62 - 117 1 2 1 + Sale of fixed assets 4 70 10

- 201 - 432 - 458 Change in holdings of long-term securities: - increase/ + decrease - 600 - 548 - 313

- 268 - 475 - 474 B. Liquidity change from investments - 629 - 540 - 420

924 81 -5 584 Change in borrowings through the issuance of securities: + increase/ - decrease -5 584 81 924- 3 309 147 Change in Equity Certificate/subordinated loan capital: + increase/ - decrease 147 309 - 3

921 390 -5 437 C. Liquidity change from financing -5 437 390 921

1 858 1 044 - 424 A + B + C. Total change in liquidity - 366 619 1 4682 352 4 210 5 254 + Liquid funds at the start of the period 3 433 2 814 1 346

4 210 5 254 4 830 = Liquid funds at the end of the period 3 067 3 433 2 814

Liquid funds are defined as cash-in-hand, claims on central banks,plus loans to and claims on credit institutions.

Statement of cash flowsParent Bank

(Amounts in NOK million)

Group

12/22

Note 1 - Accounting Principles

Notes

The Group’s quarterly accounts have been prepared in accordance with stock exchange rules and regulations and International Financial

Reporting Standards (IFRS), including IAS 34 relating to interim reporting. The quarterly accounts do not comprise all information which

is required in complete annual accounts and should be read in conjunction with the 2008 Annual Accounts. IAS 1 – presentation of the

financial accounts – has been amended in 2009, involving several changes in the presentation of the profit and loss account – now “Statement of comprehensive income” as well as the statement of changes in equity capital. Items which are recognised directly in

equity capital shall now also be presented in the Statement of comprehensive income as extended profit and loss account items. In the

equity capital statement transactions between the owners and other transactions are kept separate.

In accordance with the rules and regulations dated 16 October 2008 issued by the Ministry of Finance, it is now permitted to reclassify

securities in a trading portfolio from the category ‘Market value with any value changes shown through the profit and loss account’ to the

category ‘Hold until maturity’ and ‘Loans and claims’. The SNN Group decided to apply such reclassification to large parts of its interest-

bearing portfolio with effect from 01.07.08. Future assessments within these categories shall be calculated at amortized cost, which means that earlier write-downs of values and interest are to be amortized and included in the profit and loss account as interest income

over the remaining life of the items in question. Reference is made to Note 12.

The remaining portfolio of certificates and bonds is assessed at market value through the profit and loss account. To the extent that there is an active market in the securities in question, known market prices are applied in order to establish actual value. For parts of the

portfolio (portfolio of CDOs – Collateralised Debt Obligations), observable prices were not available, and the Bank has therefore applied alternative assessment methods according to IFRS 39 in order to determine actual value (‘Fair Market Value’) as at 31.12.09 for the

securities involved.In the absence of direct prices for the financial instruments, broad market indexes are used. These follow fluctuations

in the credit markets, and are thought to reflect relevant re-pricing of credit risk in relation to pricing of the types of securities in

question. Credit indexes used are ‘Itraxx Europe Investment Grade Index’, ‘CDX North America’ Index’ and ‘CMBX North America’ (with relevant rating in relation to the Bank’s portfolio).

13/22

31.12.07 31.12.08 31.12.09 31.12.09 31.12.08 31.12.07

Equity and related capital resources

3 566 3 656 4 247 Core capital eksclusive minority interests 5 157 4 452 4 095

0 0 0 Result for the period 0 0 0

0 0 0 Deduction Fund for Evaluation Differences - 810 - 703 - 380

0 - 6 0 Deduction Fund for unrealised gains 0 - 6 0

- 160 - 54 - 121 Deduction set aside dividend - 121 - 54 - 160

326 421 346 Perpetuan non-call bonds 346 421 326

Share core capital from consolidated financial institutions 1 436 559 0

- 20 0 - 11 Deduction deffered tax - 1 - 1 - 15

- 358 - 501 - 678 Deduction subordinated capital in other financial institutions (50 %) 0 - 146 - 111

- 108 - 80 - 80 Deduction adjusted expected amount lost (50 %) - 82 - 71 - 129

Core capital adequacy reserve (50 %) - 391 - 391 - 284

3 246 3 436 3 703 Core capital 5 534 4 060 3 342

928 1 039 1 262 Subordinated loan capital 1 262 1 039 928

Share supplementary capital from consolidated institutions 282 240 0

- 358 - 501 - 678 Deduction subordinated capital in other financial institutions (50 %) 0 - 146 - 111

- 108 - 80 - 80 Deduction adjusted expected amount lost (50 %) - 82 - 71 - 129

Core capital adequacy reserve (50 %) - 391 - 391 - 284

462 458 504 Supplementary capital 1 071 671 404

3 708 3 894 4 207 Equity and related capital resources 6 605 4 731 3 746

Risk-weighted assets base

21 943 20 235 20 834 Credit risk 22 030 20 235 22 402

6 0 0 Settlement/Delivery risk 0 0 6

1 334 1 102 1 239 Position,foreign exchange and commodity risks 1 364 1 220 1 334

2 896 2 944 2 302 Operational risk 3 117 3 549 3 134

3 289 6 918 7 623 Standardised approach 0 8 472 3 967

Standardised approach consolidated financial institutions 17 028 8 131 0

- 716 -1 002 -1 357 Deduction subordinated capital in other financial institutions (100 %) - 28 - 291 - 221

- 216 - 160 - 160 Deduction adjusted expected amount lost (100 %) - 163 - 143 - 208

Core capital adequacy reserve (100 %) - 782 - 783 - 568

28 536 30 037 30 481 Total risk-weighted assets base - IRB 42 566 40 390 29 846

37 702 39 726 39 126 Basel I risk-weighted assets base 57 915 49 799 39 423

35 817 35 753 31 301 Adjusted risk-weighted assets base 46 332 44 819 37 452

9.06 % 9.61 % 11.83 % Core capital adequacy ratio 11.94 % 9.06 % 8.92 %

1.29 % 1.28 % 1.61 % Supplementary capital adequacy ratio 2.31 % 1.50 % 1.08 %

10.35 % 10.89 % 13.44 % Capital adequacy ratio 14.26 % 10.56 % 10.00 %

196 276 352 Non-performing commitments 386 307 216

326 418 383 + Non-performing commitments, impaired 417 449 347

131 193 220 - Individual write-down for impaired value 232 203 135

391 501 515 = Net bad and doubtful commitments 571 553 428

- 58 62 27 + Period's change in individual write-down for impaired value 29 68 - 62

- 13 37 30 + Period's change in collective write-down for impaired value 36 40 - 13

+ Period's confirmed losses against which individual write-downs

105 123 121 were previously made 124 126 110

+ Period's confirmed losses against which individual write-downs

5 5 5 were previously not made 10 8 7

25 59 13 - Recoveries in respect of previously confirmed losses 14 59 25

14 168 170 = Total losses on loans 185 183 17

Individual write-downs for impaired value:

Individual write-downs for impaired value

189 131 193 on loans and guarantees as at 01.01. 203 135 196

- Confirmed losses during the period on loans and guarantees,

105 123 121 against which individual write-downs for impaired value has prev. been made 127 124 110

47 20 48 - Reversal of previous years' individual write-downs for impaired value 49 20 49

+ Increase in write-downs for impaired value for commitments against which

51 27 25 individual write-downs for impaired value were previously made 28 27 52

+ Write-downs for impaired value for commitments against which no

43 178 171 individual write-downs for impaired value was previously raised 177 185 46

= Individual write-downs for impaired value

131 193 220 on loans and guarantees * 232 203 135

Collective write-downs for impaired value:

Collective write-downs for impaired value against losses on loans

174 166 196 and guarantees as at 01.01. 204 170 179

+ Period's collective write-downs for impaired value against losses

- 8 30 31 on loans and guarantees 34 34 - 9

= Collective write-downs for impaired value against losses on loans,

166 196 227 and guarantees 238 204 170

*Individual write-downs for impaired value on guarantees, NOK 4 million, are included in the Balance Sheet as liabilities under 'Provisions against

liabilities'.

Note 2 - Capital Adequacy

Group

Note 5 - Individual- and collective write-downs for impaired value

Note 4 - Losses incorporated in the accounts

Note 3 -Net bad and doubtful commitments

Parent Bank

(Amounts in NOK million)

New capital adequacy rules and regulations (Basel II – EU’s new directives for capital adequacy) were implemented in Norway with effect from 1

January 2007. SpareBank 1 Nord-Norge has received permission from The Financial Supervisory Authorityof Norway (FSAN) to apply internal calculation methods (Internal Rating-Based Approach) for credit risk from 1 January 2007. With effect from 2007, therefore, the statutory

minimum capital adequacy requirement for credit risk will be based on the Bank’s internal assessment of risk. This will make the statutory minimum capital adequacy requirement more risk-sensitive, which means that the capital requirement will to a larger extent correspond to the

risk contained in the underlying portfolios in question. The use of internal calculation methods will involve comprehensive demands on the Bank’s organisation, competence, risk models and risk management systems. As a result of transitional rules relating to the new directive mentioned

above, IRB-banks will still not experience the full impact of the reduced regulatory capital requirements until 2010. Until 2010, banks have to report on a parallel basis, both according to the old capital adequacy calculations and Basel II. During the period 2007-2010, an annual reduction of the risk-adjusted calculation basis in relation to the old method (socalled correction of 'floor') is permitted. The calculation basis in 2009

therefore amounts to 80 per cent of the calculated basis according to the Basel I rules and regulations.

14/22

31.12.07 31.12.08 31.12.09 31.12.09 31.12.08 31.12.07

398 305 0 Central government administration and social security administration 1 307 398 181 249 140 Counties and municipalities 170 286 231

2 831 2 562 2 420 Agriculture, forestry, fisheries, hunting and fish farming 2 545 2 694 2 941 21 146 125 Production of crude oil and natural gas 125 146 21

1 359 1 261 1 116 Industry and mining 1 240 1 372 1 4571 135 1 267 2 109 Building and construction, power and water supply 2 408 1 570 1 3761 559 1 694 1 195 Wholesale and retail trade; hotel and restaurant industry 1 355 1 892 1 704

0 124 419 International shipping and pipeline transport 419 126 18 064 8 165 7 443 Financing, property management and business services 7 296 8 054 7 8251 050 1 448 1 463 Transport and communication 1 795 1 755 1 261 788 846 694 Other service industries 789 900 817 203 198 286 Insurance, fund management and financial services 157 118 198

31 305 31 168 28 970 Retail banking market 29 827 31 990 31 932 51 58 51 Foreign retail banking market 53 58 51

48 945 49 491 46 431 Gross lending 48 180 51 268 50 213

0 0 0 Central government administration and social security administration 0 0 0 0 0 0 Counties and municipalities 0 0 0 0 41 50 Agriculture, forestry, fisheries, hunting and fish farming 50 41 0 0 0 0 Production of crude oil and natural gas 0 0 0

11 78 24 Industry and mining 25 78 11 3 7 9 Building and construction, power and water supply 9 7 4

16 19 6 Wholesale and retail trade; hotel and restaurant industry 6 21 16 0 0 1 International shipping and pipeline transport 1 0 0 7 29 33 Financing, property management and business services 34 29 8 2 7 2 Transport and communication 7 9 2 2 1 2 Other service industries 3 3 2 0 0 0 Insurance, fund management and financial services 0 0 0 6 15 25 Retail banking market 30 21 7 0 0 0 Foreign retail banking market 0 0 0 0 0 0 Non individual specific write-downs public market 0 0 0

- 8 21 31 Collective write-downs public market 31 22 - 8 0 9 0 Collective write-downs retail market 3 11 0 0 0 0 Unallocated market 0 0 0

39 227 183 Gross losses 199 242 42 25 59 13 Recoveries from previously written off losses 14 59 25 14 168 170 Net losses 185 183 17

257 284 622 Central government administration and social security administration 622 284 2574 463 4 837 5 532 Counties and municipalities 5 532 4 837 4 4631 036 1 018 763 Agriculture, forestry, fisheries, hunting and fish farming 763 1 018 1 036

1 2 1 Production of crude oil and natural gas 1 2 1 642 657 412 Industry and mining 412 657 642

1 461 1 536 1 587 Building and construction, power and water supply 1 587 1 536 1 4611 460 1 352 1 322 Wholesale and retail trade; hotel and restaurant industry 1 322 1 352 1 460

12 13 23 International shipping and pipeline transport 23 13 123 155 3 880 2 773 Financing, property management and business services 2 764 3 866 3 154 792 711 844 Transport and communication 844 711 792 622 567 346 Insurance, fund management and financial services 340 553 604

1 872 1 852 1 758 Other service industries 1 758 1 852 1 87216 076 17 650 18 663 Retail banking market 18 663 17 651 16 076

204 240 246 Foreign retail banking market 246 240 20432 053 34 599 34 892 Deposits from customers 34 877 34 572 32 034

Note 8 - Deposits broken down by sector and industry

Group(Amounts in NOK million)

Note 6 - Loans broken down by sector and industry

Note 7 - Losses broken down by sector and industry

Parent Bank

15/22

Parent Bank Group

31.12.07 31.12.08 31.12.09 31.12.09 31.12.08 31.12.07

2 1 1 Repossessed assets 1 1 1

446 764 285 Accrued income 292 771 456

18 25 33 Prepayments 44 31 25

199 147 235 Other assets 241 247 255

665 937 554 Total other assets 578 1 050 737

442 504 471 Costs incurred 586 609 536

119 100 82 Provisioning against incurred liabilities and costs 107 105 125

357 274 539 Other liabilities 549 369 390

918 878 1 092 Total other liabilities 1 242 1 083 1 051

Note 10 - Other assets

Note 11 - Other liabilities

(Amounts in NOK million)

Note 12 - Investment in bonds

(Amounts in NOK million) 01.07.08 30.09.08 31.12.08 31.03.09 30.06.09 30.09.09 31.12.09Hold until maturityBook value 3 109 3 194 3 498 3 222 3 058 2 923 2 650Nominal value (nominal amount) 3 182 3 265 3 588 3 281 3 111 2 969 2 689Theoretical market value 3 109 3 122 3 358 3 053 2 942 2 885 2 623

Loans and claimsBook value 698 720 739 689 682 639 629Nominal value (nominal amount) 737 760 809 755 751 663 656Theoretical market value 698 687 675 650 646 621 599

Total book value 3 807 3 914 4 237 3 911 3 740 3 562 3 279

As a result of extraordinary market conditions, parts of the Bank’s ordinary securities portfolio became illiquid in 2008. Following the changes in international accounting standards in October 2008 (see note 1), the SNN Group decided to reclassify parts of the Bank’s bond portfolio as at 01.07.09 from the category ‘Market value with inclusion of value changes over the profit and loss account’ to the categories ‘Hold until maturity’ and ‘Loans and claims’ as the securities in question no longer was expected to be sold before maturity. In the category ‘Hold until maturity’ the Bank includes quoted securities, whereas unquoted securities has been put into the category of ‘Loans and claims.'

In the categories ‘Hold until maturity’ and ‘Loans and claims’ the securities are assessed at amortized cost. After the reclassification, the writedowns made earlier will be reversed over the portfolio’s remaining life, which on average is 1,91 year as at 31.12.09, and included in the profit and loss account as interest income. For the last half year of 2008, such inclusion of income amounts to NOK 18 million. As at 31.12.09 the amount booked as income is NOK 26 million. If the reclassification had not been made, the Group would have charged NOK 212 million to the profit and loss account in the third and fourth quarter of 2008 due to increased credit spreads. This unrealised loss would have been reduced to NOK 18 as at 31.12.09. It was necessary to apply a NOK 46 million write-down due to the permanent impairment of value in this portfolio as at 31.12.08. A further NOK 17 million write-down has been made on this part of the portfolio as at 31.12.09. The portfolio had an NOK 478 million unrealised loss on foreign exchange as at 31.12.08. As at 31.12.09 the loss was NOK 3 million.

Note 9 - Subsidiaries

(Amounts in NOK 1 000) EquityShare of Eq.% 31.12.09 31.12.08 31.12.07 31.12.09 31.12.08 31.12.07

SpareBank 1 Finans Nord-Norge AS 100 64 912 19 625 19 371 286 798 241 128 199 257

SpareBank 1 Nord-Norge Invest AS 100 -64 779 -33 831 13 238 -9 274 55 533 86 292

Eiendomsdrift AS 100 2 075 2 055 3 380 44 756 55 142 48 655

EiendomsMegler 1 Nord-Norge AS 100 3 783 -9 823 - 254 17 334 13 579 11 901

SpareBank 1 Nord-Norge Securities ASA 79.25 2 087 1 805 5 108 10 168 5 506 5 526

Sparebanken Factoring 0 637 4 858 0 0 14 980 0

BBL Eiendomsmegling AS 0 0 - 550 0 0 5 958 0

Profit from ordinary operations after tax

Sparebanken Factoring was sold at 31.03.09. BBL Eiendomsmegling AS are included in accounts for EiendomsMegler 1 Nord-Norge AS.

16/22

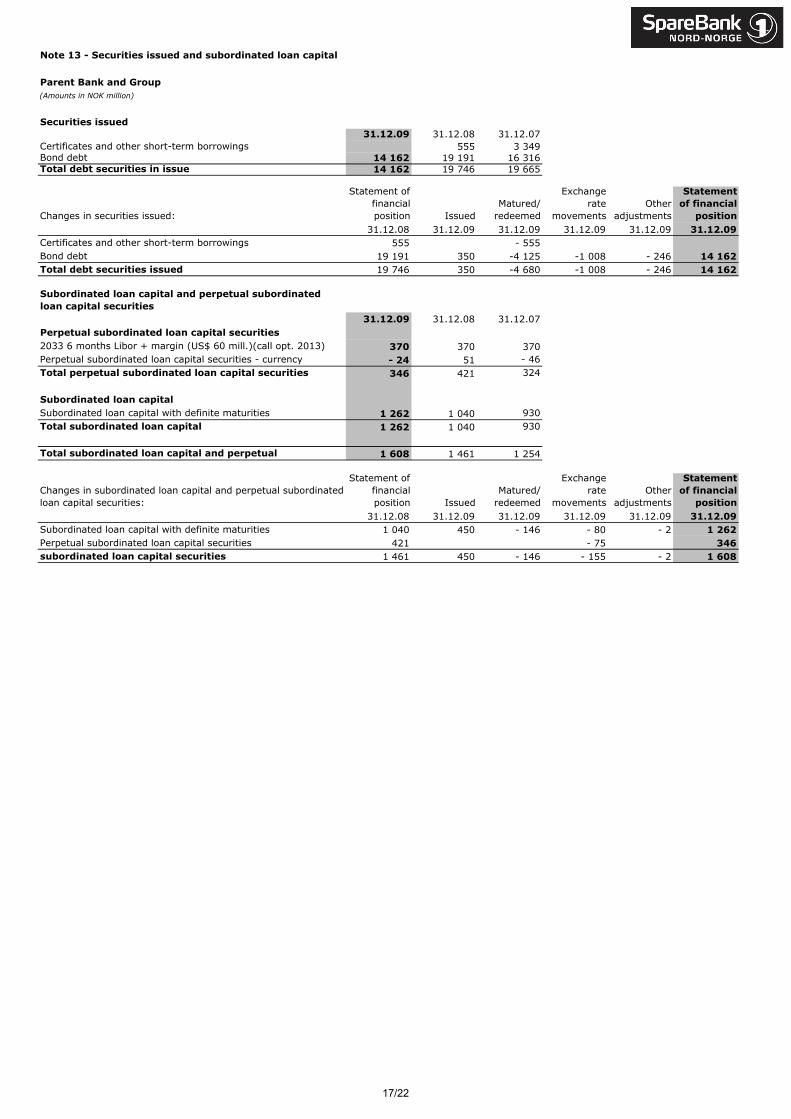

Parent Bank and Group(Amounts in NOK million)

Securities issued31.12.09 31.12.08 31.12.07

Certificates and other short-term borrowings 555 3 349Bond debt 14 162 19 191 16 316Total debt securities in issue 14 162 19 746 19 665

Changes in securities issued:

Statement of financial position Issued

Matured/redeemed

Exchange rate

movementsOther

adjustments

Statement of financial

position31.12.08 31.12.09 31.12.09 31.12.09 31.12.09 31.12.09

Certificates and other short-term borrowings 555 - 555 Bond debt 19 191 350 -4 125 -1 008 - 246 14 162Total debt securities issued 19 746 350 -4 680 -1 008 - 246 14 162

Subordinated loan capital and perpetual subordinated loan capital securities

31.12.09 31.12.08 31.12.07Perpetual subordinated loan capital securities2033 6 months Libor + margin (US$ 60 mill.)(call opt. 2013) 370 370 370Perpetual subordinated loan capital securities - currency - 24 51 - 46Total perpetual subordinated loan capital securities 346 421 324

Subordinated loan capitalSubordinated loan capital with definite maturities 1 262 1 040 930Total subordinated loan capital 1 262 1 040 930

Total subordinated loan capital and perpetual 1 608 1 461 1 254

Changes in subordinated loan capital and perpetual subordinated loan capital securities:

Statement of financial position Issued

Matured/redeemed

Exchange rate

movementsOther

adjustments

Statement of financial

position31.12.08 31.12.09 31.12.09 31.12.09 31.12.09 31.12.09

Subordinated loan capital with definite maturities 1 040 450 - 146 - 80 - 2 1 262Perpetual subordinated loan capital securities 421 - 75 346subordinated loan capital securities 1 461 450 - 146 - 155 - 2 1 608

Note 13 - Securities issued and subordinated loan capital

17/22

Note 14 - Financial derivatives

Parent Bank and Group

(Amounts in NOK million)

Fair value hedging transactions 31.12.09 31.12.08 31.12.07Net loss charged to the statement of comprehensive income in

respect of hedging instruments in connection with actual value 102 - 408 - 26

Total gain from hedging objects relating to the hedged risk - 74 375 23

Total fair value hedging transactions 28 - 33 - 3

Fair value through statement of comprehensive income 31.12.09 31.12.08 31.12.07

Fair value Fair value Fair value

Foreign currency instruments Contract Assets Liabilites Contract Assets Liabilites Contract Assets Liabilites

Foreign exchange financial derivatives (forwards) 3 367 28 38 5 280 16 31 4 776 2 5

Currency swaps 5 934 103 34 14 564 34 11 7 622 10 3

Currency options

Total non-standardised contracts 9 301 131 72 19 844 50 42 12 398 12 8

Standardised foreign currency contracts (futures)

Total foreign currency instruments 9 301 131 72 19 844 50 42 12 398 12 8

Interest rate instruments

Interest rate swaps (including cross currency) 15 743 134 196 12 566 170 272 8 302 101 58

Short,-term interest rate swaps (FRA)

Other interest rate contracts 173 5 9 986 19 31 725 112 131

Total non-standardised contracts 15 916 139 205 13 552 189 303 9 027 213 189

Standardised interest rate contracts (futures)

Total interest rate instruments 15 916 139 205 13 552 189 303 9 027 213 189

Hedging of funding loans

Foreign currency instruments

Foreign exchange financial derivatives (forwards)

Currency swaps

Total, non-standardised contracts

Standardised foreign currency contracts (futures)

Total foreign currency instruments

Interest rate instruments

Interest rate swaps (including cross currency) 6 808 291 42 8 373 408 22 6 239 51 100

Short-term interest rate swaps (FRA)

Other interest rate contracts

Total, non-standardised contracts 6 808 291 42 8 373 408 22 6 239 51 100

Standardised interest rate contracts (futures)

Total interest rate instruments 6 808 291 42 8 373 408 22 6 239 51 100

Total interest rate instruments 22 724 430 247 21 925 597 325 15 266 264 289

Total foreign currency instruments 9 301 131 72 19 844 50 42 12 398 12 8

Total 32 025 561 319 41 769 647 367 27 664 276 297

The Bank's main Board of Directors has determined limits for maximum risk for the Bank's interest rate positions. Routines have

been established to ensure that positions are maintained within these limits.

Interest rate swaps......................................... : Commitments to exchange one set of cash flow for another over an agreed period.

Foreign exchange derivatives........................... : Agreements to buy or sell a fixed amount of currency at an agreed future date at a rate of

exchange which has been agreed in advance Currency swaps.............................................. : Agreements relating to the swapping of currency- and interest rate terms and conditions,

periods and amounts having been agreed in advance. Interest rate- and currency swap agreements ... : Agreements involving the swapping of currency- and interest rate terms and conditions,

periods and amounts having been agreed in advance. Options ......................................................... : Agreements where the seller gives the buyer a right, but not an obligation to either sell or

buy a financial instrument or currency at an agreed date or before, and at an agreed amount.

SpareBank 1 Nord-Norge enters into hedging contracts with respected Norwegian and foreign banks in order to reduce its own risk. Financial

derivatives transactions are related to ordinary banking operations and are done in order to reduce the risk relating to the Bank’s funding

loans from the financial markets, and in order to cover and reduce risk relating to customer-related activities. Only hedging transactions relating to the Bank’s funding loan operations are defined as ‘fair value hedging’ in accordance with IFRS standard IAS 39. Other hedging

transactions are defined as ordinary accounts-related hedging. The Bank does not use cash flow hedging.

18/22

Note 15 - Business Areas

Group31.12.09

(Amounts in NOK million)Retail

Banking Market

Public Banking Market

Leasing Unallocated Total

Net interest income 599 539 98 - 18 1 218Net fee- and commission income 191 171 22 78 462Other operating income 0 0 0 479 479Operating costs 468 421 26 57 972Result before losses 322 289 94 482 1 187

Losses 16 154 14 1 185Result before tax 306 135 80 481 1 002

Loans and advances to customers 29 021 17 410 2 183 - 434 48 180Individual write-downs for impaired value on loans and advances to customers - 33 - 183 - 12 0 - 228Collective write-downs for impaired value on loans and advances to customers - 59 - 168 - 10 - 1 - 238Other assets 0 0 37 16 488 16 525Total assets per business area 28 929 17 059 2 198 16 053 64 239

Deposits from customers 18 909 15 983 0 - 15 34 877Other liabilities and equity capital 0 0 2 198 27 164 29 362Total equity and liabilities per business area 18 909 15 983 2 198 27 149 64 239

31.12.08

Net interest income 764 500 67 - 11 1 320Net fee- and commission income 208 137 - 2 51 394Other operating income 0 0 0 - 67 - 67Operating costs 529 346 26 70 971Result before losses 443 291 39 - 97 676

Losses - 7 175 15 0 183Result before tax 450 116 24 - 97 493

Loans and advances to customers 31 226 18 265 2 063 - 286 51 268Individual write-downs for impaired value on loans and advances to customers - 37 - 154 - 10 0 - 201Collective write-downs for impaired value on loans and advances to customers - 58 - 138 - 8 0 - 204Other assets 0 0 136 14 508 14 644Total assets per business area 31 131 17 973 2 181 14 222 65 507

Deposits from customers 17 905 16 694 0 - 27 34 572Other liabilities and equity capital 0 0 2 181 28 754 30 935Total equity and liabilities per business area 17 905 16 694 2 181 28 727 65 507

Management has made an assessment of which business areas are deemed reportable with respect to form of distribution, products and customers. The primary format of reporting takes as a starting point risk and yield profiles of various assets and reporting is divided into private customers (Retail Banking Market), business customers (Corporate and Public Market) and leasing. Apart from what is included in this list, the Group does not have any companies or segments which are of significant importance. The Bank operates in a limited geograpfical area and reporting along the lines of geograpfic segments provides little additional information.

19/22

Trading statistics

#NAVN?

741

885

2 55

9 20

461

8 83

181

5 20

31

270

439

1 20

1 37

2

259

220 58

3 33

558

8 98

567

7 54

7

2 11

8 73

842

1 87

339

6 16

156

8 41

7 781

553

181

045

281

907

275

475

1 02

6 88

765

2 31

6

2 57

6 47

642

2 44

1

621

058

366

282

0

500 000

1 000 000

1 500 000

2 000 000

2 500 000

3 000 000

jan.

08

feb.

08m

ar.0

8

apr.0

8m

ay.0

8

jun.

08

jul.0

8au

g.08

sep.

08

oct.0

8no

v.08

dec.

08

jan.

09

feb.

09m

ar.0

9

apr.0

9m

ay.0

9

jun.

09

jul.0

9au

g.09

sep.

09

oct.0

9no

v. 0

9de

c.09

Price trend NONG

0102030405060708090100110120130140150160170

jan.08

mar.08

mai.08

jul.08

sep.08

nov.08

jan.09

mar.09

mai.09

jun.09

aug.09

oct.09

dec.09

NOK

Note 16 - Primary Capital Certificates (PCCs)

The 20 largest PCC holders as at 31.12.09

Number Share of PCC Holders of PCCs PCC CapitalPareto Aksjer Norge 1 033 588 5.77%Pareto Aktiv 522 628 2.92%MP Pensjon 418 279 2.34%Frank Mohn AS 381 362 2.13%Tonsenhagen Forretningssentrum AS 319 126 1.78%Bank of New York Mellon, client account 285 430 1.59%Grunnfond Invest AS 239 821 1.34%Framo Development AS 238 798 1.33%JPMorgan Chase Bank, client account 213 996 1.19%Forsvarets Personellservice 172 034 0.96%Sparebanken Rogalands Pensjonskasse 165 407 0.92%Karl Ditlefsen, Tromsø 154 359 0.86%Sparebankstiftelsen 153 478 0.86%Trond Mohn 143 279 0.80%Citibank N.A. 140 154 0.78%Pareto VPF 139 520 0.78%Terra Utbytte Verdipapirfond 122 271 0.68%Olsen & Co’s pensjonskasse 121 787 0.68%JPMorgan Chase Bank, client account 117 769 0.66%Troms Kraft Invest AS, Tromsø 115 133 0.64%TOTAL 5 198 219 29.02%

Dividend policy