8/4/2019 Session 5 HDFC-JOINT CERTIFICATION PROGRAMME HDFC-IBS Mumbai

http://slidepdf.com/reader/full/session-5-hdfc-joint-certification-programme-hdfc-ibs-mumbai 1/66

SUPPORT SERVICES – MARKETING OF SERVICES PRODUCTS

Session 5- Dr.P.R.Kulkarni

4 / 1 8 / 2 0 1 2

1

D r .P .R .

K ul k ar ni

8/4/2019 Session 5 HDFC-JOINT CERTIFICATION PROGRAMME HDFC-IBS Mumbai

http://slidepdf.com/reader/full/session-5-hdfc-joint-certification-programme-hdfc-ibs-mumbai 2/66

MARKETING Generally, marketing is understood as selling of products or

services. Some consider advertising or promoting a product as

marketing.

The idea of marketing is much wider. It is essentially related tocustomer.

Market : the word market is common parlance refer to theplace where goods can be sold or bought.

Marketing :Marketing is the business function that identifies thecurrent unfulfilled need and wants, defines and measures theirmagnitude, determines which target markets the organization

can best serve and decide on appropriate products, services,and programmes to serve these market, thus market serves aslink between a society‟s need and its pattern of industrialresponse-Kotler

4 / 1 8 / 2 0 1 2

2

D r .P .R .K ul k ar ni

8/4/2019 Session 5 HDFC-JOINT CERTIFICATION PROGRAMME HDFC-IBS Mumbai

http://slidepdf.com/reader/full/session-5-hdfc-joint-certification-programme-hdfc-ibs-mumbai 3/66

MARKETING MANAGEMENT American Management Association has defined Marketing

Management as “ Marketing Management is the process of planning and executing the conception, pricing , promotionand distribution of goods ,services and idea to createexchanges with the target groups that satisfy customer andorganizational objective.”

Functions of Marketing Management :The functions ofmarketing management are : Analysis, Planning,Implementation and Control..

Analysis : There is need to understand customer,trends andchanges in the environment and internal strength andweaknesses for drawing out effective market plan.

This require collection of information on these ares.

4 / 1 8 / 2 0 1 2

3

D r .P .R .K ul k ar ni

8/4/2019 Session 5 HDFC-JOINT CERTIFICATION PROGRAMME HDFC-IBS Mumbai

http://slidepdf.com/reader/full/session-5-hdfc-joint-certification-programme-hdfc-ibs-mumbai 4/66

Planning : it covers both strategic planning for the longterm marketing direction of the firm –selection of target,estimate of requirement resources.

Implementation : The implementation of strategic andtactical plan requires staffing, allocation of task,budgeting ,

Control :Measurement and evaluation of progressagainst the goals and target spelt.

Products and services :A Product is defined as“anything that has the capacity to provide thesatisfaction, use or perhaps the profit desired by thecustomers. Product & service are usedinterchangeably in banking parlance.

Banks‟ products are their deposits / borrowing

schemes / other products like credit card or foreignexchange transaction which are tangible andmeasurable whereas service can be such products +the way / manner in which they are offered.

4 / 1 8 / 2 0 1 2

4

D r .P .R .K ul k ar ni

8/4/2019 Session 5 HDFC-JOINT CERTIFICATION PROGRAMME HDFC-IBS Mumbai

http://slidepdf.com/reader/full/session-5-hdfc-joint-certification-programme-hdfc-ibs-mumbai 5/66

What is services ? Kotler defines services as “ A

services is any act or performance that one party canoffer to another that is essentially intangible and does not

result in ownership of any things. Its production mayormay not be tied to a physical product”

Characteristics of Service products :

Intangibility : not in in the physical form –lecture given.

Inseparability : The consumer presence is in mostcases necessary at time of production.

Heterogeneity : The services offered are not similar alltime to all customer.

Perish ability : This means that service unit can not bestocked.

4 / 1 8 / 2 0 1 2

5

D r .P .R .K ul k ar ni

8/4/2019 Session 5 HDFC-JOINT CERTIFICATION PROGRAMME HDFC-IBS Mumbai

http://slidepdf.com/reader/full/session-5-hdfc-joint-certification-programme-hdfc-ibs-mumbai 6/66

MARKETING OF FINANCIAL SERVICES The characteristics of services such as intangibility, in

separation, ,heterogeneity and perishability, are presentin financial services too.

Financial Market in India consists of credit market, equitymarket, insurance market,the money market. Mutualfunds.

Marketing of Nanking products :Banking marketing is theaggregate function, directed at providing services tosatisfy the customer‟s financial needs and wants , moreeffectively than competitors keeping in view theorganizational objectives of the bank. It highlight on (1)Banks provide services (2) Aim is to satisfy customerneed (3) Nature of need financial products (4)competitive element ,effective and

4 / 1 8 / 2 0 1 2

6

D r .P .R .K ul k ar ni

8/4/2019 Session 5 HDFC-JOINT CERTIFICATION PROGRAMME HDFC-IBS Mumbai

http://slidepdf.com/reader/full/session-5-hdfc-joint-certification-programme-hdfc-ibs-mumbai 7/66

The team model includes:Service level management: Using service levelagreements as a basis for process/service improvement.User support: Making end-users aware of the facilities

available and be able to exploit them to the best effect insupport of their needs.Requirements/Change management: Monitoring therequirements of end-users and taking them into accountduring the ongoing development and delivery of services

and systems.Relationship management: Managing relationshipswith providers at all levels including: strategic, servicedelivery and contractual levels.Service management: Establishing suitable baselineson which to track performance relating to service deliveryand capability improvement.Business continuity: Establishing an ongoing appraisalof risk and assuring that the necessary servicecomponents are recognized within business continuityplans; ensuring that business continuity measures are

adequately tested.

4 / 1 8 / 2 0 1 2

7

D r .P .R .K ul k ar ni

8/4/2019 Session 5 HDFC-JOINT CERTIFICATION PROGRAMME HDFC-IBS Mumbai

http://slidepdf.com/reader/full/session-5-hdfc-joint-certification-programme-hdfc-ibs-mumbai 8/66

MANAGING SERVICE DELIVERY

There should be a detailedagreement of the requiredservice levels and thus theexpected performance andquality of service to be

delivered.Where the provider is an in-house

department, the level of servicerequired will be set out in aService Level Agreement (SLA).

Wherever there are formalagreements, on service levelsas elsewhere, there is often aneed for some flexibility. This isparticularly true in the earlystages of an agreement.

Establish what levels of service arerequiredService levelmanagement is the process ofmanaging the performanceprovided to the customer as

specified in the contractualperformance metrics.

It balances cost and quality ofservices in order to provide thecustomer with value for money.

Points to be consideredWhat needs to be done to maintainservice delivery

4 / 1 8 / 2 0 1 2

8

D r .P .R .K ul k ar ni

8/4/2019 Session 5 HDFC-JOINT CERTIFICATION PROGRAMME HDFC-IBS Mumbai

http://slidepdf.com/reader/full/session-5-hdfc-joint-certification-programme-hdfc-ibs-mumbai 9/66

Price comparisons offer a quickand effective way to gaugewhether you are getting value for

money.Providers could be obliged tobenchmark their own costs, orthose of their subcontractors, by

the contract.Compare the value for moneyyou are getting with what otherorganizations are getting.Compare the way you manage

contracts with the way otherorganizations manage theirs.

Compare prices and learn fromothers.Benchmarking is the practice ofmaking like-for-like comparisonsbetween organizations with theaim of ensuring continuing valuefor money, getting better

performance, and improvingbusiness practices.

MANAGING SERVICE DELIVERY (Contd.)

4 / 1 8 / 2 0 1 2

9

D r .P .R .K ul k ar ni

8/4/2019 Session 5 HDFC-JOINT CERTIFICATION PROGRAMME HDFC-IBS Mumbai

http://slidepdf.com/reader/full/session-5-hdfc-joint-certification-programme-hdfc-ibs-mumbai 10/66

Risks can relate to many aspectsof the contract, including

fluctuation in demand, lack ofprovider capacity, change inrequirement and transfer of skilledstaff (on either side).All risks should be identified andmanaged.Risks should be placed with theparty best placed to manage them

– possibly the provider, althoughthey will want compensation inreturn.

Risks placed with the provider arereferred to as „transferred risks‟.Business risk cannot betransferred to the provider. Thefinal responsibility for achieving

outcomes remains with thecustomer.

Manage the risks.Risk is defined as uncertainty of

outcome, whether positiveopportunity or negative threat.In the area of contractmanagement, managing riskmeans identifying and controllingfactors that may have an impact onfulfillment.

MANAGING SERVICE DELIVERY (Contd.)

4 / 1 8 / 2 0 1 2

10

D r .P .R .K ul k ar ni

8/4/2019 Session 5 HDFC-JOINT CERTIFICATION PROGRAMME HDFC-IBS Mumbai

http://slidepdf.com/reader/full/session-5-hdfc-joint-certification-programme-hdfc-ibs-mumbai 11/66

Aim to optimise the ratio betweenvalue and cost. Realising thatvalue for money is notsynonymous with lowest cost.Carefully consider all the benefitsthat the contract provides in

relation to the ongoing investmentit requires.All costs associated with thecontract must be taken intoconsideration: set-up costs,

recurring costs, fixed costs, unitcosts, and the organizations own

EnsureEnsuring value for money is aboutthe trade-off between servicequality and cost.A key objective for themanagement of any contract is to

ensure that it continues to achievevalue for money over time.

Quality measures might assesssuch aspects as completeness,availability, capacity, reliability,

flexibility and timeliness, amongothers.Some aspects of a service maybe measurable by numericalmeans; others may require

subjective assessment.

Measure quality as well as quantity.The quality of the service beingdelivered must be assessed.

This means creating and usingquality metrics - measurementsthat allow the quality of a service tobe measured.

MANAGING SERVICE DELIVERY (Contd.)

4 / 1 8 / 2 0 1 2

11

D r .P .R .K ul k ar ni

8/4/2019 Session 5 HDFC-JOINT CERTIFICATION PROGRAMME HDFC-IBS Mumbai

http://slidepdf.com/reader/full/session-5-hdfc-joint-certification-programme-hdfc-ibs-mumbai 12/66

It will normally be theprovider‟s responsibility to

manage service continuity,and this will be stipulatedin the contract but it willneed to be taken intoaccount in theorganization‟s widerbusiness continuity plan.Those aspects of a serviceidentified as critical may

require carefulconsideration and/or thecreation of a BusinessContinuity Plan.

Ensureservice continuityA major part of contract

management isconsidering servicecontinuity – what willhappen if the service fails oris interrupted.

MANAGING SERVICE DELIVERY (Contd.)

4 / 1 8 / 2 0 1 2

12

D r .P .R .K ul k ar ni

8/4/2019 Session 5 HDFC-JOINT CERTIFICATION PROGRAMME HDFC-IBS Mumbai

http://slidepdf.com/reader/full/session-5-hdfc-joint-certification-programme-hdfc-ibs-mumbai 13/66

PRODUCT

Product :Kotler has defined product thus “A product is any

thing that can be offered to market for attention , acquisition,use or consumption that might satisfy a want or needs.

Banking Products: Banks are in the business of acceptingthe deposits for lending or investment.

A typical retail banking product mix are :saving account,

current account, anywhere banking account, senior citizenaccount.

Fixed deposits , cumulative fix deposits, recurring deposits.

Loans : vehicle loans, housing loans, personal loan, creditcard

Other services : telephone bill payment, safe deposit lockerdemand draft ,demat account

4 / 1 8 / 2 0 1 2

13

D r .P .R .K ul k ar ni

8/4/2019 Session 5 HDFC-JOINT CERTIFICATION PROGRAMME HDFC-IBS Mumbai

http://slidepdf.com/reader/full/session-5-hdfc-joint-certification-programme-hdfc-ibs-mumbai 14/66

PRODUCT LIFE CYCLE

This concept is one of the fundamental notions andaffect the marketing strategies substantially.

1. This concept implies that a product have limitedlife span.

2. The sale of the product during its life span passesthrough distinct stages

3. Each of the stages poses different challengesopportunities and problems

4. Profit rise and fall at different stages

5. Different marketing strategies are required foreach of the four stages

4 / 1 8 / 2 0 1 2

14

D r .P .R .K ul k

ar ni

8/4/2019 Session 5 HDFC-JOINT CERTIFICATION PROGRAMME HDFC-IBS Mumbai

http://slidepdf.com/reader/full/session-5-hdfc-joint-certification-programme-hdfc-ibs-mumbai 15/66

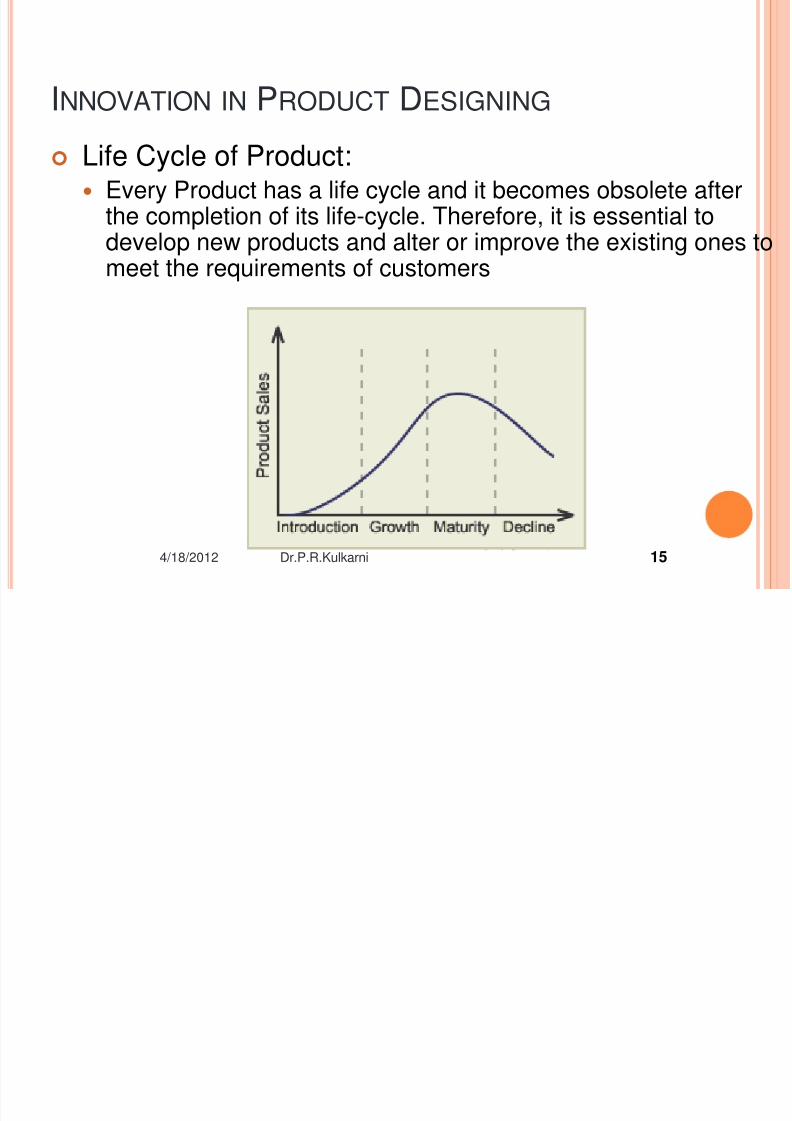

INNOVATION IN PRODUCT DESIGNING

Life Cycle of Product: Every Product has a life cycle and it becomes obsolete after

the completion of its life-cycle. Therefore, it is essential todevelop new products and alter or improve the existing ones to

meet the requirements of customers

4/18/2012 15Dr.P.R.Kulkarni

8/4/2019 Session 5 HDFC-JOINT CERTIFICATION PROGRAMME HDFC-IBS Mumbai

http://slidepdf.com/reader/full/session-5-hdfc-joint-certification-programme-hdfc-ibs-mumbai 16/66

Product Life Cycle (PLC) & Product Strategies:

Each product passes through he following stages in its life span

i) Introductory stage – low sales, negative profits due to lack ofawareness, limited distribution and unfamiliarity with the product.

ii) Growth stage – sales tend to grow and profits increase.Market acceptance is the key factor. Competitive strategies by otherbanks can affect the growth. Promotional strategies should be changedto keep up the sales.

iii) Maturity stage – indicator is initial stability and then slow down involume of sales / profit. This gives indication about changes in products /

strategies. iv) Decline stage – downward shift / drift in sales and reduction in profit

Using life cycle to manage marketing of products:

i. High growth rate in consumer durable, car and housing markets. Banksstarted giving liberal loans. Banks introduced new products.

ii. Demand was growing, so also competition. This resulted n maturity orsaturation which compelled some banks to adjust the pricing

downwards.iii. SB Accounts also reached maturity phase because of growing customer

awareness for higher yield products.iv. To overcome, banks started new products like flexi - accounts & also

products which provide safety, short term liquidity, comfortable yield andtax concessions.

16

4 / 1 8 / 2 0 1 2

D r .P .R .K ul k

ar ni

8/4/2019 Session 5 HDFC-JOINT CERTIFICATION PROGRAMME HDFC-IBS Mumbai

http://slidepdf.com/reader/full/session-5-hdfc-joint-certification-programme-hdfc-ibs-mumbai 17/66

NEW PRODUCT DEVELOPMENT

New Product Development Strategy:

It starts at the Maturity / Decline phase is due to lack ofdemand or obsolescence.

Stiff competition compels a bank to think of new ideas

for survival. Based on customer changing needs.

Based on new ideas from research and developmentteam.

4 / 1 8 / 2 0 1 2

17

D r .P .R .K ul k

ar ni

8/4/2019 Session 5 HDFC-JOINT CERTIFICATION PROGRAMME HDFC-IBS Mumbai

http://slidepdf.com/reader/full/session-5-hdfc-joint-certification-programme-hdfc-ibs-mumbai 18/66

STAGES IN NEW PRODUCT DEVELOPMENT

Generation of Product Ideas

Screening of Ideas

Commercial Feasibility

Product Designing & Evaluation

Test Marketing

Lunching the Product

4 / 1 8 / 2 0 1 2

18

D r .P .R .K ul k

ar ni

8/4/2019 Session 5 HDFC-JOINT CERTIFICATION PROGRAMME HDFC-IBS Mumbai

http://slidepdf.com/reader/full/session-5-hdfc-joint-certification-programme-hdfc-ibs-mumbai 19/66

PRODUCT DESIGNING & EVALUATION

The company must ask these questions: Whywould a customer buy this product ?, What wouldbe the benefit ?, How might this product be used ?

Test the usefulness of the new product idea withcustomers and have an understanding of theproduct as viewed by the customer.

4

/ 1 8 / 2 0 1 2

19

D r .P .R .K ul k

ar ni

8/4/2019 Session 5 HDFC-JOINT CERTIFICATION PROGRAMME HDFC-IBS Mumbai

http://slidepdf.com/reader/full/session-5-hdfc-joint-certification-programme-hdfc-ibs-mumbai 20/66

TEST MARKETING

Test marketing can be very time consuming,expensive and prone to competitive sabotage.

Companies must plan carefully during this stage.

It is the controlled release of the product so that the

sales, customer, manufacturing and supportorganizations can test and modify the product.

4

/ 1 8 / 2 0 1 2

20

D r .P .R .K ul k

ar ni

8/4/2019 Session 5 HDFC-JOINT CERTIFICATION PROGRAMME HDFC-IBS Mumbai

http://slidepdf.com/reader/full/session-5-hdfc-joint-certification-programme-hdfc-ibs-mumbai 21/66

LUNCHING THE PRODUCT

Launch of product consist of following:

Developing the Market.

Correct Sales channel.

Increasing volume to support the launch.

Supporting the product.

4

/ 1 8 / 2 0 1 2

21

D r .P .R .K ul k

ar ni

8/4/2019 Session 5 HDFC-JOINT CERTIFICATION PROGRAMME HDFC-IBS Mumbai

http://slidepdf.com/reader/full/session-5-hdfc-joint-certification-programme-hdfc-ibs-mumbai 22/66

FEEDBACK ON PRODUCT

PERFORMANCE.

New Product success depends on following:

Incorporating customer feedback based on Test Marketconducted.

Before incorporating feedback suitable quantitative and

qualitative measures should be analyzed.

4

/ 1 8 / 2 0 1 2

22

D r .P .R .K ul k

ar ni

8/4/2019 Session 5 HDFC-JOINT CERTIFICATION PROGRAMME HDFC-IBS Mumbai

http://slidepdf.com/reader/full/session-5-hdfc-joint-certification-programme-hdfc-ibs-mumbai 23/66

Product Analysis:

Product Mix analysis is imperative to decide oncontinuance of existing products or adding newproducts, based on market research in thefollowing aspects –

• Potential demand

• GAP analysis

• SWOT analysis for the bank

4

/ 1 8 / 2 0 1 2

23

D r .P .R .K ul k

ar ni

8/4/2019 Session 5 HDFC-JOINT CERTIFICATION PROGRAMME HDFC-IBS Mumbai

http://slidepdf.com/reader/full/session-5-hdfc-joint-certification-programme-hdfc-ibs-mumbai 24/66

Strategies for growth in business & profits:

1. Market Penetration:

Market Penetration involves increasing sales of

an existing product in existing market. This ispossible through three strategies

i. Increasing current rate of use of a product

ii. Attracting competitive customers – SWOT

analysisiii. Attracting non-users of a product – cross selling

4

/ 1 8 / 2 0 1 2

24

D r .P .R .K ul k

ar ni

8/4/2019 Session 5 HDFC-JOINT CERTIFICATION PROGRAMME HDFC-IBS Mumbai

http://slidepdf.com/reader/full/session-5-hdfc-joint-certification-programme-hdfc-ibs-mumbai 25/66

2. Market Development – strategies involve increase in marketingeffort for existing products in new markets, attracting newcustomers for existing products and expanding areas of

business.

3. Product Development –

4. Product Diversification

It can be shown through the following figure:

4

/ 1 8 / 2 0 1 2

25

D r .P .R .K ul k

ar ni

Existing Market New Market

Existing Products

New Products

Market Penetration A

Product Development C

Market Development B

Diversification D

8/4/2019 Session 5 HDFC-JOINT CERTIFICATION PROGRAMME HDFC-IBS Mumbai

http://slidepdf.com/reader/full/session-5-hdfc-joint-certification-programme-hdfc-ibs-mumbai 26/66

4

/ 1 8 / 2 0 1 2

26

D r .P .R .K ul k

ar ni

Product Strategy Market Strategies

No market change Improved market New Market

No Product

Change

Design simplification

Greater integration

Branding change

Change in package

New uses

New users

Product Change Product line

simplification

New models

Product

customerisation

Market extension

New Product Replacement of old

product

Diversification Product

Diversification

8/4/2019 Session 5 HDFC-JOINT CERTIFICATION PROGRAMME HDFC-IBS Mumbai

http://slidepdf.com/reader/full/session-5-hdfc-joint-certification-programme-hdfc-ibs-mumbai 27/66

Product Management (Contd ) Product Development / Innovation: Role of Product in Customer Satisfaction: Any product or service developed by a bank has to satisfy the needs

of the customer. General Need of Customers are

Financial Security Quick Service Convenience Attractive Yield Low Cost Loans Personalized Service Advice / Counselling

Easy Access Simple Procedure Attractive Package Friendly Approach Variety of Products This list is only illustrative

4

/ 1 8 / 2 0 1 2

27

D r .P .R .K ul k

ar ni

8/4/2019 Session 5 HDFC-JOINT CERTIFICATION PROGRAMME HDFC-IBS Mumbai

http://slidepdf.com/reader/full/session-5-hdfc-joint-certification-programme-hdfc-ibs-mumbai 28/66

Product Management (Contd )

Product Development / Innovation:

Role of Product in Customer Satisfaction:

The product conceptualization and developmenthas to bear these needs in mind.

For example, using the PLC approach seenearlier a banker may group these needs into

following segments:

4

/ 1 8 / 2 0 1 2

28

D r .P .R .K ul k

ar ni

8/4/2019 Session 5 HDFC-JOINT CERTIFICATION PROGRAMME HDFC-IBS Mumbai

http://slidepdf.com/reader/full/session-5-hdfc-joint-certification-programme-hdfc-ibs-mumbai 29/66

Thus some needs like safety, liquidity, better yield,personalized service and convenient location and timingare the common factors which have to satisfied by anybank‟s product.

4

/ 1 8 / 2 0 1 2

29

D r .P .R .K ul k

ar ni

Young Customers A Family with teenage

children

A retired couple

Would prefer a bank which

provides security,

convenience and quick,

friendly service at convenient

hours

Would have need for proper

saving with safety of funds

reasonable yield and

availability of low cost loans

for children’s education,

convenient location and

convenient hours

Would prefer high safety,

higher yield, counselling

advice and personalized

service at convenient

location

8/4/2019 Session 5 HDFC-JOINT CERTIFICATION PROGRAMME HDFC-IBS Mumbai

http://slidepdf.com/reader/full/session-5-hdfc-joint-certification-programme-hdfc-ibs-mumbai 30/66

4

/ 1 8 / 2 0 1 2

30

D r .P .R .K ul k

ar ni

8/4/2019 Session 5 HDFC-JOINT CERTIFICATION PROGRAMME HDFC-IBS Mumbai

http://slidepdf.com/reader/full/session-5-hdfc-joint-certification-programme-hdfc-ibs-mumbai 31/66

PRODUCT MODIFICATION

In the maturity stage of its life cycle the sale of the

product decline. At this stage, efforts to stimulate sales of the product are

made by modifying the product . They are:

1. Quality improvement :Objective of improving the

functional performance.2. Features Improvement : Additional of new features

3. Style improvement :improvement in aesthetic appeal.

The purpose of making such modification is to get more

consumers in using the products

4

/ 1 8 / 2 0 1 2

31

D r .P .R .K ul k

ar ni

8/4/2019 Session 5 HDFC-JOINT CERTIFICATION PROGRAMME HDFC-IBS Mumbai

http://slidepdf.com/reader/full/session-5-hdfc-joint-certification-programme-hdfc-ibs-mumbai 32/66

Product Management (Contd )

Product Development / Innovation:

Innovating a product essentially means developing a productresulting in an increase in the product line.

New product development starts with the maturity or decline of an

existing product line or due to lack of demand or due toobsolescence of a product. Stiff competition compels a bank to thinkof new ideas for survival or success in a given market. Based onchanging customer wants and needs the bank‟s market researchdepartment generates new ideas.

The very modern manifestation of new product development hasbeen the customer-convenient-credit card.

Normally such ideas for new products pass through following stages:

(Contd on next slide)

4

/ 1 8 / 2 0 1 2

32

D r .P .R .K ul k

ar ni

8/4/2019 Session 5 HDFC-JOINT CERTIFICATION PROGRAMME HDFC-IBS Mumbai

http://slidepdf.com/reader/full/session-5-hdfc-joint-certification-programme-hdfc-ibs-mumbai 33/66

ENHANCEMENTS / MODIFICATION BASED

ON FEEDBACK.

Customer feedback can result into followingenhancements:

Modification in existing design of product.

Additional security features.

Customized Statement.

Online Banking facilities etc.

Based on feasibility study above feedbacks can beimplemented subject to availability of resources andbenefits.

4

/ 1 8 / 2 0 1 2

33

D r .P .R .K ul k

ar ni

8/4/2019 Session 5 HDFC-JOINT CERTIFICATION PROGRAMME HDFC-IBS Mumbai

http://slidepdf.com/reader/full/session-5-hdfc-joint-certification-programme-hdfc-ibs-mumbai 34/66

PRODUCT DIVERSIFICATION

Diversification refers to entering attractive opportunitieswhich are outside the existing business of the firm.

There are three types of diversifications ;

Concentric diversification Horizontal diversification

Conglomerate diversification

4

/ 1 8 / 2 0 1 2

34

D r .P .R .K ul k

ar ni

8/4/2019 Session 5 HDFC-JOINT CERTIFICATION PROGRAMME HDFC-IBS Mumbai

http://slidepdf.com/reader/full/session-5-hdfc-joint-certification-programme-hdfc-ibs-mumbai 35/66

BRANDING OF BANKING PRODUCT

Brand is the name, term, sign, symbol . or design orcombination of these.

Brand has become an important part of the product asthey import the perceived vale to the product.

Branding of service product is not new to us.

LIC brought out its product with brand names even whenthere was no competition.

Bank brand their product and customers are familiarizedwith this brand names.

Seven financial institutions found place in the list top 100brands.

4

/ 1 8 / 2 0 1 2

35

D r .P .R .K ul k

ar ni

8/4/2019 Session 5 HDFC-JOINT CERTIFICATION PROGRAMME HDFC-IBS Mumbai

http://slidepdf.com/reader/full/session-5-hdfc-joint-certification-programme-hdfc-ibs-mumbai 36/66

Most of them were from North American and Europeanregion.

Branding in the bank use to display the trust and

confidence because the customers preference wassecurity of money.

City ever sleeps (city Bank), World Local bank –HSBC,trusted family bank –Dena Bank, Building Relationship

beyond time and Taking technology to common man-Indian Bank

Good people to grow with –IOB are the some of theexample of branding bank services.

4

/ 1 8 / 2 0 1 2

36

D r .P .R .K ul k

ar ni

8/4/2019 Session 5 HDFC-JOINT CERTIFICATION PROGRAMME HDFC-IBS Mumbai

http://slidepdf.com/reader/full/session-5-hdfc-joint-certification-programme-hdfc-ibs-mumbai 37/66

. Elements of Product Mix or Product Package:

Product Mix means the total range of products offered by a bank.

Product Mix has three main characteristics:

i) Width, ii) Depth & iii) Consistency. Depth depends upon number of products in each line.

Consistency means whether products have production affinity &market affinity.

Frequent changes are made in Product Mix for diversification.

Broader Product Mix enables better business turnover and minimizethe risk of failure.

4

/ 1 8 / 2 0 1 2

37

D r .P .R .K ul k

ar ni

8/4/2019 Session 5 HDFC-JOINT CERTIFICATION PROGRAMME HDFC-IBS Mumbai

http://slidepdf.com/reader/full/session-5-hdfc-joint-certification-programme-hdfc-ibs-mumbai 38/66

Factors affecting Product Mix Product Package:

i. Cost of production / Delivery

ii. Demand from customers

iii. Advertising / Distribution Costiv. Policy of the Bank

Acceptability of Product / Product Mix depends on:

i. Consumer acceptance

ii. Satisfactory performanceiii. Adequate distribution

iv. Effective packaging/ branding

v. Good service / delivery

4

/ 1 8 / 2 0 1 2

38

D r .P .R .K ul k

ar ni

8/4/2019 Session 5 HDFC-JOINT CERTIFICATION PROGRAMME HDFC-IBS Mumbai

http://slidepdf.com/reader/full/session-5-hdfc-joint-certification-programme-hdfc-ibs-mumbai 39/66

Branding in Marketing: A brand is the name or design which identifies the products or services of

a manufacturer and distinguishes them from those of competitors.

Generally before deciding brands, the following questions have toanswered satisfactorily:

1. Is the brand name essential?

2. What brand name would suit?3. Should product be branded separately or as a product line?

4. Is it necessary to segment a market for each brand?

5. Is brand needed for strengthening existing market segment or form anew product?

While selecting a brand name a bank should:

i. Choose a short & simple one

ii. Prefer one which is easy to pronounce and remember

iii. Avoid confusing or negative connotations

iv. Ensure that it suits the characteristics of a product market

v. If the bank‟s name is highly established & accepted the brand name should includethat (bank‟s) name also like „Citicard‟ or „Indbank‟ fund or „Bobcard‟, etc

4

/ 1 8 / 2 0 1 2

39

D r .P .R .K ul k ar ni

8/4/2019 Session 5 HDFC-JOINT CERTIFICATION PROGRAMME HDFC-IBS Mumbai

http://slidepdf.com/reader/full/session-5-hdfc-joint-certification-programme-hdfc-ibs-mumbai 40/66

BRANDING IN MARKETING

Advantages of Branding to Buyers (Customers)

a) Brands are dependable guides to contents, processes,qualities, etc

b) They make shopping of various products feasible andconvenient

c) They assure satisfaction

d) They satisfy the status needs or the emotional needs ofthe customers

4

/ 1 8 / 2 0 1 2

40

D r .P .R .K ul k ar ni

Ad f B di S ll (B k)

8/4/2019 Session 5 HDFC-JOINT CERTIFICATION PROGRAMME HDFC-IBS Mumbai

http://slidepdf.com/reader/full/session-5-hdfc-joint-certification-programme-hdfc-ibs-mumbai 41/66

Advantages of Branding to Sellers (Bank)

a) It ensures repeat sales through identification

b) It ensures product stability through customer

loyaltyc) It helps segmenting a market

d) Customer even pays a higher price for brandedproduct than an unbranded

e) It shields from price competition

f) Successful brands add to the corporate image ofthe bank

The brand establishes after undergoing thefollowing chain:

Rejection Non-recognition Recognition Preference Loyalty Insistence Repeat Buying

4

/ 1 8 / 2 0 1 2

41

D r .P .R .K ul k ar ni

8/4/2019 Session 5 HDFC-JOINT CERTIFICATION PROGRAMME HDFC-IBS Mumbai

http://slidepdf.com/reader/full/session-5-hdfc-joint-certification-programme-hdfc-ibs-mumbai 42/66

Branding in Marketing: Role of Brand inBank Marketing:

In banking industry as the competition is „cut

throat‟ and products are quite similar as to the

basic nature and benefits / returns to thecustomers the service delivery and branding areexcellent tools which enable a bank to createand maintain an image among the customers

4

/ 1 8 / 2 0 1 2

42

D r .P .R .K ul k ar ni

I I di th b k h b ti th i di ti t k b

8/4/2019 Session 5 HDFC-JOINT CERTIFICATION PROGRAMME HDFC-IBS Mumbai

http://slidepdf.com/reader/full/session-5-hdfc-joint-certification-programme-hdfc-ibs-mumbai 43/66

In India the banks have been creating their distinct marks byestablishing sign offs for their total image like „A bank with

personal touch’ or „Friendly Bank’, ‘ Good to Bank With’; ‘ Bank to

bank upon’ or ‘Growing with you’, etc.

Such sign offs, indicates the positioning adopted by a bank withinthe perceptual marketplace to gain a more advantageousposition

Some examples of brands are:

4

/ 1 8 / 2 0 1 2

43

D r .P .R .K ul k ar ni

Bank Prodcut Brand

Citi Bank

State Bank of India

Canara bank

Indian Bank

Citi Bank

Credit Card

Mutual Fund

Growth Fund Schemes

Housing Loan

Car Loans

Citi Bank card

SBI Mutual Fund

Can Growth

Can ShareInd Shelter

Citimobile

8/4/2019 Session 5 HDFC-JOINT CERTIFICATION PROGRAMME HDFC-IBS Mumbai

http://slidepdf.com/reader/full/session-5-hdfc-joint-certification-programme-hdfc-ibs-mumbai 44/66

Branding in Marketing:

It can be, therefore, said that brands are very important asproduct (marketing) strategy in marketing of bank‟s services

as branding indicates how the organization chooses to usebranding as an integral part of its overall marketing strategy

To the customer such brand name means a means to identifythe product and differentiate the product from other similarproducts in the market.

In a customer‟s language, two questions have to answered

satisfactorily in this branding effort:

i. What is it in this bank which is different form other banksin terms of its position, sign off and product range?

ii. What are the product brands which are more beneficialwhich this bank offers distinct from other bank‟s products?

4

/ 1 8 / 2 0 1 2

44

D r .P .R .K ul k ar ni

8/4/2019 Session 5 HDFC-JOINT CERTIFICATION PROGRAMME HDFC-IBS Mumbai

http://slidepdf.com/reader/full/session-5-hdfc-joint-certification-programme-hdfc-ibs-mumbai 45/66

4

/ 1 8 / 2 0 1 2

45

D r .P .R .K ul k ar ni

8/4/2019 Session 5 HDFC-JOINT CERTIFICATION PROGRAMME HDFC-IBS Mumbai

http://slidepdf.com/reader/full/session-5-hdfc-joint-certification-programme-hdfc-ibs-mumbai 46/66

PRICING OF BANKING PRODUCTS

Price is the second major element of marking mix.

Price is the only one that generate revenue while otherelements incurred cost.

Several factors influence price and hence its determination iscomplex process.

Objectives of Pricing: there are several objectives whichfirms have in pricing.

Out of these objectives some are primary and secondary

The objectives generally pursued by the firm in setting pricesof product can broadly classified in seven major objective

1. Profit 2. survival 3. Market shre 4. Cash flow 5. status-quo 6Product quality 7 communication image

4

/ 1 8 / 2 0 1 2

46

D r .P .R .K ul k ar ni

8/4/2019 Session 5 HDFC-JOINT CERTIFICATION PROGRAMME HDFC-IBS Mumbai

http://slidepdf.com/reader/full/session-5-hdfc-joint-certification-programme-hdfc-ibs-mumbai 47/66

PRICING OF BANK PRODUCT AND SERVICES

There are two major cost which have to considered while

pricing bank products They are (a) interest cost (b) servicing cost

Normally interest cost constitutes 67% o the price andservice cost is around 33% in any bank products . Banknow price each of their services.

Traditionally, bank have been adopting pricing (ROI) onthe basis of value of loan or best on the development ofpriorities.

But these days ROI offered deposits and charge on loans

and advances is :1. Cost of fund based

2. Market related

4

/ 1 8 / 2 0 1 2

47

D r .P .R .K ul k ar ni

8/4/2019 Session 5 HDFC-JOINT CERTIFICATION PROGRAMME HDFC-IBS Mumbai

http://slidepdf.com/reader/full/session-5-hdfc-joint-certification-programme-hdfc-ibs-mumbai 48/66

Other factors which impact in Bank pricing :

1. Risk and Return

2. Monetary Policy

3. Capital adequacy4. Cost befit analysis

4 / 1 8 / 2 0 1 2

48

D r .P .R .K ul k ar ni

8/4/2019 Session 5 HDFC-JOINT CERTIFICATION PROGRAMME HDFC-IBS Mumbai

http://slidepdf.com/reader/full/session-5-hdfc-joint-certification-programme-hdfc-ibs-mumbai 49/66

DISTRIBUTION CHANNEL

The goods reach from producers to consumersthrough a chain of entities associated with theprocess directly or indirectly.

Service products (bank) have distinct

characteristics hence the distribution of serviceproduct is complex.

Banking services mainly depend upon directdistribution through own net work of the branches.

With the technological revolution in banking in

addition branches many more delivery channels areused by the banks to make their product reach thecustomer.

4 / 1 8 / 2 0 1 2

49

D r .P .R .K ul k ar ni

8/4/2019 Session 5 HDFC-JOINT CERTIFICATION PROGRAMME HDFC-IBS Mumbai

http://slidepdf.com/reader/full/session-5-hdfc-joint-certification-programme-hdfc-ibs-mumbai 50/66

Branches are the primary distribution outlets forbanking services. These fixed in location andconsumers are required to visit the branch for thetransactions.

Technological Channels :

Telephone banking and call centers

Automated teller machines

Personal computer

Plastic cards

Virtual branches and automated video banking.

4 / 1 8 / 2 0 1 2

50

D r .P .R .K ul k ar ni

8/4/2019 Session 5 HDFC-JOINT CERTIFICATION PROGRAMME HDFC-IBS Mumbai

http://slidepdf.com/reader/full/session-5-hdfc-joint-certification-programme-hdfc-ibs-mumbai 51/66

4 / 1 8 / 2 0 1 2

51

D r .P .R .K ul k ar ni

8/4/2019 Session 5 HDFC-JOINT CERTIFICATION PROGRAMME HDFC-IBS Mumbai

http://slidepdf.com/reader/full/session-5-hdfc-joint-certification-programme-hdfc-ibs-mumbai 52/66

S ALES & DISTRIBUTION S YSTEM

Sales Promotion:

Sales Promotion means, the bank‟s well organized, planned

and goal oriented efforts which must 52be in line with itsoverall business goals and objectives in the desired marketareas keeping specific needs of customers in mind.

The promotion efforts include the communication channels of:

o Advertising

o Publicity

o Sales Promotion

o Person-to-person communicationo Bank‟s internal communication process, etc.

4 / 1 8 / 2 0 1 2

52

D r .P .R .K ul k a

r ni

8/4/2019 Session 5 HDFC-JOINT CERTIFICATION PROGRAMME HDFC-IBS Mumbai

http://slidepdf.com/reader/full/session-5-hdfc-joint-certification-programme-hdfc-ibs-mumbai 53/66

Composition of Product Mix

4 / 1 8 / 2 0 1 2

53

D r .P .R .K ul k a

r ni

Mass Communication Person-to-Person Communication

Advertising Personal Sales

Publicity Internal Communication

Sales Promotion

Public Relation

Objectives of Sales Promotion:

Objectives of Sales Promotion are:

1. Informing/telling/educating potential customer

2. Informing existing customers about new products / services

3. Following up with existing/potential customers for schemes introduced4. Approaching a new segment of customers to attract them to promote new

scheme.

8/4/2019 Session 5 HDFC-JOINT CERTIFICATION PROGRAMME HDFC-IBS Mumbai

http://slidepdf.com/reader/full/session-5-hdfc-joint-certification-programme-hdfc-ibs-mumbai 54/66

Distribution Channels:

Direct Channels:

i. Branch Network

ii. Electronic Channels – ATM, Internet Banking, PhoneBanking, Mobile Phone Banking, Online Anywhere Banking,etc

iii. Banking at door step

In-Direct Channels:

i. Direct Marketing Agents (DMS)

ii. Direct Selling Agents (DSA) – Telemarketing Executives(TMEs), Field Sales Personnel, namely Direct SalesExecutives (DSE),/ Business Development Executives(BDEs)

Issues to be considered:

Channel Selection Channel Management

Empanelment of channel partners

Monitoring a channel partner – integrity, performance &productivity rewards.

4 / 1 8 / 2 0 1 2

54

D r .P .R .K ul k a

r ni

8/4/2019 Session 5 HDFC-JOINT CERTIFICATION PROGRAMME HDFC-IBS Mumbai

http://slidepdf.com/reader/full/session-5-hdfc-joint-certification-programme-hdfc-ibs-mumbai 55/66

DSA (DIRECT SELLING AGENTS)

WITH limited branch networks, private sector banks areincreasingly depending on outside agencies to sell theirretail products

These sales personnel are given variable pay dependingon the volumes of business they bring in, making the

situation very tricky if the bank is not careful in tracking thequality of the assets they bring in.

ICICI Bank has seen 100 per cent of its incremental growthin its home loan portfolio through its DSA network. Homeloans disbursed by ICICI Bank for the year 2002-03 were

Rs 7,000 crore. Even its, by now famous, `loan melas' areconducted by DSAs under the supervision of itsemployees.

4 / 1 8 / 2 0 1 2

55

D r .P .R .K ul k a

r ni

8/4/2019 Session 5 HDFC-JOINT CERTIFICATION PROGRAMME HDFC-IBS Mumbai

http://slidepdf.com/reader/full/session-5-hdfc-joint-certification-programme-hdfc-ibs-mumbai 56/66

BANKER AS A DSA/DMA

In a bank branch DSA/DMA is the branch manager,

officer, manager , marketing manager, the front linepeople and sub staff who offer various services

The banking offers various non –conventional services tocustomers.

The job of the DMA/DSA is to collect the information

about the customer with all details and create a database.

Create awareness among the customer educate themabout the user friendliness of the system.

Convince them about the security aspects, generatereport to accommodate the need of the customers andmanagement.

4 / 1 8 / 2 0 1 2

56

D r .P .R .K ul k a

r ni

8/4/2019 Session 5 HDFC-JOINT CERTIFICATION PROGRAMME HDFC-IBS Mumbai

http://slidepdf.com/reader/full/session-5-hdfc-joint-certification-programme-hdfc-ibs-mumbai 57/66

DMA (DIRECT MARKETING AGENTS)

Role of Direct Marketing Agents in banks are following: To market and publicize the loan schemes / products of banks

DMA collect the loan applications of the interested parties with requisitefees as per rules of the bank in the shape of cheques / draft and deliverto the concerned bank's branch.

To carry on thorough verification of the account to be introduced – of the

applicants, seller of the property, guarantors and property to be providedas security for loan.

To educate the customers on the policies and terms of lending of bankand to cover the company against any claim or damage arising out ofnon-compliance of any of the terms and conditions as above.

To ensure regular payment of installments in the accounts introduced byhim and timely deposition of Post Dated Cheques.

To ensure recovery in the event of default / non-payment in any account. To protect the interest of the company and ensure that image of the

company is not tarnished by any deeds performed / statements made byhim.

4 / 1 8 / 2 0 1 2

57

D r .P .R .K ul k a

r ni

8/4/2019 Session 5 HDFC-JOINT CERTIFICATION PROGRAMME HDFC-IBS Mumbai

http://slidepdf.com/reader/full/session-5-hdfc-joint-certification-programme-hdfc-ibs-mumbai 58/66

Direct Selling Agents (DSA)

Code of Conduct for Direct Selling Agents:

Declaration to abide by the Code of Conduct

Salient aspects of the Code of Conduct Tele-calling a prospective customer (Prospect)

Consent to be obtained Not to call a person who is flagged in “do not disturb list”

Time of contact – normally between 09:30 hrs & 19:00 hrs

Maintain prospects privacy

Leaving a message in the event when the prospect is notavailable – the message must indicate the purpose of call; isregarding, selling or distributing a bank product.

No misleading statements / misrepresentations permitted

Tele-marketing antiquates – pre-call, during call, post-call.

Gifts or bribes –

not to accept any gifts / bribes of any kind fromprospects

Precautions to be taken on visits / contacts – maintain adequatedistance, no visiting large numbers, etc

Other important aspects – appearance & dress code

4 / 1 8 / 2 0 1 2

58

D r .P .R .K ul k a

r ni

8/4/2019 Session 5 HDFC-JOINT CERTIFICATION PROGRAMME HDFC-IBS Mumbai

http://slidepdf.com/reader/full/session-5-hdfc-joint-certification-programme-hdfc-ibs-mumbai 59/66

MONITORING A CHANNEL PARTNER

As channel partnerships develop and become morecomplex, however, the need to measure their effectivenessbecomes crucial. banks not content with mere incrementalrevenue are looking for ways to analyze channels, refinethem for maximum return and avoid any pitfalls.

the most sophisticated metric is analyzing which individualpartners is performing well or poorly. That means findingways to assign appropriate sales allocation to individualactivity and pinpointing the exact location of the point ofsale,

Automated systems, such as MarketStar'sPartnerDynamics software, can help manage channelinitiatives with a list of daily activities for specific DSAs

4 / 1 8 / 2 0 1 2

59

D r .P .R .K ul k a

r ni

8/4/2019 Session 5 HDFC-JOINT CERTIFICATION PROGRAMME HDFC-IBS Mumbai

http://slidepdf.com/reader/full/session-5-hdfc-joint-certification-programme-hdfc-ibs-mumbai 60/66

INTEGRITY

Globally, the banking and financial services sector is one ofthe largest users of information systems. This has held truein India too, where banks and financial institutions are oneof the largest deployers of IT in the country.

With the RBI actively encouraging the banks to shift tointernet banking and advocating real-time clearingsystems, the IT adoption rate in the banking industry isbound to increase. Banks with a smaller footprint are alsocatching up with the larger players in moving towardsconnected systems. As technology adoption takes place ona war footing, care should be taken that effective securitysystems and IT safeguards are in place.

The off shoring of the back end processing transactions of

global financial institutions to India has increased theimportance of security. Maintaining the integrity,confidentiality and availability of data is a new concern thatbanks have to contend with.

4 / 1 8 / 2 0 1 2

60

D r .P .R .K ul k a

r ni

8/4/2019 Session 5 HDFC-JOINT CERTIFICATION PROGRAMME HDFC-IBS Mumbai

http://slidepdf.com/reader/full/session-5-hdfc-joint-certification-programme-hdfc-ibs-mumbai 61/66

PRODUCTIVITY REWARDS

Cash incentives are in the form of a bonus. A bonus is anincentive payment that is supplemental to the base wage. Ithas the advantage of providing employees with more payfor putting out a greater effort. A Spot bonus could also beused; it is an unplanned bonus given for an employeeseffort unrelated to an established performance measure.For example, an employee may receive a spot bonus for

working long hours to keep a client or fill their order. Manyservice managers are finding that cash is not as powerfulfor motivating a employees performance. Today'semployees want more from their jobs than just money;people want higher positions and internal recognition

Incentives can also be in the form of non-cash items. Themost popular of the non-cash incentives include free

merchandise, travel, recognition and status. Other types ofnon-cash incentives are, tuition credits, shares of stock,consumer merchandise, flexible working hours, companycar, paid time off as well as health services

4 /

1 8 / 2 0 1 2

61

D r .P .R .K ul k a

r ni

FINANCIAL PLANNING AND FINANCIAL ADVISORY

8/4/2019 Session 5 HDFC-JOINT CERTIFICATION PROGRAMME HDFC-IBS Mumbai

http://slidepdf.com/reader/full/session-5-hdfc-joint-certification-programme-hdfc-ibs-mumbai 62/66

18 April 2012 Dr. P.R Kulkarni 62

RESPONSIBILITIES

Financial planning is the process of establishing personal and financial goals of anindividual and his/her family and meeting them through proper management ofhis/her personal finance. The financial goals may involve buying a home or a car,children‟s marriage and education, funds for medical treatment, retirement,vacation abroad etc. The on-going process involves taking stock of all existingresources, developing a plan to use them, and systematically implementing theplan in order to achieve short and long-term goals. The plan must be monitoredand reviewed periodically so that adjustments can be made, if necessary, toassure that it continues to move toward the client‟s financial goals.

Financial Planner is an expert in the process of financial planning which essentiallyinvolves: establishing and defining the client-planner relationship; gathering clientdata, including goals; analyzing and evaluating the client's financial status;developing and presenting financial planning recommendations and/oralternatives; implementing the financial planning recommendations and monitoringthe financial planning recommendations. Using this process, financial planner can

help his clients work out where they want to be financially and what needs to bedone to be there. Financial Planner specifically gives his analysis and advice onpersonal financial statements, investments, taxation, debt & risk management,cash flows, insurance, stocks, trusts, retirement and other components of personalfinance.

8/4/2019 Session 5 HDFC-JOINT CERTIFICATION PROGRAMME HDFC-IBS Mumbai

http://slidepdf.com/reader/full/session-5-hdfc-joint-certification-programme-hdfc-ibs-mumbai 63/66

18 April 2012 Dr. P.R Kulkarni 63

FUNCTIONS AND RESPONSIBILITIES

Financial Planning Services - Inflation, falling interest rates

and fluctuating market conditions require to plan financescarefully

International Services -

Mutual Funds -

Business Select - a range of financial services andpersonalized business-banking solutions that help tomaximize business potential

MEANING AND CONSTITUENTS OF WEALTH

8/4/2019 Session 5 HDFC-JOINT CERTIFICATION PROGRAMME HDFC-IBS Mumbai

http://slidepdf.com/reader/full/session-5-hdfc-joint-certification-programme-hdfc-ibs-mumbai 64/66

18 April 2012 Dr. P.R Kulkarni 64

MANAGEMENT

Wealth Management is a professional service whichis the combination of financial/investment advice,accounting/tax services, and legal/estate planning forone fee.

Wealth Management is classified as an advancedtype of financial planning that provides individualsand even families with private banking, estateplanning, asset management, legal serviceresources, trust management, investment

management, taxation advice, and portfoliomanagement. Thus, wealth managementencompasses asset management, client advisoryservices, and the distribution of investment products.

8/4/2019 Session 5 HDFC-JOINT CERTIFICATION PROGRAMME HDFC-IBS Mumbai

http://slidepdf.com/reader/full/session-5-hdfc-joint-certification-programme-hdfc-ibs-mumbai 65/66

18 April 2012 Dr. P.R Kulkarni 65

ADVISORY ROLE

Wealth management is a high level form of private banking

that provides various types of investment, insurance and bankproducts and services.

Persons engaged in wealth management usually work forbrokerage firms, large banks, trust departments, or

investment and portfolio management firms. Boutique firmssuch as a Registered Investment Advisor also tend to providea wide array of family office services.

8/4/2019 Session 5 HDFC-JOINT CERTIFICATION PROGRAMME HDFC-IBS Mumbai

http://slidepdf.com/reader/full/session-5-hdfc-joint-certification-programme-hdfc-ibs-mumbai 66/66

4 /

1 8 / 2 0 1 2

66

D r .P .R .K ul k a

r ni