Service Tax Voluntary Compliance

Encouragement Scheme, 2013

S B Gabhawalla & Co

Prelude….

S B Gabhawalla & Co

A Limited is a dealer in software. Its’ purchases were for Rs. 99 crores and sales were for Rs. 100 crores. It is served with a SCN demanding ST of Rs. 12.36 crores with

consequential penalties

B Limited is a security agency who collected service tax of Rs. 12.36 crores but did not pay to the Government due to stated cash flow issues. The Auditor has qualified this non payment in CARO, but the

Department has still not issued a notice

C is an unregistered beauty parlour who has collected service tax from the customers but not disclosed in accounts. The Service Tax Department is unaware of the beauty parlour till

date.

Should each of them be treated similarly?

Background

S B Gabhawalla & Co

Evolution of the Service Tax Law breeding both

“culprits” and “victims”

Relevant Recent Legislative Amendments impacting

“culprits” and “victims”:

Rationalisation of Penal Provisions

Heavy Emphasis on Recovery

Prosecution

Background (Contd.)

Why doesn’t a “victim” comply voluntarily even after knowing the exposure?

Tax Payable on Gross Receipts

High Rate of Interest, Unreasonable Late Filing Fees & Delayed Registration Penalties

Despite Section 73(3), suppression routinely alleged even in cases of voluntary compliance

What encourages a “culprit” to not comply voluntarily?

Period of Limitation

18 months in general

5 years in case of suppression, etc.

Upper Cap on penalties

Reduced penalties for captured transactions / in cases where the payment is made immediately post adjudication.

S B Gabhawalla & Co

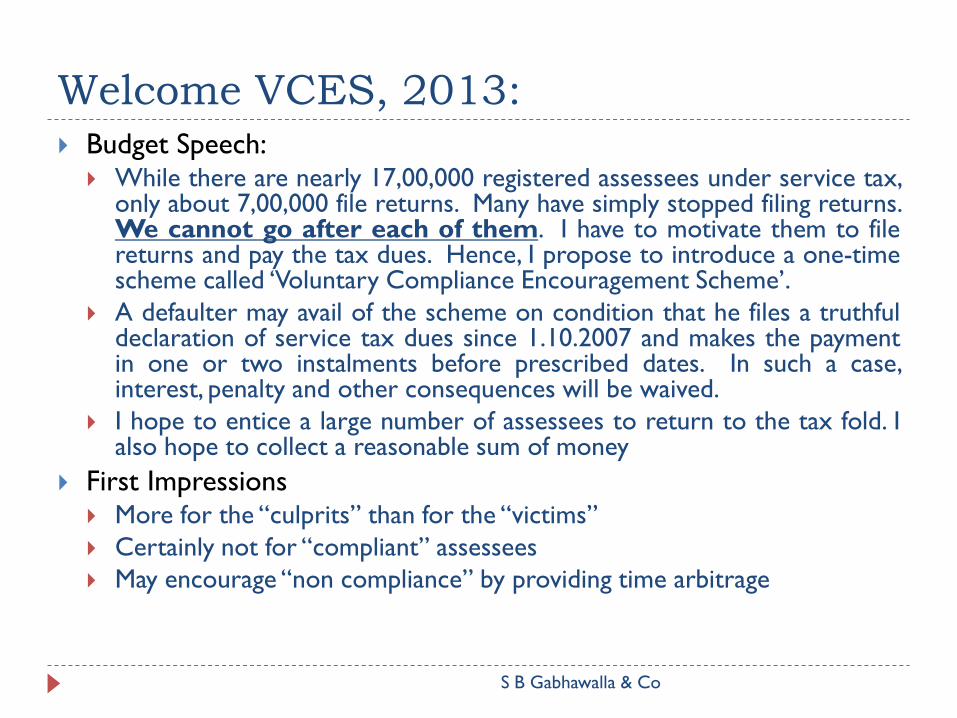

Welcome VCES, 2013:

S B Gabhawalla & Co

Budget Speech: While there are nearly 17,00,000 registered assessees under service tax,

only about 7,00,000 file returns. Many have simply stopped filing returns. We cannot go after each of them. I have to motivate them to file returns and pay the tax dues. Hence, I propose to introduce a one-time scheme called ‘Voluntary Compliance Encouragement Scheme’.

A defaulter may avail of the scheme on condition that he files a truthful declaration of service tax dues since 1.10.2007 and makes the payment in one or two instalments before prescribed dates. In such a case, interest, penalty and other consequences will be waived.

I hope to entice a large number of assessees to return to the tax fold. I also hope to collect a reasonable sum of money

First Impressions More for the “culprits” than for the “victims”

Certainly not for “compliant” assessees

May encourage “non compliance” by providing time arbitrage

From the Past…

S B Gabhawalla & Co

Year Nature of Scheme Applicable for

1998 Kar Vivad Samadhan Scheme Disputes pending at various forums

2004 Extraordinary Tax Payer

Friendly Scheme

Pending Dues to be paid with interest

No penalties to be demanded

No immunity from other proceedings

2008 Service Tax Dispute

Resolution Scheme

Disputes pending at various forums

2013 Voluntary Compliance

Encouragement Scheme

Pending Tax Dues to be paid.

Immunity from Interest

Immunity from Penalties

Immunity from Other Proceedings

VCES: The Macro Picture of the Scheme

Pay Service Tax on or before the due dates

Cannot be paid from CENVAT Credit

Is this merely a cash flow issue?

No Interest to be paid

No Penalties

No Proceedings under the Act

Due Date Amount to be paid

31.12.2013 50% of the tax dues

30.06.2014 Balance 50% of the tax

dues without interest

31.12.2014 Balance 50% of the tax

dues with interest for

the period from

01.07.2014 till the date

of actual payment

S B Gabhawalla & Co

Comparative Snapshot…

S B Gabhawalla & Co

Normal Cases VCES Cases

Service Tax Amount Payable Fully after

utilisation of CENVAT

Credit

Payable Fully before

utilisation of CENVAT

Credit

Possibility of Refund in case of

favourable verdict

Subject to limitation and

unjust enrichment

Not Possible

Interest Payable @ 18% p.a. Not Payable till

30.06.2014

Penalties Payable up to the tax

amount

Not Payable

Late Filing Fees Payable up to Rs.

20000/- per return

Not Payable

Prosecution Can be initiated Immunity Granted

Recovery Proceedings Can be initiated Not till conclusion of

Scheme

VCES: Process Steps:

S B Gabhawalla & Co

Registration (if not already obtained earlier)

Application to be made in Form VCES1

Acknowledgement of Application in Form VCES2

Payment of Tax Dues as per Instalments prescribed

Final Acknowledgement of Discharge in Form VCES3

SCN for tax dues within one year if declaration “substantially false”

Rejection of Declaration if investigation is pending

What are the pivots?

S B Gabhawalla & Co

Eligibility

Tax Dues

Immunity

Eligibility

S B Gabhawalla & Co

Who is eligible – Section 106(1)

S B Gabhawalla & Co

Any person may declare his tax dues in respect of which

no notice or an order of determination under section 72 or

section 73 or section 73A of the Chapter has been issued or

made before the 1st day of March, 2013:

Provided that any person who has furnished return under

section 70 of the Chapter and disclosed his true liability, but

has not paid the disclosed amount of service tax or any part

thereof, shall not be eligible to make declaration for the period

covered by the said return:

Provided further that where a notice or an order of

determination has been issued to a person in respect of any

period on any issue, no declaration shall be made of his tax

dues on the same issue for any subsequent period

Practical Issues…

S B Gabhawalla & Co

SCN is issued for classifying discount as BAS, but assessee is of the view that the transaction is trading, matter pending for adjudication. Assessee has also received certain maintenance charges for which no SCN has been issued. Whether he can apply for VCES?

Declaration can be filed in respect of any other “issue” not covered by SCN – Sr. 3 of CBEC Circular

What if the assessee has also received commission from some third party, which is payable under BAS

Whether this is “same issue” or “other issue”?

SCN is issued for delayed/non payment of service tax for period from 01-04-2002 to 31-03-2007. There are further instances of delayed /non payment of service tax.

Whether this is “same issue” or “other issue”?

Practical Issues (Contd)…

S B Gabhawalla & Co

SCN is erroneously issued for delayed filing of returns for the

period from 01-04-2003 to 31-03-2004 even though the

returns were filed in time. The reply has been filed but no

order is issued till date. There are subsequent delays in

payment of taxes, some cases of non payment of taxes and

delay in filing of returns.

Whether declaration can be filed.

What if SCN is issued for one premises and not for other

premises?

Whether the other premises can apply for VCES for the same issue?

Whether the other premises can apply for VCES for other issues?

What if the SCN is issued after 01.03.2013?

Who is not eligible – Section 106(2)

S B Gabhawalla & Co

Where a declaration has been made by a person against whom,— an inquiry or investigation in respect of a service tax not levied or

not paid or short-levied or short-paid has been initiated by way of search of premises under section 82 of the Chapter;

issuance of summons under section 14 of the Central Excise Act, 1944 (1 of 1944), as made applicable to the Chapter under section 83 thereof; or

requiring production of accounts, documents or other evidence under the Chapter or the rules made thereunder; or Section 72 of the Act

Rule 5A of the Service Tax Rules

an audit has been initiated,

and such inquiry, investigation or audit is pending as on the 1st day of March, 2013

The declaration shall be “rejected”

Practical Issues:

S B Gabhawalla & Co

What if Audit Notice is issued for One premises and dues are pending for another premises?

One period and dues are pending for another period?

What if a manufacturer is issued intimation for audit under Excise Act? Whether he can apply for VCES for services rendered/received by him?

What if a third party is issued summons for services rendered by a person Summons issued to manufacturer for services rendered by job worker

What if the audit intimation is issued and served on 01.03.2013?

What if the audit is concluded (FAR issued) but SCN is not served?

How to ascertain whether the inquiry, etc. is pending or concluded?

How to ascertain that the information is called for under Rule 5A of the Service Tax Rules?

Is there any time frame for rejection of declaration?

Summary of Non Eligibility

S B Gabhawalla & Co

“Tax Dues” Tax Paid before 01.03.2013 (interest or penalties unpaid)

Tax pertaining to period after 31.12.2012

“Issue Driven Ineligibility” Cases where SCN has been issued, but pending

adjudication

Cases where Order is passed but pending in Appeals

Cases where tax is unpaid but is disclosed in returns

“Blanket Ineligibility” Search Conducted before 01.03.2013 and inquiry is

pending

Summons issued under section 14 and inquiry is pending

Letter requiring production of accounts, documents or evidence and inquiry is pending

Audit has been initiated and pending

Tax Dues

S B Gabhawalla & Co

Tax Dues

S B Gabhawalla & Co

“tax dues" means the service tax due or payable under

the Chapter or any other amount due or payable under

section 73A thereof, for the period beginning from the

1st day of October, 2007 and ending on the 31st day of

December, 2012 including a cess leviable thereon under

any other Act for the time being in force, but not paid as

on the 1st day of March, 2013

Practical Issues:

Whether following situations covered?

Tax Collected but not paid

Tax not collected but undisputed

Tax not collected but disputed

Tax Payable under Composition/Presumptive Options

Tax/Income not disclosed in accounts

Tax payable under reverse charge mechanism

Wrong Availment of CENVAT Credit

Wrong Utilisation of CENVAT Credit

Payment of Amount under Rule 6 of CENVAT Credit Rules

Reversal on Removal of Inputs/Capital Goods

Reversal on account of non payment of input services

Irregular Self Adjustment of Service Tax

S B Gabhawalla & Co

Practical Issues:

S B Gabhawalla & Co

How to determine the period for “tax dues”?

Tax for period between 01.10.2007 to 31.12.2012 only covered

RCM Invoice of November 2012, not paid till June 2013.

Whether the declaration is for block period or specific return periods?

Whether amount from 01.10.2007 to 31.03.2008 can be demanded? (Extended Period of Limitation is also concluded)

Whether payment of demand results in admission of suppression on the part of service provider?

Will this result in denial of credit to the service recipient?

Whether partial tax dues can be declared?

Whether tax dues can be declared for a partial period?

What if the tax dues are found to be incorrect later?

How to calculate the tax dues?

S B Gabhawalla & Co

Identify Services

Identify Taxable Services

Identify Point of Taxation &

Situs of Service

Claim Exemptions

Claim Abatements

Apply Valuation Rules

Claim Cum Tax Benefit

Reduce Tax Paid/Disclosed

in Returns

Balance is Tax Dues

Immunity

S B Gabhawalla & Co

VCES: Scope of Immunity:

S B Gabhawalla & Co

Section 108

(1) Notwithstanding anything contained in any provision of the Chapter, the declarant, upon payment of the tax dues declared by him under sub-section (1) of section 107 and the interest payable under the proviso to sub-section (4) thereof, shall get immunity from penalty, interest or any other proceeding under the Chapter

(2) Subject to the provisions of section 111, a declaration made under sub-section (1) of section 107 shall become conclusive upon issuance of acknowledgement of discharge under sub-section (7) of section 107 and no matter shall be reopened thereafter in any proceedings under the Chapter before any authority or court relating to the period covered by such declaration.

Broad Comparison With Other Schemes

S B Gabhawalla & Co

Kar Vivad Samadhan Scheme, 1998 – Section 90(3) Every order passed under sub-section (1), determining the sum payable under

this Scheme, shall be conclusive as to the matters stated therein and no matter covered by such order shall be reopened in any other proceeding under the direct tax enactment or indirect tax enactment or under any other law for the time being in force.

Service Tax Dispute Resolution Scheme, 2008 – Section 96(3) Every order passed under sub-section (1), determining the sum payable under

this Scheme, shall be conclusive as to the matters stated therein and no matter covered by such order shall be reopened in any other proceeding under the Chapter.

Service Tax Voluntary Compliance Encouragement Scheme, 2013 – Section 108(2) Subject to the provisions of section 111, a declaration made under sub-section

(1) of section 107 shall become conclusive upon issuance of acknowledgement of discharge under sub-section (7) of section 107 and no matter shall be reopened thereafter in any proceedings under the Chapter before any authority or court relating to the period covered by such declaration.

VCES:

Safeguard Against Incorrect Declarations

S B Gabhawalla & Co

Section 111

(1) Where the Commissioner of Central Excise has reasons to

believe that the declaration made by a declarant under this

Scheme was substantially false, he may, for reasons to be

recorded in writing, serve notice on the declarant in respect

of such declaration requiring him to show cause why he

should not pay the tax dues not paid or short-paid.

(2) No action shall be taken under sub-section (1) after the

expiry of one year from the date of declaration.

(3) The show cause notice issued under sub-section (1) shall be

deemed to have been issued under section 73, or as the case

may be, under section 73A of the Chapter and the provisions

of the Chapter shall accordingly apply

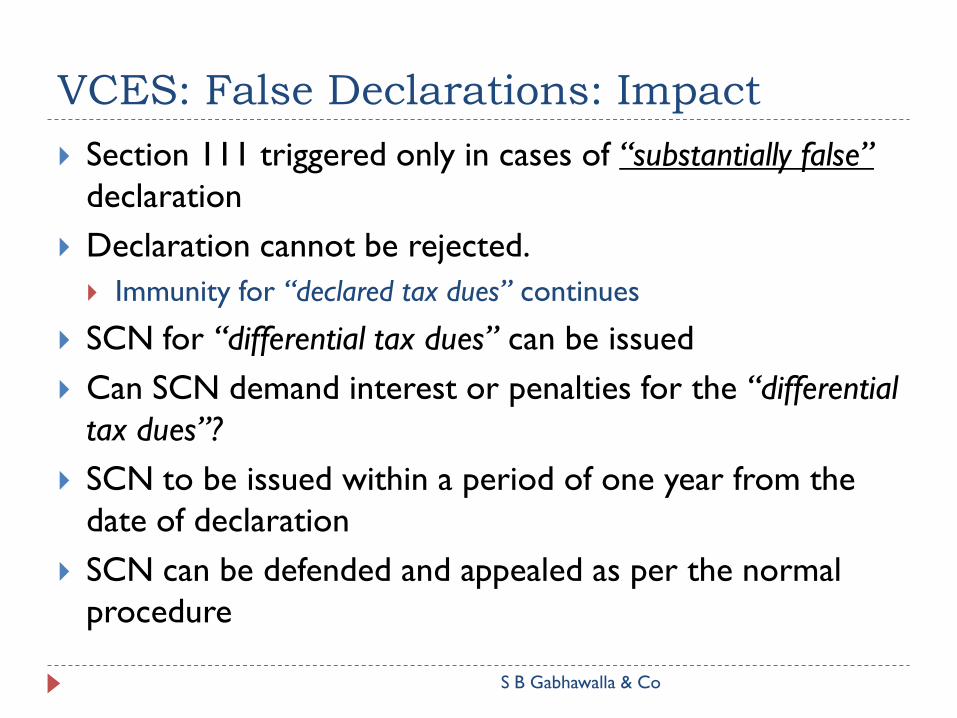

VCES: False Declarations: Impact

S B Gabhawalla & Co

Section 111 triggered only in cases of “substantially false”

declaration

Declaration cannot be rejected.

Immunity for “declared tax dues” continues

SCN for “differential tax dues” can be issued

Can SCN demand interest or penalties for the “differential

tax dues”?

SCN to be issued within a period of one year from the

date of declaration

SCN can be defended and appealed as per the normal

procedure

Summary of Immunity Offered

S B Gabhawalla & Co

Interest

Penalties

Any Other Proceedings under the Chapter relating to the period covered by the declaration CBEC Clarification Sr. 2 Late Fees / Penalties for delayed registration

These are proceedings under the Chapter and therefore immunity is granted.

An unregistered declarant registers and declares under VCES. Can EA Audit be conducted for periods upto 31.12.2012?

Can scrutiny be undertaken by issuing summons / letters under Rule 5A? Before VCES3 is issued?

After VCES3 is issued?

Whether the following can be investigated

post VCES3?

S B Gabhawalla & Co

Issues covered by “tax dues” declared in VCES3

Interpretation of Value (inclusion of free issue materials and services, reimbursement claims)

Interpretation of Tax Rate for the tax dues declared (incorrect interpretation of PoT Rules, deemed completion of service, composition for ongoing contracts)

Exchange Rate applicable for cross border transactions

Classification (Clubs or Association Services vs. Negative List)

Issues not covered by “tax dues” but pertaining to the same period

Exemption

Exports

Non Taxable Transactions

CENVAT Credit

What is the time frame for the above investigations?

Can EA Audit be conducted for periods upto 31.12.2012?

Can scrutiny be undertaken by issuing summons / letters under Rule 5A?

Is this an opportunity in disguise?

Tips and Traps:

S B Gabhawalla & Co

Beware of Reconciliation Issues

Confidentiality of Declaration

Impact on Pending Litigation to be considered

May imply acceptance of tax liability

No Scope for any refund whatsoever

Recovery Proceedings under Section 87 if tax dues not

paid in time

Thank You